GS-Hydro | Annual Report 2008 GS-Hydro | Annual Report 2008 ... welded is an inherently more...

64

GS-Hydro | Annual Report 2008 Marine Land Offshore

Transcript of GS-Hydro | Annual Report 2008 GS-Hydro | Annual Report 2008 ... welded is an inherently more...

GS-Hydro | Annual Report 2008

Mar

ine

Lan

d

Off

sho

re

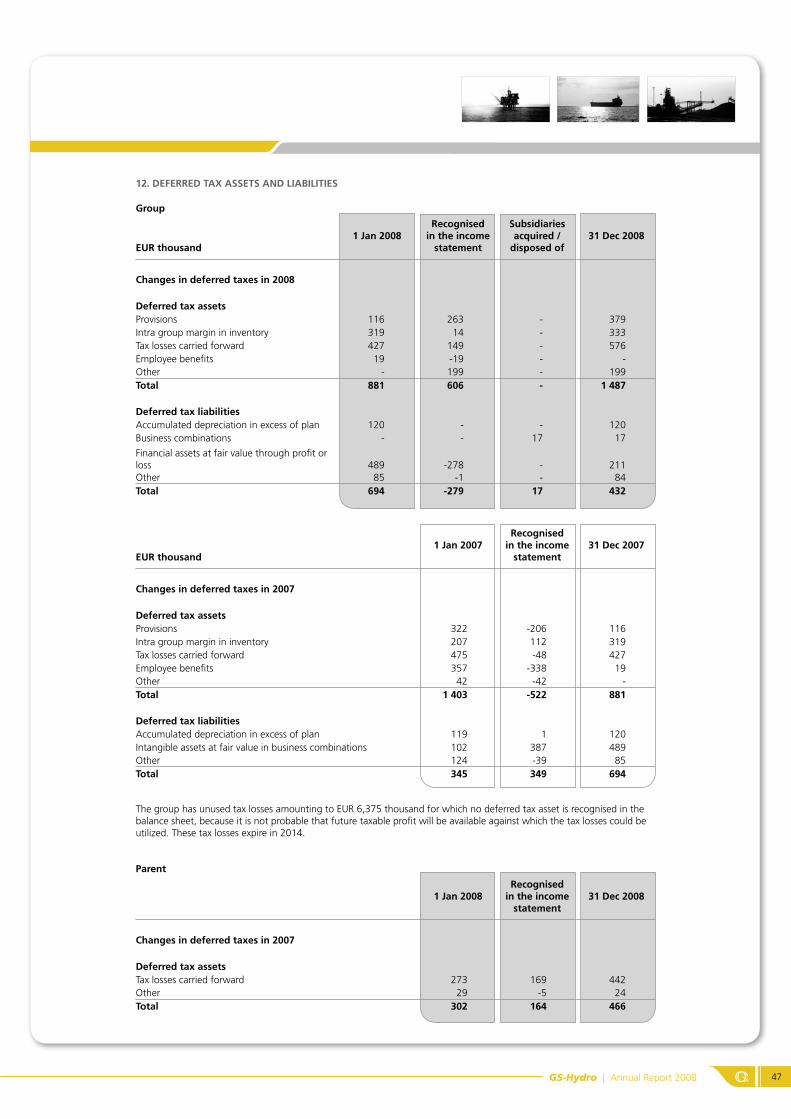

GS-Hydro | Annual Report 2008 2

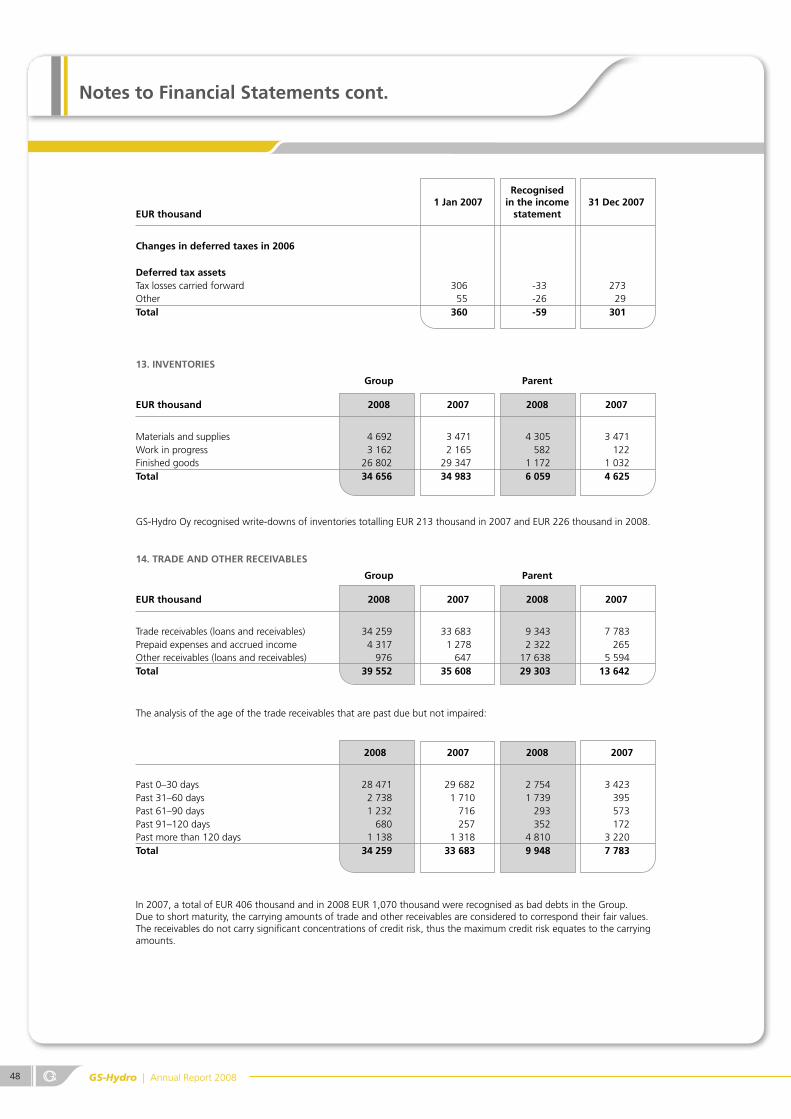

GS-Hydro in brief

Headquartered in Finland, GS-Hydro is the world’s leading supplier of non-welded piping systems. Operations began in 1974 with the commercialization of an innovative flange which allowed the rapid and secure connection of pipes without the need for welding.

The company operates in the global market for industrial piping, primarily in the offshore and marine industries, as well as in selected land-based industries. The main application for non-welded piping is in hydraulic power transmission, where very high pressures place stringent requirements on piping systems.

GS-Hydro develops and manufactures original GS-branded flanges at its own facility in Finland, while globally sourcing other piping products required by customers. The key benefits of GS-Hydro’s non-welded piping are zero fire hazard, inherent cleanliness, leak-free reliability and rapid on-site installation. Employing 640 piping system specialists, GS-Hydro operates directly through its own subsidiaries in 17 countries, covering the key markets in Europe, Asia and North America. Selected agents and distributors complete the world-wide sales and customer service channel.

With over three decades of experience, and its technology validated in tens of thousands of demanding applications, GS-Hydro is uniquely able to deliver turn-key piping projects to global customers’ local sites virtually anywhere in the world.

GS-Hydro is a wholly-owned subsidiary of Sweden-based Ratos AB, a listed private equity company.

Headquarters

Subsidiaries

Agents

GS-Hydro | Annual Report 2008 3

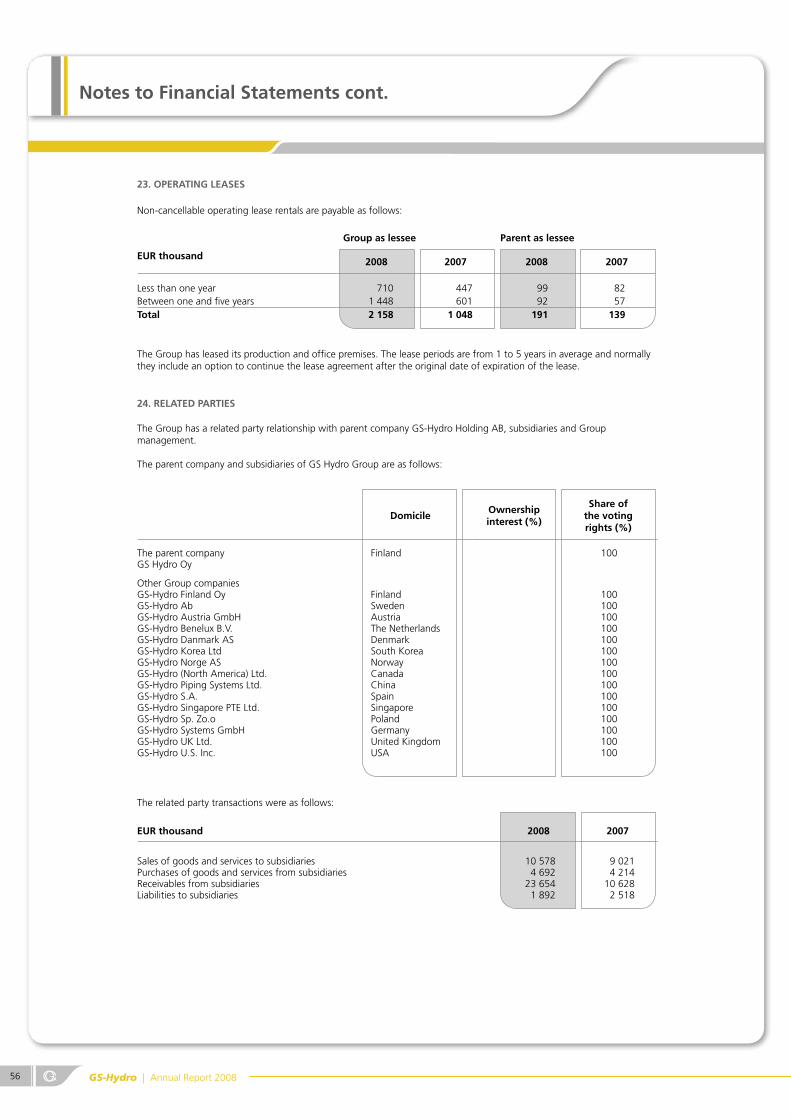

CONTENTS

GS-Hydro in brief . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2Year 2008 in review . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4Letter from the President & CEO . . . . . . . . . . . . . . . . . . 6Our offering and market segments . . . . . . . . . . . . . . . . 8Markets and customers in 2008. . . . . . . . . . . . . . . . . . 10Our strategy. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16Non-welded: benefiting the environment. . . . . . . . . . . 18Personnel. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20Board of Directors´ report. . . . . . . . . . . . . . . . . . . . . . . 22 Financial Statements . . . . . . . . . . . . . . . . . . . . . . . . . . 26 Consolidated income statement . . . . . . . . . . . . . . . 26 Consolidated balance sheet . . . . . . . . . . . . . . . . . . 27 Consolidated cash flow statement . . . . . . . . . . . . . 28 Consolidated statement of changes in equity . . . . . 29 Income statement for the parent company . . . . . . . 30 Balance sheet for the parent company . . . . . . . . . . 31 Cash flow statement for the parent company . . . . . 32 Statement of changes in parent company equity . . 33Notes to Financial Statements . . . . . . . . . . . . . . . . . . . 34 Auditor´s report . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 58Corporate governance . . . . . . . . . . . . . . . . . . . . . . . . . 59Board of Directors . . . . . . . . . . . . . . . . . . . . . . . . . . . . 60Executive Committee . . . . . . . . . . . . . . . . . . . . . . . . . . 61Market insight . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 62Historical milestones . . . . . . . . . . . . . . . . . . . . . . . . . . 63

GS-Hydro | Annual Report 2008 4 GS-Hydro | Annual Report 2008

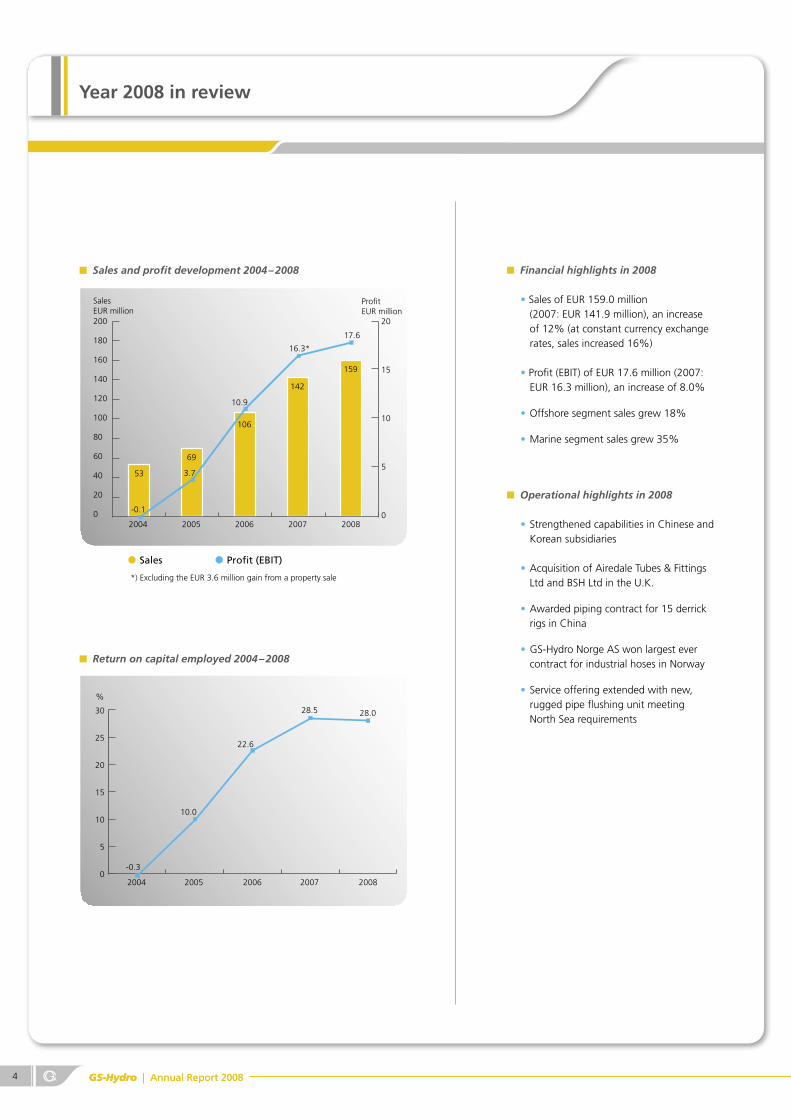

Year 2008 in review

Financial highlights in 2008 • Sales of EUR 159.0 million (2007: EUR 141.9 million), an increase of 12% (at constant currency exchange rates, sales increased 16%) • Profit (EBIT) of EUR 17.6 million (2007: EUR 16.3 million), an increase of 8.0%

• Offshore segment sales grew 18%

• Marine segment sales grew 35%

Operational highlights in 2008

• Strengthened capabilities in Chinese and Korean subsidiaries

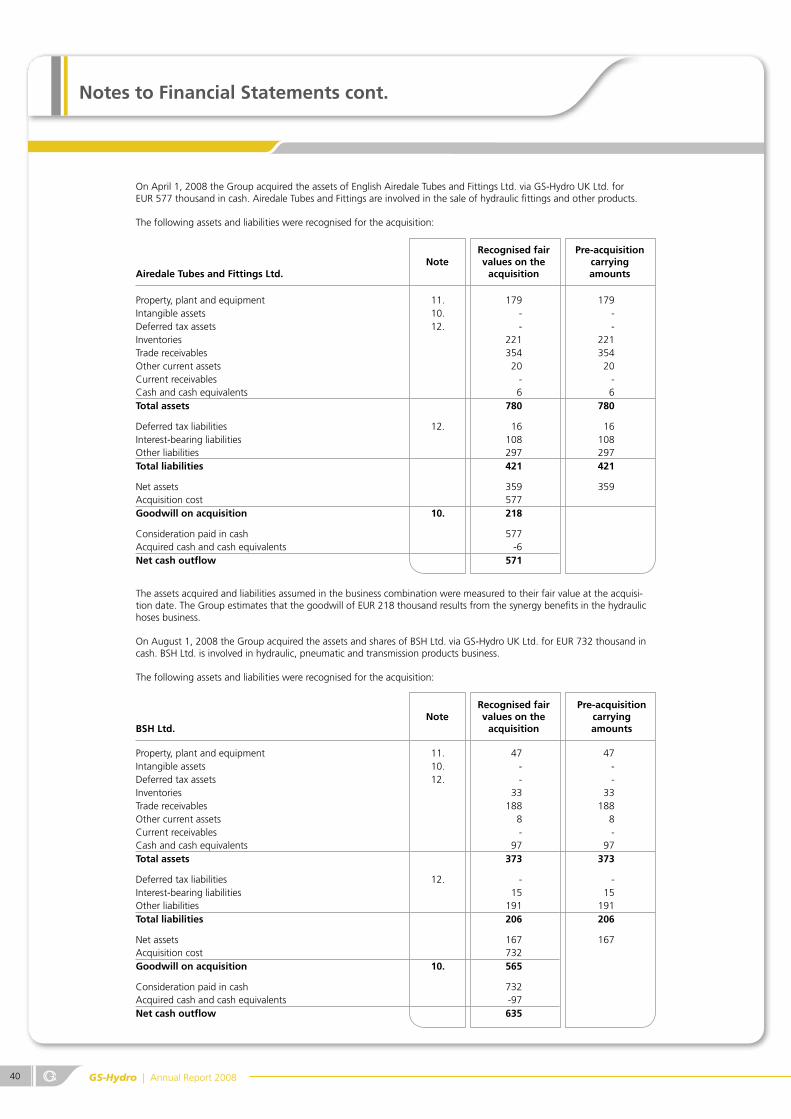

• Acquisition of Airedale Tubes & Fittings Ltd and BSH Ltd in the U.K.

• Awarded piping contract for 15 derrick rigs in China

• GS-Hydro Norge AS won largest ever contract for industrial hoses in Norway

• Service offering extended with new, rugged pipe flushing unit meeting North Sea requirements

30

25

20

15

10

5

0

%

2004 2005 2006 2007 2008

28.028.5

22.6

10.0

-0.3

Return on capital employed 2004 – 2008

Sales and profit development 2004 – 2008

Sales Profit (EBIT)

200

180

160

140

120

100

80

60

40

20

0

20

15

10

5

0

SalesEUR million

ProfitEUR million

2004 2005 2006 2007 2008

159

17.6

142

106

69

53

16.3*

3.7

10.9

-0.1

*) Excluding the EUR 3.6 million gain from a property sale

GS-Hydro | Annual Report 2008 5

Systems

Products

Services

Revenues by type of business

57%

12%

31%

Revenues by segment

Offshore

Marine

Land-based

34%37%

29%

Offshore segment Sales development 2004 – 2008, CAGR 46%

80

70

60

50

40

30

20

10

0

54

46

29

1611

2004 2005 2006 2007 2008

EUR million

Marine segment Sales development 2004 – 2008, CAGR 23%

2004 2005 2006 2007 2008

46

3428

1814

80

70

60

50

40

30

20

10

0

EUR million

Land-based segment Sales development 2004 – 2008, CAGR 20%

5962

49

3528

2004 2005 2006 2007 2008

80

70

60

50

40

30

20

10

0

EUR million

GS-Hydro | Annual Report 2008 6

Despite market turbulence, 2008 turned out to be a good year for GS-Hydro, with the company setting new records for both sales and profits. Sales rose to EUR 159 million in 2008, from EUR 142 million in 2007, which represents growth of 12% (16% at constant currency exchange rates). Operating results also developed posi-tively. Profit before interest and taxes (EBIT) improved to a record EUR 17.6 million in 2008, from EUR 16.3 million in 2007.

The strategy to focus our sales efforts on the Offshore and Marine segments was rewarded during the final months of 2008. While our customers in the Land-based segment reduced their orders, the order flow from our offshore and marine customers continued to be strong. Activity in the Offshore and Marine segments was especially strong for GS-Hydro in Asia and North America. Overall, we can be pleased with our performance in what was a challeng-ing year.

At the beginning of 2008 we invested in developing our local presence in Asia through our own frontline subsidiaries. As a result, these units performed well during the second half of the year. With the strong growth in local frontline subsidiaries of the past few years, we also focused on developing our organizational structure in 2008. Now, all subsidiaries report directly either to the President & CEO or to a member of the Executive Committee. Today, we can be confident that all of our operations around the world are on a sound footing, giving us the confidence to develop the global busi-ness further, despite the tougher times we are currently facing. We maintain our goal of strong, long-term growth and have identified many initiatives to seize in order to be successful.

Our core strategy is to emphasize system sales and our ability to work together with our customers to add significant value to their businesses. Large, turn-key projects concretely demonstrate all of the skills we can offer, and several success stories from 2008 are highlighted in this annual report. The efforts to build partner-ships with our strategic customers and selected suppliers paid off handsomely during the year. Most of the growth in sales can be attributed to increased business with our main strategic customers. This positive development was also reflected in the higher ratings we received in our customer satisfaction measurements.

Focusing on organic growth in 2008, we did not participate in any major merger and acquisition activity, although we continue to fol-low opportunities with interest. Two small acquisitions were made to support our local product business in the U.K. The integration of these businesses into GS-Hydro UK has gone smoothly and sales have grown strongly in the UK subsidiary.

Letter from the President & CEO

GS-Hydro | Annual Report 2008 7

In the marketing efforts to new potential customers we are putting increased emphasis on communicating the benefits of non-welded technology. In 2008, we arranged an increased number of customer events to promote non-welded technology. Non-welded solutions have clear advantages regarding worker safety and non-welded is an inherently more environmentally responsible method of joining pipes than arc welding.

With the overriding theme of improving operating efficiency, we also aim to make great strides in internal development during 2009. The backbone of our effort will be the work required to unify operations under a planned new enterprise resource planning (ERP) system. Although fully implementing the ERP system is a long-term project, the first implementation stages will highlight the large potential information technology offers to improve opera-tions and to facilitate seamless and effective co-operation. In 2009, we also have plans to improve competence levels, through our GS-Academy, improve internal communications and develop quality management.

With the changes in the market, cash management needs to take a greater role in the Group. We will therefore be emphasizing actions to improve efficiencies particularly, in logistics and financing.

The GS-Hydro Group has demonstrated very strong operating per-formance over the last few years. The operating profits have been retained and re-invested in the business to finance the rapid growth we were experiencing since 2005. In September 2008, GS-Hydro was refinanced, resulting in a release of EUR 50 million to Ratos.

The outlook for 2009 is very uncertain and there are signs that our main markets will be weaker than last year. However, we are enter-ing this uncertain period as a very strong company. We also have new market areas available to us which have substantial growth potential. We are therefore confidently moving ahead to face our new challenges. Last year I wrote that we need to be able to react fast to any changes in our business environment in order to sustain profitable growth. My observation then was more prescient than I could have imagined, it is worth repeating in this year’s shareholder letter.

I wish to thank all our employees and customers for making 2008 a successful year for GS-Hydro. The past four years of strong growth have radically transformed GS-Hydro into a professional mid-sized company. I believe that our next phase of development will be no less interesting.

Thomas RönnholmPresident & CEO

GS-Hydro | Annual Report 2008 8

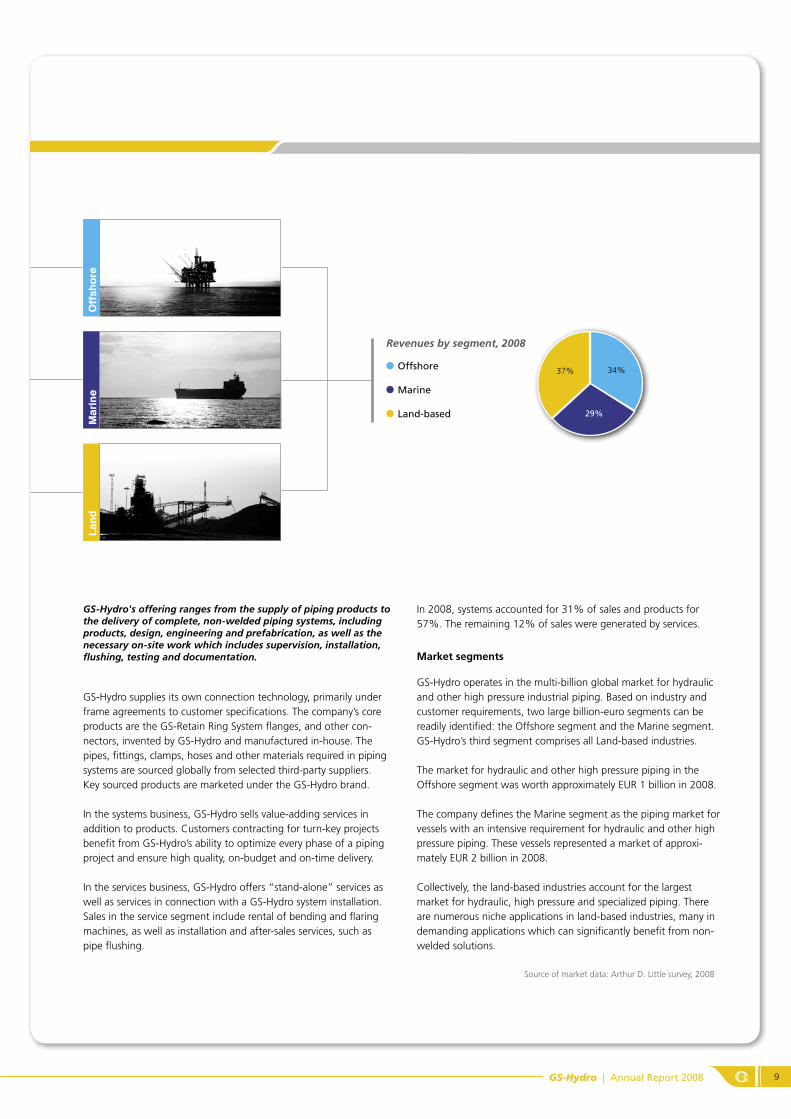

Our offering and market segments

Systems

Products

Services

Revenues by type of business, 2008

57%

12%

31%

Systems

Products

Services

GS-Hydro | Annual Report 2008 9

GS-Hydro's offering ranges from the supply of piping products to the delivery of complete, non-welded piping systems, including products, design, engineering and prefabrication, as well as the necessary on-site work which includes supervision, installation, flushing, testing and documentation.

GS-Hydro supplies its own connection technology, primarily under frame agreements to customer specifications. The company’s core products are the GS-Retain Ring System flanges, and other con-nectors, invented by GS-Hydro and manufactured in-house. The pipes, fittings, clamps, hoses and other materials required in piping systems are sourced globally from selected third-party suppliers. Key sourced products are marketed under the GS-Hydro brand.

In the systems business, GS-Hydro sells value-adding services in addition to products. Customers contracting for turn-key projects benefit from GS-Hydro’s ability to optimize every phase of a piping project and ensure high quality, on-budget and on-time delivery.

In the services business, GS-Hydro offers “stand-alone” services as well as services in connection with a GS-Hydro system installation. Sales in the service segment include rental of bending and flaring machines, as well as installation and after-sales services, such as pipe flushing.

Source of market data: Arthur D. Little survey, 2008

In 2008, systems accounted for 31% of sales and products for 57%. The remaining 12% of sales were generated by services.

Market segments

GS-Hydro operates in the multi-billion global market for hydraulic and other high pressure industrial piping. Based on industry and customer requirements, two large billion-euro segments can be readily identified: the Offshore segment and the Marine segment. GS-Hydro’s third segment comprises all Land-based industries.

The market for hydraulic and other high pressure piping in the Offshore segment was worth approximately EUR 1 billion in 2008. The company defines the Marine segment as the piping market for vessels with an intensive requirement for hydraulic and other high pressure piping. These vessels represented a market of approxi-mately EUR 2 billion in 2008. Collectively, the land-based industries account for the largest market for hydraulic, high pressure and specialized piping. There are numerous niche applications in land-based industries, many in demanding applications which can significantly benefit from non-welded solutions.

Off

sho

reM

arin

e

Revenues by segment, 2008

Offshore

Marine

Land-based

34%37%

29%

Lan

d

GS-Hydro | Annual Report 2008 10

Markets and customers in 2008

Offshore segment

Offshore segment sales as a share of total GS-Hydro sales

Non-welded share of sales in the overall Offshore piping market

GS-Hydro Offshore segment sales

80

70

60

50

40

30

20

10

0

54

46

2007 2008

EUR million

34%

Non- welded 30%

Welded 70%

Offshore is GS-Hydro’s most important segment, accounting for the highest sales to a single industry in 2008. The Offshore yards build and convert some of the largest and most com-plex structures on earth, ranging from mobile jack-up rigs to semi-submersible drilling rig hulls weighing up to 16,000 tons. A modern offshore oil platform for deep-water exploration or production has to operate in some of the most hostile environ-mental conditions known to man, placing rigorous demands on hydraulic power systems.

The primary applications for GS-Hydro piping systems are in high-pressure hydraulics for the drilling package, cranes, winches, motion compensation systems and the main ring line. In addition, GS-Hydro is a significant supplier of high pressure and specialty piping systems in all areas of offshore installations, including drilling, utilities and processing. Since the hydraulic content is significantly larger on a drilling unit than on a production unit, oil and gas exploration is the main driving force behind the company’s growth in the Offshore segment.

The total global market for hydraulic and other high pressure piping in the offshore industry is estimated to be EUR 1 billion. Non-welded technology penetration is estimated at 30%, implying a total non-welded piping market value of approximately EUR 300 million in 2008.

In 2008, GS-Hydro’s sales to the Offshore segment rose 18% to EUR 54.2 million and accounted for 34% of GS-Hydro’s total sales.

Source of market data: Arthur D. Little survey, 2008

GS-Hydro | Annual Report 2008 11

2008 win: The Blackford Dolphin offshore project

In late 2008, GS-Hydro completed a series of piping project deliver-ies for the upgrade of the Blackford Dolphin semi-submersible offshore drilling platform, converting it for deepwater operation. Now fully upgraded, the Blackford Dolphin can drill for oil or gas at up to a depth of 7000 feet (2300 meters). The various sub-projects/systems included piping for the derrick, the ring main hydraulics, the blowout preventer (BOP)-system for oil testing, water-tight doors, raiser columns, hose cooling, propulsion and hydraulic valves. In total, GS-Hydro delivered and installed over 5 kilometers of non-welded piping on the platform.

The Blackford Dolphin platform was upgraded in the Netherlands by a globally operating offshore and marine customer. This was the first project where GS-Hydro employed an on-site project secretary to manage purchase orders and invoicing on a daily basis – with highly satisfactory results.

GS-Hydro Benelux B.V. won the contract based on their track record of successfully executing turn-key projects for customers in the Netherlands in the past. In this complex project the customer required all the skills and services GS-Hydro offers, in addition to piping and connector materials. The GS-Hydro Benelux subsidi-ary co-operated with the GS-Hydro UK unit on implementation, together supplying engineering, prefabrication, installation, testing, flushing and full documentation services for the piping systems.

In Spring 2009, the Blackford Dolphin platform is off the coast of the Republic of Ghana in Africa, drilling the deepwater Hyedua wells to appraise the oil reserves of the recently discovered Jubilee field. GS-Hydro piping is enabling the platform to drill to a total depth of nearly 4 kilometers in a water depth exceeding 1.2 kilometers. Ghana has already struck oil in the shallow waters of the Jubilee field, enabling the country to be an oil producer as early as 2010. With the reserves already estimated to be as much as 1.8 billion barrels of oil, further successful finds could enable this West African country to become a significant oil exporter.

GS-Hydro – Creating Value Together

GS-Hydro | Annual Report 2008 12

Markets and customers in 2008

Marine segmentGS-Hydro Marine segment sales

80

70

60

50

40

30

20

10

0 2007 2008

EUR million

46

34

Marine segment sales as a share of total GS-Hydro sales

29%

Non-welded share of sales in the overall Marine piping market

Non- welded 20%

Welded 80%

GS-Hydro´s piping solutions are extensively used in the ship-building industry for hydraulic, seawater and other piping systems. With ship owners’ special requirements for high integ-rity and cleanliness, fast installation and flexible engineering, GS-Hydro’s non-welded piping can offer significant time and cost benefits for shipyards and their suppliers.

Marine is another important segment for GS-Hydro, generating a piping market with sales of approximately EUR 2 billion. Tug boats, offshore supply vessels, chemical tankers, fishing vessels, naval ships, dredgers and seismic vessels are all examples of ships in the Marine segment with an intensive requirement for hydraulic and other high pressure piping.

Non-welded piping penetration in the Marine segment is estimated at approximately 20%, implying a total non-welded piping market value of approximately EUR 400 million in 2008.

In 2008, GS-Hydro’s sales to the Marine segment rose 35% to EUR 46.2 million and accounted for 29% of GS-Hydro’s total sales.

Source of market data: Arthur D. Little survey, 2008

GS-Hydro | Annual Report 2008 13

2008 win: The Seven Atlantic Diving Support / Offshore Construction Vessel

In 2008, GS-Hydro’s UK subsidiary won a contract to install over 10 kilometers of non-welded stainless steel and tungum piping solutions on the Seven Atlantic, a unique, fully Dynamic Positioned Diving Support / Offshore Construction Vessel (DSV). The hydraulic piping for the Air Dive System Equipment, Hoop Boom, Constant Tension Winches, and Triple Drum Winches, as well as the vital gas piping for the diving spread, was supplied by GS Hydro. For the diving spread, GS-Hydro supplied non-welded piping systems for gas management, the divers’ environmental control unit (ECU) and the ancillary systems.

The Seven Atlantic was designed and is being built in the Nether-lands by the IHC Merwede, the world leader in specialized offshore subsea construction vessels, to fulfill the requirements of a contract Subsea 7. With a capacity for 150 personnel, a heave-compensated 120 ton crane and a large deck area of 1200 square meters, the vessel will be the most versatile and advanced of its kind.

GS-Hydro won the contract due to its ability to rapidly implement piping in concert with the suppliers of the diving spread, the well treatment, the robotically operated vehicles (ROV), and the crane equipment. During the contract negotiation phase, GS-Hydro was best able to meet the yard’s requirements for delivery, hook-up and commissioning times in synchronization with other suppliers’ engineering and production stages. Internally, GS-Hydro benefited from being able to bring together expertise from several frontline subsidiaries.

Diving Support Vessels (DSV) are designed to facilitate air and satu-ration diving. By saturating their bloodstream with inert helium and spending their rest periods also at similar deep-sea pressures, divers

avoid the need for time-consuming frequent decompression and the risk of decompression sickness, “the bends”. Saturation diving spreads have been developed to allow divers to work effectively on oil or gas wells and piping deep underwater for long periods of time. Saturation divers operate in some of the harshest condi-tions known to man. Indeed, the challenge of working under such extreme conditions is not dissimilar to space travel.

In the Seven Atlantic, the diving spread has a total of eight chambers, twin diving bells and two observation-class robotically operated vehicles. The diving spread will enable up to 24 divers in eight teams to work up to a depth of 350 meters and live under the equivalent sea water pressure for up to 28 days at a time. Non-welded piping was a clear choice for the cleanliness needed in the breathing systems for the diving spread. GS-Hydro’s non-welded technology ensures that the divers breathe gas mixtures free of contamination.

The project is a high profile showcase for GS-Hydro’s capabilities. On schedule for delivery in mid 2009, the Seven Atlantic is part of the largest single contract award in the history of the UK subsea sector.

GS-Hydro – Creating Value Together

GS-Hydro | Annual Report 2008 14

Land-based segment sales as a share of total GS-Hydro sales

Markets and customers in 2008

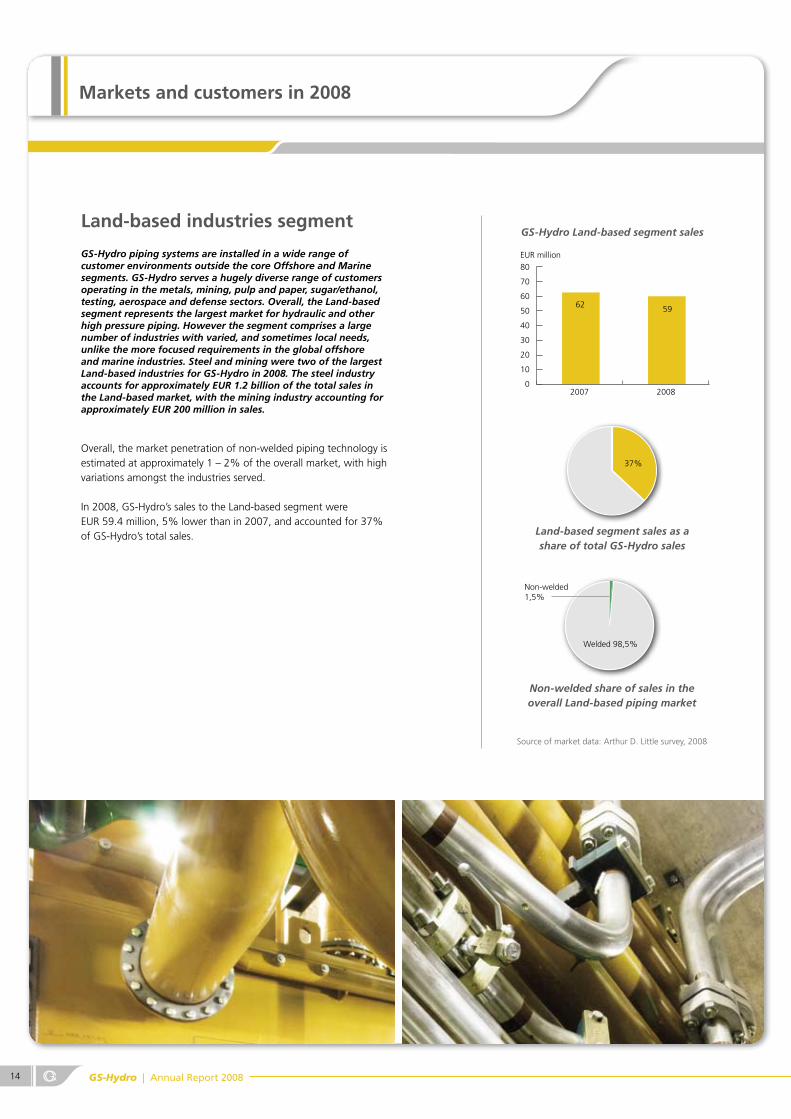

Land-based industries segment

Non-welded share of sales in the overall Land-based piping market

5962

GS-Hydro Land-based segment sales

80

70

60

50

40

30

20

10

0 2007 2008

EUR million

37%

Welded 98,5%

Non-welded 1,5%

GS-Hydro piping systems are installed in a wide range of customer environments outside the core Offshore and Marine segments. GS-Hydro serves a hugely diverse range of customers operating in the metals, mining, pulp and paper, sugar/ethanol, testing, aerospace and defense sectors. Overall, the Land-based segment represents the largest market for hydraulic and other high pressure piping. However the segment comprises a large number of industries with varied, and sometimes local needs, unlike the more focused requirements in the global offshore and marine industries. Steel and mining were two of the largest Land-based industries for GS-Hydro in 2008. The steel industry accounts for approximately EUR 1.2 billion of the total sales in the Land-based market, with the mining industry accounting for approximately EUR 200 million in sales.

Overall, the market penetration of non-welded piping technology is estimated at approximately 1 – 2% of the overall market, with high variations amongst the industries served.

In 2008, GS-Hydro’s sales to the Land-based segment were EUR 59.4 million, 5% lower than in 2007, and accounted for 37% of GS-Hydro’s total sales.

Source of market data: Arthur D. Little survey, 2008

GS-Hydro | Annual Report 2008 15

2008 win: Metal Forge and extrusion presses for Danieli Breda

In 2008, GS-Hydro delivered multiple hydraulic piping systems to Danieli Breda’s forge and extrusion press installations in Russia, Italy, Germany and Australia. GS-Hydro has earned the role of preferred supplier to Danieli Breda through the successful implantation of over ten forge projects, to date. Danieli Breda, a division of the Italy-based Danieli Group, is a world-leading supplier of turn-key forging presses rated up to an immense 100 MN of force.

Danieli Breda has been successful through offering its custom-ers improved product quality while reducing their production and depreciation costs. One of their largest projects of the year was the installation of a new 30-MN forge press for a major steel mill mod-ernization program in Russia.In total, the press required delivery of over 3 kilometers of on-site hydraulic piping, weighing in at over 20 000 kilograms.

Forging squeezes metal into the desired shape, resulting in inher-ently stronger parts compared to the more traditional hammering. Most metals are cold forged, but iron and steel, being extremely hard, need to be hot forged. Not surprisingly, a forge press requires the application of considerable force. Indeed, Danieli Breda deliv-ers forges rated up to an immense 100 million newtons of force. This level of controlled force is only achieved in practice through the transfer of power via hydraulic piping. In extrusion, there is a similar need for tremendous force to squeeze metal through a die into the desired shape.

GS-Hydro Finland Oy won the Danieli Breda projects based on prov-en ability in turn-key project management and the ability to benefit from the worldwide reach of the whole GS-Hydro Group. The large diameters of the hydraulic pipes, combined with the high maximum working pressure of 350 bar, made GS-Hydro non-welded connec-tions a reliable choice. In addition, the numerous T-junctions in such complex systems make non-welded technology the only practical solution for assured cleanliness with on-site flushing. With cleanliness and leak-free operation assured, Danieli Breda can realize its customer promise of lower production and depreciation costs.

GS-Hydro – Creating Value Together

GS-Hydro | Annual Report 2008 16

Our strategy

Moving up the value chain

GS-Hydro’s strategy is to increase its “footprint” in its customers’ businesses by increasingly selling systems, value-adding services together with materials and products. The company is pursuing specific strategies to market and sell major projects and deepen its relationships with its key customers. The company is also systemati-cally developing the after-sales capabilities required to serve the total installed base of non-welded installations. The company be-lieves that its growing ability to implement large turn-key projects creates a barrier to entry for smaller competitors and a sustainable business model as a system provider.

Converting the market to clean non-welded solutions

GS-Hydro is making long-term marketing investments to promote the benefits of GS-Hydro non-welded technology compared to traditional arc welding, as well as promoting the use of original GS-Hydro connections compared to other materials. The benefits of GS-Hydro non-welded piping are zero fire hazard, inherent cleanli-ness, leak-free reliability, small space requirement and full docu-mentation, as well as pre-fabrication for fast, on-site installation.

The company’s marketing strategies have proven successful so far, especially in Europe, and continue to be implemented. The plan is to repeat this marketing success in North America and the growing Asian markets.

Developing personnel skills

GS-Hydro invests in recruiting and training skilled personnel in or-der to allow GS-Hydro to partner with its customers and be valued as an expert consultant in their choice of solutions.

Unifying operations

During the last few years operating margins have been positively impacted by integrating local and HQ operations, as well as increas-ing cooperation between frontline subsidiaries more efficiently. Strategies to further unify and integrate sourcing, administration and manufacturing are to be implemented in order to fully realize the operating efficiencies of a unified global enterprise.

Non-welded piping solutions are a small but growing segment of the overall industrial piping solutions market, where the majority of piping systems are installed using traditional “hot” arc weld-ing. In 2008, the size of the hydraulic and other high pressure industrial piping market was estimated to be EUR 13 billion, ex-cluding the markets in automotive and off-highway applications, which GS-Hydro does not address. In 2008, non-welded solutions accounted for approximately 6% market share, or approximately EUR 800 million in annual sales. With 94% of the market still served by traditional welding, GS-Hydro has significant long-term growth potential.

GS-Hydro is the leading supplier of non-welded piping solutions, with a market share approaching 20% overall. In the Offshore and Marine segments, the more demanding applications where GS-Hydro has focused its marketing, the company has signifi-cantly higher market shares.

GS-Hydro | Annual Report 2008 17

We provide innovative, non-welded piping solutions for demanding applications.

Mission

Vision

The recognized global leader in non-welded piping products, systems and services.

Partnering with customers and selected suppliers, we deliver high-quality products, systems and services worldwide. Our people provide the best service level, consistently.

Competitive strategy

GS-Hydro | Annual Report 2008 18

Non-welded: benefiting the environment

GS-Hydro’s business is fundamentally about replacing welding, a traditional but environmentally detrimental method of joining pipe sections. Our solutions offer a clean, safe alternative that takes advantage of modern working methods. Compared to welding, non-welded products and services are genuinely in the interest of a better environment, economical use of resources and environmental sustainability, as well as improved worker health and safety.

Using GS-Hydro’s connectors and services makes good business sense for customers in terms of overall costs, absence of fire haz-ard, cleanliness, leak-free reliability, documentation, prefabrication and speed of implementation. When also considering the positive environmental benefits, the case for using non-welded piping solu-tions is even stronger.

A clean start

GS-Hydro’s non-welded piping has the overwhelming benefit that the pipe spools and connectors are delivered ready-clean from the pre-fabrication process. Since the materials are not contaminated in the first place, a simple oil flush is all that is required before a GS-Hydro non-welded piping system is commissioned. Welded pip-ing systems, however, require acid flushing to dissolve and remove left-over contaminates from welding. An acid flush needs to be fol-lowed by acid-neutralizing flushing, flushing with hydraulic oil and finally filtering. Apart from being a time consuming activity in the most expensive phase of a piping project, cleaning produces large quantities of liquid toxic waste for disposal.

Sustainably clean

Maximum cleanliness is important in hydraulic systems because they utilize sophisticated components with high-tolerance moving parts, such as servo-valves, proportional valves and piston pumps. Contaminates remaining in the piping after commissioning gradu-ally destroy hydraulic components from within. Even sub micron-sized particles aggregate over time, forming larger particles that eventually have a destructive effect. Cleanliness is therefore not just an issue for the piping, but quickly becomes an issue for the entire hydraulic system. A clean system will not only reduce the need for frequent filter and fluid changing, but also increase the longevity of all hydraulic components used. Important for environmental sustainability, cleaner, well-maintained hydraulic systems also result in lower power consumption and less energy wasted.

During its working lifetime, hydraulic piping is subject to continu-ous vibration. Despite clamping the pipes securely, the enormous forces in hydraulics systems always result in some level of move-ment. Vibration does not affect non-welded connectors, but welded piping joints may be left with rough internal edges, called “welding icicles”. These imperfections can not always be success-fully removed by flushing, and vibration can cause small pieces of metal residue to break off – eventually damaging hydraulic components.

GS-Hydro | Annual Report 2008 19

Non-welded connectors are designed to be serviceable. By contrast, repairing welded hydraulic piping is very challenging. Welding qual-ity is highly dependent on individual welder skill. If weak, poorly welded joints need to be repaired, the entire piping system may need to be rewelded, followed by acid cleaning, neutralizing and oil flushing before being finally recommissioned.

Removing welding removes environmental risks

Traditional arc welding is “hot work” which inevitably creates the risk of explosions. Indeed welding is not possible in many demand-ing applications, such as installing piping on oil rigs or tankers. Welding torches emit gases, particulates and fumes which are poisonous in confined spaces and detrimental to the atmosphere. Welding results in small amounts of slag and solid residual waste for disposal, but the most insidious danger to the environment is the on-site storage of acids, neutralizing liquids and waste flushing oils which creates serious toxic spill risks to the local groundwater and soils.

GS-Hydro | Annual Report 2008 20

Personnel

With continued growth in operations, the number of personnel employed by GS-Hydro increased during the year. At the end of 2008, the company employed 640 piping specialists in 17 coun-tries, an increase from 527 in 2007.

Growth in personnel outpaced growth in sales during the year. This was partly due to the business mix continuing to evolve to include more added-value sales of services and projects, which are inherently more labor intensive, as well as the result of replacing outsourced labor with own skilled personnel.

The need to also broaden the range of competences available to the Group was another factor behind the continued growth in recruitment. In previous years, the main concern had been recruit-ment necessary to keep up with the rapid expansion in sales. In rec-ognition of the fact that GS-Hydro needs to attract and retain the best possible candidates, a unified global recruitment and induction process was introduced in 2008.

GS-Hydro’s goal of developing the Group into a unified global operation has tremendous implications for our personnel and personnel management, especially in the areas of competence and learning development. The future development of Group Human Resources management is a strategic imperative. The Group’s growth ambitions require personnel that are flexible, motivated and, above all, customer focused. Raising the personnel’s individual competence levels and the combined experience of the workforce will be crucial to the company’s future success.

During the year, strong emphasis was placed on increasing compe-tence in turn-key project delivery and strategic account manage-ment. During the 2008 strategy review process, it was decided to form an internal Competence and Learning Center to share globally agreed forms of development in knowledge, skills and attitude development. The main development area for the Center in 2008 was product and application knowledge sharing. Piloted in Asia, the resulting comprehensive, global training concept is ready for roll-out to other subsidiaries in 2009.

Our people, their knowledge and competence, are our strongest asset through which we can add value to our customers’ business. In turn, GS-Hydro recognizes that personnel satisfaction is vital for their continued commitment.

Company values and principles

Satisfaction of customers’ requirements and expectations is the key to realizing the value proposition GS-Hydro offers. The company trains all employees on understanding these requirements. Each individual employee within the organization is responsible for the quality of their own work and its development. Company policy is continuous improvement of functional quality of processes and services and provides the necessary resources for compliance with the quality policy. The performance of suppliers in understanding and supporting our quality policy is monitored closely. A code of business ethics has been actively communicated and shared with all GS-Hydro frontline subsidiaries and its enforcement is closely monitored by management.

GS-Hydro | Annual Report 2008 21

Health & Safety policy

GS-Hydro is committed to ensuring the health, safety and welfare of its employees as well as the safety of their working environment. The company accepts responsibility for customers and visitors who may be affected by our operations and ensures that statutory duties and obligations to them are met at all times. Company principle is that every employee in the company is provided with information, instruction and training as necessary, to carry out their duties safely. Management takes the responsibility to ensure that all processes and systems of work are designed to comply with all relevant local Health & Safety legislative requirements. GS-Hydro provides a safe and healthy working environment for its employees, customers and associates.

GS-Hydro | Annual Report 2008 22

Board of Directors´report

The Board of Directors hereby submit their report for 2008.

Ownership structure

Since 2004, the GS-Hydro Group has been wholly-owned by Sweden-based Ratos AB, a private equity company listed on the NASDAQ OMX Stockholm stock exchange. As part of the re-financ-ing of the Group in 2008, the corporate structure was reorganized as Ratos transferred its ownership of GS-Hydro Oy into a wholly owned holding company, GS Hydro Holding AB.

Operations

The GS-Hydro Group delivers complete, non-welded piping sys-tems, products (material packages and products) and services to its customers. The Group has a factory, located in Hämeenlinna, Finland, for manufacturing and developing its flange connectors. The business mix by sales is approximately 57% products and 43% systems and services. The main application for non-welded technology is in hydraulics, where the high-pressure sets demand-ing requirements on pipe connection quality. The Group operates directly through its own subsidiaries in 17 countries, covering the main markets of Europe, Asia and North America. Selected agents and distributors support sales in certain other markets.

In 2008, GS-Hydro acquired two small operations in the UK, BSH Ltd and Airedale Tubes & Fittings Ltd, which are wholly-owned by GS-Hydro UK Ltd.

Markets

GS-Hydro divides its markets into three segments: Offshore, Marine and Land-based. The latter segment comprises customers in several industries, including the metals, mining, pulp and paper, sugar/eth-anol, testing, aerospace and defense industries. Significant custom-ers for GS-Hydro are, for example, operators of oil exploration rigs, rig equipment manufacturers, shipyards and heavy engineering companies. In the Marine segment, GS-Hydro’s offering is mainly utilized by vessels with intensive hydraulic requirements, including those serving the offshore sector.

The markets for GS-Hydro products have grown rapidly during the last few years on the back of strong global growth in indus-trial investment, world trade and, in particular, new investments into oil and gas exploration. In 2008, the economies in most of GS-Hydro’s geographical market areas grew modestly overall, with strong growth at the beginning of the year, and modest growth or contraction at the end of the year.

The price of oil largely determines investments in oil exploration. In 2008, the price of oil was volatile. The average price for oil was $100/barrel (WTI), up 38% from 2007, which encouraged investments in the offshore industry. This was reflected by the good demand for GS-Hydro’s projects, materials and services in the Offshore and also Marine segments throughout the year. A significantly lower oil price at the end of the year had a negative impact on the rig manufacturers’ order intake but the yards’ order books remain at high levels. The overall demand outlook for piping systems remains positive also due the strong underlying drivers for long-term growth in the Offshore segment. The strong develop-ment in sales for the Marine segment reflected the large order books shipyards had built in the prior years. At the beginning of 2009, shipyard orders are, however, very weak. The Land-based segment experienced a slow-down in sales towards the end of 2008 due to the global recession.

Sales and financial result

Sales in 2008 benefitted from the long-term marketing of the benefits of GS-Hydro’s offering and the Group’s strategy to focus on the growing Offshore and Marine segments. GS-Hydro’s sales totaled EUR 159.0 million in 2008 (2007: EUR 141.9 million), an increase of 12% from 2007. At constant currency exchange rates, sales increased 16% in 2008 compared to 2007. Marine was the fastest growing segment of the Group, with sales up 35% in 2008. The Marine segment represented 29% (24%) of total sales in 2008. Sales to the Offshore segment also grew significantly faster than the overall growth in Group sales, with growth of 18%. The Offshore segment accounted for 34% (32%) of sales in 2008. Sales to the Land-based segment were slightly lower in 2008, compared to 2007, and accounted for 37% (44%) of Group sales.

For 2008, the operating profit before interests and taxes (EBIT) improved by 8.0% compared to 2007 and amounted to EUR 17.6 million, (2007: EUR 16.3 million, excluding the profit on the sale of real estate). In 2008, the positive development in profit was primarily attributable to the increased volume of sales. For 2008, the return on capital employed was 28%, compared to 28.5% in 2007. The profit before interest and taxes (EBIT) was 11.1% of sales in 2008 (2007: 11.5%). The financial expenses include a cost of EUR 1.358 million (2007: EUR 0.276 million) from currency rate fluctuations. The Group did not have financial instruments to hedge foreign currency risks at the balance sheet date.

GS-Hydro | Annual Report 2008 23

Investments, amortization and depreciation

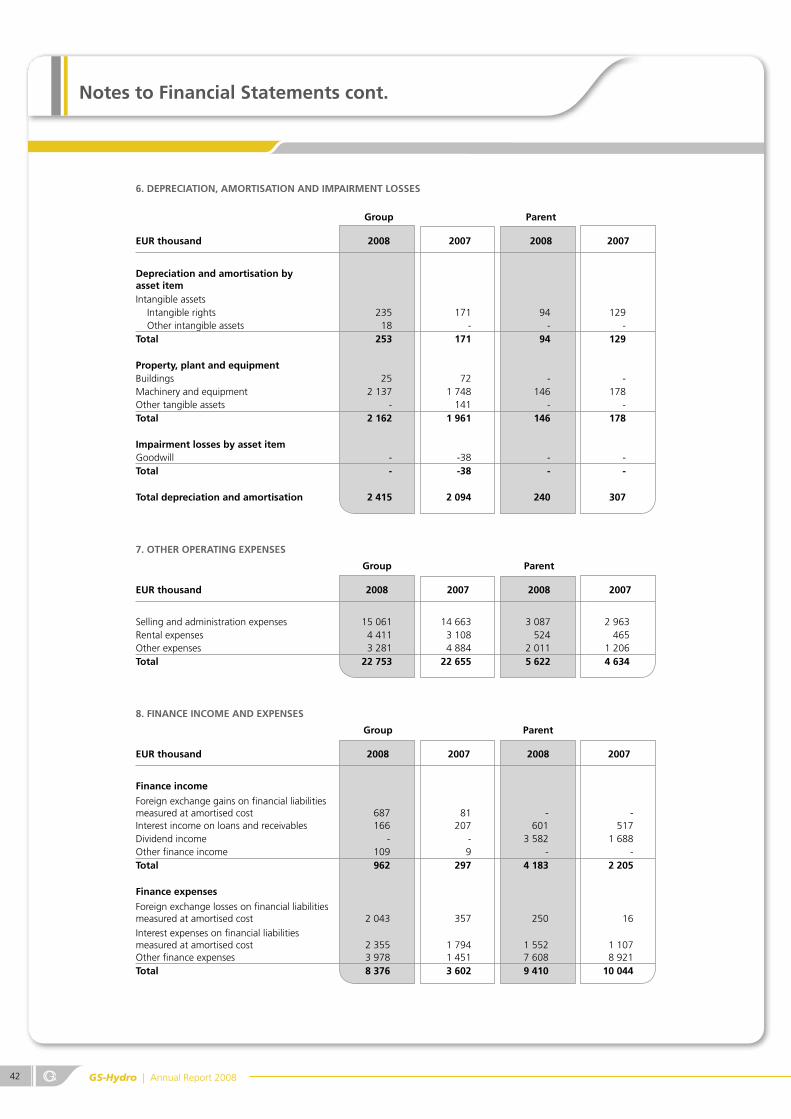

Investments in property, plant and equipment amounted to EUR 4.887 million in 2008 (2007: EUR 3.253 million), the increase was largely due to the acquisition of machinery and equipment. Depre-ciation and amortization totaled EUR 2.415 million in 2008 (2007: EUR 2.094 million).

Acquisition costs

Net acquisition costs for the purchase of the businesses in Norway and the U.K. were EUR 1.746 million in 2008. There were no acqui-sition costs recorded in 2007. The acquisition of Slangeservice Stord AS, via GS-Hydro Norge AS, was made in 2007, but the financial impact is recorded in 2008.

Refinancing

In September 2008, GS-Hydro was re-financed, resulting in a release of EUR 50 million. Ratos conducted the refinancing through selling all of its shares in GS-Hydro to a newly established entity, GS Hydro Holding AB, wholly owned by Ratos. The change in the par-ent company’s ownership triggered the repurchasing of the Group’s synthetic shares and options, as agreed under the terms of the option program. The costs of the re-financing are reflected in the increase in net financing costs, which rose to EUR 8.38 million, of which the one-time cost of repurchasing the synthetic shares and options was EUR 3.458 million. In 2007, total financing costs were EUR 3.602 million, including costs of EUR 1.106 million related to the synthetic shares and options.

Balance sheet, financing and cash flow

Net cash flow from operating activities for 2008 was positive and amounted to EUR 2.267 million (2007: EUR -1.088 million). The main reasons for the improvement in 2008 were the improved operating profit (when excluding the extraordinary items in 2007) and the small drop in inventories. These factors were partially offset by higher accounts receivable, lower accounts payable and higher net financing costs.

The cash position was EUR 11.24 million (2007: EUR 7.20 million). Inventories decreased slightly to EUR 34.7 million in 2008 (2007: EUR 35.0 million), resulting in a modest increase in inventory turns.

Liquidity and debt

At the year end 2008, liquid funds were EUR 11.24 million (2007: EUR 7.20 million) and interest-bearing liabilities totaled EUR 44.907 million (2007: EUR 36.097 million). Net debt amounted to EUR 33.67 million (2007: EUR 28.90 million). Interest-bearing liabilities consist of interest-bearing bank loans and credit limits. In 2008, the equity ratio was 33.4% (2007: 33.8%).

The Group signed a new facility agreement in September 2008. The EUR 60 million financing agreement with institutional investors includes term loans amounting to EUR 25 million, short term com-mitted credit limits amounting to an additional EUR 25 million and committed guarantees and L/C’s for EUR 10 million. The Group has covered the related interest risks by hedging 50% of the term loan interests with interest SWOPs which link the otherwise employed 3-month interest periods into a 3-year fixed rate. The Group uses hedge accounting for the interest. The SWOPs and changes in SWOP values were booked directly to the equity in the balance sheet.

Orders received and order book

Orders received in 2008 totaled EUR 165 million (2007: EUR 143 million), an increase of 15% from 2007. At the end of 2008 the order book totaled EUR 33 million, compared to EUR 30 million at the end of 2007.

Risk management

Business risks can be allocated to three categories: Financial Risks, Business Risks related to system deliveries and Raw Material Risks related to material availability and cost variability.

- Financial Risks: currency exchange rate risk and other financial risks are covered centrally at GS-Hydro Group level, The contractual cash flows are hedged through forward contracts by the sales subsidiaries on a case-by-case basis when receivables or payables are in a foreign currency. Receivables collection has high importance to mitigate risks related to accounts receivable outstanding.

- Business Risks: These risks relate to system deliveries around the world. Successful system deliveries not only secure profitability and growth, but are also the corner stone of customer satisfac- tion with GS-Hydro. Senior management has a system in place for specific risk review of all customer projects greater than EUR 250 thousand.

GS-Hydro | Annual Report 2008 24

Board of Directors´report

- Raw Material Risks: These risks relate to the availability and cost of raw materials and are addressed by working in close coopera- tion with strategic suppliers.

GS-Hydro management is responsible for continuous assessment of potential business risks and their impact on company operations.

Short-term risks and uncertainties

The global economic situation is highly uncertain due to the finan-cial crisis and global economic downturn. GS-Hydro’s operations are subject to market risks, eased to some extent by the fact that the system business is late-cyclical. However, shipbuilding in par-ticular has been affected by significant order cancellations due to lower shipping utilization rates, combined with significant increases in financing costs. Furthermore, customers’ and suppliers’ financial situations will increase risks related to collection of receivables and the level of bad debts.

Personnel

At year-end 2008, the GS-Hydro Group employed 640 people in 17 countries, compared to 527 people in 2007. The corresponding cost of salaries and wages was EUR 34.436 million in 2008 (2007: EUR 28.881 million). The average number of personnel in 2008 was 584 compared to 466 in 2007. With the high growth in sales, the number of employees at GS-Hydro Group has correspondingly increased over the last three years. Developing human resources is a strategic priority for the company.

Research and development

The Group’s R&D activities are centralized in the GS-Supply unit in Finland. R&D activities primarily concentrate on ensuring the competitiveness of GS-Hydro’s product offering by maintaining type approvals and certificates. In addition, R&D also develops new products. In 2008, R&D expenses were EUR 0.1 million (2007: EUR 0.1 million).

Quality and certificates

Quality Management System

GS-Hydro operates under a Quality Management System, conform-ing to the International Standard ISO 9001:2000. The company’s Leadership System also complies with ISO 9001:2000. Quality of operations, products and customer solutions are critical business factors for GS-Hydro. The company manufactures, sources and

delivers only products and materials which have all the relevant certificates needed in different customer segments. In system sales, the Quality Management System also covers projects and services for piping system implementations. The annual customer satisfac-tion measurement audit, used to monitor the effectiveness of operations, showed improved customer experiences in 2008.

Certification

GS-Piping System products have undergone rigorous test programs and have been certified by leading global oil companies and classifi-cation agencies, including Lloyd’s Register, the American Bureau of Shipping and Bureau Veritas. GS-Piping Systems are also specifically approved to be used offshore by NORSOK (piping specifications IS70, IS80, GS70 and JS80). GS-Hydro as a manufacturer of piping systems has been audited by DNV according Directive 97/23/EC on Pressure Equipment and is allowed to affix a CE-mark followed by the DNV identification number to its piping system deliveries.

Health and safety

GS-Hydro is responsible for ensuring the health, safety and wel-fare of its employees and their working environment. Company management has the responsibility to ensure that all processes and systems of work are designed to comply with all relevant Health and Safety legislative requirements.

Environmental sustainability

GS-Hydro believes its product innovations are in the interest of en-vironmental safety, economical use of resources and environmental sustainability. The company’s environmental system complies with legal obligations, identification of environmental aspects and risk. The company aims for continuous improvement in environmental performance when developing operations, processes and products. In 2008, the Group conducted an internal environmental survey of its facilities world-wide. No major environmental risks were identi-fied in the survey.

Competition

GS-Hydro operates in a competitive environment. The company’s non-welded offering is a relatively recent innovation and competes mainly with traditional welded solutions, which represent the bulk of the market. GS-Hydro also competes with smaller, locally operating companies specialized in delivering non-welded piping systems. In materials and products, the company also competes with diversified multi-national companies. Non-welded piping

GS-Hydro | Annual Report 2008 25

solutions compete favorably with traditional welding on criteria such as high cleanliness, serviceability, pre-fabrication, rapid on-site installation, and zero-fire hazard. The material costs for non-welded solutions are sometimes higher than for welded solutions, but GS-Hydro’s piping solutions compete favorably on overall system costs, implementation times, and piping life-cycle costs. Addition-ally, GS-Hydro’s high-quality solutions improve customers’ business metrics, including higher up-times, lower maintenance costs and lower investment depreciation costs.

Outlook for 2009

The growth in global gross domestic production is forecast to be negative in 2009. The global recession, which has deepened during the first months of 2009, will also impact growth and profitability at GS-Hydro. However, the Group has built a strong foundation during the last few years which will enable it to cope with slowing markets. During this period of uncertainty, the Group will also use the opportunities to further develop internal skills and efficiencies in preparation for the resumption of market growth.

During the first months of 2009 the demand for GS-Hydro’s solu-tions has been good, but due to the global financial and economic uncertainty it is very difficult to forecast the Group’s full-year performance for 2009.

Proposals of the Board of Directors The Board proposes that no dividend be paid for 2008.

GS-Hydro | Annual Report 2008 26

Financial Statements

Note 1 Jan–31 Dec 2008 1 Jan–31 Dec 2007

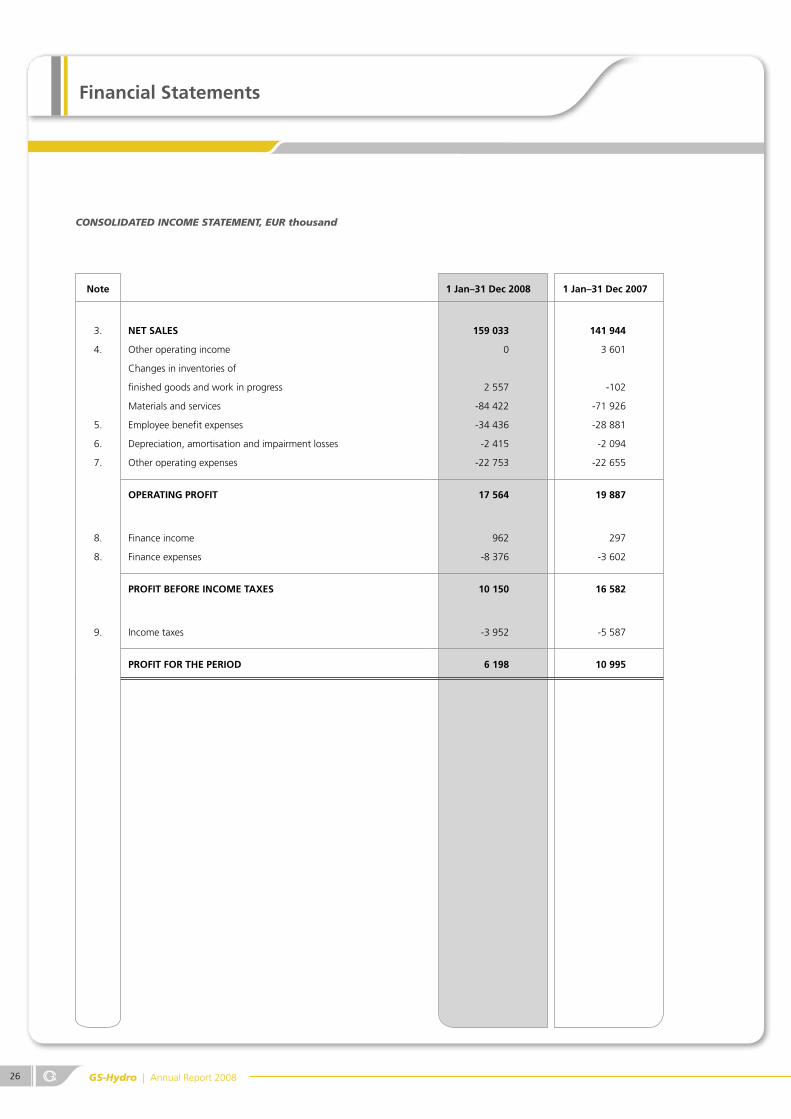

3. NET SALES 159 033 141 944

4. Other operating income 0 3 601

Changes in inventories of

finished goods and work in progress 2 557 -102

Materials and services -84 422 -71 926

5. Employee benefit expenses -34 436 -28 881

6. Depreciation, amortisation and impairment losses -2 415 -2 094

7. Other operating expenses -22 753 -22 655

OPERATING PROFIT 17 564 19 887

8. Finance income 962 297

8. Finance expenses -8 376 -3 602

PROFIT BEFORE INCOME TAXES 10 150 16 582

9. Income taxes -3 952 -5 587

PROFIT FOR THE PERIOD 6 198 10 995

CONSOLIDATED INCOME STATEMENT, EUR thousand

GS-Hydro | Annual Report 2008 27

CONSOLIDATED BALANCE SHEET, EUR thousand

Note 31 Dec 2008 31 Dec 2007

ASSETS

Non-current assets

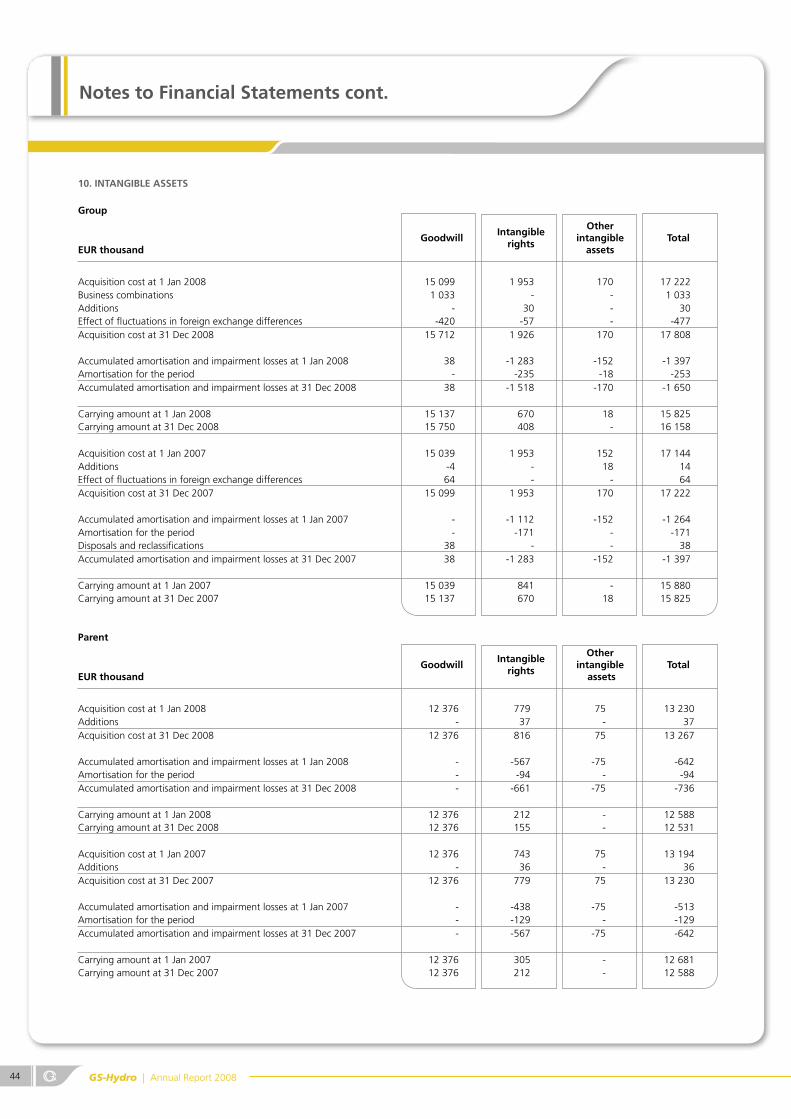

2.,10. Goodwill 15 750 15 137

10. Other intangible assets 408 688

11. Property, plant and equipment 8 343 6 455

17. Non-current receivables 397 440

12. Deferred tax assets 1 487 881

Total non-current assets 26 385 23 601

Current assets

13. Inventories 34 656 34 983

14. Trade and other receivables 39 552 35 608

Current tax receivables 393 112

15. Cash and cash equivalents 11 235 7 196

Total current assets 85 836 77 899

TOTAL ASSETS 112 221 101 500

EQUITY AND LIABILITIES

16. Equity

Share capital 4 528 4 528

Other reserves 6 256 6 325

Translation differences -691 49

Retained earnings 27 443 23 426

Total equity 37 536 34 328

Non-current liabilities

12. Deferred tax liabilities 432 694

18. Provisions 136 177

19. Interest-bearing liabilities 20 953 3 397

Total non-current liabilities 21 521 4 268

Current liabilities

20. Trade and other payables 28 544 29 446

Current tax liabilities 666 758

19. Interest-bearing liabilities 23 954 32 700

Total current liabilities 53 164 62 904

Total liabilities 74 685 67 172

TOTAL EQUITY AND LIABILITIES 112 221 101 500

GS-Hydro | Annual Report 2008 28

Financial Statements cont.

CONSOLIDATED CASH FLOW STATEMENT, EUR thousand

Note 1 Jan–31 Dec 2008 1 Jan–31 Dec 2007

Cash flows from operating activities

Profit for the period 6 198 10 995

Adjustments:

Depreciation, amortisation and impairment losses 2 415 2 094

Gains on sales of property, plant and equipment - -2 837

Finance income and expenses 7 414 3 305

Income taxes 3 952 5 587

Other adjustments 1 356 276

Change in working capital:

Change in trade and other receivables -5 714 -8 108

Change in inventories -1 034 -11 298

Change in trade and other payables -1 015 6 332

Change in provisions -41 -155

Interests paid -6 334 -3 247

Interests received 287 272

Income taxes paid -5 217 -4 304

Net cash flow from operating activities 2 267 -1 088

Cash flows from investing activities

2. Acquisition of subsidiaries, net of cash at the acquisition date -1 476 -

Acquisition of property, plant and equipment -4 887 -3 253

Proceeds from sale of investments - 6 438

Net cash flow from investing activities -6 363 3 185

Cash flows from financing activities

Proceeds (+) / repayment (-) of non-current liabilities 17 294 -1 658

Proceeds (+) / repayment (-) of current liabilities -8 727 3 323

Payment of finance lease liabilities -20 -19

Net cash flow from financing activities 8 547 1 646

Change in cash and cash equivalents 4 451 3 743

Cash and cash equivalents at the beginning of the financial period 7 196 3 532

Effect of foreign exchange rate fluctuations -412 -79

Cash and cash equivalents at the end of the financial period 11 235 7 196

GS-Hydro | Annual Report 2008 29

CONSOLIDATED STATEMENT OF CHANGES IN EQUITY, EUR thousand

Share capital

Other reserves

Hedging reserve

Translation reserve

Retained earnings Total

Equity at 31 Dec 2006 4 528 6 325 -258 12 504 23 099

Change in translation differences 334 334

Profit for the period 10 995 10 995

Recognised income and expenses for the period 334 10 995 11 329

Other adjustments -100 -100

Equity at 31 Dec 2007 4 528 6 325 76 23 399 34 328

Equity at 1 Jan 2008 4 528 6 325 76 23 399 34 328

Change in translation differences -2 921 -2 921

Recognised profit or loss of hedging of cash flow -69 -69

Profit for the period 6 198 6 198

Recognised income and expenses for the period -69 -2 921 6 198 3 208

Equity 31 Dec 2008 4 528 6 325 -69 -2 845 29 597 37 536

GS-Hydro | Annual Report 2008 30

Financial Statements cont.

INCOME STATEMENT FOR THE PARENT COMPANY, EUR thousand

Note 1 Jan–31 Dec 2008 1 Jan–31 Dec 2007

3. NET SALES 25 167 21 236

4. Other operating income 2 562 2 340

Changes in inventories of finished goods and work in progress 1 434 751

Materials and services -16 609 -13 675

5. Employee benefit expenses -3 338 -2 497

6. Depreciation, amortisation and impairment losses -240 -307

7. Other operating expenses -5 622 -4 634

OPERATING PROFIT 3 355 3 213

8. Finance income 4 183 2 205

8. Finance expenses -9 410 -10 044

PROFIT BEFORE INCOME TAXES -1 872 -4 626

9. Income taxes 17 -81

LOSS/PROFIT FOR THE PERIOD -1 855 -4 707

GS-Hydro | Annual Report 2008 31

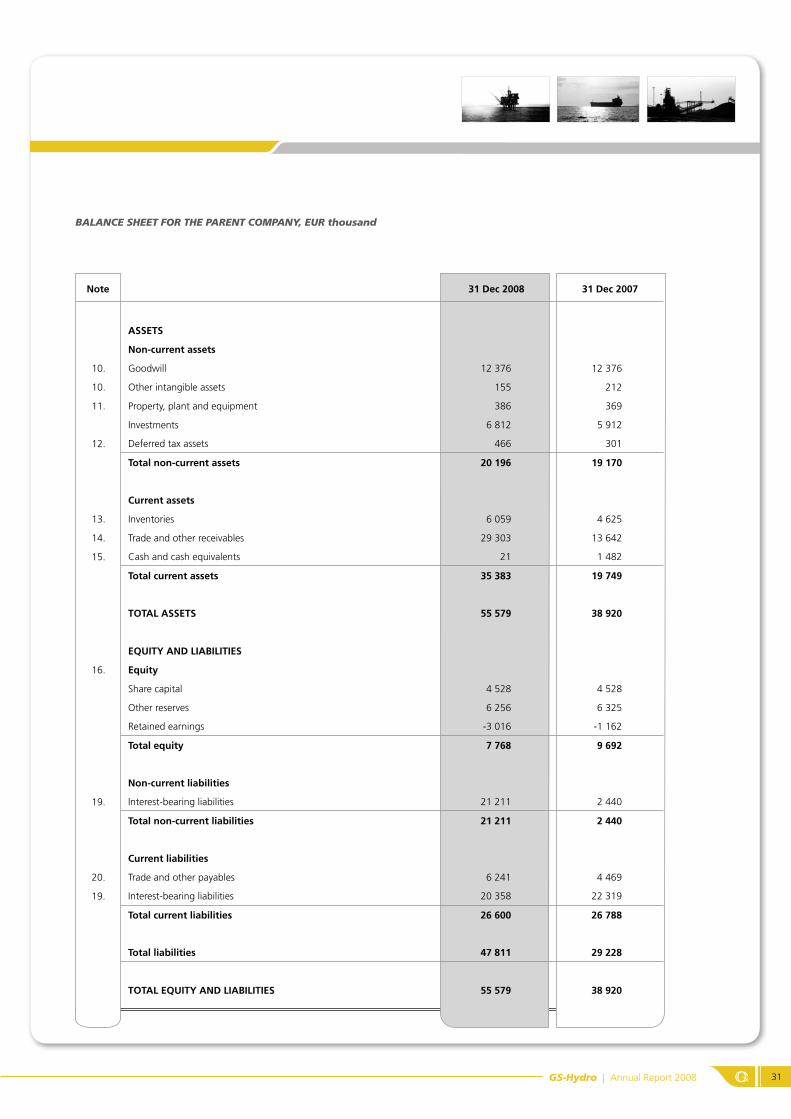

BALANCE SHEET FOR THE PARENT COMPANY, EUR thousand

Note 31 Dec 2008 31 Dec 2007

ASSETS

Non-current assets

10. Goodwill 12 376 12 376

10. Other intangible assets 155 212

11. Property, plant and equipment 386 369

Investments 6 812 5 912

12. Deferred tax assets 466 301

Total non-current assets 20 196 19 170

Current assets

13. Inventories 6 059 4 625

14. Trade and other receivables 29 303 13 642

15. Cash and cash equivalents 21 1 482

Total current assets 35 383 19 749

TOTAL ASSETS 55 579 38 920

EQUITY AND LIABILITIES

16. Equity

Share capital 4 528 4 528

Other reserves 6 256 6 325

Retained earnings -3 016 -1 162

Total equity 7 768 9 692

Non-current liabilities

19. Interest-bearing liabilities 21 211 2 440

Total non-current liabilities 21 211 2 440

Current liabilities

20. Trade and other payables 6 241 4 469

19. Interest-bearing liabilities 20 358 22 319

Total current liabilities 26 600 26 788

Total liabilities 47 811 29 228

TOTAL EQUITY AND LIABILITIES 55 579 38 920

GS-Hydro | Annual Report 2008 32

Financial Statements cont.

CASH FLOW STATEMENT FOR THE PARENT COMPANY, EUR thousand

Note 1 Jan–31 Dec 2008 1 Jan–31 Dec 2007

Cash flows from operating activities

Profit for the period -1 855 -4 707

Adjustments:

Depreciation, amortisation and impairment losses 240 307

Finance income and expenses 5 227 7 839

Income taxes -17 81

Change in working capital:

Change in trade and other receivables -4 029 5 206

Change in inventories -1 434 -751

Change in trade and other payables 1 773 -4 004

Interests paid -1 095 -1 159

Interests received 151 227

Income taxes paid -124 -22

Net cash flow from operating activities -1 165 3 016

Cash flows from investing activities

2. Acquisition of subsidiaries, net of cash at the acquisition date -3 000 -3 858

Acquisition of property, plant and equipment -60 -103

Acquisition of intangible assets -37 -36

Loans granted -13 790 -1 612

Dividend received 3 248 1 688

Net cash flow from investing activities -13 639 -3 921

Cash flows from financing activities

Proceeds (+) / repayment (-) of non-current liabilities 15 303 1 444

Proceeds (+) / repayment (-) of current liabilities -1 942 -6

Payment of finance lease liabilities -19 -19

Net cash flow from financing activities 13 343 1 420

Change in cash and cash equivalents -1 461 515

Cash and cash equivalents at the beginning of the financial period 1 482 967

Cash and cash equivalents at the end of the financial period 21 1 482

GS-Hydro | Annual Report 2008 33

STATEMENT OF CHANGES IN PARENT COMPANY EQUITY, EUR thousand

Share capital

Other reserves

Hedging reserve

Retained earnings

Total

Equity at 31 Dec 2006 4 528 6 325 3 545 14 399

Profit for the period -4 707 -4 707

Recognised income and expenses for the period -4 707 -4 707

Other adjustments

Equity at 31 Dec 2007 4 528 6 325 -1 162 9 692

Equity at 1 Jan 2008 4 528 6 325 -1 162 9 692

Recognised profit or loss of hedging of cash flow -69 -69

Profit for the period -1 855 -1 855

Recognised income and expenses for the period -69 -1 855 -1 924

Equity at 31 Dec 2008 4 528 6 325 -69 -3 016 7 768

GS-Hydro | Annual Report 2008 34

Notes to Financial Statements

CONTENTS

35 Reporting entity

Reporting entity . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 35 1. Significant accounting policies . . . . . . . . . . . . . . . . . . . . . . . 35 2. Business combinations, EUR thousand . . . . . . . . . . . . . . . . . 39 3. Distribution of net sales . . . . . . . . . . . . . . . . . . . . . . . . . . . . 41 4. Other operating income . . . . . . . . . . . . . . . . . . . . . . . . . . . . 41 5. Employee benefit expenses . . . . . . . . . . . . . . . . . . . . . . . . . . 41 6. Depreciation, amortisation and impairment losses. . . . . . . . . 42 7. Other operating expenses . . . . . . . . . . . . . . . . . . . . . . . . . . . 42 8. Finance income and expenses . . . . . . . . . . . . . . . . . . . . . . . . 42 9. Income taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 43 10. Intangible assets . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 44 11. Property, plant and equipment . . . . . . . . . . . . . . . . . . . . . . . 45 12. Deferred tax assets and liabilities. . . . . . . . . . . . . . . . . . . . . . 47 13. Inventories . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 48 14. Trade and other receivables. . . . . . . . . . . . . . . . . . . . . . . . . . 48 15. Cash and cash equivalents . . . . . . . . . . . . . . . . . . . . . . . . . . 48 16. Capital and reserves . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 49 17. Pension obligations. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 49 18. Provisions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 51 19. Carrying amounts of financial non-current and

current liabilities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 51 20. Trade and other payables . . . . . . . . . . . . . . . . . . . . . . . . . . . 54 21. Financial risk management . . . . . . . . . . . . . . . . . . . . . . . . . . 54 22. Capital management . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 55 23. Operating leases . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 56 24. Related parties . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 56 25. Commitments and contingent liabilities . . . . . . . . . . . . . . . . 57 26. Events after the balance sheet date. . . . . . . . . . . . . . . . . . . . 57

GS-Hydro | Annual Report 2008 35

REPORTING ENTITY

GS-Hydro Oy delivers complete, non-welded piping systems, prefabricated piping modules, separate piping components and after-sales services to its customers. GS-Hydro Oy is the parent company of the GS-Hydro Group, which is a part of the Ratos Group. The parent company of the Ratos Group is Ratos AB which is domiciled in Stockholm, Sweden. On Sep-tember 3rd, 2008, Ratos reorganized the corporate structure by transferring its ownership of GS-Hydro Oy into a wholly owned holding company, GS Hydro Holding AB.

Copies of the consolidated financial statements of GS-Hydro Oy are available at the GS-Hydro Oy’s main office, Lauta-tarhankatu 4, 13110 Hämeenlinna, Finland.

At its meeting on 30 March 2009, the Board of Directors of GS-Hydro Oy approved the publishing of these financial state-ments.

1. SIGNIFICANT ACCOUNTING POLICIES

Basis of preparation

These are the second consolidated financial statements of GS-Hydro Oy prepared in accordance with the International Financial Reporting Standards (IFRS), complying with the IAS and IFRS standards, as well as the Standing Interpretations Committee (SIC) and the International Financial Reporting Interpretations Committee (IFRIC) interpretations effective on 31 December 2008. In the Finnish Accounting Act and ordinances based on the provisions of the Act, IFRS refer to the standards and to their interpretations adopted in accordance with the procedures laid down in the regulation (EC) No 1606/2002 of the European parliament and of the Council. The notes to the financial statements are also in accordance with the requirements of Finnish Accounting and Companies’ Act supporting the IFRS requirements.

The parent company GS-Hydro Oy applies the same accounting principles as the GS-Hydro Group. GS-Hydro Oy’s date of transition to IFRS was 1 January 2006 and IFRS 1 First-time Adoption of International Financial Reporting Standards was applied in the transition. The Group applies the exemption provided in IFRS 1, which states that if a subsidiary becomes a first-time adopter later than its parent, the subsidiary may measure its assets and liabilities at the transition date at those amounts that were used in the Group reporting prior to the transition date. Ratos AB’s transition date to IFRS reporting was 1.1.2004.

The consolidated financial statements have been prepared on the historical cost basis except for those financial instru-ments that are measured to their fair value with changes in their value shown in the profit and loss statement. The consolidated financial statements are presented in thousands of euros.

Principles of consolidation

The consolidated financial statements include the parent company GS-Hydro Oy and all subsidiaries under the parent’s control. Control exists when over 50% of the voting rights are held directly or indi rectly by the parent company, or the parent company has otherwise the power to govern a subsidiary’s financial and operating policies.

The mutual shareholding has been eliminated by the purchase method. The financial statements of acquired subsidiaries are includ ed in the consolidated financial statements from the date that control commences, until the date that control ceases. Intra-Group transactions, receivables, liabilities and unrealised gains, as well as intra-Group distribution of profits, are eliminated. Unrealised losses are eliminated only to the extent that there is no evidence of impairment.

Items denominated in foreign currencies

The consolidated financial statements are presented in euro, which is the Group’s functional and presentation currency. The foreign currency transactions are translated into the functional currency using the exchange rate at the transaction date - in practice, a rate corresponding to approximately the transaction date exchange rate used in the translation. Receivables and liabilities denominated in foreign currency are translated into the functional currency using the exchange rate at the balance sheet date. The foreign exchange gains and losses relating to operating activities are included in the items above the operating profit, while foreign exchange gains and losses relating to financing activities are included in the finance income and expenses.

The income statements of those Group companies, whose functional currency is other than euro, are translated into euro by using the average exchange rate for the period and the balance sheets are translated at the exchange rate prevailing on the balance sheet date. The translation difference arising from such translations is recognised as a separate compo-nent of equity. Respectively, translation differences arising from the elimination of foreign subsidiaries’ acquisition cost and post-acquisition retained equity components are recognised as translation differences in equity. When a subsidiary is disposed of, the cumulative translation differences are recognised in the income statement as part of the gain or loss on the sale. Translation differences that have arisen before the adoption of IFRS in the Group reporting have been recognised in retained earnings and such translation differences will not, on disposal of the subsidiary, be recognised in the income statement in the future. From the IFRS transition date of the Ratos Group, 1 January 2004, the translation differences aris-ing from the consolidation are presented as a separate component of equity in the financial statements of GS-Hydro Oy. consolidation are presented as a separate component of equity in the financial statements of GS-Hydro Oy.

1.

GS-Hydro | Annual Report 2008 36

Notes to Financial Statements cont.

Intangible assets

GoodwillGoodwill represents the excess of the acquisition cost over the Group’s share of the fair values of the identifiable assets, liabilities and contingent liabilities on the acquisition date. In respect of business combinations carried out prior to the IFRS transition date of the Ratos Group, i.e. 1 January 2004, the carrying amount of goodwill is the carrying amount under FAS (Finnish Accounting Standards) on the date of transition, according to the transition rules in IFRS 1.

Goodwill is carried at acquisition cost, less accumulated impairment losses. Goodwill is not amortized, but is tested annu-ally for impairment.

Other intangible assets

Other intangible assets are recognised in the balance sheet at cost if they can be reliably measured and it is probable that the future economic benefits will flow to the Company. Other intangible assets are depreciated on a straight-line basis over their useful lives, which are 4 – 10 years.

Property, plant and equipment

Items of property, plant and equipment are measured at acquisition cost less accumulated depreciation and impairment losses. Normal maintenance costs are expensed as incurred.

Depreciation on property, plant end equipment is calculated on a straight-line basis over their estimated useful lives. Land areas are not depreciated. The estimated useful lives are as follows:

Buildings 25–40 yearsStructures 5–10 yearsMachinery and equipment 3–10 yearsOther tangible assets 5 years

The residual value and the useful life of the items of property, plant and equipment are reviewed on each balance sheet date and adjusted when necessary to reflect any changes in expected economic benefits. Gains and losses on disposal of property, plant and equipment are included in either other operating income or other operating expenses.

Impairment

On each balance sheet date the Group assesses whether there are indications of impairment of assets. If such indications exist, the assets’ recoverable amount is estimated. Goodwill is tested annually irrespective of whether any indications exist. The recoverable amount is the higher of an asset’s fair value (less the costs to sell) and its value in use. Value in use represents the present value of the discounted future net cash flows expected to be derived from the asset or a cash-generating unit. The discount rate used is a pre-tax interest rate.

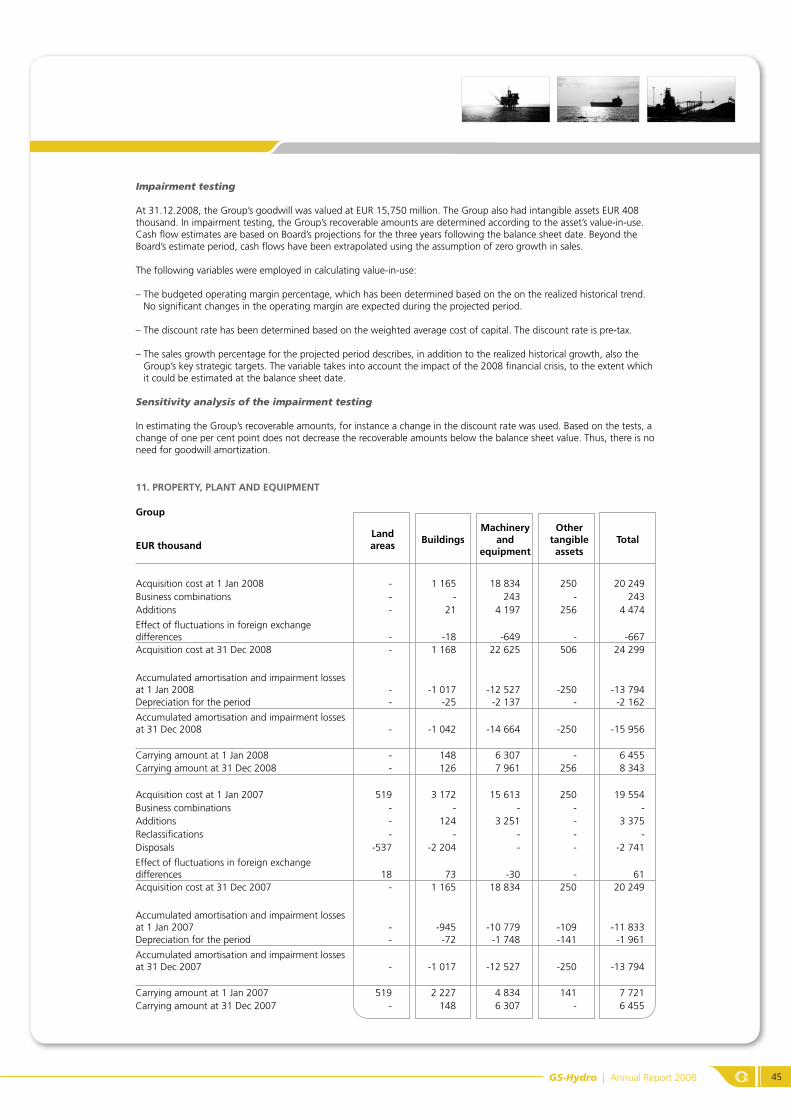

An impairment loss is recognised when the carrying amount of an asset exceeds its recoverable amount. When the impairment loss is recognised, the Group also reassesses the useful life of the asset. An impairment loss, other than an impairment loss in respect of goodwill, is reversed if there is a change in the estimates used to determine the recoverable amount of an asset. An impairment loss is reversed only to the extent that the asset’s carrying amount does not exceed the carrying amount that would have been determined had no impairment loss been recognised in prior periods. An impairment loss in respect of goodwill is never reversed.

Inventories

Inventories are measured at procurement costs or at the lower net realisable value. Net realisable value is the estimated selling price in the ordinary course of business, less the estimated costs of completion and costs to sell. Inventories are measured using the FIFO method (first-in, first-out). The cost of finished goods and work in progress consists of raw mate-rials, direct labour and other direct costs, as well as an appropriate share of production overheads.

Leases

The Group has leased items of machinery and equipment under finance and operating lease agreements. Those leases, which transfer substantially all the risks and rewards incidental to ownership of an asset to the lessee, are classified as finance leases. Assets acquired under finance leases are capitalised at the lower of their fair value or present value of mini-mum lease payments at the beginning of the lease period. Lease payments are divided into reduction of the lease liability and the interest charge for the period, so that a constant rate of interest is recognised on the outstanding balance of the lease liability. The lease liability is included in interest-bearing liabilities on the balance sheet.

Leases, which do not transfer the risks and rewards incidental to ownership of an asset to the lessee, are classified as operating leases. Rental payments made under operating leases are expensed as incurred.

Employee benefits

The Group’s pension plans are classified as defined contribution plans or defined benefit plans. Under defined contribu-tion plans, the Group pays fixed contributions into a separate entity and these payments are recognised as expenses in the

GS-Hydro | Annual Report 2008 37

period to which they relate. In respect of defined contribution plans, the Group does not have any legal or constructive obligation to pay further contributions if the entity, which receives the payments, does not hold sufficient assets to pay all employee benefits relating to employee service in the current and prior periods.

In respect of each defined benefit plan, the pension liability presented in the balance sheet is calculated using the pro-jected unit credit method. The pension costs are recognised as an expense in the income statement over the working lives of the employees based on actuarial calculations. The discount rate used in calculating the present value of the pension obligation is the yield on high quality corporate bonds or government bonds with a similar maturity to the obligation. The present value of the pension obligation to be recognised as a liability in the balance sheet is derived from the pension plan assets (measured at fair value on the balance sheet date), the proportion of unrecognised actuarial gains and losses, and the past service costs.

Actuarial gains and losses arise from the changes in actuarial assumptions used, or differences between the actuarial assumptions and actual outcomes. All accumulated actuarial gains and losses were recognised in retained earnings in the opening balance sheet at 1 January 2004 when GS-Hydro adopted IFRS-standards in its Group reporting to Ratos Group. Subsequently, the Group applied the corridor method, according to which the actuarial gains and losses are recognised in the income statement over the average remaining working lives of the employees to the extent that they exceed, by 10%, the greater of the present value of the defined benefit obligation or the fair value of the plan assets.

Past service costs are recognised as an expense, in equal portions, over the period during which the benefits vest. In case the benefits vest immediately, they are also recognised immediately in the income statement.

Borrowing costs

Borrowing costs are recognised as an expense in the period in which they are incurred.

Research and development expenditure

Research expenditure is recognised in the income statement as an expense as incurred. The Group has no such expendi-ture on development activities that would qualify under the capitalisation criteria set out in IAS 38 Intangible Assets.

Provisions

A provision is recognised when, as a result of a past event, the Group has a present legal or constructive obligation, whose realisation is probable and which can be measured reliably. The settlement of the obligation requires an outflow of economic benefits from the Group. The provisions consist mainly of the guarantee provisions.

Income taxes