GP Bullhound Market Update Tech Sector Offers Silver ... · GP Bullhound Market Update . Tech...

30

1 October 2011 GP Bullhound Market Update Tech Sector Offers Silver Lining to Eurozone Clouds Alessandro Casartelli [email protected] Office: +44 207 101 7594 Manish Madhvani [email protected] Office: +44 207 101 7567 Julien Oussadon [email protected] Office: +44 207 101 7587

Transcript of GP Bullhound Market Update Tech Sector Offers Silver ... · GP Bullhound Market Update . Tech...

1

October 2011 GP Bullhound Market Update Tech Sector Offers Silver Lining to Eurozone Clouds

Alessandro Casartelli [email protected] Office: +44 207 101 7594

Manish Madhvani [email protected] Office: +44 207 101 7567

Julien Oussadon [email protected] Office: +44 207 101 7587

2

TABLE OF CONTENTS

1 GENERAL ECONOMIC ENVIRONMENT

2 M&A AND IPO MARKET

3 DIGITAL MEDIA TRENDS

3

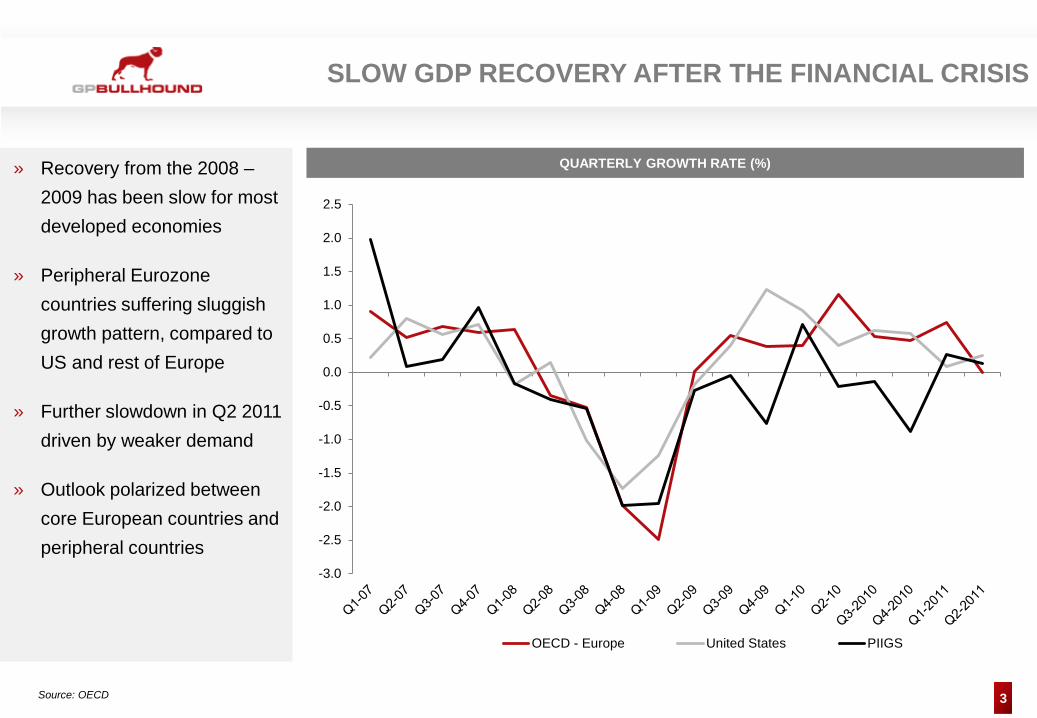

SLOW GDP RECOVERY AFTER THE FINANCIAL CRISIS

QUARTERLY GROWTH RATE (%)

Source: OECD

» Recovery from the 2008 – 2009 has been slow for most developed economies

» Peripheral Eurozone countries suffering sluggish growth pattern, compared to US and rest of Europe

» Further slowdown in Q2 2011 driven by weaker demand

» Outlook polarized between core European countries and peripheral countries

-3.0

-2.5

-2.0

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

OECD - Europe United States PIIGS

4

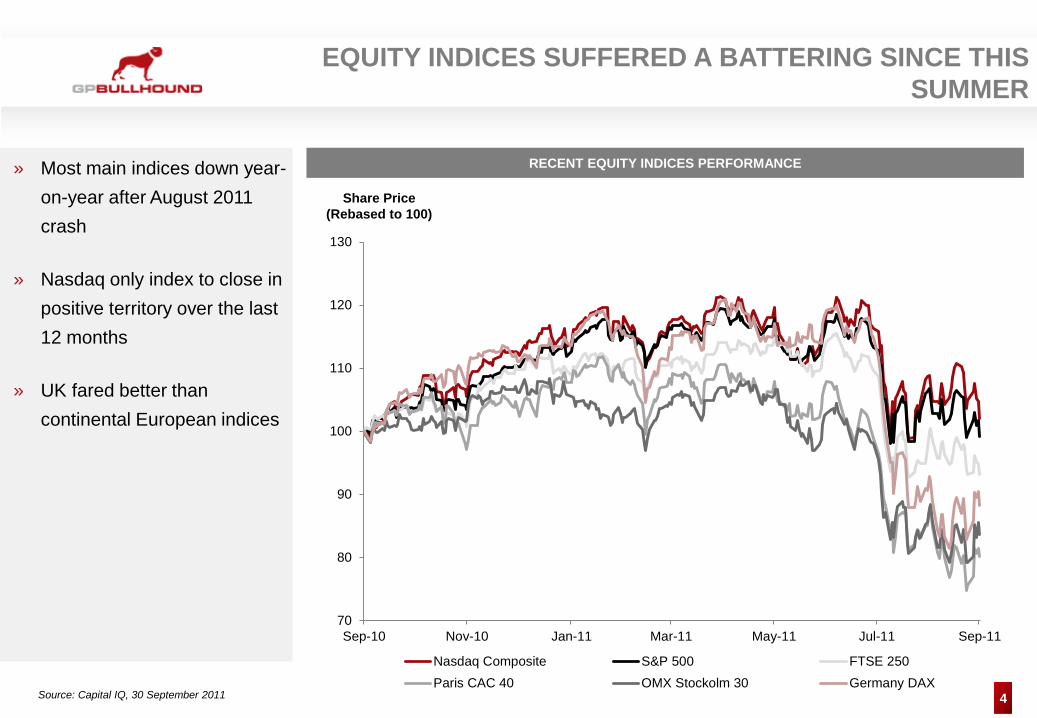

EQUITY INDICES SUFFERED A BATTERING SINCE THIS SUMMER

RECENT EQUITY INDICES PERFORMANCE

Source: Capital IQ, 30 September 2011

» Most main indices down year-on-year after August 2011 crash

» Nasdaq only index to close in positive territory over the last 12 months

» UK fared better than continental European indices

70

80

90

100

110

120

130

Sep-10 Nov-10 Jan-11 Mar-11 May-11 Jul-11 Sep-11

Nasdaq Composite S&P 500 FTSE 250Paris CAC 40 OMX Stockolm 30 Germany DAX

Share Price (Rebased to 100)

5

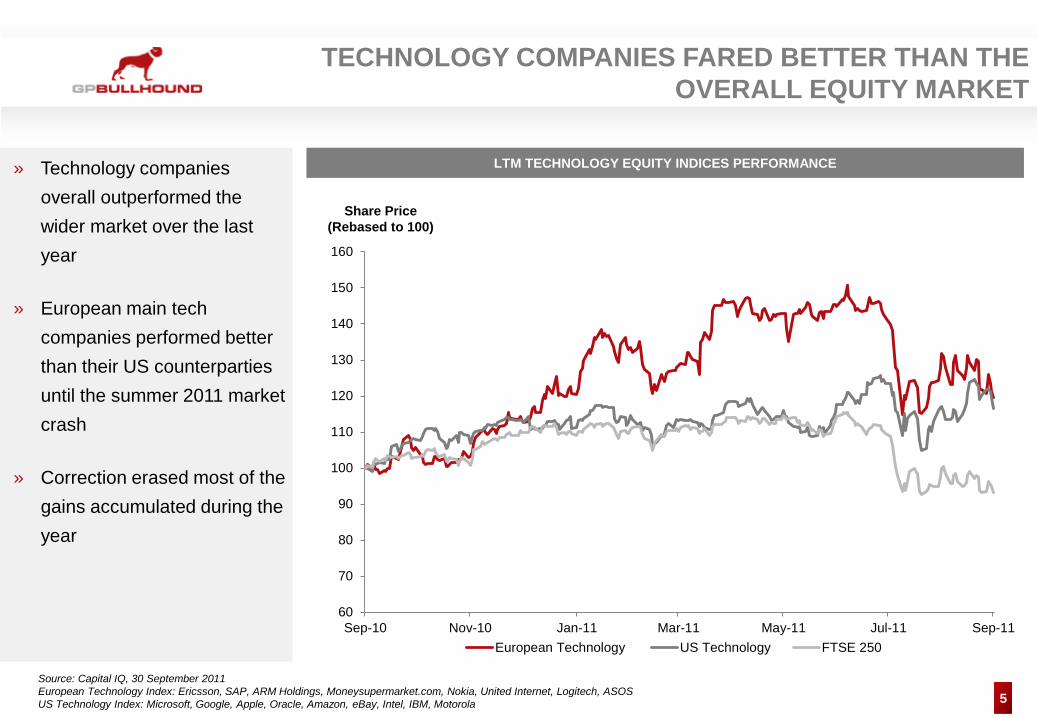

TECHNOLOGY COMPANIES FARED BETTER THAN THE OVERALL EQUITY MARKET

LTM TECHNOLOGY EQUITY INDICES PERFORMANCE

Source: Capital IQ, 30 September 2011 European Technology Index: Ericsson, SAP, ARM Holdings, Moneysupermarket.com, Nokia, United Internet, Logitech, ASOS US Technology Index: Microsoft, Google, Apple, Oracle, Amazon, eBay, Intel, IBM, Motorola

» Technology companies overall outperformed the wider market over the last year

» European main tech companies performed better than their US counterparties until the summer 2011 market crash

» Correction erased most of the gains accumulated during the year

60

70

80

90

100

110

120

130

140

150

160

Sep-10 Nov-10 Jan-11 Mar-11 May-11 Jul-11 Sep-11European Technology US Technology FTSE 250

Share Price (Rebased to 100)

6

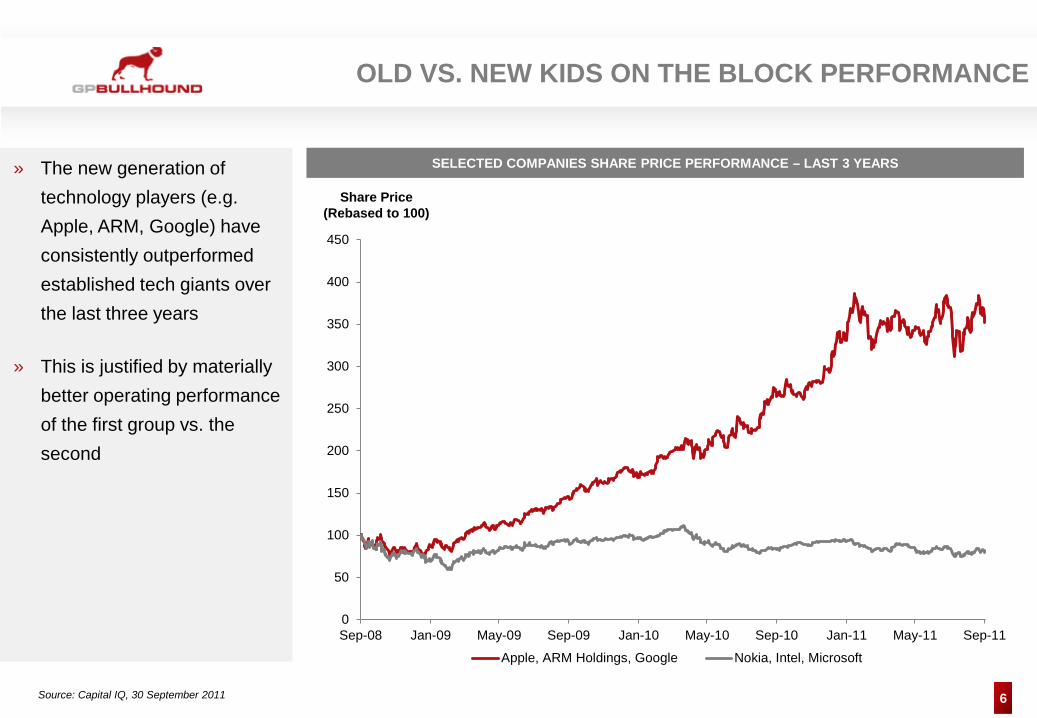

OLD VS. NEW KIDS ON THE BLOCK PERFORMANCE

SELECTED COMPANIES SHARE PRICE PERFORMANCE – LAST 3 YEARS

Source: Capital IQ, 30 September 2011

» The new generation of technology players (e.g. Apple, ARM, Google) have consistently outperformed established tech giants over the last three years

» This is justified by materially better operating performance of the first group vs. the second

0

50

100

150

200

250

300

350

400

450

Sep-08 Jan-09 May-09 Sep-09 Jan-10 May-10 Sep-10 Jan-11 May-11 Sep-11

Apple, ARM Holdings, Google Nokia, Intel, Microsoft

Share Price (Rebased to 100)

7

0.0x

2.0x

4.0x

6.0x

8.0x

10.0x

Q2 09 Q3 09 Q4 09 Q1 10 Q2 10 Q3 10 Q4 10 Q1 11 Q2 11 Q3 11

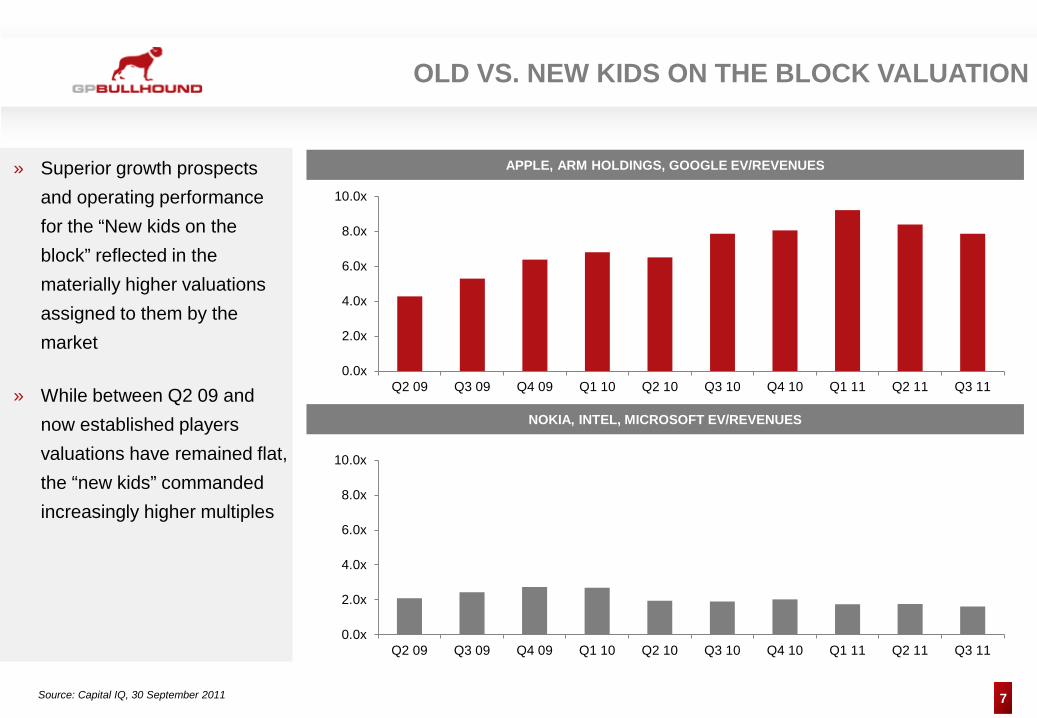

OLD VS. NEW KIDS ON THE BLOCK VALUATION

NOKIA, INTEL, MICROSOFT EV/REVENUES

Source: Capital IQ, 30 September 2011

APPLE, ARM HOLDINGS, GOOGLE EV/REVENUES

0.0x

2.0x

4.0x

6.0x

8.0x

10.0x

Q2 09 Q3 09 Q4 09 Q1 10 Q2 10 Q3 10 Q4 10 Q1 11 Q2 11 Q3 11

» Superior growth prospects and operating performance for the “New kids on the block” reflected in the materially higher valuations assigned to them by the market

» While between Q2 09 and now established players valuations have remained flat, the “new kids” commanded increasingly higher multiples

8

TABLE OF CONTENTS

1 GENERAL ECONOMIC ENVIRONMENT

2 M&A AND IPO MARKET

3 DIGITAL MEDIA TRENDS

9

$315m

$855m

$464m$230m

$358m

$1,137m $1,153m$913m

$2,207m

$665m

$322m$444m

$234m

$1,383m

$380m

$823m

$1,746m

$396m

$860m$641m

2007 2008 2009 2010 2011 YTD

23 212 39 293 36 197 27 264 48 150 26 200 33 172 47 218 30 173 34 194

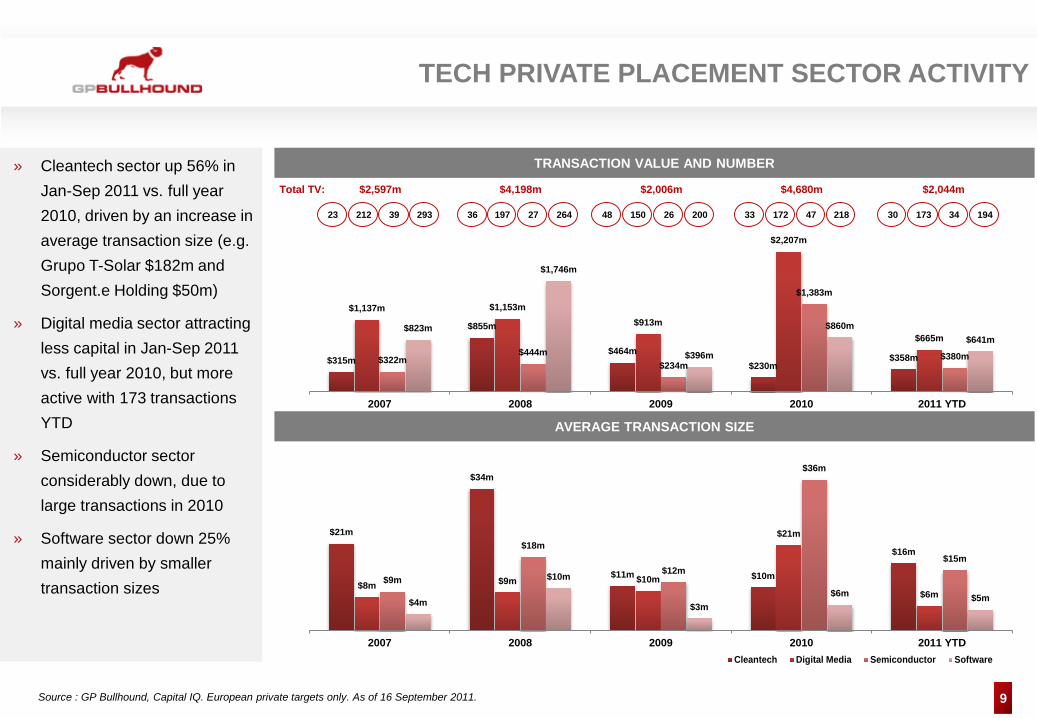

TECH PRIVATE PLACEMENT SECTOR ACTIVITY

TRANSACTION VALUE AND NUMBER

Source : GP Bullhound, Capital IQ. European private targets only. As of 16 September 2011.

» Cleantech sector up 56% in Jan-Sep 2011 vs. full year 2010, driven by an increase in average transaction size (e.g. Grupo T-Solar $182m and Sorgent.e Holding $50m)

» Digital media sector attracting less capital in Jan-Sep 2011 vs. full year 2010, but more active with 173 transactions YTD

» Semiconductor sector considerably down, due to large transactions in 2010

» Software sector down 25% mainly driven by smaller transaction sizes

AVERAGE TRANSACTION SIZE

Cleantech Digital Media Semiconductor Software

$21m

$34m

$11m $10m

$16m

$8m $9m $10m

$21m

$6m$9m

$18m

$12m

$36m

$15m

$4m

$10m

$3m$6m $5m

2007 2008 2009 2010 2011 YTD

$2,597m $4,198m $2,006m $4,680m $2,044m Total TV:

10

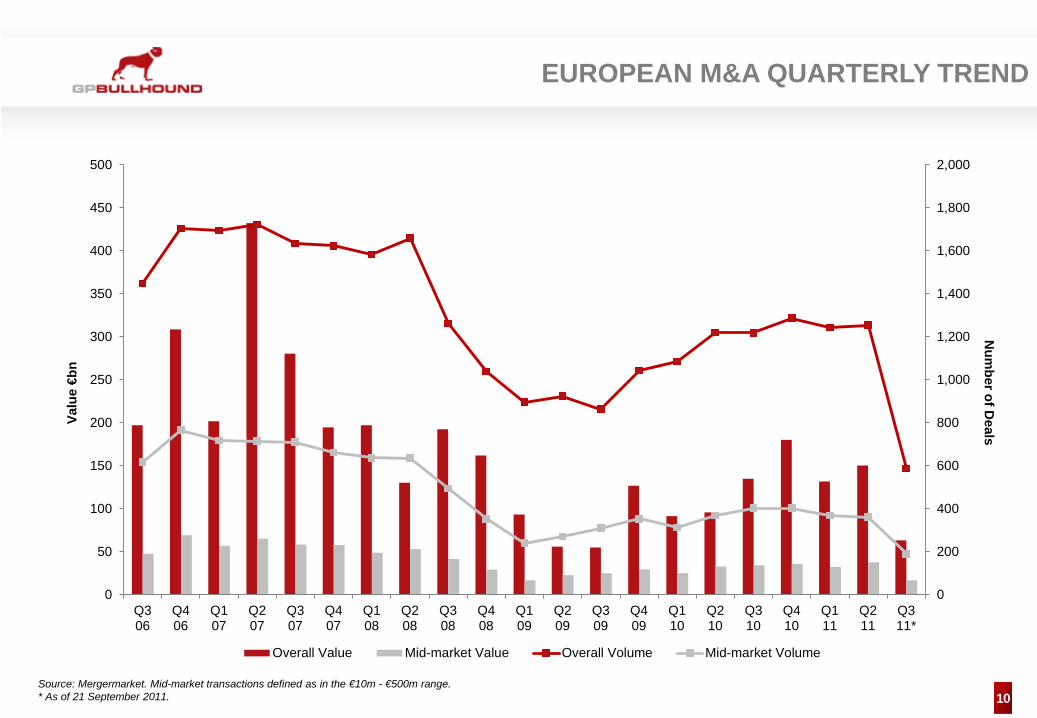

EUROPEAN M&A QUARTERLY TREND

Source: Mergermarket. Mid-market transactions defined as in the €10m - €500m range. * As of 21 September 2011.

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

0

50

100

150

200

250

300

350

400

450

500

Q306

Q406

Q107

Q207

Q307

Q407

Q108

Q208

Q308

Q408

Q109

Q209

Q309

Q409

Q110

Q210

Q310

Q410

Q111

Q211

Q311*

Overall Value Mid-market Value Overall Volume Mid-market Volume

Num

ber of Deals

Valu

e €b

n

11

$67m

$127m

$46m $51m

$206m

$67m

$103m

$135m

$45m$35m

$67m

$200m

$121m

$154m

$52m$37m

$78m$56m

$34m $41m

2007 2008 2009 2010 2011 YTD

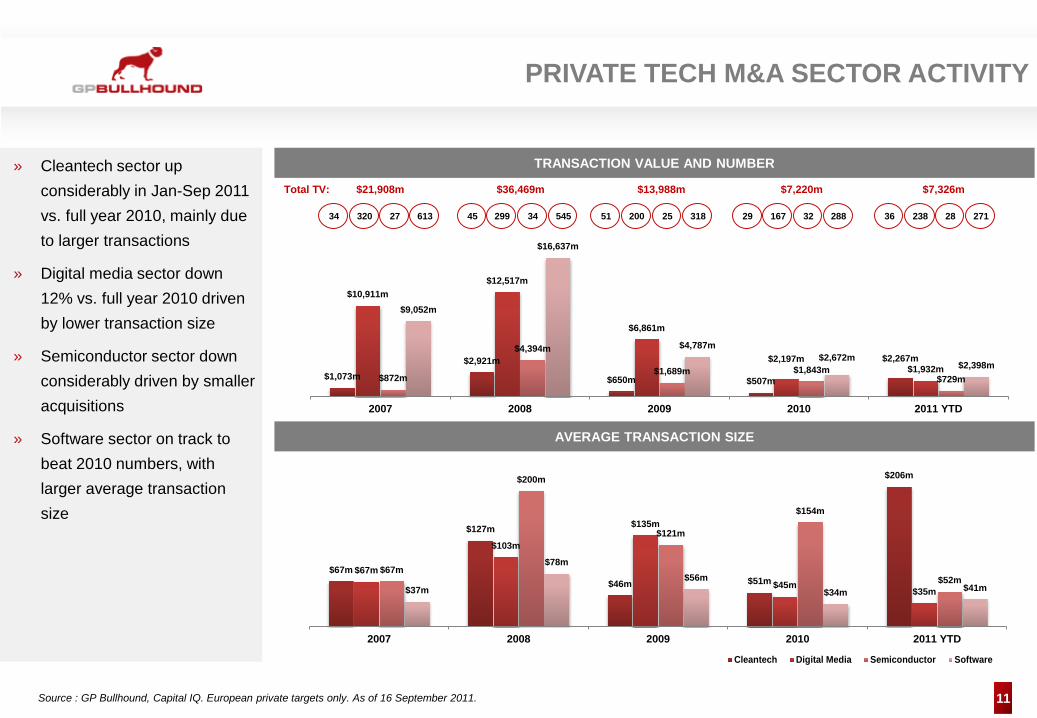

PRIVATE TECH M&A SECTOR ACTIVITY

» Cleantech sector up considerably in Jan-Sep 2011 vs. full year 2010, mainly due to larger transactions

» Digital media sector down 12% vs. full year 2010 driven by lower transaction size

» Semiconductor sector down considerably driven by smaller acquisitions

» Software sector on track to beat 2010 numbers, with larger average transaction size

Cleantech Digital Media Semiconductor Software

TRANSACTION VALUE AND NUMBER

AVERAGE TRANSACTION SIZE

Source : GP Bullhound, Capital IQ. European private targets only. As of 16 September 2011.

$21,908m $36,469m $13,988m $7,220m $7,326m Total TV:

$1,073m$2,921m

$650m $507m

$2,267m

$10,911m$12,517m

$6,861m

$2,197m$1,932m

$872m

$4,394m

$1,689m $1,843m$729m

$9,052m

$16,637m

$4,787m$2,672m

$2,398m

2007 2008 2009 2010 2011 YTD

34 320 27 613 45 299 34 545 51 200 25 318 29 167 32 288 36 238 28 271

12

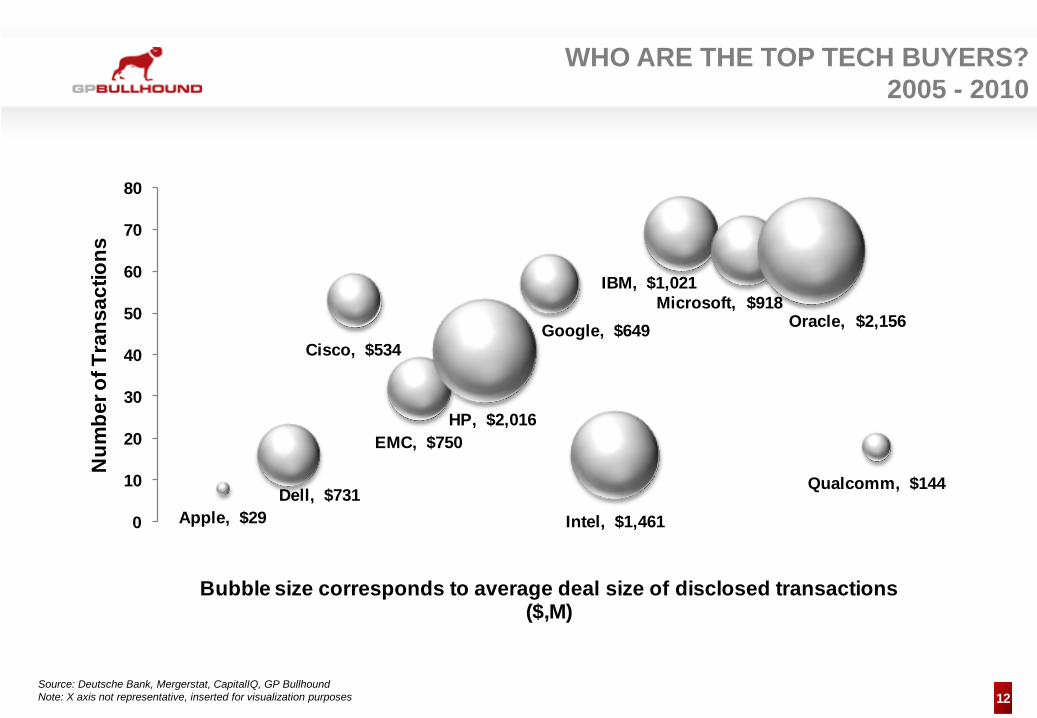

Apple, $29 Dell, $731

Cisco, $534

EMC, $750 HP, $2,016

Google, $649

Intel, $1,461

IBM, $1,021 Microsoft, $918

Oracle, $2,156

Qualcomm, $144

0

10

20

30

40

50

60

70

80

0 2 4 6 8 10 12

Num

ber o

f Tra

nsac

tions

Bubble size corresponds to average deal size of disclosed transactions ($,M)

WHO ARE THE TOP TECH BUYERS? 2005 - 2010

Source: Deutsche Bank, Mergerstat, CapitalIQ, GP Bullhound Note: X axis not representative, inserted for visualization purposes

13

0

10,000

20,000

30,000

40,000

50,000

60,000Sep-11Sep-10Sep-09

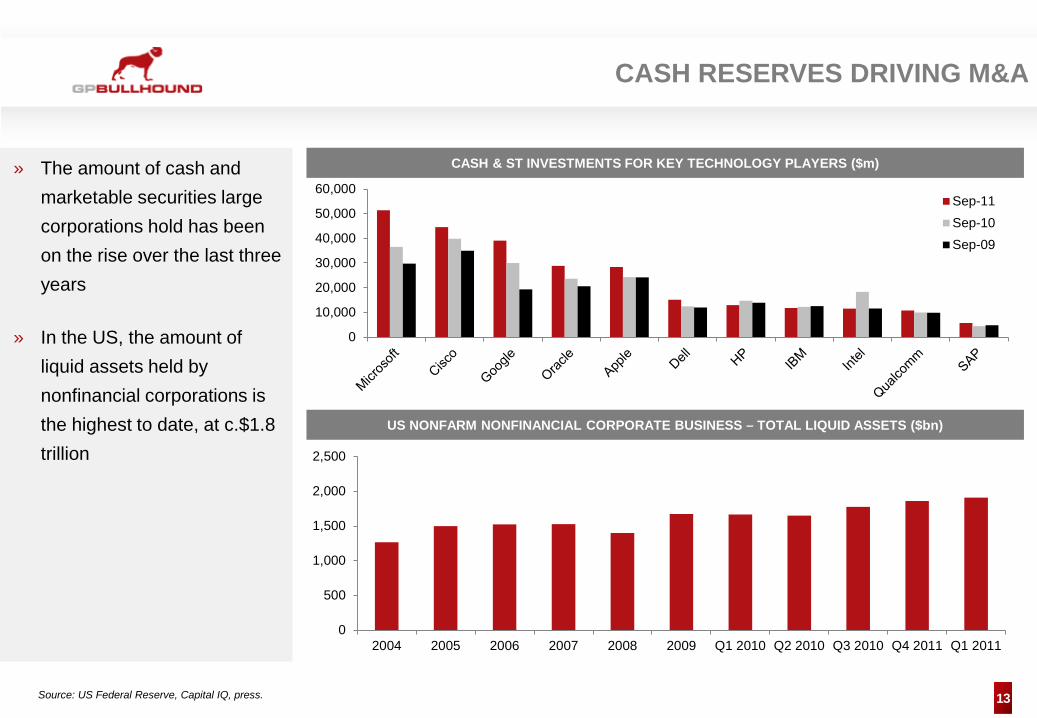

CASH RESERVES DRIVING M&A

CASH & ST INVESTMENTS FOR KEY TECHNOLOGY PLAYERS ($m)

Source: US Federal Reserve, Capital IQ, press.

US NONFARM NONFINANCIAL CORPORATE BUSINESS – TOTAL LIQUID ASSETS ($bn)

0

500

1,000

1,500

2,000

2,500

2004 2005 2006 2007 2008 2009 Q1 2010 Q2 2010 Q3 2010 Q4 2011 Q1 2011

» The amount of cash and marketable securities large corporations hold has been on the rise over the last three years

» In the US, the amount of liquid assets held by nonfinancial corporations is the highest to date, at c.$1.8 trillion

14

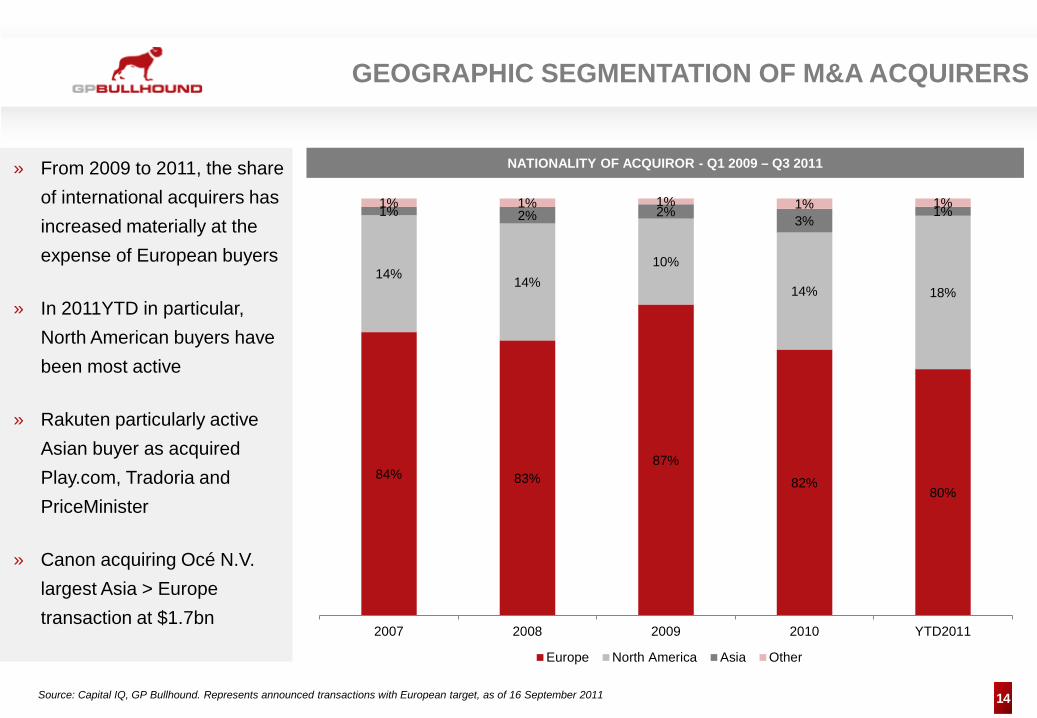

GEOGRAPHIC SEGMENTATION OF M&A ACQUIRERS

NATIONALITY OF ACQUIROR - Q1 2009 – Q3 2011

84% 83% 87%

82% 80%

14% 14% 10%

14% 18%

1% 2% 2% 3%

1% 1% 1% 1% 1% 1%

2007 2008 2009 2010 YTD2011

Europe North America Asia Other

Source: Capital IQ, GP Bullhound. Represents announced transactions with European target, as of 16 September 2011

» From 2009 to 2011, the share of international acquirers has increased materially at the expense of European buyers

» In 2011YTD in particular, North American buyers have been most active

» Rakuten particularly active Asian buyer as acquired Play.com, Tradoria and PriceMinister

» Canon acquiring Océ N.V. largest Asia > Europe transaction at $1.7bn

15

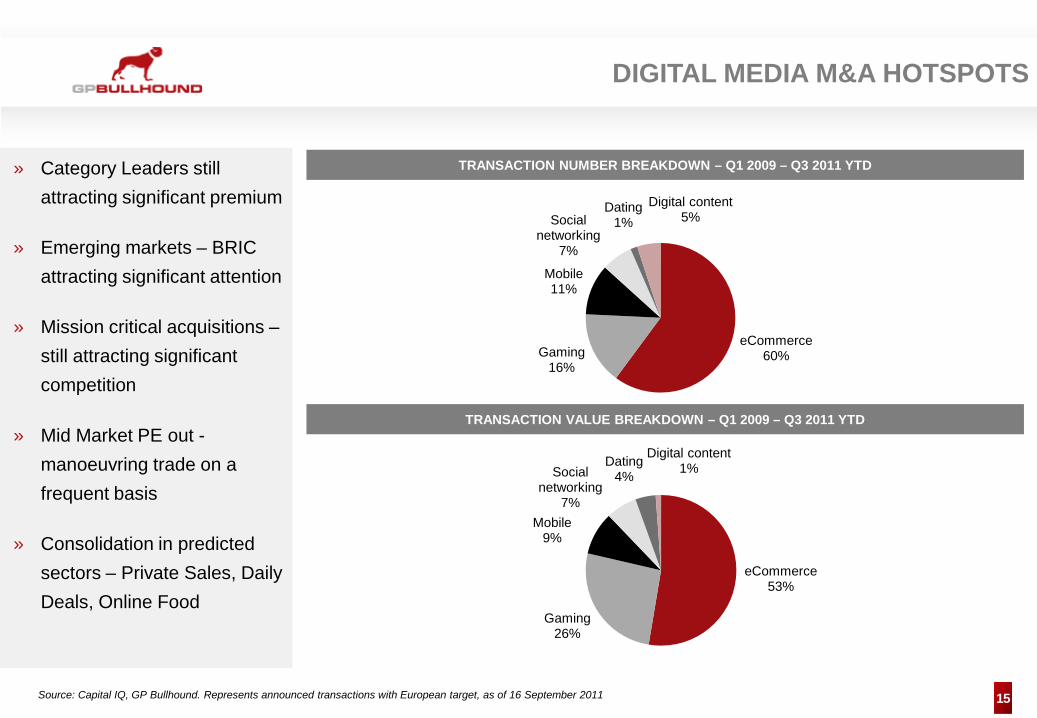

DIGITAL MEDIA M&A HOTSPOTS

TRANSACTION VALUE BREAKDOWN – Q1 2009 – Q3 2011 YTD

TRANSACTION NUMBER BREAKDOWN – Q1 2009 – Q3 2011 YTD

eCommerce 60% Gaming

16%

Mobile 11%

Social networking

7%

Dating 1%

Digital content 5%

eCommerce 53%

Gaming 26%

Mobile 9%

Social networking

7%

Dating 4%

Digital content 1%

Source: Capital IQ, GP Bullhound. Represents announced transactions with European target, as of 16 September 2011

» Category Leaders still attracting significant premium

» Emerging markets – BRIC attracting significant attention

» Mission critical acquisitions –still attracting significant competition

» Mid Market PE out -manoeuvring trade on a frequent basis

» Consolidation in predicted sectors – Private Sales, Daily Deals, Online Food

16

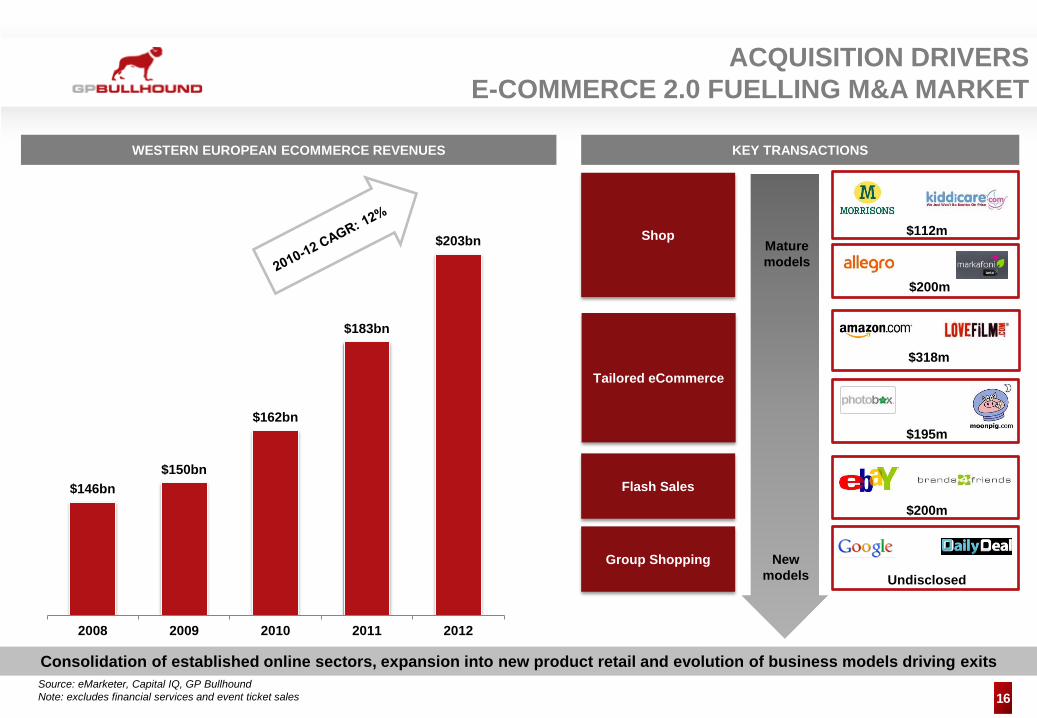

ACQUISITION DRIVERS E-COMMERCE 2.0 FUELLING M&A MARKET

$146bn $150bn

$162bn

$183bn

$203bn

2008 2009 2010 2011 2012

Consolidation of established online sectors, expansion into new product retail and evolution of business models driving exits

Flash Sales

New models

Mature models

Shop $112m

$200m

$318m

WESTERN EUROPEAN ECOMMERCE REVENUES

Source: eMarketer, Capital IQ, GP Bullhound Note: excludes financial services and event ticket sales

KEY TRANSACTIONS

Tailored eCommerce

$195m

$200m

Group Shopping Undisclosed

17

$639m

$826m

$1,025m

$1,213m

$1,372m

$1,526m

2009 2010 2011 2012 2013 2014

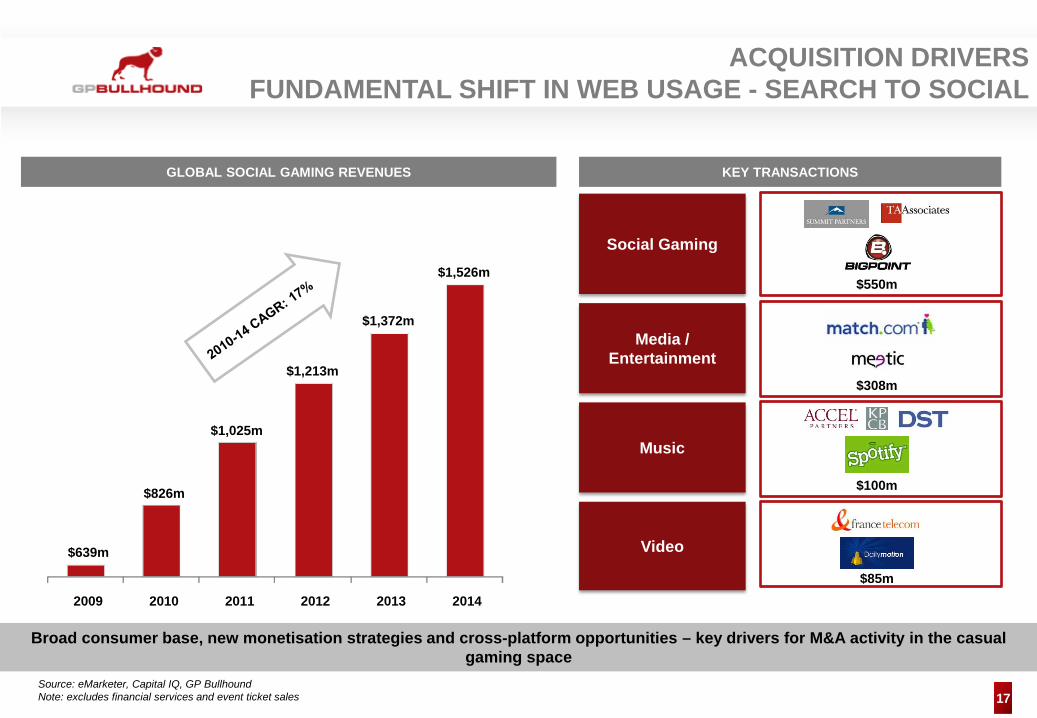

ACQUISITION DRIVERS FUNDAMENTAL SHIFT IN WEB USAGE - SEARCH TO SOCIAL

Media / Entertainment

Video

Social Gaming

$550m

Music

Source: eMarketer, Capital IQ, GP Bullhound Note: excludes financial services and event ticket sales

Broad consumer base, new monetisation strategies and cross-platform opportunities – key drivers for M&A activity in the casual gaming space

GLOBAL SOCIAL GAMING REVENUES KEY TRANSACTIONS

$308m

$100m

$85m

18

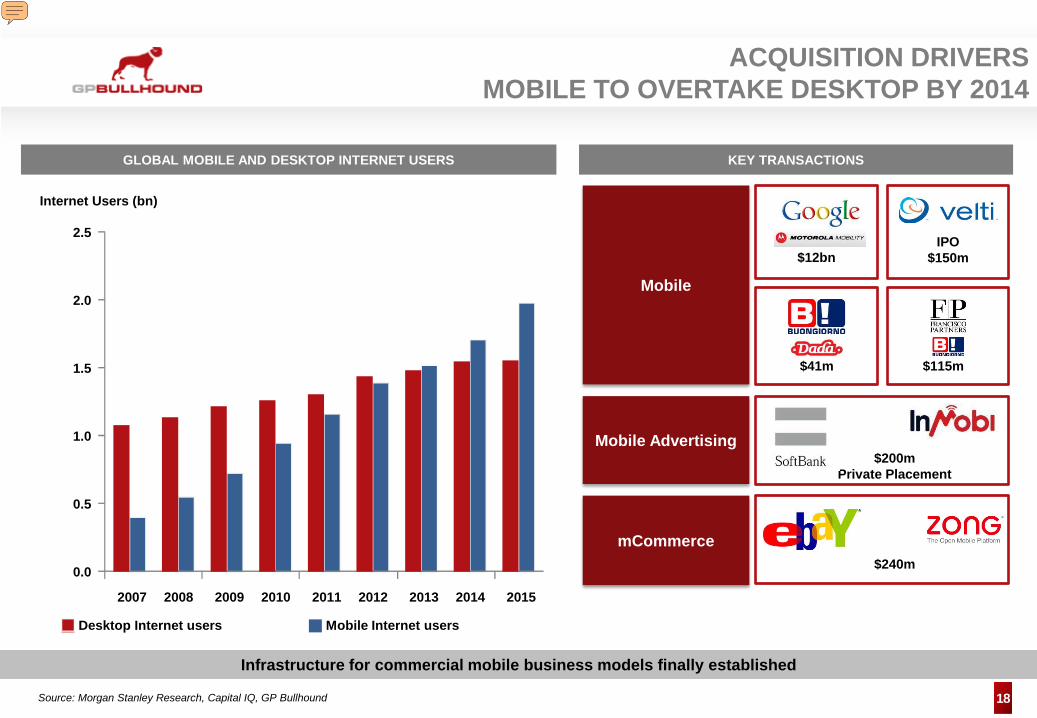

ACQUISITION DRIVERS MOBILE TO OVERTAKE DESKTOP BY 2014

mCommerce

Mobile

$240m

$41m $115m

$12bn

0.0

0.5

1.0

1.5

2.0

2.5

2007 2009 2011 2013 2015

Internet Users (bn)

Desktop Internet users Mobile Internet users

2008 2010 2012 2014

Source: Morgan Stanley Research, Capital IQ, GP Bullhound

Infrastructure for commercial mobile business models finally established

GLOBAL MOBILE AND DESKTOP INTERNET USERS KEY TRANSACTIONS

IPO $150m

Mobile Advertising $200m

Private Placement

Presenter

Presentation Notes

Future consolidation expected in mobile payments Landgrab / scale necessary to make model work mobile advertising (regional leaders will form – eg imimobile in Asia) Location based services – introduction of NFC

19 Source: Societe Generale, Capital IQ, GP Bullhound

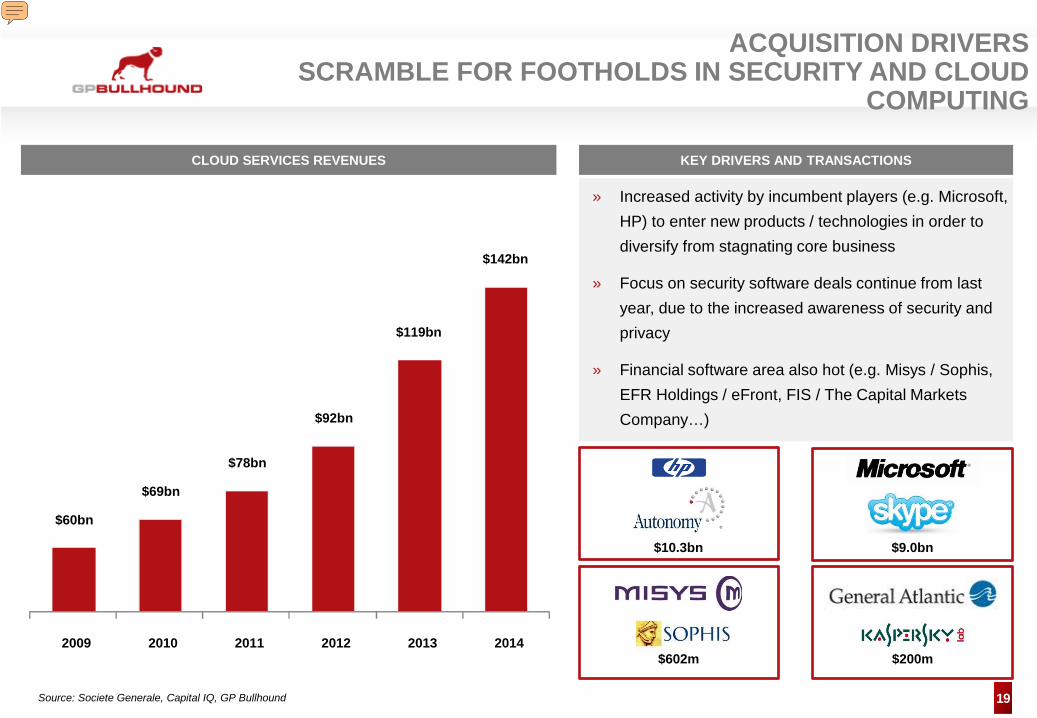

ACQUISITION DRIVERS SCRAMBLE FOR FOOTHOLDS IN SECURITY AND CLOUD

COMPUTING

$10.3bn

$602m $200m

» Increased activity by incumbent players (e.g. Microsoft, HP) to enter new products / technologies in order to diversify from stagnating core business

» Focus on security software deals continue from last year, due to the increased awareness of security and privacy

» Financial software area also hot (e.g. Misys / Sophis, EFR Holdings / eFront, FIS / The Capital Markets Company…)

CLOUD SERVICES REVENUES KEY DRIVERS AND TRANSACTIONS

$60bn

$69bn

$78bn

$92bn

$119bn

$142bn

2009 2010 2011 2012 2013 2014

$9.0bn

Presenter

Presentation Notes

SaaS attracting intense attention from PE players given efficient cash cycle and visibility on revenues

20 Source: Capital IQ, Company Information as of 30 September 2011

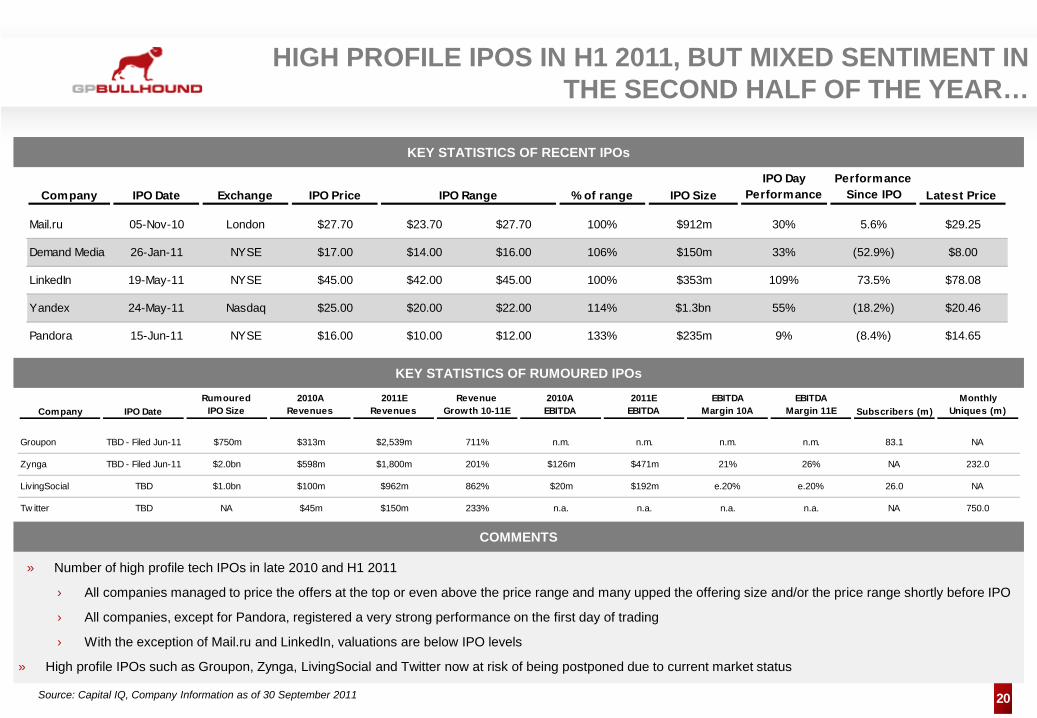

» Number of high profile tech IPOs in late 2010 and H1 2011

› All companies managed to price the offers at the top or even above the price range and many upped the offering size and/or the price range shortly before IPO

› All companies, except for Pandora, registered a very strong performance on the first day of trading

› With the exception of Mail.ru and LinkedIn, valuations are below IPO levels

» High profile IPOs such as Groupon, Zynga, LivingSocial and Twitter now at risk of being postponed due to current market status

KEY STATISTICS OF RECENT IPOs

HIGH PROFILE IPOS IN H1 2011, BUT MIXED SENTIMENT IN THE SECOND HALF OF THE YEAR…

COMMENTS

KEY STATISTICS OF RUMOURED IPOs

Company IPO Date Exchange IPO Price IPO Range % of range IPO SizeIPO Day

PerformancePerformance

Since IPO Latest Price

Mail.ru 05-Nov-10 London $27.70 $23.70 $27.70 100% $912m 30% 5.6% $29.25

Demand Media 26-Jan-11 NYSE $17.00 $14.00 $16.00 106% $150m 33% (52.9%) $8.00

LinkedIn 19-May-11 NYSE $45.00 $42.00 $45.00 100% $353m 109% 73.5% $78.08

Yandex 24-May-11 Nasdaq $25.00 $20.00 $22.00 114% $1.3bn 55% (18.2%) $20.46

Pandora 15-Jun-11 NYSE $16.00 $10.00 $12.00 133% $235m 9% (8.4%) $14.65

Company IPO DateRumoured

IPO Size2010A

Revenues 2011E

RevenuesRevenue

Growth 10-11E2010AEBITDA

2011EEBITDA

EBITDAMargin 10A

EBITDAMargin 11E Subscribers (m)

Monthly Uniques (m)

Groupon TBD - Filed Jun-11 $750m $313m $2,539m 711% n.m. n.m. n.m. n.m. 83.1 NA

Zynga TBD - Filed Jun-11 $2.0bn $598m $1,800m 201% $126m $471m 21% 26% NA 232.0

LivingSocial TBD $1.0bn $100m $962m 862% $20m $192m e.20% e.20% 26.0 NA

Tw itter TBD NA $45m $150m 233% n.a. n.a. n.a. n.a. NA 750.0

21

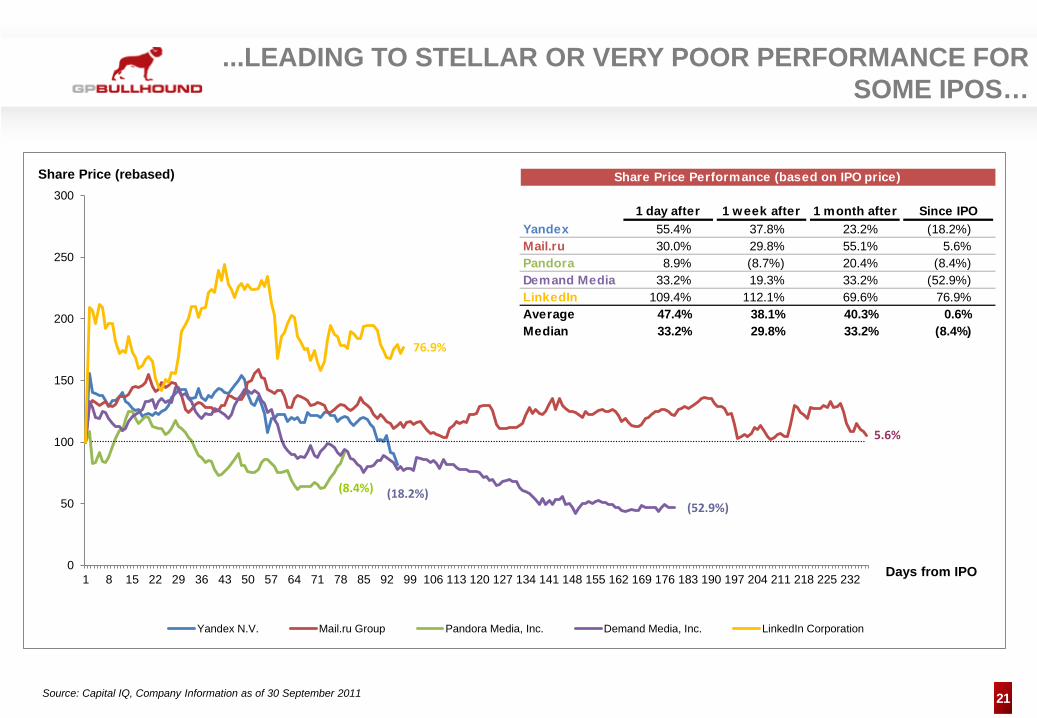

(18.2%)

5.6%

(8.4%)(52.9%)

76.9%

0

50

100

150

200

250

300

1 8 15 22 29 36 43 50 57 64 71 78 85 92 99 106 113 120 127 134 141 148 155 162 169 176 183 190 197 204 211 218 225 232

Yandex N.V. Mail.ru Group Pandora Media, Inc. Demand Media, Inc. LinkedIn Corporation

Days from IPO

Share Price (rebased)

...LEADING TO STELLAR OR VERY POOR PERFORMANCE FOR SOME IPOS…

Source: Capital IQ, Company Information as of 30 September 2011

Share Price Performance (based on IPO price)

0 1 day after 1 week after 1 month after Since IPOYandex 55.4% 37.8% 23.2% (18.2%)Mail.ru 30.0% 29.8% 55.1% 5.6%Pandora 8.9% (8.7%) 20.4% (8.4%)Demand Media 33.2% 19.3% 33.2% (52.9%)LinkedIn 109.4% 112.1% 69.6% 76.9%Average 47.4% 38.1% 40.3% 0.6%Median 33.2% 29.8% 33.2% (8.4%)

22

SO IN SUMMARY, IT COULD GO EITHER WAY

23

TABLE OF CONTENTS

1 GENERAL ECONOMIC ENVIRONMENT

2 M&A AND IPO MARKET

3 DIGITAL MEDIA TRENDS

24

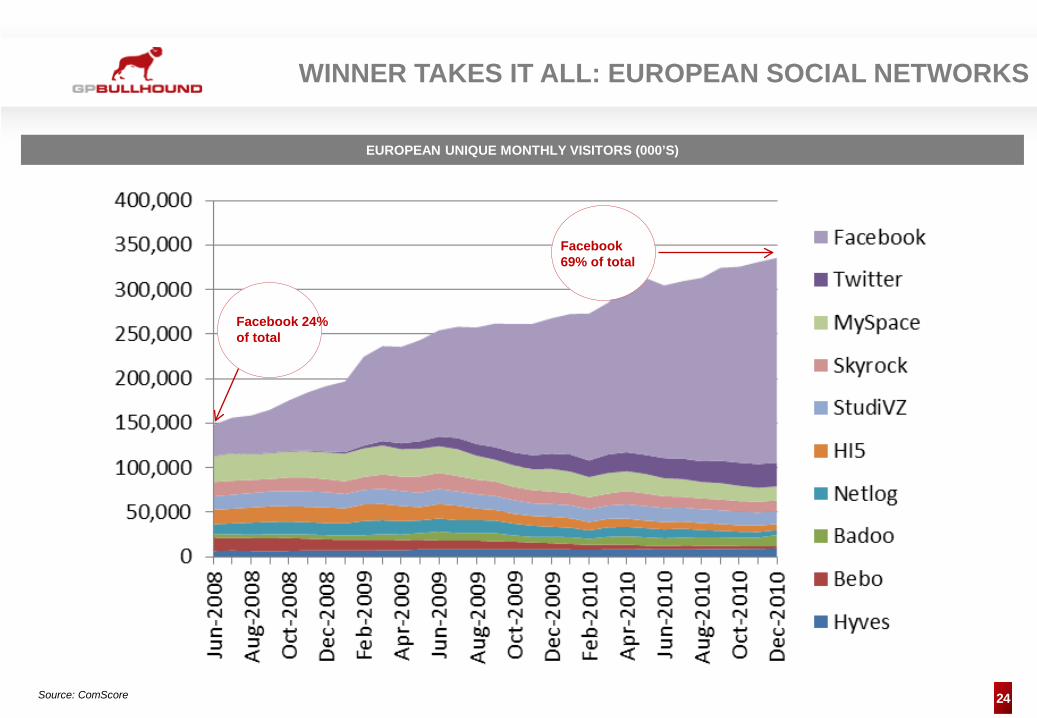

WINNER TAKES IT ALL: EUROPEAN SOCIAL NETWORKS

Source: ComScore

Facebook 24% of total

Facebook 69% of total

EUROPEAN UNIQUE MONTHLY VISITORS (000’S)

25

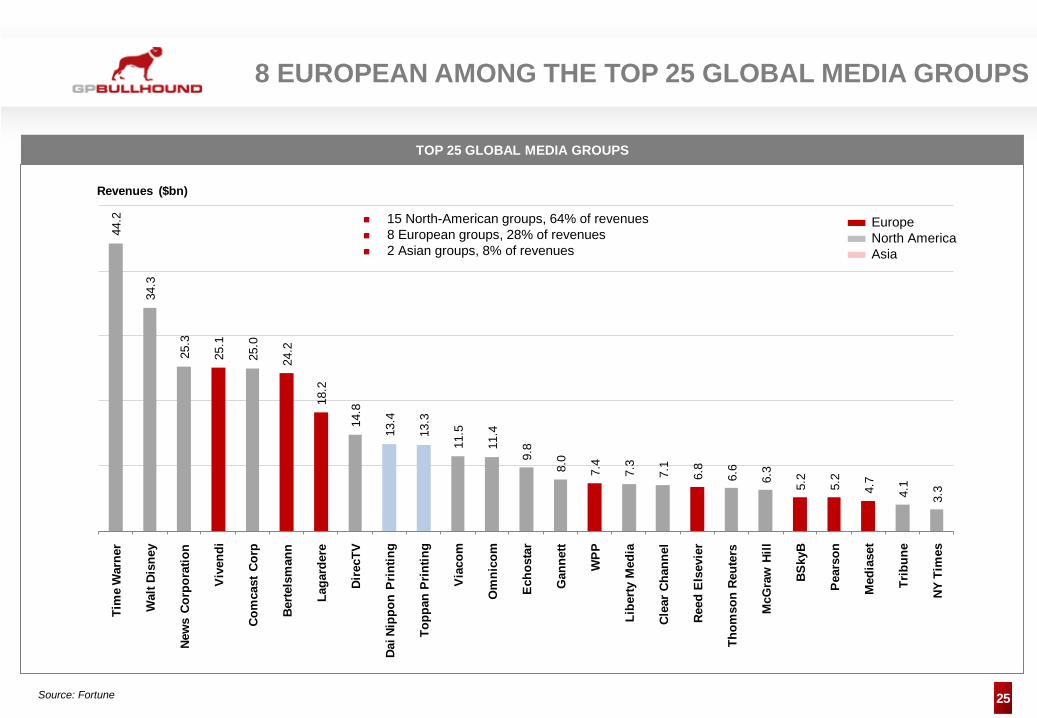

TOP 25 GLOBAL MEDIA GROUPS

8 EUROPEAN AMONG THE TOP 25 GLOBAL MEDIA GROUPS

Source: Fortune

44.2

34.3

25.3

25.1

25.0

24.2

18.2

14.8

13.4

13.3

11.5

11.4

9.8

8.0

7.4

7.3

7.1

6.8

6.6

6.3

5.2

5.2

4.7

4.1

3.3

Tim

e W

arne

r

Wal

t Dis

ney

New

s Co

rpor

atio

n

Vive

ndi

Com

cast

Cor

p

Berte

lsm

ann

Laga

rder

e

Dire

cTV

Dai N

ippo

n Pr

intin

g

Topp

an P

rintin

g

Viac

om

Om

nico

m

Echo

star

Gan

nett

WPP

Libe

rty M

edia

Clea

r Cha

nnel

Reed

Els

evie

r

Thom

son

Reut

ers

McG

raw

Hill

BSky

B

Pear

son

Med

iase

t

Trib

une

NY T

imes

Revenues ($bn)

Europe North America Asia

15 North-American groups, 64% of revenues 8 European groups, 28% of revenues 2 Asian groups, 8% of revenues

26

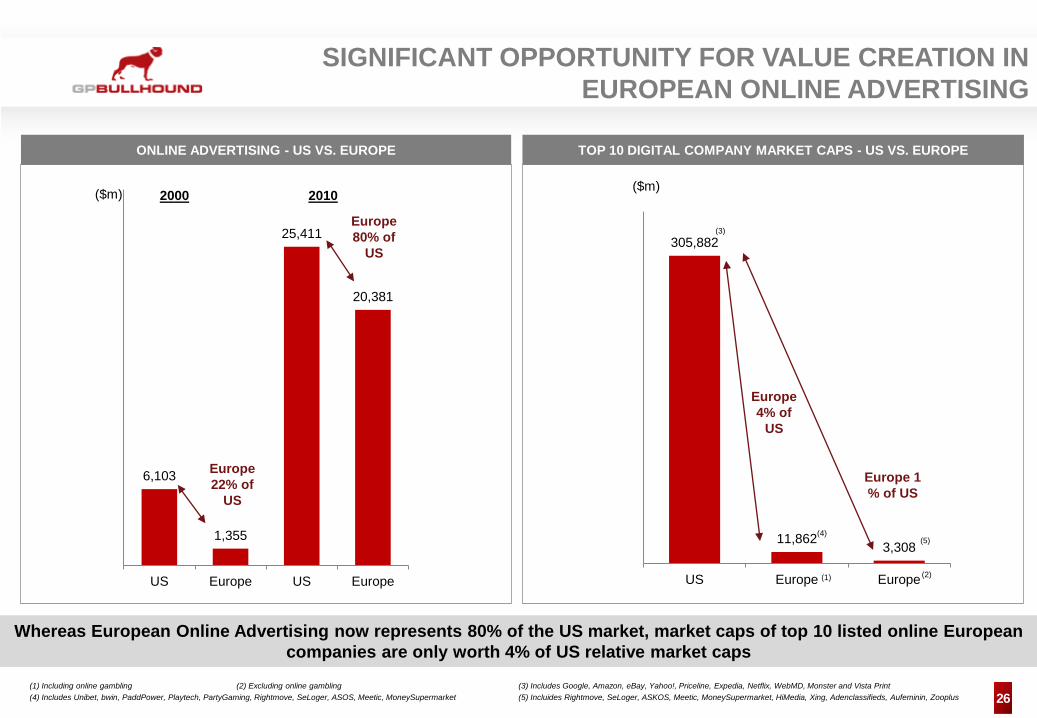

SIGNIFICANT OPPORTUNITY FOR VALUE CREATION IN EUROPEAN ONLINE ADVERTISING

TOP 10 DIGITAL COMPANY MARKET CAPS - US VS. EUROPE ONLINE ADVERTISING - US VS. EUROPE

(1) Including online gambling (2) Excluding online gambling (3) Includes Google, Amazon, eBay, Yahoo!, Priceline, Expedia, Netflix, WebMD, Monster and Vista Print (4) Includes Unibet, bwin, PaddPower, Playtech, PartyGaming, Rightmove, SeLoger, ASOS, Meetic, MoneySupermarket (5) Incluides Rightmove, SeLoger, ASKOS, Meetic, MoneySupermarket, HiMedia, Xing, Adenclassifieds, Aufeminin, Zooplus

6,103

1,355

25,411

20,381

US Europe US Europe

2000 2010 ($m)

Europe 22% of

US

Europe 80% of

US 305,882

11,862 3,308

US Europe Europe

Europe 4% of

US

Europe 1 % of US

($m)

(3)

(4) (5)

(1) (2)

Whereas European Online Advertising now represents 80% of the US market, market caps of top 10 listed online European companies are only worth 4% of US relative market caps

27

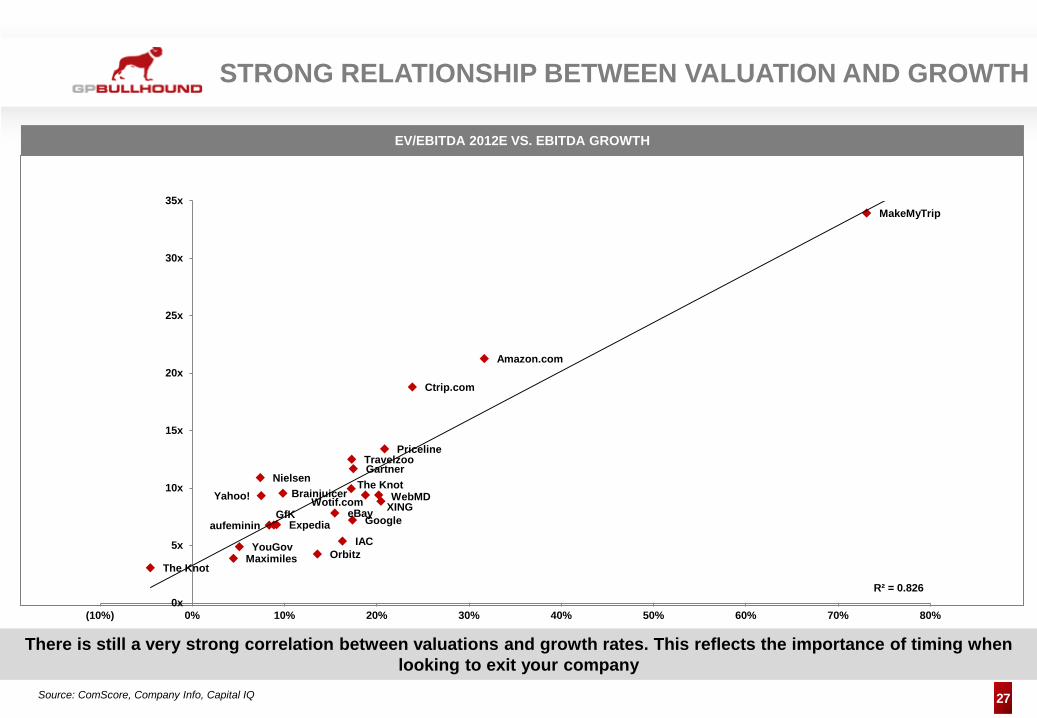

STRONG RELATIONSHIP BETWEEN VALUATION AND GROWTH

Source: ComScore, Company Info, Capital IQ

EV/EBITDA 2012E VS. EBITDA GROWTH

There is still a very strong correlation between valuations and growth rates. This reflects the importance of timing when looking to exit your company

aufemininXINGWebMD

The KnotMaximiles

The Knot

Expedia

Orbitz

PricelineTravelzoo

Ctrip.com

MakeMyTrip

Wotif.com

NielsenGartner

GfK

YouGov

Brainjuicer

Yahoo!

IAC

Amazon.com

eBay

R² = 0.8260x

5x

10x

15x

20x

25x

30x

35x

(10%) 0% 10% 20% 30% 40% 50% 60% 70% 80%

28

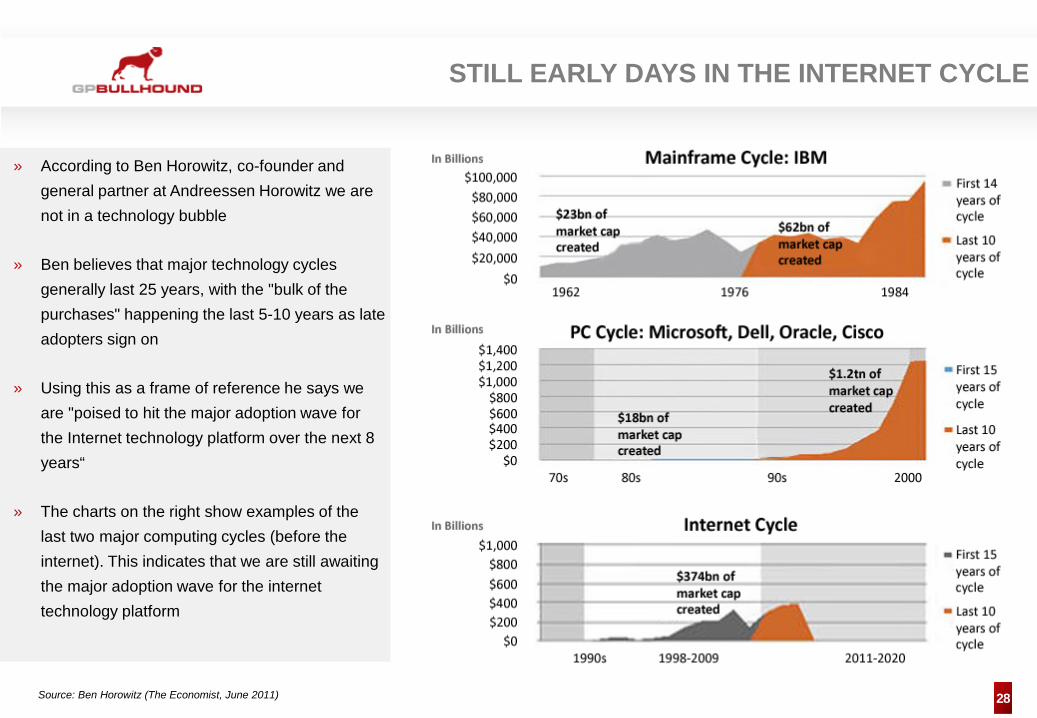

STILL EARLY DAYS IN THE INTERNET CYCLE

Source: Ben Horowitz (The Economist, June 2011)

» According to Ben Horowitz, co-founder and general partner at Andreessen Horowitz we are not in a technology bubble

» Ben believes that major technology cycles generally last 25 years, with the "bulk of the purchases" happening the last 5-10 years as late adopters sign on

» Using this as a frame of reference he says we are "poised to hit the major adoption wave for the Internet technology platform over the next 8 years“

» The charts on the right show examples of the last two major computing cycles (before the internet). This indicates that we are still awaiting the major adoption wave for the internet technology platform

29

Stockholm Birger Jarlsgatan 5 111 45 Stockholm +46 (0) 8 5450 7414

San Francisco One Maritime Plaza, Suite 1620 San Francisco, CA 94111 +1 (415) 986 0191

ANALYST PROFILES

GLOBAL PRESENCE & ACCESS

Julien Oussadon Vice President

Contact Details [email protected] Office: +44 207 101 7587

Background M&A at Arma Partners M&A at Soc Gen B.Sc from Boston University’s School of

Management

Alessandro Casartelli Analyst

Contact Details [email protected] Office: +44 207 101 7594

Background M&A at Bank of America Merrill Lynch M.Sc from Bocconi University / ESADE B.Sc from Bocconi University / University of

Texas

Manish Madhvani Co-Founder / Partner

Contact Details [email protected] Office: +44 207 101 7567

Background Co-founder of GP Bullhound M&A at Barclays Capital MA in Marketing and LLB in Law at

Southampton University

London 52 Jermyn Street London, SW1Y 6LX +44 (0) 20 7101 7560

30

SAN FRANCISCO OFFICE ONE MARITIME PLAZA, SUITE 1620, SAN +1(415) 986 7480

FAX +1(415) 986 0180 MEMBER OF FINRAFRANCISCO, CA 94111

TEL

HQ: LONDON OFFICE 52 JERMYN STREET, LONDON SW1Y 6LX TEL +44(0)207 101 7560 FAX +44(0)207 101 7561 AUTHORISED AND REGULATED BY THE FSA

SAN FRANCISCO OFFICE ONE MARITIME PLAZA, SUITE 1620 SAN FRANCISCO, CA 94111 TEL +1(415) 986 0191 FAX +1(415) 986 0180 MEMBER OF FINRA

HQ: LONDON OFFICE 52 JERMYN STREET, LONDON SW1Y 6LX TEL +44(0)207 101 7560 FAX +44(0)207 101 7561 AUTHORISED AND REGULATED BY THE FSA

STOCKHOLM OFFICE BIRGER JARLSGATAN 5 111 45 STOCKHOLM, SWEDEN TEL +46(0)8 545 074 14 FAX: +46(0)8 545 071 01

Disclaimer: Information contained in the document does not constitute an offer to buy or sell or the solicitation of any offer to buy or sell any securities. This document is made available for general information purposes only and is intended for professional investors who have a high degree of financial sophistication and knowledge. This document and any of the products and information contained herein are not intended for the use of retail investors in the UK or any other territory. Although all reasonable care has been taken to ensure that the information contained in this document is accurate and current, no representation or warranty, express or implied, is made by GP Bullhound LLP as to its accuracy, completeness and currency. This report contains forward-looking statements, which involve risks and uncertainties. Actual results may differ significantly from the results described in the forward-looking statements. In particular, but without limiting the preceding sentences, you should be aware that statements of fact or opinion made, may not be up-to-date or may not represent the current opinion (whether public or confidential) of GP Bullhound LLP. In addition, opinions and estimates are subject to change without notice. This report does not constitute a specific investment recommendation or advice upon which you should rely based upon, or irrespective of, your personal circumstances. Use of this document is not a substitute for obtaining proper investment advice from an authorized investment professional. Potential retail investors are urged to consult their own authorized investment professional before entering into any investment agreement. Past performance of securities is not necessarily a guide to future performance and the value of securities may fall as well as rise. In particular, investments in the technology sector can involve a high degree of risk and investors may not get back the full amount invested. GP Bullhound LLP is authorised and regulated by the Financial Services Authority in the United Kingdom and is registered in England No. OC352636 Registered office: GP Bullhound LLP, 52 Jermyn Street, London, SW1Y 6LX http://www.gpbullhound.com, [email protected], +44 20 7101 7560

![[Master Class Programmatic Trading May 2014] Keynote by Simon Nicholls Partner at GP Bullhound](https://static.fdocuments.in/doc/165x107/558e21031a28ab93398b4673/master-class-programmatic-trading-may-2014-keynote-by-simon-nicholls-partner-at-gp-bullhound.jpg)