Government of Karnataka - fpibangalore.gov.in · Government of Karnataka ... in the year 2003. FRBM...

52

i Government of Karnataka Report: IMPACT OF FISCAL RULES ON STATE FINANCES IN INDIA: A COMPARATIVE STUDY OF SOUTHERN STATES Center for Financial Accountability and Decentralization Fiscal Policy Institute Kengeri, Bengaluru-60 February, 2017

Transcript of Government of Karnataka - fpibangalore.gov.in · Government of Karnataka ... in the year 2003. FRBM...

i

Government of Karnataka

Report:

IMPACT OF FISCAL RULES ON STATE FINANCES IN INDIA: A COMPARATIVE

STUDY OF SOUTHERN STATES

Center for Financial Accountability and Decentralization

Fiscal Policy Institute

Kengeri, Bengaluru-60

February, 2017

ii

iii

TABLE OF CONTENTS

Abstract ii

Executive Summary iii

List of Chapters v

List of Tables vi

List of Illustrations vi

List of Appendices vi

List of Abbreviations vii

iv

Abstract:

Indian economy was under severe fiscal distress in the early and late 90s. Combined fiscal

deficit of Centre and State Governments has reached almost double digit in early 2000. In order

to overcome the fiscal distress, Government of India initiated rule based fiscal correction

mechanism and enacted Fiscal Responsibility & Budget Management Act in 2003. Following

the Central Government, many State Governments have enacted Fiscal Responsibility

Legislations (FRLs). This study examines and compares the FRLs across southern Indian States

namely Andhra Pradesh, Karnataka, Kerala and Tamil Nadu. FRLs have been amended by

State Governments several times in lieu of redefinition of fiscal deficit, implementation of 13th

Finance Commission recommendations and mostly in the name of stimulus package to

overcome the 2008 global financial crisis.

Trend analysis indicated that there is a clear improvement in fiscal health of all southern States.

However, how significant is this improvement forms an empirical question. This study using

structural break analysis finds that there is a significant change in fiscal indicators in the fiscal

reform period. Karnataka’s fiscal indicators have moved in the expected direction, i.e.

reduction in revenue expenditure and non-development expenditure and increase in

development expenditure. Contrary to the expectations, in Tamil Nadu and Kerala, deficits are

growing at a faster rate in reform period than earlier. Southern States except Karnataka, have

adhered to FRLs by cutting the capital outlay. This was clearly found in insignificant growth

of capital outlay in reform period as well as insignificant changes in non-development

expenditure. State Government should strictly follow laid down fiscal consolidation roadmap

by raising the tempo of capital outlay and minimizing the non-development expenditure.

Breaching fiscal consolidation path using unconventional amendments would result in

unsustainable deficits and debt.

v

Executive Summary

The combined fiscal deficit of Centre and States Governments reached almost double digits in

the early 2000s. Higher deficits and mounting debt in late 90s and early 2000s paved the way

for rule based fiscal correction mechanism in India. In order to overcome the fiscal distress,

Government of India initiated rule based fiscal correction mechanism and enacted the Fiscal

Responsibility & Budget Management Act in 2003. Following the Central Government, many

State Governments also enacted Fiscal Responsibility Legislations (FRLs). This study

examines and compares the FRLs across southern Indian States namely, Andhra Pradesh,

Karnataka, Kerala and Tamil Nadu. Higher deficits across southern States were mainly due to

implementation of pay revisions, huge subsidies, waiver of farm loans etc.

Karnataka was the first State to implement fiscal responsibility legislation followed by Tamil

Nadu, Kerala and Andhra Pradesh. Among the southern States, Karnataka has a unique and

distinguished position in the FRL. Its 17 Fiscal Management Principles cover several aspects

including inter-generational equity. There is only one limitation with Karnataka’s FRL which

is the lack of an independent external assessment body to review the compliance of the state

government to FRL.

State governments have amended FRLs several times to provide counter recession measures.

In the name of global financial crisis, all the southern States have postponed the target dates.

In addition to this, to accommodate new definition of fiscal deficit and to pursue

recommendations of Thirteenth Finance Commissions, state governments have amended the

FRLs. Between 2003-04 and 2014-15, Tamil Nadu Government have amended the FRL five

times.

Trend analysis indicates that there is change in trends and patterns of fiscal indicators after the

enactment of FRLs across southern states. All the southern states except Kerala have kept their

fiscal variables (as a percent of GSDP) well within the prescribed limit as per FRLs, particularly

for deficit indicators and liabilities. Even though, fiscal indicators as percent to GSDP are

within the limit, it is important to know and keep a check on its growth rate. To measure the

impact of FRL on fiscal variables (on its growth), time series econometrics, particularly dummy

variable method was used for the analysis. The result showed that there is some significant

variation in fiscal indicators, however it is state specific. For Andhra Pradesh, impact of FRL

on select fiscal indicators is not significant except for social service spending. For Karnataka,

which lead in formation, implementation of FRL is clearly denoted in its performance. Even

vi

though there was no significant change or reduction in growth of deficit indicators for

Karnataka, growth in other variables like interest payments, revenue expenditure, non-

development expenditure has significantly came down whereas growth in capital outlay,

development expenditure has gone up. However, Karnataka Government should be cautious

that its liabilities are growing at a much faster rate in the reform period than before and hence

require careful handling of the same.

Significant impact of FRL was also seen on Kerala State finances. Liabilities, interest payments

have declined whereas development expenditure and capital outlay has gone up significantly.

However, capital outlay has declined as a percent to GSDP in reform period. There are certain

similarities between Tamil Nadu and Kerala in fiscal performance during the reform period.

Contrary to expectations, deficits have increased in the reform era and capital outlay got

reduced. Karnataka is the only state in which non-development expenditure has declined

significantly, in other three States there was no significant change.

These results have several policy implications. Southern states except Karnataka were not able

to reduce non-developmental expenditure growth significantly after the reforms. Capital outlay

component was the most affected portion of expenditure. State could achieve the fiscal

consolidation targets due to better economic growth and consequent tax buoyancy in early

reform period, and also by cutting capital outlay. States must strictly adhere to existing fiscal

consolidation roadmap without amending it several times in order to achieve the laid down

targets. There must be some strict rule to limit these amendments several times by providing

unconventional reasons. Breaks in the laid road map would certainly result in unsustainable

deficits and debt in near future.

vii

List of Chapters

Chapter-1:

Economic Profile of Southern States 1 - 5

Chapter-2:

Trends and Patterns in Fiscal Indicators 6 - 12

Chapter-3:

Rule Based Fiscal Correction Mechanism 13 - 20

Chapter-4:

Impact of FRLs on Fiscal Indicators 21 - 29

Chapter-5:

Conclusion and Policy Implications 30 - 31

Bibliography 32 - 33

Appendix 34 - 43

viii

List of Tables

1.1 Real Per-Capita Income 03

1.2 Sectoral Composition of GSDP in Southern States 04

1.3 HDI Ranking of Southern States 05

2.1 Revenue Composition of Southern States 07

2.2 Expenditure Composition of Southern States 09

3.1 Incentive Fund Allocated & Released under FRF to Southern States 14

3.2 State-wise amount adjusted under DSS during 2002-03 to 2004-05 15

3.3 Debt Relief & Interest Relief under DCRF 16

3.4 Fiscal Indicators: Numerical ceilings & Achievement 18

4.1 Fiscal Indicators in Pre-FRL and FRL Period (% of GSDP) 21

4.2 Structural Break Analysis Result (Fiscal deficit & Revenue Deficit) 24

4.3 Structural Break Analysis Result (Liabilities & Interest Payments) 26

4.4 Structural Break Analysis Result (Own Tax Revenue) 26

4.5 Structural Break Analysis Result (Rev Exp & Cap Outlay) 27

4.6 Structural Break Analysis Result (Dev Exp & Non-Dev Exp) 28

4.7 Structural Break Analysis Result (Soc Ser Exp & Eco Ser Exp) 29

List of Illustrations

1.1 Real GSDP Growth of Southern States 02

2.1 Fiscal Deficit of Southern States 10

2.2 Revenue Deficits of Southern States 11

2.3 Liabilities of Southern States 12

List of Appendices

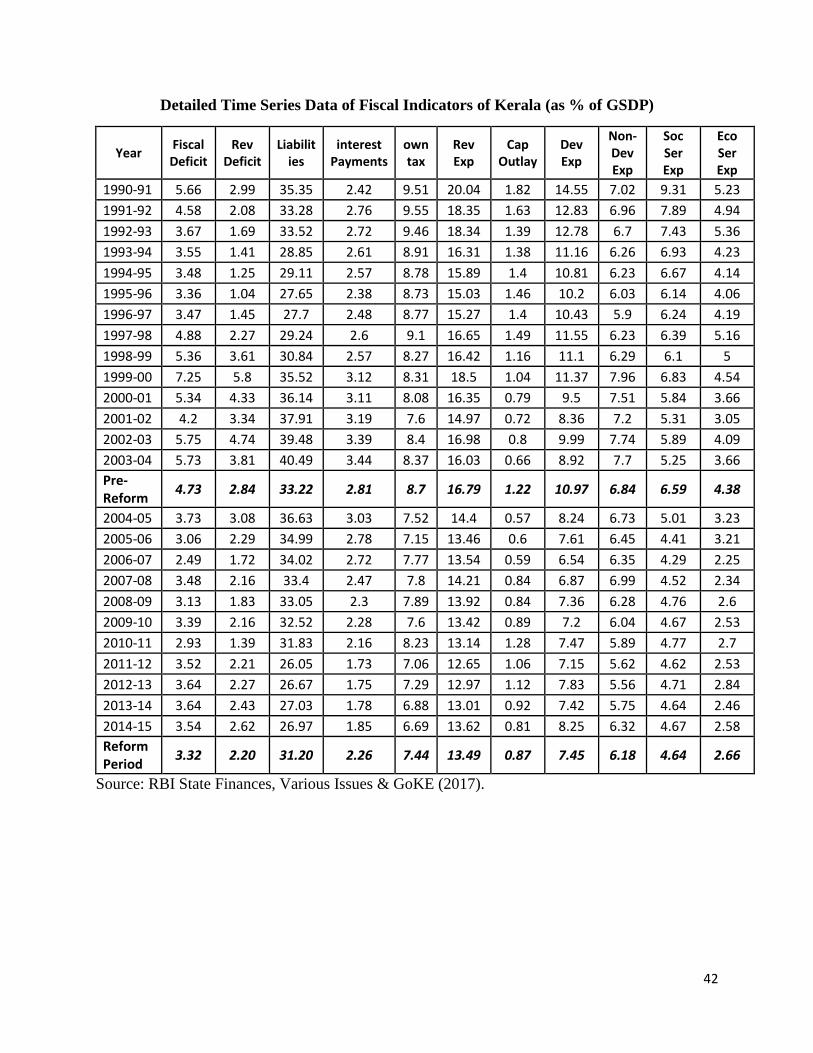

1. Fiscal Responsibility Legislations of Southern States: a detailed view 34-39

2. Detailed Time Series data of Fiscal Indicators 40-43

ix

List of Abbreviations

APFRBMA: Andhra Pradesh Fiscal Responsibility & Budget Management Act

BoP: Balance of Payments

FRA: Fiscal Responsibility Act

FRBM: Fiscal Responsibility and Budget Management

FRF: Fiscal Reforms Facility

FRL: Fiscal Responsibility Legislation

GDP: Gross Domestic Product

GSDP: Gross State Domestic Product

HDI: Human Development Index

HPEC: High-Powered Expert Committee

KCGGA: Karnataka Ceiling on Government Guarantee Act

KeFRA: Kerala Fiscal responsibility Act

KFRA: Karnataka Fiscal Responsibility Act

MTFP: Medium Term Fiscal Plan

MTFRP: Medium Term Fiscal Reforms Program

NIPFP: National Institute of Public Finance and Policy

PCI: Per Capita Income

TNFRA: Tamil Nadu Fiscal Responsibility Act

UNDP: United Nations Development Program

1

Impact of Fiscal Rules on State Finances in India: A Comparative Study of

Southern States

Excessive fiscal deficits are one of the major macroeconomic problems facing by Indian economy.

This problem was intensified in 1990s and early 2000s. Combined fiscal deficit of Centre and State

Governments crossed 9% of GDP in the year 2001-02. In order to control the excessive deficits,

Central Government initiated rule based fiscal correction mechanism by enacting Fiscal

Responsibility and Budget Management Act (FRBM Act) in the year 2003. FRBM Act specifies

certain numerical limits or targets to be achieved by the Government. As per which Government

has to limit the fiscal deficit to 3% of GDP and revenue deficit to be nil.

Many Indian States, in late 1990s, faced the problem of huge fiscal deficits and growing stock of

debt. As per the recommendations of the 12th Finance Commission, many of the State

Governments have enacted Fiscal Responsibility Legislations in the last decade. This report

analyses whether there is a significant change in the fiscal indicators after the commencement of

FRLs in Southern States, namely Andhra Pradesh, Karnataka, Kerala & Tamil Nadu. Southern

Indian States have been considered for the analysis as they are comparable in terms of per capita

income level and GSDP growth (these States have been classified as middle income States).

Report contains five chapters. First chapter provides a profile of Southern States in terms of GSDP

growth and composition, per capita income and other economic indicators. Second chapter

discusses trends and patterns in fiscal indicators of Southern States. In the third chapter a detailed

note on Fiscal Responsibility Legislations are provided. It also includes reasons for amendments

of the FRLs by time and forth. Fourth Chapter analyses impact of the fiscal consolidation

legislations on State finances by using time series econometric technique. Last chapter provides

conclusion to the report along with certain policy implications.

2

Chapter-1

Economic Profile of Southern States

Southern States have experienced modest growth on an average over the last two and half decade.

GSDP growth of Andhra Pradesh and Kerala between 1990-91 and 2014-15 were 6.4% and 6.7%

respectively, whereas for Karnataka and Tamil Nadu it was 7%. Figure-1.1 provides trends in real

GSDP growth of Southern States from 1990-91 to 2014-15.

Figure-1.1

Real GSDP Growth of Southern States (in %)

Data Source: RBI State Finances: A Study of Budget, Various Issues

The Indian economy faced severe crisis in terms of low growth, high inflation, worsening Balance

of Payments (BoP) situation etc in early 90s, where impact was reflected on State’s growth too. In

early 90s, GSDP growth of all the four States was just around 3%. With the introduction of major

structural reforms, India’s GDP and also States GSDP started moving upwards. Southern States

have achieved growth of 8% in the year 1993-94. However, in the corresponding years, there was

a decline in the GSDP growth owing to setback in agricultural production due to unfavorable

monsoons and widespread recessionary trend in industrial production in Karnataka (GoK, 1994).

The situation further worsened in late 1990s once again due to bad monsoons and consequent high

food inflation in Karnataka (GoK, 1999).

-4

-2

0

2

4

6

8

10

12

14

16

18

IN %

YEARAndhra Pradesh Karnataka Kerala Tamil Nadu

3

However, economic situation improved for the Southern States in 2001-02, particularly for

Karnataka with timely and wide spread monsoons and low inflation level and this trend continued

till 2006-07 (GoK, 2007). With the onset of global financial crisis in the year 2008, Indian

economy as a whole saw a drastic decline in output growth and same was reflected in terms of low

GSDP growth in the year 2008-09 and 2009-10 for the Southern States. Many of the State

Governments took steps to overcome the crisis by announcing stimulus packages for revival of

economic activities and its impact was reflected in reasonable output growth.

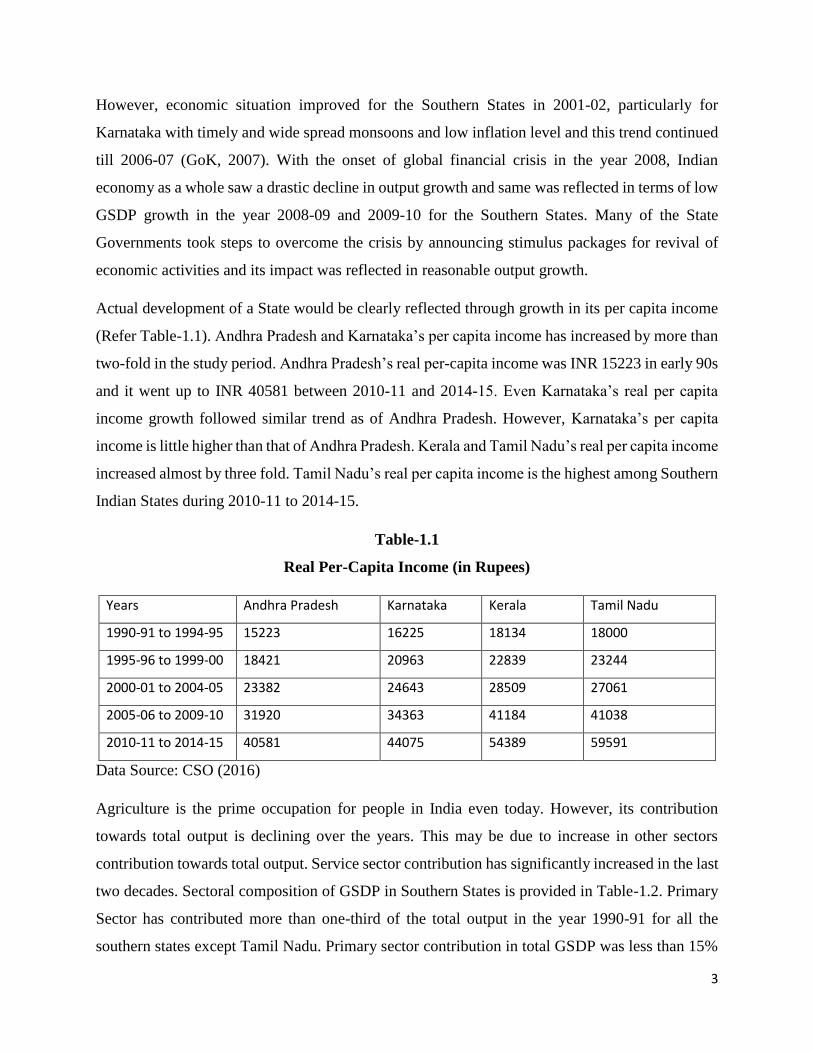

Actual development of a State would be clearly reflected through growth in its per capita income

(Refer Table-1.1). Andhra Pradesh and Karnataka’s per capita income has increased by more than

two-fold in the study period. Andhra Pradesh’s real per-capita income was INR 15223 in early 90s

and it went up to INR 40581 between 2010-11 and 2014-15. Even Karnataka’s real per capita

income growth followed similar trend as of Andhra Pradesh. However, Karnataka’s per capita

income is little higher than that of Andhra Pradesh. Kerala and Tamil Nadu’s real per capita income

increased almost by three fold. Tamil Nadu’s real per capita income is the highest among Southern

Indian States during 2010-11 to 2014-15.

Table-1.1

Real Per-Capita Income (in Rupees)

Years Andhra Pradesh Karnataka Kerala Tamil Nadu

1990-91 to 1994-95 15223 16225 18134 18000

1995-96 to 1999-00 18421 20963 22839 23244

2000-01 to 2004-05 23382 24643 28509 27061

2005-06 to 2009-10 31920 34363 41184 41038

2010-11 to 2014-15 40581 44075 54389 59591

Data Source: CSO (2016)

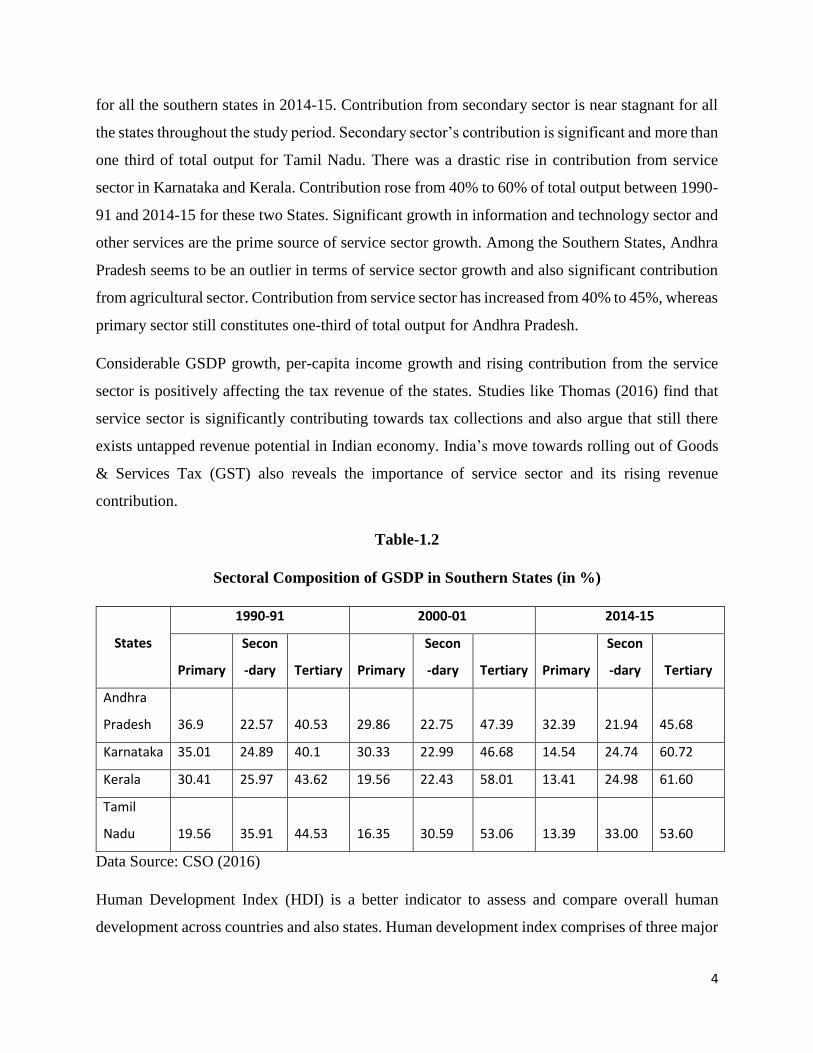

Agriculture is the prime occupation for people in India even today. However, its contribution

towards total output is declining over the years. This may be due to increase in other sectors

contribution towards total output. Service sector contribution has significantly increased in the last

two decades. Sectoral composition of GSDP in Southern States is provided in Table-1.2. Primary

Sector has contributed more than one-third of the total output in the year 1990-91 for all the

southern states except Tamil Nadu. Primary sector contribution in total GSDP was less than 15%

4

for all the southern states in 2014-15. Contribution from secondary sector is near stagnant for all

the states throughout the study period. Secondary sector’s contribution is significant and more than

one third of total output for Tamil Nadu. There was a drastic rise in contribution from service

sector in Karnataka and Kerala. Contribution rose from 40% to 60% of total output between 1990-

91 and 2014-15 for these two States. Significant growth in information and technology sector and

other services are the prime source of service sector growth. Among the Southern States, Andhra

Pradesh seems to be an outlier in terms of service sector growth and also significant contribution

from agricultural sector. Contribution from service sector has increased from 40% to 45%, whereas

primary sector still constitutes one-third of total output for Andhra Pradesh.

Considerable GSDP growth, per-capita income growth and rising contribution from the service

sector is positively affecting the tax revenue of the states. Studies like Thomas (2016) find that

service sector is significantly contributing towards tax collections and also argue that still there

exists untapped revenue potential in Indian economy. India’s move towards rolling out of Goods

& Services Tax (GST) also reveals the importance of service sector and its rising revenue

contribution.

Table-1.2

Sectoral Composition of GSDP in Southern States (in %)

States

1990-91 2000-01 2014-15

Primary

Secon

-dary Tertiary Primary

Secon

-dary Tertiary Primary

Secon

-dary Tertiary

Andhra

Pradesh 36.9 22.57 40.53 29.86 22.75 47.39 32.39 21.94 45.68

Karnataka 35.01 24.89 40.1 30.33 22.99 46.68 14.54 24.74 60.72

Kerala 30.41 25.97 43.62 19.56 22.43 58.01 13.41 24.98 61.60

Tamil

Nadu 19.56 35.91 44.53 16.35 30.59 53.06 13.39 33.00 53.60

Data Source: CSO (2016)

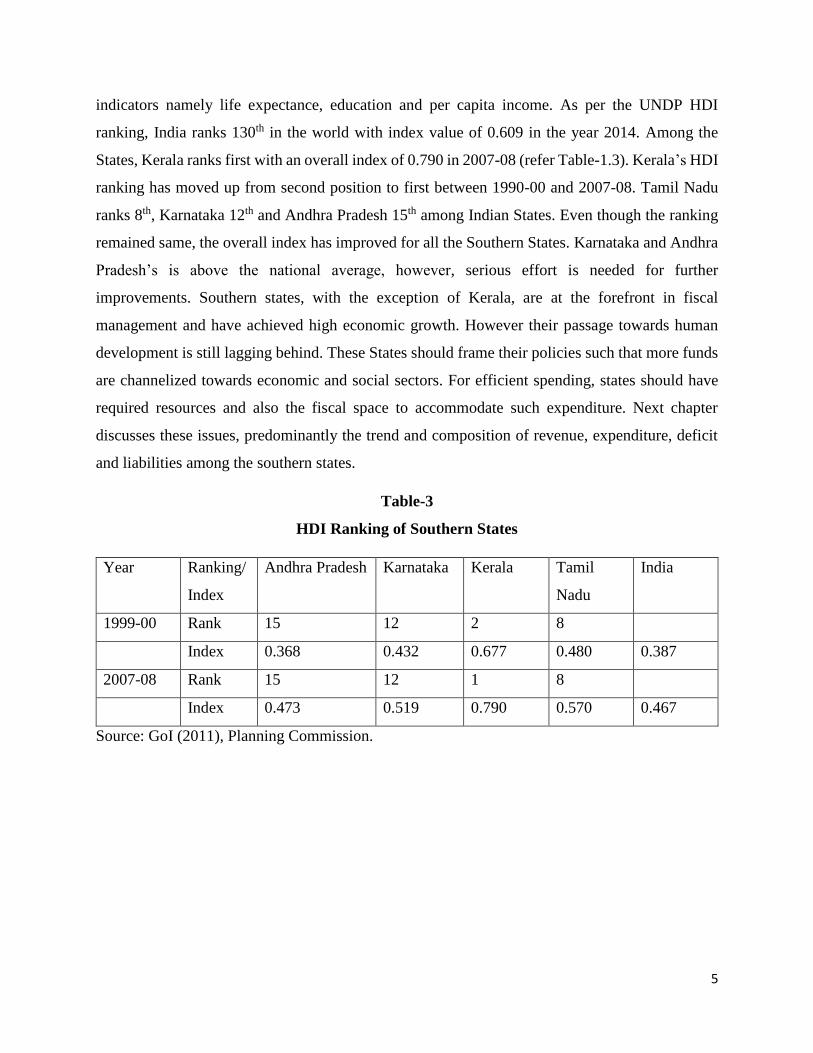

Human Development Index (HDI) is a better indicator to assess and compare overall human

development across countries and also states. Human development index comprises of three major

5

indicators namely life expectance, education and per capita income. As per the UNDP HDI

ranking, India ranks 130th in the world with index value of 0.609 in the year 2014. Among the

States, Kerala ranks first with an overall index of 0.790 in 2007-08 (refer Table-1.3). Kerala’s HDI

ranking has moved up from second position to first between 1990-00 and 2007-08. Tamil Nadu

ranks 8th, Karnataka 12th and Andhra Pradesh 15th among Indian States. Even though the ranking

remained same, the overall index has improved for all the Southern States. Karnataka and Andhra

Pradesh’s is above the national average, however, serious effort is needed for further

improvements. Southern states, with the exception of Kerala, are at the forefront in fiscal

management and have achieved high economic growth. However their passage towards human

development is still lagging behind. These States should frame their policies such that more funds

are channelized towards economic and social sectors. For efficient spending, states should have

required resources and also the fiscal space to accommodate such expenditure. Next chapter

discusses these issues, predominantly the trend and composition of revenue, expenditure, deficit

and liabilities among the southern states.

Table-3

HDI Ranking of Southern States

Year Ranking/

Index

Andhra Pradesh Karnataka Kerala Tamil

Nadu

India

1999-00 Rank 15 12 2 8

Index 0.368 0.432 0.677 0.480 0.387

2007-08 Rank 15 12 1 8

Index 0.473 0.519 0.790 0.570 0.467

Source: GoI (2011), Planning Commission.

6

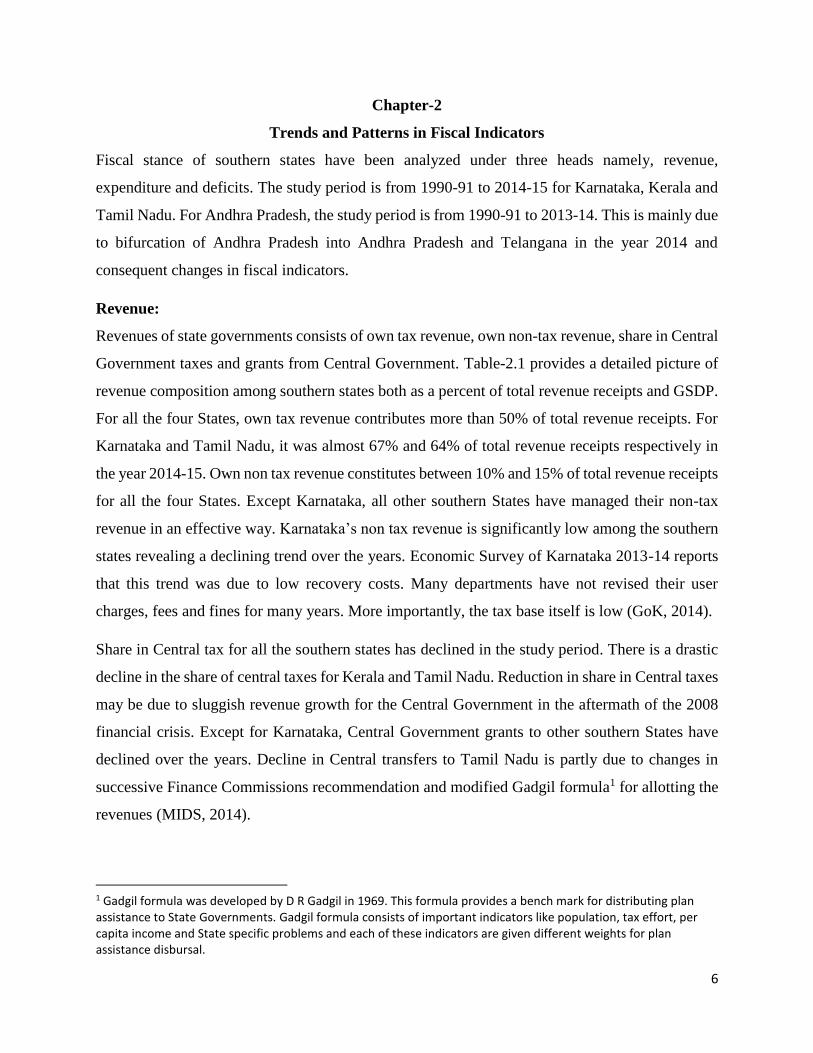

Chapter-2

Trends and Patterns in Fiscal Indicators

Fiscal stance of southern states have been analyzed under three heads namely, revenue,

expenditure and deficits. The study period is from 1990-91 to 2014-15 for Karnataka, Kerala and

Tamil Nadu. For Andhra Pradesh, the study period is from 1990-91 to 2013-14. This is mainly due

to bifurcation of Andhra Pradesh into Andhra Pradesh and Telangana in the year 2014 and

consequent changes in fiscal indicators.

Revenue:

Revenues of state governments consists of own tax revenue, own non-tax revenue, share in Central

Government taxes and grants from Central Government. Table-2.1 provides a detailed picture of

revenue composition among southern states both as a percent of total revenue receipts and GSDP.

For all the four States, own tax revenue contributes more than 50% of total revenue receipts. For

Karnataka and Tamil Nadu, it was almost 67% and 64% of total revenue receipts respectively in

the year 2014-15. Own non tax revenue constitutes between 10% and 15% of total revenue receipts

for all the four States. Except Karnataka, all other southern States have managed their non-tax

revenue in an effective way. Karnataka’s non tax revenue is significantly low among the southern

states revealing a declining trend over the years. Economic Survey of Karnataka 2013-14 reports

that this trend was due to low recovery costs. Many departments have not revised their user

charges, fees and fines for many years. More importantly, the tax base itself is low (GoK, 2014).

Share in Central tax for all the southern states has declined in the study period. There is a drastic

decline in the share of central taxes for Kerala and Tamil Nadu. Reduction in share in Central taxes

may be due to sluggish revenue growth for the Central Government in the aftermath of the 2008

financial crisis. Except for Karnataka, Central Government grants to other southern States have

declined over the years. Decline in Central transfers to Tamil Nadu is partly due to changes in

successive Finance Commissions recommendation and modified Gadgil formula1 for allotting the

revenues (MIDS, 2014).

1 Gadgil formula was developed by D R Gadgil in 1969. This formula provides a bench mark for distributing plan assistance to State Governments. Gadgil formula consists of important indicators like population, tax effort, per capita income and State specific problems and each of these indicators are given different weights for plan assistance disbursal.

7

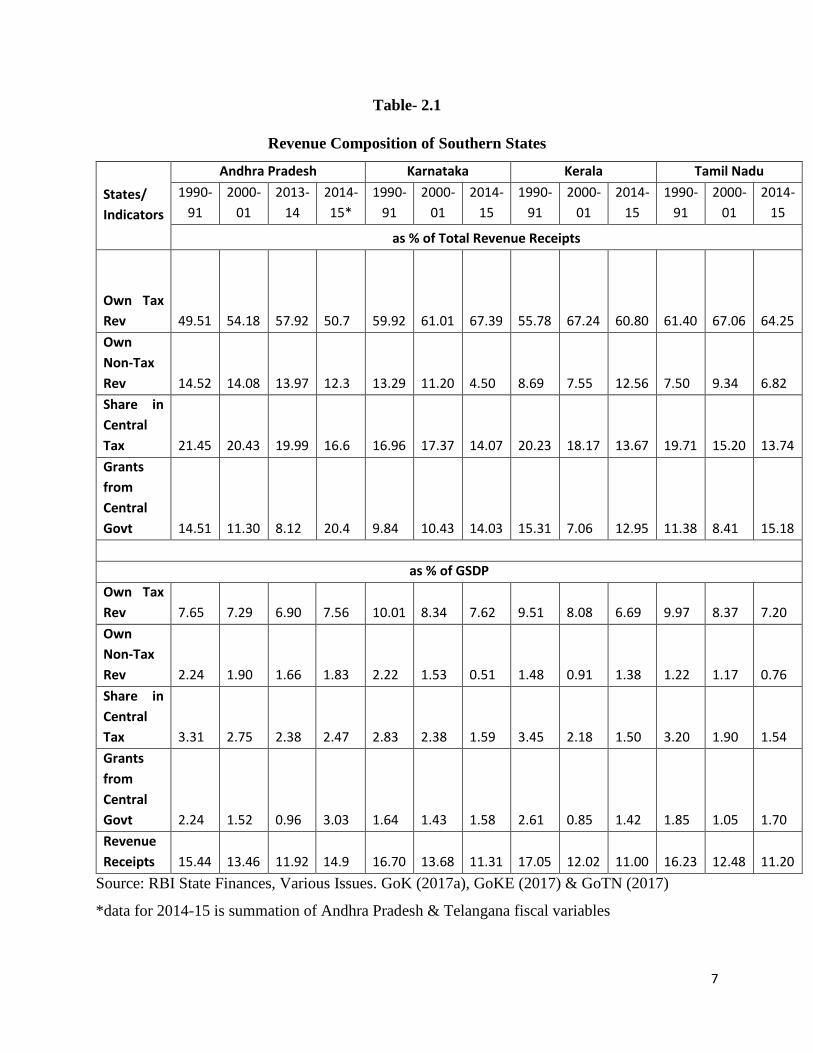

Table- 2.1

Revenue Composition of Southern States

States/

Indicators

Andhra Pradesh Karnataka Kerala Tamil Nadu

1990-

91

2000-

01

2013-

14

2014-

15*

1990-

91

2000-

01

2014-

15

1990-

91

2000-

01

2014-

15

1990-

91

2000-

01

2014-

15

as % of Total Revenue Receipts

Own Tax

Rev 49.51 54.18 57.92 50.7 59.92 61.01

67.39 55.78 67.24 60.80 61.40 67.06 64.25

Own

Non-Tax

Rev 14.52 14.08 13.97 12.3 13.29 11.20 4.50 8.69 7.55 12.56 7.50 9.34 6.82

Share in

Central

Tax 21.45 20.43 19.99 16.6 16.96 17.37 14.07 20.23 18.17 13.67 19.71 15.20 13.74

Grants

from

Central

Govt 14.51 11.30 8.12 20.4 9.84 10.43 14.03 15.31 7.06 12.95 11.38 8.41 15.18

as % of GSDP

Own Tax

Rev 7.65 7.29 6.90 7.56 10.01 8.34 7.62 9.51 8.08 6.69 9.97 8.37 7.20

Own

Non-Tax

Rev 2.24 1.90 1.66 1.83 2.22 1.53 0.51 1.48 0.91 1.38 1.22 1.17 0.76

Share in

Central

Tax 3.31 2.75 2.38 2.47 2.83 2.38 1.59 3.45 2.18 1.50 3.20 1.90 1.54

Grants

from

Central

Govt 2.24 1.52 0.96 3.03 1.64 1.43 1.58 2.61 0.85 1.42 1.85 1.05 1.70

Revenue

Receipts 15.44 13.46 11.92 14.9 16.70 13.68 11.31 17.05 12.02 11.00 16.23 12.48 11.20

Source: RBI State Finances, Various Issues. GoK (2017a), GoKE (2017) & GoTN (2017)

*data for 2014-15 is summation of Andhra Pradesh & Telangana fiscal variables

8

Karnataka stands first in own tax revenue collection with 7.62% of GSDP in the year 2014-15. It

also assumes first place in overall revenue receipts amounting 11.31% of GSDP in 2014-152. Tax-

GSDP ratio is the best indicator of tax efforts of any Government. This achievement is mainly due

to better tax efforts3 of Karnataka Government when compared to other States. A study on State

Finances of Karnataka (ISEC, 2014) reveals that Karnataka stands first among 14 major Indian

States in the tax efforts pertaining to excise duty, motor vehicle tax and occupies second place in

sales tax collection for the year 2010-11. Increase in central grants to states in 2014-15 was mainly

due to increase in central assistance to state plans following a move to restructure ‘Centrally

Sponsored Schemes’ and reduce their number from 126 to 66. Because of this restructuring, grants

flow from center to states has increased in the year 2014-15 (Mukherjee, 2014).

Expenditure:

Government Expenditure in practice is being classified under three different heads, namely

1. Revenue expenditure and capital expenditure

2. Plan Expenditure and Non-plan Expenditure

3. Development Expenditure and Non-Development expenditure

An expert committee on Efficient Management of Public Expenditure, constituted by Planning

Commission, India, has recommended to follow revenue expenditure and capital expenditure

classification and do away with plan and non-plan classification (GoI, 2011a). Expert committee

observed that over a period of time several issues have cropped up with regard to distinction

between plan and non-plan expenditure and are becoming an obstacle in outcome based budgeting

and hence, this classification has to be removed.

Following on going practice with regard to expenditure classifications, present study concentrates

on revenue and capital expenditure and also on development and non-development expenditure

classifications. In the capital expenditure, capital outlay component is considered as it implies

actual capital formation in the economy. Spending on interest payments was also tracked as it is

one of the major items of government committed expenditures.

2 Andhra Pradesh own-tax revenue-GSDP ratio was 11.9% in 2013-14. 3 Tax effort is the ratio of actual tax revenue of a Government to its taxable capacity.

9

Table-2.2 provides expenditure composition of southern states under two broad heads, namely

revenue expenditure & capital outlay and development & non-development expenditure. Revenue

expenditure as a percent of GSDP has declined for all the southern states (refer Table-2.2). This

reduction is highest for Kerala and Tamil Nadu with almost 5% to 6% of GSDP. This may be due

to strict fiscal consolidation roadmap. Capital outlay has increased marginally for all the southern

states except Kerala where it actually declined for the year 2014-15 when compared to early 2000s.

However, Karnataka has the highest capital outlay to GSDP ratio when compared to other southern

states. This implies that Karnataka has followed a better fiscal consolidation roadmap without

cutting down the capital outlay component of the expenditure. The development and non-

development expenditure has declined for all the southern states. The decline in development

expenditure is highest for Kerala. Interest payments, which is one of the major component in total

expenditure has declined significantly. This scenario is mostly due to fiscal correction mechanisms

adopted by the state governments, where they cap debt and deficits.

Table-2.2

Expenditure Composition of Southern States (as % of GSDP)

States/

Indicators

Andhra Pradesh Karnataka Kerala Tamil Nadu

1990-

91

2000-

01

2013-

14

2014-

15*

1990-

91

2000-

01

2014-

15

1990-

91

2000-

01

2014-

15

1990-

91

2000-

01

2014-

15

Rev Exp 15.9 15.9 11.9 17.4 17.0 15.4 11.3 20.0 16.4 13.6 18.0 14.8 11.8

Cap

Outlay 1.33 1.88 1.64 2.08 2.81 1.80 2.13 1.82 0.79 0.80 0.71 1.05 1.63

Dev Exp 12.7 11.8 9.85 15.1 14.3 11.5 9.66 14.6 9.50 8.24 13.7 9.41 9.90

Non-Dev

Exp 4.37 5.90 4.05 4.6 5.04 5.20 4.05 7.02 7.51 6.32 4.64 5.69 3.91

Interest

payments 1.70 2.62 1.39 1.6 1.87 2.20 1.02 2.42 3.11 1.85 1.45 2.13 1.43

Source: RBI State Finances, Various Issues. GoK (2017a), GoKE (2017) & GoTN (2017)

*data for 2014-15 is summation of Andhra Pradesh & Telangana fiscal variables

10

Deficits and Liabilities:

Developing nations need to spend more to achieve higher rate of economic growth. However, they

have hard budget constraints to finance the required amount. Excess spending over the revenues

leads to deficit and higher deficit results in accumulation of debt. Fiscal deficit is one of the major

macroeconomic issues facing by many States and also the Central Government in India. Fiscal

deficit is the difference between total expenditure (both revenue expenditure and capital

expenditure) and revenue receipts and non-debt capital receipts.

Fiscal deficit level for southern states, particularly for Kerala in early 90s was under alarming

situation (refer Figure-2.1). After the 1991 economic reforms, there was a reduction in fiscal

deficits for these states. However, in late 90s and early 2000s, it increased drastically. Once again

for Kerala fiscal deficit stood at 7.25% of GSDP in 1999-00. Deficit indicators started deteriorating

for Karnataka in 1997-98 and this trend continued for next three years. This trend was due to

constant own tax revenue and marginal decline in non-tax revenues as well as Central Government

transfers (Rao & Chakraborty, 2006). Stagnant revenue efforts in Karnataka, in late 90s was due

to insufficient tax efforts and erosion of tax base due to granting of tax exemptions to industries

(GoK, 2005). While the resource saw stagnation, expenditure saw a steep increase. The extension

of certain recommendations of 5th Pay Commission to Karnataka State Government employees

caused severe strain on available resources. The increase in expenditure especially on salaries,

pensions and interest payments imposed serious pressure on State Finances (GoK, 2005).

Figure-2.1

Fiscal Deficit of Southern States (% of GSDP)

Source: RBI State Finances, Various Issues. GoK (2017a), GoKE (2017) & GoTN (2017)

0

1

2

3

4

5

6

7

8

% O

F G

SDP

YEARAP Karnataka Kerala Tamil Nadu

11

For Andhra Pradesh, during 1999-00 salary expenditure grew by more than 28% mainly on account

of implementation of pay revisions (GoAP, 2000). Between 1995-96 and 1998-99 it grew at an

average of 12%. In order to overcome the fiscal distress, state governments have enacted fiscal

responsibility laws to cap the excessive spending and keep deficits under control. With the fiscal

reforms and also better economic growth rate, deficits have declined considerably until 2008. With

the onset of global financial crisis in 2008, fiscal deficit started rising again. Similar trend can be

witnessed in revenue deficits among southern states (refer Figure-2.2). Revenue deficit was highest

for all states in late 90s and early 2000 mainly owing to implementation of pay revisions. Kerala

appears to be an outlier among the southern states in managing the revenue balance. Kerala’s

revenue deficit level is highest among the southern states. Finance minister, Government of Kerala,

in the 2016-17 Budget Speech mentions that higher revenue deficit is due to inordinate rise in

expenditure for paying arrears of pay revision. There was a sharp decline in state tax receipts. He

further added that “mismanagement and corruption in tax administration are the main reasons

behind the collapse of tax receipts. In addition to this, anarchy in expenditure has also contributed

to present crisis. Decisions were taken in an adhoc manner, often without consulting Finance

Department, outside the scope of what was specified in the budget” (GoKE, 2016).

Figure-2.2

Revenue Deficits of Southern States (% of GSDP)

Source: RBI State Finances, Various Issues. GoK (2017a), GoKE (2017) & GoTN (2017)

There is a clear trend in liabilities of all the southern states. Kerala has the highest liabilities (as %

of GSDP) when compared to other southern states. Hump shaped pattern can be witnessed in the

trend, with peak in early 2000s. There was a significant decline in the liabilities after 2003-04 with

-3

-2

-1

0

1

2

3

4

5

6

7

% O

F G

SDP

YEARAP Karnataka Kerala Tamil Nadu

12

the implementation of state specific fiscal reforms. Among the southern states, Kerala is

categorized as a fiscally stressed state by the Central Government. As per the new norms, states

which have debt-GSDP ratio of 27% and more are classified as fiscally stressed ones. Earlier, the

threshold was 35% of GSDP or more (GoKE, 2016).

Figure-2.3

Liabilities of Southern States (% of GSDP)

Source: RBI State Finances, Various Issues. GoK (2017a), GoKE (2017) & GoTN (2017)

The trends and patterns clearly imply that there is a positive trend in maintaining fiscal balances

after 2003-04. This would probably be because of rule based fiscal correction mechanism followed

by the Indian states. Next chapter briefly discusses and compares the rule based fiscal correction

mechanisms followed by the southern states and adherence to it.

0

5

10

15

20

25

30

35

40

45

% O

F G

SDP

YEARAP Karnataka Kerala Tamil Nadu

13

Chapter-3

Rule Based Fiscal Correction Mechanism

A ‘Fiscal Rule’ imposes a long lasting constraint on fiscal policy through numerical limits on

budgetary aggregates. Fiscal rules typically aim at correcting distorted incentives and containing

pressures to overspend, particularly in good times, so as to ensure fiscal responsibility and debt

sustainability (Schaechter et al, 2012). As per Organization for Economic Cooperation and

Development (OECD), fiscal consolidation is a policy aimed at reducing government deficits and

debt accumulation.

Excessive deficit spending by the Government would adversely impact the macro economy.

Higher fiscal deficits lead to inflation, higher interest rate and adversely affect the economic

growth and external sector balance. Several studies like Khundrakpam & Pattnaik (2010) have

found that fiscal deficit creates inflationary situation. Few other studies like Ramu, M R & Gayithri

(2016) and Ramu, M R (2016) have found that fiscal deficit adversely affects economic growth

and external sector variables in India. Fiscal deficit level for both Central and State Governments

has peaked in early 2000s. The reasons are increased military spending, subsidies etc for the

Central Government. There are several factors which are responsible for the emergence of

unsustainable fiscal imbalance in the States. Anand, Bagchi & Sen (2002) argue that on the demand

side, fiscal problems of both the Centre and States would appear to have been the product of

‘Populism’ and deficit bias of unstable Government in democracy. On the supply side, budget

problem of the states seem to reflect a softening of hard budget constraint implicit in the

Constitution restrictions on their borrowing and in adequate oversight on the part of Centre. In

order to control the deficit and debt, Government of India constitutionally enacted Fiscal

Responsibility and Budget Management Act in the year 2003. Several States followed the path of

Central Government and enacted State specific fiscal responsibility legislations. Karnataka

Government was the first to enact the Fiscal responsibility legislation in the year 2002, even before

the Central Government.

There are few schemes which incentivized and also obliged the state governments to enact fiscal

responsibility legislations. They are:

1. Fiscal Reforms Facility (2000-01 to 2004-05)

14

Pursuant to the recommendations of the Eleventh Finance Commission, Government of India

created a Fiscal Reforms Facility (FRF) for incentivizing the states to undertake Medium Term

Fiscal Reforms Program (MTFRP) for fiscal consolidation. The state governments were asked to

draw up MTFRP incorporating time-bound action points on fiscal objectives and reforms, power

sector reforms, public sector restructuring and budgetary reforms. FRF envisaged that if the state

on an average achieves a five percentage point reduction in revenue deficit as percentage of

revenue receipts consistently each year, by the year 2005-06 the sector as whole would come into

revenue balance. An incentive fund was created and release of it was based on the single

monitorable fiscal objective as mentioned above. Karnataka has availed maximum of allocated

fund under FRF (refer Table-3.1). Tamil Nadu has received the highest amount followed by

Andhra Pradesh.

Table-3.1

Incentive Fund Allocated & Released under FRF to Southern States

(in INR crore)

States Incentive Fund Allocated Released

Andhra Pradesh 427.84 221.61

Karnataka 286.15 217.23

Kerala 208.48 64.44

Tamil Nadu 402.36 305.44

Source: MoF (2017)

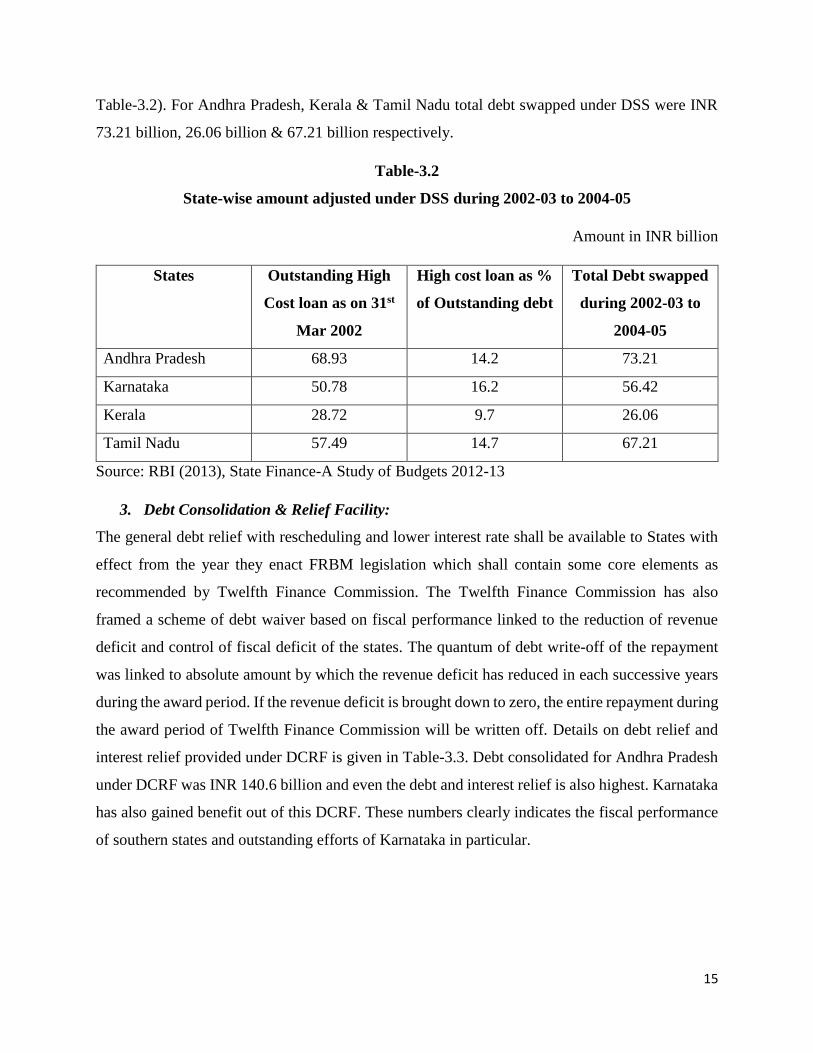

2. Debt Swap Scheme:

Government of India formulated a Debt Swap Scheme (DSS) realizing the mounting burden of

interest payments on the states and supplement their effort towards fiscal management. The

scheme was in operation from 2002-03 to 2004-05. The scheme capitalized on the current low

interest regime, to enable states to prepay expensive loans contracted from Government of India,

with low coupon bearing small savings and open market loans. This scheme covered outstanding

high cost loans with interest rate of 13% and above. An amount of INR 106076 crore was prepaid

to Government of India by the States from small saving loans and open market borrowings. Total

debt swapped under DSS for Karnataka during 2002-03 to 2004-05 was INR 56.42 billion (refer

15

Table-3.2). For Andhra Pradesh, Kerala & Tamil Nadu total debt swapped under DSS were INR

73.21 billion, 26.06 billion & 67.21 billion respectively.

Table-3.2

State-wise amount adjusted under DSS during 2002-03 to 2004-05

Amount in INR billion

States Outstanding High

Cost loan as on 31st

Mar 2002

High cost loan as %

of Outstanding debt

Total Debt swapped

during 2002-03 to

2004-05

Andhra Pradesh 68.93 14.2 73.21

Karnataka 50.78 16.2 56.42

Kerala 28.72 9.7 26.06

Tamil Nadu 57.49 14.7 67.21

Source: RBI (2013), State Finance-A Study of Budgets 2012-13

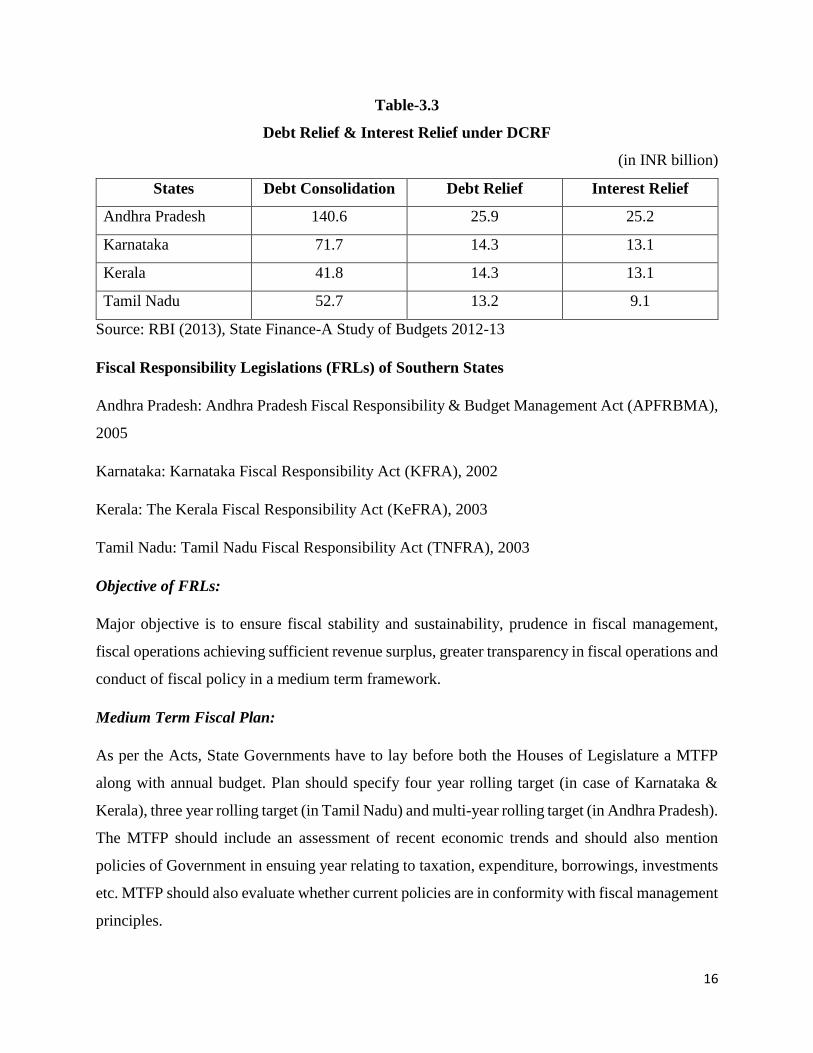

3. Debt Consolidation & Relief Facility:

The general debt relief with rescheduling and lower interest rate shall be available to States with

effect from the year they enact FRBM legislation which shall contain some core elements as

recommended by Twelfth Finance Commission. The Twelfth Finance Commission has also

framed a scheme of debt waiver based on fiscal performance linked to the reduction of revenue

deficit and control of fiscal deficit of the states. The quantum of debt write-off of the repayment

was linked to absolute amount by which the revenue deficit has reduced in each successive years

during the award period. If the revenue deficit is brought down to zero, the entire repayment during

the award period of Twelfth Finance Commission will be written off. Details on debt relief and

interest relief provided under DCRF is given in Table-3.3. Debt consolidated for Andhra Pradesh

under DCRF was INR 140.6 billion and even the debt and interest relief is also highest. Karnataka

has also gained benefit out of this DCRF. These numbers clearly indicates the fiscal performance

of southern states and outstanding efforts of Karnataka in particular.

16

Table-3.3

Debt Relief & Interest Relief under DCRF

(in INR billion)

States Debt Consolidation Debt Relief Interest Relief

Andhra Pradesh 140.6 25.9 25.2

Karnataka 71.7 14.3 13.1

Kerala 41.8 14.3 13.1

Tamil Nadu 52.7 13.2 9.1

Source: RBI (2013), State Finance-A Study of Budgets 2012-13

Fiscal Responsibility Legislations (FRLs) of Southern States

Andhra Pradesh: Andhra Pradesh Fiscal Responsibility & Budget Management Act (APFRBMA),

2005

Karnataka: Karnataka Fiscal Responsibility Act (KFRA), 2002

Kerala: The Kerala Fiscal Responsibility Act (KeFRA), 2003

Tamil Nadu: Tamil Nadu Fiscal Responsibility Act (TNFRA), 2003

Objective of FRLs:

Major objective is to ensure fiscal stability and sustainability, prudence in fiscal management,

fiscal operations achieving sufficient revenue surplus, greater transparency in fiscal operations and

conduct of fiscal policy in a medium term framework.

Medium Term Fiscal Plan:

As per the Acts, State Governments have to lay before both the Houses of Legislature a MTFP

along with annual budget. Plan should specify four year rolling target (in case of Karnataka &

Kerala), three year rolling target (in Tamil Nadu) and multi-year rolling target (in Andhra Pradesh).

The MTFP should include an assessment of recent economic trends and should also mention

policies of Government in ensuing year relating to taxation, expenditure, borrowings, investments

etc. MTFP should also evaluate whether current policies are in conformity with fiscal management

principles.

17

Fiscal Management Principles:

Karnataka’s FRL is unique when it comes to fiscal management principle. Karnataka Fiscal

Responsibility Act specifies 17 principles which include maintaining debt at prudent level,

managing guarantees and liabilities prudently, borrowings to be used for capital formation,

maintaining integrity of tax system, and pursuing expenditure policies that would provide impetus

to economic growth, poverty reduction & improvement in human welfare. It also includes aspects

of inter-generational equity, publicizing the information etc. Fiscal responsibility principles of

other states basically prescribe the fiscal targets to be achieved. Tamil Nadu FRL has few similar

Principles as exhibited in Karnataka’s FRL. Detailed review of FRLs of southern states is provided

in Appendix-1.

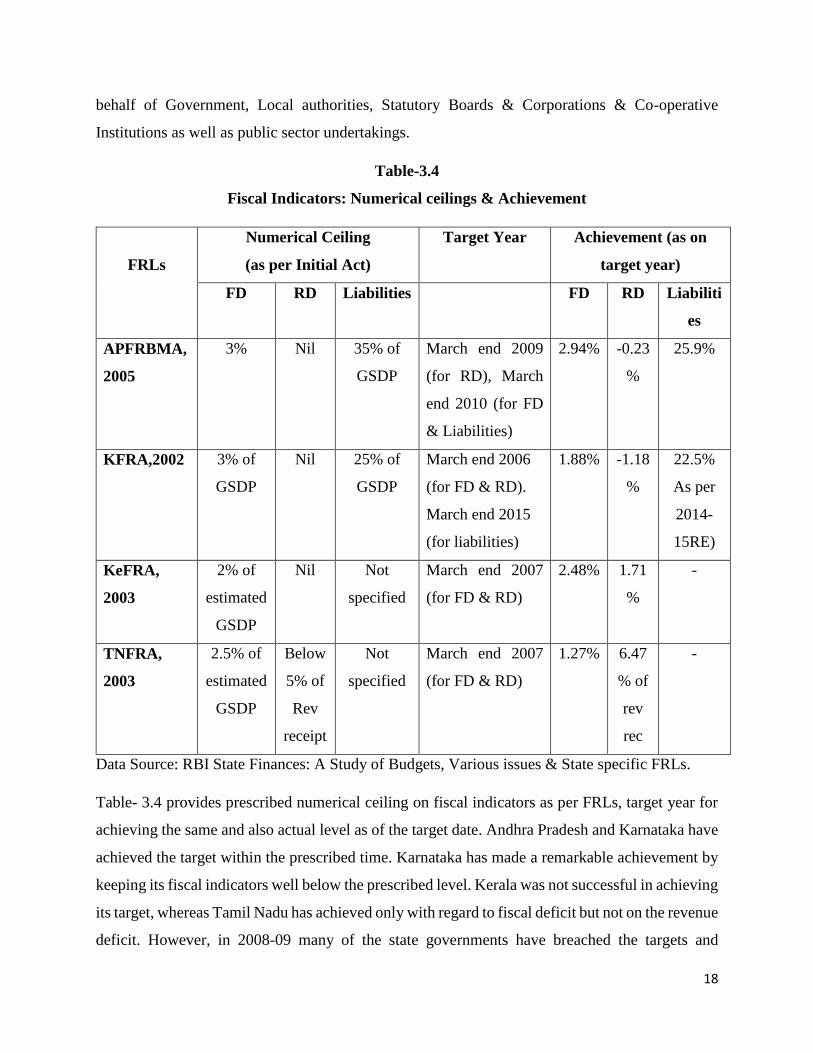

Fiscal Indicators: Central FRA and also State FRAs defines Fiscal Indicators as the measures

such as numerical ceilings and proportion to GSDP (GDP for Central Government), as may be

prescribed for evaluation of fiscal position of state governments.

FRLs specifies limits on fiscal deficit, revenue deficit, liabilities, guarantees provided by the

Governments.

Definitions:

Fiscal deficit: Total disbursement from the Consolidated Fund of the state (excluding repayment

of debt) over total receipts into the fund excluding the debt receipts during a financial year.

Revenue deficit: Difference between revenue receipts and revenue expenditure

Liabilities: It means the liabilities under the Consolidate Fund of the state and Public Account of

the state.

Guarantees: (a) Government Guarantee: as per Karnataka Ceiling on Government Guarantee Act,

1999 (KCGGA, 1999), Government Guarantee implies the guarantee given by State Government

on behalf of Departmental Undertakings, Public Sector Undertakings, Local Authorities, Statutory

Boards & Corporations & Co-operative Institutions (GoK, 2017). (b). Performance Guarantee

includes the letters of comfort, power purchase agreement, state support agreement, concession

agreement for infrastructure project and other agreements guaranteed in certain performance on

18

behalf of Government, Local authorities, Statutory Boards & Corporations & Co-operative

Institutions as well as public sector undertakings.

Table-3.4

Fiscal Indicators: Numerical ceilings & Achievement

FRLs

Numerical Ceiling

(as per Initial Act)

Target Year Achievement (as on

target year)

FD RD Liabilities FD RD Liabiliti

es

APFRBMA,

2005

3% Nil 35% of

GSDP

March end 2009

(for RD), March

end 2010 (for FD

& Liabilities)

2.94% -0.23

%

25.9%

KFRA,2002

3% of

GSDP

Nil 25% of

GSDP

March end 2006

(for FD & RD).

March end 2015

(for liabilities)

1.88% -1.18

%

22.5%

As per

2014-

15RE)

KeFRA,

2003

2% of

estimated

GSDP

Nil Not

specified

March end 2007

(for FD & RD)

2.48% 1.71

%

-

TNFRA,

2003

2.5% of

estimated

GSDP

Below

5% of

Rev

receipt

Not

specified

March end 2007

(for FD & RD)

1.27% 6.47

% of

rev

rec

-

Data Source: RBI State Finances: A Study of Budgets, Various issues & State specific FRLs.

Table- 3.4 provides prescribed numerical ceiling on fiscal indicators as per FRLs, target year for

achieving the same and also actual level as of the target date. Andhra Pradesh and Karnataka have

achieved the target within the prescribed time. Karnataka has made a remarkable achievement by

keeping its fiscal indicators well below the prescribed level. Kerala was not successful in achieving

its target, whereas Tamil Nadu has achieved only with regard to fiscal deficit but not on the revenue

deficit. However, in 2008-09 many of the state governments have breached the targets and

19

amended the FRLs several times after that. Reasons for amendments and revised target dates are

given in the sub section- Amendments below.

Along with liabilities, FRLs also restricts the guarantees provided by the state government. As per

KCGGA,1999 the total outstanding guarantee by state government as on 1st April of any year shall

not exceed 80% of state revenue receipts of the second preceding year as in the books of

Accountant General of the State. APFRBMA limits the annual incremental risk weighted

guarantees to 90% of total revenue receipts in the year preceding of current year. TNFRA 2003

prescribes to cap the outstanding risk weighted guarantees to 100% of the total revenue receipts in

the preceding year or 10% of GSDP.

Measures for Fiscal Transparency:

As per the FRLs, Governments have to disclose any changes in accounting standards, policies

&practices. Governments should also disclose liabilities, commitments, losses incurred, contracts,

subsidy payments etc.

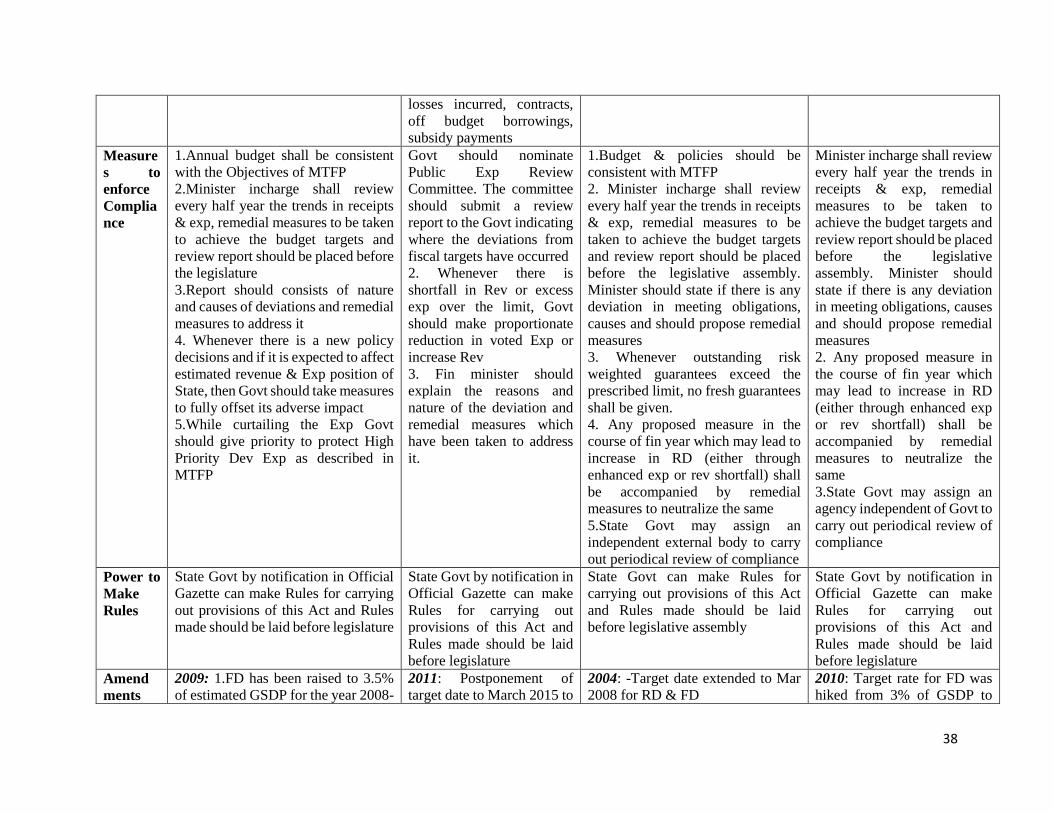

Measures to Enforce Compliance:

Annual budget of States should be consistent with the MTFP objectives. Minister in-charge shall

review trends in receipts and expenditure, should explain the reasons of there are deviations and

should also suggest remedial measures. Karnataka’s FRL specifically mentions that while

curtailing expenditure, government should give priority to protect high priority development

expenditure as prescribed in the MTFP. As per Kerala’s FRL, government should nominate Public

Expenditure Review Committee to assess the report. Andhra Pradesh and Tamil Nadu FRL

suggests to the government to assign the review work to an independent agency. Karnataka’s FRL

lacks such prescription and it has to be incorporated in the Karnataka Fiscal Responsibility Act.

Power to Make Rules:

State Governments by notification in Official Gazette can make rules for carrying out provisions

of this Act and Rules which should be laid before legislature.

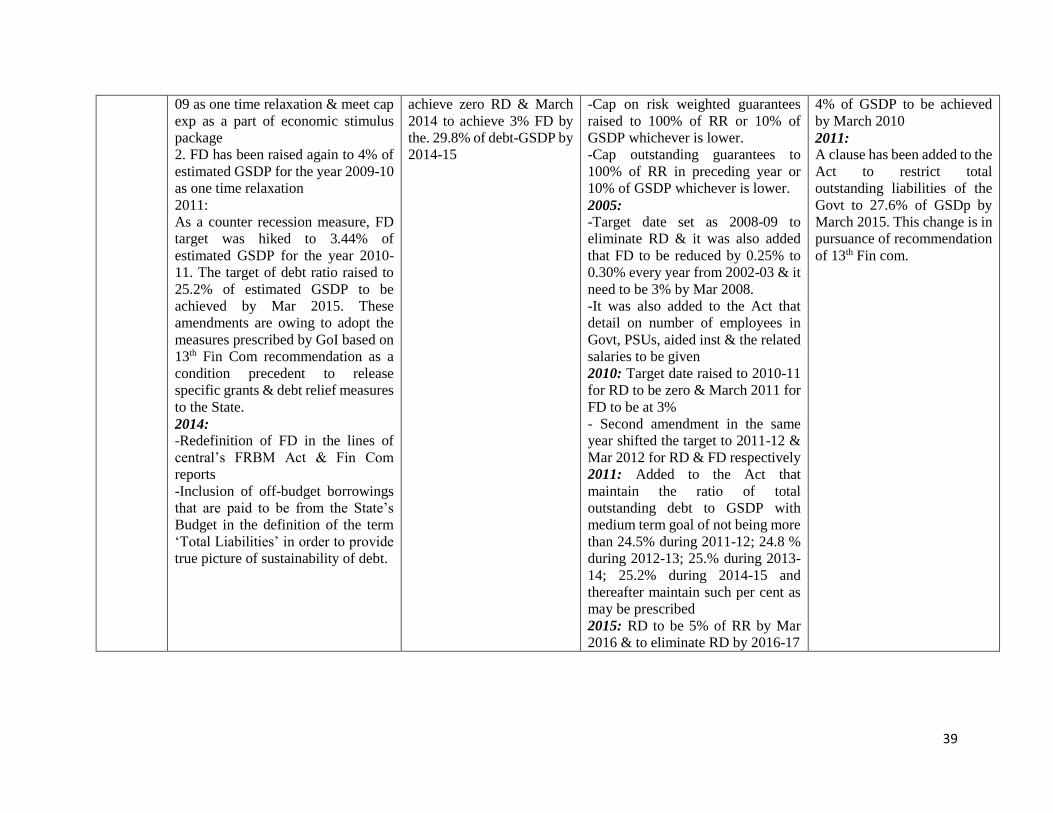

Amendments to FRLs:

Karnataka Government amended Karnataka Fiscal Responsibility Act in the year 2009 and 2011.

Fiscal deficit target as percent of GSDP increased to 3.5% for the year 2008-09 as one time

relaxation and to meet capital expenditure as a part of economic stimulus package to overcome the

20

financial crisis. Further, target was raised to 4% as one time relaxation for the year 2009-10. As a

counter recession measure, once again FD target was hiked to 3.44% of estimated GSDP for the

year 2010-11. The target of debt ratio raised to 25.2% of estimated GSDP to be achieved by March

2015. These amendments were due to adopting the measures prescribed by Government of India

based on Thirteenth Finance Commission recommendation as a condition precedent to release

specific grants & debt relief measures to the state. In the year 2014, Act was amended to

incorporate the redefinition of fiscal deficit in the lines of Central’s FRBM Act and Finance

Commission reports. Off-budget borrowings that are to be paid from the State’s budget are

included in the definition of term ‘Total Liabilities’ in order to provide true picture of sustainability

of debt.

Kerala Government has amended FRA in the year 2011 and postponed the target date to March

2015. Tamil Nadu, as on date, has amended Tamil Nadu Fiscal Responsibility Act five times. First

amendment was in 2004. Target date was extended from 2007 to 2008. Cap on risk weighted

guarantees raised to 100% of revenue receipts or 10% of GSDP whichever is lower. Cap

outstanding guarantees to 100% of revenue receipts in preceding year or 10% of GSDP whichever

is lower. TNFRA was amended in 2005 to extend the target date. It was added to the Act that

details of number of employees in Government, Public Sector Undertakings, aided institutions and

the related salaries are be given. Act was amended in 2010, 2011 and in 2015 to extend the target

date.

Andhra Pradesh Government amended APFRBMA, 2005 in the year 2010 and 2011. Cap on fiscal

deficit raised from 3% of GSDP to 4% of GSDP in 2010 amendment. Amendment in 2011 was

mainly to accommodate 13th Finance Commission’s recommendations.

21

Chapter-4

Impact of FRLs on Fiscal Indicators

Descriptive analysis as presented in Chapter-2 indicated the changing trends and pattern of fiscal

indicators in the study period. Table-4.1 provides an average of fiscal indicators as % to GSDP in

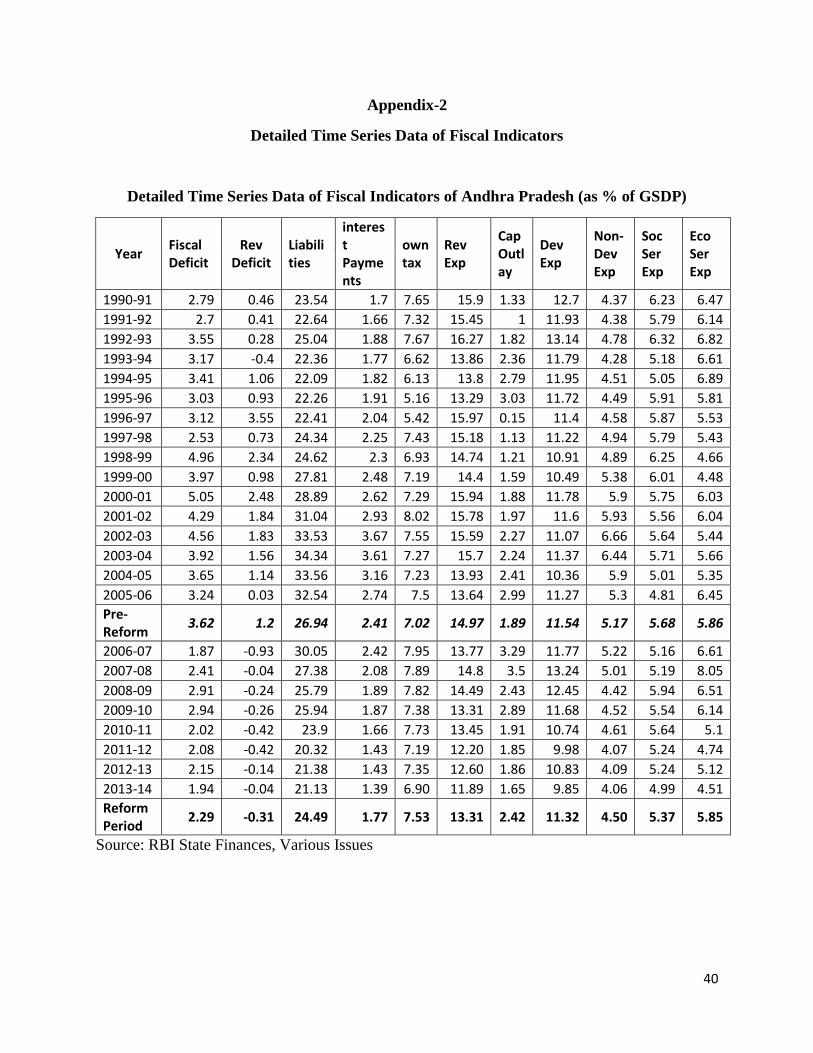

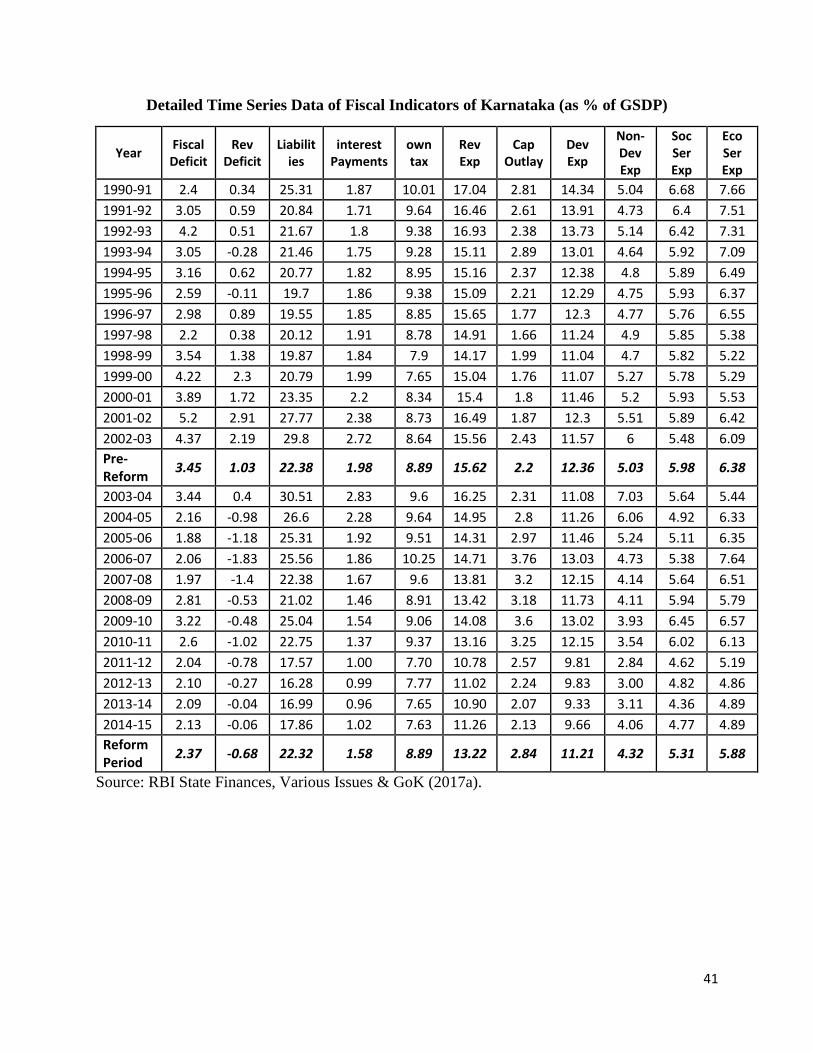

the pre-reform4 and reform period. Pre-reform (pre-FRL) period is from 1990-91 to 2002-03 for

Karnataka, 1990-91 to 2003-04 for Kerala & Tamil Nadu and 1990-91 to 2005-06 for Andhra

Pradesh. Post reform period is until 2014-15 (until 2013-14 for Andhra Pradesh) from the year of

FRL enforcement. A detailed time series data of fiscal variables in pre-reform and reform period

is provided in Appendix-2.

Table-4.1

Fiscal Indicators in Pre-FRL and FRL Period (% of GSDP)

States / Indicators

FD RD Liabilities

Interest Payments

Own Tax Rev

Rev Exp

Cap Outlay

Dev Exp

Non-Dev Exp

Soc Ser

Eco Ser

Andhra Pradesh

Pre-FRL

3.62 1.2 26.94 2.41 7.02 14.97 1.89 11.54 5.17 5.68 5.86

FRL 2.29 -0.31 24.49 1.77 7.53 13.31 2.42 11.32 4.5 5.37 5.85

Karnataka

Pre-FRL

3.45 1.03 22.38 1.98 8.89 15.62 2.2 12.36 5.03 5.98 6.38

FRL 2.37 -0.68 22.32 1.58 8.89 13.22 2.84 11.21 4.32 5.31 5.88

Kerala

Pre-FRL

4.73 2.84 33.22 2.81 8.7 16.79 1.22 10.97 6.84 6.59 4.38

FRL 3.32 2.2 31.2 2.26 7.44 13.49 0.87 7.45 6.18 4.64 2.66

Tamil Nadu

Pre-FRL

3.16 2.11 22.52 1.89 8.9 16 1.01 11.32 5.06 6.28 5.04

FRL 2.00 -0.12 20.64 1.52 8.23 12.19 1.92 8.91 4.48 5.17 3.55

Source: RBI State Finances, Various Issues. GoK (2017a), GoKE (2017) & GoTN (2017)

Table-4.1 denotes that there is a healthy change in all the fiscal indicators. Fiscal deficit and

revenue deficit as a percent of GSDP has declined for all the southern states. Liabilities have

declined for all selected states except Karnataka where there is only a minute decline in liabilities

from 22.38% to 22.32% of GSDP. Consequent to reduction in liabilities, interest payments have

also declined. With regard to own tax revenue, there was only a marginal increase for Andhra

4 Reform here refers to fiscal reforms through enactment of FRLs

22

Pradesh, whereas it remained same for Karnataka. For Tamil Nadu and Kerala, it declined in

reform era. Revenue expenditure has declined and capital outlay went up in the reform era for all

the southern states except Kerala where capital outlay has declined. Non-development expenditure

declined marginally for all the four States, but development expenditure as percent of GSDP too

declined for Kerala and Tamil Nadu almost by 3% of GSDP. Even though there is minimal

variation with regard to social service spending, economic service expenditure has declined for all

the southern states and the decline is maximum for Kerala followed by Tamil Nadu.

All the southern states except Kerala have kept their fiscal variables (as a percent of GSDP) well

within the prescribed limit as per FRLs particularly for deficit indicators and liabilities. Even

though, fiscal indicators as % to GSDP are within the limit, it is important to know and keep a

check on its growth rate. It is also important to know whether the change is significant or not. To

measure the impact of FRL on growth of fiscal indicators, time series econometrics is being used

here for the analysis. It may happen that even though there might be a reduction or expansion of a

particular variable in the reform era than earlier but that change may not be a significant one. These

dynamics can be clearly captured by using time series econometrics. A brief methodological note

of the same is given below.

Methodology:

Time Period: 1990-91 to 2014-15

Dummy variable technique is being adopted for the analysis. Structural change can be effectively

captured using dummy variable technique if exact year of break is known. Even in advanced

Regime Switching models, dummy variable are being used.

Consider following equation

lnFD𝑡 = α1 + β1𝑡𝑖𝑚𝑒 + 𝒖𝒕 …….. (1)

In equation-1 lnFD is natural log of fiscal deficit, time is the independent variable. Subscript ′𝒕′

indicates time. α, β & 𝑢 are the parameters to be estimated. Estimation of equation-1 indicates how fiscal

deficit has grown in the study period.

To see a structural break, equation-1 need to be modified as follows

lnFD𝑡 = α1 + β1𝑡𝑖𝑚𝑒 + β2𝐹𝑅𝐴 𝑑𝑢𝑚𝑚𝑦𝑡 + 𝒖𝒕 …….. (2)

23

Where 𝐹𝑅𝐴 𝑑𝑢𝑚𝑚𝑦 is the dummy variable introduced to capture the impact of Fiscal Responsibility

Act on fiscal variable, say fiscal deficit. For instance FRA came into force in the year 2003-04 for

Karnataka and in order to capture its impact, we have considered 2004-05 as break year (with

assumption that its impact may not be immediate and takes at least a lag of one year). Hence FRA

dummy takes values of ‘1’ after 2004-05 and ‘0’ before that. β2 is a differential intercept which

shows how much change has happened in fiscal deficit after the FRLs.

There is a possibility that it is not just the intercept but also the slope coefficient might have

changed (Gujarati, 2011). If both differential intercept and differential slope dummies are

introduced, equation-2 need to be modified as follows

lnFD𝑡 = α1 + β1𝑡𝑖𝑚𝑒 + β2𝐹𝑅𝐴 𝑑𝑢𝑚𝑚𝑦𝑡 + β3𝑡𝑖𝑚𝑒 × 𝐹𝑅𝐴 𝑑𝑢𝑚𝑚𝑦𝑡 + 𝒖𝒕 …….. (3)

β3 is the differencial slope coefficient. Movement or growth in the fiscal indicators before and in

reform era can be derived from equation-3.

Fiscal deficit growth in Pre-FRA period

lnFD𝑡 = α1 + β1𝑡𝑖𝑚𝑒

Fiscal deficit growth in FRA period

lnFD𝑡 = (α1 + β2𝐹𝑅𝐴 𝑑𝑢𝑚𝑚𝑦𝑡) + (β1𝑡𝑖𝑚𝑒 + β3𝑡𝑖𝑚𝑒 × 𝐹𝑅𝐴 𝑑𝑢𝑚𝑚𝑦𝑡)

Variables: All the major fiscal variables have been considered for the analysis. Variables are

classified under three major heads namely deficit indicators, revenue variables & expenditure

variables. Deficit related variables includes fiscal deficit, revenue deficit, liabilities and also

interest payments. States’ own tax revenue is considered as revenue indicator. Expenditure

variables include revenue expenditure, capital outlay, development & non-development

expenditure, social service and economic service expenditure. For each State and each variable,

separate regression has been run. This exercise provides a detailed picture of impact of fiscal rule

on each fiscal variable across States.

All the variables have been converted into 2004-05 prices using state specific GSDP deflator. Year

2004-05 for Karnataka, 2005-06 for Kerala and Tamil Nadu and 2006-07 for Andhra Pradesh has

been considered as break year and introduced FRA time dummy, which takes values of ‘1’ after

the said years and ‘0’ before that.

24

Discussion on Results

Deficit Indicators:

Regression results on FRLs impact on fiscal deficit and revenue deficit across the southern states

are presented in Table-4.2. In the Table-4.2 FRA is the time dummy and it is the intercept for the

regression equation representing fiscal reforms period and FRA*time is the slope coefficient.

Significant FRA (intercept) indicates that there is a shift in base of regression equation in reform

period. A significant slope coefficient indicates that there is structural break in the growth of

dependent variable. Insignificant LM-test statistics indicate that there is no autocorrelation

problem. R-squared value is high for all the models as required under time series analysis.

Table- 4.2

Structural Break Analysis Results (Fiscal Deficit & Revenue Deficit)

Andhra Pradesh Karnataka Kerala Tamil Nadu

Fisc

al D

efi

cit

Constant 8.006 (0.00)* 7.39 (0.00)* 7.48(0.00)* 7.95(0.00)*

Time 0.065 (0.00)* 0.09(0.00)* 0.072(0.00)* 0.061(0.00)*

FRA 0.481 (0.51) -0.796 (0.05)** -1.21 (0.18) -3.211 (0.00)*

FRA*time -0.036 (0.31) 0.007 (0.74) 0.048 (0.10)*** 0.135 (0.00)*

R-squared 0.77 0.87 0.85 0.75

LM-test Stats 0.74 (0.49) 1.94 (0.16) 2.06 (0.15) 1.42 (0.26)

Re

ven

ue

De

fici

t Constant 8.75 (0.00)* 8.36(0.00)* 6.23(0.00)* 8.8203 (0.00)*

Time 0.0006(0.96) 0.048(0.00)* 0.138(0.00)* 0.016 (0.39)

FRA -0.6801 (0.53) -1.82 (0.00)* 0.073 (0.96) -3.193 (0.00)*

FRA*time 0.011 (0.82) 0.021 (0.21) -0.039 (0.65) 0.113 (0.00)*

R-squared 0.32 0.85 0.84 0.70

LM-test Stats 1.07 (0.32) 1.34 (0.29) 0.79 (0.46) 1.37 (0.28)

Note: p-values are given in parenthesis ( ). *sig at 1% level, **sig at 5% level & ***sig at 10%

level

As indicated by significant coefficient of Time variable, Fiscal deficit has grown at a significant

rate in the pre-reform era for all the southern states (refer Table-4.2). For Andhra Pradesh there

was no significant impact of fiscal rule on reducing fiscal deficit. Andhra Pradesh has witnessed

significant growth of fiscal deficit in pre-reform period. This was basically owing to increased

salary bill, introduction of new welfare schemes, huge subsidy burden and most importantly

changes in political power. For Karnataka, there is a significant decline in the base value of fiscal

deficit but there was no significant impact on growth of fiscal deficit. Notably, for Kerala fiscal

deficit is growing at a faster rate in the reform period than earlier. Fiscal deficit has grown by 7.2%

25

in pre-reform period, which is growing at 12% in the reform period. For Tamil Nadu there is no

significant reduction in the fiscal deficit after the FRL.

Similar impact was observed on revenue deficit level. Impact of fiscal rule is not significant in

reducing fiscal deficit growth for Andhra Pradesh and Kerala. For Karnataka, only the base got

reduced but no significant change in its growth. Interestingly, revenue deficit is growing at a faster

rate and much significantly in reform period compared to pre-reform period for Tamil Nadu. The

growth rate is in double digit. Significant growth in revenue deficit is mainly owing to drastic fall

in commercial tax and sales tax collection, implementation of many popular programs as promised

by political parties during elections like free distribution of mixer grinder, laptops, color TVs,

special public distribution system, social security pension schemes etc (GoTN, 2016a). Many other

important programs like free power up to 100 units to domestic consumers, waiver of agricultural

loans of small and marginal farmers owed to the cooperative institutions have indeed increased the

expenditure of state and consequently lead to higher revenue deficit (GoTN, 2016).

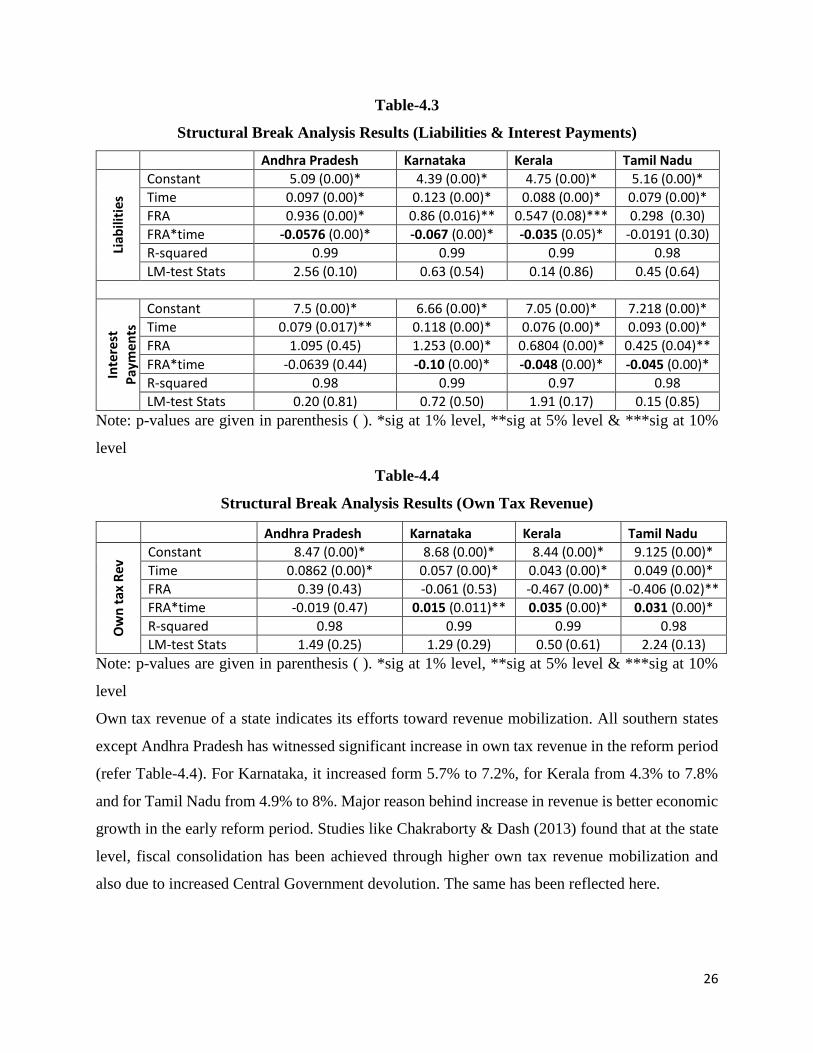

In the case of Liabilities (refer Table-4.3), all southern states except Tamil Nadu have achieved

significant reduction in its growth. However constant value has increased in the reform period.

Growth rate has declined from 9.7% in pre-reform era to 3.9% in reform period for Andhra

Pradesh, from 12.3% to 5.6% for Karnataka and from 8.8% to 5.3% for Kerala. Interest Payments

constitute major portion of expenditure both for Central Government and also among the states.

Structural break analysis results (refer Table-4.3) indicate that interest payments growth have

significantly declined for Karnataka, Kerala and Tamil Nadu. However, the constant value has

significantly increased. The decline in interest payment burden is mainly due to softening of

interest rates on Government securities in the reform period, particularly in mid of last decade.

Also measures like debt swap schemes in a low interest rate regime has benefited the states in

reducing interest rates (Chakraborty, 2005). Low interest rates in the reform period is the main

reason behind reduction in interest payments. Reduction in deficits and consequently the liabilities

has also contributed for reduction in interest payments. A report on Tamil Nadu State Finances

argue that reduction in liabilities (even though not significant for Tamil Nadu) and interest

payments was due to diversification of debt portfolio towards cheapest source of borrowing like

external loans, open market loans etc (MIDS, 2014).

26

Table-4.3

Structural Break Analysis Results (Liabilities & Interest Payments)

Andhra Pradesh Karnataka Kerala Tamil Nadu

Liab

iliti

es

Constant 5.09 (0.00)* 4.39 (0.00)* 4.75 (0.00)* 5.16 (0.00)*

Time 0.097 (0.00)* 0.123 (0.00)* 0.088 (0.00)* 0.079 (0.00)*

FRA 0.936 (0.00)* 0.86 (0.016)** 0.547 (0.08)*** 0.298 (0.30)

FRA*time -0.0576 (0.00)* -0.067 (0.00)* -0.035 (0.05)* -0.0191 (0.30)

R-squared 0.99 0.99 0.99 0.98

LM-test Stats 2.56 (0.10) 0.63 (0.54) 0.14 (0.86) 0.45 (0.64)

Inte

rest

P

aym

en

ts

Constant 7.5 (0.00)* 6.66 (0.00)* 7.05 (0.00)* 7.218 (0.00)*

Time 0.079 (0.017)** 0.118 (0.00)* 0.076 (0.00)* 0.093 (0.00)*

FRA 1.095 (0.45) 1.253 (0.00)* 0.6804 (0.00)* 0.425 (0.04)**

FRA*time -0.0639 (0.44) -0.10 (0.00)* -0.048 (0.00)* -0.045 (0.00)*

R-squared 0.98 0.99 0.97 0.98

LM-test Stats 0.20 (0.81) 0.72 (0.50) 1.91 (0.17) 0.15 (0.85)

Note: p-values are given in parenthesis ( ). *sig at 1% level, **sig at 5% level & ***sig at 10%

level

Table-4.4

Structural Break Analysis Results (Own Tax Revenue)

Andhra Pradesh Karnataka Kerala Tamil Nadu

Ow

n t

ax R

ev Constant 8.47 (0.00)* 8.68 (0.00)* 8.44 (0.00)* 9.125 (0.00)*

Time 0.0862 (0.00)* 0.057 (0.00)* 0.043 (0.00)* 0.049 (0.00)*

FRA 0.39 (0.43) -0.061 (0.53) -0.467 (0.00)* -0.406 (0.02)**

FRA*time -0.019 (0.47) 0.015 (0.011)** 0.035 (0.00)* 0.031 (0.00)*

R-squared 0.98 0.99 0.99 0.98

LM-test Stats 1.49 (0.25) 1.29 (0.29) 0.50 (0.61) 2.24 (0.13)

Note: p-values are given in parenthesis ( ). *sig at 1% level, **sig at 5% level & ***sig at 10%

level

Own tax revenue of a state indicates its efforts toward revenue mobilization. All southern states

except Andhra Pradesh has witnessed significant increase in own tax revenue in the reform period

(refer Table-4.4). For Karnataka, it increased form 5.7% to 7.2%, for Kerala from 4.3% to 7.8%

and for Tamil Nadu from 4.9% to 8%. Major reason behind increase in revenue is better economic

growth in the early reform period. Studies like Chakraborty & Dash (2013) found that at the state

level, fiscal consolidation has been achieved through higher own tax revenue mobilization and

also due to increased Central Government devolution. The same has been reflected here.

27

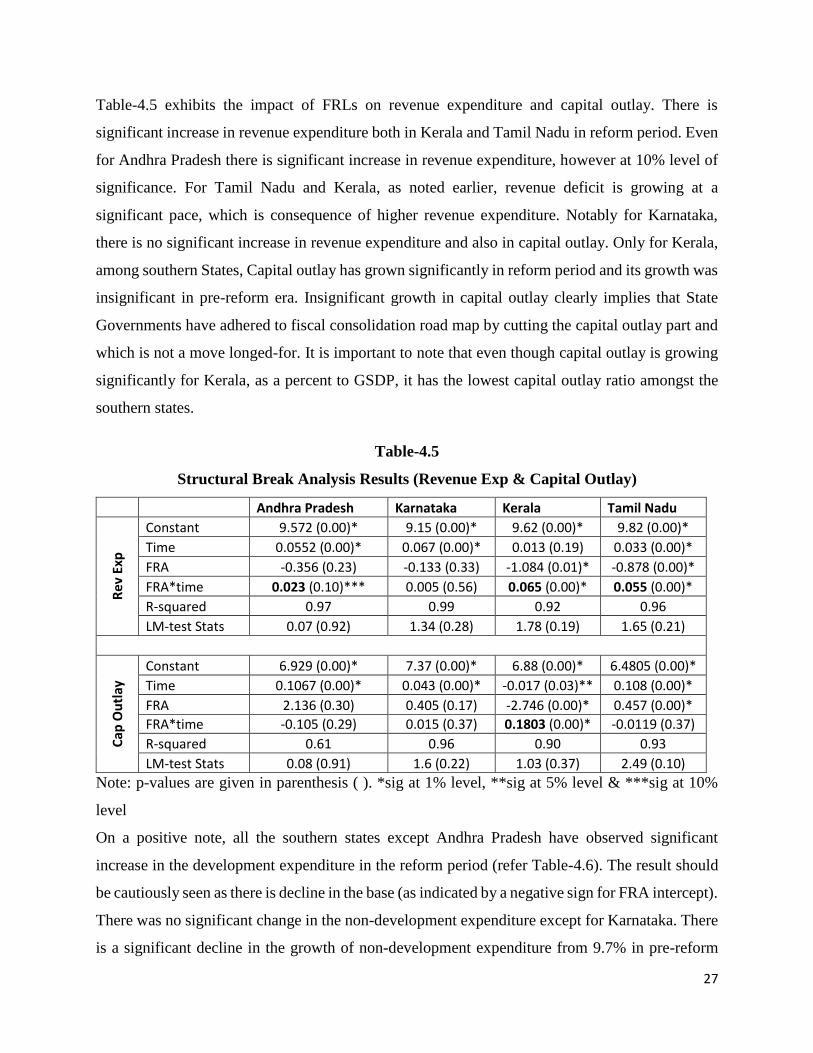

Table-4.5 exhibits the impact of FRLs on revenue expenditure and capital outlay. There is

significant increase in revenue expenditure both in Kerala and Tamil Nadu in reform period. Even

for Andhra Pradesh there is significant increase in revenue expenditure, however at 10% level of

significance. For Tamil Nadu and Kerala, as noted earlier, revenue deficit is growing at a

significant pace, which is consequence of higher revenue expenditure. Notably for Karnataka,

there is no significant increase in revenue expenditure and also in capital outlay. Only for Kerala,

among southern States, Capital outlay has grown significantly in reform period and its growth was

insignificant in pre-reform era. Insignificant growth in capital outlay clearly implies that State

Governments have adhered to fiscal consolidation road map by cutting the capital outlay part and

which is not a move longed-for. It is important to note that even though capital outlay is growing

significantly for Kerala, as a percent to GSDP, it has the lowest capital outlay ratio amongst the

southern states.

Table-4.5

Structural Break Analysis Results (Revenue Exp & Capital Outlay)

Andhra Pradesh Karnataka Kerala Tamil Nadu

Re

v Ex

p

Constant 9.572 (0.00)* 9.15 (0.00)* 9.62 (0.00)* 9.82 (0.00)*

Time 0.0552 (0.00)* 0.067 (0.00)* 0.013 (0.19) 0.033 (0.00)*

FRA -0.356 (0.23) -0.133 (0.33) -1.084 (0.01)* -0.878 (0.00)*

FRA*time 0.023 (0.10)*** 0.005 (0.56) 0.065 (0.00)* 0.055 (0.00)*

R-squared 0.97 0.99 0.92 0.96

LM-test Stats 0.07 (0.92) 1.34 (0.28) 1.78 (0.19) 1.65 (0.21)

Cap

Ou

tlay

Constant 6.929 (0.00)* 7.37 (0.00)* 6.88 (0.00)* 6.4805 (0.00)*

Time 0.1067 (0.00)* 0.043 (0.00)* -0.017 (0.03)** 0.108 (0.00)*

FRA 2.136 (0.30) 0.405 (0.17) -2.746 (0.00)* 0.457 (0.00)*

FRA*time -0.105 (0.29) 0.015 (0.37) 0.1803 (0.00)* -0.0119 (0.37)

R-squared 0.61 0.96 0.90 0.93

LM-test Stats 0.08 (0.91) 1.6 (0.22) 1.03 (0.37) 2.49 (0.10)

Note: p-values are given in parenthesis ( ). *sig at 1% level, **sig at 5% level & ***sig at 10%

level

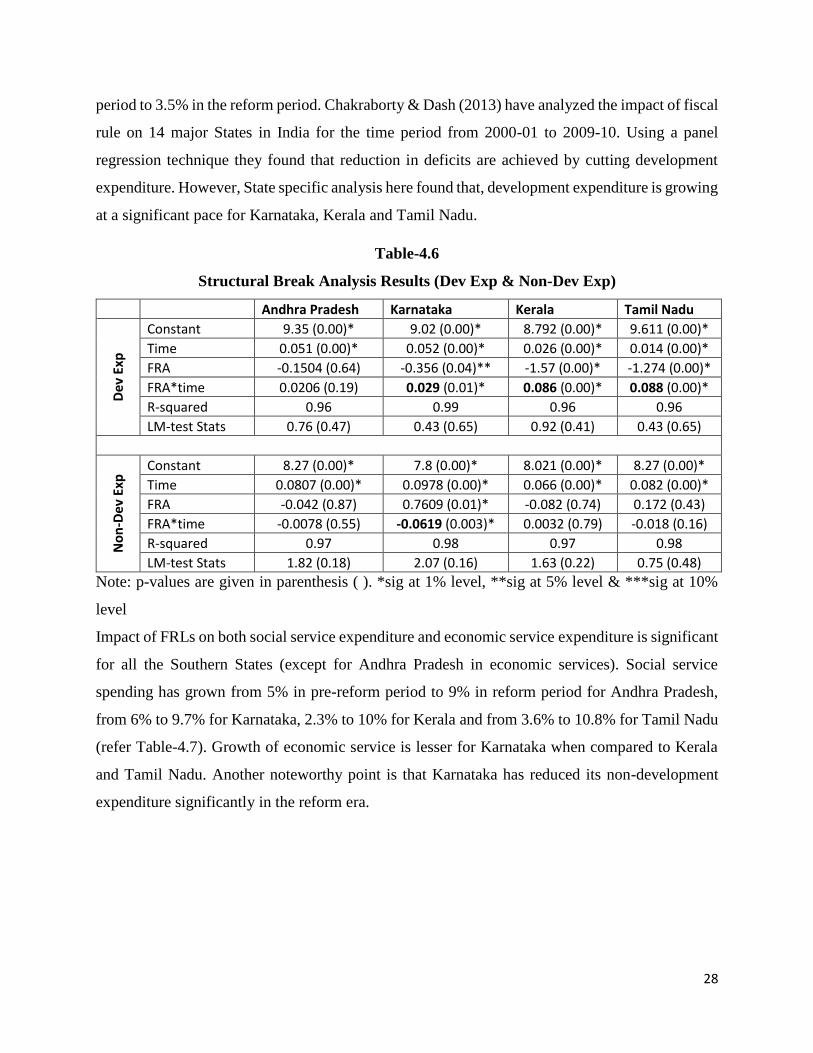

On a positive note, all the southern states except Andhra Pradesh have observed significant

increase in the development expenditure in the reform period (refer Table-4.6). The result should

be cautiously seen as there is decline in the base (as indicated by a negative sign for FRA intercept).

There was no significant change in the non-development expenditure except for Karnataka. There

is a significant decline in the growth of non-development expenditure from 9.7% in pre-reform

28

period to 3.5% in the reform period. Chakraborty & Dash (2013) have analyzed the impact of fiscal

rule on 14 major States in India for the time period from 2000-01 to 2009-10. Using a panel

regression technique they found that reduction in deficits are achieved by cutting development

expenditure. However, State specific analysis here found that, development expenditure is growing

at a significant pace for Karnataka, Kerala and Tamil Nadu.

Table-4.6

Structural Break Analysis Results (Dev Exp & Non-Dev Exp)

Andhra Pradesh Karnataka Kerala Tamil Nadu

De

v Ex

p

Constant 9.35 (0.00)* 9.02 (0.00)* 8.792 (0.00)* 9.611 (0.00)*

Time 0.051 (0.00)* 0.052 (0.00)* 0.026 (0.00)* 0.014 (0.00)*

FRA -0.1504 (0.64) -0.356 (0.04)** -1.57 (0.00)* -1.274 (0.00)*

FRA*time 0.0206 (0.19) 0.029 (0.01)* 0.086 (0.00)* 0.088 (0.00)*

R-squared 0.96 0.99 0.96 0.96

LM-test Stats 0.76 (0.47) 0.43 (0.65) 0.92 (0.41) 0.43 (0.65)

No

n-D

ev

Exp

Constant 8.27 (0.00)* 7.8 (0.00)* 8.021 (0.00)* 8.27 (0.00)*

Time 0.0807 (0.00)* 0.0978 (0.00)* 0.066 (0.00)* 0.082 (0.00)*

FRA -0.042 (0.87) 0.7609 (0.01)* -0.082 (0.74) 0.172 (0.43)

FRA*time -0.0078 (0.55) -0.0619 (0.003)* 0.0032 (0.79) -0.018 (0.16)

R-squared 0.97 0.98 0.97 0.98

LM-test Stats 1.82 (0.18) 2.07 (0.16) 1.63 (0.22) 0.75 (0.48)

Note: p-values are given in parenthesis ( ). *sig at 1% level, **sig at 5% level & ***sig at 10%

level

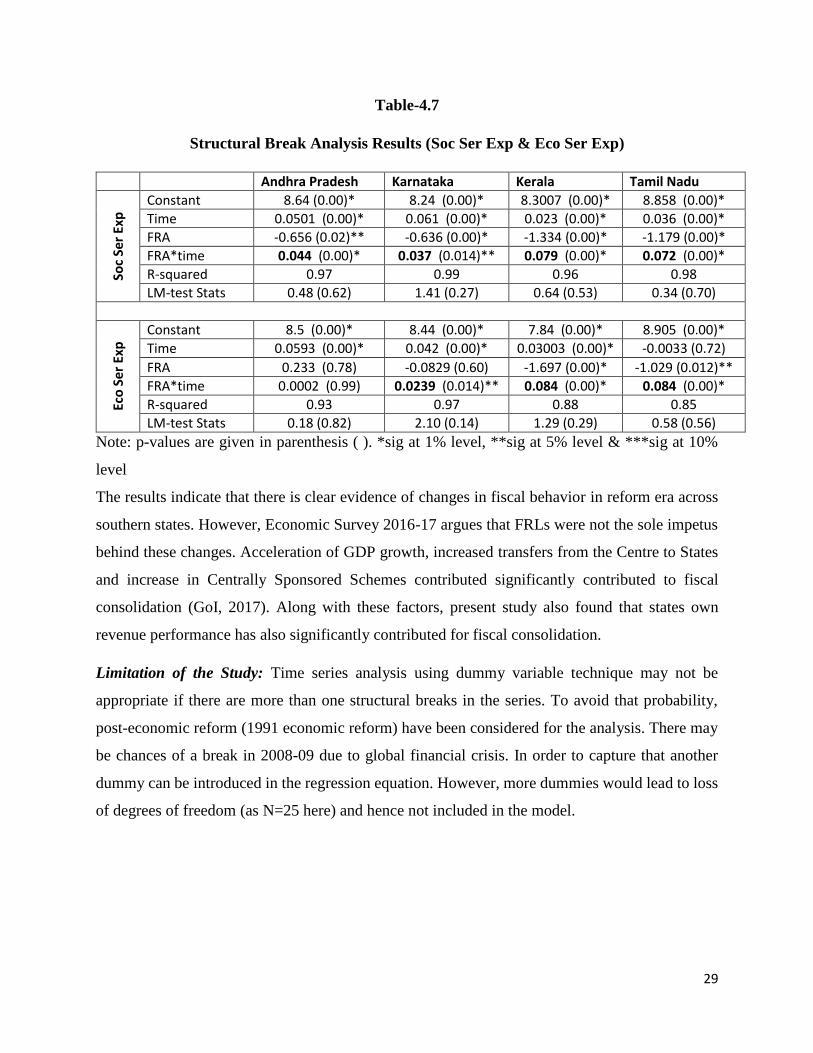

Impact of FRLs on both social service expenditure and economic service expenditure is significant

for all the Southern States (except for Andhra Pradesh in economic services). Social service

spending has grown from 5% in pre-reform period to 9% in reform period for Andhra Pradesh,

from 6% to 9.7% for Karnataka, 2.3% to 10% for Kerala and from 3.6% to 10.8% for Tamil Nadu

(refer Table-4.7). Growth of economic service is lesser for Karnataka when compared to Kerala

and Tamil Nadu. Another noteworthy point is that Karnataka has reduced its non-development

expenditure significantly in the reform era.

29

Table-4.7

Structural Break Analysis Results (Soc Ser Exp & Eco Ser Exp)

Andhra Pradesh Karnataka Kerala Tamil Nadu

Soc

Ser

Exp

Constant 8.64 (0.00)* 8.24 (0.00)* 8.3007 (0.00)* 8.858 (0.00)*

Time 0.0501 (0.00)* 0.061 (0.00)* 0.023 (0.00)* 0.036 (0.00)*

FRA -0.656 (0.02)** -0.636 (0.00)* -1.334 (0.00)* -1.179 (0.00)*

FRA*time 0.044 (0.00)* 0.037 (0.014)** 0.079 (0.00)* 0.072 (0.00)*

R-squared 0.97 0.99 0.96 0.98

LM-test Stats 0.48 (0.62) 1.41 (0.27) 0.64 (0.53) 0.34 (0.70)

Eco

Ser

Exp

Constant 8.5 (0.00)* 8.44 (0.00)* 7.84 (0.00)* 8.905 (0.00)*

Time 0.0593 (0.00)* 0.042 (0.00)* 0.03003 (0.00)* -0.0033 (0.72)

FRA 0.233 (0.78) -0.0829 (0.60) -1.697 (0.00)* -1.029 (0.012)**

FRA*time 0.0002 (0.99) 0.0239 (0.014)** 0.084 (0.00)* 0.084 (0.00)*

R-squared 0.93 0.97 0.88 0.85

LM-test Stats 0.18 (0.82) 2.10 (0.14) 1.29 (0.29) 0.58 (0.56)

Note: p-values are given in parenthesis ( ). *sig at 1% level, **sig at 5% level & ***sig at 10%

level

The results indicate that there is clear evidence of changes in fiscal behavior in reform era across

southern states. However, Economic Survey 2016-17 argues that FRLs were not the sole impetus

behind these changes. Acceleration of GDP growth, increased transfers from the Centre to States

and increase in Centrally Sponsored Schemes contributed significantly contributed to fiscal

consolidation (GoI, 2017). Along with these factors, present study also found that states own

revenue performance has also significantly contributed for fiscal consolidation.

Limitation of the Study: Time series analysis using dummy variable technique may not be

appropriate if there are more than one structural breaks in the series. To avoid that probability,

post-economic reform (1991 economic reform) have been considered for the analysis. There may

be chances of a break in 2008-09 due to global financial crisis. In order to capture that another

dummy can be introduced in the regression equation. However, more dummies would lead to loss

of degrees of freedom (as N=25 here) and hence not included in the model.

30

Chapter-5

Conclusion and Policy Implications

Higher deficits and mounting debt in late 90s and early 2000s paved the way for rule based fiscal

correction mechanism in India. Higher deficits across southern states were mainly due to

implementation of pay revisions, huge subsidies, waiver of farm loans etc. For instance, in Andhra

Pradesh the rice subsidy given in the year 1995-96 was so huge that it was about half of total

budgetary allocations to education and health together. There are recent episodes in Tamil Nadu

that government wants to amend the FRLs in order to fulfill the promise they have made during

Assembly elections.

Karnataka was the first State to implement fiscal responsibility legislation followed by Tamil

Nadu, Kerala and Andhra Pradesh. Among the southern states, Karnataka has a unique and

distinguished feature in the FRL. Its 17 Fiscal Management Principles covers several aspects

including inter-generational equity. There is only one limitation with Karnataka’s FRL is lack of

independent external assessment body to review the compliance of the State Government to FRL.

State Governments have amended FRLs several times to provide counter recession measures. In

the name of global financial crisis, all the southern states have postponed the target dates. In

addition to it, to accommodate new definition of fiscal deficit and to pursue recommendations of

Thirteenth Finance Commissions State Governments have amended the FRLs. Between 2003-04

and 2014-15 Tamil Nadu Government have amended FRL five times. There must be some strict

rule to limit these amendments several times by providing unconventional reasons.

Trend analysis indicated that there is change in trends and patterns of fiscal indicators after the

enactment of FRLs across southern states. All the southern states except Kerala have kept their

fiscal variables (as a percent of GSDP) well within the prescribed limit as per FRLs particularly

for deficit indicators and liabilities. Even though, fiscal indicators as % to GSDP are within the

limit, it is important to know and keep a check on its growth rate. To measure the impact of FRL

on fiscal variables (on its growth), time series econometrics, particularly dummy variable method

was used for the analysis. The result showed that there are some significant variations in fiscal

indicators, however, it is state specific. For Andhra Pradesh, impact of FRL on select fiscal

indicators is not significant except for social service spending. Karnataka which lead in formation,

31

implementation of FRL is clearly denoted in its performance. Even though there was no significant

change in deficit indicators growth for Karnataka, growth in other variables like interest payments,

revenue expenditure, non-development expenditure have significantly come down whereas growth

in capital outlay, development expenditure have gone up. This clearly implies that Karnataka’s

fiscal indicators are on right track. However, Karnataka Government should be cautious that its

liabilities are growing at a much faster rate in reform period than before and hence require careful

handling of the same.

Significant impact of FRL was also seen on Kerala State finances. Liabilities, interest payments

have declined whereas development expenditure and capital outlay have gone up significantly.

However, as a percent to GSDP capital outlay has declined in reform period. There are certain

similarities between Tamil Nadu and Kerala in the fiscal performance in reform period. Contrary

to the expectations, deficits are growing at a faster rate for Tamil Nadu and Kerala. Karnataka is

the only state in which growth of non-development expenditure has declined significantly in

reform period, in other states there were no significant changes.

These results have several policy implications. Southern states except Karnataka were not able to

reduce growth in non-developmental expenditure significantly after the reforms. Capital outlay

part was the most affected portion of expenditure. States could achieve the fiscal consolidation

targets due to better economic growth and consequent tax buoyancy in early reform period and

also by cutting capital outlay. States must strictly adhere to existing fiscal consolidation roadmap

without amending it several times in order to achieve the laid down targets. Breaks in the laid road

map would certainly result in unsustainable deficits and debt in near future.

32

Bibliography

Chakraborty, P. (2005). Debt Swap Schemes in Low Interest Rate Regime: Unequal Gains and Future

Worries. Economic & Political Weekly, 40, 4357-4362.

Chakraborty, P., & Dash, B. B. (2013). Fiscal Reforms, Fiscal Rule and Development Spending: How Indian

States have Performed? NIPFP Working Paper-122.