Government of Karnataka - fpibangalore.gov.in · Disaster Management ... Government of Karnataka....

64

Government of Karnataka Fiscal Architecture of India: A Comparative Study of Finance Commission Reports (13th & 14th) Fiscal Policy Institute Centre for Financial Accountability and Decentralisation

Transcript of Government of Karnataka - fpibangalore.gov.in · Disaster Management ... Government of Karnataka....

Government of Karnataka

Fiscal Architecture of India:

A Comparative Study of Finance Commission Reports

(13th & 14th)

Fiscal Policy Institute

Centre for Financial Accountability and

Decentralisation

2

Table of Contents

Preface .......................................................................................................................................................... 4

1. Executive Summary .................................................................................................................................. 5

2. List of Acronyms ...................................................................................................................................... 8

3. List of Tables .......................................................................................................................................... 11

4. List of Figures ......................................................................................................................................... 12

5. Introduction ............................................................................................................................................. 13

5.1. About the 14th Finance Commission ................................................................................................ 13

6. Objectives of the Study ........................................................................................................................... 15

7. Literature Review .................................................................................................................................... 16

8. Methodology Adopted ............................................................................................................................ 20

9. Findings and Discussion ......................................................................................................................... 21

9.1. Tax Devolution from the Union to the States .................................................................................. 21

9.1.1. Sharing of Union Taxes Comparison ........................................................................................ 22

9.1.2. Understanding the Degree of Tax Devolution Proposed by the 14th Finance Commission ...... 23

9.2. Local Bodies and Local Governments ............................................................................................. 25

9.2.1. Observations about the State Finance Commissions (SFCs) by the 13th Finance Commission 25

9.2.2. Reforms Suggested by the 14th Finance Commission to Strengthen the Local Bodies ............ 25

9.3. Grants-in-Aid ................................................................................................................................... 26

9.3.1. Grants-in-Aid Comparison ........................................................................................................ 27

9.3.2. Understanding Need-based Grants ............................................................................................ 27

9.4. Public Utilities ................................................................................................................................. 28

9.4.1. Public Utilities Comparison ...................................................................................................... 29

9.5. Public Sector Enterprises ................................................................................................................. 30

9.6. Co-operative Federalism .................................................................................................................. 32

9.6.1. Co-operative Federalism Comparison ...................................................................................... 32

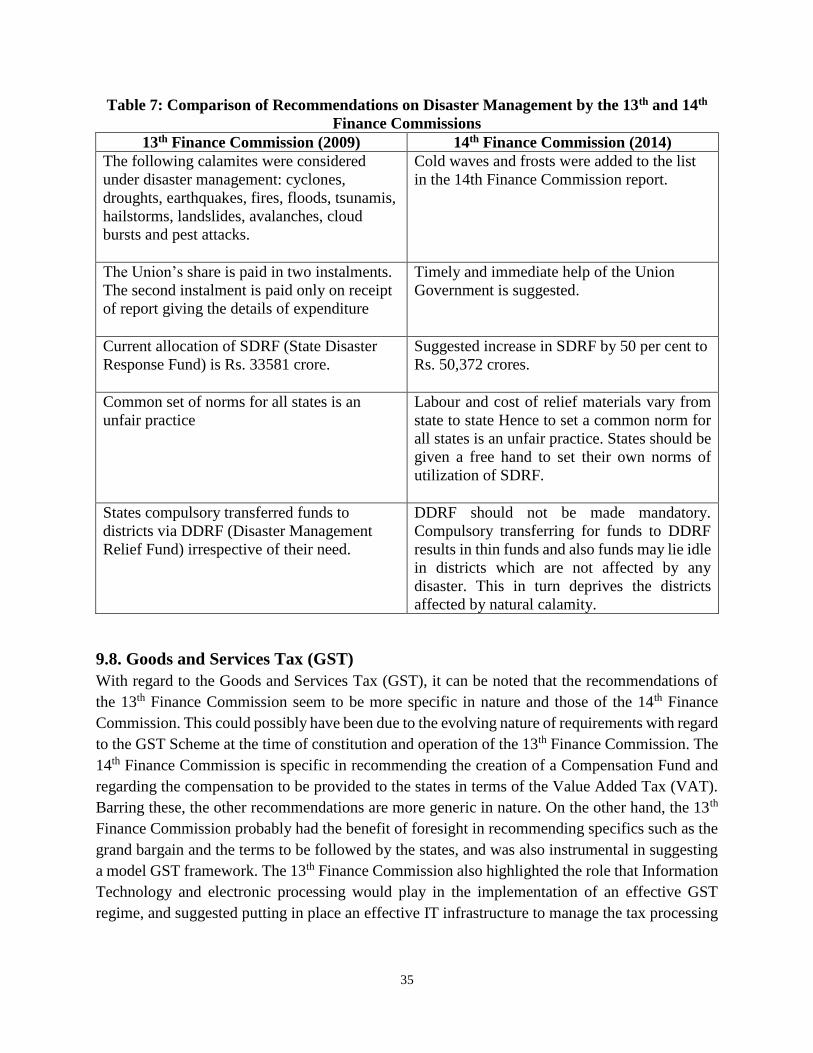

9.7. Disaster Management ....................................................................................................................... 34

9.7.1. Disaster Management Comparison ........................................................................................... 34

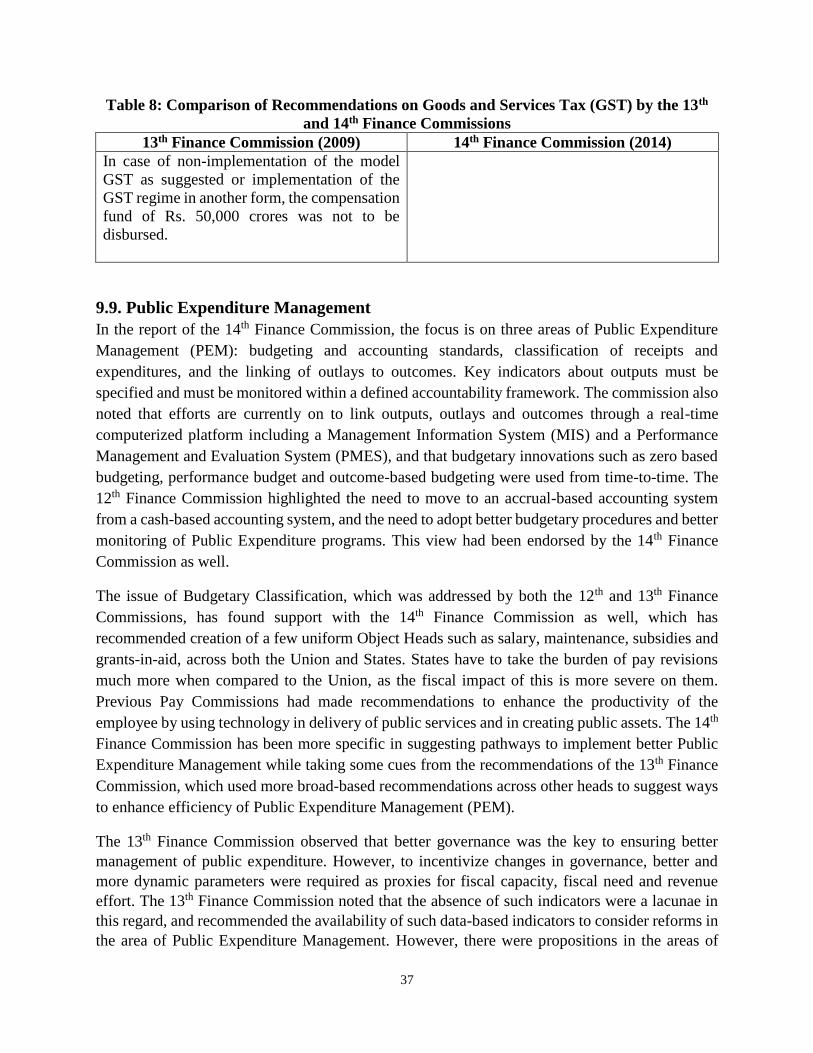

9.8. Goods and Services Tax (GST) ....................................................................................................... 35

9.8.1. Goods and Services Tax (GST) Comparison ............................................................................ 36

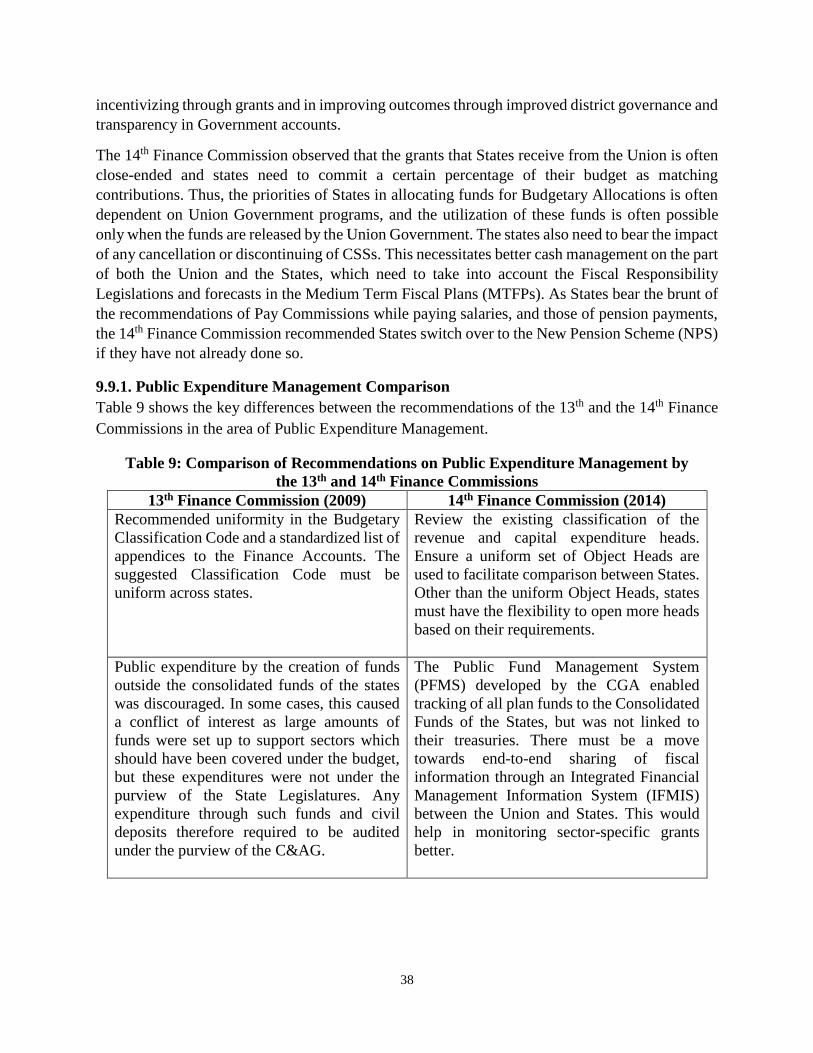

9.9. Public Expenditure Management ..................................................................................................... 37

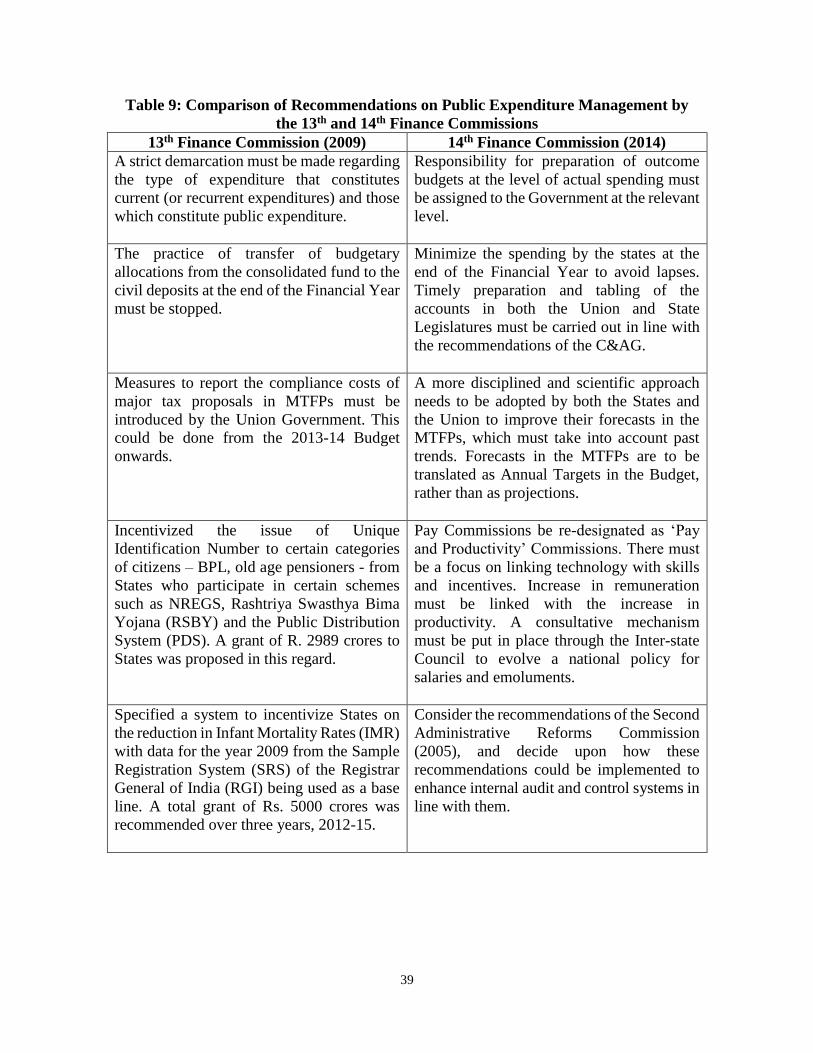

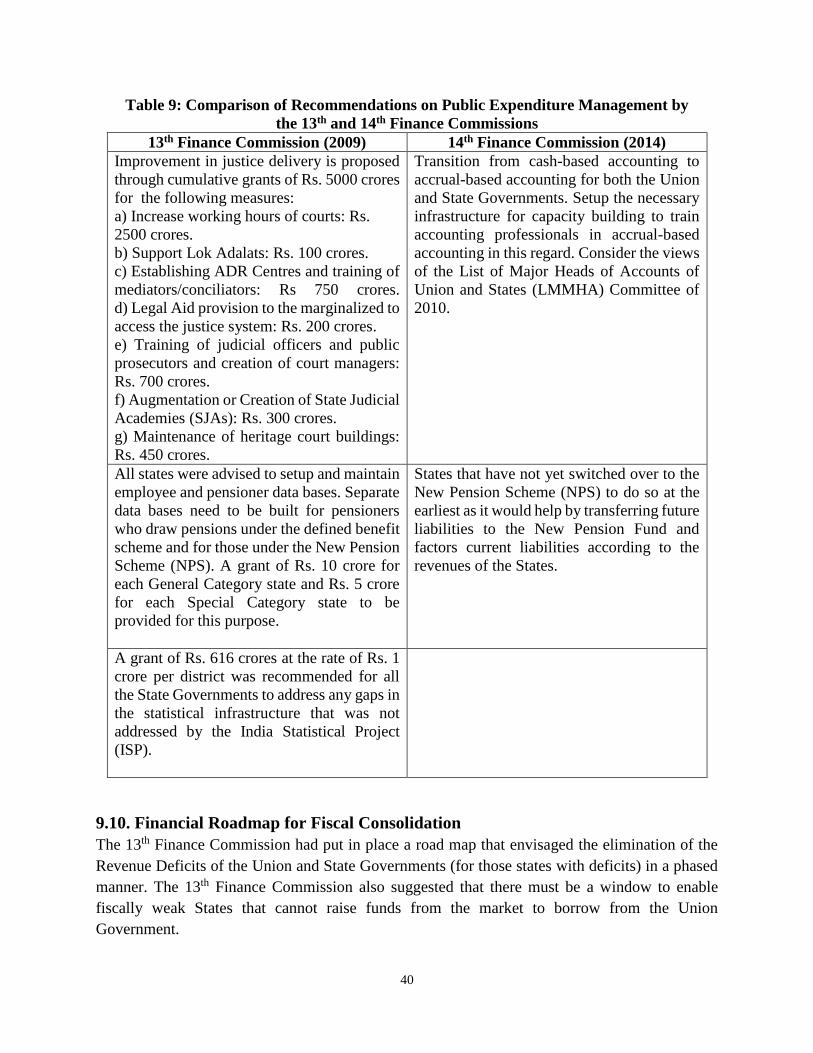

9.9.1. Public Expenditure Management Comparison .......................................................................... 38

3

9.10. Financial Roadmap for Fiscal Consolidation ................................................................................. 40

9.10.1. Financial Roadmap for Fiscal Consolidation Comparison ..................................................... 41

10. Observations on Compliance ................................................................................................................ 44

10.1. Observations Regarding Compliance in the MTFP 2013-17 of Karnataka with regard to

Recommendations of the 13th Finance Commission ............................................................................... 44

10.1.1. GSDP Calculation ................................................................................................................... 44

10.1.2. Adherence to Fiscal Responsibility ......................................................................................... 44

10.1.3. Debt Sustainability Indicators ................................................................................................. 44

10.1.4. Other Issues ............................................................................................................................. 45

10.2. Observations Regarding Compliance in the MTFP 2015-19 of Karnataka with regard to

Recommendations of the 13th and 14th Financial Commissions ............................................................. 45

10.2.1. General Overview of the Economy ......................................................................................... 45

10.2.2. Creation of the Fiscal Management Review Committee and its Observations ....................... 45

10.2.3. Key Fiscal Challenges for the State of Karnataka .................................................................. 46

10.2.4. Sharing of Union Taxes .......................................................................................................... 47

10.2.5. Centrally Sponsored Schemes (CSSs) .................................................................................... 47

10.2.6. Gross State Development Product (GSDP) Calculation ......................................................... 48

10.2.7. Adherences to Fiscal Responsibility Legislations (FRLs) ...................................................... 49

10.2.8. Debt Sustainability Indicators ................................................................................................. 50

10.2.9. Plan and Non-plan Expenditure .............................................................................................. 50

10.3. Observations Regarding Compliance in the MTFP 2016-2020 of Karnataka with regard to

Recommendations of the 13th and 14th Financial Commissions 10.3.1. Revision in Methodology of

GSDP Estimation and Calculation .......................................................................................................... 51

10.3.2. Debt Sustainability Indicators ................................................................................................. 51

10.3.3. Constitution of the 4th Karnataka State Finance Commission (SFC) ...................................... 51

10.4. Implementation of the Recommendations of the 13th and 14th Finance Commissions by the

Karnataka State Finance Commission (SFC) .......................................................................................... 51

11. Conclusion .......................................................................................................................................... 533

12. REFERENCES ................................................................................................................................... 544

13. Appendices .......................................................................................................................................... 577

13.1. Understanding IFMIS and PFMS ................................................................................................ 577

13.2. States with ratio values of own taxes/GSDP closer to that of Karnataka .................................... 578

4

Preface

This report, titled Fiscal Architecture of India: A Comparative Study of Finance Commission

Reports (13th & 14th), is the outcome of a research study through a short-term consultancy

engagement with the Fiscal Policy Institute (FPI), Government of Karnataka. This research study

was undertaken with a view to understand the implications of the approach followed by the 14th

Finance Commission in addressing issues along different dimensions and how it differed in doing

so from its predecessor, the 13th Finance Commission.

The 14th Finance Commission, which was a constitutionally mandated body headed by Dr. Y. V.

Reddy, was noted for its change in approach and degree of devolution of taxes. A more

comprehensive view to understand the differences between the recommendations of the 13th and

the 14th Finance Commissions was adopted by comparing the recommendations made in 10 areas.

In addition to this, how these recommendations impacted the state of Karnataka and the degree of

compliance by the state in terms of guidelines outlined in the applicable Medium Term Fiscal

Plans (MTFPs) for the time period were also examined. Important sections of academic literature

on Finance Commissions from the time-period of around the 13th Finance Commission were

summarized.

Dr. Kishinchand Poornima Wasdani was the short-term consultant who undertook this study by

compiling and analysing the required literature in the allotted span of time. This report is an

original work done by the short-term consultant and is the intellectual property of the FPI. The

findings of this study have been presented only at an event at the FPI to a restricted audience, and

have not been presented to other academic bodies or at any seminar or conference.

Shri. K. K. Sharma, IPoS

Adviser & Faculty, FPI

Smt. Prachi Pandey, IA&AS

Director FPI

5

1. Executive Summary

The 14th Finance Commission, headed by Dr. Y. V. Reddy, has been in the news for its departure

from tradition in terms of the methodology and degree of tax devolution to the states. It is often

mentioned that this commission proposed the highest percentage of tax devolution in fiscal history.

Although this is one of the primary reasons, there are many other areas in which the 14th Finance

Commission has made significant changes in the mode and focus of issues to be addressed, when

compared to its immediate predecessor, the 13th Finance Commission, which was headed by Prof.

Vijay L. Kelkar.

This study is an attempt to examine the differences in the recommendations proposed by the 13th

and the 14th Finance Commissions in ten different areas, namely: (i) sharing of union taxes; (ii)

local governments; (iii) grants-in-aid; (iv) pricing of public utilities; (v) public sector enterprises;

(vi) co-operative federalism; (vii) disaster management; (viii) goods and services tax (GST); (ix)

public expenditure management; and (x) financial roadmap for fiscal consolidation.

The 14th Finance Commission took into account a more dynamic approach towards population

and considered forest cover to be an important parameter while ignoring past fiscal discipline when

proposing the weights to be used for devolution. Although the proposed devolution figure of 42

per cent is 10 per cent higher than the figure proposed by the 13th Finance Commission, the degree

of difference in actual devolution may be around 3 per cent, as the total devolution by the previous

Finance Commission, when considering grants as well, would have been around 39 per cent. While

the 13th Finance Commission was harsh in its observations with regard to constitution and

recommendations of the State Finance Commissions (SFCs), the 14th Finance Commission

focused more on strengthening local bodies through innovative taxation proposals.

The structure of grants-in-aid has been significantly altered by the 14th Finance Commission, as

the previous Finance Commission had grants divided into plan and non-plan expenditure. In view

of the increased degree of devolution, the states are now free to decide on deployment of funds

with the additional fiscal space available. The 14th Finance Commission also made some key

recommendations in the use and pricing of public utilities such as electricity, transportation and

water. The 13th Finance Commission had highlighted some key lacunae in these areas, while the

14th Finance Commission proposed more concrete measures in terms of amendments of

legislations, setting up of authorized bodies, tariff revision and metering of consumption.

While the 13th Finance Commission made observations about the sorry state of the performance

of the Public Sector Units (PSUs) and proposed divestment in terms of their land holdings and

assets and increased monitoring by the Union, the 14th Finance Commission endorsed the view

and made proposals about more concrete methods to classify the PSUs and modes of divestment.

6

With the creation of the NITI Aayog which has replaced the erstwhile Planning Commission, the

outcome is an advisory body which cannot monitor the utilization of funds in the state.

The 13th Finance Commission was of the view to restore formula-based plan transfers and of

creating a new state finances division in the Ministry of Finance (MoF) to advise the Government

on centre-state fiscal arrangements and financial relations. In the background of the changing

relationship between the centre and the states, the 14th Finance Commission took a more

progressive view and proposed new institutional arrangements for strengthening and monitoring

the grants in important sectors identified among public services, emphazised the role of the

availability of natural resources to states in fiscal policy making, and proposed the expansion of

powers of the Inter-state Council. The 14th Finance Commission has also proposed innovative

ways of funding to augment the National Disaster Response Fund (NDRF), more freedom to the

states in the utilization of the State Disaster Response Fund (SDRF) and making the District

Disaster Response Fund (DDRF) non-mandatory as the needs of disaster-prone districts could be

different.

A key issue that is under discussion these days (in view of the recent Constitutional Amendment)

is that of the Goods and Services Tax (GST). While comparing the recommendations of the 13th

and the 14th Finance Commissions on GST, it could be noted that the recommendations were more

specific in case of the 13th Finance Commission, which suggested a grand bargain between the

Union and the States, the creation of a model GST framework, and the use of Information

Technology (IT) in managing tax processing effectively. While citing its inability to estimate the

losses to the states due to the absence of a Revenue Neutral Rate (RNR), the 14th Finance

Commission did recommend the provision of VAT compensation to the states along with suitable

temporary and long-term arrangements to enable the introduction of the GST regime.

Both the 13th and the 14th Finance Commissions supported streamlining of budgetary

classification in Public Expenditure Management (PEM). Both Commissions were of the view that

the Medium Term Fiscal Plans (MTFPs) of states could be used for better monitoring and

forecasting. The 13th Finance Commission was more focused on enforcement of fiscal discipline

and incentivization for the states on indicators of public scheme implementation, public health,

and provision of better judicial services, and recommended that states setup and maintain

employee and pensioner data bases for those under the old and new pension schemes. Some

innovative proposals by the 14th Finance Commission in this regard were the transition from cash-

based accounting to accrual-based accounting, the use of IT to create an Integrated Financial

Management Information System between the Union and the States, and the re-organization of

Pay Commissions as Pay and Productivity Commissions.

Given the classification of states and their special needs, the issue of managing deficits is often a

sensitive one. While the 13th Finance Commission was of the view that the Revenue Deficit of the

Union was to be reduced progressively and altogether eliminated by 2013-14, the 14th Finance

7

Commission was more specific in terms of the targets of Fiscal and Revenue Deficits of the Union

Government and in specifying eligibility norms for borrowing by the States in terms of their fiscal

discipline. However, both the Finance Commissions were of the view that the Fiscal Responsibility

and Budget Management (FRBM) Act needed to be amended to enable better fiscal consolidation

in view of an economically volatile environment and supported the creation of an independent

Fiscal Council to assess and monitor the implementation of fiscal policies.

Another aspect of this study involved the review of academic literature around the

recommendations of the 14th and previous Finance Commissions, from roughly around the last 15

years. The literature review has provided critical insights into the issues faced by the country in

the context of addressing issues of state deficits, bettering centre-state relations, and different

modes of devolution from the Union to the States.

The third aspect involved in this study has been the examination of the steps taken by the state of

Karnataka with regard to the recommendations of the 14th and previous Finance Commissions.

Interestingly, due to overlapping of the terms of the 3rd and 4th Karnataka State Finance

Commissions (SFCs) with those of the 13th and 14th Finance Commissions, a situation has been

created wherein the recommendations of these two Finance Commissions need to be adequately

reflected in the SFC Reports. Therefore, the Medium Term Fiscal Plan (MTFP) of the Government

of Karnataka which were applicable for the afore-mentioned time periods were selected and

compliances and steps taken in line with the recommendations of these Commissions were studied.

Although Karnataka has one of the best ratio values for States Own Tax Revenues (SOTR)/GSDP

as a percentage, there is scope for significant improvement in the revenues from non-tax receipts.

Also, the revenue surplus can come down due to increasing subsidy burdens and committed

expenditure (on salaries, pensions and interest payments). This points towards the requirement of

moderation in subsidy spending by the state.

Though the revenue scenario in Karnataka can be improved, the state is taking progressive steps,

as exhibited by the enactment of Fiscal Responsibility Legislations (FRLs) and the use of newer

methodologies to calculate the GSDP. The indicators and ratios for the state were found to be

better than the prescribed FRL norms. The debt sustainability indicators are also healthy. However,

the change in the mode of disbursal by the 14th Finance Commission has affected the state

adversely with regard to funding for schemes.

8

2. List of Acronyms

Acronym Expansion

ADR Alternative Dispute Resolution

AMTM Assam, Meghalaya, Tripura and Mizoram

ATF Aviation Turbine Fuel

ATR Action Taken Report

BE Budget Estimate

BPL Below Poverty Line

C&AG Comptroller and Auditor General of India

CGA Controller General of Accounts

CSF Consolidated Sinking Fund

CSO Central Statistical Office

CSS Centrally Sponsored Scheme

CSR Corporate Social Responsibility

CST Central Sales Tax

DDRF District Disaster Response Fund

DES Directorate of Economics and Statistics, Government of Karnataka

DMF Disaster Mitigation Fund

DRF Disaster Response Fund

EU European Union

FC Finance Commission

FD Fiscal Deficit

FMRC Fiscal Management Review Committee

FRBM Fiscal Responsibility and Budget Management

FRL Fiscal Responsibility Legislation

FY Financial Year

GDP Gross Domestic Product

GoI Government of India

GSDP Gross State Domestic Product

GST Goods and Services Tax

GVA Gross Value Added

HDI Human Development Indicator

HSD High Speed Diesel

IFMIS Integrated Financial Information Management System

IMR Infant Mortality Rate

IP Interest Payments

ISC Inter-state Council

9

Acronym Expansion

ISP India Statistical Project

IT Information Technology

KFR Karnataka Fiscal Responsibility

LMMHA List of Major and Minor Heads of Accounts of Union and States

MCA Ministry of Corporate Affairs

MIS Management Information System

MoF Ministry of Finance

MS Motor Spirit

MTFP Medium Term Fiscal Plan

NCCF National Calamity and Contingency Fund

NDRF National Disaster Response Fund

NIF National Investment Fund

NITI National Institution for Transforming India

NPS New Pension Scheme

NREGS National Rural Employment Guarantee Scheme

NSS National Savings Scheme

NSSF National Small Savings Fund

NSSO National Sample Survey Office

NWMA Normal Ways and Means Advances

OG Outstanding Guarantee

OGD Open Government Data

PDS Public Distribution System

PEM Public Expenditure Management

PFMS Public Fund Management System

PMES Performance Management and Evaluation System

PPP Public-Private Partnership

PRI Panchayat Raj Institution

PSU Public Sector Unit

RBI Reserve Bank of India

RD Revenue Deficit

RE Revised Estimate

RGI Registrar General of India

RNR Revenue Neutral Rate

RoI Return on Investment

RR Revenue Receipts

RSBY Rashtriya Swasthya Bima Yojana

RTA Rail Tariff Authority

SDRF State Disaster Response Fund

SERC State Electricity Regulatory Commission

10

Acronym Expansion

SFC State Finance Commission

SJA State Judicial Academy

SOTR State's Own Tax Revenues

SPG State Plan Grant

SPSU State Public Sector Unit

SRS Sample Registration System

STPI Software Technology Parks of India

STT Security Transaction Tax

SWMA Special Ways and Means Advances

TL Total Liabilities

ToR Terms of Reference

UID Unique Identification Number

ULB Urban Local Body

USA United States of America

UT Union Territory

VAT Value Added Tax

WRA Water Regulatory Authority

11

3. List of Tables

Table No.

Table Description

Table 1 Parameter Weights adopted by the 13th and 14th Finance

Commissions (in per cent)

Table 2 Comparison of Recommendations on Sharing of Union Taxes by

the 13th and 14th Finance Commissions

Table 3 Comparison of Recommendations on Grants-in-Aid by the 13th

and 14th Finance Commissions

Table 4 Comparison of Recommendations on Public Utilities by the 13th

and 14th Finance Commissions

Table 5 Comparison of Recommendations on Public Sector Enterprises by

the 13th and 14th Finance Commissions

Table 6 Comparison of Recommendations on Co-operative Federalism by

the 13th and 14th Finance Commissions

Table 7 Comparison of Recommendations on Disaster Management by the

13th and 14th Finance Commissions

Table 8 Comparison of Recommendations on Goods and Services Tax

(GST) by the 13th and 14th Finance Commissions

Table 9 Comparison of Recommendations on Public Expenditure

Management by the 13th and 14th Finance Commissions

Table 10 Comparison of Recommendations on Financial Roadmap for

Fiscal Consolidation by the 13th and 14th Finance Commissions

Table 11 Adherence to Fiscal Responsibility Legislations by the State of

Karnataka

Table 12 SOTR as a percentage of GSDP for Five Selected States/UTs from

2009-10 to 2013-14

Table 13 Aggregate Subsidies and Transfers reported by Tamil Nadu in the

Medium Term Fiscal Plan 2011-12 (Indian Rupees in crores)

Table 14 Subsidy Spending by Four Selected States from 2009-10 to 2014-

15 (Indian Rupees in crores)

12

4. List of Figures

Figure No. Figure Description

Figure 1 Degree of Tax Devolution (in percentage) Proposed by

Successive Finance Commissions

Figure 2 Trends in SOTR as a percentage of GSDP for States/UTs

from 2009-10 to 2013-14

Figure 3 Trends in SOTR as a percentage of GSDP for Five Selected

States/UTs from 2009-10 to 2013-14

Figure 4 Trends in Subsidy Spending by Four Selected States from

2009-10 to 2014-15 (Indian Rupees in crores)

13

5. Introduction

After 69 years of independence and implementation of 12 Five-Year plans, the Government of

India heeded to the long standing demand of the States to give them the desired fiscal freedom to

decide upon the implementation of schemes. The 14th Finance Commission, constituted under

Article 280 of the Constitution of India, decided to devolve maximum money to States and to allow

them the freedom to plan their course of development in place of the previous practice of enforcing

the fiscal schemes from the Union. In other words, a fundamental shift in India’s Federal

relationship was made-reduction in Union-based planning (centralized planning) was replaced by

a corresponding increase in State-level planning (decentralized planning). The new Government

believes that economic development would be possible only through the development of the states

and its strong conviction about Cooperative Federalism are the major reasons behind the new

approach of the finance commission. It was with these beliefs that the recommendations of the 14th

Financial Commission have been wholeheartedly accepted.

Increased money will give the states the required freedom to tailor make the development schemes

to suit their needs. The increase in the devolution to 42 per cent would provide for a balance

between the degree of autonomy of states in determining their expenditures and yet allow for the

centre to make certain specific-purpose grants to the states. The 14th Finance Commission has also

addressed the request of the States to reduce the number of Centrally Sponsored Schemes (CSS)

as well as the outlays on them. This gives an extra physical space to the states to create productive

capital assets.

The rationale behind these changes lies in the weakening of the planning process. The chairperson

of the Finance Commission Dr. Y.V Reddy was probably aware that there were plans to abolish

the Planning Commission which was in charge of the Centrally Sponsored Schemes (CSSs) and

State plan grants, due to its continuous defiance to the directives to empower the States in line with

the needs of the modern economy. In view of the above, some degree of responsibility of planning

for the states was delegated to the respective states. Devolution of taxes and powers have also been

carried out in response to the desire of the states to allow them the desired freedom of planning

and implementation.

5.1. About the 14th Finance Commission

The 14th Finance Commission was constituted under the orders of the President of India in line

with Article 280 of the Constitution on 2nd January 2013, and submitted its report on 15th December

2014. The Commission was chaired by Dr. Y. V. Reddy, former Governor of the Reserve Bank of

India (RBI). The recommendations of this Finance Commission would be implemented over a

period of five years, from 1st April 2015 to 31st March 2020. The major functions of the Finance

Commission are:

14

(i) Tax devolution from the Union to the States: The Finance Commission governs the total

transfer of the taxes from the union to the states. It includes tax devolution under Article 280 and

Grants-in Aid under Article 275 of the Constitution.

(ii) Advisory role in financial assistance to Panchayat Raj Institutions (PRI) and Municipalities:

The decision of funding Panchayat Raj Institutions and Municipalities would be undertaken under

the prerogative of State Financial Commissions using the Consolidated Fund of the States. In order

to strengthen the finances of the States so that effective financial assistance could be provided to

Panchayat Raj Institutions (PRI) and Municipalities, the Financial Commission plays an advisory

role.

(iii) Grants-in-Aid (under Article 275): Finance commission is in charge of prescribing the norm

and the quantum of grants in line with the needs of States. In principal, it is the special purpose

grants (or Gap-filling Gants) given to States to meet the difference between the assessed

expenditure on the non-plan revenue account of each State and the projected revenue including the

share of a State in Central Taxes.

(iv) Other Functions: The other functions include all other matters referred by the President of

India. In case of the 14th Finance Commission, the matters referred include the following:

(i) Pricing of public utilities – how much to levy and how to levy.

(ii) Fiscal Deficit Review of both the Union and States

(iii) Disinvestment of the PSUs

(iv) Goods and Services Tax

(v) Climate change and sustainable development

15

6. Objectives of the Study

The main objectives of this research study were:

1) Comparison of the 13th and 14th Financial Commission Report on the following parameters:

(i) Sharing of Union Taxes

(ii) Local Governments

(iii) Grants-in-Aid

(iv) Pricing of Public utilities

(v) Public sector enterprises

(vi) Co-operative Federalism

(vii) Disaster Management

(viii) Goods and Services Tax (GST)

(ix) Public expenditure management

(x) Financial Roadmap for Fiscal Consolidation

2) Discussions on the changes in the new Finance Commission report (14th): Alterations in the

existing schemes, deletions of existing schemes or policies and additions of new schemes and

policies if any.

3) Review of the existing academic literature on the 13th and 14th Finance Commissions.

4) Discussion on the operationalization of the recommendations of the Finance Commissions in

the State of Karnataka by considering the references made to these in the applicable Medium Term

Fiscal Plans (MTFPs).

16

7. Literature Review

This section highlights important reviews of academic literature in the context of challenges and

reforms from the time period of the constitution of the 13th Finance Commission and onwards.

Gurumurthi (2003) noted that gap filling approach followed by Eleventh and other previous

finance commissions had resulted in penalizing fiscally prudent states and in rewarding fiscally

in-disciplined states. It was observed that many countries such as Argentina, Hungary, Indonesia

and others have avoided the gap filling approach of fiscal transfers to their provinces. Another

area which required critical examination was the need to continue the current redistribution

between plan and non-plan expenditure in the budgetary classification. Isaac and Chakraborty

(2008) opined that 12th Finance Commission had witnessed an increase in the share of conditional

and tied transfers to the states and concluded that the existing inter-governmental transfer system

has resulted in an increasing vertical imbalance, conditional and tied grants through various

Centrally Sponsored Schemes, and posed a question mark to the basic autonomy of states. There

existed a need to develop an incentive-compatible transfer system by keeping in mind sub-national

fiscal autonomy. Asymmetric application of financing constraints on centre and states through

restrictions on sub-national borrowings was common in federal countries. Countries such as

Australia and Germany followed a co-operative framework for design and implementation of debt

control while USA followed rule-based control. Lahiri (2000) noted that India followed

administrative control and hard budget constraints had kept State deficits in check but also that the

Centre needs to improve its own fiscal discipline. Regarding sub-national fiscal rules, there were

two basic approaches: In the autonomous approach, the initiative for establishing rules arose from

individual sub-national governments, while in a coordinated approach, all sub-national

governments would be subject to uniform rules to ensure fiscal discipline under the surveillance

of central authority. In this regard, Kopits (2001) had stated that the autonomous approach adopted

in the bill without mentioning state or local jurisdiction seems a logical choice for India. However,

poor fiscal performance of some states and mixed success with past bailouts could press the case

for a co-ordinated approach.

As the vertical and horizontal imbalance among the different sub-national governments could lead

to uneven development of the economy, Hajra et al. (2008) suggested a few options. The 13th

Finance Commission should emphasize on the requirement of the quality of the fiscal adjustment

for higher capital expenditure and enhancement of infrastructure and social sector spending with

beneficial impact on growth and employment. It was also suggested that in the process of fiscal

transfers, the 13th Finance Commission could opt to include the efforts to increase non-tax revenue

as a criterion for horizontal devolution and could give due weight to the need to enhance social-

sector expenditure as a criterion for horizontal sharing. More purpose-specific grants which could

enable enhancement in the level of human development across the states could be considered in

addition to abolishing the post-devolution non-plan revenue deficit grant in view of the elimination

of revenue deficit in the post-FRL phase.

17

Based on a study of budget 2008-09, Ganguly (2009) attempted to address some issues before the

13th Finance Commission and tried to fill the gap in RBI’s assessment of state finances. Due to

recession and other factors, there was an imminent squeeze on the fiscal domain of the states and

as other committed expenditures were about to rise, states needed to undergo larger tax reforms

for broadening their tax base and softening of their fiscal targets for the short-term. Moreover, it

was required to reconsider the channel of the fund transfers from centre to states and thus centre-

state relations. In that continuation of the framework suggested by Ganguly (2009), Pethe (2009)

stated that the 13th Finance Commission needed to devise a formula that moves towards incentive

compatibility. Emphasis was laid on devolving greater proportion to states, given their mandate

for provision of social-sector public goods, diminishing discretionary fiscal space, and assigning

greater weight to the efficiency criteria within the statutory devolution formula. Further, the paper

suggested the computation of income-distance criterion by keeping in mind the intra-state variation

and that decentralization must be strengthened by adding a criterion to the statutory devolution

formula (Pethe, 2009).

Rao et al. (2008), studying the 13th Finance Commission, argued that as far as the transfer system

was concerned even if it may be difficult to make drastic changes in the relative shares of the

states, the commission should give up the tax filling approach. Though it was difficult to change

the share of the states in its recommendations, a paradigm shift could be made to change structure

of incentives and accountability could be included as an inherent part of the transfer system and

this could fully equalize expenditure on basic healthcare and education. While analyzing the 13th

Finance Commission, Chakraborty (2010) concluded that while the proposed increase in vertical

share would help the states, the horizontal distribution formula did not seem can make any

progressivity of transfers. The design of the horizontal distribution formula was such that the fiscal

capacity distance and index of fiscal discipline are in conflict with each other as the former tries

to increase the capacity of the states to spend more and the latter tries to limit their expenditure in

relation to own revenues. Reddy (2009) stated that the 13th Finance Commission was constrained

in making a realistic assessment of the resources and expenditure needs of the centre and the state.

A two-year period was recommended instead of a five-year period, as, during fiscal crisis resource

transfer to states may witness a contraction and it would be unfair to bind the states to such a

dispensation for five years.

Chakraborty (2010) noted that the approach and framework followed by the 13th Finance

Commission with regard to horizontal distribution, the revised road map for fiscal consolidation,

the design of grants to local bodies and various other specific transfers was different from that of

earlier Finance Commissions (FCs). The other strengths of the 13th Finance Commission were the

direct measure of fiscal capacity rather than the per capita income and its use in horizontal

distribution formula and the granting of a predicable share of resources from the central pool of

taxes to local bodies, unlike the ad hoc grants of absolute amount awarded by the earlier FCs.

However, it was also noted that the 13th Finance Commission undermined the fiscal autonomy in

case of bodies in lower levels of Government in a multi-level financial system, and some grants,

18

such as those for elementary education, had design problems and could not augment expenditure.

Further, the road map for fiscal consolidation that provides different fiscal adjustment paths to

different states to reach the target of a fiscal deficit of 3 per cent of GDP can be questionable. This

reinforces the view of the 12th Finance Commission, however, this should not be imposed as state-

specific levels of sustainable deficit differ depending on state-specific growth, the interest rate on

debt and the level of primary deficit.

Chakraborty and Bhadra (2010) noted that the economic recession had resulted in a decline in

fiscal transfers, and that stagnant revenue buoyancy has compressed fiscal space of the states.

Even after increasing the limits of the state level market borrowings, the sub-national fiscal

imbalance did not seem to be solved. The paper concluded that the 13th Finance Commission’s

recommendations of incentive grants linked to adherence to these state-specific adjustment paths

of main fiscal variables like revenue deficit, fiscal deficit and the outstanding debt to GSDP ratio

may impose unnecessary rigidities in state-level fiscal operations. A critique by Dholakia (2010)

on the research by Chakraborty and Bhadra (2010) said that a state’s role was very limited and was

not very significant, and that economic crises are better addressed at the national levels as was

demonstrated by the financial crisis. Even if states had their own fiscal agenda, they needed to

address medium and long-term fiscal objectives rather than short-term objectives. Dholakia (2010)

analyzed two important aspects of the recommendations of the 13th Finance Commission. The

increase in the weight of the Index of Financial Discipline from 7.5 per cent to 17.5 per cent in the

tax devolution scheme by dropping the tax-GSDP ratio, and the Fiscal Capacity Criterion (with

47.5 per cent weightage) replacing the equalization objective of the 12th Finance Commission

which had 50 per cent weightage. Such changes were not desirable as their outcomes would not

be satisfactory, with richer states receiving increased tax shares and relatively low-income states

receiving very low share of allocations.

The 13th Finance Commission has forayed much beyond the domain of a FC by recommending as

many as 12 different types of grants with a host of conditionalities. However, as per Rao G (2010),

response to the report has been muted and there is hardly any serious analysis and discussion except

on the recommendations related to GST. The other major concern of the 13th Finance Commission

Report is the abundance of conditionalities imposed and the questions over the design and

implementations of these conditions, in addition to monitoring compliance. As a result, some

states have raised the issue of autonomy as it may not be possible to implement all conditionalities.

Moreover, some of the conditions can be met only in long-term and not in the award period of 13th

Finance Commission. It is questionable how conditions could be enforced when there are no

incentives, as State Governments and local bodies could lose grants if the conditions are not

fulfilled. Regarding GST regime, there should be some freedom and choices to the states. Rao K

(2010) noted that it was desirable to retain some commitments on the same. The classification of

goods and services in to different categories should remain the same across all States and at the

Union Government-level, and there should be harmonization in compliance and administration.

For the floor rates, references could be taken from Canada or the European Union (EU). Das-Gupta

19

(2010) criticized the 13th Finance Commission for not having chosen the best possible route to

ensure public expenditure more outcome-oriented, even though a number of suggestions were

made in its report to achieve output-oriented outlays.

Kumar (2015) observed that the recommendations of the 14th Finance Commission had brought in

a new era of co-operative federalism between the Union and States. Grants to local bodies and to

11 states that had a revenue deficit would provide a huge fillip, but would also discourage the

Union to become involved in the affairs of the states henceforth. Sharma (2015), in a study on

federalism, has also noted that the true essence of collaborative federalism would work only when

there are “balanced, transparent and distortion-free system of inter-governmental fiscal relations”.

By considering both the plan and non-plan share of revenue requirements in the divisible pool,

there will be a burden on the Union which would lose Rs.1 50,000 crore to the States in 2015-16

when compared to 2014-15 (Sharma, 2015).

D’Souza (2015) reviewed the recommendations of the 14th Finance Commission, and noted a

significant difference from the earlier Finance Commissions, in that the Terms of Reference (ToR)

of the 14th Finance Commission did not restrict the Commission’s mandate only to the non-plan

revenue of the States, nor was there a requirement to consider commitment of the Union

Government to provide budgetary support to the plan. Other critical issues that helped the 14th

Finance Commission were the option to consider demographic changes since 1971, the assessment

of the Fiscal Responsibility and Budget Management (FRBM) Acts that were in force. The 14th

Finance Commission was also “obliged to review public enterprises and prioritize them”, and this

would lead to a list of non-priority public enterprises that could be put up for divestment (D’Souza,

2015).

This represented a shift in paradigm from the earlier approach of increasing plan transfers for

Centrally Sponsored Schemes (CSSs). This shift has been made without an increase in aggregate

transfers, but by a change in the composition of untied Transfers. He also observed that the 14th

Finance Commission has increased the share of untied grants to the States, enabling them to decide

on their financial future (D’Souza, 2015).

Another important change in the recommendations of the 14th Finance Commission was the move

away from the “historical distinctions between general and special category states”, while at the

same time providing for a grant of Rs. 1,94,821 crore to the North-eastern states. This was done to

account for any fiscal imbalances that could arise out of the high cost of public service delivery

and low revenue capacity. However, it was also noted that the use of the income distance formula

may not be the best manner to devolve funds, as this may not encourage the preservation of

incentives for better performance by the States during the period (D’Souza, 2015).

Regarding the Inter-state Council (ISC), D’Souza (2015) adopts a cautious tone, suggesting that it

needs to be a more consultative body to address the proposed issues of identifying sectors for

1 The abbreviation “Rs.” used in this Report denotes Indian Rupees.

20

grants and recommending resources for the North-east while taking into consideration economic

and environmental concerns. This view has found support by Sharma (2015), who suggests that

the ISC can be viewed as a “constitutional entity which can provide the institutional backing to the

vision of collaborative federalism in India.” It has been proposed that the ISC would be entrusted

with “decision-making responsibilities and tasks such as policy research and investigation”, and

must have a more expanded role, functioning as a collaborative body.

On the issue of the proposed bi-annual public debt report, especially in the context of a national

debate on the creation of a Debt Management Agency, it is critical to note that the Government

would need to manage targets for reduction in debt (medium or long-term objective) and targets

for inflation and growth (short-term objective). D’Souza (2015) has re-stated the observations of

the 14th Finance Commission, that while the role of the Union in disciplining States with regard to

fiscal discipline has been noteworthy, its own allegiance to the rules has not been impressive.

The survey by Sharma (2015) also found support a proposal to convert the Finance Commission

into a permanent body, as this would provide for annual projections and allocations with an

increased level of monitoring, which would be considerably different from the five-year

projections that are currently in vogue. Respondents also suggested that there needs to be a culture

of transparency and accountability through periodic dissemination of public information on

performance of public services.

8. Methodology Adopted

A qualitative research methodology has been used in this research study. Wherever possible, the

parameters present in the recommendations of the 13th and 14th Finance Commissions under

similar heads have been compared and presented on the basis of similarity in terms of the concerns

they intend to address. Observations on compliance by the State of Karnataka regarding these

recommendations in the applicable Medium Term Fiscal Plans (MTFPs) have been made.

Wherever necessary figures for comparable parameters have been employed and analyzed using

percentage analysis technique. Data for the study has been drawn from published academic and

Government or Government-approved sources.

21

9. Findings and Discussion

In this section, the key areas in which the prominent recommendations of the 14th Finance

Commission have been made are discussed, and have also been compared with those of the 13th

Finance Commission wherever applicable.

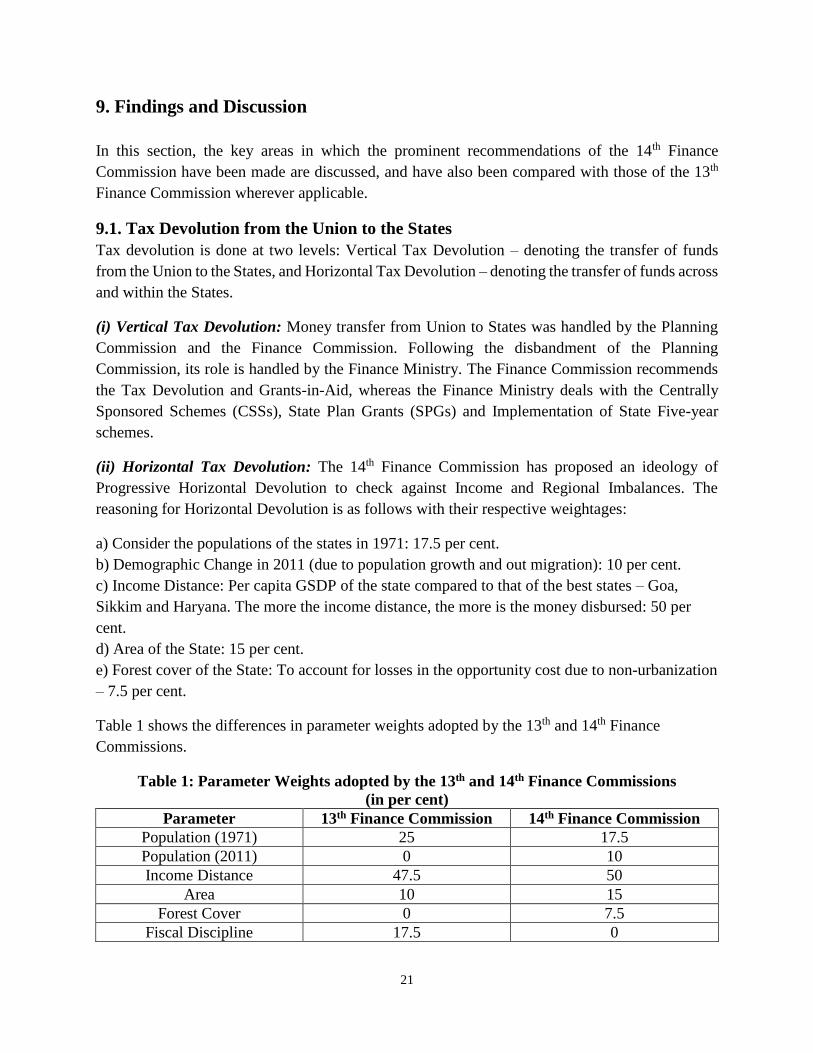

9.1. Tax Devolution from the Union to the States

Tax devolution is done at two levels: Vertical Tax Devolution – denoting the transfer of funds

from the Union to the States, and Horizontal Tax Devolution – denoting the transfer of funds across

and within the States.

(i) Vertical Tax Devolution: Money transfer from Union to States was handled by the Planning

Commission and the Finance Commission. Following the disbandment of the Planning

Commission, its role is handled by the Finance Ministry. The Finance Commission recommends

the Tax Devolution and Grants-in-Aid, whereas the Finance Ministry deals with the Centrally

Sponsored Schemes (CSSs), State Plan Grants (SPGs) and Implementation of State Five-year

schemes.

(ii) Horizontal Tax Devolution: The 14th Finance Commission has proposed an ideology of

Progressive Horizontal Devolution to check against Income and Regional Imbalances. The

reasoning for Horizontal Devolution is as follows with their respective weightages:

a) Consider the populations of the states in 1971: 17.5 per cent.

b) Demographic Change in 2011 (due to population growth and out migration): 10 per cent.

c) Income Distance: Per capita GSDP of the state compared to that of the best states – Goa,

Sikkim and Haryana. The more the income distance, the more is the money disbursed: 50 per

cent.

d) Area of the State: 15 per cent.

e) Forest cover of the State: To account for losses in the opportunity cost due to non-urbanization

– 7.5 per cent.

Table 1 shows the differences in parameter weights adopted by the 13th and 14th Finance

Commissions.

Table 1: Parameter Weights adopted by the 13th and 14th Finance Commissions

(in per cent)

Parameter 13th Finance Commission 14th Finance Commission

Population (1971) 25 17.5

Population (2011) 0 10

Income Distance 47.5 50

Area 10 15

Forest Cover 0 7.5

Fiscal Discipline 17.5 0

22

The key issues while disbursing money to the States were:

(i) Formula based unconditional transfer of taxes to the State.

(ii) Different states have different requirements, and so the approach of ‘one size fits all’ is not

correct

(iii) The Union Government would do away with the Centrally Sponsored Schemes (CSS) in

favour of new arrangement with the States to devolve mutually benefit schemes.

The key recommendation of the 14th Finance Commission is the devolution of 42 per cent of

Union taxes from the Union to the States. These taxes recommended for devolution by the 14th

Finance Commission will NOT include the following taxes:

(i) Taxes levied by the Union but collected and kept by the States under Article 268. These taxes

do not go into the Consolidated Fund of India.

Examples: Stamp Duties on cheques, promissory notes, insurance policies and share transfers.

Excise Duties on medicinal and toiletry preparations with alcohol and narcotics.

(ii) Taxes levied and collected by the Union but assigned to the States under Article 269 of the

Constitution.

(iii) Interstate Commerce - Central Sales Tax (CST) – belongs to the exporter state but is retained

by the Union.

(iv) Taxes under Article 270 and Surcharges levied under Article 271 would not fall under the

purview of devolution of taxes.

(v) Divisible Pool of Central Taxes – All the Central Taxes such as Corporation Tax, Income Tax,

Excise Duty, Service Tax, Customs Duty, STT and Wealth Tax.

This recommendation of the 14th Finance Commission represented a huge leap over the similar

recommendation made by the 13th Finance Commission, which suggested the devolution of 32 per

cent of taxes from the Union to the States. The following table discusses the difference between

the recommendations of the two Finance Commissions for the sharing of the taxes.

9.1.1. Sharing of Union Taxes Comparison

Table 2 shows the key differences between the recommendations of the 13th and the 14th Finance

Commissions in the area of Sharing of Union Taxes.

23

Table 2: Comparison of Recommendations on Sharing of Union Taxes by the 13th and

14th Finance Commissions

13th Finance Commission (2009) 14th Finance Commission (2014)

States share in net proceeds of Union Tax

revenue 32 per cent.

States share in net proceeds of Union Tax

revenue increased to 42 per cent. Highest

increase by any Finance Commission.

Rs.3,37,808 crore was transferred as tax

devolution.

Rs.5,23,958 crore to be transferred as tax

devolution.

States with high fiscal discipline

benefited.

States with high forest cover to be

benefited by horizontal devolution.

13th FC accounted for 7 per cent of net

transfers from Centre to State in ways of

grants.

14th FC scrapped away 7per cent grants

and diverted it through increase in tax

devolution.

Centrally sponsored schemes were funded

by the Union.

Through net increase in transfer to states.

States will be held responsible for

centrally sponsored schemes.

Note on Dissent by Prof. Abhijit Sen, Member of the 14th Finance Commission – Prof. Abhijit Sen

was not in agreement with quantum of tax devolution. According to him only 38 per cent of taxes

must be allocated for vertical distribution. The allocation of a high level of taxes of 42 per cent

will force the Union to cut down its plans over a period of time. Also the gap between the rich and

poor states will increase and create faults in federalism.

9.1.2. Understanding the Degree of Tax Devolution Proposed by the 14th Finance

Commission

Figure 1: Degree of Tax Devolution (in percentage) Proposed by Successive Finance

Commissions

(Source: Adapted by the author from Gurumurthi (2016))

29.00 29.50 30.5032.00

42.00

0.00

5.00

10.00

15.00

20.00

25.00

30.00

35.00

40.00

45.00

X XI XII XIII XIV

24

Figure 1 shows the trend in degrees of devolution of taxes (in percentage on the Y-axis) proposed

by successive Central Finance Commissions (from the 10th to the 14th Finance Commissions, as

represented by the respective roman numerals on the X-axis). For the span from the 10th Finance

Commission until the 13th Finance Commission, the percentage increase in devolution was 3

percentage points, i.e., from 29 per cent to 32 per cent. This has suddenly increased by 10

percentage points to 42 per cent in line with the recommendations of the 14th Finance Commission.

In mathematical terms, this presents itself to be a radical increase in devolution, especially in the

background of the incremental approach followed by the past few Finance Commissions. This has

been acknowledged to be the biggest ever increase in tax devolution (Government of India, 2015).

However, an examination of the trend alone does little to explain the actual reasoning behind this

step.

The 14th Finance Commission has shifted from the approach used by the previous Finance

Commissions regarding the devolution of taxes, in that the entire revenue expenditure needs of a

State have been considered without making a distinction between plan and non-plan expenditures

(14th Finance Commission, 2014). This was also made possible due to the distinction in the Terms

of Reference, which, unlike in the past, did not “restrict the Commission to meeting non-plan

revenue expenditure requirements alone” (Bakshi and Upadhyay, 2015; D’Souza, 2015). In view

of this comprehensive approach undertaken by the 14th Finance Commission, the Post-devolution

Revenue Deficit Grants are intended to cover the entire revenue deficits of the States, as applicable

(14th Finance Commission, 2014).

The shift in paradigm, from the earlier approach of increasing transfers for Centrally Sponsored

Schemes (CSSs) has been made possible through a difference in composition of untied transfers,

and cannot be seen only as an increase in the aggregate (D’Souza, 2015). To understand the

increase in devolution from another perspective, the total transfers (including devolution and

grants) specified by the 13th Finance Commission, was around 39 per cent (“Accelerating

devolution”, 2015). This figure is comparable to the 42 per cent devolution proposed by the 14th

Finance Commission with a shift in its approach, and does not seem to indicate a radical increase.

It is therefore, misleading to compare the recommended devolution figures specified by the 13th

and 14th Finance Commissions, according to Prof. M. Govinda Rao, member of the 14th Finance

Commission, as it does not present the full picture (Bakshi and Upadhyay, 2015). So, while there

has been a radical increase in the level of tax devolution due to the novel approach followed by

the 14th Finance Commission, only a thorough understanding of the reasoning behind the exercise

can help in determining the actual nature of increase in tax devolution.

25

9.2. Local Bodies and Local Governments

9.2.1. Observations about the State Finance Commissions (SFCs) by the 13th Finance

Commission

An earlier attempt of maintaining Fiscal disciple was by creating SFCs which did not take off very

well with the States. The 13th Finance Commission made some observations with regard to the

financial autonomy provided to the States in decision-making about the funds allocated to them

and the current state of affairs. This trend had been following based on observations from previous

commissions also:

(i) 73rd Constitutional Amendment in 1992 mandates the creation of State Financial Commissions

(SFCs) which would advise the state on distribution of funds from the State’s Consolidated Fund.

SFCs were supposed to have been constituted within a year of the amendment and thereafter at

regular intervals of 5 years. However, this has not been done at regular intervals.

(ii) The recommendations of these State Finance Commissions (SFCs) have not been implemented

by the states in the specified time-frame. It was noted that the Action Taken Report (ATR) about

the recommendations made by the State Finance Commissions (SFCs) had not been tabled in the

State Legislatures.

(iii) Some states implemented the recommendations of the SFCs, but this was not done in the

specified time-frame.

(iv) There is an observable lack of synchronicity between the State Finance Commissions and the

Finance Commission constituted by the Union Government.

9.2.2. Reforms Suggested by the 14th Finance Commission to Strengthen the Local Bodies

The 14th Finance Commission has recommended the following Tax Reforms within the States

with the objective of increasing the revenue of the State and ensure the maintenance of Fiscal

discipline in the State.

(i) States must devolve some of their taxes to the Panchayat Raj Institutions (PRIs). They could

also empower local bodies to collect taxes.

(ii) States must share the mining royalties earned in a region with the Panchayat Raj bodies in that

region. Likewise Property Tax and Advertising Tax must also be shared.

(iii) States can expand Entertainment Tax. They can either devolve the taxes earned on Cable

Television, Internet Cafes and Boat Rides to the PRIs or empower the local bodies to collect taxes

on these.

(iv) Professional Tax: It has been recommended that the Professional Tax under Article 276 of

the Constitution be raised to Rs. 12,000/- per annum when compared to the existing Rs. 2,500/-

26

per annum. Local bodies are already levying Professional Taxes in the states of Kerala and Tamil

Nadu.

(v) Property Tax

a) Property tax is often not raised with a view to keep the voters happy. However, the value of

property also rises and it must be taxed accordingly.

b) Assessment of Property Tax must be done every 4-5 years.

c) Stringent Action must be recommended against the defaulters.

d) As per Article 285(1): Union properties cannot be taxed by a state/local body. While the 13th

Financial Commission recommended that these properties be taxed, the 14th Financial

Commission has recommended that local bodies should be compensated in this exercise.

(vi) North-Eastern States

a) As per sections 9 and 9A of the 73rd amendment of the Constitution of India dealing with PRIs

and Local Bodies, the devolution of taxes does not apply to the states of Assam, Meghalaya,

Tripura and Mizoram (AMTM).

b) Article 275(1) of the Constitution needs to be amended so that the recommendations of the

14th Finance Commission for the PRI would hold.

(vii) Municipal Bonds

a) To create smart cities, there is a need for Municipal Corporation to have a corpus of funds.

b) Large Municipal Corporations are recommended to launch Municipal Bonds directly in the

market.

c) For smaller municipal corporations, the States are expected to create a market intermediary

company that would act on their behalf in the open market and handle the issue and sale of

Municipal Bonds.

(viii) Sector-specific Grants such as those for strengthening the Police and the Judiciary will not

be given anymore to the states, in view of the high degree of devolution of 42 per cent of taxes.

9.3. Grants-in-Aid

Grants-in-aid refer to grants made by the Union to the States in excess of the allocation of taxes to

the States by the Finance Commission with an objective of the Strengthening the Finance position

of urban and rural local bodies like Municipalities and Panchayat Raj Institutions (PRIs)

respectively.

(i) Vertical Devolution: The 14th Financial Commission has mandated a disbursal of Rs. 2.87 lakh

crore as grants-in-aid in excess of the recommended devolution of 42 per cent of taxes. Rs. 2 lakh

crores have been demarcated for disbursal to Rural Local Bodies and Rs. 87,000 crores have been

earmarked for disbursal to Urban Local Bodies.

(ii) Horizontal Devolution: The Horizontal devolution is done by calculating the formula with 90

per cent weightage for the state’s population in 2011 and 10 per cent weightage for the state’s area.

27

(iii) Rural and Urban Local Body Grants: Rural Local Bodies will receive grants through a fixed

basic proportion of 90 per cent and a performance-based proportion of 10 per cent. Urban Local

Bodies will receive grants through a fixed basic proportion of 80 per cent and a performance-based

proportion of 20 per cent. Performance will be evaluated based on the submission of audited

reports and the degree of effectiveness of implementation of schemes.

9.3.1. Grants-in-Aid Comparison

Table 3 shows the key differences between the recommendations of the 13th and the 14th Finance

Commissions in the area of Grants-in-Aid.

Table 3: Comparison of Recommendations on Grants-in-Aid by the 13th and 14th Finance

Commissions

13th Finance Commission (2009) 14th Finance Commission (2014)

The normal central assistance was given

by the Planning Commission.

All the grants were subsumed as vertical

devolution increased to 42 per cent.

Grants to state was divided into plan and

non-plan expenditure

Grants are now proposed to rural and urban

local bodies as performance grant and

grants for disaster relief and revenue

deficit.

Funds were diversified into sector-specific

and state-specific grants

Both sector specific and state specific

grants have been scrapped. It now focuses

on need based grants. Freedom of

deployment is with the state.

9.3.2. Understanding Need-based Grants

The term ‘need-based’ is related to the sector-specific requirements and grants of the States. A

brief background is necessary to understand this issue better. The Report of the 13th Finance

Commission was very specific in recommending grants to States for achieving targets in different

areas such as incentivization of the UID, reduction of infant mortality, improvement in justice

delivery, training of police personnel and innovation in public systems, to name a few (13th Finance

Commission, 2009). On the other hand, the 14th Finance Commission has categorized requests for

sector-specific grants into four areas: general administration (judiciary and police), environment,

and social sectors (including elementary education, health, drinking water and sanitation) (14th

Finance Commission, 2014).

Finance Commissions have noted that as the requirements to be addressed for each state in

different sectors to address are different, this has led to considerable inter-state disparity.

Equalizing the grants for States, even in specific areas, is an exercise in itself. As an example, the

14th Finance Commission Report cites the case of the 12th Finance Commission, which attempted

this exercise for grants in the areas of elementary education and healthcare, but finding it very

28

difficult to do so, ended up recommending grants to cover only 15 per cent of the short fall in the

education sector and 30 per cent of the short fall in the healthcare sector. When these grants are

examined in terms of their relative magnitudes, it has been noted that the grants recommended by

the 13th Finance Commission in the healthcare and elementary education sectors were estimated

to be only 1.57 per cent and 1.95 per cent of the total likely revenue expenditure of all states, i.e.,

not a significant proportion (14th Finance Commission, 2014). This serves as a pointer to increasing

the financial autonomy of States by providing them with the required fiscal space to design and

implement their schemes.

The 14th Finance Commission has stated that while the case of the environment has been dealt with

by accounting for the forest cover in the State in the formula for horizontal devolution, handling

disparities in requirements of the States in the other three areas must be done by utilizing the

additional fiscal space available to the States in view of the increased level of tax devolution. In

addition to the dropping of the distinctions between plan and non-plan expenditures, a post-

devolution deficit grant of Rs. 1,94,821 crores has been recommended for eleven states (14th

Finance Commission, 2014).

The experiences of previous Finance Commissions with sector-specific grants have not been

encouraging. Disbursal of grants to the States in specific sectors was usually accompanied by

requirements of matching contributions from the States, or with certain conditions. Finance

Commissions broadly specified the guidelines, while actual implementation details were left to the

State and Union Governments. The other key concern is that as the Finance Commission is not a

permanent body, the delivery of sector-specific and monitoring of schemes/States for satisfying

the requisite conditions has not been consistent over the years. Therefore, while agreeing that the

States would require assistance from the Union Government to meet their needs in the specified

sectors, it has been noted that the mechanism of meeting sector-specific requirements of States is

not best addressed through Finance Commissions (14th Finance Commission, 2014).

Grants in the areas of health, education, drinking water, and sanitation must be designed and

monitored by the States in tandem with the Union Government. The 14th Finance Commission has

hinted that the implementation of grants in these areas must be based on principles of co-operative

federalism. The Commission has also added that grants for specific projects or schemes by the

states would not be considered, as these were best left to the States themselves (14th Finance

Commission, 2014).

Thus, ‘need-based’ in the context of grants can be understood as those areas mentioned above

which need to be addressed by the States in view of the additional level of fiscal devolution

provided by the 14th Finance Commission in its recommendations.

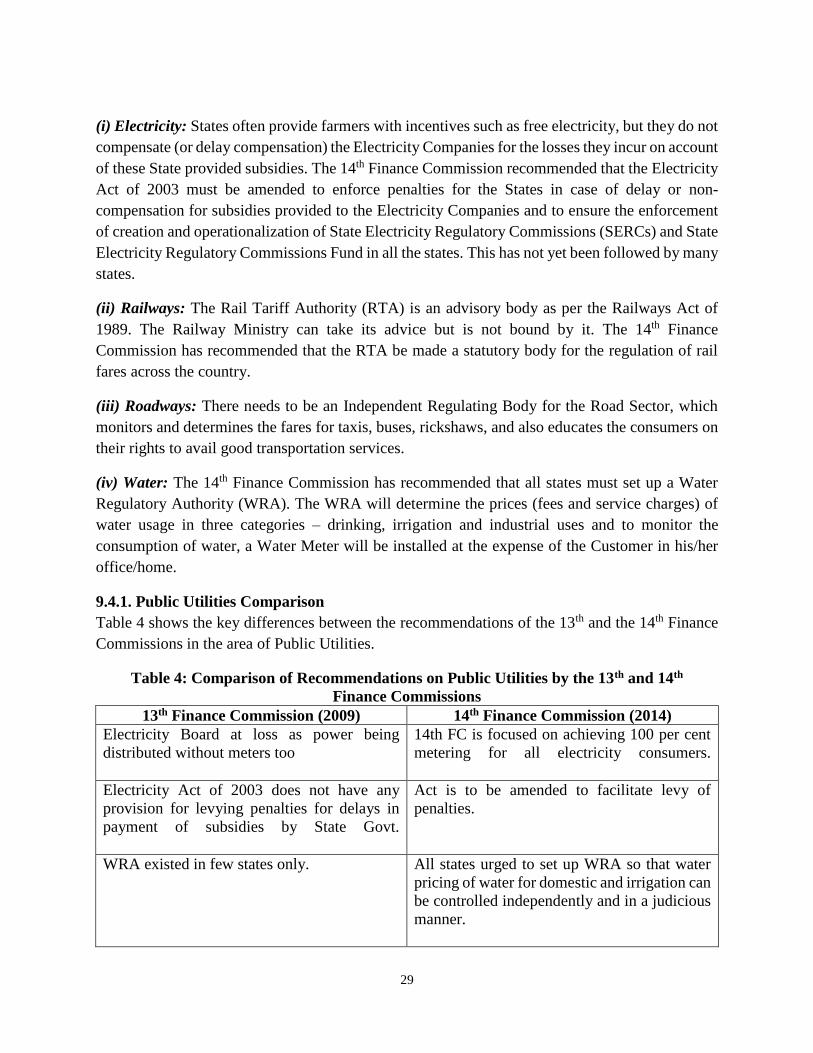

9.4. Public Utilities

This section focuses on the improvements suggested by the 14th Finance Commission in the

accountability and pricing of key public utilities such as Electricity, Transportation and Water.

29

(i) Electricity: States often provide farmers with incentives such as free electricity, but they do not

compensate (or delay compensation) the Electricity Companies for the losses they incur on account

of these State provided subsidies. The 14th Finance Commission recommended that the Electricity

Act of 2003 must be amended to enforce penalties for the States in case of delay or non-

compensation for subsidies provided to the Electricity Companies and to ensure the enforcement

of creation and operationalization of State Electricity Regulatory Commissions (SERCs) and State

Electricity Regulatory Commissions Fund in all the states. This has not yet been followed by many

states.

(ii) Railways: The Rail Tariff Authority (RTA) is an advisory body as per the Railways Act of

1989. The Railway Ministry can take its advice but is not bound by it. The 14th Finance

Commission has recommended that the RTA be made a statutory body for the regulation of rail

fares across the country.

(iii) Roadways: There needs to be an Independent Regulating Body for the Road Sector, which

monitors and determines the fares for taxis, buses, rickshaws, and also educates the consumers on

their rights to avail good transportation services.

(iv) Water: The 14th Finance Commission has recommended that all states must set up a Water

Regulatory Authority (WRA). The WRA will determine the prices (fees and service charges) of

water usage in three categories – drinking, irrigation and industrial uses and to monitor the

consumption of water, a Water Meter will be installed at the expense of the Customer in his/her

office/home.

9.4.1. Public Utilities Comparison

Table 4 shows the key differences between the recommendations of the 13th and the 14th Finance

Commissions in the area of Public Utilities.

Table 4: Comparison of Recommendations on Public Utilities by the 13th and 14th

Finance Commissions

13th Finance Commission (2009) 14th Finance Commission (2014)

Electricity Board at loss as power being

distributed without meters too

14th FC is focused on achieving 100 per cent

metering for all electricity consumers.

Electricity Act of 2003 does not have any

provision for levying penalties for delays in

payment of subsidies by State Govt.

Act is to be amended to facilitate levy of

penalties.

WRA existed in few states only. All states urged to set up WRA so that water

pricing of water for domestic and irrigation can

be controlled independently and in a judicious

manner.

30

Table 4: Comparison of Recommendations on Public Utilities by the 13th and 14th

Finance Commissions

13th Finance Commission (2009) 14th Finance Commission (2014)

Water charges collected on the basis of

property tax.

Water charges should be determined on

volumetric basis and this is possible only if

water meters are fixed.

Tariff revision was controlled by elections if

any.

Tariff revision must be revised once a year in

April irrespective of election year or not.

Increase in fuel costs and power purchase was

subsumed by Electricity board.

Increase in Fuel cost, power purchase must be

passed to consumers twice a year.

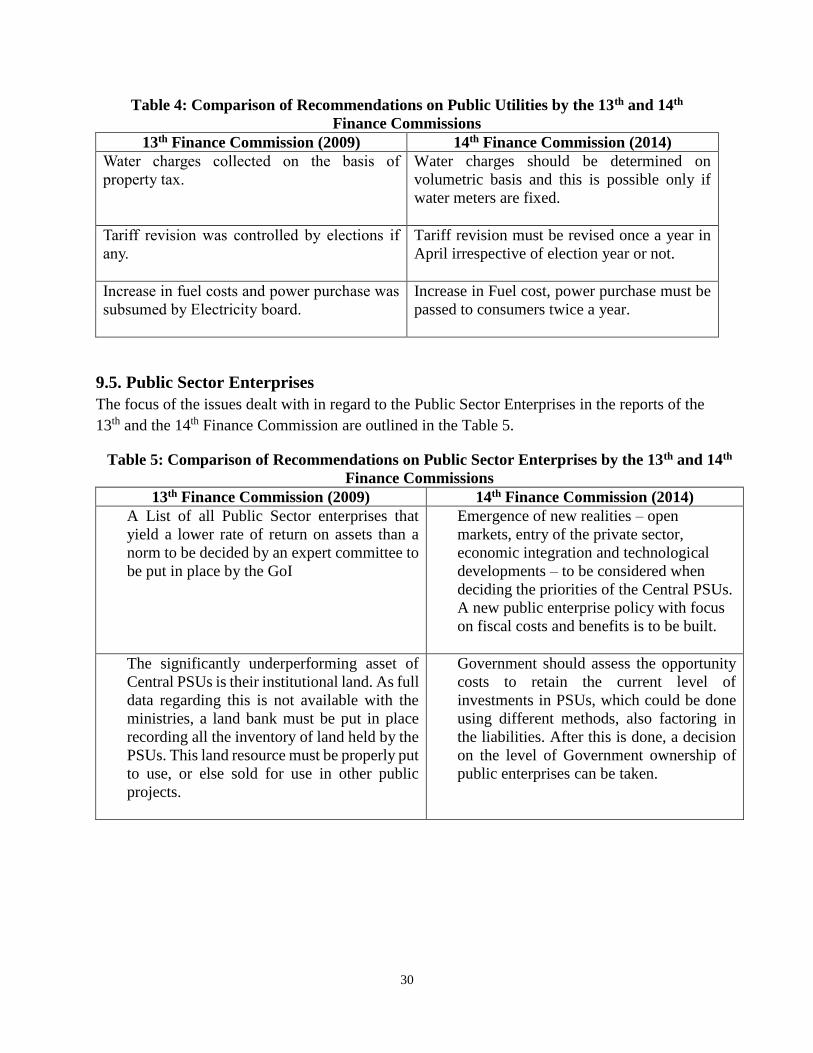

9.5. Public Sector Enterprises

The focus of the issues dealt with in regard to the Public Sector Enterprises in the reports of the

13th and the 14th Finance Commission are outlined in the Table 5.

Table 5: Comparison of Recommendations on Public Sector Enterprises by the 13th and 14th

Finance Commissions

13th Finance Commission (2009) 14th Finance Commission (2014)

A List of all Public Sector enterprises that

yield a lower rate of return on assets than a

norm to be decided by an expert committee to

be put in place by the GoI

Emergence of new realities – open

markets, entry of the private sector,

economic integration and technological

developments – to be considered when

deciding the priorities of the Central PSUs.

A new public enterprise policy with focus

on fiscal costs and benefits is to be built.

The significantly underperforming asset of

Central PSUs is their institutional land. As full

data regarding this is not available with the

ministries, a land bank must be put in place

recording all the inventory of land held by the

PSUs. This land resource must be properly put

to use, or else sold for use in other public

projects.

Government should assess the opportunity

costs to retain the current level of

investments in PSUs, which could be done

using different methods, also factoring in

the liabilities. After this is done, a decision

on the level of Government ownership of

public enterprises can be taken.

31

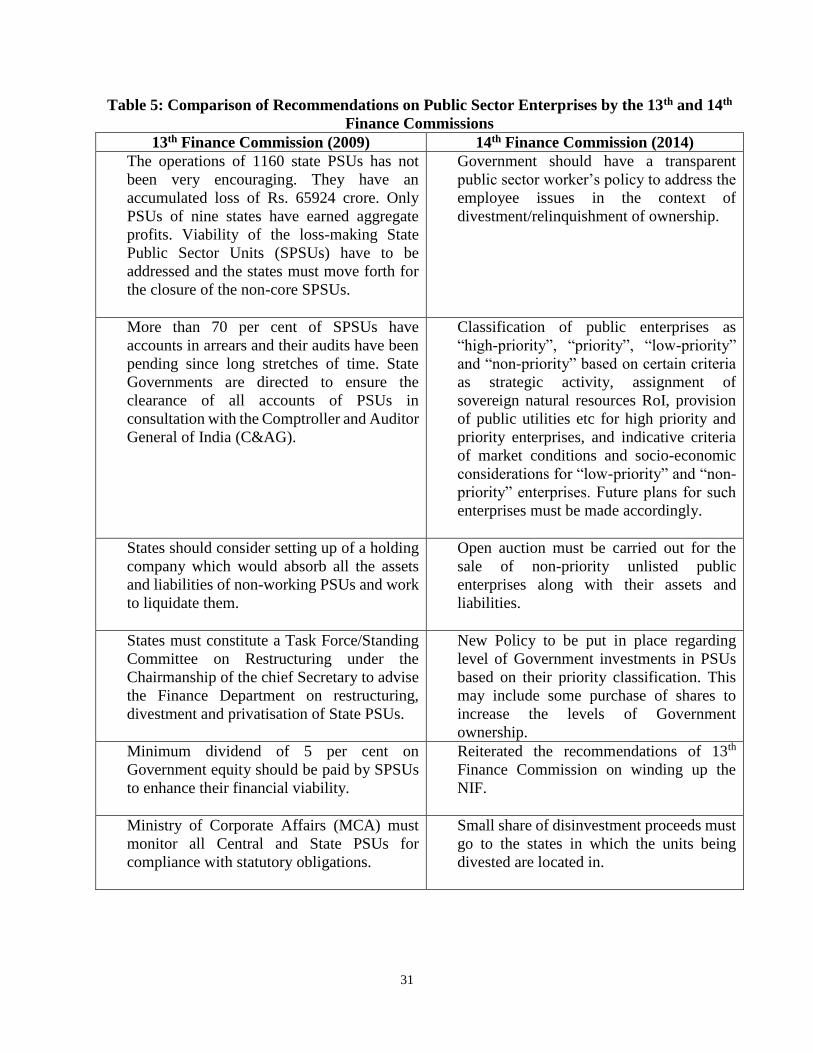

Table 5: Comparison of Recommendations on Public Sector Enterprises by the 13th and 14th

Finance Commissions

13th Finance Commission (2009) 14th Finance Commission (2014)

The operations of 1160 state PSUs has not

been very encouraging. They have an

accumulated loss of Rs. 65924 crore. Only

PSUs of nine states have earned aggregate

profits. Viability of the loss-making State

Public Sector Units (SPSUs) have to be

addressed and the states must move forth for

the closure of the non-core SPSUs.

Government should have a transparent

public sector worker’s policy to address the

employee issues in the context of

divestment/relinquishment of ownership.

More than 70 per cent of SPSUs have

accounts in arrears and their audits have been

pending since long stretches of time. State

Governments are directed to ensure the

clearance of all accounts of PSUs in

consultation with the Comptroller and Auditor

General of India (C&AG).

Classification of public enterprises as

“high-priority”, “priority”, “low-priority”

and “non-priority” based on certain criteria

as strategic activity, assignment of

sovereign natural resources RoI, provision

of public utilities etc for high priority and

priority enterprises, and indicative criteria

of market conditions and socio-economic

considerations for “low-priority” and “non-

priority” enterprises. Future plans for such

enterprises must be made accordingly.

States should consider setting up of a holding

company which would absorb all the assets

and liabilities of non-working PSUs and work

to liquidate them.

Open auction must be carried out for the

sale of non-priority unlisted public

enterprises along with their assets and

liabilities.

States must constitute a Task Force/Standing

Committee on Restructuring under the

Chairmanship of the chief Secretary to advise

the Finance Department on restructuring,

divestment and privatisation of State PSUs.

New Policy to be put in place regarding

level of Government investments in PSUs

based on their priority classification. This

may include some purchase of shares to

increase the levels of Government

ownership.

Minimum dividend of 5 per cent on

Government equity should be paid by SPSUs

to enhance their financial viability.

Reiterated the recommendations of 13th

Finance Commission on winding up the

NIF.

Ministry of Corporate Affairs (MCA) must

monitor all Central and State PSUs for

compliance with statutory obligations.

Small share of disinvestment proceeds must

go to the states in which the units being

divested are located in.

32

Table 5: Comparison of Recommendations on Public Sector Enterprises by the 13th and 14th

Finance Commissions