Going mainstream – how absolute return is moving into the

28

Going mainstream – how absolute return is moving into the regulated market

Transcript of Going mainstream – how absolute return is moving into the

Going mainstream –how absolute return is moving into theregulated market

Contents

1. Foreword

2. Executive summary

4. Part One: Defining our terms: what we mean by ‘absolute return’

7. Part Two: The rise of regulated absolute return funds in Europe

11. Part Three: Factors set to drive absolute return demand

16. Part Four: Employing absolute return in a portfolio

21. Part Five: Evaluating absolute return strategies

24. Conclusion

Going mainstream – how absolute return is moving into the regulated market 1

Foreword

The concept of investing to achieve an absolute return has been around for over 60 years andhas enabled the global hedge fund market to grow to a total value of more than US$1.6 trillion(EUR1.28trn)1. But it is only since 2002 that investors in Europe have been able to accessabsolute return approaches through authorised investment vehicles.

So eight years on, are absolute return strategies still an ‘alternative’ investment or do they yetrank with relative return approaches as mainstream investment choices?

In this paper, we want to provide an assessment of the role of absolute return investing in theregulated investment market. We outline the different types of strategies that have emerged,we look at the growth in the regulated market to date. We also put forward reasons why webelieve absolute return approaches are well placed to capture significant investor interest in thenext few years.

We also look to examine the role of absolute return strategies in a portfolio – and explore if theycan genuinely contribute to a better trade-off between risk and reward for investors. Finally welook at due diligence and the factors that we believe must be made explicit if investors are to besure that an absolute return strategy has an appropriate and achievable investment objective.

We hope this paper offers useful insight into how absolute return funds have developed as asector over the past decade and how they can be best deployed in an investment portfolio.

Threadneedle Asset Management, June 2010

1Hedge Fund Research Group, total industry figure for Q1 2010

Going mainstream – how absolute return is moving into the regulated market2

Executive summary

This report aims to provide an overview of the regulated absolute return market: it assesses thegrowth of the market to date, drivers that are likely to encourage inflows into the sector overthe next 10 years and explores how absolute return funds can be used most effectively within aportfolio. Finally it assesses the factors that need to be taken into account to identify suitablefunds and fund managers.

1. Defining our terms; what we mean by absolute returnAbsolute return investing refers to the discipline of targeting a positive investment return over agiven period of time, irrespective of market conditions. It is therefore distinct from a traditionalrelative return approach that looks to outperform a market or asset class but has no commitmentto deliver positive returns. A range of strategies have been developed to achieve persistentlypositive returns. The majority of these take both long and short positions on stocks/assetclasses/markets using derivative-based techniques. Common strategies include portable alpha,pairs trading, cash enhancement and multi-asset investing.

2. The rise of regulated absolute return funds in EuropeInvestors in the regulated European market have only been able to access derivative-basedabsolute return strategies since the introduction of the EU’s UCITS III fund directive in 2002,which permitted hedge fund-like investment techniques in regulated funds. This legislationprecipitated sharply rising inflows into absolute return strategies between 2002 and 2008 –although there were marked outflows during the peak of the credit crisis.

Subsequently, net inflows have partially recovered as hedge fund managers start to use the UCITSstructure to distribute regulated versions of their offshore strategies. This trend is likely to continue –particularly as European-based hedge fund managers now face the prospect of their own regulationin the form of the EU’s proposed Alternative Investment Fund Managers (AIFM) Directive.

Within individual markets, there appears to be some correlation between stock marketuncertainty/volatility and levels of interest in absolute return strategies. In the UK, for example,the IMA Absolute Return sector was the biggest-selling open-ended fund sector of late-2008/2009 alongside corporate bonds and property. Initial breakdowns of the UCITS III marketsuggest that the most prevalent absolute return strategies are long/short equity, credit/bond-based strategies and multi-strategy funds.

3. Factors set to drive absolute return demandAbsolute return funds currently only account for around 1% of UCITS-regulated assets. Butthere are a number of factors now at play that could drive significant inflows into regulatedabsolute return approaches in the next five to 10 years.

First, as low interest rates persist, absolute return funds may experience significant demandfrom yield-seeking investors seeking capital preservation - especially as concerns continueregarding sovereign debt. Second, stock market volatility has increased sharply. This mayincrease the appeal of absolute return strategies both as a means of managing portfolio volatilityand actively profiting from periods of market downturn (ie through short-selling).

Third, as correlations between asset classes such as equities, bonds and commodities increase,investors need to find new ways to diversify their portfolios. The low levels of correlation thatmany absolute return strategies display with overall asset-class movements may – again – driveinvestor interest.

Finally, the burden of investment risk is shifting from companies and the state to individuals aspension provision shifts from a defined-benefit to a defined contribution model. As millions ofEuropeans are forced to manage investment risks themselves, we anticipate that absolute returnfunds will become increasingly important – especially among older workers and those in retirement.

Going mainstream – how absolute return is moving into the regulated market 3

4. Employing absolute return in a portfolioAbsolute return is a valuable investment tool. But it should not be viewed as a replacement forrelative return investing. Rather, our research shows that it is a valuable component that can beused to enhance a portfolio’s risk-reward profile.

Performance analysis reveals that certain groups of attributes can be assigned to absolute returnand relative return funds. Namely:

Absolute return funds display a narrow range of returns in all market conditions; a higher likelihoodof delivering positive outperformance when market returns are negative and a tendency tounderperform when markets are rising strongly.

Conversely, relative return funds display a broader range of returns (which widen when marketreturns are also extreme); a greater likelihood to deliver negative returns when market returns arenegative and the potential to deliver very strong positive returns when markets are rising strongly.

Given these attributes, there are market environments when it may benefit an investor tofavour absolute return strategies over relative return strategies and vice versa. Absolute returnfunds are likely to offer the best return when the market environment is negative or volatile on a sustained basis. Relative return funds offer superior return potential when markets areexperiencing a strong growth phase.

Our analysis shows that portfolios that are able to have exposure to both relative return andabsolute return funds are likely to have a more attractive risk-return profile than portfolios thatare restricted to one type of strategy. But in addition, actively rotating a portfolio’s allocationtowards either absolute return or relative return, depending on the market environment, cansignificantly enhance returns and reduce losses.

This suggests that the decision to skew a portfolio towards either a relative return or absolutereturn bias could be treated as an additional source of investment return alongside other traditionalinvestment decisions, such as market and asset allocation.

5. Evaluating absolute return strategiesAbsolute return funds are a highly valuable tool for investors and their wider availability should bewelcomed. However, investors need to be sure that funds are appropriate to their needs and alsothat a fund manager has the appropriate mix of skills and experience to deliver absolute returnfunds while also meeting the requirements of the regulated funds market.

To this end, we have outlined a list of areas that we believe need to be assessed as part of anydue diligence process – and for which managers should readily supply information. These include:the experience of the manager in managing absolute return strategies (specifically aspects suchas short-selling and managing leverage); the manager’s experience in meeting the requirementsof the regulated fund market; the target return and the timeframe to deliver this return; whereand why the fund allocates its risk budget; volatility parameters; suitability of underlyinginvestments; market correlations; liquidity and a fund’s charging structure.

ConclusionAbsolute return funds still only account for a tiny fraction of the European regulated fundsmarket but the sector is evolving. The sector is now seeing heightened interest in the wake ofthe credit crisis as investors look for new ways to manage risks against a background of lowinterest rates – and more managers migrate from the unregulated to the regulated market.

The key concern now is whether investor demand can be matched by appropriate strategies runby managers with the necessary dual experience in running absolute return mandates andmeeting the requirements of the regulated fund market. Until performance track records arelong enough to identify those ‘high-value’ managers who are proven to have the appropriatecombined skills-set, deep due diligence of absolute return funds remains essential.

Going mainstream – how absolute return is moving into the regulated market4

Part One:Defining our terms: what we mean by ‘absolute return’

Absolute return investing refers to the discipline of targeting a positive investment returnover a given period of time, irrespective of market conditions. Often it involves seekingto outperform a named cash or inflation benchmark.

This is distinct from relative return investing, where the target is to outperform a market, indexor benchmark portfolio whose value can fall as well as rise. Under a relative return mandate, afund can deliver a negative return and still achieve its outperformance target so long as it fallsless than the benchmark in question. Absolute return funds have only delivered on their remit ifthey produce a positive return in line with or in excess of their benchmark.

The key attributes of any absolute return strategy are: Aims for consistently positive returns over a given time period Low or zero correlation with market movements High alpha content – with returns generated by investor skill

Absolute return is therefore highly consistent with most investors’ primary reason fortaking on investment risk – namely to achieve a return above that available on ‘risk-free’cash deposits.

Methods of achieving absolute returnInvestment professionals have explored a range of strategies to achieve a persistently positivereturn regardless of the market environment. The majority of these take both long and shortpositions on stocks/asset classes/markets. Some strategies may be long-only (but may notnecessarily classify themselves as absolute return, as a result). Some of the most commonstrategies are as follows:

i. Portable alpha (long-short)This involves building an actively-managed relative return portfolio, aiming to outperform a givenindex or market. Using an index swap, the performance of the index (‘beta’) is hedged, leavingonly the excess return (‘alpha’) generated by the portfolio manager. This can then be addedonto the beta of another lower-risk or uncorrelated asset class which is provided using a low-cost derivative such as an index future.

Diagram 1: Using portable alpha to generate absolute returns

Alphaengine

Beta

(marketreturn)

Risk-freereturn

Risk-freereturn

Eg:Govt bondsLibor

Excessreturn

Alpha

(managerreturn)

Beta risk isstripped

out usingderivatives

Risk-freereturn

+ =Absolute

return

‘Absolute return istherefore highlyconsistent with mostinvestors’ primaryreason for taking oninvestment risk –namely to achieve areturn above thatavailable on ‘risk-free’cash deposits.’

Going mainstream – how absolute return is moving into the regulated market 5

ii. Pairs trading/market neutral (long-short)This involves a portfolio manager taking simultaneous positions in two different but comparablesecurities, eg, the shares of two companies in the same sector. A long position is taken in thesecurity expected to perform best out of the two, while a short position is taken in the expectedunderperformer. Pairs trading reduces the importance of predicting which direction the shareswill move in. So long as the manager is correct in how the two will perform relative to oneanother, a positive return will be achieved – see Diagram 2.

Diagram 2: Scenarios in which a pairs trade will achieve a positive return

iii. Cash enhancement (long-short)This involves two elements. The first is a portfolio of investments, typically short-dated bonds,designed to generate a return roughly in line with cash deposits. This portfolio is then used ascollateral for derivative trades using long and short positions to reflect the manager’s views onmarkets, asset classes and individual stocks or shares. Provided these positions are correct, theprofits from the derivative strategies can be used to augment the return on the low-risk bondportfolio, thereby delivering a low-risk cash-plus return – see Diagram 3.

Diagram 3: Cash enhancement strategy

A B

A A

B

B

Profit

Profit

Profit

Pairs trade:Long position on Share A (outperformer)Short position on Share B (underperformer)A positive return will be achieved in all of the following events:

+ =

Low-riskbond

portfolio

Derivativetrades

Cash-likereturn

Cashreturn

AlphaAlphageneration

Used ascollateral for

Going mainstream – how absolute return is moving into the regulated market6

iv. Multi-asset (long only)This is a long-only strategy that has the flexibility to move across different asset classes, marketsand strategies, depending on which is expected to deliver a positive return. The portfolio’s defaultposition is 100% cash. Only if the manager has a view that a particular market or asset class willdeliver a positive return will s/he deviate from this. While the manager won’t use derivatives tocreate short positions, derivatives may be used to achieve tactical exposure to an asset classswiftly and efficiently. Maximum exposure to higher-risk asset classes will often be restricted.These multi-asset strategies are sometimes referred to as ‘total return’ to differentiate themfrom funds that can take short positions.

Diagram 4: Multi-asset long-only strategy

Benefits and drawbacks of absolute return investingThe strategies above will each have their advantages and disadvantages but the key benefitsand drawbacks of an absolute return approach can be summarised as follows:

Benefitsi. Increases the opportunity setBy taking both long and short positions, a manager can make money in both rising and fallingmarkets. A long-only manager can only make money from their non-cash positions when marketsare rising. A long/short manager can therefore make profits from two set of convictions: whichsecurities, sectors or markets s/he believes are going to rise and which s/he believes are goingto fall.

ii. Reduces reliance on market returnsAn absolute return approach that strips out beta-driven returns reduces an investor’s reliance onthe direction of markets to make profits. Returns tend to have far lower correlation with marketmovements than is the case with relative return strategies, so market risk is reduced.

iii. Reduces volatility and improves cash preservationTactics such as taking symmetrical long and short positions across stocks and/or holding highcash exposures are designed to minimise volatility. Many strategies make cash preservation astated goal.

Drawbacksi. Increases opportunity for miscalling market/stock/asset movementsA long-short strategy doubles the opportunity set to generate returns but it also doubles the riskof miscalling a position. Moreover, losses on a long position are limited to the current value ofthe security. Losses on a mis-called short position are potentially unlimited as there is no limiton how far a security could rise in value.

Falling stock markets

Maximum100% ofportfolio

Maximum50% of

portfolio

Bonds

Cash

Real Assets etc

Convertibles

Equities

Rising stock markets

Going mainstream – how absolute return is moving into the regulated market 7

ii. Likely to lag strongly rising marketsIn their bid to generate consistently positive returns and minimise volatility, absolute returnfunds are likely to underperform in strongly rising markets and therefore will not be suitablewhere an investor is seeking to maximise return.

iii. Greater reliance on manager skillWhere a fund employs a strategy that looks to neutralise market movements (beta) it becomesreliant on manager skill (alpha) to generate return. Selection of an experienced and provenmanager becomes vital.

In shortAbsolute return investing is a distinct investment discipline from traditional relative returninvesting. It can use a variety of approaches to achieve its target positive returns, typically usinglong and short positions, high cash exposures and flexibility in terms of asset allocation. In thenext section we will assess how investors have responded to the opportunity to accessabsolute return approaches through regulated markets.

Part Two:The rise of regulated absolute return funds in Europe

The concept of absolute return investing has been around since the creation of the firsthedge funds in the late-1940s, which were designed to reduce risk by neutralising marketmovements.

Over the next 50 years, the expansion of absolute return investing took place in the unregulatedhedge fund sector and institutional investment market, while regulated products were restrictedto long-only strategies. However, the past decade has seen developments that have enabledthe absolute return concept to migrate from the unregulated to the regulated market.

UCITS III brings absolute return to the regulated marketUndertakings for Collective Investment in Transferable Securities (UCITS) are a set of Europeandirectives designed to enable retail distribution of any compliant fund across the 30 countries ofthe European Union, provided a fund is registered in at least one member state. As well asenabling fund distribution across Europe, the UCITS ‘brand’ has also achieved recognition inother markets including Asia and South America.

In the late-1990s, the UCITS requirements were revised to enable a broader range of strategiesto be marketed to investors, to reflect advances in financial markets. ‘UCITS III’ was designedto enable more investors to benefit from risk management and return-generation techniquespreviously only available via the unregulated hedge fund market.

From 2002, the UCITS III directive enabled European regulated funds to: Use derivatives (for example, futures, options and swaps and contracts for difference) to

generate investment returns, not simply for efficient portfolio management.

Invest in diversified indices and their derivatives (including hedge fund indices).

Retain unlimited cash positions and use money market instruments more extensively.

Exercise greater flexibility to combine multiple asset classes in a single fund.

Unlike their unregulated hedge fund counterparts, UCITS III funds cannot short sell a stock, butthey can use derivatives to take ‘synthetic’ short positions.

Going mainstream – how absolute return is moving into the regulated market8

The UCITS regime also imposes strict requirements regarding risk management, investor accessand reporting in order to make funds transparent and accountable. These requirements include:

Assessing and reporting Value at Risk (VaR)

Periodic stress-testing simulations

Maximum redemption period of 14 days2, with redemption at net asset value

Indicative daily pricing

Fund diversification through the 5/10/40 rule3

Comprehensive reporting and a simplified prospectus

Independent fund board

In other words, the UCITS III directive has enabled hedge fund techniques to be applied in ahighly regulated investment structure. Demand from investors was initially strong. By the endof 2006, total net assets in UCITS III funds with a total/absolute return mandate exceededEUR80 billion – see Diagram 5. However, the sector saw a sharp outflow of funds during thecredit crisis – effectively halving funds under management to close to EUR40 billion. Thisoutflow has been partially reversed in 2008-2009. By the end of 2009, AUM in totalreturn/absolute return UCITS funds represented about 1% of total net assets in European-domiciled UCITS funds4.

Diagram 5: Total net assets in UCITS total return/absolute return strategies

Source: Lipper FMI. As at 31 December 2009.

‘Newcits’ – hedge funds move to the regulated marketThe strength of the UCITS brand has also attracted strong inflows from hedge fund investors.Following high-profile hedge fund fraud such as the Madoff affair, more investors are nowseeking out the more rigorous standards on liquidity, reporting, risk management and custodythat the regulated market offers. To capture this migration, many hedge fund managers are nowchoosing to launch UCITS III equivalents – dubbed ‘Newcits’– of their most popular strategies.

This migration largely accounts for the strong uptick in UCITS III inflows shown in Diagram 5over 2008-2009. Given the size of the global hedge fund market (EUR1.28 trillion5) it couldcontinue to be responsible for huge inflows into the regulated absolute return market over themedium term.

0

10000

20000

30000

40000

50000

60000

70000

80000

90000

2002 2003 2004 2005 2006 2007 2008 2009

EUR

mn

2In practice most funds are providing weekly or daily liquidity.3This requires that no more than 10% of a UCITS fund’s net assets may be invested in transferable securities or money marketinstruments issued by the same body, with a further aggregate limit of 40% of net assets on exposures of greater than 5% tosingle issuers.4The European Fund and Asset Management Association estimates that EUR5.29 trillion of net assets was held in EuropeanUCITS funds as at end-2009, with a further EUR1.74 trillion in non-UCITS funds.5Hedge Fund Research Group, total industry figure of US$1.67 trillion for Q1 2010.

Going mainstream – how absolute return is moving into the regulated market 9

A further push factor could be the EU’s proposed Alternative Investment Fund Managers(AIFM) directive. This is looking to provide a regulatory framework for non-UCITS fundsincluding hedge funds, real estate and private equity funds. However, it may encourage morealternative managers to adopt UCITS legislation rather than be caught by the untestedobligations of the AIFM directive.6

According to Hedge Fund Research, more than 200 hedge funds offerings were UCITS III-compliant products as at end-February 2010, with total assets under management in excess ofUS$35 billion.

Source: IMA/Morningstar/FTSE.

6UCITS compliance may also be more appealing than the AIFM directive as it automatically enables managers to distributefunds to retail investors, whereas the AIFM only offers an automatic passport for distribution to professional investors.

Country focus: the UKIndividual markets are creating their own sectors to classify regulated absolute return funds.In the UK, the Investment Management Association (IMA) launched a sector specifically foropen-ended funds with an absolute return objective in April 2008. Classified as a specialistsector, it covers funds managed with “the aim of delivering absolute (ie more than zero)returns in any market conditions”. Funds in this sector would normally expect to deliver anabsolute return over a 12-month period.

Inflows into the sector have experienced strong momentum. During and in the wake of thecredit crisis, the sector has competed with corporate bonds and property as the best-sellingasset class, achieving the highest net sales of any IMA sector in Q2-Q3 2008 and Septemberand December 2009 – see Diagram 6 below.

The strong growth in net sales towards the end of 2009 is particularly interesting given that,by this time, equity markets had mounted a sustained recovery. This contradicts the idea thatabsolute return investing is only of interest to investors during periods of market downturn –although it may reflect the attraction of absolute return strategies both during and after periodsof severe market volatility.

Diagram 6: Net sales in the IMA Absolute Return sector Apr 2008 – Dec 2009 versus FTSE All-Share performance

-100

0

100

200

300

400

500

InstitutionalRetail

Best-selling IMA sector –Q2 and Q3 2008

Best-selling IMA sector –Sept and Dec 2009

600

700

800

900

1,000

Apr-08 Jul-08 Oct-08 Jan-09 Apr-09 Jul-09 Oct-09

Net

sal

es (

£mn

s)

FTS

E A

ll-Sh

are

FTSE All-Share

3500.0

3000.0

2500.0

2000.0

1500.0

1000.0

Going mainstream – how absolute return is moving into the regulated market10

Absolute return market by strategyData group Citywire has been one of the first analysts to assess the composition of the Europeanabsolute-return UCITS market (and coined the term ‘newcits’). Analysing 276 UCITS-compliantfunds that use derivatives as a central part of their investment process, it has categorised fundsinto 13 peer groups. Its analysis shows that long-short equity strategies account for the largestsingle category (by number of funds), followed by credit-based strategies, multi-strategy funds,then market neutral accounting for just under 10% of constituents. Traditionally illiquid hedge-fund strategies such as event-driven investing account for the lowest number of constituents.

Diagram 7: Composition of the ‘newcits’ market (by % of constituents)

Source: Citywire – www.citywire.co.uk. As at 30 April 2010.

In shortThe introduction of UCITS III regulation triggered very strong growth in the regulated absolutereturn sector in Europe and in other markets. Although the sector suffered substantial outflowsduring the credit crisis, the migration of hedge fund strategies to the regulated UCITS marketlooks likely to continue to drive investor interest and continue to capture new asset inflows.

In the next section, we will assess a number of factors that may drive investor demand forabsolute return approaches in the next five to 10 years.

Credit Strategies 16%

Multi Strategy13%

Market Neutral9%

Currency7%

Emerging Market Equity inc Asia 5% Global Macro

5% Managed Futures 5%

Volatility Trading 5%

Commodities 4%

Fund of Funds 4%

Event Driven 1%Convertibles 1%

Other 11%

Long/Short Equity25%

Data provided by Citywire using their Newcits categories. Further information on Citywire’s Newcits database can be found on www.newcits.com

‘the migration of hedgefund strategies to theregulated UCITS marketlooks likely to continueto drive investorinterest.’

Going mainstream – how absolute return is moving into the regulated market 11

Part Three:Factors set to drive absolute return demand

As we saw in the previous section of this report, the nascent regulated absolute returnsector has experienced strong inflows from investors attracted by the concept of fundsthat aim to deliver consistently positive returns.

Even so, absolute return still only accounts for around 1% of UCITS-regulated assets. But in ourview, there are a number of factors now at play that could drive significant inflows into absolutereturn approaches, causing these strategies to account for a much larger proportion of theEuropean regulated funds market in the next five to 10 years.

i. Low interest rates demand alternatives for low-risk investorsWith cash yielding almost zero as interest rates languish at historic lows, risk-averse investorsneed alternative means to preserve capital while achieving above-inflation returns.

Certainly, the growing sales in absolute return strategies have coincided with a sustained declinein bank base rates. As long as central banks need to keep interest rates low in order to bolstereconomic growth, investors will continue to look for low-risk alternatives to low-paying deposits.Given concerns over traditional cash alternatives such as sovereign debt, absolute return strategiesare well placed to capture inflows from low-risk investors.

However, the fund industry needs to be careful that investors are not sold absolute return fundsas a direct substitute for zero-risk deposits. The additional risks involved and the basis forperformance must be clearly explained.

ii. Market volatility has increasedWhile the last 50 years have seen sustained stock market gains, data also suggests the periodsof growth are getting shorter and the fluctuations in markets are getting deeper. As Diagram 8shows, rolling three-year volatility on the MSCI World Index of global equities has more thandoubled since 2007.

Diagram 8 – Rising volatility in equities

Source: MSCI/Morningstar/Threadneedle. As at 31 March 2010.

MS

CI A

C W

orl

d In

dex

Ro

lling

3-year volatility

MSCI AC World Index

1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Rolling 3 Year Volatility

0

50

100

150

200

250

300

350

400

450

0%

5%

10%

15%

20%

25%

30%

Going mainstream – how absolute return is moving into the regulated market12

Absolute return strategies may be more appealing in a more volatile market environment fortwo reasons. First, many strategies specifically aim to reduce the impact of market volatility.Second, by taking both long and short positions, they can actively prosper from market volatilityand outperform their long-only counterparts. For both of these reasons, signs of sustainedmarket volatility should encourage inflows into absolute return strategies.

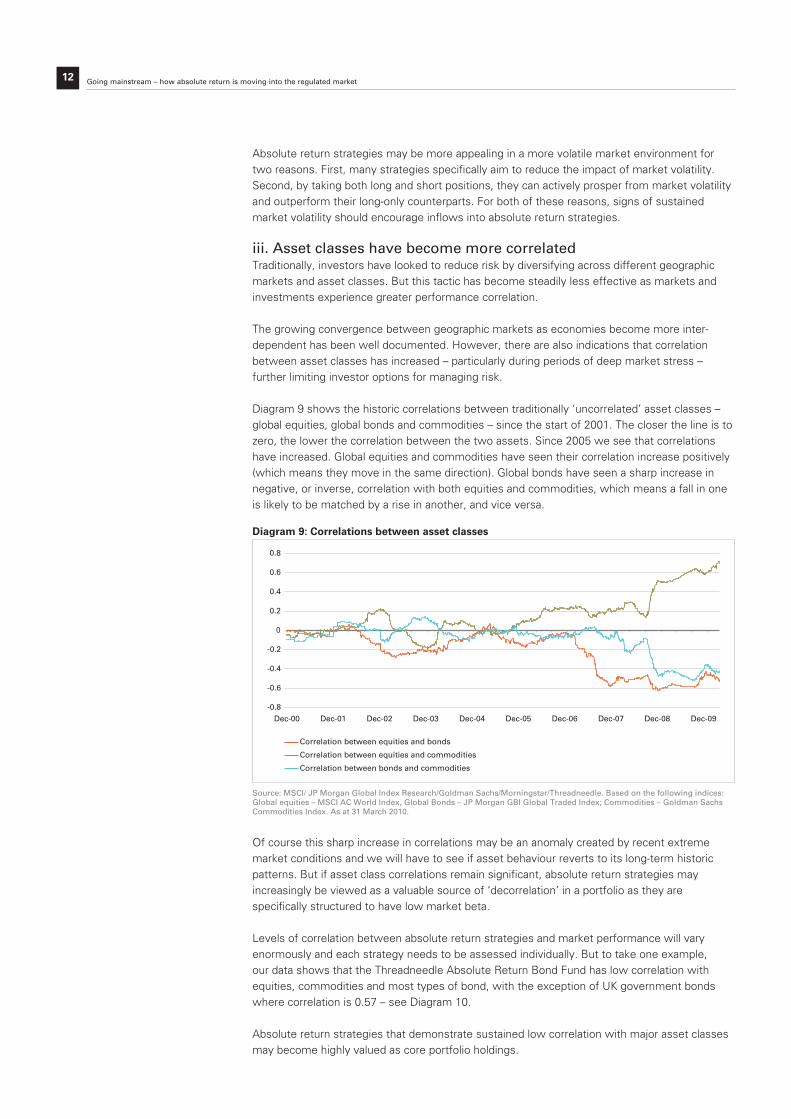

iii. Asset classes have become more correlatedTraditionally, investors have looked to reduce risk by diversifying across different geographicmarkets and asset classes. But this tactic has become steadily less effective as markets andinvestments experience greater performance correlation.

The growing convergence between geographic markets as economies become more inter-dependent has been well documented. However, there are also indications that correlationbetween asset classes has increased – particularly during periods of deep market stress –further limiting investor options for managing risk.

Diagram 9 shows the historic correlations between traditionally ‘uncorrelated’ asset classes –global equities, global bonds and commodities – since the start of 2001. The closer the line is tozero, the lower the correlation between the two assets. Since 2005 we see that correlationshave increased. Global equities and commodities have seen their correlation increase positively(which means they move in the same direction). Global bonds have seen a sharp increase innegative, or inverse, correlation with both equities and commodities, which means a fall in oneis likely to be matched by a rise in another, and vice versa.

Diagram 9: Correlations between asset classes

Source: MSCI/ JP Morgan Global Index Research/Goldman Sachs/Morningstar/Threadneedle. Based on the following indices:Global equities – MSCI AC World Index, Global Bonds – JP Morgan GBI Global Traded Index; Commodities – Goldman SachsCommodities Index. As at 31 March 2010.

Of course this sharp increase in correlations may be an anomaly created by recent extrememarket conditions and we will have to see if asset behaviour reverts to its long-term historicpatterns. But if asset class correlations remain significant, absolute return strategies mayincreasingly be viewed as a valuable source of ‘decorrelation’ in a portfolio as they arespecifically structured to have low market beta.

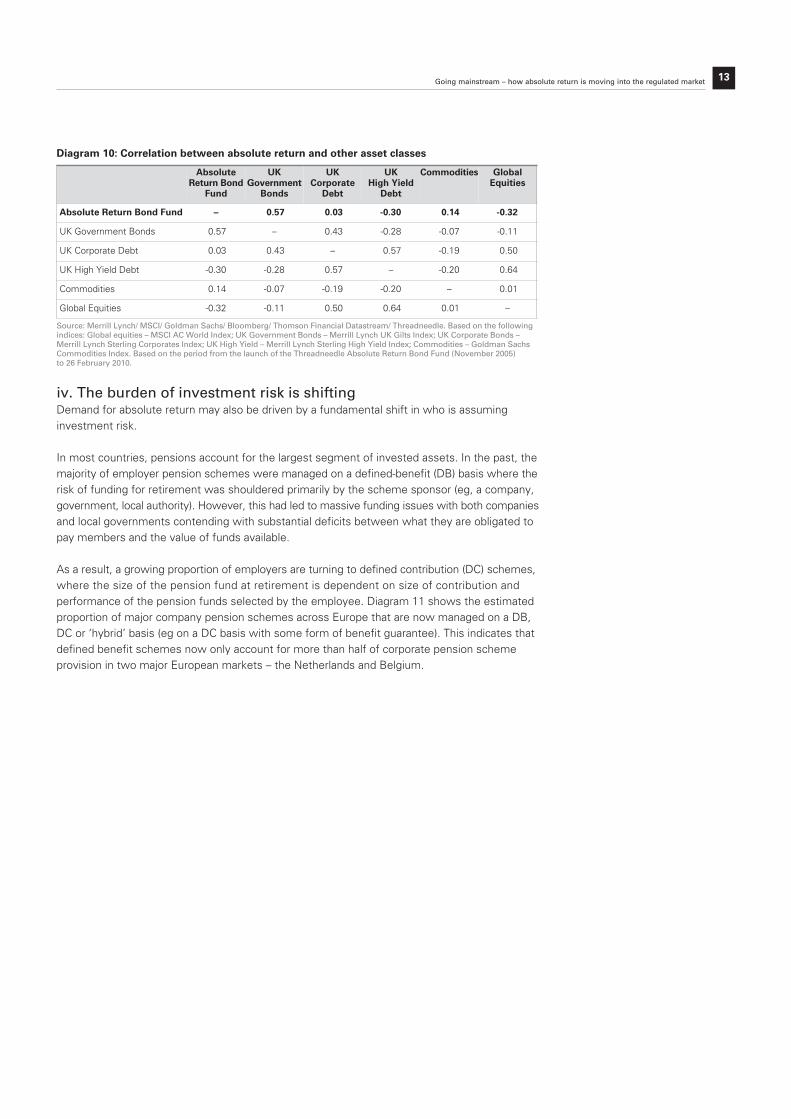

Levels of correlation between absolute return strategies and market performance will varyenormously and each strategy needs to be assessed individually. But to take one example, our data shows that the Threadneedle Absolute Return Bond Fund has low correlation withequities, commodities and most types of bond, with the exception of UK government bondswhere correlation is 0.57 – see Diagram 10.

Absolute return strategies that demonstrate sustained low correlation with major asset classesmay become highly valued as core portfolio holdings.

-0.8

-0.6

-0.4

-0.2

0

0.2

0.4

0.6

0.8

Dec-00 Dec-01 Dec-02 Dec-03 Dec-04 Dec-05 Dec-06 Dec-07 Dec-08 Dec-09

Correlation between equities and bonds

Correlation between equities and commodities

Correlation between bonds and commodities

Going mainstream – how absolute return is moving into the regulated market 13

Diagram 10: Correlation between absolute return and other asset classes

Source: Merrill Lynch/ MSCI/ Goldman Sachs/ Bloomberg/ Thomson Financial Datastream/ Threadneedle. Based on the followingindices: Global equities – MSCI AC World Index; UK Government Bonds – Merrill Lynch UK Gilts Index; UK Corporate Bonds –Merrill Lynch Sterling Corporates Index; UK High Yield – Merrill Lynch Sterling High Yield Index; Commodities – Goldman SachsCommodities Index. Based on the period from the launch of the Threadneedle Absolute Return Bond Fund (November 2005) to 26 February 2010.

iv. The burden of investment risk is shiftingDemand for absolute return may also be driven by a fundamental shift in who is assuminginvestment risk.

In most countries, pensions account for the largest segment of invested assets. In the past, themajority of employer pension schemes were managed on a defined-benefit (DB) basis where therisk of funding for retirement was shouldered primarily by the scheme sponsor (eg, a company,government, local authority). However, this had led to massive funding issues with both companiesand local governments contending with substantial deficits between what they are obligated topay members and the value of funds available.

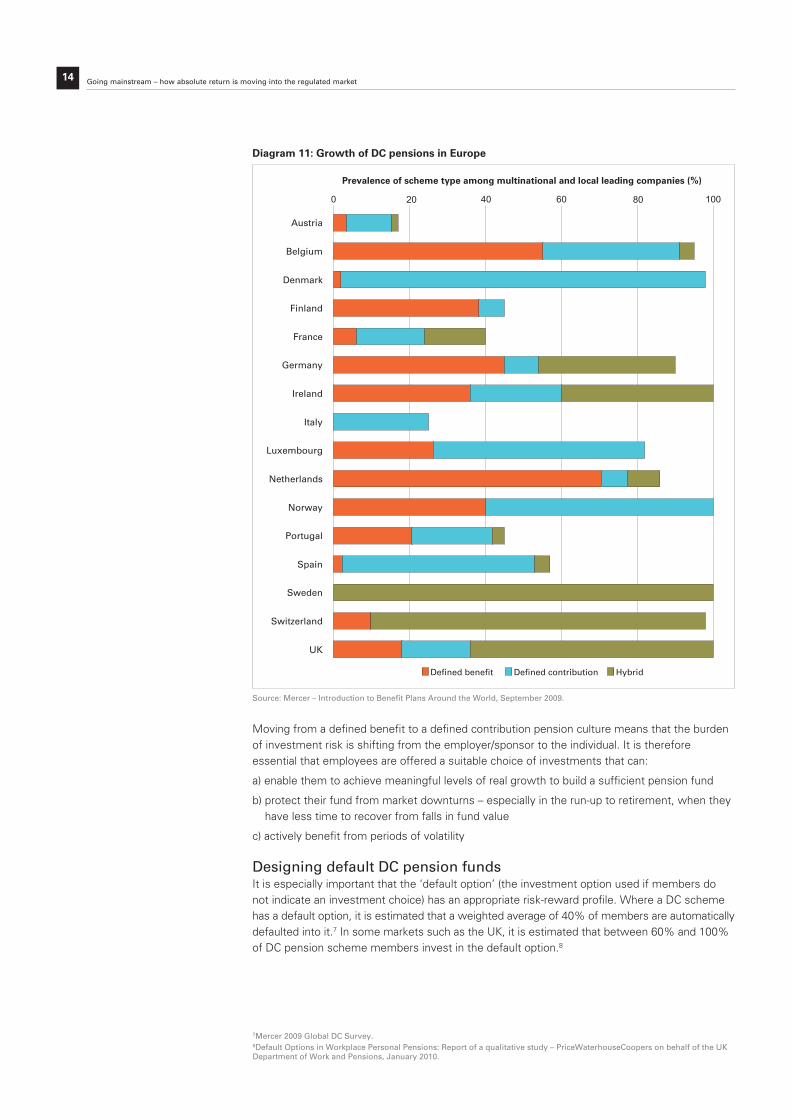

As a result, a growing proportion of employers are turning to defined contribution (DC) schemes,where the size of the pension fund at retirement is dependent on size of contribution andperformance of the pension funds selected by the employee. Diagram 11 shows the estimatedproportion of major company pension schemes across Europe that are now managed on a DB,DC or ‘hybrid’ basis (eg on a DC basis with some form of benefit guarantee). This indicates thatdefined benefit schemes now only account for more than half of corporate pension schemeprovision in two major European markets – the Netherlands and Belgium.

AbsoluteReturn Bond

Fund

UKGovernmentBonds

UK CorporateDebt

UK High YieldDebt

Commodities GlobalEquities

Absolute Return Bond Fund – 0.57 0.03 -0.30 0.14 -0.32

UK Government Bonds 0.57 – 0.43 -0.28 -0.07 -0.11

UK Corporate Debt 0.03 0.43 – 0.57 -0.19 0.50

UK High Yield Debt -0.30 -0.28 0.57 – -0.20 0.64

Commodities 0.14 -0.07 -0.19 -0.20 – 0.01

Global Equities -0.32 -0.11 0.50 0.64 0.01 –

Going mainstream – how absolute return is moving into the regulated market14

Diagram 11: Growth of DC pensions in Europe

Source: Mercer – Introduction to Benefit Plans Around the World, September 2009.

Moving from a defined benefit to a defined contribution pension culture means that the burdenof investment risk is shifting from the employer/sponsor to the individual. It is thereforeessential that employees are offered a suitable choice of investments that can:

a) enable them to achieve meaningful levels of real growth to build a sufficient pension fund

b) protect their fund from market downturns – especially in the run-up to retirement, when theyhave less time to recover from falls in fund value

c) actively benefit from periods of volatility

Designing default DC pension fundsIt is especially important that the ‘default option’ (the investment option used if members donot indicate an investment choice) has an appropriate risk-reward profile. Where a DC schemehas a default option, it is estimated that a weighted average of 40% of members are automaticallydefaulted into it.7 In some markets such as the UK, it is estimated that between 60% and 100%of DC pension scheme members invest in the default option.8

0 20 40 60 80 100

Austria

Belgium

Denmark

Finland

France

Germany

Ireland

Italy

Luxembourg

Netherlands

Norway

Portugal

Spain

Sweden

Switzerland

UK

Prevalence of scheme type among multinational and local leading companies (%)

Defined benefit Defined contribution Hybrid

7Mercer 2009 Global DC Survey.8Default Options in Workplace Personal Pensions: Report of a qualitative study – PriceWaterhouseCoopers on behalf of the UKDepartment of Work and Pensions, January 2010.

Going mainstream – how absolute return is moving into the regulated market 15

A common default option is a lifestyling, or ‘target date’, strategy. This may begin as 100%invested in global equity, moving to a final allocation of bonds and cash, with the switch typicallystarting five to 10 years before retirement. Typically, the equity element is passively invested,meaning that investors are fully exposed to market declines. Should we experience a repeat ofthe market decline witnessed in 2008, then a pension scheme member who is 100% invested ina passively-managed global equity fund is likely to have seen their fund fall in value by a third.

Granted, a lifestyling option will only expose members to this level of equity risk 10 years or morebefore their selected retirement date. However, this level of decline in pension assets across40-100% of the working population may be viewed as unacceptable – politically and economically.

Absolute return funds could have a crucial role in helping to manage these investment risks formillions of individuals. If included as part of a default option, an absolute return strategy couldpotentially enable members to:

achieve cash-plus returns at low levels of risk

reduce their reliance on equity market performance

generate investment returns even when markets are falling

For investors nearing retirement, absolute return funds can also offer a benefit over traditionalbond funds in that their performance won’t be tied to the same factors (ie bond yields) that willultimately determine the return that retirees achieve on their retirement annuity.

To date, interest among DC pension schemes in absolute return approaches has been low,partially because so few funds have the three-year performance record generally required bytrustees and consultants. However, anecdotal data suggests that major employers are startingto introduce absolute return strategies in their default DC fund design.

We accept that an investment strategy using derivatives to achieve investment return is likelyto be viewed with caution by both trustees and scheme members. However, as the effectiverisk reduction attributes of absolute return strategies become better known and more fundsbuild a sufficient performance record, we anticipate these funds will play a growing role in DCpension scheme design – and in any investment vehicle where preservation of investmentgrowth is key.

In shortIncreased market volatility, reduced risk diversification opportunities and sustained low interestrates could all potentially drive demand for absolute return approaches. Plus, as more individualsare required to manage their own investment risks, the ability to achieve attractive returnswhile limiting downside losses will be increasingly valuable.

In the next section we look at how these attributes of absolute return funds can be employedmost effectively within a portfolio.

‘as more individuals arerequired to managetheir own investmentrisks, the ability toachieve attractivereturns while limitingdownside losses will beincreasingly valuable.’

Going mainstream – how absolute return is moving into the regulated market16

Part Four: Employing absolute return in a portfolio

As we have hoped to show throughout this paper, mainstream interest in absolute returnstrategies is strong and there are many drivers that may cause this approach to becomemore dominant.

However, we do not believe absolute return investing should be viewed as a replacement forrelative return investing. Rather, it is a valuable component that can be used to enhance a portfolio’srisk-reward profile. In this section, we want to explore how absolute return strategies differ fromtheir relative return counterparts and consider what this tells us about the role that absolute returnmight play within a portfolio.

i. Investment attributes of absolute return and relative returnRelative return and absolute return strategies both offer investors a valuable set of attributes –each of which have their role to play within an investment portfolio.

To demonstrate this, we have compared two Threadneedle UK-registered OEIC funds that investin the same universe.

Absolute return (AR) – Threadneedle Absolute Return Bond Fund is an absolute returnstrategy investing in global bond markets. It employs a cash enhancement approach and canuse both long and short positions. Its benchmark is 3-month LIBOR.

Relative return (RR) – Threadneedle Global Bond Fund is a long-only strategy investingin global bond markets. (NB: Although its stated aim is as a total return fund, this fund’s long-only approach enables us to treat it as a relative return fund.) Its benchmark is the JPMGlobal Bond Ex Japan Index.

Diagram 12 shows discrete quarterly returns for these two funds over the four most recentcalendar years. The JPM Global Bond ex Japan Index is included as proxy for the global bondmarket (the fund data is therefore gross of fees and tax to enable like-for-like comparisons).

2006-2009 is the only four-year period for which data for both funds is available (ThreadneedleAbsolute Return Bond Fund was launched in November 2005). The limitations of demonstratingfund performance over one short period of time are acknowledged. There again, the extremesexperienced in fixed income markets over these four years makes them a very interestingtest period to assess how relative return and absolute return strategies behave in differentmarket conditions.

Going mainstream – how absolute return is moving into the regulated market 17

Diagram 12: Quarterly returns from absolute return and relative return bond strategies 2006-2009

Note: All data is quoted in: GBP. Fund data is sourced from Morningstar. Index data provided by Thomson Reuters Datastreamand JPMorgan. Fund data is quoted on a Bid-Bid basis with Income re-invested at Bid. Fund data is gross of tax and totalexpense ratios to facilitate comparison with indices.

Diagram 13 – Risk analysis of absolute return and relative return bond funds

Note: we have shown risk measures over three years as this is conventional for these metrics *assumes 4% risk-free rate.Source: Morningstar. As at 31 December 2009.

We can make a number of observations about the performance of the two funds over this period:

Absolute performance the absolute return (AR) strategy delivered the most consistent positive returns – delivering

positive performance in 14 out of 16 periods.

the AR strategy achieved positive returns in five out of eight periods when market returnswere negative; the RR fund posted negative returns in all eight periods that market returnswere negative.

The AR fund only outperformed a positive market return in two instances (Q406 and Q307) –in both cases these immediately followed a negative market return.

Volatility the AR strategy experienced a narrower band of returns, with shallow gains and losses.

the RR fund achieved a much wider range of returns (although the range reduces significantlyif we strip out the anomalous returns of Q408).

Both funds have delivered positive risk-return results as measured by Sharpe and Information Ratios. In both cases, the absolute return fund has delivered the higher returnper unit of risk taken.

Returns the RR fund achieved its strongest returns when bond market returns were also highly positive.

the AR fund was most likely to lag both the market and the RR fund during periods of strongbond market performance – however, these were also the periods when the AR fund deliveredits highest positive returns.

-20

-10

0

10

20

30

40

Q1 06 Q306 Q107 Q307 Q108 Q308 Q109 Q309

Ret

urn

(%

)

ABSOLUTE RETURN – Threadneedle Absolute Return Bond Fund

RELATIVE RETURN – Threadneedle Global Bond Fund

MARKET RETURN – JPM Global (ex Japan) Bond Index

Risk analysis over 3 years Threadneedle Absolute Return Bond Fund Threadneedle Global Bond Fund

Absolute volatility 4.0% 15.0%

Sharpe Ratio* 1.34 0.72

Information Ratio 1.22 0.23

Going mainstream – how absolute return is moving into the regulated market18

With the strong caveat that this data is quite limited and covers only a brief period of time, wecan assign certain groups of attributes to the absolute return and the relative return funds –shown in Diagram 14 below:

Diagram 14: Key attributes of absolute v relative return funds

ii. Allocating strategies by market environmentFrom these attributes, we can conclude that there are market environments when it maybenefit an investor to favour absolute return strategies over relative return strategies and viceversa. We would summarise these periods as follows:

Diagram 15: Potential strategy weighting against market performance

In summary, absolute return funds are likely to offer the best return when the marketenvironment is negative or volatile on a sustained basis. Relative return funds offer the strongreturn opportunity when markets are experiencing a strong growth phase. Outperformance ofeither type of fund is less apparent when markets are in the very early stages of recovery. Thatsaid, the consistently lower volatility of absolute return funds may lead investors to favour themin uncertain market conditions.

To test these conclusions, we wanted to see how rotating weightings to these two differentstrategies would have affected returns over the four-year period. We also wanted to see ifactively allocating between the two strategies would be more effective than statically allocatingweightings to them. To do this, we tested six portfolios:

Portfolios 1 and 2 are 100% invested in the Absolute Return and the Relative Return strategiesrespectively for the whole period.

Portfolio 3 is evenly weighted 50:50 across the Absolute Return and the Relative Returnstrategies for the whole period.

Portfolio 4 is overweight Absolute Return, with the portfolio allocated 70% Absolute Return:30% Relative Return for the whole period.

Portfolio 5 is overweight Relative Return, with the portfolio allocated 30% Absolute Return:70% Relative Return for the whole period.

Portfolio 6 is rotated between the two funds in line with the market environment as shown inDiagram 16:

Q106-Q207 – 100% Absolute ReturnQ307-Q408 – 100% Relative ReturnQ109-Q409 – 100% Absolute Return

Absolute return fund Relative return

Narrow range of returns in all market conditions Broader range of returns – widening when marketreturns are also extreme

Likely to deliver positive outperformance when marketreturns are negative

Likely to deliver negative returns when market returnsare negative

Potential to outperform when markets are in initialrecovery – but not conclusive

Potential to outperform when markets are in initialrecovery – but not conclusive

Likely to underperform relative return funds whenmarkets are rising strongly

Potential to deliver very strong positive returns whenmarkets are rising strongly

Marketenvironment

Stronglynegative

Mediumnegative/volatile

Initial recovery

Medium positive

Strongly positive

Absolute ReturnFund

OVERWEIGHT OVERWEIGHT EQUAL WEIGHT UNDERWEIGHT UNDERWEIGHT

Relative ReturnFund

UNDERWEIGHT UNDERWEIGHT EQUAL WEIGHT OVERWEIGHT OVERWEIGHT

Going mainstream – how absolute return is moving into the regulated market 19

Diagram 16: Fund rotation for Portfolio 6

Source: Morningstar, Thomson Reuters Datastream and JPMorgan.

The performance results of the six portfolios are shown in Diagram 17 below. We can see that,of the two ‘pure’ bond portfolios (see Portfolios 1 and 2), the relative return portfolio producedthe highest total return over the period but with almost four times the volatility of the absolutereturn portfolio.

Combining the two strategies in different static combinations (Portfolios 3, 4 and 5) has helpedto improve return and reduced the worst quarterly loss. However the most dramatic resultshave come from Portfolio 6, where allocation between the two portfolios has been activelyrotated. Here we see that the total return is almost double the return from any of the other fiveportfolios while the worst quarterly loss is just -4.0%. Upside has been dramatically enhancedwhile downside losses have been limited.

Diagram 17: Performance of test portfolios 2006-2009

Source: Morningstar.

Caveats to this data must be stressed:- Performance is based on one specific period of time.

- Data is based on the performance of two specific funds and therefore may not be representativeof the behaviour of all relative return and absolute return strategies.

- This data only relates to global bonds – extrapolation for other asset classes needs to be treatedwith caution.

0

1

Q Q Q Q Q Q Q Q

Ret

urn

(%)

-20

-10

20

30

40

Q1 06 Q3 06 Q1 07 Q3 07 Q1 08 Q3 08 Q1 09 Q3 09

100% Absolute Return 100% Absolute Return100% Relative Return

ABSOLUTE RETURN – Threadneedle Absolute Return Bond Fund

RELATIVE RETURN – Threadneedle Global Bond Fund

MARKET RETURN – JPM Global (ex Japan) Bond Index

Portfolio Total return Quarterly Return Volatility

Best Median Worst

Portfolio 1100% Absolute Return

36.5% 7.4% 1.2% -3.4% 5.7%

Portfolio 2:100% Relative Return

45.3% 37.4% -0.6% -10.5% 20.9%

Portfolio 3:50% Absolute Return50% Relative Return

42.5% 22.4% 0.3% -3.9% 12.6%

Portfolio 4:75% Absolute Return 25% Relative Return

40.5% 16.4% 0.7% -3.6 9.4%

Portfolio 5:25% Absolute Return 75% Relative Return

44.0% 28.4% 0.0% -6.6% 15.8%

Portfolio 6:Rotated portfolio– see Diagram 16

88.8% 37.4% 1.2% -4.0% 18.3%

Going mainstream – how absolute return is moving into the regulated market20

- We have been able to determine the optimal rotation points for the two strategies in retrospect.In real life, an investor is highly unlikely to anticipate inflexion points in the markets so accurately.

- Rotating between strategies can give rise to additional dealing costs or tax liabilities, whichhave not been accounted for in our data.

Nonetheless we would suggest that our data tentatively indicates two points:

1. Portfolios that are able to have exposure to both relative return and absolute return funds arelikely to have a more attractive risk-return profile than portfolios that are restricted to one typeof strategy;

2. Actively rotating a portfolio’s allocation towards either absolute return or relative return,depending on the market environment, can significantly enhance returns and reducedownside losses.

iii. Defining a new source of returnInvesting in absolute or relative return strategies is not an either/or decision. Our researchsuggests that holding both relative and absolute return strategies can improve a portfolio’s risk-return profile.

But, more than this, our research suggests each type of strategy can offer greater or lesserattractions in different market environments. As such, actively managing allocations to relativeand absolute return strategies in response to the market environment can further enhanceportfolio performance.

This suggests that the decision to skew a portfolio towards either a relative return or absolutereturn bias can be treated as an additional source of investment return alongside othertraditional investment decisions, such as to which asset classes and markets to allocate – see Diagram 18 below.

In our exercise, we have shown the behaviour of absolute and relative return funds within theglobal bond sector. But the decision to rotate between the two philosophies could equally bemade for other asset classes. In this way, investors or portfolio managers have another usefullever by which to generate return and manage risk.

Diagram 18: Increasing the sources of return in a portfolio

In shortThe particular set of attributes offered by absolute return strategies can play a valuablerole in a portfolio and are especially effective when used in combination with relativereturn funds – particularly if allocations are actively managed.

In the last section of the report, we will consider how absolute return funds need to beevaluated so that investors can identify appropriate and well-managed strategies.

Sources of return in a portfolio

Cash

Asset allocation

Bonds Equities Other

Market Market Market

Absolute/Relative

Absolute/Relative

Absolute/Relative

‘The particular set ofattributes offered byabsolute returnstrategies can play avaluable role in aportfolio and areespecially effectivewhen used incombination withrelative return funds –particularly ifallocations are activelymanaged.’

Going mainstream – how absolute return is moving into the regulated market 21

Part Five:Evaluating absolute return strategies

Absolute return funds are a highly valuable tool for investors and their wider availabilityshould be welcomed. Even so, it needs to be fully understood that investing to produce a consistently positive return is a different discipline from investing to beat a marketbenchmark and requires a different, less widely-available skill set.

Concerns over the availability of appropriate skills to manage absolute return strategies in theregulated market have been voiced widely. In a recent review of the UK asset managementindustry conducted by the Investment Management Association, a number of IMA memberfirms interviewed voiced doubts about the ability of a large number of firms to achieve absolutereturns consistently. One respondent remarked:

“Even if 100% of the population decided that they wanted an absolute return product, itshould not be used as a substitute for relative return. The talent and capability is not there to deliver it.”9

The absolute return sector has been one of the biggest-selling sectors since the credit crisis.We believe there is a real risk that, as demand for absolute return funds continues, less able orexperienced asset managers may look to fill this demand.

In addition, there is still a strong tendency to treat the absolute return market as a homogenoussector of low-risk strategies when, in fact, it contains a huge diversity of investment approacheswith a very wide range of risk profiles. So even where a manager is experienced, investors maybe tempted to invest in strategies that may not be appropriate in terms of their risk profile orinvestment remit. In some cases, investors may be over-confident simply because a fund isUCITS-compliant.

Conducting due diligenceFor all the reasons above, we believe investors need to place substantial emphasis on duediligence when selecting an absolute return fund and its manager.

To ensure that investors make appropriate choices, we believe management firms should makeinformation on all of the following aspects of their funds and processes readily available.

1. Management team’s experienceManaging an absolute return strategy is a different discipline from relative return investing. The portfolio team and its associated analysts should have an established record in absolutereturn investing – particularly where a strategy involves short-selling.

Given that track records in the regulated absolute return sector are still relatively short, a strongperformance record in the unregulated hedge-fund sector is currently a major bonus, althoughwe expect this will recede as the regulated absolute return sector builds a long-termperformance record.

It is also important to remember that the additional strictures imposed by UCITS III in terms ofliquidity, leverage and permissible investments mean that hedge fund managers who have beensuccessful in their offshore strategies may not necessarily achieve the same results in theirregulated fund versions.

Firms that possess extensive experience in both the unregulated and regulated fund marketsmay be best positioned to deliver strong performance in the regulated absolute return sector.

9Asset Management in the UK 2008 – Investment Management Association, published July 2009.

Going mainstream – how absolute return is moving into the regulated market22

2. Target returnAn absolute return fund’s target return (be it an absolute figure or the excess over its benchmark)can be a good initial indicator of a strategy’s risk profile. The higher the target return, the moreaggressive a strategy will need to be.

Obviously, an investor should also analyse a fund’s success in achieving its target return. Again,given the immaturity of most regulated absolute return funds, most performance track recordsare too short to indicate levels of performance consistency.

3. Timeframe to deliver the target returnFunds should indicate over what period they intend to deliver their target absolute return. Inmany cases, the timeframe to deliver a positive return is 12 months but other funds mayannualise their performance over a period of three years. Investors need to consider if thetarget return is consistently achievable in the expected timeframe. The shorter the timeframe,the less risk a fund can afford to take.

4. Suitability of the fund’s benchmarkAn absolute return fund will typically measure its performance against a ‘risk-free rate’ – such asa cash benchmark, or against inflation. A benchmark is only relevant if it accurately reflects a fund’sinvestable neutral position – ie how it would invest, and the return that would be achieved, if theportfolio manager had no investment view. Otherwise, a benchmark is simply acting as an arbitraryhurdle rate for the fund.

A cash benchmark indicates a target return above zero. Even so, investors should be aware thatif the interest rate on the cash benchmark drops sharply, so will the fund’s target return.

5. Suitability of underlying asset classesAs with any type of investment fund, the suitability of the underlying asset classes needs to beassessed against an investor’s risk profile. While absolute return funds generally look to reducemarket volatility, an absolute return fund investing in emerging markets is still likely to be morevolatile than a fund that focuses on investment grade bonds.

6. Transparency of risk allocationThe portfolio manager should be able to indicate all sources of return in a fund. There should betransparency as to how and where risk is being budgeted to achieve the target return – and thereasoning behind each risk allocation.

7. Volatility parametersAbsolute return funds will often have a remit to deliver cash-plus returns with as little volatilityas possible. If so, they should impose limits on the maximum absolute volatility that returnsshould experience and have a clear strategy to ensure that portfolio fluctuations remain withinthese parameters. Investors should be able to assess to what extent a fund has remained withinthese parameters and be able to access information about the maximum drawdown (the maximumpercentage loss from peak to trough) experienced by a fund over different time periods.

8. Correlation with marketsWhere an absolute return fund aims to strip out market risk, its correlation with the markets inwhich it invests should be low (ie close to zero). Persistently high correlation suggests returnsare dependent on capturing beta rather than manager skill.

9. Credit riskWhere an absolute return strategy invests extensively in cash instruments, the credit quality ofthese instruments needs to be assessed carefully. Some funds may restrict themselves tohighly-rated treasury securities. Some credit instruments may involve high exposure to particularsectors such as financials. An absolute return manager with high cash exposure should demonstratethe skills and resources to monitor the credit risk of the cash instruments they hold.

Going mainstream – how absolute return is moving into the regulated market 23

10. Market leverageUCITS funds are not permitted to borrow to finance investment positions. However, derivativescan be used to gain market exposure for only a small initial outlay – which creates ‘marketleverage’. Like any kind of leverage this can amplify both gains and losses, so the fund’s policyon maximum levels of leverage needs to be clear.

11. Access and liquidityAuthorised absolute return funds have to adhere to strict requirements regarding investor accessand liquidity. Even so, a fund should have a clear policy to manage redemptions and minimisethe need to sell investments or unwind positions involuntarily if there are high net outflows fromthe fund. Liquidity should be assessed particularly carefully where a hedge fund manager hasonly recently entered the authorised fund market for the first time and is less experienced inworking within the liquidity restrictions demanded by UCITS regulations.

12. FeesMany absolute return funds solely levy conventional ad valorem annual management charges,but some may also have a performance fee. This may be deducted as a percentage of anyoutperformance in the net asset value above a stated hurdle rate. The hurdle rate, the basis forthe high water mark and the size of the performance fee all need to be assessed alongside allother ongoing charges.

In shortUntil there is sufficient mass to classify different absolute return strategies with greater granularity,deep due diligence remains essential in order to differentiate between strategies, theirrespective goals and risk profiles – as well as the experience and skills of each managementteam. Investors also have to be mindful that track records in the sector are still very short and itis difficult to assess managers on their past performance. In particular, it is still hard to see whichmanagers are achieving their target return consistently. This will become less of an issue overtime. However, while the majority of constituents have performance records of less than fiveyears, investors need to proceed cautiously when selecting funds. It is also important to rememberthat track records in the unregulated fund market may not always be replicable in a regulatedfund which has additional liquidity, leverage and investment constraints.

‘deep due diligenceremains essential inorder to differentiatebetween strategies’

Going mainstream – how absolute return is moving into the regulated market24

Conclusion

Absolute return strategies have been available in the regulated European investment market forless than a decade. They still account for only a small fraction of funds under management –around EUR50 billion of a European UCITS market that is estimated to be worth EUR5,299 billionaccording to the European Fund and Asset Management Association (EFAMA).

Yet the market is growing swiftly and interest in it has accelerated as investors seek new ways tomanage risk and combine the best elements of the hedge fund market and the regulated market.

Even during the period that it has taken to write this report, we have seen many new fund launches,often from established and respected names in the hedge fund industry entering the regulatedfund market for the first time.

The role of absolute returnThe attributes demonstrated by absolute return funds (low volatility, cash-plus returns, low marketcorrelation) enable them to play a unique role in a portfolio in terms of steadying performancethroughout the market cycle and enabling investors to achieve attractive returns in both up anddown markets. As more onus is placed on private individuals to shoulder investment risk, theseattributes should become increasingly prized.

But absolute return funds are not a cure-all. There are times when they will underperform otherfunds. As such, absolute return strategies are most powerful as part of a diversified portfoliothat also includes traditional relative return strategies. Given the growing diversity of the absolutereturn sector, it is now possible for investors to ‘match’ relative and absolute return approachesacross many different asset classes including equities, government bonds, credit and currency,and across both developed and emerging markets.

It is often assumed that – given their typically low-risk profile – absolute return funds will generallybe treated as a “static” long-term portfolio holding. Certainly, they can play this role very well.

But we also envisage that many investors will look to use absolute return strategies in moredynamic ways. As our analysis has shown, actively rotating between relative return and absolutereturn strategies at different stages of the market cycle can have a dramatic and positive impacton returns achieved and losses avoided. As such, the decision to allocate to absolute return orrelative return could be treated as an additional source of value-add in an investment strategy,alongside other traditional asset allocation and market allocation decisions.

Winners in the sectorOur key concern for the sector is whether investor demand can be matched by manager skill. It is understandable that fund managers may view absolute return as a means to stymie fundoutflows at times of market volatility or downturn. But absolute return investing is a specialistskill that relative return managers cannot acquire overnight. The skills required can be found inthe unregulated hedge fund market but those managers, conversely, have to be able to adapt tothe great restrictions on permissible investments, leverage, liquidity and risk management thatthe regulated fund market demands.

The absolute return managers that are likely to do best – and are likely to be seen of greatest value –therefore, are those that both possess a long-term track record in the hedge fund market andalso deep experience of compliance in the regulated fund market. Managers possessing onlyone of these sets of attributes are likely to struggle to meet investor (and regulator) expectations.

Going mainstream – how absolute return is moving into the regulated market 25

Diagram 19: Skills convergence of high-value absolute return managers

Equally, there is a concern that investors may be lulled by the presence of a regulated fund structureto invest in quasi-hedge fund strategies that are not appropriate. Absolute return funds are oftenbought as low-risk investments but this is not always the case. The risk-reward profiles of thesefunds can vary hugely and investors must not assume that cash-plus returns mean cash-likelevels of risk.

For all these reasons, deep due diligence is essential. The promise of absolute returns is veryenticing – and will continue to attract strong inflows over the next five to 10 years. The biggestchallenge for investors now is determining which managers and which funds can consistentlydeliver on that promise.

Hedge fundexperience Short-selling Leverage Derivative

management

High-valueabsolute returnmanagers

UCITS experience Liquidity rules Investment &

leveragerestrictions

Reportingrequirements

06.10/ T2335_Valid to 12.10

Important informationPlease remember that past performance is not a guide to the future and the value of investments can fall as well as rise, and therefore an investor may not get back theamount invested. Changes in exchange rates may also affect the value of investments. The research and analysis included in this document has been produced byThreadneedle for its own investment management activities, may have been acted upon prior to publication and is made available here incidentally. Information obtainedfrom external sources is believed to be reliable but its accuracy or completeness cannot be guaranteed. Any opinions expressed are made as at the date of publicationbut are subject to change without notice. Subscriptions to a fund may only be made on the basis of the current Prospectus or Simplified Prospectus and the latest annualor interim reports, which can be obtained free of charge on request. The Absolute Return Bond Fund may hold up to 100% in cash or money market securities. Therefore,investors should be aware that the Fund may not participate fully in a market rise. The Fund’s exposure involves short sales of securities and leverage which increasesthe risk of the Fund. Short selling is designed to make a profit from falling prices. However, if the value of the underlying investment increases, the short position willnegatively affect the Fund’s value. Leverage amplifies the effect of changes in the price of an investment on the Fund’s value. As such, leverage can enhance returns toshareholders but can also increase losses. For the avoidance of doubt, this Fund does not offer any form of guarantee with respect to investment performance, and noform of capital protection will apply. The Global Bond Fund may deduct its annual management charge from capital rather than income. This may erode capital orreduce the potential for capital growth over time. The interest rate on most government and corporate bonds will not increase in line with inflation. Thus, over time, thereal value of investors’ income could fall.

Issued by Threadneedle Asset Management Limited. Authorised and regulated by the FSA. Registered in England & Wales No 984167, 60 St Mary Axe, London EC3A8JQ. Threadneedle is a brand name, and both the name and logo are trademarks or registered trademarks of the Threadneedle group of companies. threadneedle.co.uk

For investment professional use only(not for onward distribution to, or to be relied upon by, private investors).