GLOBAL VALUE CHAINS AND TRADE IN VALUE … VALUE CHAINS AND TRADE IN VALUE ADDED: THE NEED FOR NEW...

25

GLOBAL VALUE CHAINS AND TRADE IN VALUE ADDED: THE NEED FOR NEW POLICY THINKING Nadim Ahmad, Head of Trade and Competitiveness Statistics Division 1 Copenhagen: 21 November, 2016

-

Upload

truongtuong -

Category

Documents

-

view

218 -

download

1

Transcript of GLOBAL VALUE CHAINS AND TRADE IN VALUE … VALUE CHAINS AND TRADE IN VALUE ADDED: THE NEED FOR NEW...

GLOBAL VALUE CHAINS AND TRADE IN

VALUE ADDED:

THE NEED FOR NEW POLICY THINKING

Nadim Ahmad, Head of Trade and Competitiveness Statistics Division 1

Copenhagen: 21 November, 2016

International fragmentation of production

Explosion of trade in intermediates as firms specialise in stages (tasks) of production

2

Escape slides: Air Cruisers (USA)

Horizontal Stabiliser:

Alenia Aeronautica (Italy)

Centre fuselage: Alenia Aeronautica (Italy)

Final assembly: BoeingCommercial Airplanes (USA)

Vertical Stabiliser: Boeing

Commercial Airplanes (USA)

Landing gear: Messier-Dowti (France)

Electric brakes: Messier-Bugatti (France)

Tires: Bridgestone Tires (Japan)

Doors & windows:

Zodiac Aerospace (USA)

PPG Aerospace (USA)

Tools/Software: Dassault Systemes (France)

Navigation: Honeywell (USA)

Pilot control system: Rockwell Colins (USA)

Wiring: Safran (France)

Centre wing box:

Fuji Heavy Industries (Japan)

Engines: GE Engines (USA),

Rolls Royce (UK)

Wing box: Mitsubishi Heavy Industries (Japan)

Wing ice protection: GKN Aerospace (UK)

Engine nacelles: Goodrich (USA)Aux. power unit: Hamilton

Sundstrand (USA)

Flight deck seats:

Ipeco (UK)

Lavatories:

Jamco (Japan)

Cargo doors: Saab (Sweden)

Forward fuselage:

Kawasaki Heavy Industries (Japan)

Spirit Aerosystems (USA)

Raked wing tips: Korean Airlines

Aerospace division (Korea)

Passenger doors:

Latécoère Aéroservices (France)

Prepreg composites:

Toray (Japan)

Rear fuselage:

Boeing South Carolina (USA)

Final consumption

3

7

5

62

Final assembly

1

4

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1

23

4

5

67

Value added in the country of final production

Value added by first tier suppliers

Value added by second tier suppliers

Trade in inputs (first

tier suppliers)

Trade in inputs(second tier

suppliers)

Decomposition of gross exports

Resulting in multiple counting…..

…..in conventional trade statistics

• With the potential to create ‘misleading perceptions’ and imperfect policies:

3

0

20

40

60

80

100

120

140

160

180

200

Ex

po

rts

Imp

ort

sE

xp

ort

sIm

po

rts

Ex

po

rts

Imp

ort

sE

xp

ort

sIm

po

rts

Ex

po

rts

Imp

ort

sE

xp

ort

sIm

po

rts

Ex

po

rts

Imp

ort

sE

xp

ort

sIm

po

rts

Ex

po

rts

Imp

ort

sE

xp

ort

sIm

po

rts

Ex

po

rts

Imp

ort

sE

xp

ort

sIm

po

rts

Ex

po

rts

Imp

ort

sE

xp

ort

sIm

po

rts

Ex

po

rts

Imp

ort

sE

xp

ort

sIm

po

rts

Ex

po

rts

Imp

ort

sE

xp

ort

sIm

po

rts

Ex

po

rts

Imp

ort

sE

xp

ort

sIm

po

rts

Ex

po

rts

Imp

ort

sE

xp

ort

sIm

po

rts

Ex

po

rts

Imp

ort

sE

xp

ort

sIm

po

rts

Ex

po

rts

Imp

ort

sE

xp

ort

sIm

po

rts

Ex

po

rts

Imp

ort

sE

xp

ort

sIm

po

rts

Ex

po

rts

Imp

ort

sE

xp

ort

sIm

po

rts

Ex

po

rts

Imp

ort

sE

xp

ort

sIm

po

rts

Ex

po

rts

Imp

ort

sE

xp

ort

sIm

po

rts

LUX IRL SVK HUN EST BEL NLD CZE SVN CHE ISL DNK KOR AUT POL DEU SWE PRT FIN NOR ISR CHL MEX ESP GRC CAN GBR NZL ITA FRA TUR AUS JPN USA

Gross Trade, % of GDP

1993 2013

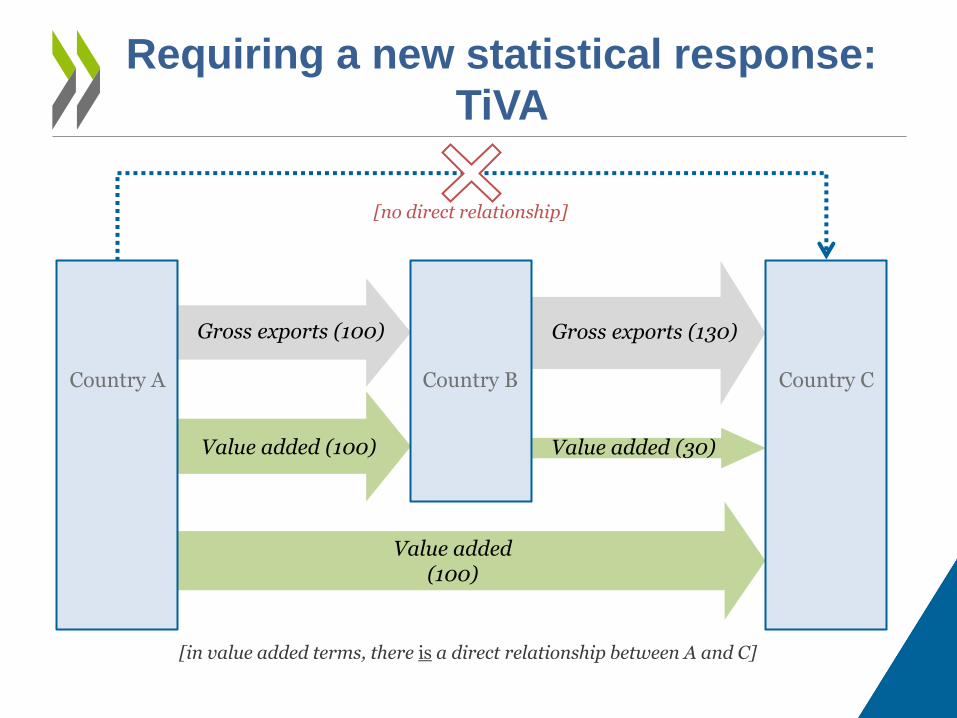

Requiring a new statistical response:

TiVA

Gross exports (100) Gross exports (130)

Value added (100)

Value added (100) Value added (30)

Country A Country B Country C

[no direct relationship]

[in value added terms, there is a direct relationship between A and C]

Most intermediate imports are used for exports..

5

0%

10%

20%

30%

40%

50%

60%

70%

80%

Agric

ulture

Min

ing

Food p

roducts

Textile

s &

appare

l

Wood &

paper

Coke &

petrole

um

Chem

icals

Rubber &

pla

stics

Non-m

eta

llic

min

erals

Basic

meta

ls

Fabric

ate

d m

eta

ls

Machin

ery

ICT &

ele

ctronic

s

Ele

ctric

al m

achin

ery

Moto

r vehic

les

Oth

er tra

nsport

Oth

er m

anufa

ctu

res

Utilities

Whole

sale

, re

tail &

hote

ls

Tra

nsport &

tele

com

s

Fin

ance &

insura

nce

Busin

ess s

erv

ices

Oth

er s

erv

ices

Tota

l

2011 2009 2008

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

Agric

ulture

Min

ing

Food p

roducts

Textile

s &

appare

l

Wood &

paper

Coke &

petrole

um

Chem

icals

Rubber &

pla

stics

Non-m

eta

llic

min

erals

Basic

meta

ls

Fabric

ate

d m

eta

ls

Machin

ery

ICT &

ele

ctronic

s

Ele

ctric

al m

achin

ery

Moto

r vehic

les

Oth

er tra

nsport

Oth

er m

anufa

ctu

res

Utilities

Whole

sale

, re

tail &

hote

ls

Tra

nsport &

tele

com

s

Fin

ance &

insura

nce

Busin

ess s

erv

ices

Oth

er s

erv

ices

Tota

l

2011 2009 2008

0%

10%

20%

30%

40%

50%

60%

70%

80%

Agric

ulture

Min

ing

Food p

roducts

Textile

s &

appare

l

Wood &

paper

Coke &

petrole

um

Chem

icals

Rubber &

pla

stics

Non-m

eta

llic

min

erals

Basic

meta

ls

Fabric

ate

d m

eta

ls

Machin

ery

ICT &

ele

ctronic

s

Ele

ctric

al m

achin

ery

Moto

r vehic

les

Oth

er tra

nsport

Oth

er m

anufa

ctu

res

Utilities

Whole

sale

, re

tail &

hote

ls

Tra

nsport &

tele

com

s

Fin

ance &

insura

nce

Busin

ess s

erv

ices

Oth

er s

erv

ices

Tota

l

2011 2009 2008

0%

10%

20%

30%

40%

50%

60%

70%

80%

Agric

ulture

Min

ing

Food p

roducts

Textile

s &

appare

l

Wood &

paper

Coke &

petrole

um

Chem

icals

Rubber &

pla

stics

Non-m

eta

llic

min

erals

Basic

meta

ls

Fabric

ate

d m

eta

ls

Machin

ery

ICT &

ele

ctronic

s

Ele

ctric

al m

achin

ery

Moto

r vehic

les

Oth

er tra

nsport

Oth

er m

anufa

ctu

res

Utilities

Whole

sale

, re

tail &

hote

ls

Tra

nsport &

tele

com

s

Fin

ance &

insura

nce

Busin

ess s

erv

ices

Oth

er s

erv

ices

Tota

l

2011 2009 2008

Imported intermediate inputs used for exports, by import category: %

Sweden Norway

Finland Denmark

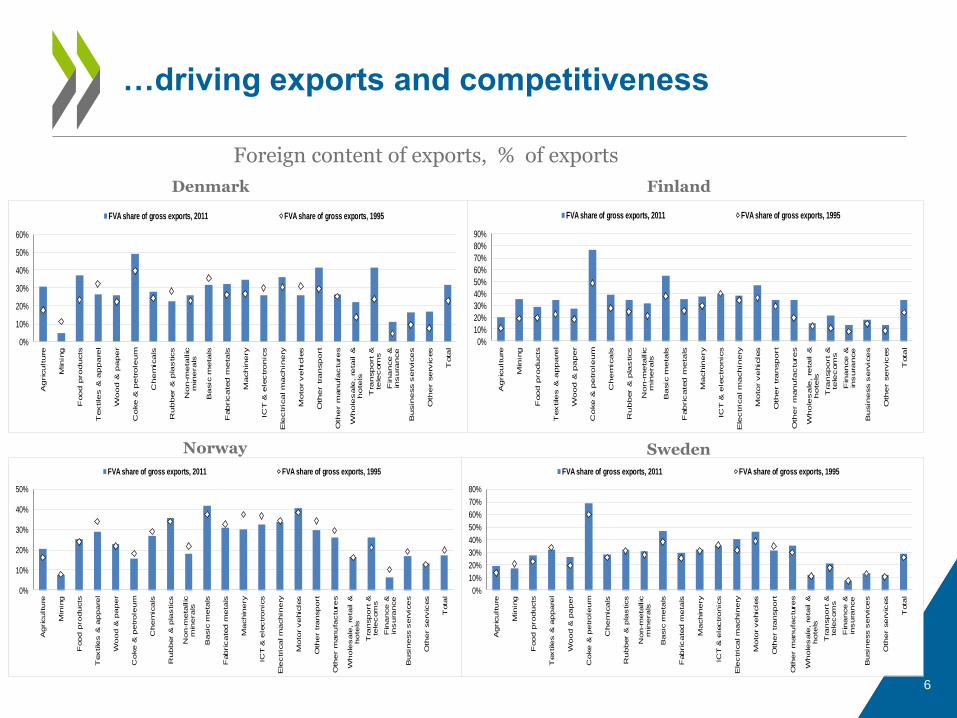

…driving exports and competitiveness

6

Foreign content of exports, % of exports

Sweden Norway

Finland Denmark

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

Agric

ulture

Min

ing

Food p

roducts

Textile

s &

appare

l

Wood &

paper

Coke &

petrole

um

Chem

icals

Rubber &

pla

stics

Non-m

eta

llic

min

erals

Basic

meta

ls

Fabric

ate

d m

eta

ls

Machin

ery

ICT &

ele

ctronic

s

Ele

ctric

al m

achin

ery

Moto

r vehic

les

Oth

er tra

nsport

Oth

er m

anufa

ctu

res

Whole

sale

, re

tail &

hote

ls

Tra

nsport &

tele

com

s

Fin

ance &

insura

nce

Busin

ess s

erv

ices

Oth

er s

erv

ices

Tota

l

FVA share of gross exports, 2011 FVA share of gross exports, 1995

0%

10%

20%

30%

40%

50%

60%

Agric

ulture

Min

ing

Food p

roducts

Textile

s &

appare

l

Wood &

paper

Coke &

petrole

um

Chem

icals

Rubber &

pla

stics

Non-m

eta

llic

min

erals

Basic

meta

ls

Fabric

ate

d m

eta

ls

Machin

ery

ICT &

ele

ctronic

s

Ele

ctric

al m

achin

ery

Moto

r vehic

les

Oth

er tra

nsport

Oth

er m

anufa

ctu

res

Whole

sale

, re

tail &

hote

ls

Tra

nsport &

tele

com

s

Fin

ance &

insura

nce

Busin

ess s

erv

ices

Oth

er s

erv

ices

Tota

l

FVA share of gross exports, 2011 FVA share of gross exports, 1995

0%

10%

20%

30%

40%

50%

Agric

ulture

Min

ing

Food p

roducts

Textile

s &

appare

l

Wood &

paper

Coke &

petrole

um

Chem

icals

Rubber &

pla

stics

Non-m

eta

llic

min

erals

Basic

meta

ls

Fabric

ate

d m

eta

ls

Machin

ery

ICT &

ele

ctronic

s

Ele

ctric

al m

achin

ery

Moto

r vehic

les

Oth

er tra

nsport

Oth

er m

anufa

ctu

res

Whole

sale

, re

tail &

hote

ls

Tra

nsport &

tele

com

s

Fin

ance &

insura

nce

Busin

ess s

erv

ices

Oth

er s

erv

ices

Tota

l

FVA share of gross exports, 2011 FVA share of gross exports, 1995

0%

10%

20%

30%

40%

50%

60%

70%

80%A

gric

ulture

Min

ing

Food p

roducts

Textile

s &

appare

l

Wood &

paper

Coke &

petrole

um

Chem

icals

Rubber &

pla

stics

Non-m

eta

llic

min

erals

Basic

meta

ls

Fabric

ate

d m

eta

ls

Machin

ery

ICT &

ele

ctronic

s

Ele

ctric

al m

achin

ery

Moto

r vehic

les

Oth

er tra

nsport

Oth

er m

anufa

ctu

res

Whole

sale

, re

tail &

hote

ls

Tra

nsport &

tele

com

s

Fin

ance &

insura

nce

Busin

ess s

erv

ices

Oth

er s

erv

ices

Tota

l

FVA share of gross exports, 2011 FVA share of gross exports, 1995

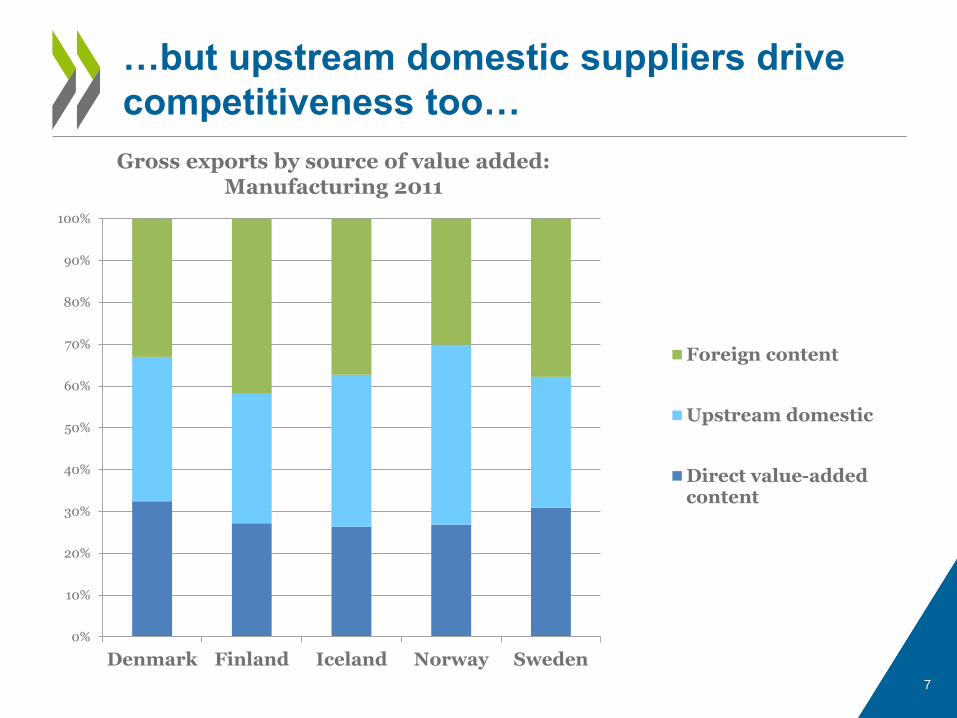

…but upstream domestic suppliers drive

competitiveness too…

7

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Denmark Finland Iceland Norway Sweden

Foreign content

Upstream domestic

Direct value-addedcontent

Gross exports by source of value added: Manufacturing 2011

….including services..

8

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

IDN

CH

L

KO

R

CH

N

US

A

ME

X

JP

N

GR

C

IND

CA

N

NO

R

AU

S

ZA

F

ISL

GB

R

RU

S

DE

U

AU

T

BR

A

SV

K

TU

R

CZE

ES

P

ISR

SV

N

PO

L

IRL

ES

T

PR

T

HU

N

NZL

NLD

ITA

FIN

SW

E

CH

E

LU

X

DN

K

BE

L

FR

A

Construction Wholesale, retail & hotels Transport & telecoms Finance & insurance Business services Other services 1995, Total

Services value added embodied in manufacturing exports, by country

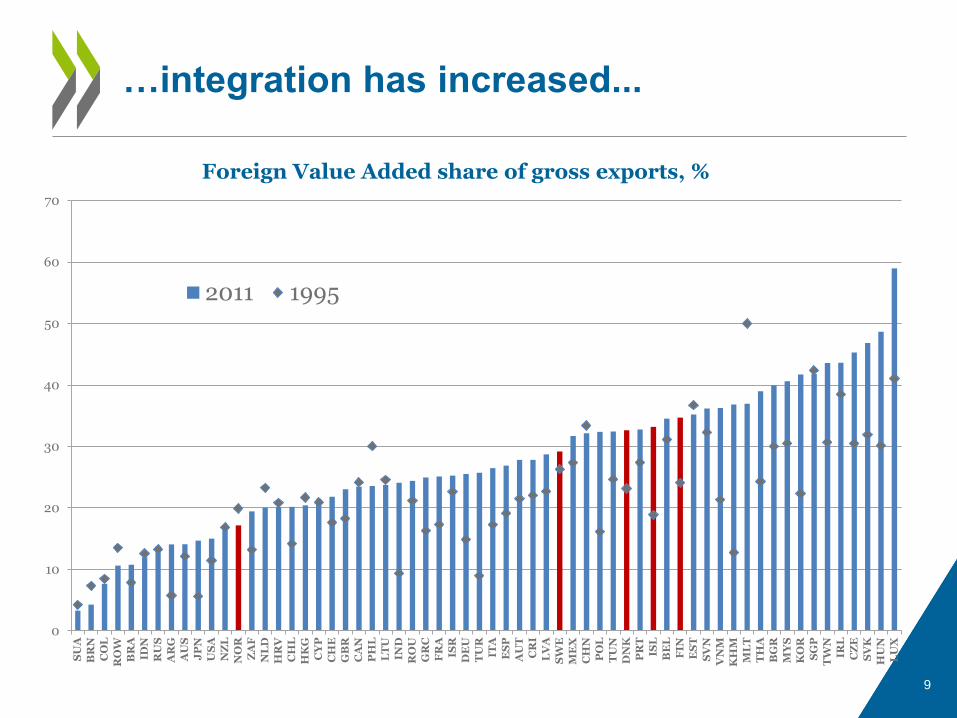

…integration has increased...

9

Foreign Value Added share of gross exports, %

0

10

20

30

40

50

60

70

SU

A

BR

N

CO

L

RO

W

BR

A

IDN

RU

S

AR

G

AU

S

JP

N

US

A

NZ

L

NO

R

ZA

F

NL

D

HR

V

CH

L

HK

G

CY

P

CH

E

GB

R

CA

N

PH

L

LT

U

IND

RO

U

GR

C

FR

A

ISR

DE

U

TU

R

ITA

ES

P

AU

T

CR

I

LV

A

SW

E

ME

X

CH

N

PO

L

TU

N

DN

K

PR

T

ISL

BE

L

FIN

ES

T

SV

N

VN

M

KH

M

ML

T

TH

A

BG

R

MY

S

KO

R

SG

P

TW

N

IRL

CZ

E

SV

K

HU

N

LU

X

2011 1995

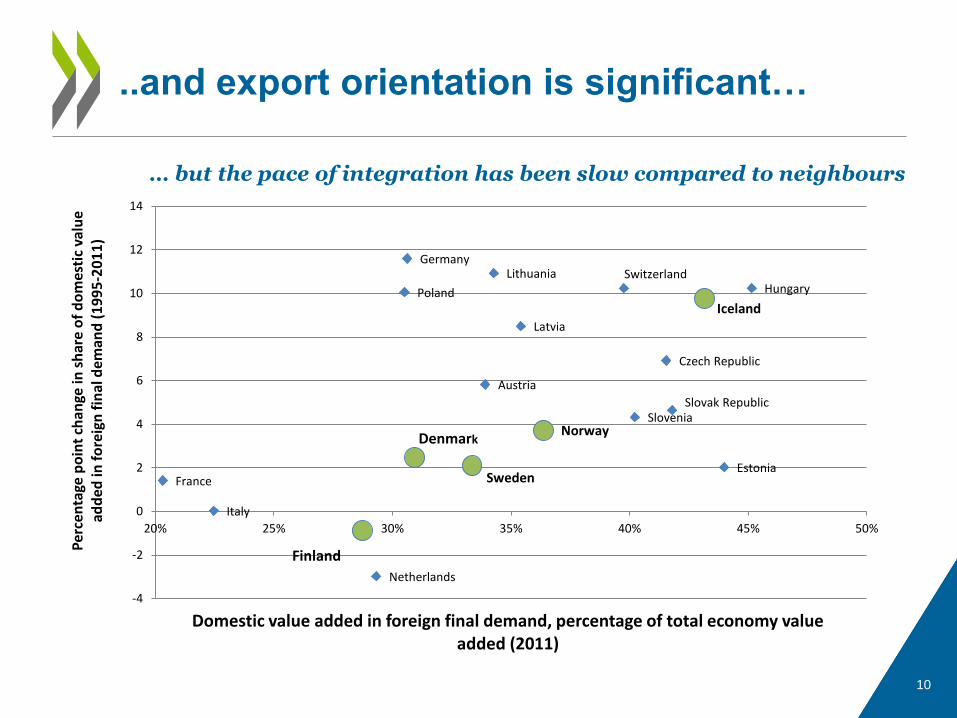

..and export orientation is significant…

10

Austria

Czech Republic

Denmark

Estonia

Finland

France

Germany

Hungary

Iceland

Italy

Latvia

Netherlands

Norway

Poland

Slovak Republic Slovenia

Sweden

Switzerland Lithuania

-4

-2

0

2

4

6

8

10

12

14

20% 25% 30% 35% 40% 45% 50%

Per

cen

tage

po

int

chan

ge in

sh

are

of

do

mes

tic

valu

e ad

ded

in f

ore

ign

fin

al d

eman

d (

19

95

-20

11

)

Domestic value added in foreign final demand, percentage of total economy value added (2011)

… but the pace of integration has been slow compared to neighbours

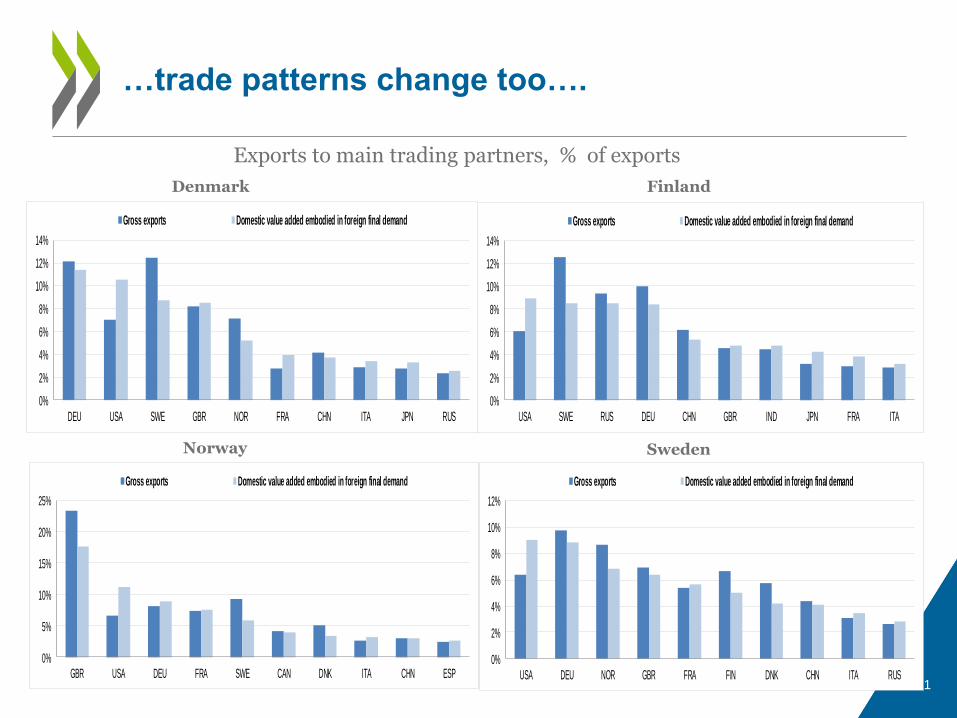

…trade patterns change too….

11

Exports to main trading partners, % of exports

Sweden Norway

Finland Denmark

0%

2%

4%

6%

8%

10%

12%

14%

DEU USA SWE GBR NOR FRA CHN ITA JPN RUS

Gross exports Domestic value added embodied in foreign final demand

0%

2%

4%

6%

8%

10%

12%

14%

USA SWE RUS DEU CHN GBR IND JPN FRA ITA

Gross exports Domestic value added embodied in foreign final demand

0%

5%

10%

15%

20%

25%

GBR USA DEU FRA SWE CAN DNK ITA CHN ESP

Gross exports Domestic value added embodied in foreign final demand

0%

2%

4%

6%

8%

10%

12%

USA DEU NOR GBR FRA FIN DNK CHN ITA RUS

Gross exports Domestic value added embodied in foreign final demand

…adding important insights…

12

-50

0

50

100

150

200

250

300

Gross

Value added

US trade deficit with selected partners, 2011, USD bn

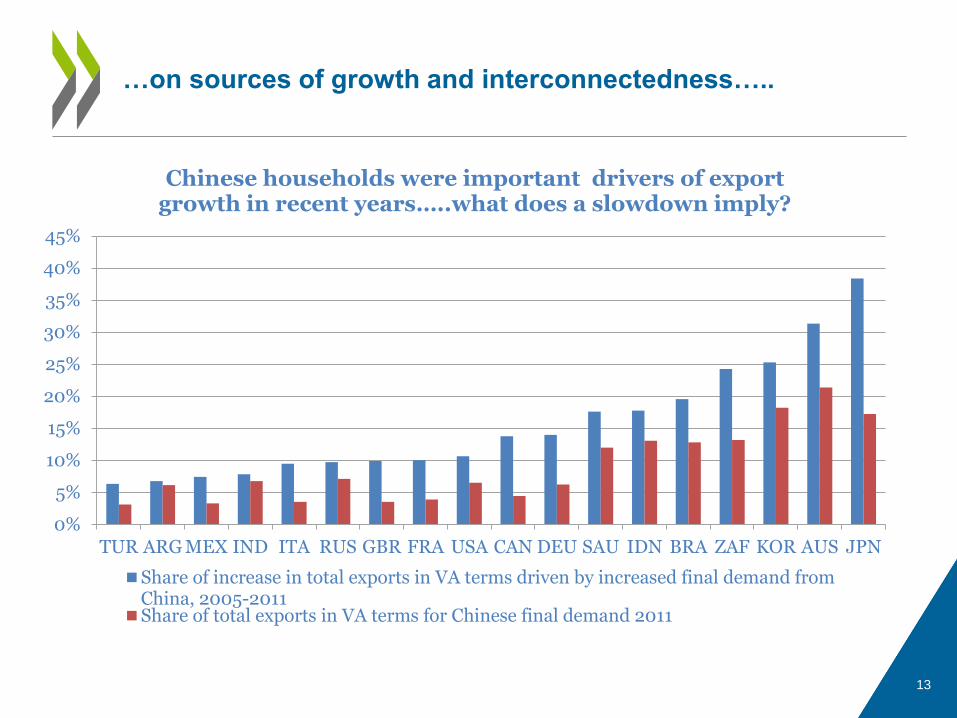

…on sources of growth and interconnectedness…..

13

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

TUR ARG MEX IND ITA RUS GBR FRA USA CAN DEU SAU IDN BRA ZAF KOR AUS JPN

Chinese households were important drivers of export growth in recent years…..what does a slowdown imply?

Share of increase in total exports in VA terms driven by increased final demand fromChina, 2005-2011Share of total exports in VA terms for Chinese final demand 2011

…the feedback loop…

14

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Mexico

ROW

US

Mexico’s exports by origin of value-added, 2011

Investment

Trade

Production

But this only scratches at the surface

15

Jobs

Actors - SMEs

Inequalities

• that we put ‘global’ at the heart of ‘national’

– But with a granularity that provides insights on the actors and their heterogeneity

– Improving our understanding of interconnectedness and benefits, challenges and consequences of globalisation

• Whilst also improving GDP

– In other words new internationally integrated economic accounting systems

Global production requires

16

• To create expanded TIVA highlighting the role of SMEs and MNEs and Traders in global production

Trailblazing collaboration with Nordic

council…

17

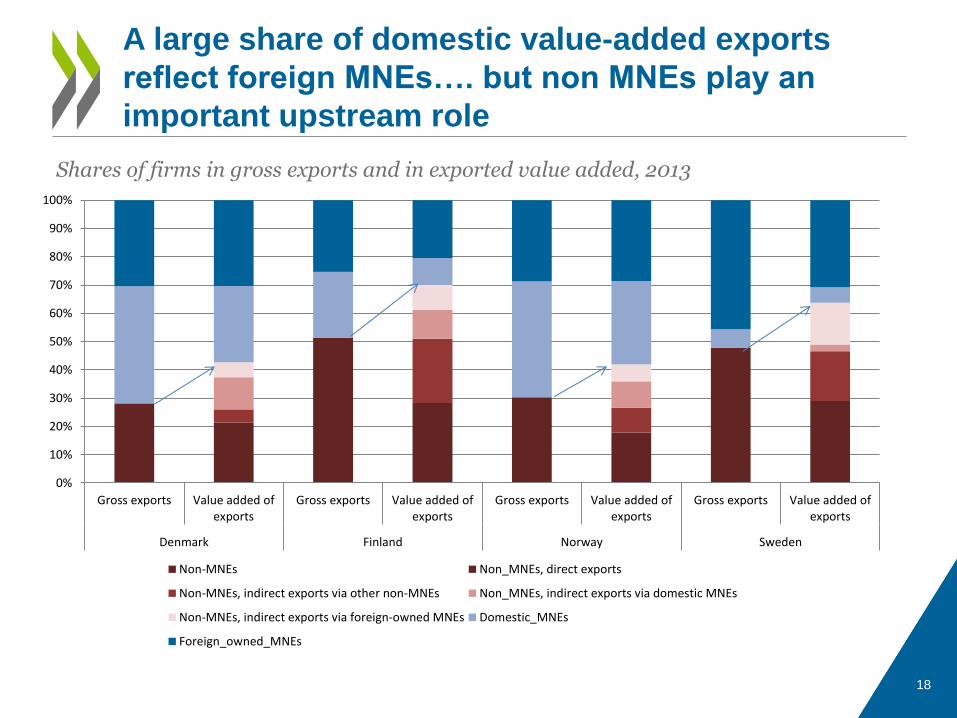

A large share of domestic value-added exports

reflect foreign MNEs…. but non MNEs play an

important upstream role

18

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Gross exports Value added ofexports

Gross exports Value added ofexports

Gross exports Value added ofexports

Gross exports Value added ofexports

Denmark Finland Norway Sweden

Non-MNEs Non_MNEs, direct exports

Non-MNEs, indirect exports via other non-MNEs Non_MNEs, indirect exports via domestic MNEs

Non-MNEs, indirect exports via foreign-owned MNEs Domestic_MNEs

Foreign_owned_MNEs

Shares of firms in gross exports and in exported value added, 2013

…meaning that SMEs are highly

integrated (directly and indirectly)

19

Shares of firms in gross exports and in exported value added, 2013

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Gross exports Value addedexports

Gross exports Value addedexports

Gross exports Value addedexports

Gross exports Value addedexports

Denmark Finland Norway Sweden

Independent - Micro

Independent - Small

Independent - Medium

Dependent - Micro

Dependent - Small

Dependent - Medium

Large

… particularly dependent SMEs…

20

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

1.8

2

No

n-M

NEs

Do

mes

tic

MN

Es

Fore

ign

-ow

ned

MN

Es

No

n-M

NEs

Do

mes

tic

MN

Es

Fore

ign

-ow

ned

MN

Es

No

n-M

NEs

Do

mes

tic

MN

Es

Fore

ign

-ow

ned

MN

Es

No

n-M

NEs

Do

mes

tic

MN

Es

Fore

ign

-ow

ned

MN

Es

Denmark Finland Norway Sweden

Value added generated at domestic suppliers for each Euro of value added at exporter, by firm type , 2013

But spillovers are higher from domestic MNEs..

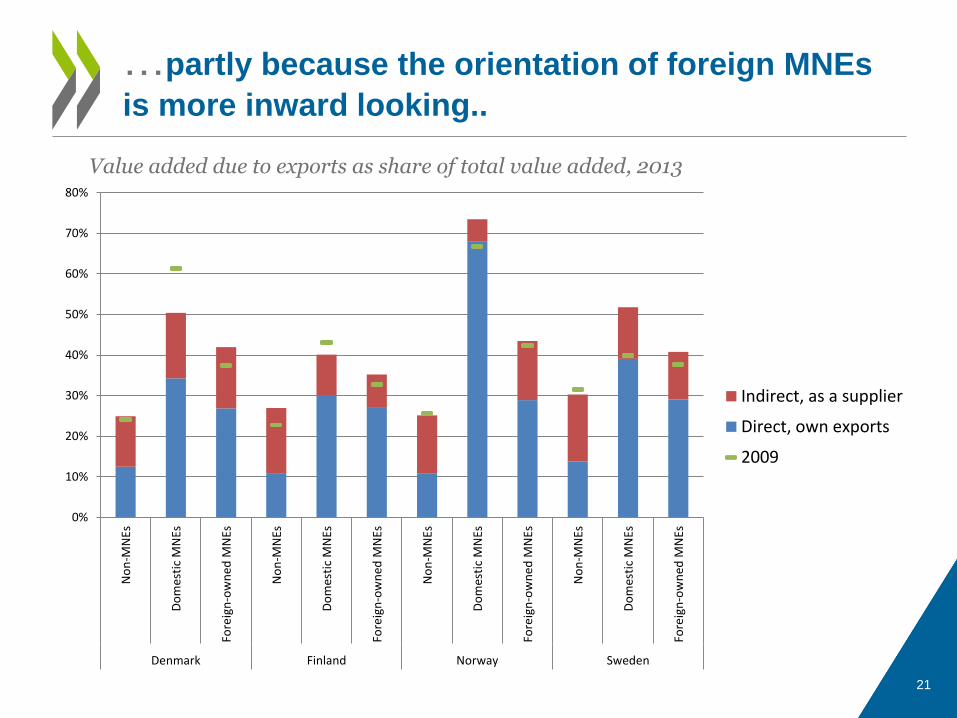

…partly because the orientation of foreign MNEs

is more inward looking..

21

0%

10%

20%

30%

40%

50%

60%

70%

80%

No

n-M

NEs

Do

mes

tic

MN

Es

Fore

ign

-ow

ned

MN

Es

No

n-M

NEs

Do

mes

tic

MN

Es

Fore

ign

-ow

ned

MN

Es

No

n-M

NEs

Do

mes

tic

MN

Es

Fore

ign

-ow

ned

MN

Es

No

n-M

NEs

Do

mes

tic

MN

Es

Fore

ign

-ow

ned

MN

Es

Denmark Finland Norway Sweden

Indirect, as a supplier

Direct, own exports

2009

Value added due to exports as share of total value added, 2013

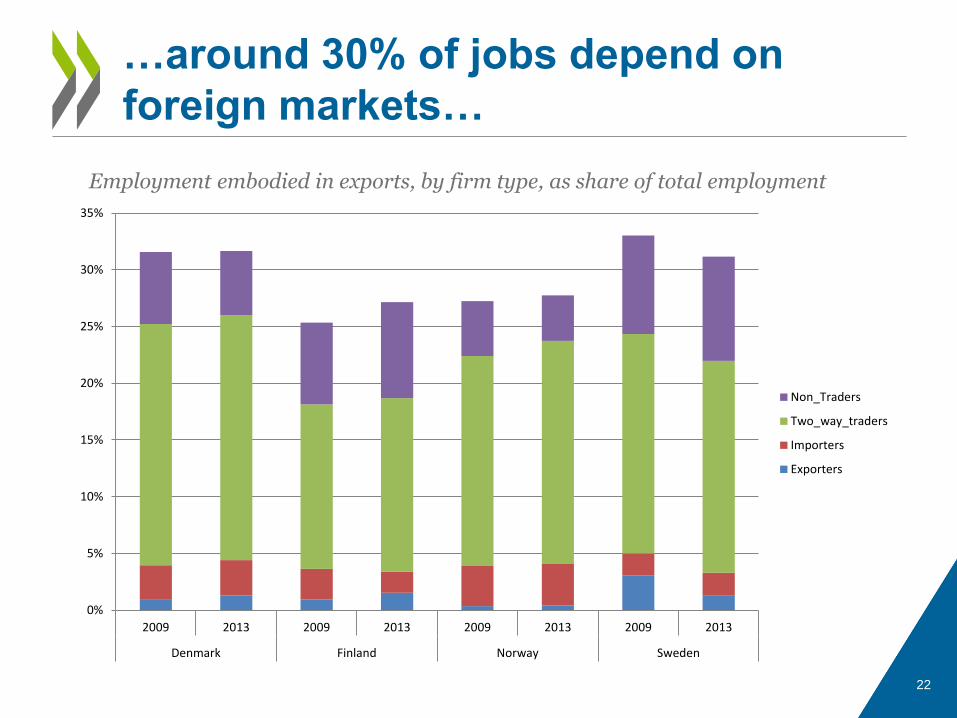

…around 30% of jobs depend on

foreign markets…

22

0%

5%

10%

15%

20%

25%

30%

35%

2009 2013 2009 2013 2009 2013 2009 2013

Denmark Finland Norway Sweden

Non_Traders

Two_way_traders

Importers

Exporters

Employment embodied in exports, by firm type, as share of total employment

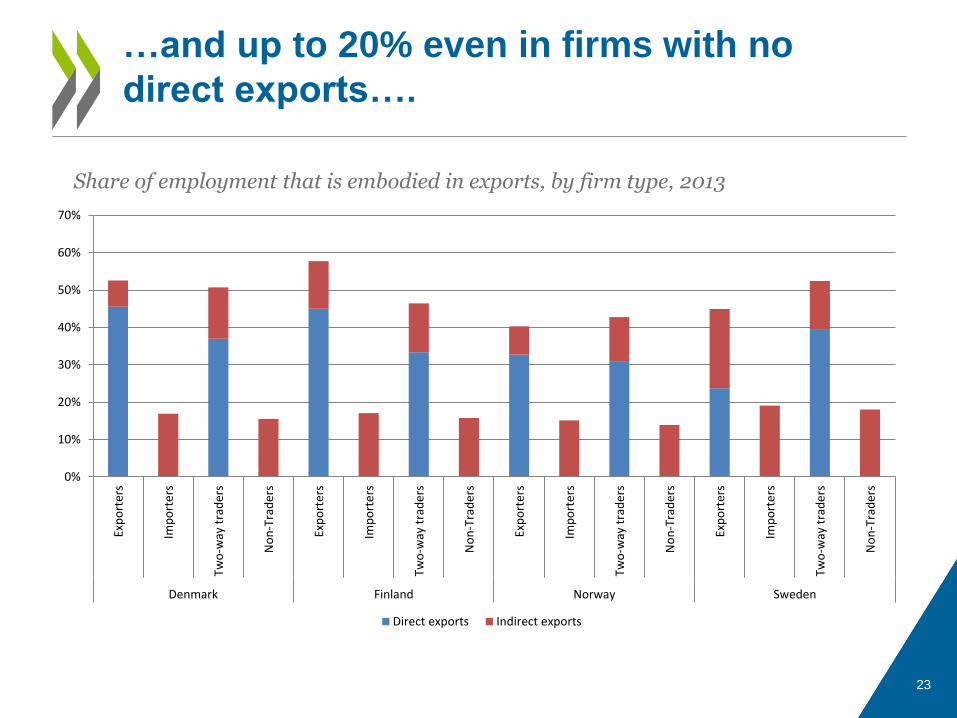

…and up to 20% even in firms with no

direct exports….

23

0%

10%

20%

30%

40%

50%

60%

70%

Exp

ort

ers

Imp

ort

ers

Two

-way

tra

de

rs

No

n-T

rad

ers

Exp

ort

ers

Imp

ort

ers

Two

-way

tra

de

rs

No

n-T

rad

ers

Exp

ort

ers

Imp

ort

ers

Two

-way

tra

de

rs

No

n-T

rad

ers

Exp

ort

ers

Imp

ort

ers

Two

-way

tra

de

rs

No

n-T

rad

ers

Denmark Finland Norway Sweden

Direct exports Indirect exports

Share of employment that is embodied in exports, by firm type, 2013

• Forthcoming report to accompany today’s report

• Build on momentum from the collaboration with the Nordics but also advance with other countries

• To help build the 21st century statistical information systems needed for 21st century production

Next steps

24