GLOBAL TRENDS IN SEAFOOD DEMAND, SUPPLY, TRADE AND …

54

GLOBAL TRENDS IN SEAFOOD DEMAND, SUPPLY, TRADE AND PRICES by Stefania Vannuccini Fishery Statistician (Commodities) FAO Fisheries and Aquaculture Statistics and Information Service Woods Hole, 24-25 May 2011

Transcript of GLOBAL TRENDS IN SEAFOOD DEMAND, SUPPLY, TRADE AND …

GLOBAL TRENDS IN SEAFOOD DEMAND, SUPPLY, TRADE AND PRICES

by Stefania VannucciniFishery Statistician (Commodities)

FAO Fisheries and Aquaculture Statistics and Information Service

Woods Hole, 24-25 May 2011

Outline

• Overview• Production• Utilization• Consumption• Trade• Prices• Outlook

Overview: last two decade

• Increase in global aquaculture production

• Rising demand for fish and fishery products

• Growth in world trade of fish and fishery products

• Global call for responsible management

World fishery production

0

30

60

90

120

150

1950 1960 1970 1980 1990 2000 2009

Aquaculture

Capture

million tonnes

World fishery productionmillion tonnes

0

30

60

90

120

150

1950 1960 1970 1980 1990 2000 2009

Aquaculture(marine waters)

Aquaculture(inland waters)

Capture (inlandwaters)

Capture (marinewaters)

World fishery productionmillion tonnes

2009 2010 e 2011f 2011/2010

Production 144.6 145.1 149.0 2.7%

Capture 88.9 87.0 88.5 1.8%

Aquaculture 55.7 58.1 60.4 4.0%

e: estimation; f: forecast

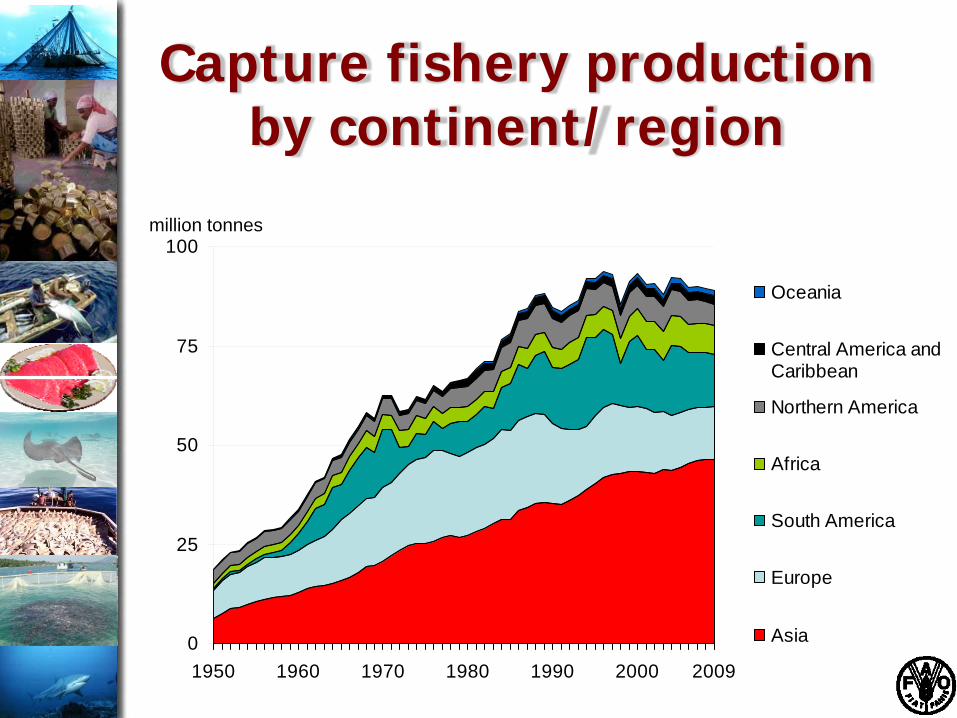

Capture fishery productionby continent/region

0

25

50

75

100

1950 1960 1970 1980 1990 2000 2009

Oceania

Central America andCaribbean

Northern America

Africa

South America

Europe

Asia

million tonnes

2009 Capture: top producers

China17%

Peru8%

USA5%

Russian Federation

Chile4%

Others47%

Japan4%

India5%

Indonesia6%

Capture fishery productionby ISSCAAP division

0

25

50

75

100

1950 1960 1970 1980 1990 2000 2009

Miscellaneousaquatic animals

Diadromous fishes

Crustaceans

Molluscs

Freshwater fishes

Marine fishes

million tonnes

2009 Capture by species groups

Tunas, bonitos, billfishes

7%

Salmons, trouts, smelts

1%Other diadromous

1%

Other pelagics35%

Other marine fishes32%

Shrimps, prawns4%

Miscellaneous aquatic animals

0.5%Other molluscs1%

Bivalves2%

Squids, cuttlefishes, octopuses

4%Other crustaceans3%

Freshwater fishes10%

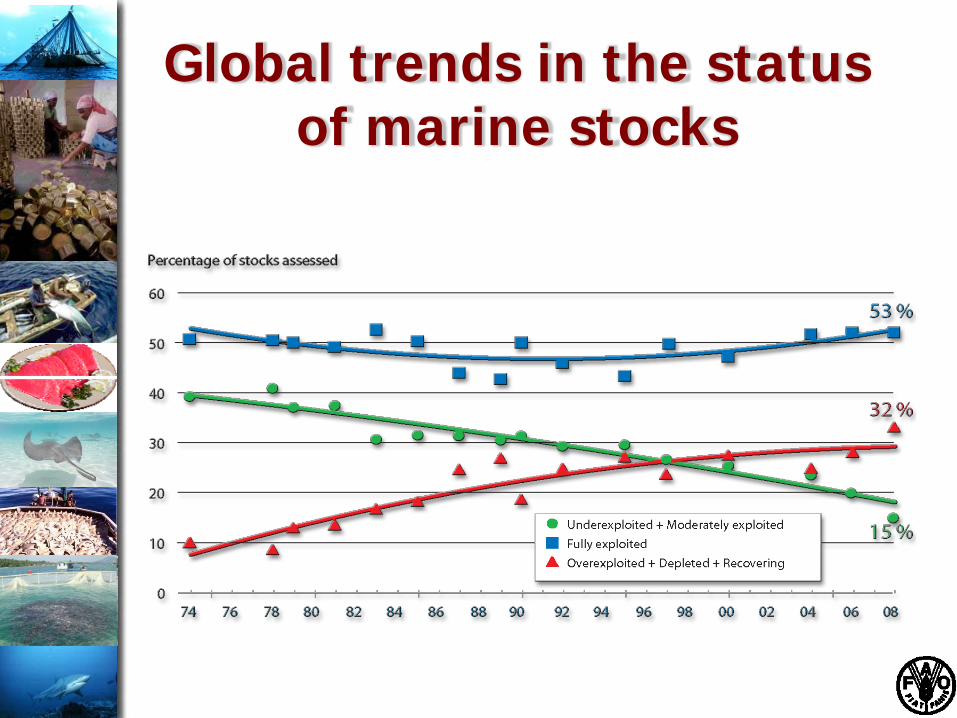

Global trends in the status of marine stocks

Aquaculture productionby continent/region

0

20

40

60

1950 1960 1970 1980 1990 2000 2009

Oceania

Central Americaand Caribbean

Northern America

Africa

South America

Europe

Asia

million tonnes

2009 Aquaculture: top producers

China62%

Viet Nam5% India

7%

Thailand3%

Indonesia3%

Bangladesh2%

Norway2%

Chile1%

Others15%

Aquaculture productionby ISSCAAP division

million tonnes

0

20

40

60

1950 1960 1970 1980 1990 2000 2009

Miscellaneousaquatic animals

Marine fishes

Diadromousfishes

Crustaceans

Molluscs

Freshwater fishes

2009 Aquaculture by species groups

Freshwater fishes56%

Bivalves22%

Other molluscs3%

Other crustaceans3%

Miscellaneous aquatic animals

1%

Tunas, bonitos, billfishes

0.0%

Other pelagics0.4%

Salmons, trouts, smelts

4%

Other marine fishes3%

Shrimps, prawns6%

Squids, cuttlefishes, octopuses

0.0%

Other diadromous2%

China

0

25

50

75

100

1950 1970 1990 2009

World excluding China China

0

20

40

60

1950 1970 1990 2009

Capture Aquaculture

Annual growth rate

-2

0

2

4

6

8

10

12

1960-1969 1970-1979 1980-1989 1990-1999 2000-2009

Capture

Aquaculture

%

Annual growth rate Aquaculture vs agriculture

0 2 4 6 8 10 12

1970-1979

1980-1989

1990-1999

2000-2009 Meat

Milk

Eggs

Cereals

Fruit

Vegetables

Aquaculture

%

Annual growth rate Aquaculture vs meat

0

2

4

6

8

10

12

1970-1979 1980-1989 1990-1999 2000-2009

Aquaculture

Poultry Meat

Meat, Total

Sheep and Goat Meat

Beef and Buffalo Meat

%

Utilization of fish productionand per capita fish supply

0

25

50

75

100

125

150

1950 1960 1970 1980 1990 2000 20100.0

3.0

6.0

9.0

12.0

15.0

18.0Fish for human consumption

Non-food uses

Per capita food fish supply

Fish production

(million tonnes)Per capita fish supply (kg)

Share of utilization of fish production

0%

20%

40%

60%

80%

100%

1950 1960 1970 1980 1990 2000 2010

Fish for humanconsumption

Non-food uses

Utilization of fish productionbreakdown by quantity

0 10 20 30 40 50 60

Marketing fresh

Freezing

Canning

Curing

Non-food uses

Million tonnes

Fish as food

• Important role in food security• Source of proteins, minerals,

micronutrients and essential fatty acids

• 118 million tonnes• 17.2 kg/capita• 47% from aquaculture

Per capita fish supply: contribution of capture and aquaculture

0%

25%

50%

75%

100%

1950 1960 1970 1980 1990 2000 2010

Capture

Aquaculture

Per capita fish supply

Per capita fish supply

9.1

16.3

10.3

24.3

28.7

25.5

9.6

24

22.1

18.8

8.4

17.2

0 5 10 15 20 25 30

LIFDCs

Other developing

Least Developed

Developed

Industrialized

Oceania

Latin America

North America

Europe

Asia

Africa

World

kg/capita

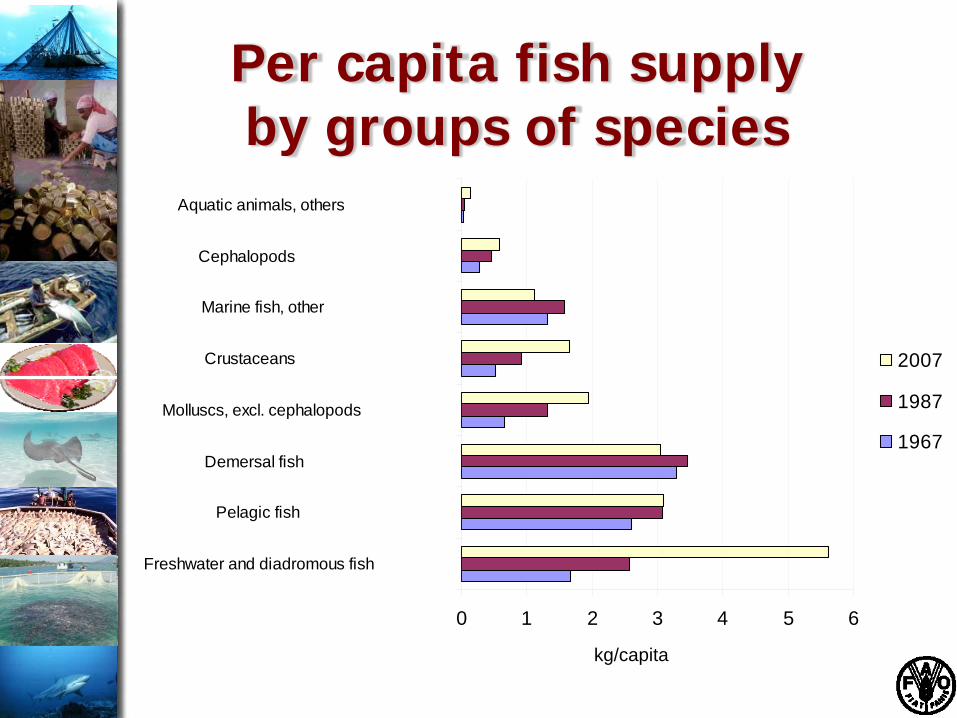

Per capita fish supplyby groups of species

0 1 2 3 4 5 6

Freshwater and diadromous fish

Pelagic fish

Demersal fish

Molluscs, excl. cephalopods

Crustaceans

Marine fish, other

Cephalopods

Aquatic animals, others

2007

1987

1967

kg/capita

Nutritional standards• Increase of the per capita food

consumption• Improvement of nutritional standards

since 1970• Change in global dietary patterns• Increase in the average global calorie

supply• Growth of the quantity of proteins, in

particular for emerging economies

Food consumption• Rising living standards• Population growth• Rapid urbanization• Increased trade• Transformation in food distribution,

transportation, marketing• Improvement in food science, technology• Value-added products• More developed economies less reactive to

income growth compared to low-income countries

Fish consumption in industrialized countries

• Diversification in the diets• Health and diet conscious• Value addition• Ready-to-cook, ready-to-eat• More fish in fresh form

Protein supply

g/capita

0

20

40

60

80

100

120

World Africa NorthAmerica

LatinAmericaand the

Caribbean

Asia Europe Oceania

Total proteins Vegetable proteins Animal proteinsMeat and offals Milk / dairy products FishEggs

Fish contribution to animal protein supply (2005-2007)

Share of production traded

0

30

60

90

120

150

1976 1981 1986 1991 1996 2001 2006 2009

Production

Exports

million tonnes

Trade by groups of species(value)

Shrimps, prawns15%

Salmons, trouts, smelts12%

Cods, hakes, haddocks

10%

Tuna9%Other pelagics

7%

Other finfish27%

Oils2%

Meals3%

Squids, cuttlefishes, octopuses

4%

Other molluscs aquatic invert

5%

Other crustaceans

6%

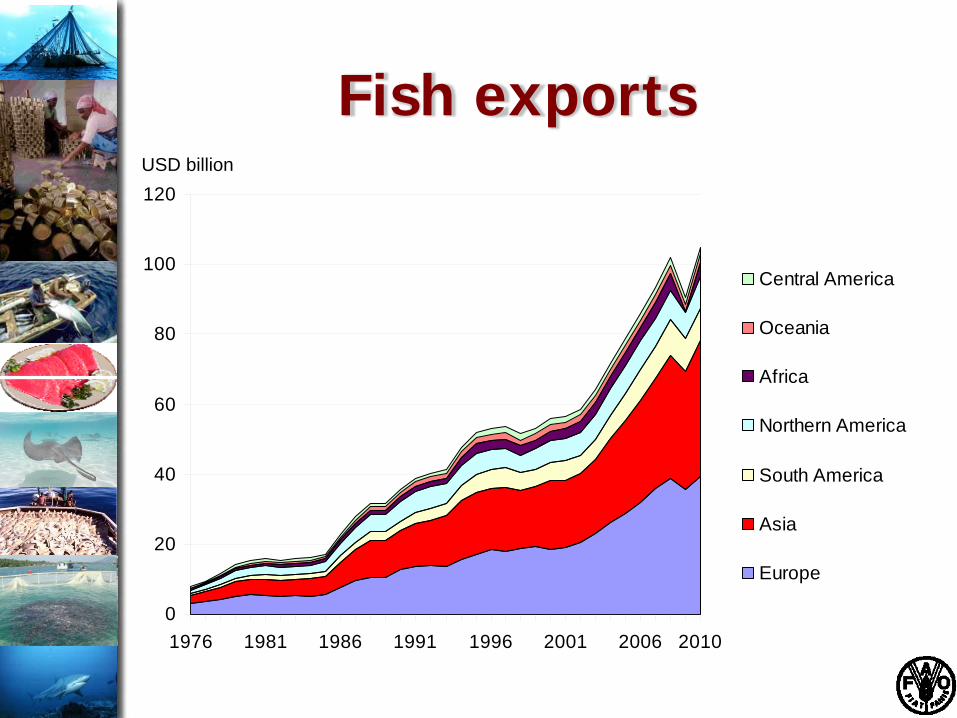

Fish exports

0

20

40

60

80

100

120

1976 1981 1986 1991 1996 2001 2006 2010

Central America

Oceania

Africa

Northern America

South America

Asia

Europe

USD billion

2009: Top exporters (value)

China 12% Norway

8%

Thailand 7%

USA 5%

Viet Nam 4%

Canada 4%

Chile 3%

Indonesia 3%

Peru 2%

Other52%

Net exports developing countries

-5

0

5

10

15

20

25

Fish Coffee Rubber Bananas Cocoa Meat Tea Sugar Tobacco Rice

1987 1997 2007

USD billion

Fish imports

0

20

40

60

80

100

120

1976 1981 1986 1991 1996 2001 2006 2010

CentralAmerica

Oceania

SouthAmerica

Africa

NorthernAmerica

Asia

Europe

USD billion

2009: Top importers (value)

UK 3.3%

China 5.7%

France5.4%

Russian Fed 2.1%

USA 14.1%

Japan 13.6%

Korea Rep 2.9%China,H.Kong

2.4%

Canada 2.1%

Other48.4%

Trends in trade• 7% decline in 2009, followed by

growth of 11% in 2010• 2010 imports estimated ad USD 110

billion and exports at USD 105 billion• Positive 2011• Wide range of product types and

participants• Increased fishery trade within regions• Growing imports among/from

developing countries

Africa

Imports in USD million

Asia

Imports in USD million

Oceania

Imports in USD million

Europe

Imports in USD million

South America

Imports in USD million

North and Central America

Imports in USD million

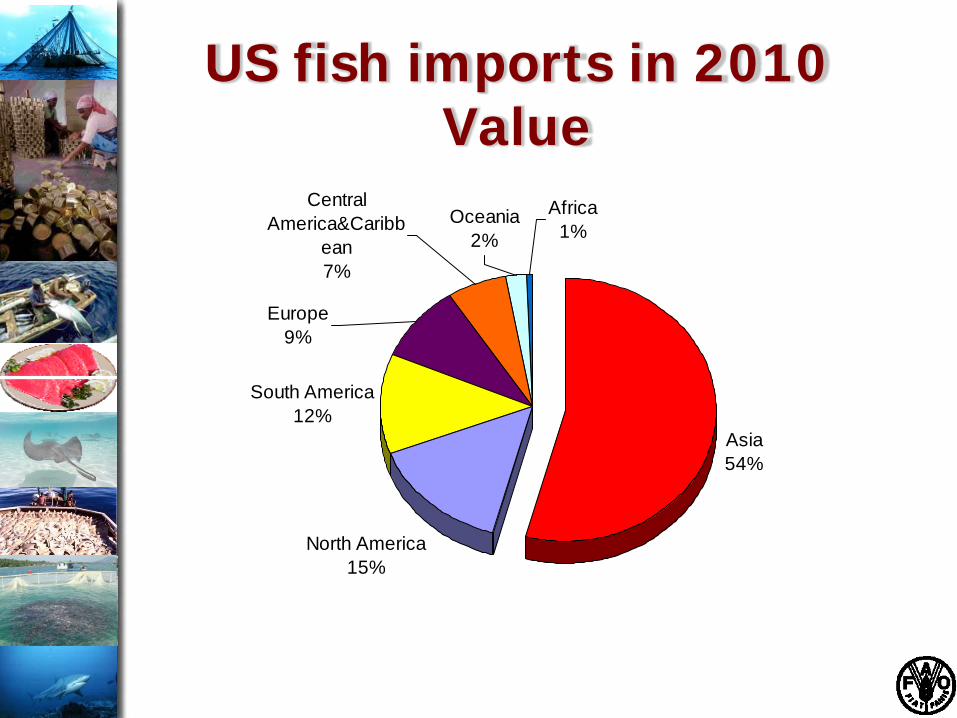

US fish imports in 2010Value

Asia54%

North America15%

South America12%

Oceania2%

Europe9%

Central America&Caribb

ean7%

Africa1%

US fish imports in 2010 Value

China14%

Thailand13%

Others34%

Canada13%

Viet Nam5%

Indonesia6%

Chile4%

Ecuador4%

Norway3%

Mexico2%

India2%

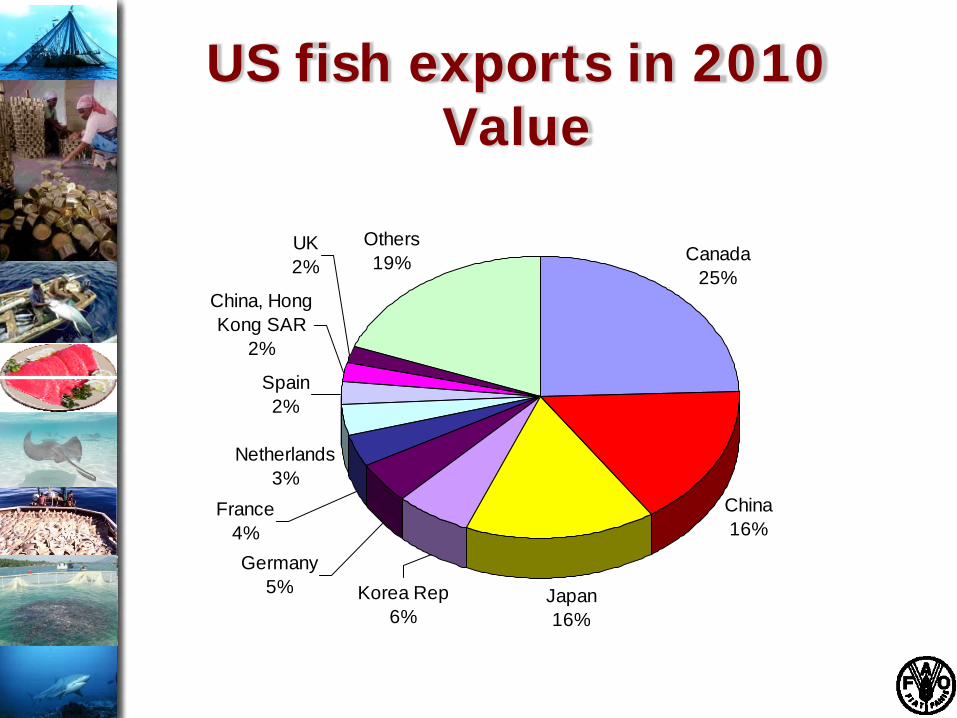

US fish exports in 2010 Value

Asia45%

Europe26%

Oceania1%

South America1%

North America24%

Africa0.4%

Central America&Carib

bean3%

US fish exports in 2010 Value

Canada25%

China16%

Japan16%

Netherlands3%

Spain2%

China, Hong Kong SAR

2%

UK2%

Others19%

Korea Rep6%

Germany5%

France4%

Fish Price Index (2005=100)

Outlook supply• Major increases will depend on aquaculture. • Factors to influence future growth of

aquaculture: – costs/availability of feed for selected species;

access and availability of areas/water– environmental impacts– availability of technology and finance– effects on biodiversity– climate changes– governance– food safety and traceability issues

• Capture: importance of implement more cautious and effective fisheries management

Outlook demand• Retail concentration in developed and

developing which will affect demand• Product development, technological

innovation• Continuous increase of trade• Increased imports from developing

countries• Outsourcing of processing will continue• Slow growth in per capita consumption