Global Trade Outlook - Lenzing...

42

Global Trade Outlook U.S. Trade Representative Gail W. Strickler

Transcript of Global Trade Outlook - Lenzing...

Global Trade Outlook

U.S. Trade Representative

Gail W. Strickler

Agenda

• Preference programs

• FTAs

• Pending negotiations 2

„ Top importing locales (apparel & non-apparel)

‟ China, Vietnam and CAFTA

Trade Overview

„ 42% of tariffs collected come from textiles and apparel

„ U.S. is largest consumer of apparel in world and continues to grow

3

U.S. Trade Outlook

Trade Preference Programs

Legislated by Congress, trade preference programs provide duty-preference to certain textile and apparel products from designated beneficiary countries that meet the program’s rules.

African Growth and Opportunity Act (AGOA)

2000-2015 Andean Trade Promotion and

Drug Eradication Act (ATPDEA)

Expired in July 2013

Caribbean Basin Trade Partnership Act

(CBTPA) 1983-2020

Jordan/Egypt Qualifying Industrial Zones (QIZs) 1997/2005-no expiration date

Haitian Hemispheric Opportunity through Partnership

Encouragement Act / Haiti Economic Lift Program (Haiti

HOPE/HELP)

2006-2020

Preference Programs

6

Qualifying Countries • Benin • Botswana • Burkina Faso • Cameroon • Cape Verde • Chad • Ethiopia • The Gambia • Ghana • Kenya • Lesotho • Liberia • Malawi • Mali • Mauritius

• Mozambique • Namibia • Niger • Nigeria • Rwanda • Senegal • Sierra Leone • South Africa* • South Sudan • Swaziland • Tanzania • Uganda • Zambia

*South Africa does not qualify as an LDC and is ineligible for 3rd party fabric provision

African Growth & Opportunity Act (AGOA)

Of the 46 members in AGOA, 25 members are eligible under the apparel provision

The apparel provision allows qualifying apparel products to enter the U.S.

duty-free and quota-free

7

„ AGOA due for renewal in 2015

‟ USTR Froman has called for a review of the program to assess how we can improve and expand its reach

„ Apparel and textiles has been a key success

‟ 22% of total non-energy related exports come from textiles and apparel

AGOA Review

8

0

200

400

600

800

1000

1200

2007 2008 2009 2010 2011 2012

Value of imports (

in m

illions US

D)

AGOA apparel imports (under apparel provision)

• Based on year-to-end calculations, the value of 2013 imports already exceeds every year except 2007

9

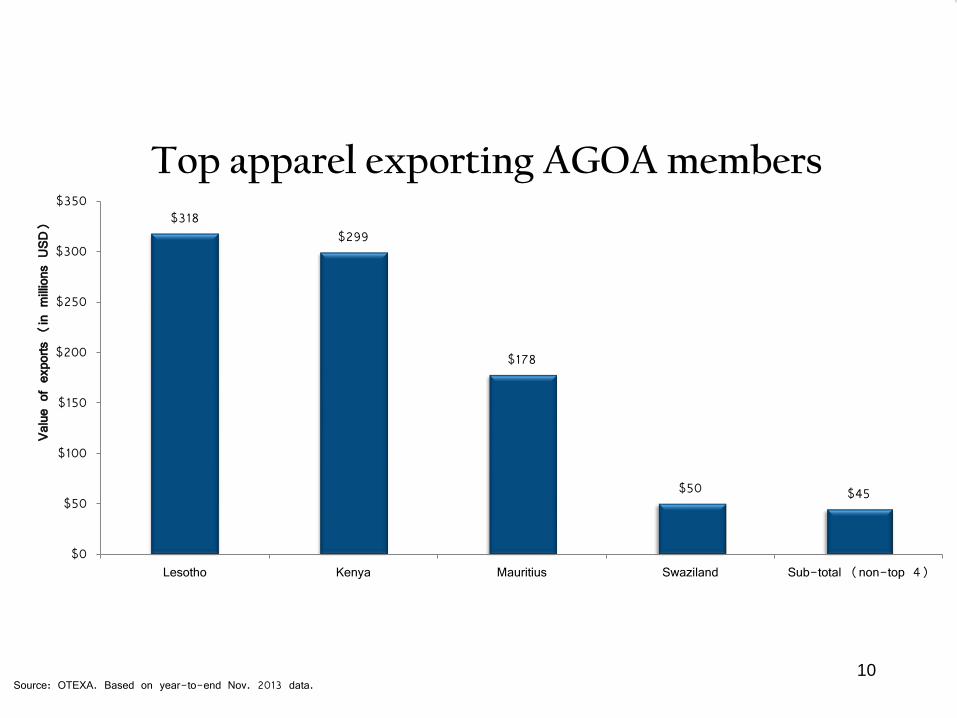

Source: OTEXA. Based on year-to-end Nov. 2013 data.

$318 $299

$178

$50 $45

$0

$50

$100

$150

$200

$250

$300

$350

Lesotho Kenya Mauritius Swaziland Sub-total (non-top 4)

Value of exports (

in m

illions US

D)

Top apparel exporting AGOA members

10

Egypt Qualifying Industrial Zones (QIZs)

„ Encompasses 15 designated industrial zones with more in discussion

„ The rules of origin: 35% of the product’s value is manufactured in Egypt, of which 10.5 percent must be of Israeli origin

• The rule of origin is the same for all products, including textiles and apparel.

• Jordan QIZ’s were superseded by the FTA

11

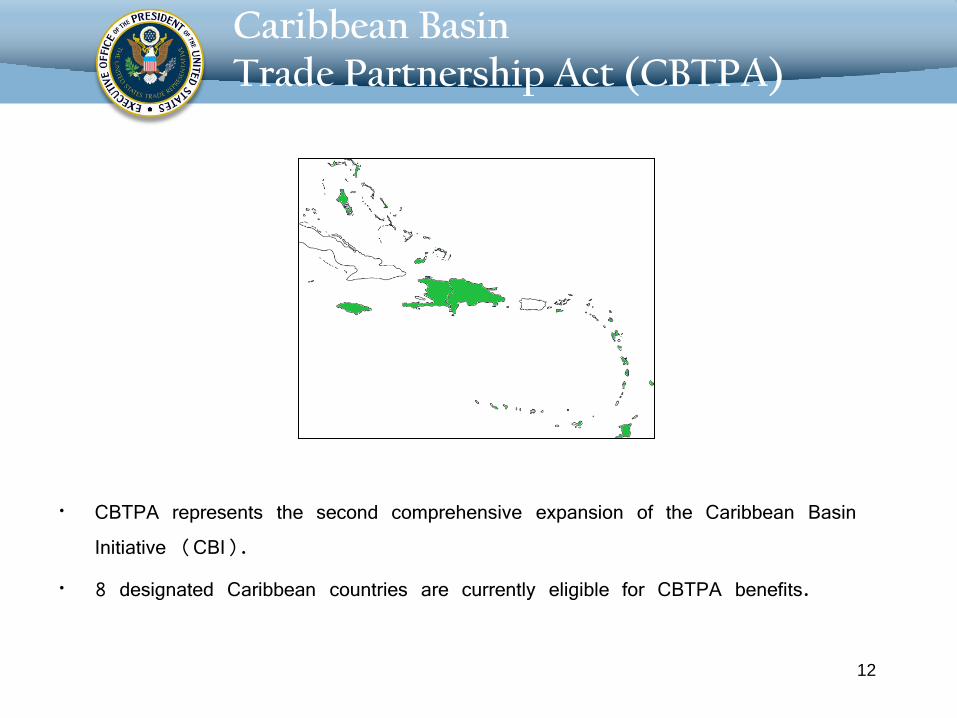

„ CBTPA represents the second comprehensive expansion of the Caribbean Basin Initiative (CBI).

„ 8 designated Caribbean countries are currently eligible for CBTPA benefits.

Caribbean Basin Trade Partnership Act (CBTPA)

12

„ The Haitian Hemispheric Opportunity through Partnership Encouragement Act of 2008 (HOPE II) allows duty-free access to the U.S. market for certain Haitian-made apparel and other articles

„ Goal: Foster stability and economic development

„ Expands the benefits from the original 2006 HOPE Act

„ Haiti is required to establish an independent labor ombudsman with monitoring, evaluation and technical support from the International Labor Organization under the TAICNAR program (Technical

Assistance Improvement and Compliance Needs Assessment and Remediation Program)

Haiti – HOPE II

13

Duty-free treatment for the following: ‟ up to 200 million square meter equivalents (SME) of knit apparel (with

some t-shirt and sweatshirt exclusions, which utilize CBTPA) and 200 million SMEs of woven apparel without regard to the country of origin of the fabric or components, as long as the apparel is wholly assembled or knit-to-shape in Haiti. Certain textile made-ups are also eligible.

‟ knit or woven apparel under a “two for one” earned import allowance

program

„ Haitian goods to enter the United States duty-free if shipped either directly from Haiti or through the Dominican Republic.

Haiti – HOPE II & HELP

14

Preference Program

Qualifying Products Additional Information EIF

Egypt QIZs 35% QIZ added value, of which 10.5% must

come from Israel Added Value may originate in QIZ country,

Israel, or the U.S. Egypt 2004

AGOA

Apparel made in designated LDCs can be

made of 3rd-party yarns or fabrics* Apparel made of U.S. or sub-Saharan

African yarns and fabrics Apparel made of yarns and fabrics in Short

Supply

Specific Cap for 3rd party yarn ‟ 3.5% of preceding year’s total apparel imports*

2000

Preference Programs

15

Preference Program

Qualifying Products Additional Information EIF

CBTPA

• Apparel sewn from fabric made and cut in the U.S. of U.S. yarn

• Apparel of U.S. fabric made of U.S. thread cut and sewn using U.S. thread

• Knit Apparel • T-Shirts • Brassieres • Certain other apparel*

Knit Apparel subject to TRQ of 970 million SMEs

T-Shirts subject to TRQ of 12 million dozens Qualifying Countries: Barbados, Belize, Guyana,

Haiti, Jamaica, Panama, St. Lucia, Trinidad and Tobago

(99% of CBTPA comes from Haiti)

2000

HOPE II /HELP

• Apparel wholly assembled in Haiti which satisfies value requirement (50% through 2014)

• All woven apparel wholly assembled in Haiti

• Certain other apparel and luggage*

Most categories of apparel imports are subject to a quantitative limit, excepting Brassieres, luggage,

and some other apparel categories

HOPE II 2008;

HELP 2010

Preference Programs

16 *Additional qualifying apparel under CBTPA can be found at http://otexa.ita.doc.gov/AGOA-CBTPA/Title_II.doc

A summary of CBTPA qualifying goods is available at http://otexa.ita.doc.gov/AGOA-CBTPA/summary_sheet.pdf

Free Trade Agreements

17

‟ Panama (EIF October 2012)

‟ Colombia (May 2012)

‟ Korea (March 2012)

‟ Peru (February 2009)

‟ Oman (January 2009)

‟ Bahrain (August 2006)

‟ CAFTA-DR

El Salvador (March 2006)

Honduras/Nicaragua (April 2006)

Guatemala (July 2006)

Dominican Republic (March 2007)

Costa Rica (January 2009)

‟ Morocco (January 2006)

‟ Australia (January 2005)

‟ Singapore (January 2004)

‟ Chile (January 2004)

‟ Jordan (December 2001)

‟ NAFTA (January 1994)

‟ Israel (September 1985)

18

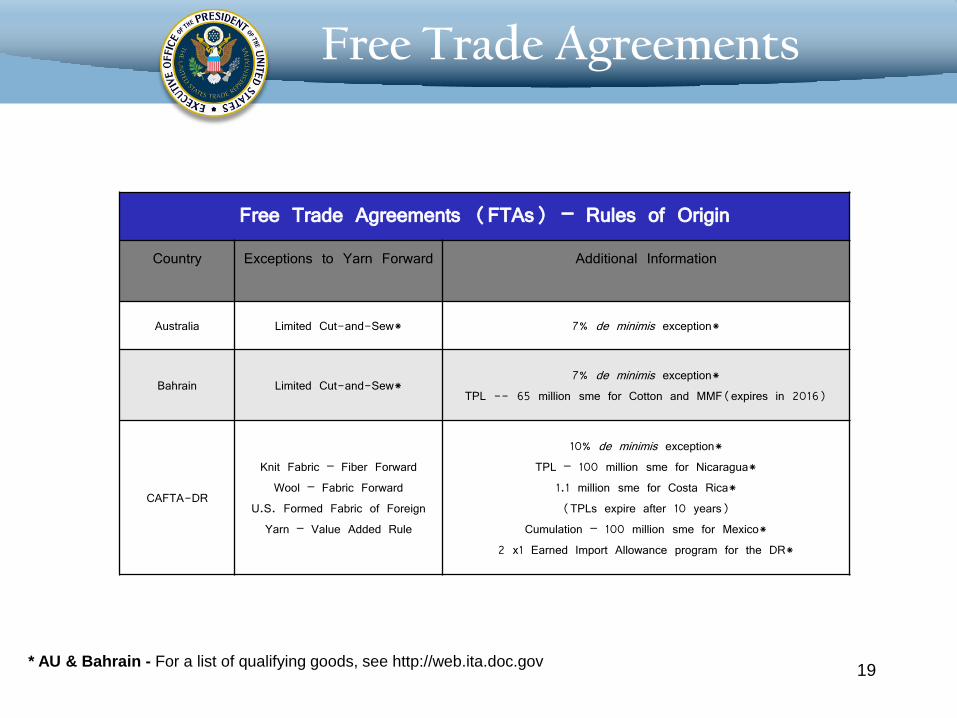

Free Trade Agreements (FTAs) ‟ Rules of Origin

Country Exceptions to Yarn Forward Additional Information

Australia Limited Cut-and-Sew* 7% de minimis exception*

Bahrain Limited Cut-and-Sew* 7% de minimis exception*

TPL -- 65 million sme for Cotton and MMF(expires in 2016)

CAFTA-DR

Knit Fabric ‟ Fiber Forward Wool ‟ Fabric Forward

U.S. Formed Fabric of Foreign Yarn ‟ Value Added Rule

10% de minimis exception* TPL ‟ 100 million sme for Nicaragua*

1.1 million sme for Costa Rica* (TPLs expire after 10 years)

Cumulation ‟ 100 million sme for Mexico* 2 x1 Earned Import Allowance program for the DR*

Free Trade Agreements

19 * AU & Bahrain - For a list of qualifying goods, see http://web.ita.doc.gov

Free Trade Agreements (FTAs) ‟ Rules of Origin

Country Exceptions to Yarn Forward Additional Information

Chile Yarn Forward 7% de minimis exception*

TPL ‟ 3 million sme (reduced to 2 million sme in 11th year of agreement)*

Israel 35% value-added rule Under the value added rule, fibers, yarns and/or fabrics can come from anywhere as long as 35% of the value of the product is added

in Israel.

Jordan 35% value-added rule Same as Israel

Morocco Yarn Forward

7% de minimis exception* TPL ‟ 30 million (expires in 2016, with reductions in the TPL

beginning in year five) Limited Cotton Cumulation*

Oman Yarn Forward 7% de minimis exception*

TPL ‟ 50 million sme for Cotton and MMF apparel (expires in 2019)

Free Trade Agreements

20

Free Trade Agreements (FTAs) ‟ Rules of Origin

Country Exceptions to Yarn Forward Additional Information

NAFTA

MMF Sweaters ‟ Fiber Forward Certain Men’s Dress Shirts ‟ Cut & Sew

Women’s Fine Cotton Underwear & Nightwear ‟ Cut & Sew

Brassieres ‟ Cut & Sew

7% de minimis exception* Extensive TPL regime that varies by product and is different for

Mexico and Canada*

Peru

Brassieres ‟ Cut & Sew Knit Fabric ‟ Fiber Forward

Nylon Filament Yarn ‟ Can be sourced from Mexico, Canada, or Israel

Viscose Rayon Filament Yarn ‟ Can be sourced from anywhere

10% de minimis exception* Narrow Elastic Fabric, Visible Lining Fabrics, Sewing Thread and

Pocketing Fabrics must be sourced within the region

Singapore Brassieres ‟ Cut & Sew

Linen/Silk Apparel ‟ Cut & Sew 7% de minimis exception*

TPL ‟ 25 million sme, expired in 2012

Colombia

Brassieres ‟ Cut & Sew Knit Fabric ‟ Fiber Forward

Nylon Filament Yarn ‟ Can be sourced from Mexico, Canada, or Israel

Viscose Rayon Filament Yarn ‟ Can be sourced from anywhere

10% de minimis exception* Narrow Elastic Fabric, Visible Lining Fabrics, Sewing Thread and

Pocketing Fabrics must be sourced within the region

Free Trade Agreements

21 *NAFTA TPLs - For a breakout of TPLs, see

http://web.ita.doc.gov/tacgi/fta.nsf/FTA/NAFTA?opendocument&country=NAFTA

Free Trade Agreements (FTAs) ‟ Rules of Origin

Country Exceptions to Yarn Forward Additional Information Textile Safeguard

Korea Yarn Forward

7% de minimis exception* Rule of origin excludes certain components ‟ sewing thread,

narrow fabrics and pocketing fabrics -- that are required under CAFTA-DR and important to U.S. producers.

No

Panama

Yarn Forward Nylon Filament Yarn ‟ Can be sourced from Mexico, Canada, or

Israel Certain Socks ‟ Sewn & Assembled

from U.S. knit-to-shape Certain Guayabera-Style Dresses and

Shirts ‟ Cut & Sew

10% de minimis exception* Narrow Elastic Fabric, Visible Lining Fabrics, Sewing Thread and

Pocketing Fabrics must be sourced within the region Yes

Free Trade Agreements

22

„ Central America is the second largest textile export market for U.S. (after NAFTA)

„ In 2010, nearly 70 percent of U.S. imports of apparel under CAFTA-DR were sewn from regional fabric and yarn.

„ End of 2014 expiration of Nicaragua Tariff Preference Limits (TPLs)

CAFTA - DR

23

24

0

1.000

2.000

3.000

4.000

5.000

6.000

7.000

8.000

_CAFTA-DR _NAFTA Peru Korea, South Colombia

Millionen

US apparel imports by FTA area (2013, year end)

Australia Brunei Chile

New Zealand Singapore Peru United States Vietnam

Malaysia

Mexico

Canada Japan

„ High-standard FTA with 12 participating countries ‟ 21st century agreement addressing IPR, labor and environmental issues

„ Framework for the future ‟ High-standard, addresses non-traditional trade issues

‟ Created to allow for the inclusion of new members

„ Timeline

‟ Expect to conclude negotiations early 2014

TPP

26

TPP

„ Apparel imports from TPP members make up 17% of total U.S. imports and are the fastest growing markets

„ Increases market access for exporters in growing markets for U.S. textiles and apparel

„ Streamlines foreign regulatory processes in TPP markets to facilitate greater participation by U.S. companies

„ Promotes regional integration and assures that benefits of the agreement accrue to other partners when possible

27

TPP & Bilateral Opportunities

28

„ Rising costs in Asia

„ US advantages in Yarn Production

‟ Low energy costs

‟ Positive and secure investment climate

„ Globally competitive

‟ Integrates US supply chain more closely with partners

„ Supports US jobs

‟ 1,860 jobs created in past 6 months

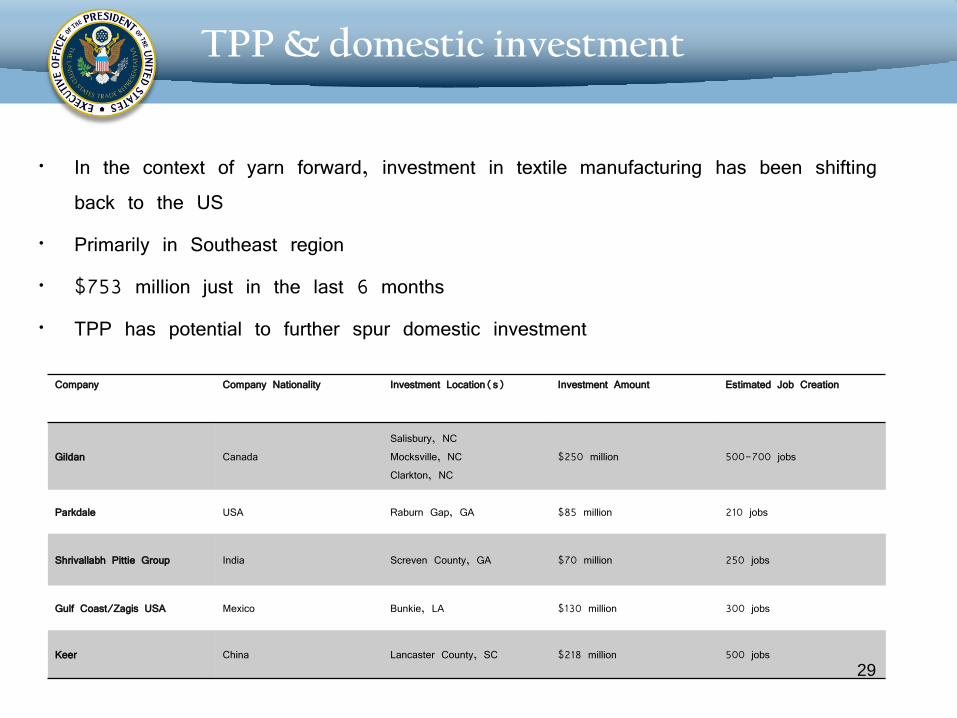

„ In the context of yarn forward, investment in textile manufacturing has been shifting back to the US

„ Primarily in Southeast region

„ $753 million just in the last 6 months

„ TPP has potential to further spur domestic investment

Company Company Nationality Investment Location(s) Investment Amount Estimated Job Creation

Gildan Canada Salisbury, NC Mocksville, NC Clarkton, NC

$250 million 500-700 jobs

Parkdale USA Raburn Gap, GA $85 million 210 jobs

Shrivallabh Pittie Group India Screven County, GA $70 million 250 jobs

Gulf Coast/Zagis USA Mexico Bunkie, LA $130 million 300 jobs

Keer China Lancaster County, SC $218 million 500 jobs

TPP & domestic investment

29

Source: OTEXA. Based on year-to-end Nov. 2013 data.

0,00

2000,00

4000,00

6000,00

8000,00

10000,00

12000,00

14000,00

CanadaMalaysia

MexicoPeru

VietnamTPP total

Value (in m

illions US

D)

U.S. Apparel Imports by TPP members

30

„ While we believe that a yarn forward rule is the best way to promote regional integration, encourage investment and create sustainable supply chains, we realize that some products may not be available from TPP partners.

„ Thus, in order to maximize the eligibility of textile and apparel products for duty preference, we have created a completely new way to establish products in short supply and allow their importation as “cut and sew”

Short supply concept

31

• NAFTA style: request rule of origin change for specific product that allows sourcing of fiber, yarn, or fabrics from outside region. U.S. first vets domestically, then consults with trading partners.

• CAFTA style: request that a specific fiber, yarn, or fabric be placed on a list that can be used in any product. Request/offer between businesses with U.S. Government determining based on submitted information whether product is available. Any availability can potentially remove a product from consideration.

Current short supply process: NAFTA & CAFTA

32

„ Simplified

„ Consolidated

„ Logical

„ Predictable

Changes under TPP Short Supply Process

33

• Governments will agree to shorts supply lists of fibers, yarns, and fabrics that can be sourced from outside the region for qualifying products. These lists will be part of the agreement when implemented

• Products must be “commercially available” to meet market needs.

• No voluminous request/offer communications need be provided

• Governments have vetted proposed products with their industries and discuss concerns to reach a resolution on which products will be included on the short supply lists

• The countries will work together to determine if products are in short supply on a temporary or permanent basis

New for TPP: Negotiated SSL

34

„ Example - 5506.3000 ‟ acrylic or modacrylic synthetic staple fiber, carded.

Entire HTS classification

„ Example - 100 percent cotton yarn-dyed woven flannel fabrics, made from 14 through 41 NM single ring-spun yarns, classified in 5208.43.0000, weighing 200 grams per square meter or less.

Subset of HTS classification

„ Example ‟ Breathable, waterproof, laminated, Man Made Fiber wovens with DWR finish used in Men's or boys', women's, or girls coats, anoraks (including ski-jackets), windbreakers and similar articles

Product with a specified end-use

Qualifying product descriptions

35

Short supply template

36

United States

European Union (28)

„ Launched summer of 2013

„ Would include the 28 EU member states

„ Comprehensive trade and investment agreement aimed to increase international competitiveness and boost growth

„ Potential to add 13 million jobs in both the US and EU

„ Third round of negotiations held in Dec. 2013

TTIP

38

„ Textiles

‟ Negotiations so far focused on regulatory issues

‟ Indicated interest in negotiating specific sectoral commitments in textiles

‟ Rules of origin have been discussed generally

TTIP

39

40

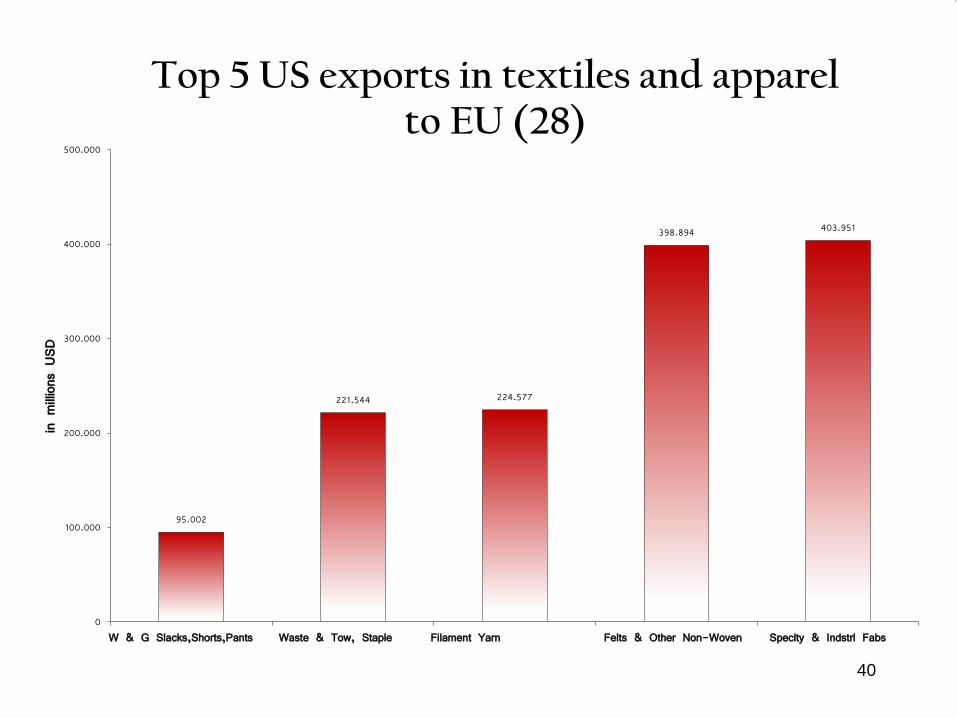

95.002

221.544 224.577

398.894 403.951

0

100.000

200.000

300.000

400.000

500.000

W & G Slacks,Shorts,Pants Waste & Tow, Staple Filament Yarn Felts & Other Non-Woven Speclty & Indstrl Fabs

in m

illions US

D

Top 5 US exports in textiles and apparel to EU (28)

41

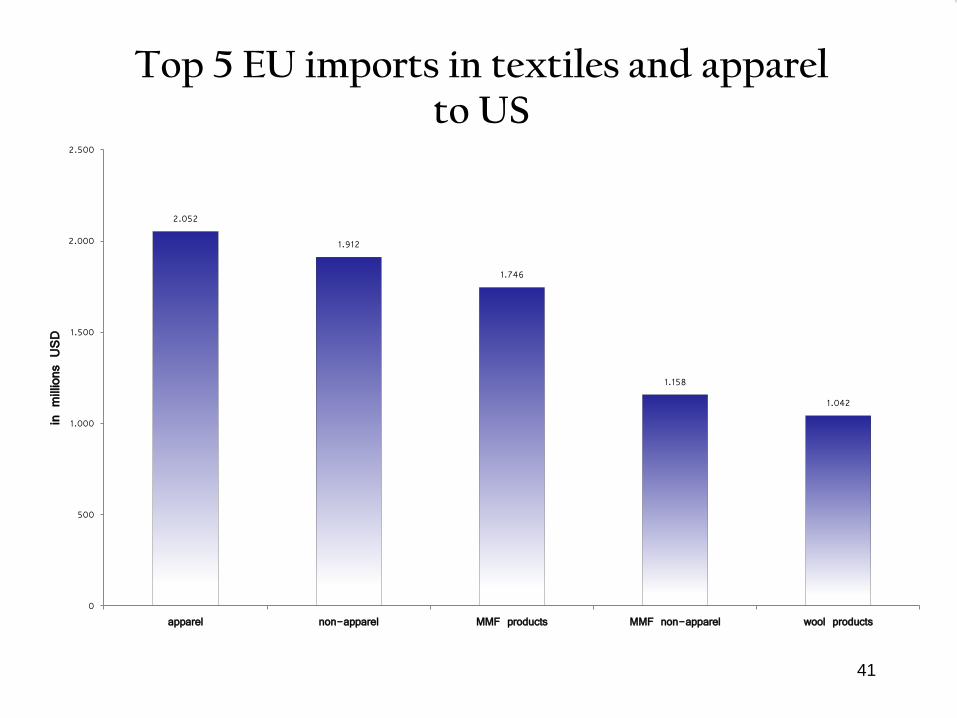

2.052

1.912

1.746

1.158

1.042

0

500

1.000

1.500

2.000

2.500

apparel non-apparel MMF products MMF non-apparel wool products

in m

illions US

D Top 5 EU imports in textiles and apparel

to US

United States Trade Representative Executive Office of the President

Gail W. Strickler

Assistant U.S. Trade Representative for Textiles & Apparel

(202) 395 – 3026

[email protected] http://www.ustr.gov/trade-topics/textiles-apparel

http://otexa.ita.doc.gov/

http://www.cbp.gov/

42