GLOBAL SUPPLY CHAIN MANAGEMENT …d332c5czpwjztv.cloudfront.net/wp-content/uploads/2014/07/...GLOBAL...

24

GLOBAL SUPPLY CHAIN MANAGEMENT SOFTWARE MARKET REPORT 2014 A CLEARWATER INTERNATIONAL TMT TEAM REPORT

Transcript of GLOBAL SUPPLY CHAIN MANAGEMENT …d332c5czpwjztv.cloudfront.net/wp-content/uploads/2014/07/...GLOBAL...

GLOBAL SUPPLY CHAINMANAGEMENT SOFTWAREMARKET REPORT 2014

A C L E A RWAT E R I N T E R N AT I O N A L T M T T E A M R E P O RT

Welcome

Companies today are constantly developing their supply chainmanagement (SCM) systems, appreciating the need for strategicSCM to be placed at the very core of their operations.

Small and mid-sized companies, as well as much larger businesses,increasingly operate global supply chains which necessitatecomplex offshoring relationships and SCM adoption. At the sametime, developments in cloud-based serving and advanced analyticshave opened up new avenues for companies to incorporate SCMand other application software into their core operations.

Today, those global supply chains also stretch ever further intoemerging economies and increased investment in emergingmarket manufacturing centres is demanding more SCM softwaretake-up. Continued strong growth in regions such as Asia andLatin America is driving heavy investment in SCM software, whilethe historically lower penetration into these markets nowpresents great opportunities for leading players.

The SCM market is also being driven by other dynamics, such asthe shortening of product lifecycles and the rise of omni-channelretailing which has led to significant growth in the warehousemanagement systems (WMS) market. The e-procurement spaceis also gaining prominence as companies strive to rationalise theirpurchasing costs, and is further escalating the shift from on-premise to cloud-based service offerings.

What does all this mean for M&A activity? Well, although thetop five SCM software vendors still account for half of themarket, beneath that it remains highly fragmented. The majorityof businesses in the sector are small and mid-sized vendors,invariably regional in their outlook, and we are now seeingtransactions that are pervading every different segment of theSCM industry.

Only this month we saw a particularly significant transaction inthe sector when Private Equity firm Accel-KKR acquiredHighJump Software and completed the merger of HighJumpwith Accellos, an existing Accel-KKR portfolio company. Thescene is most definitely set for further widespread consolidation.

We hope you enjoy the report.

@CWICFtech

/company/clearwater-international-corporate-finance

ContentsSUB-SECTOR ANALYSIS 4

A guide to the different categories that make up the SCM industry

MARKET OVERVIEW 6

The SCM market is continuing to see significant global growth

M&A ANALYSIS 10

Consolidation is driving the market as players augment their cloud offerings

E-PROCUREMENT FOCUS 13

The sector is gaining prominence as companies look for efficiencies

COMPANY INTERVIEWS 15

FourthDescartesIsotrak

PROFILES 20

A guide to 10 leading players in the SCM space

CLEARWATERINTERNATIONAL DEALS 23

Recent transactions in theTMT industry

This report is published by Clearwater International Editors: Jim Pendrill & Sarah FernandezDesign: www.creative-bridge.comSubscription: [email protected] part of this publication may bereproduced or used in any form without prior permission of Clearwater International.

Carl HoughtonGlobal Head of TMT

+44 845 052 [email protected]

GLOBAL SCM SOFTWARE MARKET R EPORT 2 0 1 42

International reach,Excellent client outcomes

AARHUS • BARCELONA • BEIJING • BIRMINGHAM • COPENHAGEN • LISBONLONDON • MADRID • MANCHESTER • NOTTINGHAM • PORTO • SHANGHAI

W W W. C L E A RWAT E R I N T E R N AT I O N A L . C O M

GLOBAL SCM SOFTWARE MARKET R EPORT 2 0 1 44

Definition

Category

TMS software guides the movementof materials to and from thewarehouse, suggesting the best modeof transport and optimum fleet size. Italso monitors the movement ofgoods and handles customs andfreight routes to ensure efficiency indelivery.

Transportation ManagementSystems (TMS)

WMS software monitors and controlsthe movement of materials within thewarehouse. It also helps design thewarehouse infrastructure, along withmanaging advanced shipmentnotifications.

Warehouse ManagementSystems (WMS)

Market Size $0.7bn $1.1bn

Drivers n Volatile fuel costs mean thatoptimum ordering quantities andtransportation methods changevery frequently, and thatdistribution channels need to berecalibrated on a regular basis.

n Globalisation of (downstream)supply chains has been more aboutrevenue growth than cost efficiencyover the last decade. Withdisruptive innovations in e-supplychains now settled and increasingcost pressure in a volatile market,developing advanced analytics–based intelligent supply chainsystems is key.

n Agile warehouse managementachieved by renting or employingstorage facilities allows rapidresponse to changing marketdemand and enables variable coststructures.

n Increasing storage rentals have ledto heightened emphasis on themicro-management of thewarehousing space, with ‘shelf-level replenishment’ becoming thenew ‘store-level replenishment’.

n Omni-channel retailing has led toa rise in the adoption of WMS, asmore and more bricks andmortar stores move towards e-retailing.

Sub-sector Analysis

Trends and Forecast n Growth is increasingly comingfrom the mid-market TMS sector.

n The TMS space has seencontinued interest in cloud-basedsolutions that require low upfrontfees and minimal ITinfrastructure.

n MarketsandMarkets forecast aCAGR (Compound AnnualGrowth Rate) of 22.8% from2013-18.

n Leading Enterprise ResourcePlanning (ERP) companies such asSAP, Oracle, Infor and Epicor havestrengthened their market positionby bundling now maturing WMS aspart of their broader ERP offerings.The result has been consolidation inthe market, leaving Manhattan as thelast large independent WMS playernot acquired by any ERP vendor.

n Technavio predicts a CAGR of16.2% between 2012-16.

A CLEARWATER INTERNAT IONAL TMT TEAM REPORT 5

Sourcing software pre-screenspotential vendors and runs eventssuch as e-auctions. Procurementsoftware carries out the actualpurchase orders, distributing theterms of purchase throughout theorganisation. It also logs expenses, aswell as taking care of reporting andcompliance issues.

$2.8bn

n Emphasis on cost control, carbonfootprint reduction and paperlessrequisitioning is driving theadoption of e-procurementsolutions.

n Increased interest in strategicsourcing application suites fromemerging markets, as productionmoves to newer manufacturinghubs.

n e-tendering by governmentsaiming to be transparent in publicsector procurements has led tothe adoption of procurementsoftware.

Sourcing and Procurement

SCP systems forecast demand byusing simulation models on historicaldata, and recommend the optimumspeed and flow of productionaccordingly. They employ advancedanalytics models to predict demand asmarket conditions change.

Supply Chain Planning (SCP)

MES manages shopfloor operationsand can be deployed on a machine orthe entire factory. It schedules andtracks each step of the productionphase of a particular job.

$3.0bn $1.5bn

n Emergence of new sellingdestinations and sourcing marketswith globalised supply chains havedriven the need for scenario- andsimulation-based modelling.

n With rapid technologicaladvancements, the life cycle ofproducts is getting shorter, requiringsupply chain executives to be awareof the latest product developmentsand have an approach based oncollaborative decision-making withall the stakeholders in the loop(especially production managers and suppliers).

n Stringent environmental regulationshave led to an increased emphasis onthe development of sustainabilitymodels to analyse and monitor usageimpact (carbon, energy, water, waste,etc.) during the planning phase.

n Emerging low-cost manufacturinghubs in Asia-Pacific are expectedto be the growth engine for MESdemand.

n The emphasis on greenproduction involves replacingpaper-based operator andprocedure manuals and datasheets with electronic documentsdelivered on mobile devices onthe shopfloor.

n The shift towards leanmanufacturing advocates theincreasing adoption of MES andits integration with WMS toestablish operating models withless working capital requirements.

n ERP vendors have a strongpresence in transaction-basedsolutions. Players with localvendor and niche segmentknowledge continue to excel instrategic procurement activities.

n As per Gartner, the market forprocurement technologies isexpected to reach $3.5bn by2015, representing a five-yearCAGR of 10.1%.

n There has been above-averagegrowth in SCP sales to thesemiconductor and other high-techindustries. The household &personal care and food & beverageindustries have both witnessedabove average growth due to astrong post-recession rebound.

n The SCP market is expected toshow a CAGR of 10% from 2011-16, according to ARC Advisory.

n Sectors where MES is extensivelydeployed include automotive,textiles and power.

n MarketsandMarkets estimates theMES market to reach $8.9bn by2016, maintaining a CAGR of13.6% from 2011-16. Technaviohas a CAGR estimate of 11.7%from 2011-15.

Manufacturing ExecutionSystems (MES)

GLOBAL SCM SOFTWARE MARKET R EPORT 2 0 1 46

Market Overview

The SCM software market is seeing significant global growth.

* Market Share Analysis: Supply Chain Management Software, Worldwide, 2012, Gartner** Technology – Software, BMO Capital Markets (Jan 2014)

Source: Gartner

Source: BMO Capital Markets

The market was estimated to be worth $8.3bn in2013 (up 7.1% year on year), but is expected to soarto $13.4bn by 2017, according to Gartner*.Meanwhile, overall IT spending is projected to reach$3.8tn this year**, up 3.1% from $3.7tn in 2013.

Enterprise software (CAGR: 6.8%) continues to drivethis growth, with SCM and Customer RelationshipManagement (CRM) witnessing double-digit growth.

North America and Western Europe remain theprime consumers of SCM software, accounting for77% of market revenue. However, strong economicgrowth in Asia and Latin America, coupled with themodernisation of the manufacturing and constructionindustries in these regions, is driving heavy investmentin SCM software in emerging markets. Also, lowerpenetration of the software and a sizeable domesticmarket, particularly in countries such as India, Chinaand Indonesia, have fuelled growth.

Asia-Pacific has continued to experience particularlyrobust growth in the sector, owing to increasinginvestment in emerging market manufacturing centres.According to an IDC forecast of the software market,the average 2012-17 CAGR for Asia-Pacific (excludingJapan), Latin America, and Central Eastern/MiddleEast/Africa (CEMA) is 8.2%. The average CAGR forNorth America, Europe and Japan is 5.4%.

Global SCM Software Market

0

3

6

9

12

15

6.0

2007 2008 2009 2010

Historical CAGR 6.8%

2011 2012 2013 2014 2015 2016 2017

6.26.8

7.78.3

8.9

10.0

11.1

12.2

13.4

6.1

Growth CAGR 10.0% (est)

$bn

Overall IT 3.1

Enterprise Software 6.8

SCM 10.0

CRM 14.4

ERP 6.2

Business Intelligence 7.2

Segment Spending Forecast CAGR (%)(2012-17)

7

Fragmented market

A CLEARWATER INTERNAT IONAL TMT TEAM REPORT

Although the top five SCM software vendors accountfor 50% of the market by value, the other half remainshighly fragmented. A majority of businesses in thesector are small and mid-sized vendors that offer awide range of regional and segment-specific best-of-breed (BoB) options.

BoB vendors continue to dominate within individualmarkets such as TMS, WMS and CRM. Meanwhile,competition between ERP and BoB vendors hasintensified over the past year, triggering significantM&A activity.

Source: BMO Capital Markets

Source: Gartner

World Enterprise Software Revenue Growth by Sub Segment

3

6

9

12

15

2013

4.5

7.0

8.6

13.5

5.5

7.4

10.6

14.8

6.2

7.2

11.2

14.7

6.7

7.2

10.1

14.6

7.1

8.0

9.7

14.6

2014 2015 2016 2017

%

–n– ERP

–n– Business Intelligence

–n– SCM

–n– CRM

Worldwide IT Spending Forecast ($bn)

Devices 6.5

Growth (%)

2014

740

Spending

2.8

Growth (%)

2013

695

Spending

10.9

Growth (%)

2012

676

Data Centre Systems 4.11492.11431.8140

Enterprise Software 6.63246.43044.7285

IT Services 4.69682.29262906

Telecom Services 2.31,6940.91,655-0.71,641

Overall IT 4.13,8752.13,7232.53,648

Spending

GLOBAL SCM SOFTWARE MARKET R EPORT 2 0 1 48

Market trends

The market dynamics of the sector remain very strongwith small and mid-sized businesses, as well as largercompanies, increasingly having global supply chains andcomplex offshoring relationships, thereby necessitatingSCM adoption.

Developments in mobility, cloud-based serving andadvanced analytics have lowered the total cost ofownership and opened up new avenues forcompanies to incorporate SCM, ERP and otherapplication software into their core operations. Otherfactors driving the market include:

n The need for reduced time to market for newproducts and services and the shortening ofproduct lifecycles has put pressure on supplychains. Cloud computing will further acceleratethis trend, fuelling the adoption of SCM software.Penetrating the vast markets of the emergingeconomies has become much easier with theadoption of cloud/internet-based technologies.

n Transport cost reduction in a volatile fuel/energymarket is an important agenda for companies andhas provided a boost to TMS adoption.

n Omni-channel retailing has led to a rise in theadoption of WMS, with an increasing number of bricks and mortar stores moving towardse-retailing.

n The advent of new selling destinations andsourcing markets, with globalised supply chains, hasled to the need for scenario- and simulation-basedmodelling. This has provided a boost to analytics-based procurement solutions.

n The emergence of low-cost manufacturing hubs inAsia-Pacific is expected to be the growth engine ofdemand for MES.

Against this backdrop, the market share of the leadingSCM players has increased in recent years as themarket consolidates, particularly in the procurementtechnology arena.

As companies increasingly appreciate the need forstrategic SCM to be placed at the very core of theiroperations, growing competition from small BoBcompanies has compelled ERP vendors to extendhistorically rigid ERP systems (designed for the low-tech manufacturing era) to more competitive on-demand subscription-based models.

Large ERP vendors, driven by the growing needamong clients for real-time purchase information, arefocusing on building analytics-based offeringsinorganically. This trend has been reflected in therecent acquisitions of KXEN and SmartOps by SAP,and by Oracle’s acquisitions of both DataRaker andCollective Intellect.

Source: Gartner

Change in Market Share - Top 5 Players

2008 2009 2010 2011 2012 2013

48 48 48

52

49

47

40

44

48

52

56

60

%

SAP

Oracle

JDA

Manhattan Associates

Epicor

Top 5 Players 2013

9

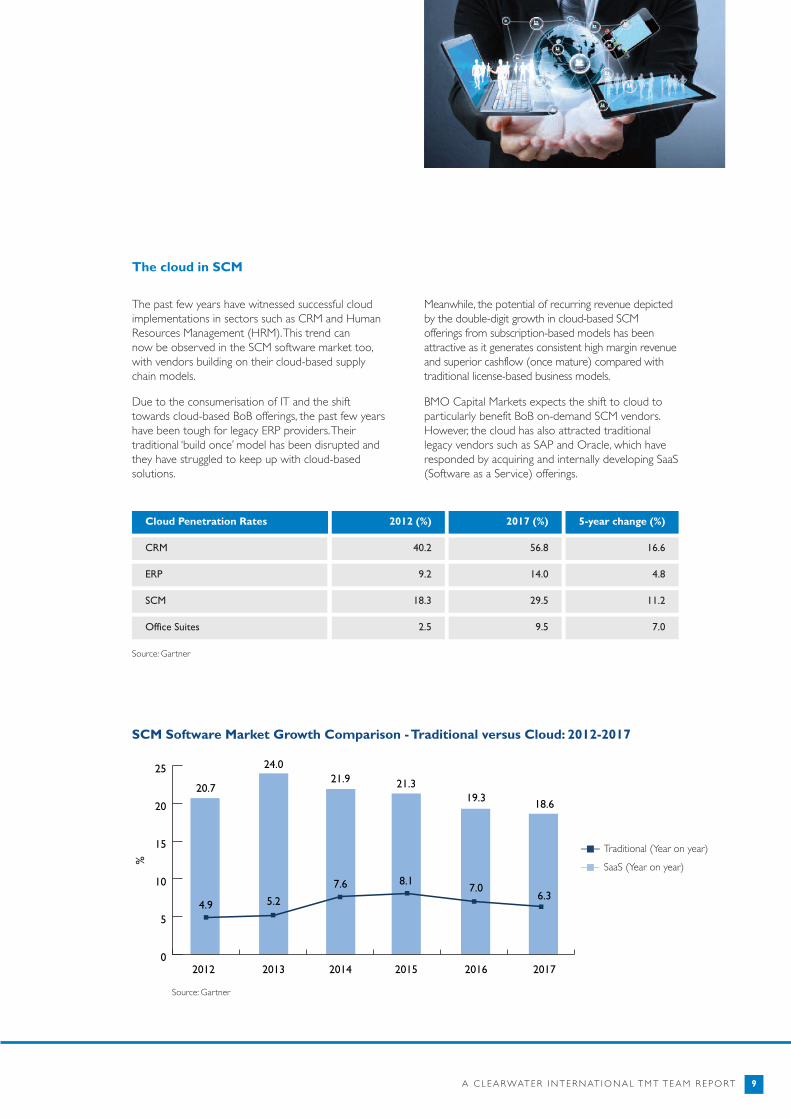

CRM 40.2 56.8 16.6

ERP 9.2 14.0 4.8

SCM 18.3 29.5 11.2

Office Suites 2.5 9.5 7.0

Cloud Penetration Rates 2012 (%) 2017 (%) 5-year change (%)

The cloud in SCM

A CLEARWATER INTERNAT IONAL TMT TEAM REPORT

The past few years have witnessed successful cloudimplementations in sectors such as CRM and HumanResources Management (HRM). This trend can now be observed in the SCM software market too,with vendors building on their cloud-based supplychain models.

Due to the consumerisation of IT and the shifttowards cloud-based BoB offerings, the past few yearshave been tough for legacy ERP providers. Theirtraditional ‘build once’ model has been disrupted andthey have struggled to keep up with cloud-basedsolutions.

Meanwhile, the potential of recurring revenue depictedby the double-digit growth in cloud-based SCMofferings from subscription-based models has beenattractive as it generates consistent high margin revenueand superior cashflow (once mature) compared withtraditional license-based business models.

BMO Capital Markets expects the shift to cloud toparticularly benefit BoB on-demand SCM vendors.However, the cloud has also attracted traditionallegacy vendors such as SAP and Oracle, which haveresponded by acquiring and internally developing SaaS(Software as a Service) offerings.

Source: Gartner

Source: Gartner

SCM Software Market Growth Comparison - Traditional versus Cloud: 2012-2017

0

5

10

15

20

25

2012 2013 2014 2015 2016 2017

4.9

7.6 8.16.3

7.05.2

20.721.9 21.3

18.619.3

24.0

%

–n– Traditional (Year on year)

–n– SaaS (Year on year)

GLOBAL SCM SOFTWARE MARKET R EPORT 2 0 1 410

M&A Analysis

The market has been characterised in recent years bysoftware players augmenting their cloud capabilities andthe concerted efforts of large ERP vendors to ramp uptheir suites with analytics-enabled SCM solutions.

This has led to significant consolidation in the market,with acquisitions pervading different segments of theSCM software industry. The graphs (below and right)highlight the consolidation trend since 2012, inparticular showing how two especially large deals -

SAP’s acquisition of Ariba and RedPrairie’s acquisitionof JDA - have dominated the market in terms of value.

However, since those transactions in 2012 there hasbeen a fall in the overall value of deals - even thoughvolumes have grown. Meanwhile, EBITDA multipleshave now stabilised at about 11.3x, indicating thatstrategic acquisitions of smaller players in the marketis continuing to attract higher multiples.

The SCM space is witnessing increasing M&A activity.

Source: Berkery Noyes

M&A Market Dynamics

0

500

1000

1500

2000

2500

3000

3500

0

Jul 09 Jan 10 Jul 10 Jan 11 Jul 11 Jan 12 Jul 12 Jan 13 Jul 13 Jan 14

446

714

290 94433

3,003

334 239520

5

10

15

20

25

7 7 78

11

14

9 9

17

22

$m

–n– Transaction Volume

–n Aggregate Value ($m)

A CLEARWATER INTERNAT IONAL TMT TEAM REPORT 11

Deals review

Deal highlights of the past year include:

n US SCM solutions provider Moduslink GlobalSolutions received an investment of $30m fromSteel Partners Holdings, as it increased itsshareholding in the company to 33%.

n Cloud-based expense tracking softwaredeveloper Xpenser was acquired by cloud-basedspend optimisation software provider Coupa toexpand the latter’s domain expertise andleadership in the area of expense management.

n SAP acquired predictive analytics-based inventoryand supply chain optimisation software developerSmartOps. The acquisition further enhancedSAP’s SCM capabilities following its takeover ofAriba in 2012. SAP also acquired KXEN,combining the company’s predictive analyticssoftware with its own advanced analyticscapabilities. The deal provides a fillip to SAP’s ownsupply chain planning and scheduling solutions.

n Cloud-based SCM solutions provider E2Openacquired icon-SCM for $34m, to integrate itsplanning and analytics capabilities with its own suite.

n French PE house Argos Soditic acquired AkaneaDéveloppement, a subsidiary of SAGE offeringTMS solutions, in a deal worth $44m.

n Manufacturing software provider Apriso wasacquired by Dassault Systèmes for $205m.

n Synova Capital acquired UK-based TMS provider Mandata.

n Kewill, a UK-based TMS provider, acquired Indianmulti-modal transportation and supply chainexecution software provider FourSoft for $43m.

n Dutch PE firm Main Capital acquired anundisclosed stake in the niche food sourcing andsupply chain monitoring software developerChainfood, as part of a buy-and-build strategy.

Source: Berkery Noyes

Median Enterprise Value Multiple

0

500

1000

1500

2000

2500

3000

3500

0

2

4

6

8

10

12

1.5 1.8

7.37.7

9.9

11.3

1.3

3.22.8 2.8

Jul 09 Jan 10 Jul 10 Jan 11 Jul 11 Jan 12 Jul 12 Jan 13 Jul 13 Jan 14

Mul

tiple

$m

–n– Value

–n– EBITDA Multiple

–n– Revenue Multiple

GLOBAL SCM SOFTWARE MARKET R EPORT 2 0 1 412

Global HealthCare Exchange

Target

Thoma Bravo

Acquirer

EGS Group PROACTIS Holdings

Impatex Freight Software The Descartes Systems Group

Chainfood Main Capital

Planipe Ordirope

Profit Systems Accellos

Epyx FleetCor

Delta Energy Solution Powel

Procurian Accenture

OB10 Tungsten

CombineNet SciQuest

Four Soft Kewill Systems

icon-SCM E2OPen

Curtis Fitch De Beers

Evenex HighJump Software

Alligacom Dicentral Corporation

Epic Data International Sylogist

Akanea Développement Argos Soditic

TDCI Infor Global Solutions

Innovative Automation SI Systems

Open Mile Echo Global Logistics

SmartOps SAP

KSD Software Norway The Descartes Systems Group

Newtron Liechtenst. Post Beteiligungs

Production Modelling Access Group

Compudata The Descartes Systems Group

Mercareon The Riverside Group

Less Software FinancialForce.Com

GXS OpenText

BigMachines Oracle

KXEN SAP

MarketMaker4 Xchanging

ChemSW Accelrys

WaveMark Cardinal Health

Ascendo System (Assets) Medius

Mandata Synova Capital

Boxlogix Automation Wynright Corporation

Triple Point Technology ION Trading Ireland

Apriso Dassault Systèmes

Netsis Yazilim Logo Yazilim

TradeCard GT Nexus

Datilog Exprivia SpA

Xpenser Coupa Software

Transite Technology 3Gtms

Moduslink Global Solutions Steel Partners Holdings

Transpole Logistics Everstone Capital Management

WAM Systems Triple Point Technology

Deals in the global SCM software market 2013-14 (most recent first)

A CLEARWATER INTERNAT IONAL TMT TEAM REPORT 13

The e-procurement space is being transformed in thecloud computing era. E-procurement has respondedstrongly to the attractive market demand forprocurement technology by escalating the shift fromon-premise to cloud-based service offerings, furtherreducing the set-up cost for companies.

The lower initial costs (savings on infrastructure),coupled with seamless upgrades, scalability andintegration, are driving the adoption of cloud-based e-procurement solutions. Recent acquisitions made bySciQuest, Coupa Software and Basware, along withSAP’s acquisition of Ariba, reflect the 'cloud war'prevailing in this space.

E-procurement in the application software market hasgained particular prominence, with companies strivingto rationalise their purchasing costs and prune theirsourcing and procurement processes in order toremain competitive in the wake of the globalslowdown.

The global procurement applications market stood at$3.7bn in 2012 (as per IDC), a growth of 2.7% year onyear. Key vendors in the procurement applicationsmarket are SAP (Ariba Inc.), Basware Corp.,BravoSolution, Iasta, Oracle and GEP.

E-procurement solutions deliver economic value,irrespective of market slowdown, resulting in healthyand stable demand. The adoption of e-procurementsolutions is receiving further impetus as companieslook to shorten their supply chains.

Market drivers

The focus on austerity and fiscal prudence in advancedeconomies, and on government transparency inemerging economies, continues to reiterate theimportance of e-tendering in the public sector.

Real-time spend analysis capabilities plus big dataanalytics and reporting are becoming a constituentmodule of e-procurement suites, making supplier riskmanagement an integral part of the sourcing function.The defence sector (one of the largest segments interms of the size of procurement deals) has increasinglywitnessed a trend of reverse auctioning forprocurement.

Currently, there are 30 major players in the market -however, most operate only regionally with manylocated in North America, Western Europe and theUK. Newer manufacturing hubs in the emergingeconomies are driving an increase in demand forstrategic sourcing applications, such as e-sourcing,contract management, supply base management(SBM) and spend analysis.

The market is fragmented, with few large players atthe top and a large base of small local vendors. Playerswith local vendor and niche segment knowledgecontinue to excel in strategic procurement activities.However, significant consolidation is required foreconomies of scale, visible from the recent deals bySciQuest and SAP.

E-procurement Focus

The lure of ERP vendors to offer cloud-based procurementsolutions is triggering further consolidation in the sector.

GLOBAL SCM SOFTWARE MARKET R EPORT 2 0 1 414

The quest for cloud-based procurement, attractivemarket demand, and interest in end-to-endapplication suites has fuelled a wave of acquisitionsby ERP vendors in this space. Notwithstanding theeconomic crisis, e-procurement business has beenbooming, attracting the attention of the largestsoftware players such as SAP, IBM and Oracle.

Recent deals have showcased the strong marketpotential and quest for acquisitions to improvescalability and presence in a fragmented market.

Recent deals in the sector include:

n Proactis Group acquired EGS to become thelargest player in the public sector procurementspace in the UK.

n Accenture acquired Procurian, a provider ofBPO services focused on the procurementfunction, for $375m.

n SAP entered cloud-based procurement with itsacquisition of Ariba, the world’s second-largestvendor serving 200,000 companies, for $4.3bn.The deal’s EV/EBITDA multiple was 36.1x,massively exceeding the market median of 9x forsoftware deals. This showcases the pursuit ofERP vendors to exploit the high-growthapplication software sub-segment.

n IBM entered the cloud-based e-procurementspace with its acquisition of Emptoris, a providerof cloud and on-premise analytics software forprocurement.

Large players are not the only companies seekinggrowth opportunities in the e-procurement market.The consolidation trend was also visible in the mid and lower layer of the market with the following deals:

n SciQuest acquired Combinenet, a provider ofadvanced sourcing software, for $43m. The deal’sEV/Revenue multiple was 3.5x.

n Xchanging acquired marketmaker4, a softwareand consulting start-up for online procurement,for $22m.

n Medius acquired the assets of e-invoicing andsourcing solutions provider Ascendo System.

n Coupa Software, the leading provider of cloud-based spend optimisation solutions, acquiredXpenser, a company that enables users to recordand track expenses more efficiently.

n Basware acquired the network and e-invoicingbusiness of Certipost for $24m.

n Informatica Software acquired Heiler Software,an e-procurement software company, for $88m.

M&A activity

A CLEARWATER INTERNAT IONAL TMT TEAM REPORT 15

INTERVIEW:

Fourth

Given that Fourth's customer base ranges from singlesite hotels, pubs and restaurants through to large,multi-brand, multi-site operators, there is certainly noshortage of new business to target.

There is actually plenty to go at with existingcustomers - as Ben Hood, Chief Executive of the fast-growing company, explains: “30% of our clients takeour whole suite of products, so there is naturalgrowth for us to be had in converting as many of theremaining 70% as possible. That's something of a holygrail for us. It's about persuading them of the vastbenefits and efficiencies that they can generate from asingle integrated system, a system where everythingtalks to each other as it should do."

This ‘end-to-end’ supply chain mantra has been core to the Fourth model since it was founded. The company is currently owned by private equityhouse ECI Partners, which invested in the businessthree years ago. Clearwater International advisedECI on that investment.

Hood accepts that not every client will want the fullsuite, especially the larger blue-chip customers. “We callit a decoupling approach, whereby you can use ourproducts as separate pieces as you see fit,” he explains.“So part of our strategy allows large blue-chips thatmay have a SAP system at the front-end managingmost of their HR data to then use specific 'best ofbreed' Fourth products behind that. The idea is thatthey start to see the benefits that just one of ourproducts can bring, so that in time they start replacingmore and more of their systems.”

Hood admits that for some international businesses it issimply unrealistic to expect them to change all theirsystems overnight. By the same token, Fourth itself is -for the time being at least - not set up to handle hugeglobal volumes. “Right now we wouldn't be able toprocess payroll in, say, 80 countries for someone. Butwhat we can do is try and lead a client down aparticular path. Big multinationals often have very clunkysystems performing core functions. Part of our job is tohelp drive their strategy, which means getting a foot inthe door and explaining what we can do for them."

Hood says there is still plenty to go at across thebroader market spectrum. “Although sometimes wemight think we have a large part of the market, in factthere are still many businesses in the hospitality sectorwhich we don't touch. We have no need to gooutside the hospitality sector, there are plenty ofopportunities within.”

There are plenty of new geographies to consider too.“We are looking at new regions all the time - forinstance, we have just started in Australia and Asiawhile we have some very good product combinationswhich lend themselves well to the hotel market in theMiddle East. When you have hotels which operate allacross the world, they want to know who yourpartners are across the world. It's time for us to startbuilding those global alliances.”

A big focus for Fourth is the US, where it acquiredAdaco - a leading provider of SaaS-based inventorymanagement solutions to the global hotel market -two years ago. Half of Adaco's customers were in theUS, and its product offering has since slotted in tobecome Fourth's purchasing product for the hotelmarket, fitting alongside Fourth's existing stock,analytics, procurement and HR systems. In terms offuture M&A strategy, Hood doesn't rule out furtherdeals if they bring “more sector expertise or naturaladd-ons”, he says.

“In this fast-moving sector, we are constantly askingourselves what we can do to push the envelope out,what we can do to maintain our client base andprovide the market with the products it needs. Wehave a saying that every business needs to be thinkingabout social, mobile, analytics and cloud. We tick allthose boxes and are on a strategic journey builtaround these concepts. For instance, the whole areaof mobile communities and engendering closercollaboration between clients is huge. We are takingour customers on a journey, building further on thepillars within their business, while really evolving theirsystems too.”

Fourth, a leading SaaS provider of back office management systemsto the leisure sector, is seeing increasing global opportunities.

GLOBAL SCM SOFTWARE MARKET R EPORT 2 0 1 416

One of the biggest North American players in theSCM market is Canadian company Descartes whichhas been a particularly acquisitive player in recentyears, buying up a number of companies in Europe.

Ed Gardner, Executive Vice President - CorporateDevelopment, says the business has set its sights on thesimple goal of being a leader in global logistics. “For anyshipment moving from A to B, there are a lot of peopleand a lot of assets required to make that processhappen and there is a lot of commonality in what wedo across the world. Our goal is to be able to connectall parties in a manageable process, help them sharethe data they need and then help them digest andleverage that data to their benefit so that they makebetter decisions.”

Gardner admits that managing supply chains can be hard enough when your business is only tradingdomestically. But if you are looking to expand globally, then the number of parties involved canrapidly increase, such that effective SCM systemsbecome absolutely crucial to the smooth running of the business.

One of the big trends that Descartes is tapping into isomni-channel retailing. As Gardner adds: “Everyone isasking ‘how do I deal with Amazon, how do I ensurethat customers get the deliveries they want, whenthey want?’ Amazon has simply changed theexpectations of consumers, and retailers are playingcatch-up. For us that is a great opportunity.”

“We can take a multi-modal, globalapproach precisely because globalsystems are so interconnected. Tofacilitate good logistics, you needdata from a lot of different people,and the global logistics networkwill only get bigger.”

He says omni-channel is now “very hot” in countriessuch as the UK, but it is also building up pace in NorthAmerica. “The region has been a bit behind in thiswhole area because it isn’t so densely populated andpeople wondered how the model could work. But it iscatching up fast now, the Amazon effect is spreading.People want something and they want it now, andretailers need to find ways of dealing with that. We are having a lot of conversations with traditionalretailers, asking them precisely how they intend tokeep up with Amazon.”

Gardner says Descartes' specialism is offering real-timeoptimisation services, looking at every order as itcomes in every second of the day. “We can then sayto the client, ‘OK here are the orders you've gotcoming in. And here is what all the service engineersare doing right now. And here is where your driversand transport systems are at that precise time’. It isabout fundamentally changing the game in terms ofhow a client provides customer service, but also anopportunity for them to add new services too.”

Gardner says another big growth area is security andhelping customers deal with an increasing regulatoryenvironment. “This has been a massive area forinvestment and growth for us over the last six orseven years, whether it be assisting airlines, oceancarriers or road hauliers comply with legislation, or justhelping exporters or importers comply with dutiesand tax requirements."

He says the regulatory drive particularly stemmedfrom 9/11 and the US government tightening securitysystems around trade movements. Specifically, thegovernment has tightened up cargo inventory systemsto ensure that the US knows exactly what cargo is onevery plane and on every ship hours before it lands ordocks. Gardner says complying with these regulationsplaces a great burden on gathering the required data,and says that governments around the world are nowadopting very similar practices.

As the world's logistics network grows ever larger, global SCMplayer Descartes is perfectly placed to capitalise.

INTERVIEW:

Descartes

A CLEARWATER INTERNAT IONAL TMT TEAM REPORT 17

“Governments want more data and want it earlier inthe process. It is also driving the requirement forlogistics players to share data earlier. A company likeus, that operates a global neutral network, can thencollect the data from the different players and handlethe multi-party requirements. Although in manycountries there are logistics players who are verygood at what they do, we can take a multi-modal,global approach precisely because global systems areso interconnected. To facilitate good logistics, youneed data from a lot of different people and theglobal logistics network will only get bigger.”

Descartes’ growing specialism in the security sectoris being stoked by M&A activity too. For instance: thecompany recently acquired KSD, a Scandinavianprovider of electronic customs filing solutions anddeveloper of software for security filing.

Gardner sees plenty of M&A opportunities in thewider SCM market. Recent Descartes deals includethe acquisitions of Swiss e-invoicing specialistCompudata, and of Exentra Transport Solutions, aprovider of SaaS driver compliance services to thelogistics industry. In the latter deal, ClearwaterInternational advised the sellers.

On the wider M&A front, Gardner feels the SCMmarket is still very fragmented as a result of the waythat the logistics industry has evolved over the years.“A lot of companies are very good at what they dowithin their own borders, and there are a lot ofniche players out there who have functionality thatwould interest us. The challenge is picking the rightones, as there are literally hundereds of companiesto choose from. We have to have a very disciplinedapproach to M&A and look for market leaders withhighly recurring revenues that will also fit culturallywith our model.”

Gardner says the European market is still particularlyfragmented. “A country such as the UK is atremendous opportunity because of the high degreeof focus on logistics value, a lot of which is beingdriven by retail and home delivery. The lessons youcan learn and the systems you can develop can thenbe exported further afield.”

CASE STUDY:

John LewisA good example of Descartes' providingomni-channel solutions is for retailer JohnLewis, whom Descartes has been workingwith on home delivery solutions.

John Lewis has been using DescartesReservations™ to improve route planning ofits in-house fleet, while reducing deliverymiles and transportation costs.

The retailer has always had its own in-housefleet of vehicles, but says in the past thecustomer had no visibility and the systemwas inefficient because there was alwaysslack in the schedule. Now the Descartessystem digests all the key supply chaininformation and then decides how bestto manage the whole delivery process more efficiently.

John Lewis says since the introduction ofDescartes’ software, it has seen a 500%increase in service take-up across itsnetwork, providing customers with a one-stop shop where they can buy products andservices all in one click whether in-store oron the web.

Adds Gardner from Descartes: “It is allabout providing very quick response timesand optimising the technology that JohnLewis has at its disposal, so that it cancontinually find the optimum delivery slots.”

GLOBAL SCM SOFTWARE MARKET R EPORT 2 0 1 418

For Isotrak Chairman Gavin Whichello, commercialsuccess is all about “finding your sweet spot”, as hecoins it. “Yes, you've got to have great focus, a robustmodel, great technology and recurring revenues. Butyou've also got to know where your sweet spot is tomake it all come together.”

For Isotrak, that sweet spot can be found insupermarkets where its leading-edge cloud-basedsoftware platform is helping reduce supply chaincosts, improve operational efficiencies, lessenenvironmental impacts and ultimately improvecustomer service.

With such a selling proposition, it is little wonder thattoday the company boasts a string of large blue-chipretailers, leading third party logistics providers andother corporates among its clients who are keen toembed Isotrak's technology in their supply chains.

Whichello says it is precisely Isotrak's ability toprovide a total fleet vision of back of store deliveriesfrom third and fourth party logistics providers, as wellas of deliveries to and from distribution centres frombranded fleets, that is so compelling for clients. He adds: “It allows supermarkets to have one view of all deliveries, whether from their fleet or from food manufacturers or from third and fourth party logistics providers.

“We have a complete supermarket delivery modeland really understand how their supply chains work.Large supermarkets can have tens of thousands ofvehicles in their fleet and what they want istechnology that they can bring in to the whole fleet.They want that total vision.”

“You’ve got to have great focus, arobust model, great technology and recurring revenues. But you’vealso got to know where your sweet spot is.”

Vehicle tracking and fleet management software is business-critical for major fleet operators and Isotrak is one of its leading specialists.

INTERVIEW:

Isotrak

A CLEARWATER INTERNAT IONAL TMT TEAM REPORT 19

Whichello says this means that Isotrak's sales andmarketing has to be absolutely focused on theentire business of the client. “Ultimately we cancreate tremendous efficiencies for supermarkets, sothat their drivers and lorries are always in the rightplace at the right time. To achieve that, we need toknow precisely what is going in and out of depots allthe time, we need to have all that data and to buildsystems to manage that.”

Isotrak's technology can also help supermarketsmanage consumer expectations in home delivery.Adds Whichello: “If you take something like thehome delivery market, then all supermarkets arefacing some serious competition down the trackand they know that their systems have to be up tothe challenge. If you look at what Amazon has doneto the home delivery market, then it doesn't take agenius to say ‘why can they not do with food whatthey have already done with books?’”

He says Isotrak’s tracking and fleet managementsoftware is among the most advanced in the world,and its products are increasingly in demand acrossthe globe. He is particularly excited by opportunitiesin North America, where routes are longer, sites are more disparate, and the growth of homedelivery is creating a greater need for fleetmonitoring and compliance.

However, the company is eyeing considerable globalexpansion too and has very strong prospects inCanada, Australia and mainland Europe. AddsWhichello: “If you take somewhere like the US, wehave taken business from local players in their ownbackyard which really says something about thestrength of our products. If anything, our productsare even more suited to the US market.”

One of Isotrak's largest US customers is Papa John'sPizza. “That's a business with 35,000 home deliverydrivers. The company wants to be optimising theirsupply chain and monitoring it as closely as they can,which is exactly where we come in.”

Expansion into the US was one of the key driversbehind the acquisition of Isotrak last year by privateequity house Lyceum Capital. The new investor hasplans to accelerate both Isotrak’s UK and NorthAmerican expansion strategies, while increasinginvestment in the development of its cloud-basedproduct suite.

Lyceum Partner Daniel Adler comments: “Isotrakhas a tried, tested, proven, intelligent and ambitiousmanagement team. Meanwhile, in terms of clients,you could not ask for a more robust set of blue-chipcustomers and recurring revenues. We have lookedat a huge number of players in this market and lovedIsotrak's model of ‘landing and expanding’.”

‘The company is eyeing considerable global expansion and hasvery strong prospects in Canada, Australia and mainland Europe.’

GLOBAL SCM SOFTWARE MARKET R EPORT 2 0 1 420

Revenues: $m2013 23,0372012 21,4242011 18,573

Revenue CAGR: 2011-2013 11%

EBIT: $m2013 6,1362012 5,3372011 6,369

EBIT CAGR:2011-2013 -2%

Revenue breakdown(2013):Software and Software related services 83%Professional and other services 17%

Geographical breakdown(2013):EMEA 47%Americas 38%APAC 15%

Workforce:66,000

Recent M&A activity:Acquired Hybris, an ERP andprocurement software vendor.

Acquired SmartOps, an SCMsoftware developer.

Acquired Ariba, aprocurement and SCMsolutions provider.

SAPGermany

SAP is the world’s third largestsoftware manufacturer bymarket capitalisation. Thecompany has more than251,000 customers in 188countries. SAP SCM is part ofthe SAP Business Suite, whichgives organisations the ability toperform business processeswith modular software that isdesigned to work with otherSAP and non-SAP software.

Revenues: $m2013 2,7182012 2,5412011 1,874

Revenue CAGR: 2011-2013 20%

EBIT: $m2013 466 2012 137 2011 234

EBIT CAGR:2011-2013 41%

Revenue breakdown(2013):Maintenance 53%Consulting 28%License 19%

Geographical breakdown(2013):Americas 57%EMEA 34%APAC 9%

Workforce:12,700

Recent M&A activity:Acquired TDCI, a productconfiguration managementsoftware developer.

Infor Global SolutionsUS

Infor has more than 70,000customers with 153 directoffices in 41 countries andimplementations and supportcapabilities in 194 countries.The company offers threeproducts - SCM WarehouseManagement, Infor SupplyChain Planning, and Infor Salesand Operations Planning.

Profiles

Revenues: $m2013 37,1802012 37,1212011 35,622

Revenue CAGR: 2011-2013 2%

EBIT: $m2013 14,695 2012 13,847 2011 12,316

EBIT CAGR:2011-2013 9%

Revenue breakdown(2013):Software 74%Hardware Systems 14%Services 12%

Geographical breakdown(2013):Americas 53%EMEA 30%APAC 17%

Workforce:120,000

Recent M&A activity:Acquired BigMachines, acloud-based developer ofsales order processing.

OracleUS

Oracle serves 400,000customers in 145 countriesacross a wide range ofindustries. It provides industry-specific supply chain softwarepackages, including Oracle E-Business Suite Supply ChainManagement, JD EdwardsEnterpriseOne Supply ChainManagement, PeopleSoftEnterprise Supply ChainManagement, and JD EdwardsWorld ManufacturingManagement.

Revenues: $m2013 99,7512012 104,5572011 106,916

Revenue CAGR: 2011-2013 -3%

EBIT: $m2013 19,8552012 22,4262011 21,513

EBIT CAGR:2011-2013 -4%

Revenue breakdown(2013):Software 26%Services 57%Systems, Technology and Hardware 17%

Geographical breakdown(2013):Americas 43%EMEA 32%APAC 23%OEM 2%

Workforce:434,246

Recent M&A activity:Acquired Emptoris, a supplychain intelligence and analyticssolutions provider.

IBMUS

IBM operates in 170 countrieswith its SCM solutionsdelivering supply chainplanning and executioncapabilities. Its SCM offeringsinclude SterlingTransportation ManagementSystem, Sterling WarehouseManagement System, SterlingSupply Chain Visibility VendorCompliance, Sterling SupplyChain Visibility, and SterlingSupplier Portal.

A CLEARWATER INTERNAT IONAL TMT TEAM REPORT 21

Revenues: $m2013 4152012 3762011 329

Revenue CAGR: 2011-2013 12%

EBIT: $m2013 101 2012 80 2011 61

EBIT CAGR:2011-2013 28%

Revenue breakdown(2013):Services 76%Software License 15%Hardware and other 9%

Geographical breakdown(2013):US 82%EMEA 12%APAC, Canada &Latin America 6%

Workforce:2,400

Manhattan AssociatesUS

Manhattan Associates hasover 1,200 global customers.The company's supply chainproducts include ManhattanSCOPE, Manhattan SCALE,and Manhattan Carrier - a suite of supply chainsoftware particularlyaddressing the needs of themotor carrier industry.

Revenues: $m2013 9622012 8552011 532

Revenue CAGR: 2011-2013 29%

EBIT: $m2013 49 2012 40 2011 (26)

EBIT CAGR:2011-2013 -

Revenue breakdown(2013):Systems 42%Services 58%

Geographical breakdown(2013):Americas 84%EMEA 11%APAC 5%

Workforce:4,600

Recent M&A activity:Acquired Solarsoft BusinessSystems, an MES and ERPsoftware vendor.

EpicorUS

Epicor has more than 20,000customers in over 150countries. Epicor SCMcapabilities are built within asingle business platform, basedon a service-orientedarchitecture. Its SCM productfeatures purchase management,sourcing and procurement,inventory management,advanced material managementand warehouse management,which is complemented by theorder and demand managementcapabilities of Epicor SalesManagement.

Revenues: $m2012 -2011 6912010 594

Revenue CAGR: 2011-2013 -

EBIT: $m2012 - 2011 128 2010 64

EBIT CAGR:2011-2013 -

Revenue breakdown(2013):Supply Chain 96%Pricing and RevenueManagement 4%

Geographical breakdown(2013):US 64%EMEA 20%APAC 16%

Workforce:3,100

Recent M&A activity:Acquired OmegaOptimization, a logisticsmanagement softwareprovider.

JDAUS

JDA's supply chainmanagement, merchandising,and pricing excellence solutionsare used by more than 2,700companies worldwide. Mergedwith JDA in 2012, RedPrairie'ssupply chain, workforce, and all-channel retail solutions areinstalled in over 60,000customer sites across morethan 50 countries.

Revenues: $m2013 6722012 6202011 582

Revenue CAGR: 2011-2013 7%

EBIT: $m2013 47 2012 30 2011 48

EBIT CAGR:2011-2013 0%

Revenue breakdown(2013):Contracts 40%Services and other 31%Products 15%SaaS and Subscription 14%

Geographical breakdown(2013):Netherlands 30%UK 17%US 6%Rest of Europe and other 47%

Workforce:4,300

Recent M&A activity:The company was recentlyacquired by AdventInternational for $1.2bn.

Unit4Netherlands

Unit4 has operations in 17European countries and inseven countries across NorthAmerica, Asia Pacific andAfrica. It serves retail, travel,education, financial services,not-for-profit, professionalservices, government,transportation, and logisticscustomers.

GLOBAL SCM SOFTWARE MARKET R EPORT 2 0 1 422

Revenues: $m2013 1512012 1272011 114

Revenue CAGR: 2011-2013 15%

EBIT: $m2013 21 2012 20 2011 15

EBIT CAGR:2011-2013 18%

Revenue breakdown(2013):Services 91%Licenses 9%

Geographical breakdown(2013):US 46%EMEA 42%Canada 9%APAC 3%

Workforce:800

Recent M&A activity:Acquired Impatex FreightSoftware, a TMS and WMSprovider.

Acquired KSD SoftwareNorway, a TMS provider.

Acquired Exentra TransportSolutions, a provider of drivercompliance solutions for theEU.

DescartesUS

The Descartes SystemsGroup has more than 10,000customers in 60 countries.The company serves globaltrade and transportationorganisations with its LogisticsTechnology Platform, whichcombines an extensive multi-modal transport networkwith its array of modular andinteroperable web andwireless logistics applications.

Revenues: $m2013 812012 942011 98

Revenue CAGR: 2011-2013 -9%

EBIT: $m2013 10 2012 (3)2011 6

EBIT CAGR:2011-2013 28%

Revenue breakdown(2012):Transportation and Logistics 43%Customs and Freight Forwarding 42%E-commerce and B2B Integration 15%

Geographical breakdown(2012):Europe 62%Americas 30%Asia 8%

Workforce:607

Recent M&A activity:Acquired FourSoft, an IndianTMS provider.

KewillUK

Kewill focuses its business onthree product suites - logistics,transportation & shipping andB2B integration. Kewill's MOVEplatform supports supply chainexecution activities for morethan 7,500 companies in morethan 100 countries.

KNOWYOURERP FROMYOUR SCM?

WWW.CLEARWATERINTERNATIONAL.COM/NEWS

READ OUR LATEST VIEWS ON TECHNOLOGYAND M&A IN THE TMT SECTOR AT OURREGULAR BLOG:

Provider of environmental,health & safety and quality &loss prevention software

Clearwater International advised onthe acquisition by Kennet Partnersand Fidelity Growth Partners Europe

Rivo Software

Corporate internet servicesprovider

Clearwater International advisedGriffin on its acquisition by MDNX

Griffin (Octium Ltd)

Leading UK-based provider ofSaaS drive compliancesolutions

Clearwater International advised the business on its sale to Descartes Systems

Providers of development,maintenance and support forintegrated software solutions

Clearwater International advisedCelenia Software in the divestiture ofthe DTI division to Vaekst Invest anda group of investors

DTI, Celenia Software

Software solutions developerfor critical operationalfunctions in complex industries

Clearwater International advised onthe sale of one shareholder’s staketo the shareholders of CriticalGroup

Critical Software

Providers of computer basedinventory management systems

Clearwater International advised onthe sale of BV Electronic to ViaVenture Partners

BV Electronic A/S

Hosting and outsource IT company

Clearwater International advised ViaVentures Partners on theiracquisition of the holding interest inthis company

Hostnordic

Provider of business criticaldata infrastructure to over 500UK companies

Clearwater International advised theshareholders on the multi-millionpound sale to LDC

Metronet

Market leading SaaS provider ofback-office hospitality systems

Clearwater International advised ECIPartners on the acquisition of FourthHospitality

Fourth Hospitality

Spanish privately owned opticalfibre cable manufacturer

Clearwater International advised onthe placement of debt

Optral

Largest Nordic supplier oftechnical software solutions

Clearwater International advised onthe sale of the group to a number offinancial investors

PLM Group

Leading provider of cloud basedIT and network services to theSME sector

Clearwater International advisedSynova Capital on the debtrefinancing of the business

Cloud XL

Exentra

A CLEARWATER INTERNAT IONAL TMT TEAM REPORT 23

W W W. C L E A RWAT E R I N T E R N AT I O N A L . C O M

AARHUS • BARCELONA • BEIJING • BIRMINGHAM • COPENHAGEN • LISBONLONDON • MADRID • MANCHESTER • NOTTINGHAM • PORTO • SHANGHAI