Global Liquids Supply Outlook - Peak Watch

35

Strategic Advisors in Global Energy Global Liquids Supply Outlook Bob MacKnight Includes: OPEC and Non-OPEC Conventional, Tar Sands, Biofuels, and Others 26 March 2008

Transcript of Global Liquids Supply Outlook - Peak Watch

Strategic Advisors in Global Energy

Global Liquids Supply Outlook

Bob MacKnight

Includes: OPEC and Non-OPEC Conventional, Tar Sands, Biofuels, and Others

26 March 2008

Global Liquids Supply Outlook | Upstream Group | Page 2

0

20,000

40,000

60,000

80,000

100,000

120,00019

95

2000

2005

2010

2015

2020

Dai

ly P

rodu

ctio

n (m

b/d)

0

20,000

40,000

60,000

80,000

100,000

120,000

Non-OPEC Crude Non-OPEC Oil SandsNon-OPEC NGL & Condensate OPEC NGL1.1% Growth 1.7% Growth2.4% Growth

37-45 mmb/d46-58 mmb/d

Call on OPEC Crude

OPEC 33-36 mmb/d

The Dilemma - The Expected Growing Gap Between Global Demand and Global Non-OPEC Supply in the Next Decade

Global Liquids Supply Outlook | Upstream Group | Page 3

1965 1970 1975 1980 1985 1990 1995 2000 2005

USA RomaniaTunisiaPeru

Dem Rep CongoCameroon

Other EuropeEgypt

PakistanPapua New Guinea

SyriaUK

GabonUzbekistan

NorwayOman

New ZealandArgentina

CongoColombiaAustraliaYemen

DenmarkMexicoChad

CanadaBrunei

MalaysiaIndiaChina

Turkmenistan

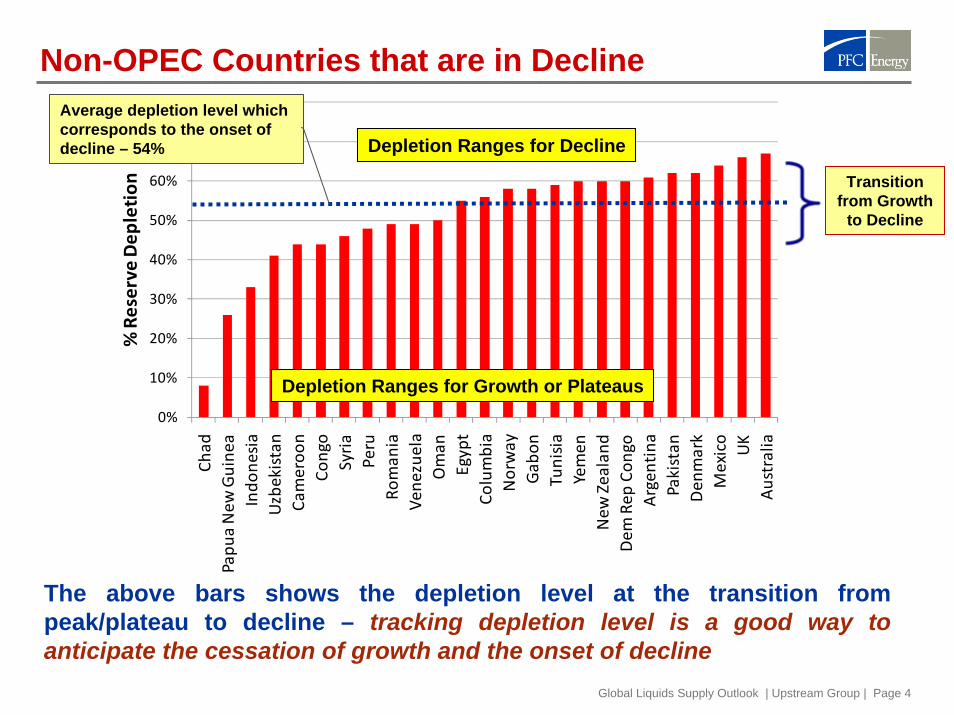

The above bars show the onset and duration of documented production peaks or plateaus – tracking country life cycle shows an acceleration of the number of countries passing from peak to decline

Countries in the decline phase

Countries in the plateau phase

Onset of Plateau

Duration of Plateau

Onset of Decline

Non-OPEC Countries in Decline or in Plateau

Global Liquids Supply Outlook | Upstream Group | Page 4

0%

10%

20%

30%

40%

50%

60%

70%

80%

Chad

Papu

a New

Guine

aIndo

nesia

Uzbekistan

Cameroo

nCo

ngo

Syria

Peru

Roman

iaVe

nezuela

Oman

Egypt

Columbia

Norway

Gab

onTunisia

Yemen

New

Zealand

Dem

Rep

Con

goArgen

tina

Pakistan

Den

mark

Mexico

UK

Australia

% Reserve

Dep

letion

The above bars shows the depletion level at the transition from peak/plateau to decline – tracking depletion level is a good way to anticipate the cessation of growth and the onset of decline

Depletion Ranges for Decline

Depletion Ranges for Growth or Plateaus

Transition from Growth

to Decline

Average depletion level which corresponds to the onset of decline – 54%

Non-OPEC Countries that are in Decline

Global Liquids Supply Outlook | Upstream Group | Page 5

0%

10%

20%

30%

40%

50%

60%

70%

80%

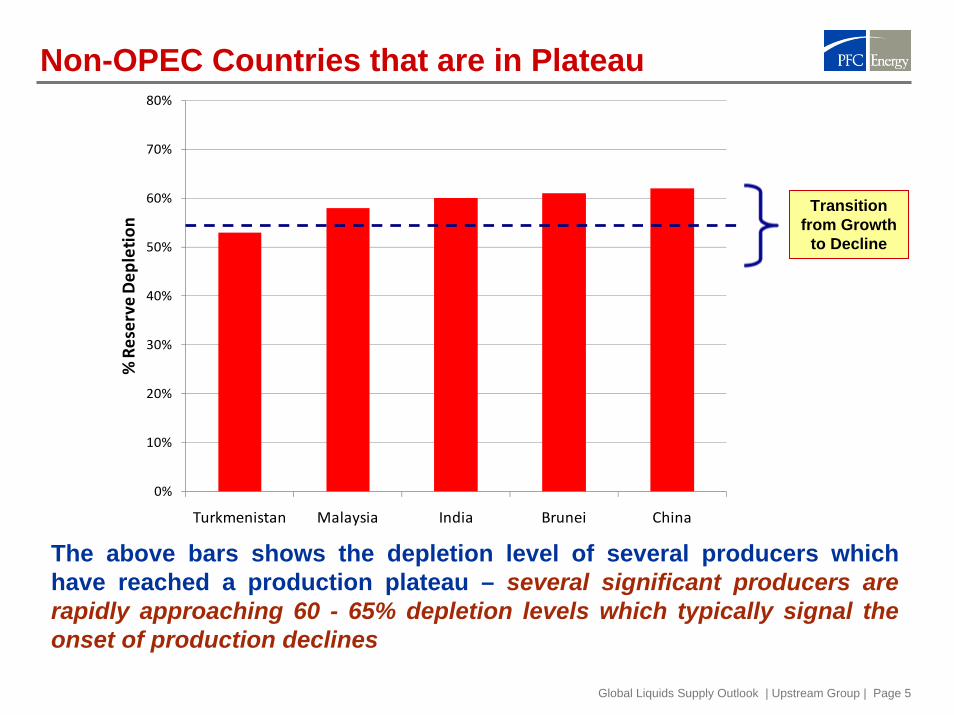

Turkmenistan Malaysia India Brunei China

% Reserve

Dep

letion

The above bars shows the depletion level of several producers which have reached a production plateau – several significant producers are rapidly approaching 60 - 65% depletion levels which typically signal the onset of production declines

Transition from Growth

to Decline

Non-OPEC Countries that are in Plateau

Global Liquids Supply Outlook | Upstream Group | Page 6

0%

10%

20%

30%

40%

50%

60%

70%

80%

% Reserve

Dep

letion

The above bars shows the depletion level of several producers, which have new discoveries and are considered very likely to increase production.

Transition from Growth

to Decline

Non-OPEC Countries with Production Growth

Global Liquids Supply Outlook | Upstream Group | Page 7

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

1965

1970

1975

1980

1985

1990

1995

2000

2005

2010

2015

2020

Dai

ly C

rude

Pro

duct

ion

(mb/

d)Global: Non-OPEC, Non-FSU, Non-Unconventional Crude

Supply Forecast (with Exploration)

P10e Forecast

P25e Forecast

P50e Forecast

P75e Forecast

P90e Forecast

PFC Energy’s models suggest that production has declined but reserve addition from exploration will keep production level above 25,000 million barrels per day until the middle of the next decade.

Possible production path if exploration results and decline rates fall at the more pessimistic end of the scale

Possible production path if exploration results and decline rates fall at the more optimistic end of the scale

Non-OPEC Crude Oil Forecast with Exploration (excluding NGLs, FSU, and Uncon. Heavy Oil)

Global Liquids Supply Outlook | Upstream Group | Page 8

FSU / Eastern Europe Crude Oil Production Forecast

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

1985

1990

1995

2000

2005

2010

2015

2020

2025

2030

Dai

ly C

rude

Pro

duct

ion

(mb/

d)FSU/ Eastern Europe Crude Supply Forecast (With Exploration)

P10e ForecastP25e ForecastP50e ForecastP75e ForecastP90e Forecast

When potential production from future exploration reserves is incorporated with current P1 and P2 reserves, total crude oil production is expected to peak within a range of 14,000 to 15,000 mb/d by the middle of the next decade.

Global Liquids Supply Outlook | Upstream Group | Page 9

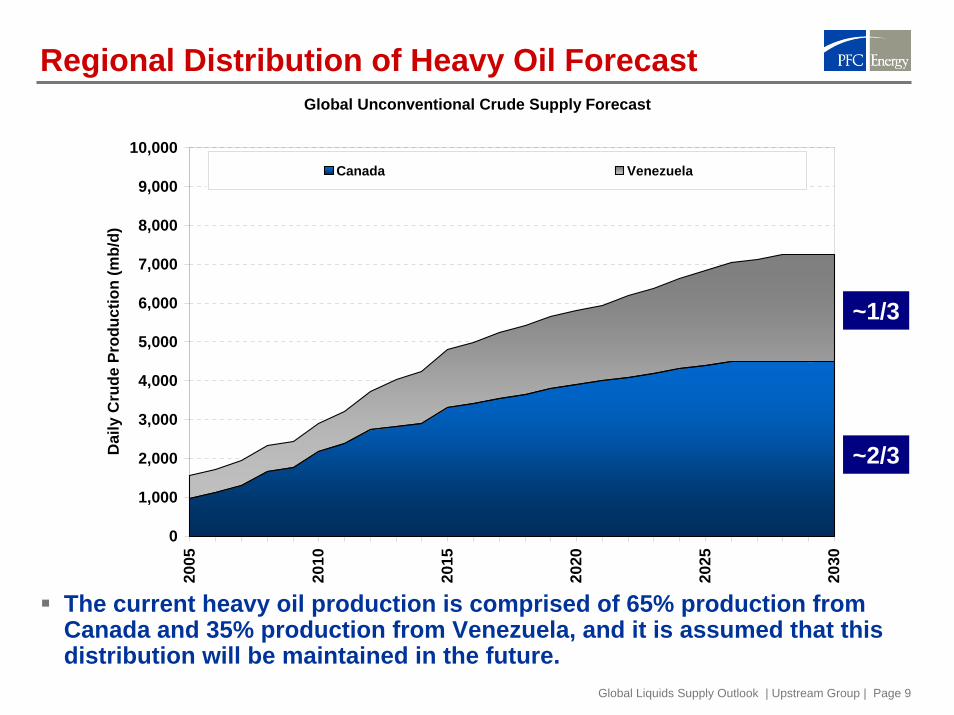

Regional Distribution of Heavy Oil Forecast

The current heavy oil production is comprised of 65% production from Canada and 35% production from Venezuela, and it is assumed that this distribution will be maintained in the future.

Global Unconventional Crude Supply Forecast

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

2005

2010

2015

2020

2025

2030

Dai

ly C

rude

Pro

duct

ion

(mb/

d)

Canada Venezuela

~2/3

~1/3

Global Liquids Supply Outlook | Upstream Group | Page 10

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

1985

1990

1995

2000

2005

2010

2015

2020

Dai

ly C

rude

Pro

duct

ion

(mb/

d)Global Non-OPEC Liquid Supply Forecast

(With Exploration)

P10e Forecast

P25e Forecast

P50e Forecast

P75e Forecast

P90e Forecast

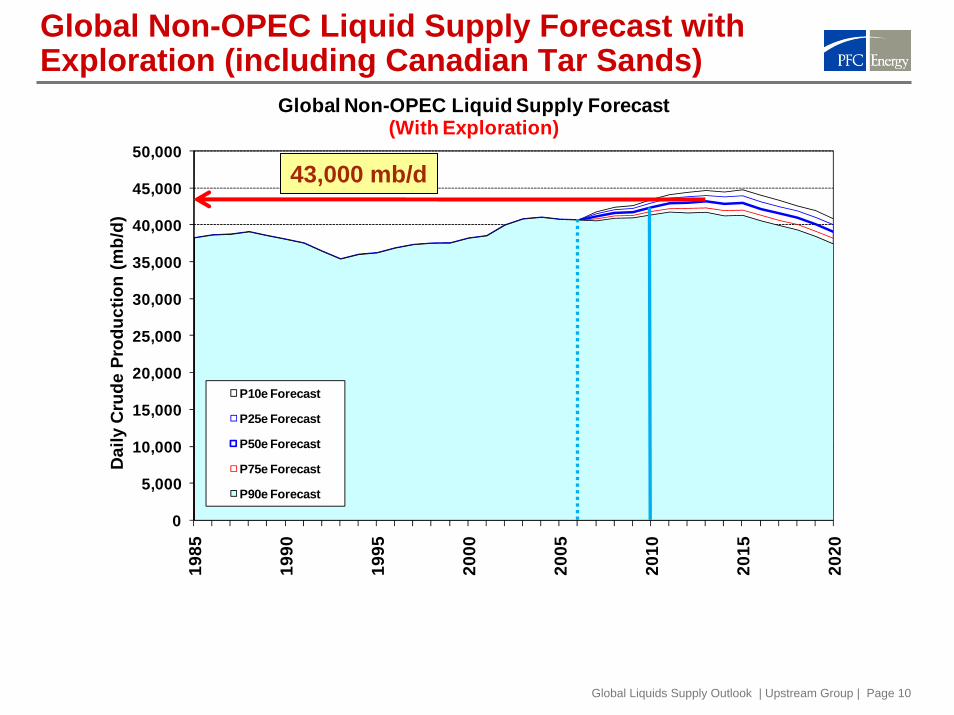

43,000 mb/d

Global Non-OPEC Liquid Supply Forecast with Exploration (including Canadian Tar Sands)

Global Liquids Supply Outlook | Upstream Group | Page 11

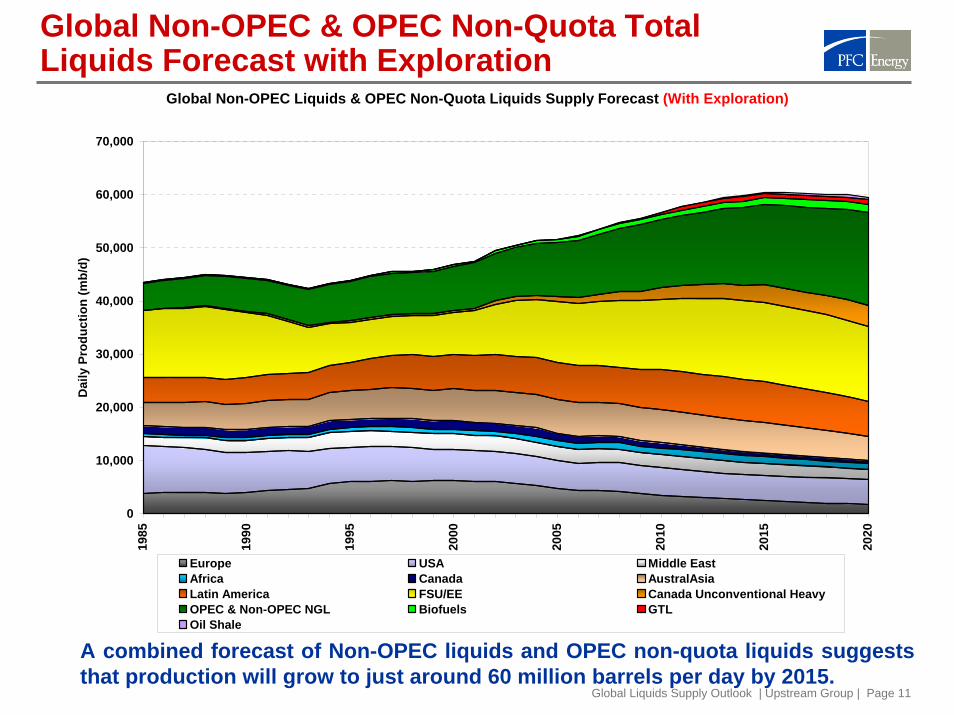

Global Non-OPEC Liquids & OPEC Non-Quota Liquids Supply Forecast (With Exploration)

0

10,000

20,000

30,000

40,000

50,000

60,000

70,00019

85

1990

1995

2000

2005

2010

2015

2020

Dai

ly P

rodu

ctio

n (m

b/d)

Europe USA Middle EastAfrica Canada AustralAsiaLatin America FSU/EE Canada Unconventional HeavyOPEC & Non-OPEC NGL Biofuels GTLOil Shale

Global Non-OPEC & OPEC Non-Quota Total Liquids Forecast with Exploration

A combined forecast of Non-OPEC liquids and OPEC non-quota liquids suggests that production will grow to just around 60 million barrels per day by 2015.

Global Liquids Supply Outlook | Upstream Group | Page 12

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

1985

1990

1995

2000

2005

2010

2015

2020

Dai

ly C

rude

Pro

duct

ion

(mb/

d)Global Non-OPEC Liquid and OPEC Non-Quota Liquid Supply Forecast

(With Exploration)

P10e Forecast

P25e Forecast

P50e Forecast

P75e Forecast

P90e Forecast

A combined forecast of Non-OPEC crude, Non-OPEC NGLs, and OPEC Non-Quota NGLs suggests that, with exploration success, production will reach 60 million barrels per day with declines beginning towards the end of the next decade.

60,000 mb/d

Global Non-OPEC Liquid & OPEC Non-Quota Liquid Supply Forecast with Exploration

Global Liquids Supply Outlook | Upstream Group | Page 13

0

10,000

20,000

30,000

40,000

50,000

60,000

Wes

t Afr

ica

Latin

Am

eric

a

Non

-OPE

CN

orth

Afr

ica

/M

iddl

e Ea

st

Aus

tral

Asi

a

Wes

tern

Euro

pe

FSU

/Ea

ster

nEu

rope

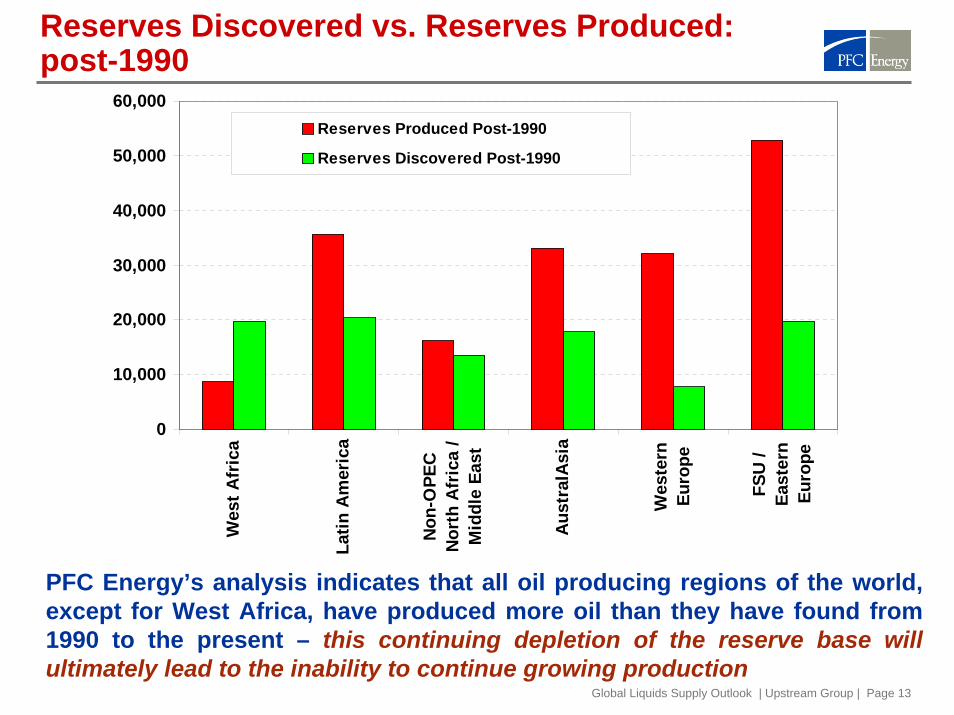

Reserves Produced Post-1990

Reserves Discovered Post-1990

PFC Energy’s analysis indicates that all oil producing regions of the world, except for West Africa, have produced more oil than they have found from 1990 to the present – this continuing depletion of the reserve base will ultimately lead to the inability to continue growing production

Reserves Discovered vs. Reserves Produced: post-1990

Global Liquids Supply Outlook | Upstream Group | Page 14

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

1951-1960 1961-1970 1971-1980 1981-1990 1991-2005

Ave

rage

Ann

ual R

eser

ves

Dis

cove

red

(mm

bo)

In order to stabilize the depletion of Non – OPEC reserves we would need to start offsetting every barrel produced with a new barrel found (either through discovery or enhanced recovery) – given current and projected levels of consumption that means we would have to return to success levels typical of the period prior to 1980

Reserves Discovered Outside of North America

Average Annual Reserve Additions Decline Every Decade, yet Demand Increases Every Decade

Global Liquids Supply Outlook | Upstream Group | Page 15

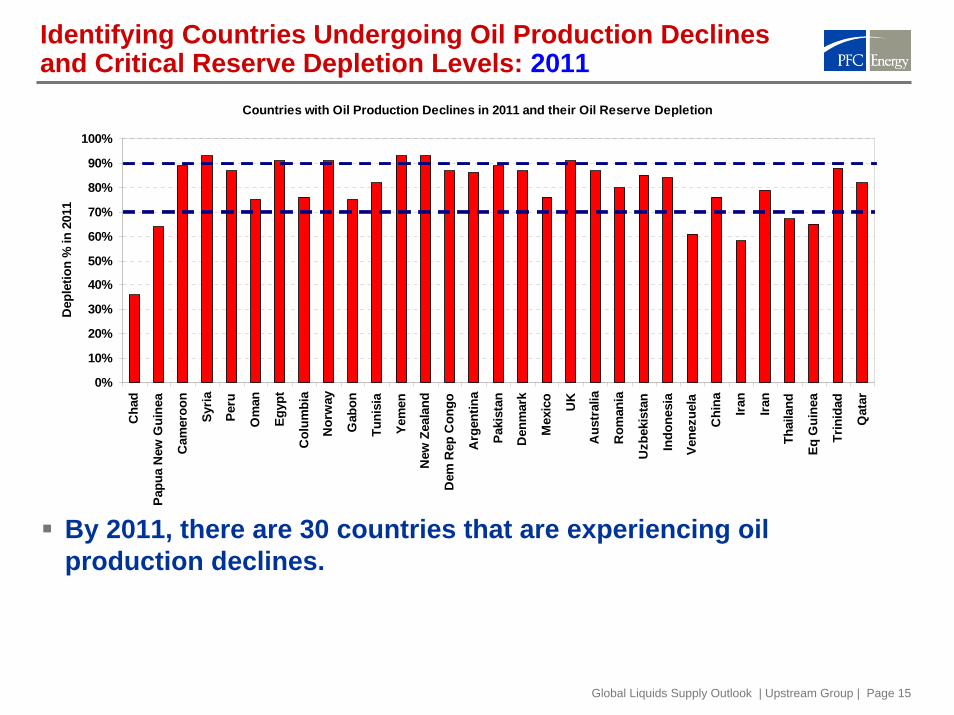

Identifying Countries Undergoing Oil Production Declines and Critical Reserve Depletion Levels: 2011

Countries with Oil Production Declines in 2011 and their Oil Reserve Depletion

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%C

had

Papu

a N

ew G

uine

a

Cam

eroo

n

Syria

Peru

Om

an

Egyp

t

Col

umbi

a

Nor

way

Gab

on

Tuni

sia

Yem

en

New

Zea

land

Dem

Rep

Con

go

Arg

entin

a

Paki

stan

Den

mar

k

Mex

ico

UK

Aus

tral

ia

Rom

ania

Uzb

ekis

tan

Indo

nesi

a

Vene

zuel

a

Chi

na Iran

Iran

Thai

land

Eq G

uine

a

Trin

idad

Qat

ar

Dep

letio

n %

in 2

011

By 2011, there are 30 countries that are experiencing oil production declines.

Global Liquids Supply Outlook | Upstream Group | Page 16

Countries Experiencing Oil Production Growth in 2011

Countries in Oil Production Growth: 2011

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Congo

Iraq

Maurita

nia

Brazil

Angola

VietnamEcua

dorAze

rbaij

anKaza

khstan

Russia

LibyaNige

riaSaudi A

rabia

United A

rab Emira

tes

Res

erve

Dep

letio

n %

In 2011, there are only 14 countries that have a sufficient oil reserve base to support production growth.

Global Liquids Supply Outlook | Upstream Group | Page 17

OPEC OutlookReserves and Production ForecastSaudi Arabia and Kuwait Crude Reserve Views

Global Liquids Supply Outlook | Upstream Group | Page 18

Concerns With OPEC Reserves

1. The Gulf members on the OPEC Group substantially increased theirofficially reported remaining reserve number during the early 1980s during the competition for OPEC quotas.

2. Since the mid 1980s OPEC countries in the Gulf has essentially kept their officially reported remaining reserve flat, despite the fact that all data bases and their own reporting indicate minor reserve additions through exploration.

3. OPEC keeps their remaining reserve numbers flat by arguing that for every barrel they produce they are able to offset this by adding a barrel through adjustments to reservoir parameters (porosity, water saturation, recovery factor, net to gross ratio, etc.).

4. When we track reserve additions through exploration and the depletion of those reserve through production, we see a much lower remaining reserve number than what is reported by OPEC.

Global Liquids Supply Outlook | Upstream Group | Page 19

Concerns With OPEC Reserves

5. The real issue here is that we really do not know what several key OPEC countries reserves really are because there is no way to independently verify them as we can in most non-OPEC countries where you have foreign companies doing the exploration and development.

6. The shape and style of these country’s remaining reserve profiles in the face of disappointing exploration results over the last 20 years and the fact that they almost exactly offset production with reserves through book keeping has to raise suspicions.

7. Our analysis suggests that OPEC overall has depleted approximately 40 percent of its reserve base with annual depletion levels running at 1 %/year (OPEC would argue that it is their policy to have 0% depletion) ….. If PFC’s estimated rate of depletion is correct then OPEC will reach the critical level of 60% in the later part of the next decade.

Global Liquids Supply Outlook | Upstream Group | Page 20

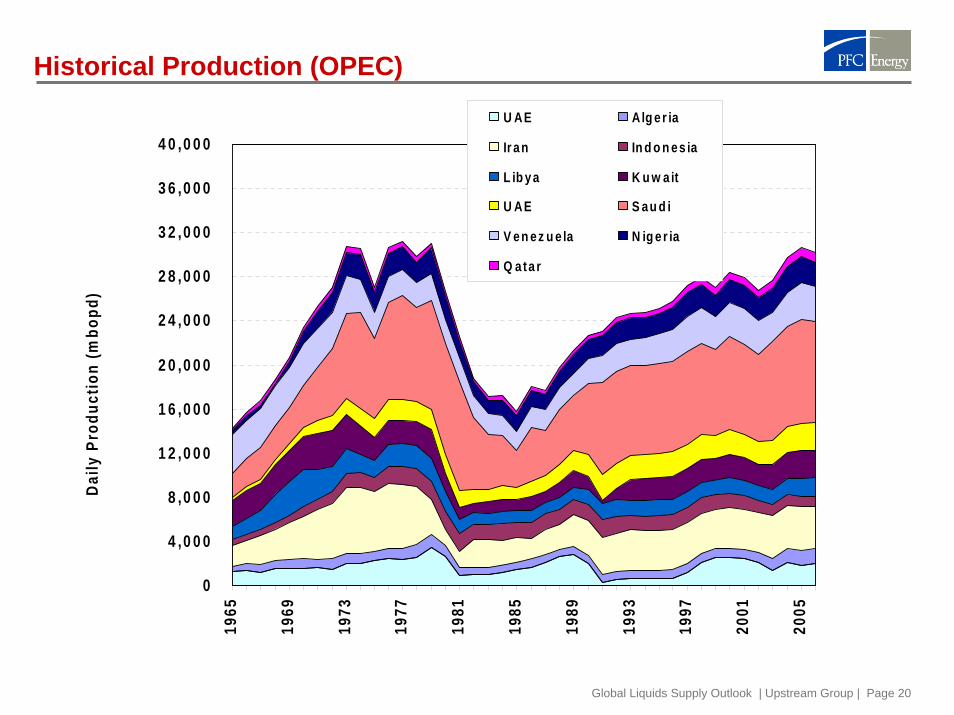

Historical Production (OPEC)

0

4 ,0 0 0

8 ,0 0 0

1 2 ,0 0 0

1 6 ,0 0 0

2 0 ,0 0 0

2 4 ,0 0 0

2 8 ,0 0 0

3 2 ,0 0 0

3 6 ,0 0 0

4 0 ,0 0 0

1965

1969

1973

1977

1981

1985

1989

1993

1997

2001

2005

Dai

ly P

rodu

ctio

n (m

bopd

)U AE Alg e r ia

Ir a n In d o n es ia

L ib y a K u w a it

U AE S au d i

V e n ez u e la N ig e r ia

Q ata r

Global Liquids Supply Outlook | Upstream Group | Page 21

OPEC Creaming Curve

C u m u la t iv e R e s e rv e s (m m b o )

0

2 0 0 ,0 0 0

4 0 0 ,0 0 0

6 0 0 ,0 0 0

8 0 0 ,0 0 0

1 ,0 0 0 ,0 0 0

1 ,2 0 0 ,0 0 0

1950

1954

1958

1962

1966

1970

1974

1978

1982

1986

1990

1994

1998

2002

2006

Cum

ulat

ive

Res

erve

s (m

mbo

)

Global Liquids Supply Outlook | Upstream Group | Page 22

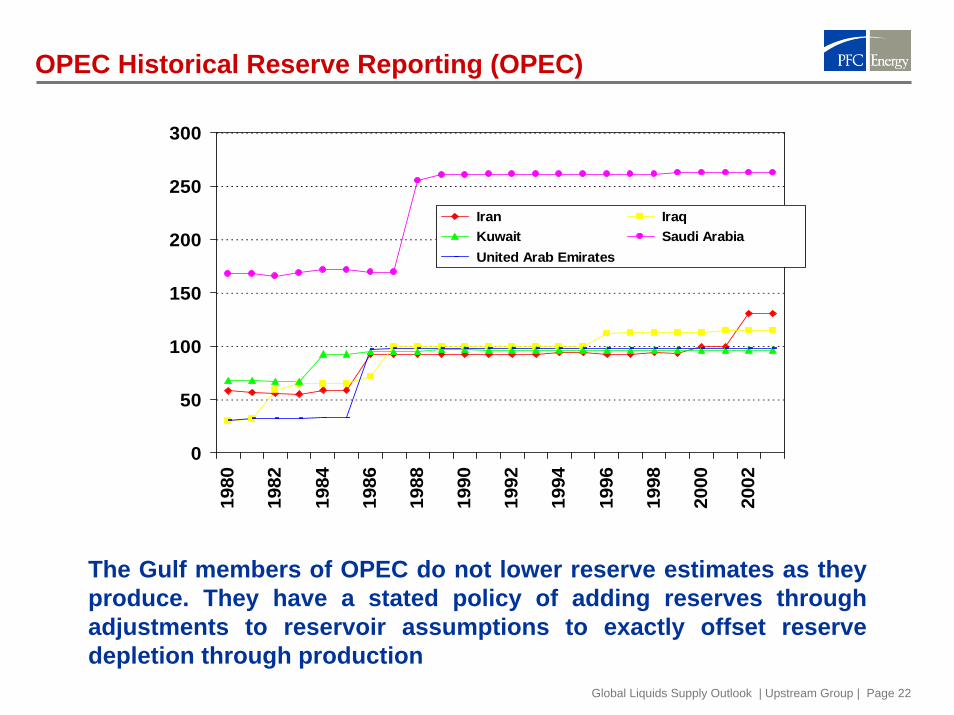

OPEC Historical Reserve Reporting (OPEC)

The Gulf members of OPEC do not lower reserve estimates as they produce. They have a stated policy of adding reserves through adjustments to reservoir assumptions to exactly offset reserve depletion through production

0

50

100

150

200

250

300

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

Iran Iraq Kuwait Saudi Arabia United Arab Emirates

Global Liquids Supply Outlook | Upstream Group | Page 23

OPEC Historical Annual Crude Production Balance (OPEC)

Like all other areas of the world, PFC Energy’s data analysis indicates that Global OPEC crude production is currently exceeding volumes discovered.

C h a r t T it le

-1 0 ,0 0 0

-8 ,0 0 0

-6 ,0 0 0

-4 ,0 0 0

-2 ,0 0 0

0

2 ,0 0 0

4 ,0 0 0

6 ,0 0 0

8 ,0 0 0

1 0 ,0 0 0

1965

1970

1975

1980

1985

1990

1995

2000

2005

Diff

eren

tial B

etw

een

Ann

ual V

olum

es P

rodu

ced

and

Ann

ual V

loum

es D

isco

vere

d (m

mbo

)

An n u a l R e s e r v e s D is c o v e r e d - An n u a l R e s e r v e s P r o d u c e d3 p e r . M o v . Av g . (An n u a l R e s e r v e s D is c o v e r e d - An n u a l R e s e r v e s P r o d u c e d )

Global Liquids Supply Outlook | Upstream Group | Page 24

Historical Saudi Reserve Additions

This is a creaming curve for Saudi. This is a view of reserve addition history over time based on the currently reported P1 and P2 reserves for all fields. For example, the fields discovered as of 1960 in aggregate had reserves of just over 200 billion barrels (as reserves are reported today).

0

3 5 ,0 0 0

7 0 ,0 0 0

1 0 5 ,0 0 0

1 4 0 ,0 0 0

1 7 5 ,0 0 0

2 1 0 ,0 0 0

2 4 5 ,0 0 0

2 8 0 ,0 0 0

3 1 5 ,0 0 0

3 5 0 ,0 0 0

1950

1955

1960

1965

1970

1975

1980

1985

1990

1995

2000

2005

Cum

ulat

ive

Res

erve

s (m

mbo

)

C u m u la t iv e R e s e rv e s

Global Liquids Supply Outlook | Upstream Group | Page 25

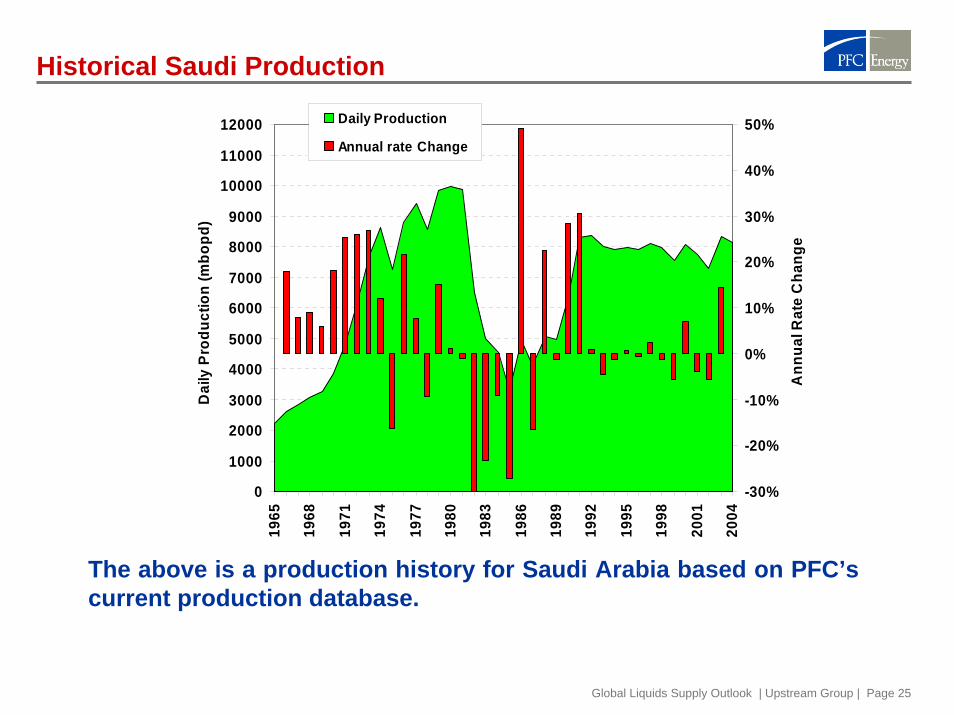

Historical Saudi Production

The above is a production history for Saudi Arabia based on PFC’s current production database.

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

10000

11000

12000

1965

1968

1971

1974

1977

1980

1983

1986

1989

1992

1995

1998

2001

2004

Dai

ly P

rodu

ctio

n (m

bopd

)

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

Ann

ual R

ate

Cha

nge

Daily Production

Annual rate Change

Global Liquids Supply Outlook | Upstream Group | Page 26

0

5 0 ,0 0 0

1 0 0 ,0 0 0

1 5 0 ,0 0 0

2 0 0 ,0 0 0

2 5 0 ,0 0 0

3 0 0 ,0 0 0

3 5 0 ,0 0 0

1965

1970

1975

1980

1985

1990

1995

2000

2005

Res

erve

s (m

mbo

)

P r o d u ced R es er v e V o lu m e

R em ain in g R es er ve V o lu m e

O ffic ia l O P E C R em a in in g R es er v e

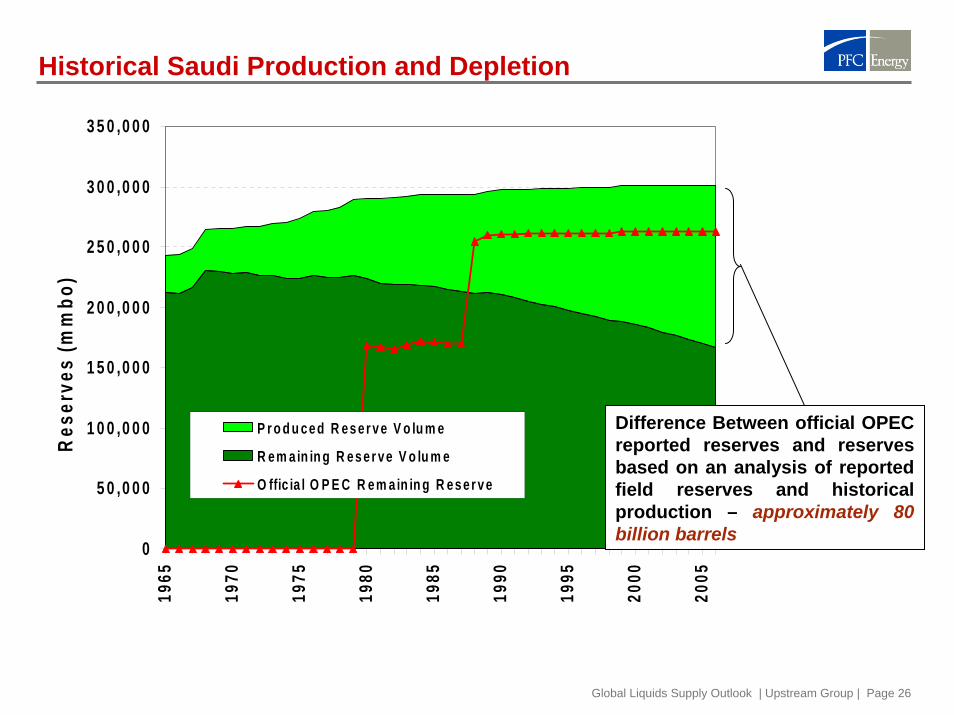

Historical Saudi Production and Depletion

Difference Between official OPEC reported reserves and reserves based on an analysis of reported field reserves and historical production – approximately 80 billion barrels

Global Liquids Supply Outlook | Upstream Group | Page 27

Historical Kuwaiti Production

The above is a production history for Kuwait based on PFC’s current production database.

0

4 0 0

8 0 0

1 ,2 0 0

1 ,6 0 0

2 ,0 0 0

2 ,4 0 0

2 ,8 0 0

3 ,2 0 0

3 ,6 0 0

4 ,0 0 0

1965

1970

1975

1980

1985

1990

1995

2000

2005

Dai

ly P

rodu

ctio

n (m

bopd

)

- 2 0 0 0

-1 6 0 0

-1 2 0 0

-8 0 0

-4 0 0

0

4 0 0

8 0 0

1 2 0 0

1 6 0 0

2 0 0 0

Prod

uctio

n - R

eser

ves

Add

ed

D a ily P ro d u c tio n C u m P ro d u c tio n /C u m R e s e rv e s

Global Liquids Supply Outlook | Upstream Group | Page 28

0

1 0 ,0 0 0

2 0 ,0 0 0

3 0 ,0 0 0

4 0 ,0 0 0

5 0 ,0 0 0

6 0 ,0 0 0

7 0 ,0 0 0

8 0 ,0 0 0

9 0 ,0 0 0

1 0 0 ,0 0 0

1 1 0 ,0 0 019

65

1970

1975

1980

1985

1990

1995

2000

2005

Res

erve

s (m

mbo

)

P r o d u c e d R e s e r ve s

R e m a in in g R e se r v e

O P E C R e p o r te d R e m a in in g R e s e r ve

Historical Kuwaiti Production and Depletion

Difference Between official OPEC reported reserves and reserves based on an analysis of reported field reserves and historical production – approximately 45 billion barrels

Global Liquids Supply Outlook | Upstream Group | Page 29

0 %1 0 %2 0 %3 0 %4 0 %5 0 %6 0 %7 0 %8 0 %9 0 %

1 0 0 %

Iraq

U AEA n g o laK uw ai t

L ib yaS a u d i

A lg e r iaN ig e r ia Ira

nV e n e z u e la Q a ta r

In d o n es iaR

eser

ve B

ase

Dep

letio

n (%

)

Historical Production and Depletion Levels (OPEC)

In Decline

Conventional Oil Production has been declining for several years calling into question currently

reported reserves

At or Near Plateau

OPEC as a whole is depleting but some countries are depleting faster than others

Global Liquids Supply Outlook | Upstream Group | Page 30

Historical Production and Depletion Levels (OPEC)

Based on our analysis OPEC as a whole has produced approximately 45 percent of all reserves discovered in OPEC to date. Understanding whether or not this is correct is critical in understanding what future world production capacity will be.

0

4 ,0 0 0

8 ,0 0 0

1 2 ,0 0 0

1 6 ,0 0 0

2 0 ,0 0 0

2 4 ,0 0 0

2 8 ,0 0 0

3 2 ,0 0 0

3 6 ,0 0 0

4 0 ,0 0 0

1965

1969

1973

1977

1981

1985

1989

1993

1997

2001

2005

Dai

ly P

rodu

ctio

n (m

bopd

)

0 %

1 0 %

2 0 %

3 0 %

4 0 %

5 0 %

6 0 %

7 0 %

8 0 %

9 0 %

1 0 0 %

Cum

Pro

d/C

um R

eser

ves

D a ily P r o d u c t io n

C u m P r o d u c t io n /C u m R e ser ve s

Global Liquids Supply Outlook | Upstream Group | Page 31

Unconstrained OPEC Production Will Peak Under 100 Million Barrels Per Day

The Growing Differential Between Non-OPEC Supply Capacity and

Global Demand

0

2 0 ,0 0 0

4 0 ,0 0 0

6 0 ,0 0 0

8 0 ,0 0 0

1 0 0 ,0 0 0

1 2 0 ,0 0 0

1995

2000

2005

2010

2015

2020

Dai

ly P

rodu

ctio

n (m

b/d)

0

2 0 ,0 0 0

4 0 ,0 0 0

6 0 ,0 0 0

8 0 ,0 0 0

1 0 0 ,0 0 0

1 2 0 ,0 0 0

N o n -O P E C C r u d e N o n -O P E C N G L & C o n d e n s a te

N o n -O P E C O il S a n d s O P E C N G L

O P E C C r u d e 1 .7 % G r o w th

2 .4 % G r o w th 1 .1 % G r o w th

Global Liquids Supply Outlook | Upstream Group | Page 32

1. In spite of high oil prices, Non-OPEC production growth has been very limited with the exception of the FSU. This trend is likely to continue through this decade.

2. Oil exploration in the last 10 years (with a few exceptions likeAngola, Sudan, Mauritania, Brazil) has been much less successfulthan in previous decades. Since 1990 reserve replacement in non-OPEC countries of most regions has been less that 35 percent.

3. Every year, in every region (including OPEC), the world producesmore oil than it finds. It is only logical to conclude that inevitably this will lead to dwindling supplies. Our current view is that absent significant improvements in recovery technologies, exploration results, or a sharp increase in exploration spending, global non-OPEC liquid hydrocarbon production rate will struggle to grow beyond 2010 and may in fact start to decline.

Given a continuation of recent trends in exploration results (field sizes, success rates, etc. and recovery factors):

Key Messages

Global Liquids Supply Outlook | Upstream Group | Page 33

4. Non-OPEC production growth between now and the end of this decade will rely heavily on production growth in Kazakhstan, Azerbaijan, Russia, Brazil, and several miscellaneous smaller producers. The real unknown here is to what degree production from these countries will fill and exceed the void left by production declines in other Non – OPEC countries.

5. If demand continues to grow beyond 2010 and if Non-OPEC production capacity plateaus or falls, OPEC will have to make up the difference resulting in an inevitable increase in dependency on OPEC sources.

Key Messages

Strategic Advisors in Global Energy

PFC Energy consultants are present in the following locations:

Bahrain

Beijing

Buenos Aires

Calgary

Houston

Kuala Lumpur

Lausanne

London

Mumbai

New York

Paris

San Francisco

Washington, D.C.

Main regional offices:

Asia

PFC Energy, Kuala LumpurLevel 27, UBN Tower #2110 Jalan P. Ramlee50250 Kuala Lumpur, MalaysiaTel (60 3) 2172-3400Fax (60 3) 2072-3599

North America

PFC Energy, Washington D.C.1300 Connecticut Avenue, N.W. Suite 800Washington, D.C. 20036, USATel (1 202) 872-1199 Fax (1 202) 872-1219

PFC Energy, Houston4545 Post Oak Place, Suite 312 Houston, Texas 77027-3110, USA Tel (1 713) 622-4447 Fax (1 713) 622-4448

Europe

PFC Energy, France19 rue du Général Foy75008 Paris, France Tel (33 1) 4770-2900Fax (33 1) 4770-5905

PFC Energy International, Lausanne19, Boulevard de la Forêt1009 Pully, Switzerland Tel (41 21) 721-1440Fax: (41 21) 721-1444

Middle East

PFC Energy, BahrainManama Center Entrance 4 - Office 705 Kingdom of BahrainTel (973) 1721-5106 Fax (973) 1721-5108

www.pfcenergy.com | [email protected] regional offices are shown in blue.

Global Liquids Supply Outlook | Upstream Group | Page 35

• For each country reserve additions (field by field) have been documented along with production history

• A decline is modeled for the producing base using current withdrawal rates and remaining reserve estimates for fields in the existing production base (an additional 15-20% volume has been added to the current estimates of P1+P2 to account for possible higher recoveries)

• All new discoveries with a development plan are documented and probabilistically modeled to add to the producing base

• All undeveloped discoveries without a development plan are modeled using country average peak rates, decline rates, development concepts, etc. and added to the producing base

• Probabilistic expected value models are built which assume that field sizes, success rates, etc. (documented since 1990) continue over the next two decades and production from these EVA models are modeled to be added to the producing base

Methodology