Global Head of AXA Global L&S CEO for Northern, … · AXA Jacques de Vaucleroy Global Head of AXA...

23

AXA Jacques de Vaucleroy Global Head of AXA Global L&S CEO for Northern, Central and Eastern Europe region Member of the AXA Management Committee October 2, 2014 Bank of America Merrill Lynch Annual Banking & Insurance CEO Conference 2014

Transcript of Global Head of AXA Global L&S CEO for Northern, … · AXA Jacques de Vaucleroy Global Head of AXA...

AXA

Jacques de Vaucleroy Global Head of AXA Global L&S

CEO for Northern, Central and Eastern Europe region

Member of the AXA Management Committee

October 2, 2014

Bank of America Merrill Lynch

Annual Banking & Insurance CEO Conference 2014

2 – Bank of America Merrill Lynch Annual Banking & Insurance CEO Conference 2014 – October 2, 2014

Cautionary note concerning forward-looking statements

Certain statements contained herein are forward-looking statements including, but not

limited to, statements that are predictions of or indicate future events, trends, plans or

objectives. Undue reliance should not be placed on such statements because, by their

nature, they are subject to known and unknown risks and uncertainties. Please refer to the

section “Cautionary statements” in page 2 of AXA’s Document de Référence for the year

ended December 31, 2013, for a description of certain important factors, risks and

uncertainties that may affect AXA’s business. AXA undertakes no obligation to publicly

update or revise any of these forward-looking statements, whether to reflect new

information, future events or circumstances or otherwise.

3 – Bank of America Merrill Lynch Annual Banking & Insurance CEO Conference 2014 – October 2, 2014

Today’s key messages

1H14 achievements in line with consistent delivery on Ambition AXA

Performing well in a low interest rate environment

Focus on G/A Protection & Health business: growing and profitable

4 – Bank of America Merrill Lynch Annual Banking & Insurance CEO Conference 2014 – October 2, 2014

1H14 achievements in line with

consistent delivery on Ambition AXA

5 – Bank of America Merrill Lynch Annual Banking & Insurance CEO Conference 2014 – October 2, 2014

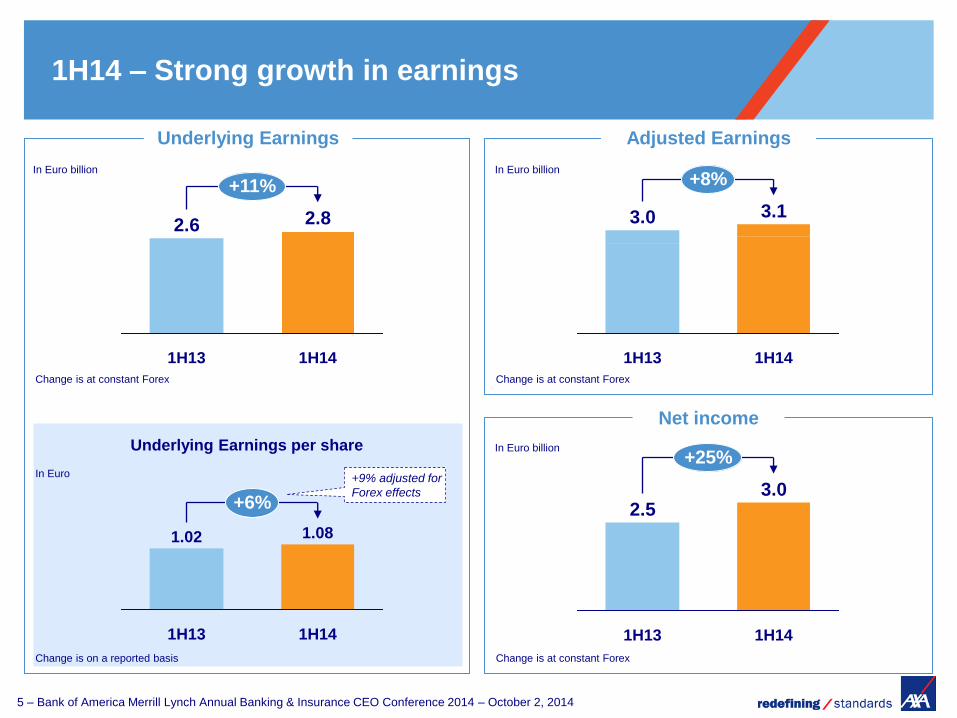

1H14 – Strong growth in earnings

Adjusted Earnings

In Euro billion

+11%

1H14

2.8

1H13

2.6

Change is at constant Forex

Underlying Earnings per share

+6%

1H14

1.08

1H13

1.02

+8%

1H14

3.1

1H13

3.0

Change is at constant Forex

+25%

1H14

3.0

1H13

2.5

Net income

Change is at constant Forex

Underlying Earnings

In Euro billion

+9% adjusted for

Forex effects

Change is on a reported basis

In Euro billion

In Euro

6 – Bank of America Merrill Lynch Annual Banking & Insurance CEO Conference 2014 – October 2, 2014

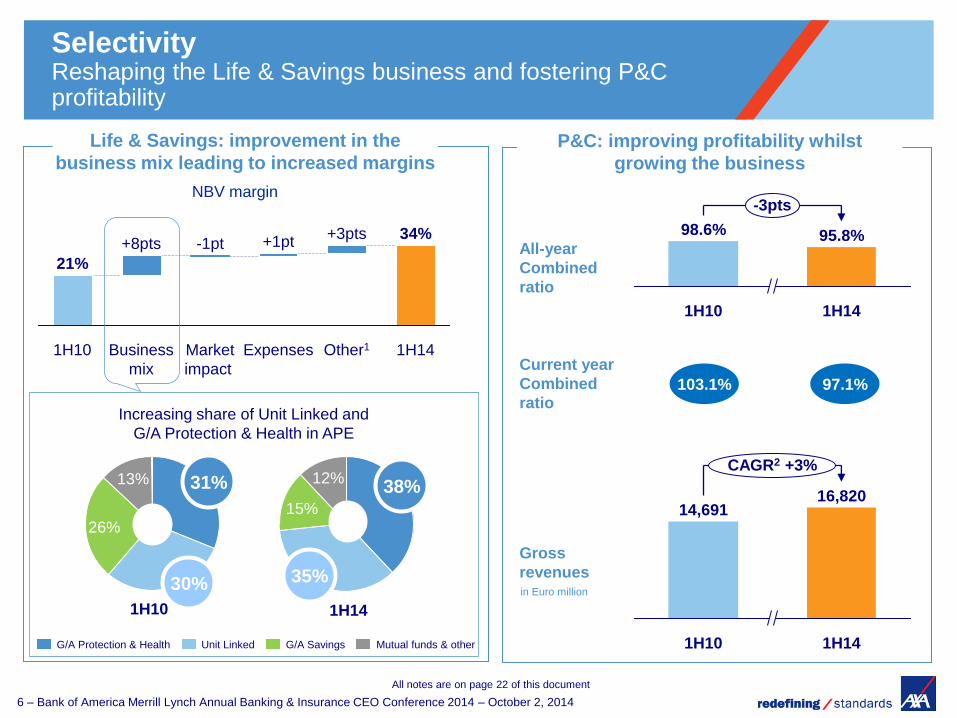

Selectivity Reshaping the Life & Savings business and fostering P&C profitability

CAGR2 +3%

1H14

16,820

1H10

14,691

in Euro million

Gross

revenues

Life & Savings: improvement in the

business mix leading to increased margins

P&C: improving profitability whilst

growing the business

Expenses

+1pt

Market

impact

-1pt

Business

mix

+8pts +3pts

Other1

34%

1H14

21%

1H10

NBV margin

Current year

Combined

ratio

98.6%

-3pts

1H14

95.8%

1H10

All-year

Combined

ratio

103.1% 97.1%

Increasing share of Unit Linked and

G/A Protection & Health in APE

13%

26%

12%

15%

1H10 1H14

G/A Savings Mutual funds & other Unit Linked G/A Protection & Health

38%

35%

31%

30%

All notes are on page 22 of this document

7 – Bank of America Merrill Lynch Annual Banking & Insurance CEO Conference 2014 – October 2, 2014

Contribution to

Group P&C

Acceleration Double-digit topline and earnings evolution in high growth markets

CAGR +23%

1H14

248

1H10

110 92

CAGR +26%

1H14

232

1H10

CAGR +12%

1H14

2,269

1H10

1,417

NBV Underlying Earnings

67

CAGR +17%

1H14

124

1H10

CAGR +15%

1H14

513

1H10

298

Revenues Underlying Earnings

In Euro million

APE

Focus on China P&C

AXA-Tian Ping1

Focus on China L&S

ICBC-AXA Life

Positive contribution to

Underlying Earnings in 1H14

Revenues Euro 0.9 billion at

1H141

1H13

39

+21%

1H14

46

APE In Euro million

Investing in brand, claims and

pricing capabilities leveraging

Group know-how

30% of premiums coming from

Direct channel in 1H14, up from

20% in 2012

+30%

1H14

364

1H13

291

Revenues In Euro million

10% 16% 10% 13% 7% 14% 8% 10% Contribution to

Group L&S

All notes are on page 22 of this document

In Euro million

Property & Casualty high growth markets

Life & Savings high growth markets

8 – Bank of America Merrill Lynch Annual Banking & Insurance CEO Conference 2014 – October 2, 2014

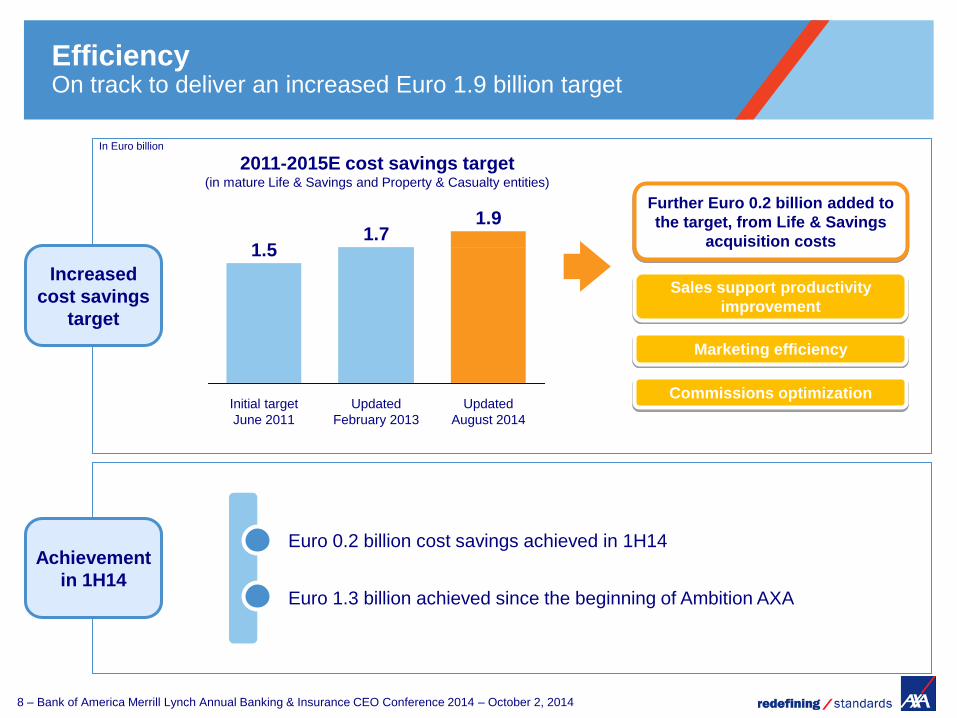

Updated

August 2014

1.9

Updated

February 2013

1.7

Initial target

June 2011

1.5

Increased

cost savings

target

Achievement

in 1H14

Efficiency On track to deliver an increased Euro 1.9 billion target

2011-2015E cost savings target (in mature Life & Savings and Property & Casualty entities)

In Euro billion

Further Euro 0.2 billion added to

the target, from Life & Savings

acquisition costs

Sales support productivity

improvement

Marketing efficiency

Commissions optimization

Euro 0.2 billion cost savings achieved in 1H14

Euro 1.3 billion achieved since the beginning of Ambition AXA

9 – Bank of America Merrill Lynch Annual Banking & Insurance CEO Conference 2014 – October 2, 2014

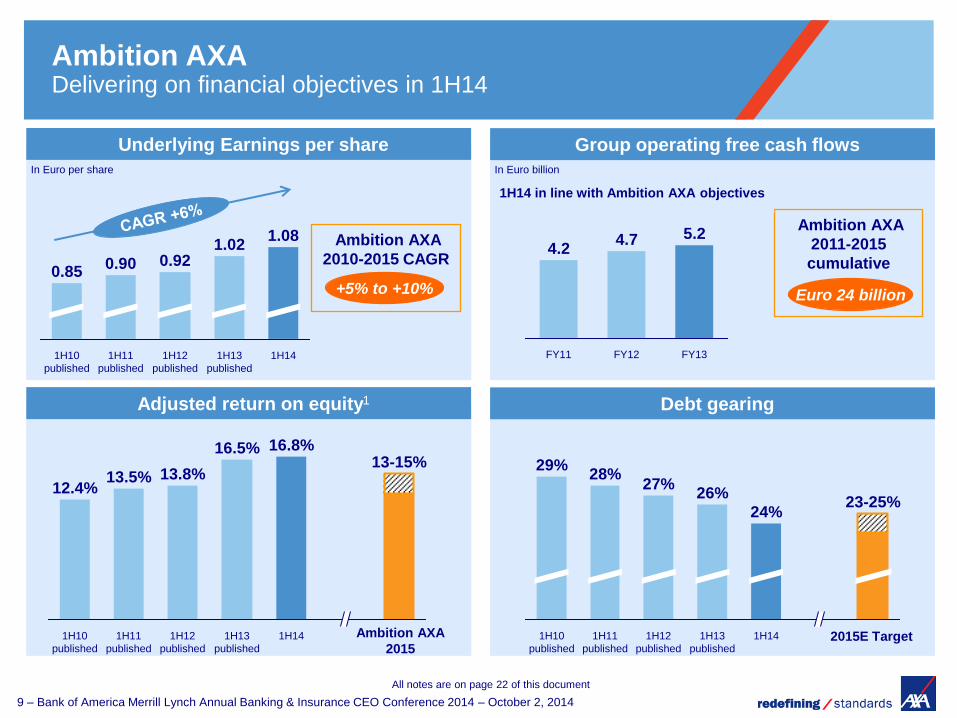

Adjusted return on equity1 Debt gearing

Underlying Earnings per share Group operating free cash flows

In Euro per share

Ambition AXA

2011-2015

cumulative

Euro 24 billion

Ambition AXA

2015

Ambition AXA

2010-2015 CAGR

+5% to +10%

1H14

1.08

1H13

published

1.02

1H12

published

0.92

1H11

published

0.90

1H10

published

0.85

23-25%

1H14

24%

1H13

published

26%

1H12

published

27%

1H11

published

28%

1H10

published

29% 13-15%

1H14

16.8%

1H13

published

16.5%

1H12

published

13.8%

1H11

published

13.5%

1H10

published

12.4%

2015E Target

FY13

5.2

FY12

4.7

FY11

4.2

1H14 in line with Ambition AXA objectives

In Euro billion

Ambition AXA Delivering on financial objectives in 1H14

All notes are on page 22 of this document

10 – Bank of America Merrill Lynch Annual Banking & Insurance CEO Conference 2014 – October 2, 2014

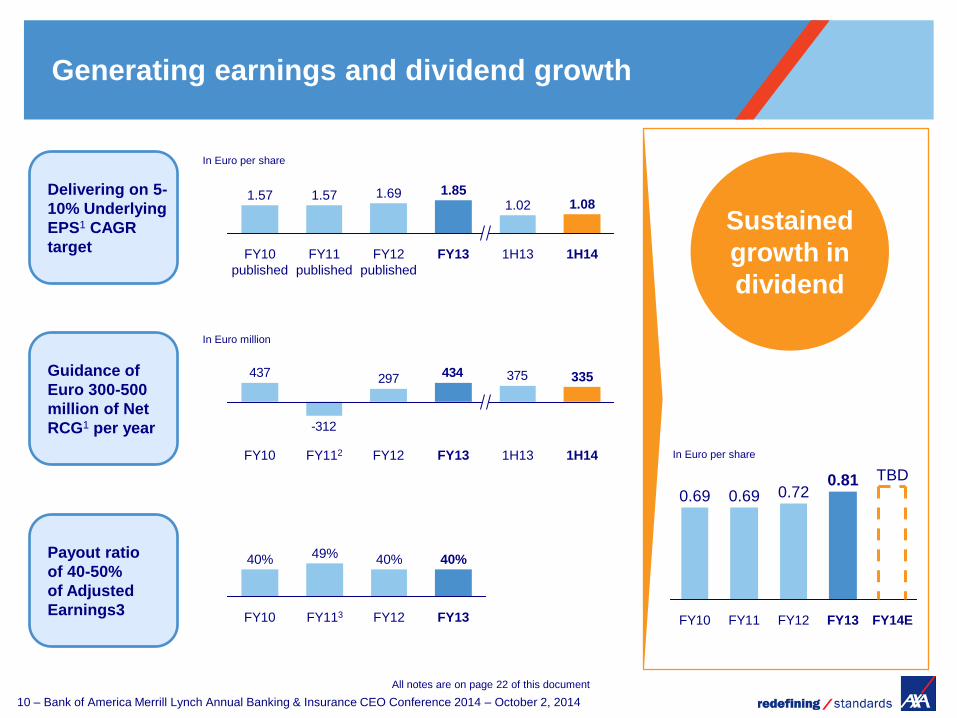

Guidance of

Euro 300-500

million of Net

RCG1 per year

Delivering on 5-

10% Underlying

EPS1 CAGR

target

Generating earnings and dividend growth

1.69

FY13 FY10

published

FY11

published

1.08 1.57

1H14

1.02

FY12

published

1.85

1H13

1.57

375297

-312

437 434

FY112 FY10

335

1H14 FY12 FY13 1H13

FY113

49% 40%

FY10 FY12 FY13

40% 40%

TBD

FY11

0.72

FY12

0.81

FY10 FY13

0.69

FY14E

0.69

Payout ratio

of 40-50%

of Adjusted

Earnings3

Sustained

growth in

dividend

In Euro per share

In Euro million

In Euro per share

All notes are on page 22 of this document

11 – Bank of America Merrill Lynch Annual Banking & Insurance CEO Conference 2014 – October 2, 2014

Performing well in a low interest rate

environment

12 – Bank of America Merrill Lynch Annual Banking & Insurance CEO Conference 2014 – October 2, 2014

Performing well in low interest rate environment (1/3)

Ca.

70% of Group pre-tax Underlying Earnings1 coming from

Property & Casualty and Protection & Health2, i.e.

businesses less sensitive to financial markets

Ca.

1 year

Duration gap maintained around one year

between assets and liabilities (which are mostly

long term in nature)

Well diversified

business mix reduces

earnings volatility

Strong ALM discipline

Decreased sensitivities

to low interest rate

environment

Note: FY13 Group Embedded Value sensitivity to a -100bps parallel shift in risk-free rates: -5%

Ca. Euro

-100 million

Estimated impact on Underlying Earnings3 should

interest rates be 100bps lower for 1 year

All notes are on page 22 of this document

13 – Bank of America Merrill Lynch Annual Banking & Insurance CEO Conference 2014 – October 2, 2014

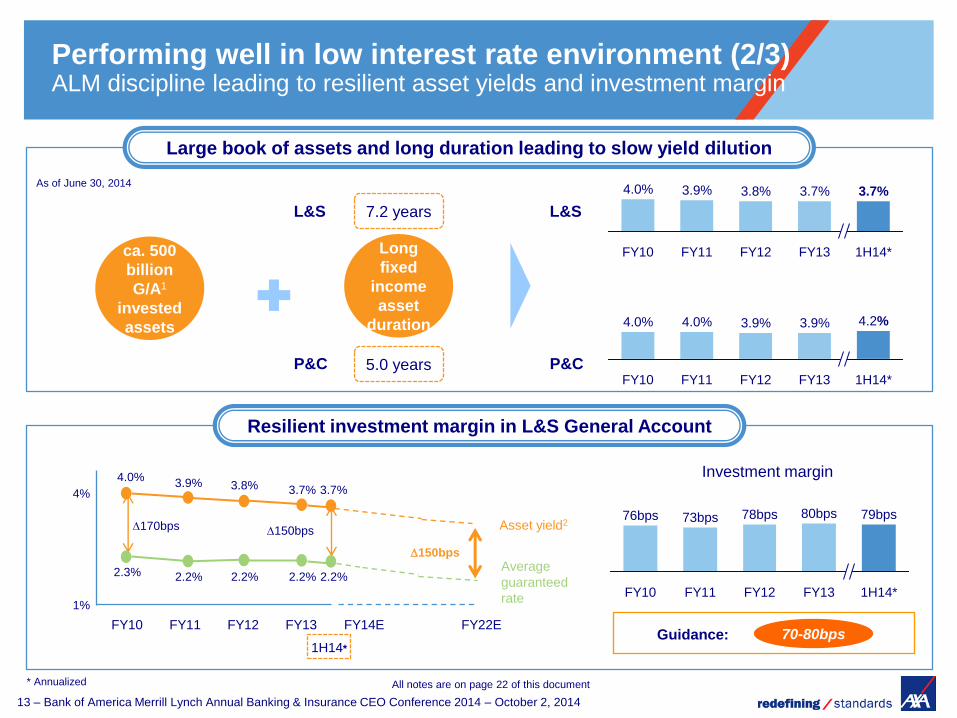

Large book of assets and long duration leading to slow yield dilution

Resilient investment margin in L&S General Account

1H14*

3.7%

FY13

3.7%

FY12

3.8%

FY11

3.9%

FY10

4.0%

1H14*

4.2%

FY13

3.9%

FY12

3.9%

FY11

4.0%

FY10

4.0%

Average

guaranteed

rate

Asset yield2 170bps 150bps

FY10 FY11 FY12 FY13

1H14*

FY14E FY22E

4.0% 3.9% 3.8% 3.7% 3.7%

2.2% 2.2% 2.2% 2.2% 2.3%

150bps

4%

1%

70-80bps Guidance:

FY13 1H14*

78bps

FY11 FY10

73bps 76bps 80bps 79bps

FY12

L&S 7.2 years

P&C 5.0 years

ca. 500

billion

G/A1

invested

assets

L&S

P&C

Long

fixed

income

asset

duration

Performing well in low interest rate environment (2/3) ALM discipline leading to resilient asset yields and investment margin

Investment margin

All notes are on page 22 of this document

As of June 30, 2014

* Annualized

14 – Bank of America Merrill Lynch Annual Banking & Insurance CEO Conference 2014 – October 2, 2014

Increasing contribution from P&H and growing top line in P&C

Strong technical profitability in Protection & Health and P&C

Performing well in low interest rate environment (3/3) Protection & Health and P&C contribute c. 70% to Group pre-tax underlying earnings

1H10 1H14 1H14

CAGR +3%

16,820 16,497

1H13

16,173

1H12 1H11

15,350

1H10

14,691

P&C Revenues Share of Protection & Health in Total L&S APE

Ambition

AXA 2015

1H14

96.0% 97.9% 97.6%

FY13

95.8% 96.6%

FY12 FY10 FY11

99.5% 94.0%

FY12 FY10

95.5%

1H141

95.5%

FY11

94.7%

FY13

94.5%

Combined ratio - Protection & Health

Profitable and consistently below 96%

Combined ratio - P&C

Strong improvement in line with Ambition AXA

38% 31%

In Euro million

All notes are on page 22 of this document

15 – Bank of America Merrill Lynch Annual Banking & Insurance CEO Conference 2014 – October 2, 2014

Focus on G/A Protection & Health:

growing and profitable

16 – Bank of America Merrill Lynch Annual Banking & Insurance CEO Conference 2014 – October 2, 2014

Population ageing

and growth

CAGR +11%

FY13

2.5

FY10

1.8

APE (in Euro billion)

APE NBV

Protection & Health as a % of Total L&S Data as of FY13

Protection & Health business

Strong volume and profitability growth An important contributor to L&S result

Further growth potential due to market dynamics

NBV margin

Medical cost

inflation Economic growth

Withdrawal of

states

FY13

47%

+12pts

59%

FY10

39% 67% 55%

Pre-tax Underlying

Earnings

17 – Bank of America Merrill Lynch Annual Banking & Insurance CEO Conference 2014 – October 2, 2014

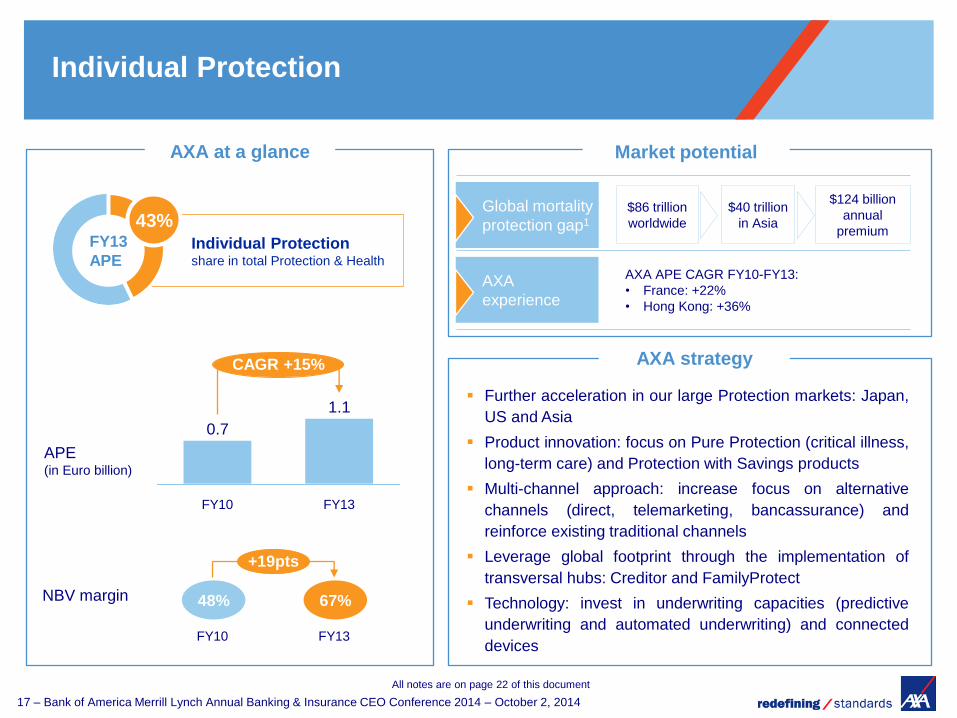

Individual Protection share in total Protection & Health

Individual Protection

AXA at a glance

FY10

0.7

FY13

1.1

CAGR +15%

APE (in Euro billion)

NBV margin

Further acceleration in our large Protection markets: Japan,

US and Asia

Product innovation: focus on Pure Protection (critical illness,

long-term care) and Protection with Savings products

Multi-channel approach: increase focus on alternative

channels (direct, telemarketing, bancassurance) and

reinforce existing traditional channels

Leverage global footprint through the implementation of

transversal hubs: Creditor and FamilyProtect

Technology: invest in underwriting capacities (predictive

underwriting and automated underwriting) and connected

devices

AXA

experience

AXA strategy

Market potential

43% FY13

APE

FY10

1.1

+19pts

1.1

FY13

48% 67%

AXA APE CAGR FY10-FY13:

• France: +22%

• Hong Kong: +36%

Global mortality

protection gap1

$86 trillion

worldwide

$40 trillion

in Asia

$124 billion

annual

premium

All notes are on page 22 of this document

18 – Bank of America Merrill Lynch Annual Banking & Insurance CEO Conference 2014 – October 2, 2014

• Wealth increase and consumerization

• Innovation and specialization

• Changes in demographic and lifestyle

• Withdrawal of states

Individual Health share in total Protection & Health

Individual Health

AXA at a glance

CAGR +10%

FY13

0.5

FY10

0.4

APE (in Euro billion)

NBV margin

Further leverage market leading position as #1 global multi-

line Health insurer (ex-US)

Further develop in six stronghold markets: France,

Germany, UK2, Japan, Hong Kong, Mexico

Increase the number of stronghold markets by 2020 with an

additional focus on high growth markets: Gulf, Malaysia,

Thailand, Indonesia and China

In high growth markets, focus on affluent and high net worth

segments

Extend health insurance towards health services and well

being management leveraging internal capacities (e.g. AXA

Assistance) and focus on digitalization

AXA strategy

Market potential

21% FY13

APE

+19pts

FY13

1.1

FY10

1.1 73% 92%

• Global health spending growth 2.6% in 2013

accelerating to 5.3% (CAGR FY14-FY17)1

Market

dynamics

Market growth

All notes are on page 22 of this document

19 – Bank of America Merrill Lynch Annual Banking & Insurance CEO Conference 2014 – October 2, 2014

Group Protection & Health share in total Protection & Health

Group Protection & Health

AXA at a glance

CAGR +8%

FY13

0.9

FY10

0.7

APE (in Euro billion)

NBV margin

Enhance growth in our stronghold markets: France,

Switzerland and Belgium

Leverage expertise from AXA France and AXA Switzerland

to increase focus in mature markets (US, Germany, Italy

and Spain) and high growth markets

Reinforce efficiency and focus on growth in Asia (Indonesia,

Hong Kong, Thailand, Singapore)

Create an aligned, global compliant offer for expats

including a worldwide network of providers and innovative

assistance services

Become Top 3 provider of employee benefits solutions for

Multi-National Companies (MAXIS)

AXA strategy

Market potential

36% FY13

APE

-1pt

FY13

1.1

FY10

1.1 33% 32%

Group P&H premiums CAGR1 (FY13-FY20)

• >3% Domestic Mature markets

• +12% Domestic High growth markets

Expat market premiums CAGR2 (FY11-FY17):

+11%

Worldwide

Group P&H

Market

All notes are on page 22 of this document

20 – Bank of America Merrill Lynch Annual Banking & Insurance CEO Conference 2014 – October 2, 2014

Today’s key messages

1H14 achievements in line with consistent delivery on Ambition AXA

Performing well in a low interest rate environment

Focus on G/A Protection & Health business: growing and profitable

21 – Bank of America Merrill Lynch Annual Banking & Insurance CEO Conference 2014 – October 2, 2014

Q&A session

Q&A session

22 – Bank of America Merrill Lynch Annual Banking & Insurance CEO Conference 2014 – October 2, 2014

All year over year comments are on comparable basis for activity indicators (constant Forex, scope and methodology), and at constant Forex for

earnings, except for EPS and CAGR growth which is on reported basis; new business margin growth from 2010 to 2014 is on reported basis too.

Page 6

1. Other includes scope, country mix, Forex impact, actuarial and modelling assumption changes

2. CAGR: Compound annual growth rate

Page 7

1. AXA-Tian Ping and ICBC-AXA Life are not included in Group revenues due to consolidation under equity method. Figures shown on the graph

correspond to the period of January 1 to June 30 and are at 100% share. Acquisition of 50% of Tian Ping was completed on February 20, 2014

Page 9

1. Underlying EPS: Underlying Earnings per share; Net RCG: Net realized capital gains

2. Greek government bond impairment

3. Net of undated debt interest charges

Page 10

1. Adjusted ROE: Return corresponds to adjusted earnings net of interest charges on undated debt. Equity corresponds to average shareholders’

equity excluding undated debt and reserves related to change in fair value

Page 12

1. Excluding holdings

2. Includes G/A Protection & Health, Property & Casualty and International Insurance

3. Estimated impact on Underlying Earnings from General Account only (G/A Savings, G/A Protection & Health and Property & Casualty)

Page 13

1. General Account 1H14 Invested assets referenced in page 57 of the financial supplement are Euro 696 billion, which include notably Euro 167

billion of Unit-linked assets and Euro 37 billion related to the banking sector

2. Projections assuming an average 2.9% Fixed Income reinvestment rate over next 9 years

Notes (1/2)

23 – Bank of America Merrill Lynch Annual Banking & Insurance CEO Conference 2014 – October 2, 2014

Page 14

1. P&H combined ratio calculation was adjusted to exclude Underlying Earnings from associates

Page 17

1. Source: Swiss Re, sigma 6/2013 “Life insurance: focusing on consumer”, “Mortality and Morbidity gaps, aging society and Implications on product

development”, 2012. Mortality protection gap is defined as the additional resources required to maintain the current living standard of dependents

(spouse, children, other) after the death of the family breadwinner. A premium rate of 0.3% as estimated by Swiss Re is used to arrive from

protection gap in Asia to estimated potential annual premiums.

Page 18

1. Source: Deloitte “2014 Global health care outlook”

2. AXA UK PPP business not included in L&S scope but in P&C

Page 19

1. Source: McKinsey Global 2013

2. Source: Roland Berger analysis 2013

Notes (2/2)

![(Axa wf global strategic bonds germany sept 2013 [kompatibilitätsmodus])](https://static.fdocuments.in/doc/165x107/5472a6ebb4af9fbe0a8b50df/axa-wf-global-strategic-bonds-germany-sept-2013-kompatibilitaetsmodus.jpg)

![Axa Magnet - Presentasi AXA Magnet [ Maestro Global Network ] Terbaru](https://static.fdocuments.in/doc/165x107/55d2ed27bb61ebdd398b462f/axa-magnet-presentasi-axa-magnet-maestro-global-network-terbaru.jpg)