Bank of America Merrill Lynch 21st Annual Financials CEO ... · AXA Thomas Buberl – Chief...

22

AXA Thomas Buberl – Chief Executive Officer Bank of America Merrill Lynch 21st Annual Financials CEO Conference | London September 29, 2016

-

Upload

nguyentuong -

Category

Documents

-

view

219 -

download

2

Transcript of Bank of America Merrill Lynch 21st Annual Financials CEO ... · AXA Thomas Buberl – Chief...

AXA

Thomas Buberl – Chief Executive Officer

Bank of America Merrill Lynch

21st Annual Financials CEO Conference | London

September 29, 2016

Certain statements contained herein are forward-looking statements including, but not limited to,

statements that are predictions of or indicate future events, trends, plans or objectives. Undue reliance

should not be placed on such statements because, by their nature, they are subject to known and

unknown risks and uncertainties. Please refer to the section “Cautionary statements” in page 2 of AXA’s

Document de Référence for the year ended December 31, 2015, for a description of certain important

factors, risks and uncertainties that may affect AXA’s business. AXA undertakes no obligation to publicly

update or revise any of these forward-looking statements, whether to reflect new information, future events

or circumstances or otherwise.

3 | AXA | BofAML 21st Annual Financials CEO Conference | London | September 29, 2016

KEY TAKEAWAYS

Transparent, realistic and credible Ambition 2020 plan Clear underlying assumptions and management levers for growth

Emphasis on execution and operations Efficiency, business growth and technical margin improvement

Earnings and balance sheet resilient to low interest rates Diversified business mix, disciplined risk management and high quality new business

4 | AXA | BofAML 21st Annual Financials CEO Conference | London | September 29, 2016

KEY TAKEAWAYS

Transparent, realistic and credible Ambition 2020 plan Clear underlying assumptions and management levers for growth

Emphasis on execution and operations Efficiency, business growth and technical margin improvement

Earnings and balance sheet resilient to low interest rates Diversified business mix, disciplined risk management and high quality new business

5 | AXA | BofAML 21st Annual Financials CEO Conference | London | September 29, 2016

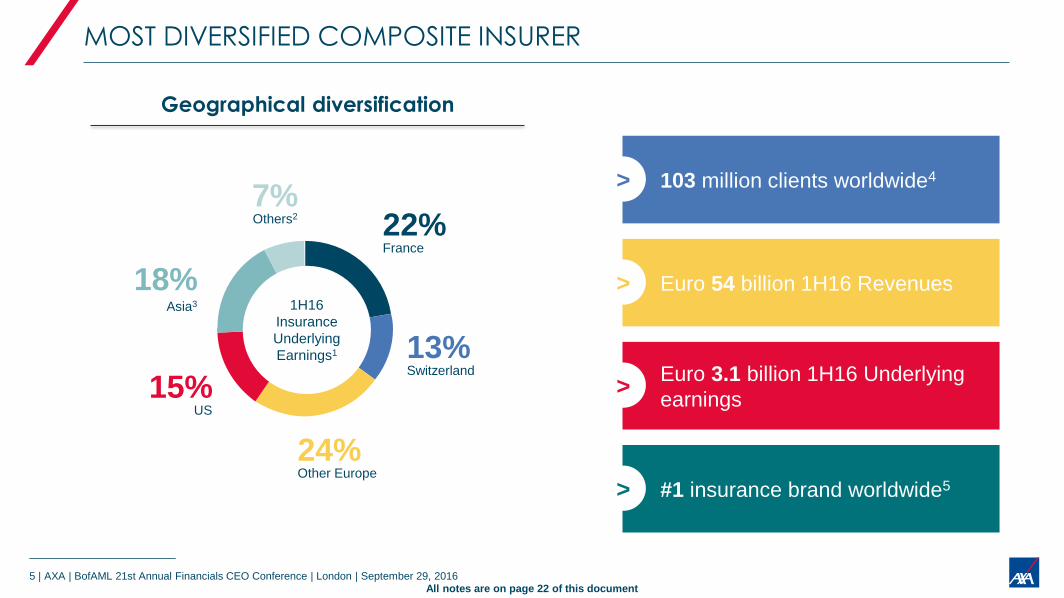

MOST DIVERSIFIED COMPOSITE INSURER

Geographical diversification

22% France

15% US

18% Asia3

7% Others2

All notes are on page 22 of this document

103 million clients worldwide4 >

Euro 54 billion 1H16 Revenues >

Euro 3.1 billion 1H16 Underlying

earnings >

#1 insurance brand worldwide5 >

1H16

Insurance

Underlying

Earnings1 13% Switzerland

24% Other Europe

6 | AXA | BofAML 21st Annual Financials CEO Conference | London | September 29, 2016

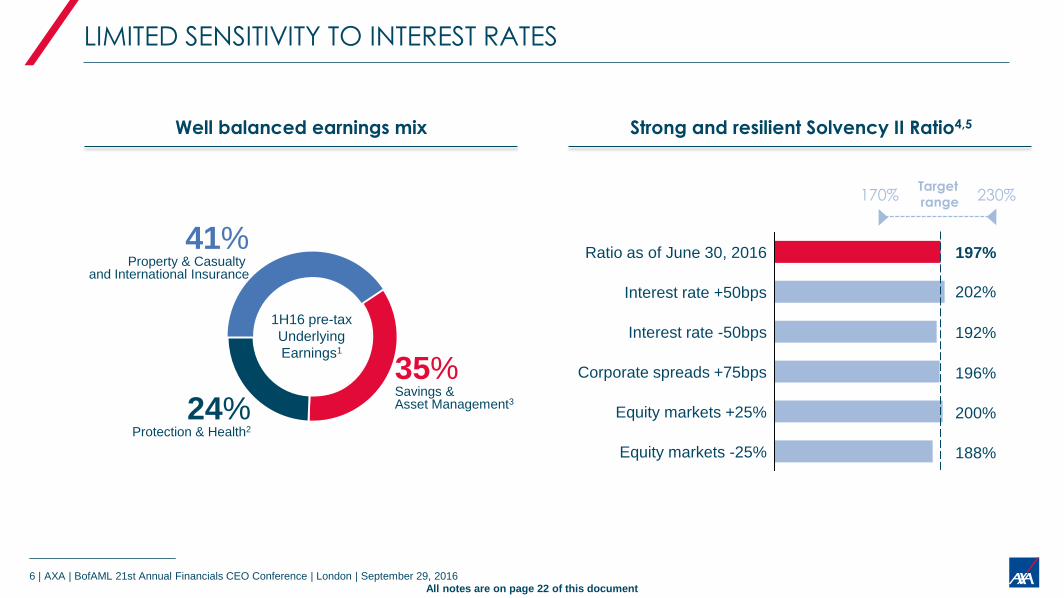

LIMITED SENSITIVITY TO INTEREST RATES

Well balanced earnings mix

1H16 pre-tax

Underlying

Earnings1

35% Savings & Asset Management3 24%

Protection & Health2

41% Property & Casualty

and International Insurance

Strong and resilient Solvency II Ratio4,5

Equity markets -25%

Equity markets +25%

Interest rate +50bps

Corporate spreads +75bps

Ratio as of June 30, 2016

Interest rate -50bps

197%

202%

192%

196%

200%

188%

170% Target

range 230%

All notes are on page 22 of this document

7 | AXA | BofAML 21st Annual Financials CEO Conference | London | September 29, 2016

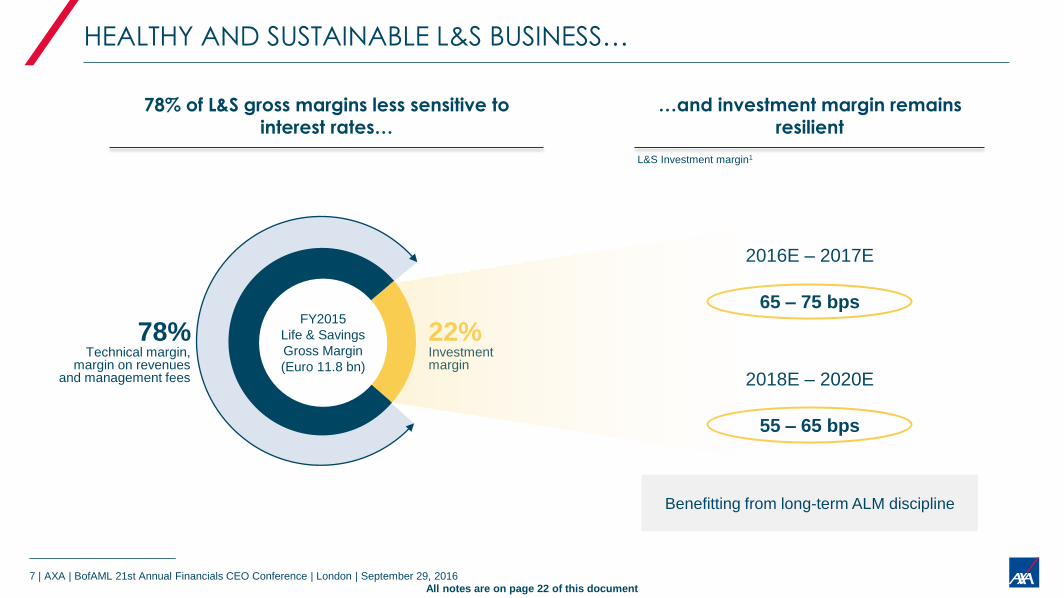

HEALTHY AND SUSTAINABLE L&S BUSINESS…

78% of L&S gross margins less sensitive to interest rates…

55 – 65 bps

65 – 75 bps

2016E – 2017E

2018E – 2020E

…and investment margin remains resilient

L&S Investment margin1

22% Investment margin

78% Technical margin,

margin on revenues and management fees

FY2015

Life & Savings

Gross Margin

(Euro 11.8 bn)

All notes are on page 22 of this document

Benefitting from long-term ALM discipline

8 | AXA | BofAML 21st Annual Financials CEO Conference | London | September 29, 2016

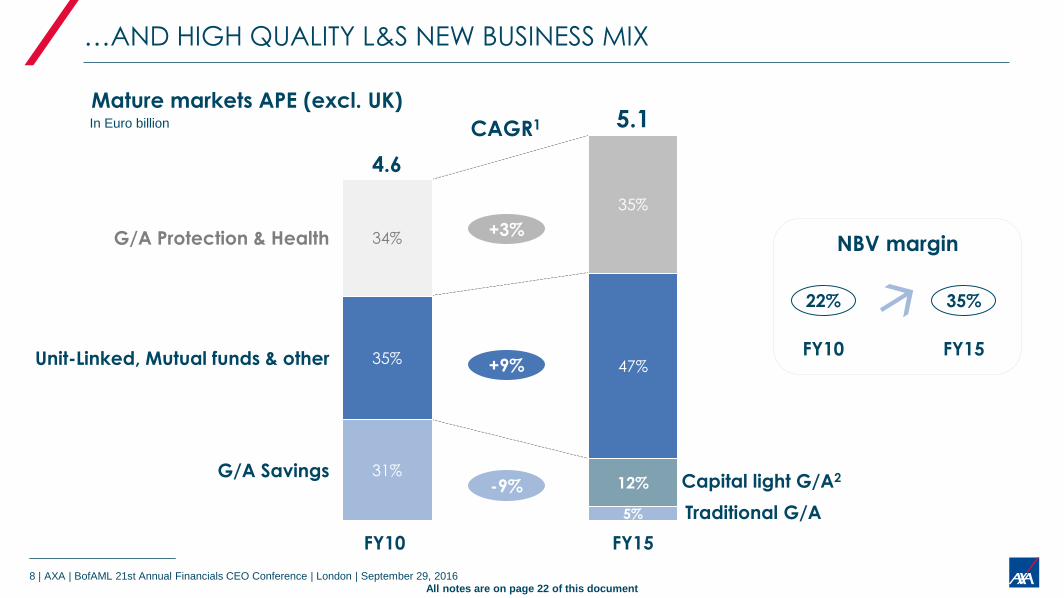

…AND HIGH QUALITY L&S NEW BUSINESS MIX

G/A Savings

Unit-Linked, Mutual funds & other

G/A Protection & Health

FY15

5.1

47%

5%

12% 31%

35%

FY10

4.6

35%

34%

In Euro billion

Mature markets APE (excl. UK)

NBV margin

22%

+3%

+9%

-9%

35%

Capital light G/A2

Traditional G/A

FY10 FY15

CAGR1

All notes are on page 22 of this document

9 | AXA | BofAML 21st Annual Financials CEO Conference | London | September 29, 2016

KEY TAKEAWAYS

Transparent, realistic and credible Ambition 2020 plan Clear underlying assumptions and management levers for growth

Emphasis on execution and operations Efficiency, business growth and technical margin improvement

Earnings and balance sheet resilient to low interest rates Diversified business mix, disciplined risk management and high quality new business

10 | AXA | BofAML 21st Annual Financials CEO Conference | London | September 29, 2016

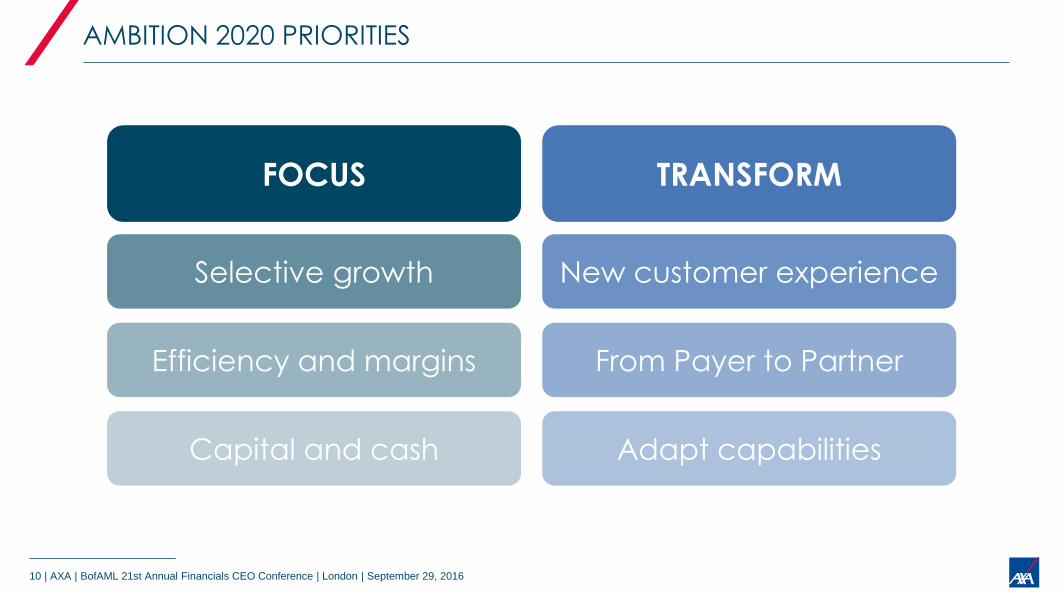

AMBITION 2020 PRIORITIES

New customer experience

From Payer to Partner

Adapt capabilities

FOCUS

Selective growth

Efficiency and margins

Capital and cash

TRANSFORM

11 | AXA | BofAML 21st Annual Financials CEO Conference | London | September 29, 2016

UNDERLYING EARNINGS PER SHARE

AMBITION 2020: KEY OBJECTIVES

EUR 28-32 bn Cumulative 2016E-2020E

GROUP OPERATING FREE CASH FLOWS

ADJUSTED RETURN ON EQUITY1

SOLVENCY II RATIO

170% - 230% Target range

12% - 14% 2016E-2020E

3-7% CAGR 2015-2020E

All notes are on page 22 of this document

12 | AXA | BofAML 21st Annual Financials CEO Conference | London | September 29, 2016

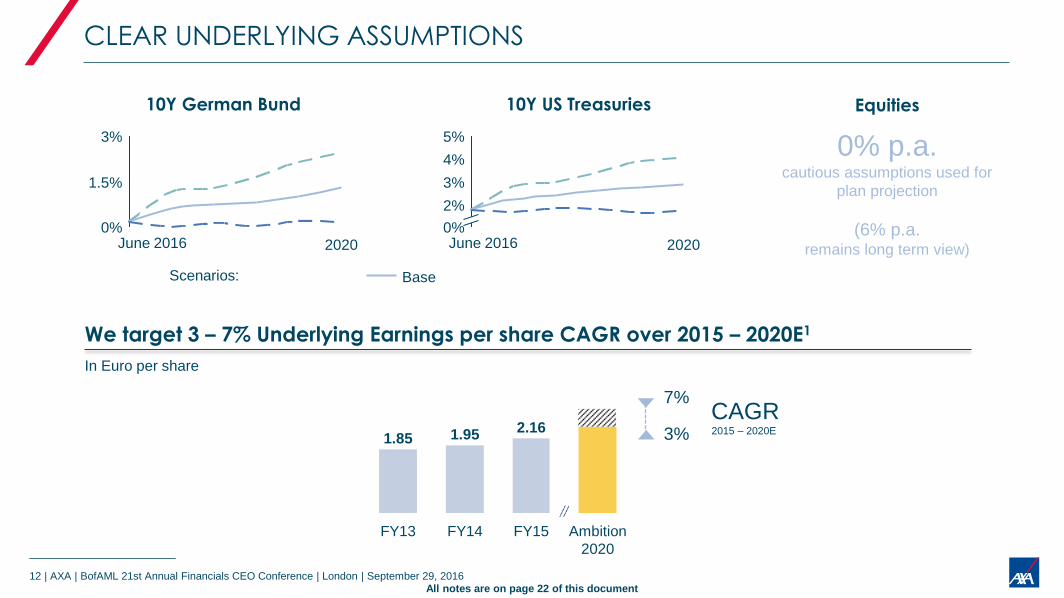

CLEAR UNDERLYING ASSUMPTIONS

FY14

2.16

FY15 Ambition

2020

1.95

FY13

1.85

We target 3 – 7% Underlying Earnings per share CAGR over 2015 – 2020E1

In Euro per share

3% CAGR 2015 – 2020E

1.5%

3%

0% 2020

0% p.a. cautious assumptions used for

plan projection

(6% p.a.

remains long term view)

0%

3%

2%

5%

4%

2020

10Y German Bund Equities 10Y US Treasuries

Unfavourable Base Favourable

June 2016 June 2016

Scenarios:

7%

All notes are on page 22 of this document

13 | AXA | BofAML 21st Annual Financials CEO Conference | London | September 29, 2016

EARNINGS GROWTH DESPITE INTEREST RATE HEADWINDS

2%

Technical

margin

M&A

1%

Growth

2%

Efficiency

3%

-5% ; -1%

3% - 7%

2015 –

2020E

UEPS

CAGR

Under management control

8% UEPS CAGR

+ =

Interest

rates

headwinds

Uncertainties

-5 to -1% UEPS CAGR

Ambition 2020

+3% to +7% CAGR

14 | AXA | BofAML 21st Annual Financials CEO Conference | London | September 29, 2016

KEY TAKEAWAYS

Transparent, realistic and credible Ambition 2020 plan Clear underlying assumptions and management levers for growth

Emphasis on execution and operations Efficiency, business growth and technical margin improvement

Earnings and balance sheet resilient to low interest rates Diversified business mix, disciplined risk management and high quality new business

15 | AXA | BofAML 21st Annual Financials CEO Conference | London | September 29, 2016

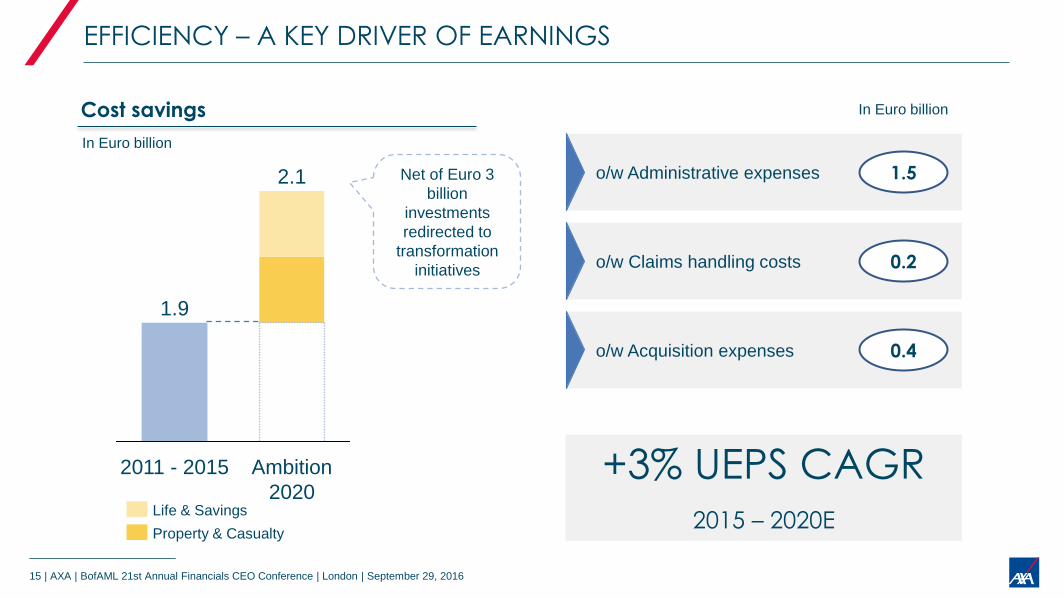

EFFICIENCY – A KEY DRIVER OF EARNINGS

In Euro billion

Cost savings

1.9

2.1

2011 - 2015 Ambition

2020 Life & Savings

Property & Casualty

o/w Administrative expenses

o/w Claims handling costs

o/w Acquisition expenses

+3% UEPS CAGR

2015 – 2020E

Net of Euro 3

billion

investments

redirected to

transformation

initiatives

1.5

0.2

0.4

In Euro billion

16 | AXA | BofAML 21st Annual Financials CEO Conference | London | September 29, 2016

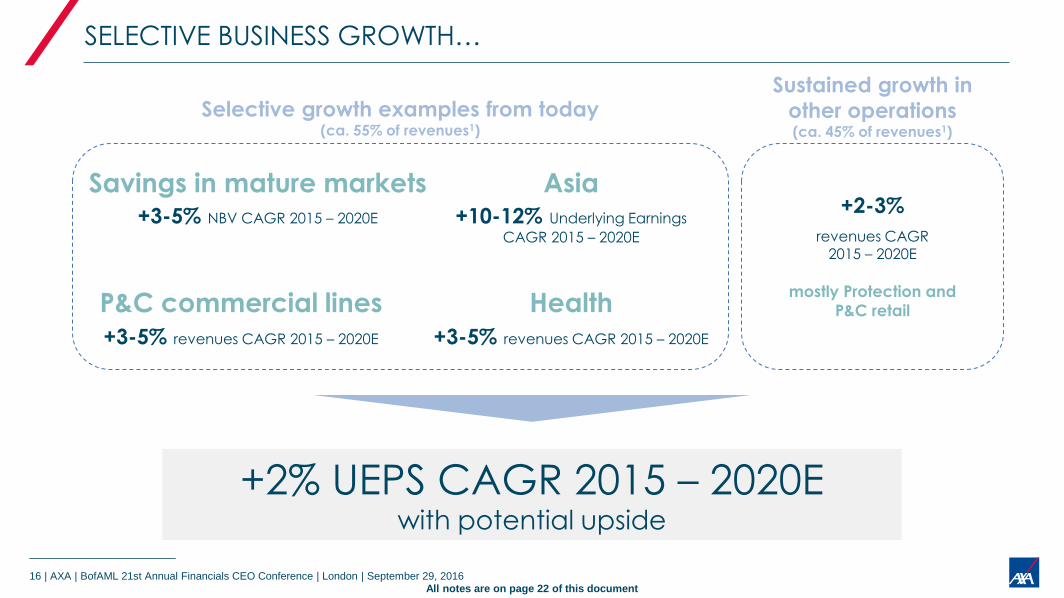

+2% UEPS CAGR 2015 – 2020E with potential upside

SELECTIVE BUSINESS GROWTH…

Selective growth examples from today (ca. 55% of revenues1)

Sustained growth in

other operations (ca. 45% of revenues1)

+2-3%

revenues CAGR 2015 – 2020E

Savings in mature markets Asia +3-5% NBV CAGR 2015 – 2020E

P&C commercial lines

+3-5% revenues CAGR 2015 – 2020E

Health

+3-5% revenues CAGR 2015 – 2020E

+10-12% Underlying Earnings

CAGR 2015 – 2020E

mostly Protection and

P&C retail

All notes are on page 22 of this document

17 | AXA | BofAML 21st Annual Financials CEO Conference | London | September 29, 2016

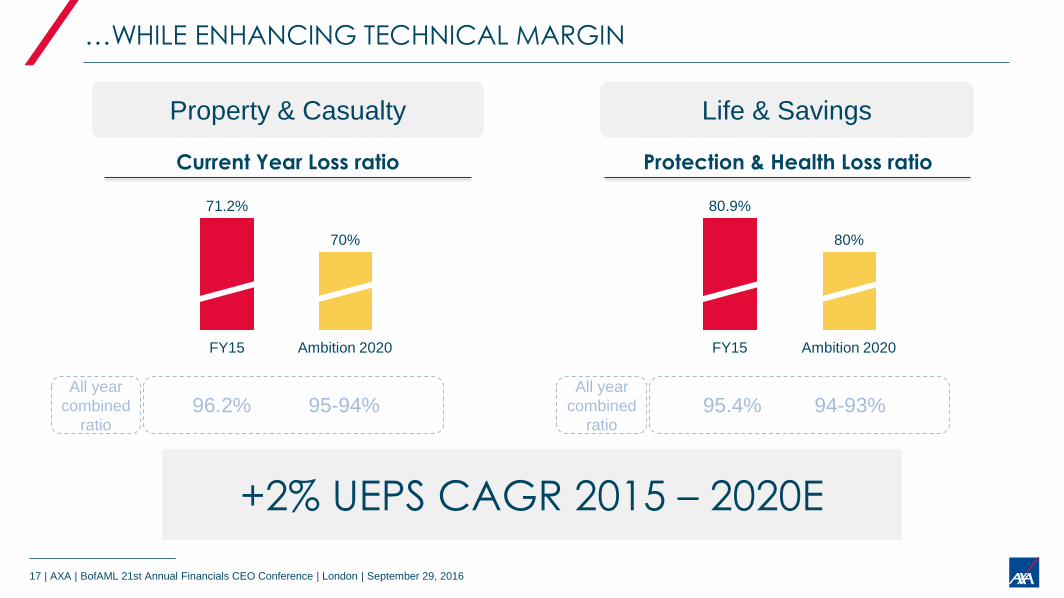

…WHILE ENHANCING TECHNICAL MARGIN

Ambition 2020

70%

FY15

71.2%

Current Year Loss ratio

Property & Casualty Life & Savings

Protection & Health Loss ratio

Ambition 2020

80%

FY15

80.9%

+2% UEPS CAGR 2015 – 2020E

96.2% 95-94% 95.4% 94-93% All year

combined

ratio

All year

combined

ratio

18 | AXA | BofAML 21st Annual Financials CEO Conference | London | September 29, 2016

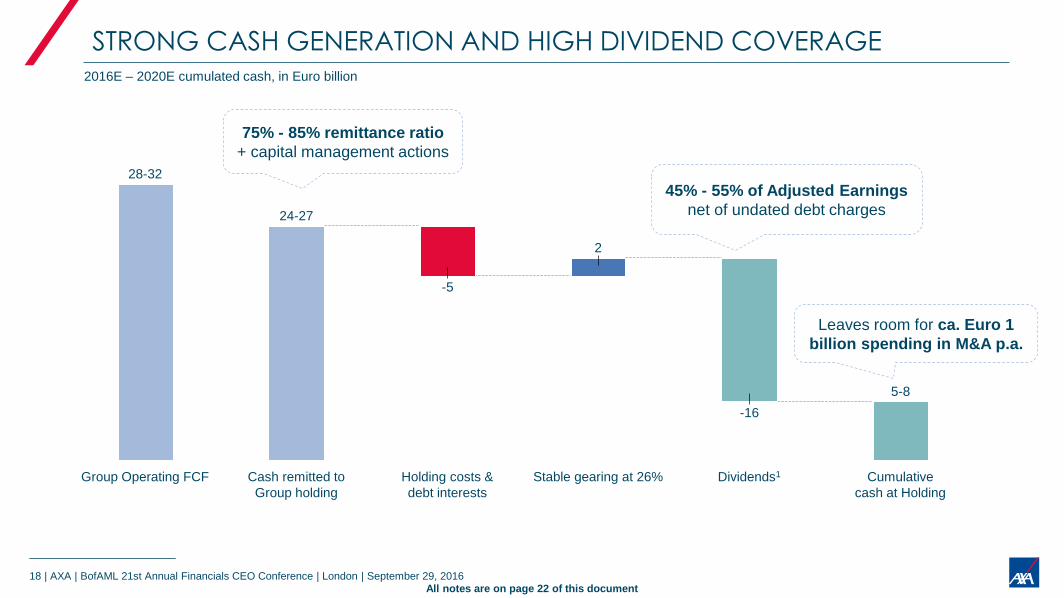

STRONG CASH GENERATION AND HIGH DIVIDEND COVERAGE

Cumulative

cash at Holding

5-8

-16

Dividends1

2

Stable gearing at 26%

24-27

Group Operating FCF

28-32

Holding costs &

debt interests

-5

Cash remitted to

Group holding

2016E – 2020E cumulated cash, in Euro billion

45% - 55% of Adjusted Earnings

net of undated debt charges

Leaves room for ca. Euro 1

billion spending in M&A p.a.

75% - 85% remittance ratio

+ capital management actions

All notes are on page 22 of this document

19 | AXA | BofAML 21st Annual Financials CEO Conference | London | September 29, 2016

SUSTAINABLE DIVIDENDS

Resilient Adjusted EPS growth 3-7% UEPS growth target

Euro 300 – 500 million

Net Realized Capital Gains guidance

Flexibility within payout ratio 45% - 55% target range

47% payout ratio at FY15

LEAVES ROOM FOR THE BOARD TO INCREASE DIVIDEND

20 | AXA | BofAML 21st Annual Financials CEO Conference | London | September 29, 2016

KEY TAKEAWAYS

Transparent, realistic and credible Ambition 2020 plan Clear underlying assumptions and management levers for growth

Emphasis on execution and operations Efficiency, business growth and technical margin improvement

Earnings and balance sheet resilient to low interest rates Diversified business mix, disciplined risk management and high quality new business

Thank You

22 | AXA | BofAML 21st Annual Financials CEO Conference | London | September 29, 2016

NOTES

Page 5

1. 1H16 insurance underlying earnings (Life & Savings ; Property & Casualty ; International Insurance).

2. Others: Includes MedLA high growth markets, Direct, International Insurance.

3. Including Japan

4. As reported in 1H16.

5. Interbrand ranking.

Page 6

1. Pre-tax 1H16 underlying earnings, excluding holdings.

2. General Account Protection & Health.

3. Including G/A Savings, Unit-Linked, Mutual Funds & other and Banking.

4. The Solvency II ratio is based on AXA’s internal model calibrated based on adverse 1/200 year shock and assuming US equivalence. AXA’s internal model was approved by ACPR on

November 18, 2015. Solvency II took effect from January 1, 2016.

5. Solvency II ratio is estimated including a theoretical amount for dividends accrued for the first semester of 2016 based on half of the full year dividends paid in 2016 for FY 2015.

Dividends are declared by the Board at its discretion based on a variety of factors described in AXA’s Annual Reports and then submitted to AXA’s shareholders for approval. This

estimate should not be considered in any way to be an indication of the actual dividend amount, if any, for the financial year 2016.

Page 7

1. L&S Investment margin in base case scenario as reported in the June 21, 2016 IR Day presentation.

Page 8

1. Compound annual growth rate.

2. G/A Savings products which, at inception, create more AFR than the economic capital they consume.

Page 11

1. Adjusted ROE: return corresponds to adjusted earnings net of interest charges on undated debt. Equity corresponds to average shareholders’ equity excluding undated debt and reserves

related to change in fair value.

Page 12

1. Average annual growth over the 5 year plan period; period-to-period results may vary.

Page 16

1. As of FY15.

Page 18

1. Euro 16 billion of dividends taking 50% payout ratio of Adjusted Earnings net of undated debt charges as an assumption, in the middle of the 45-55% payout range. Dividends are

declared by the Board in its discretion based on variety of factors described in AXA’s Annual Reports and then submitted to AXA’s shareholders for approval. The estimate should not be

considered in any way to be an indication of the actual dividend amount, if any, for future financial years.

![[Merrill Lynch] Credit Derivatives Handbook](https://static.fdocuments.in/doc/165x107/55cf97e9550346d03394646c/merrill-lynch-credit-derivatives-handbook.jpg)