Get A Rate Home Loans Buyer Kit

25

Homebuyer Planning Kit Nex t

-

Upload

amberskymktgdir -

Category

Real Estate

-

view

28 -

download

0

Transcript of Get A Rate Home Loans Buyer Kit

Homebuyer Planning Kit

Next Next

Agenda

Welcome Message

Who is Get A Rate

Our Mantra

Why Choose Get A Rate

Your Team

Our Resources

Benefits

Our Process

Where Do We Start

Pre-Approval Checklist

Simple Process

Pre-Approval Checklist

Same Day Pre-Approval

Timeline

Credit Scores

Ahead Of the Curve

Internal Control

To Do List

To Do Not List

Glossary

Next Next Prev Prev

3

Welcome Message

Why don’t we grab a cup of coffee? Let’s start there…

If your reading this, it’s because we’re really interested in getting to know you.

Why? Because we would like to help you in your goal of homeownership.

Next Next Prev Prev

4

We love what we do and are committed to it.

Our main goal is to make sure we’re of value to you.

Why? We understand that value promotes human action.

Our company recognizes how important a structured process is for the success of your

homeownership goal.

Who Are We?

We Are Get A Rate…

“A Google Minded Company with Tenacity”

Next Next Prev Prev

5

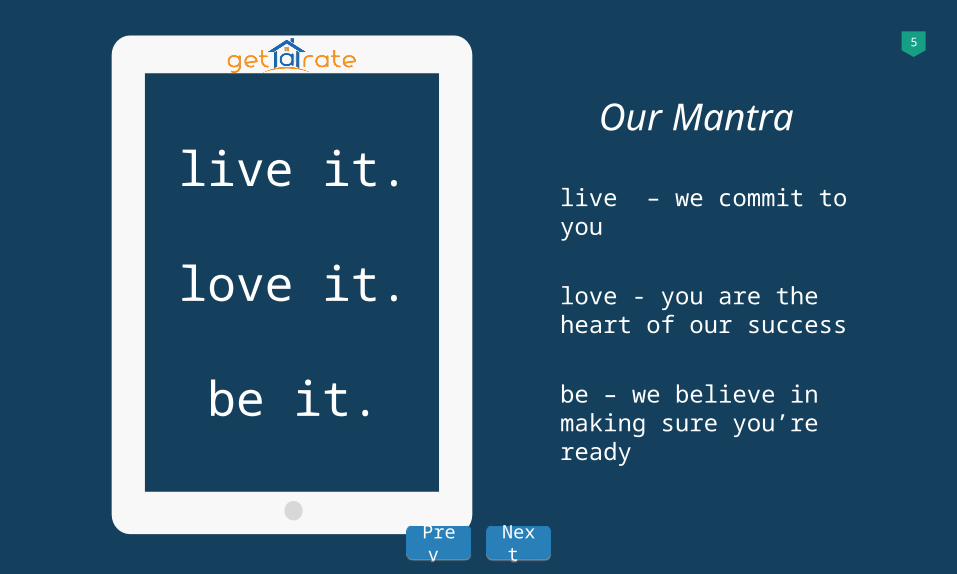

live – we commit to you

love - you are the heart of our success

be – we believe in making sure you’re ready

live it.

love it.

be it.

Our Mantra

Next Next Prev Prev

6Why Choose Get A Rate?

Streamline ProcessEasy, Efficient & Quick

ExperienceReal Answers

Real Pre-ApprovalsSave Time

Super Low RatesSave Money

Direct LenderComplete Supervision

Modern OperationConvenience

Next Next Prev Prev

We are small stars doing big things in this

universe.

Benefits To You…

Next Next Prev Prev

8

Your TeamKey Team Members

You

MLOAccount ExecutiveWith Get A Rate

UnderwriterPersonal

Underwriting Team

AppraiserTo Find Out The True Market Value Of The

Home

AttorneyTo Protect Your

Best Interest

InspectorHome Inspection

Report

InsuranceHome Owners

Insurance Policy

Michael SemaPresident

NMLS # 252607O (201) 393 - 0200

M (973) 303 - [email protected]

Sample NameRealtor AssociateREMAXO (201) 393 - 0200M (973) 303 - [email protected]

Next Next Prev Prev

9

Our ResourcesCompany Tools and Resources

Loan Options

Variety of loan options to fit all

needs.

Buyer Kits

Kits to help guide you throughout the

process.

Check Lists

Access to online or printable check lists.

Calculators

Online & mobile calculators that allow you to calculate payments -

on your time.

Client Education

Training and educational material on

the home buying process, products &

more.

Next Next Prev Prev

10Benefits To YouStructure. Structure. Structure.

Resources If you build it, they will come. Our business is based on 70% realtor referrals and we love them for it. Our training and resources are designed specifically to help you achieve success in affordable home ownership.

Structure At Get A Rate, we understand the importance of a structured process. When combining structure and discipline with an ethic of entrepreneurship, you get the magical alchemy of great performance.

Our Simple ProcessHave you ever seen a lender close a purchase loan in under 8 days? We have and continue to do so. Our in house underwriters and processors are great at what they do. They take pride in making sure you’re always updated throughout the process and your file closes on time.

TechnologyOur clients and realtors are the heart of our business. Unlike most of the industry, Get A Rate focuses its efforts on state of the art technology that improves and simplifies the approval process, speed, efficiency and productivity. What does this mean for you? Great customer service that makes you smile throughout the home buying process. Loan ProgramsMore options for consumers will always equal to more closings. Our programs start with your typical conforming, FHA, VA, USDA but also go into Super Jumbo, Construction and Non Agency programs as well. Lets not forget about our No PMI and No Condo Questionnaire programs.

ToolsWe’re a modern day company with modern day tools. Our tools are here to help you throughout the process. Our mortgage calculators help with monthly payments, amortization schedules, bi-weekly effective interest rates and more.

Next Next Prev Prev

11

Understanding Our Process

2Plan

1Lear

n

3Clos

e

During the discovery period, we get to

learn about you and your goals.

We take the discoveriesand create a plan:Rates, Programs,

Payments and more.

After selecting a plan, we finish processing

your loan and get you ready to close.

Next Next Prev Prev

12

Where Do We StartLet’s See If We’re A Right Fit

This meeting is to see if we’re a right fit for each other

over a cup of coffee.

Discuss your goals, plans, and

steps to get there.

Review the loan and rate options available to you.

The revision period is only if we need to update or change the loan or rate.

Delivery consists of the final review

and verbal agreement to work together.

Brainstorm

Final Step

Proposal

Revision

Meeting

Next Next Prev Prev

13

Start

Closer

Underwriter

Processor

MLO

Our Simple Process

It’s So Easy- We Get To Know You- Find Out About Your Goals- Home Purchase Review - Be of Value

- Complete Loan Application- Collect Initial Set of Docs- Prepare Disclosures- Submit

- Second Set of Eyes- Prepare File For Underwriting- Assistant to MLO

- Clear Conditions- Final Review- Clear To Close

- Closing Doc Prep- Wire Funds- Close

Next Next Prev Prev

14

Drivers License

Social Security

Card

Identification

Group A

Most Recent

2 Paystubs

2 Years of W2’s

2 Years of Tax

Returns

Income Docs

Group B

Most Recent

2 Bank

Statements

Proof of Funds

Group C

What Is A Pre-Approval? A Mortgage Pre-Approval is a preliminary statement that affirms according to your credit history, income and down payment reserves, you

will be able to obtain a loan up to a specific amount. It also affirms that an underwriting department has reviewed and verified your

scenario.

A Mortgage Pre-Approval is not a commitment to lend and additional documentation may be required.

Pre-Approval Checklist

List Of Documents Needed

Next Next Prev Prev

15Same Day Pre-ApprovalHere Is Where We Shine

Run FindingsVerificationApplication

03After the application is completed and documentation is verified, we make sure to run findings for eligibility.

02The most recent income, cash reserves, and credit documentations are always reviewed and verified.

01A detailed residential loan application is completed by asking the right questions.

04The final piece of the puzzle is our in-house Underwriter reviews steps 1, 2 & 3 before issuing a pre-approval.

Underwriter

Our Average Turn Time is 90 Minutes

Next Next Prev Prev

16Timeline Project ExampleWhat To Expect During The Process

Start

Week 1

Weeks 2 to 3

Week 4

Pre-ApprovalFind An Agent

Attorney Review

Submit Loan

Clear Conditions

Final Disclosures

Sign Closing Docs

PEOPLE INVOLVED

Lender Realtor Attorney Inspector Appraiser

ShopOfferFind

Attorney

InspectionAppraisal

Commitment

Title Clear To Close Final

Inspection

Next Next Prev Prev

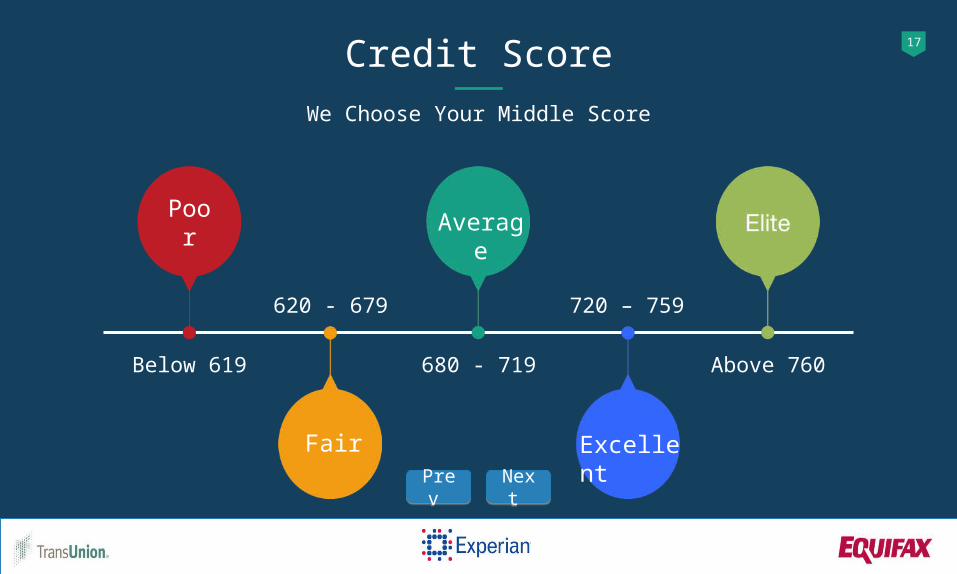

17Credit Score

We Choose Your Middle Score

620 - 679 720 – 759

Poor

Below 619 680 - 719 Above 760

Fair Excellent

Average

Next Next Prev Prev

18Ahead Of The Curvewww.GetARate.com

CalculatorsCalculate Payments On Your Own

Mortgage RatesMortgage Rate Updates

ResourceTips On Steps To Buying A Home And Much More

WebsiteOur Best Foot Forward

For The Online Consumer

Online PortalKeeping Track Of The

Progress

Mobile Upload Files From Your

Smart Phone

Next Next Prev Prev

Internal Control 19

Get A Rate vs. The Other Guy

10%

80%

10%

InternalBranch Control

100%

InternalBranch Control

Our company originates, processes, approves

and clears files to close all under one roof.

What does this mean?

Speed, Simplicity, Convenience &

Trust

Get A Rate Internal Strengths

10%

Branch

Underwriter

Closing Department

Others Get A Rate

Next Next Prev Prev

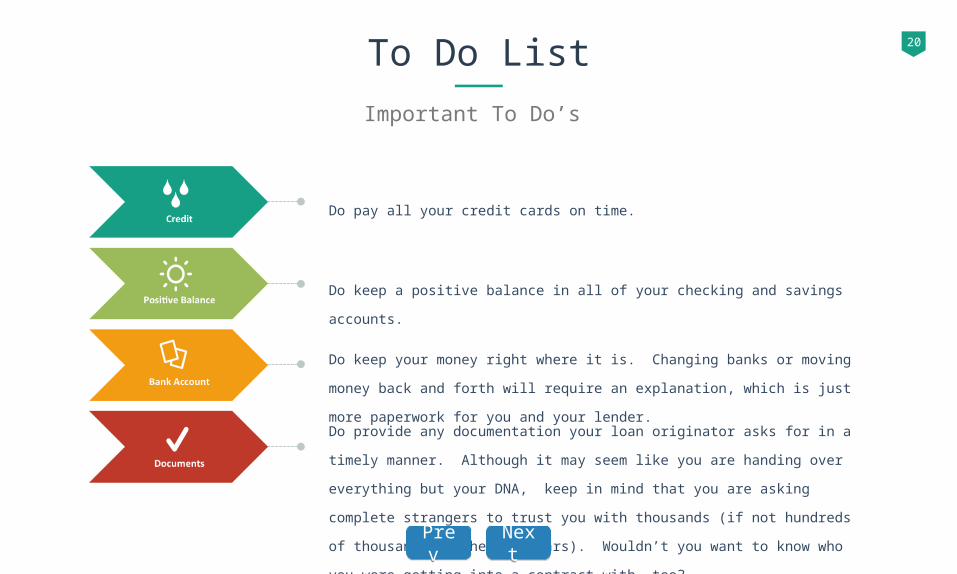

20To Do ListImportant To Do’s

Do pay all your credit cards on time.

Do keep a positive balance in all of your checking and savings accounts.

Do keep your money right where it is. Changing banks or moving money

back and forth will require an explanation, which is just more paperwork for

you and your lender.

Do provide any documentation your loan originator asks for in a timely

manner. Although it may seem like you are handing over everything but

your DNA, keep in mind that you are asking complete strangers to trust

you with thousands (if not hundreds of thousands of their dollars).

Wouldn’t you want to know who you were getting into a contract with,

too?

Next Next Prev Prev

21

Things To Not Do

Simon Says Don’t Do…

No Large Purchases Don’t Quit

Don’t use your credit card to

buy large items or things for

your home before you close.

(No excessive spending.)

Don’t quit your job.Don’t make out-of-the-

ordinary large deposits. If

you must, be prepared to

provide a clear paper trail

from where and why.

Don’t open new revolving

credit cards.

01 03

02 04No New Credit No Large Deposits

Next Next Prev Prev

22

Things To Not Do

Simon Says Don’t Do…

Don’t Lie Don’t Co-Sign

Don’t omit information. (This

can be the same as lying!)

Don’t co-sign on a loan for

anyone no matter how much

you love them or how many

times they promise to pay it

back. (This is a good rule

whether you are buying a

home or not.)

Don’t just get pre-qualified,

get pre-approved.

Don’t make sudden changes

in your spending habits or

income.

05 07

06 08Don’t Change Don’t Pre-Qualify

Next Next Prev Prev

23Real Estate & Mortgage GlossaryWe Thought You Should Know…

A Adjustable-Rate Mortgage (ARM) - Loans with an initial fixed rate period (usually 5,7 or 10 years. After the fixed rate period, your interest rate may change once per year - either up or down depending on market conditions. ARM’s are almost always lower in rate than fixed loans and can offer huge savings to first time home buyers especially those who don’t plan on staying in their home for more than 10 years.

Amortization - The paying off of a debt with a fixed repayment schedule in regular installments over a period of time. Annual Percentage Rate (APR) - The total cost of a loan, which includes not only the interest rate, but all costs associated with the loan, such as closing costs and fees. Once this is determined, the APR is then amortized over the life of the loan. In order to allow borrowers to compare various loans and lenders, the APR is required to be disclosed by the Federal Truth-in-Lending statues.

Application Fee - One time processing fee for a loan. This fee may be applied towards various costs, including the appraisal and credit report.

Appraisal - An estimate of the current market value of the property. B Buy Down - The ability for the buyer to lower their initial interest rate by providing money upfront or by paying extra points up front at the closing of the loan. C Closing - The time where buyer and seller exchange money for title and sign closing papers to a new home. This finalizes the agreements reached in the sales agreement.

Closing Costs - Refers to the lender’s costs for closing a loan or all the costs associated with closing on a piece of property as a buyer.

Conventional Mortgage - A loan that is underwritten, following specific guidelines, by banks, savings and loans or other types of mortgage companies. Typically, this refers to loans underwritten to the guidelines of Fannie Mae or Freddie Mac.

D Deed of Trust - The legal document that transfers property from one owner to another. Down Payment – The amount of your home’s purchase price you pay upfront. EEarnest Money - Upfront money provided by the borrower to the seller as a show of good faith towards the purchase price of a home.

Escrow Closing - A third party that acts as a neutral party and receives documents for the exchange of the deed by the sellers for the buyer’s money. F First Mortgage - Takes priority when there are other voluntary liens present. G Gift Letter - A letter, which details the amount of gift and name of the giver, which indicates a gift of cash to the buyer of a home. This can be provided by relatives, friends, non-profit organizations or government agencies depending on the requirements of given lender and product.

Good Faith Estimate (GFE) - A written estimate of closing costs that lenders are required to provide potential borrowers within three days of an application submission.

Next Next Prev Prev

24Real Estate & Mortgage GlossaryWe Thought You Should Know…

H Hazard Insurance - Also known as homeowner’s insurance, which covers the property from damages that may affect the value.

IInterest - The fee a lender charges for permitting the borrower to use their money for a specific length of time. Interest Rate Cap - The max amount of percentage points that ARMs may rise over a loan’s life.

LLoan Origination Fee - Fee charged by a lender to cover administrative costs of processing a loan.

Loan-to-Value Ratio (LTV) - The money borrowed in a mortgage transaction compared with the value of the property you wish to purchase. (Loan Amount / Home Value)

M Mortgage - The document providing a lien on a home in exchange for a lender’s financing. The lender secures this financed loan through this mortgage and has the ability to foreclose on this home as well.

Mortgage Banker - An entity that lends its own funds to borrowers while also bringing together lenders and borrowers. Mortgage bankers may also collect monthly payments.

O Origination Fee - A fee that is charged by a lender to cover the administrative costs of processing a loan.

PPITI ( Principal-Interest-Taxes-Insurance) - Four pieces included in a monthly mortgage payment. Portion of each payment applied to each of those elements.

Point - Each point equals one percent of your total loan amount. The more points you pay, the lower the interest rate you get.

Private Mortgage Insurance (PMI) - Paid in monthly installments by a borrower or upfront as part of the closing costs, this insurance allows a lender to lend more than 80% of the value of a property while protecting the lender on risk to the top 20%.

RRecording - Filing documents at various government agencies - local, state, and federal - to create a public record.

S Settlement Statement - Known as the HUD-1, this details the transaction paid out and received by the buyer and seller at closing, T Term - Typically 15 or 30 years, this is the life of the loan.

Title – The title is the actual document that gives evidence of ownership of a property.

Title Insurance - Title insurance protects lenders against any title dispute that may arise over a particular property. Home title insurance is a required fee paid at closing.

Next Next Prev Prev

25

Thank YouWe Look Forward To Earning Your

Business1 U.S. 46Elmwood Park, NJ, 07407

201-393-0200 [email protected]

www.GetARate.com

Michael Sema 973-303-3013

Prev Prev