German Private Equity Deal Survey 2017HY1 - United States · German PE market showed the second...

20

German Private Equity Deal Survey 2017HY1 Activities in Germany at a glance Special: Compliance Due Diligence in PE transactions 30 June 2017

Transcript of German Private Equity Deal Survey 2017HY1 - United States · German PE market showed the second...

German Private Equity Deal Survey 2017HY1Activities in Germany at a glance Special: Compliance Due Diligence in PE transactions

30 June 2017

German PE market showed the second highest deal volume since 2008 but decreased in terms of value due to the lack of multi-billion EUR deals, which could change in 2017HY2

Summary of significant results

Number of transactions

Value of transactions

M&A activity

PE sector analysis

• ►There were 91 PE-backed transactions in 2017HY1 compared to 125 in 2016HY2. After the peak in transaction volume in 2016HY2, the number of transactions remained on a very high level, with 91 transactions 2017HY1 representing the second highest volume since 2008HY1. The number of non-PE backed transactions remained stable.

• The total value of disclosed PE investments decreased from EUR 15.8bn to EUR 5.3bn in 2017HY1. This decrease was mainly driven by the absence of multi-billion EUR transactions. Value of primary PE investments decreased from EUR 10.0bn in 2016HY2 to EUR 3.4bn in 2017HY1, whereas the value of secondary investments decreased from EUR 5.8bn in 2016HY2 to EUR 1.9bn in 2017HY1.

• The largest PE transaction in 2017HY1 was the acquisition of a 20% stake in Otto Bock Healthcare by Sweden-based PE EQT for a total consideration of EUR 0.61bn.

• This represents the ongoing trend in the PE industry to expand existing business models by investing in large minority stakes.• With regard to the last twelve months (LTM), the deal value increased to EUR 21.1bn in June 2017, compared to EUR 13.5bn in

LTM June 2016. This increase on an LTM base (+56%) was mainly due to strong deal activity in 2016HY2, especially in the secondary market.

• The value of strategic acquisitions in 2017HY1 increased by 94% to EUR 23.1bn compared to 2016HY1, which was mainly caused by five deals valued above EUR 1bn. The largest deals were the acquisitions of Wirtgen Group by Deere & Company for EUR 4.6bn and the acquisition of Hamburg Südamerikanische Dampfschifffahrts-Gesellschaft by Maersk Line. The number of strategic transactions remained stable with 245 transactions in 2017HY1 compared to 248 transactions in 2016HY2.

• The largest sector with regard to transaction value was business services, which accounted for 34% of all disclosed transactions, followed by the pharma & healthcare sector (17%). The most significant transaction in the business services sector was the acquisition of Formel D by 3i and its co-investor CITIC. The pharma & healthcare sector was mainly influenced by several midsized hospital and rehab clinic deals. The information technology sector was the most active one in terms of volume (16%), followed by the pharma & healthcare sector (14%).

2 | German Private Equity Deal Survey 2017HY1 Activities in Germany at a glance

Exits

Geographical origin of PE investors

Major trends and outlook

• ►In 2017HY1, the value of trade exits decreased to EUR 0.9bn compared to 2016HY2. However, it is notable that several large portfolio companies are currently in ongoing sales processes or will enter such a process in the near future. Secondary exits also decreased to EUR 1.9bn in 2017HY1 compared to EUR 5.8bn in 2016HY2. This could be an indication for reduced exit activities after four consecutive years of high exit activity.

• ►Following the trend of the previous period, the majority of investments by value (LTM June 2017) were made by US-based PE investors. In LTM June 2017, activity levels of UK-based PE investors remained modest (EUR 2.7bn) whereas the value of investments by Germany-based PE investors increased by 28%. In terms of volume, the majority of PE investors, participating in German deals, were locally based, showing an increase from 64 transactions in LTM June 2016 to 87 transactions in LTM June 2017. The number of transactions backed by US-based PE investors remained stable at 21.

• For 2017HY2 an increasing level of deal volume and value is expected, backed by a favourable economic development in Germany and ongoing low interest rates.

• Several large portfolio companies are currently in a sales process or will be up for sale in the near future, which could lead to a recovery of exits and deal values. Further, Cinven and Bain are considering a renewed offer for Stada, which would be one of the largest PE transactions in Germany ever.

• Upcoming elections in Germany and the overall European political development are expected to have only a minor impact on the German PE market.

• EuropeanPEfundraisingachievedthehighestvaluesincethetimebeforethefinancialcrisis,leadingtoanongoingstrongdemand for targets and hence increasing prices.

3German Private Equity Deal Survey 2017HY1 Activities in Germany at a glance |

Basis of information

4 | German Private Equity Deal Survey 2017HY1 Activities in Germany at a glance

On LTM June basis, the value of disclosed PE transactions was EUR 21.1bn in 2017HY1, representing the highest value since LTM June 2007

Key Statements

• The adjacent table compares the volume of transactions in which the deal value was not disclosed, in comparison to the total volume and value of disclosed transactions in 2017HY1

• Compared to 2016HY2, the deal value of disclosed PE transactions decreased by EUR 10.5bn. The total number of PE transactions decreased from 125 in 2016HY2 to 91 in 2017HY1

• In 2017HY1 no PE deal valued at EUR 1bn or above could be observed. In particular because the takeover attempt of Stada by Bain and Cinven in June 2017 was unsuccessful

Volume of disclosed and non-disclosed PE investments

0

20

40

60

80

100

120

140

0

2

4

6

8

10

12

14

16

18

2013HY1 2013HY2 2014HY1 2014HY2 2015HY1 2015HY2 2016HY1 2016HY2 2017HY1

Value of PE investments TLG CeramTec ista International GmbHSpringer Scout CABB MauserGEA Median Kliniken Siemens Audiology Solutions SenvionBayer Diabetes Healthcare SynLab Douglas Tank & RastArmacell Bilfinger SE (Building and Facility division) Xella International GmbH OfficeFirstAirbus Group (defense electronics business)

Atotech Acetow GmbH

Volume of non-disclosed PE investmentsVolume of PE investments

EUR bnVolume of transactions

Scout SAS

Median

Bilfinger

AirbusTank & Rast

Armacell XellaInternational

OfficeFirst

Atotech

Acetow

CeramTec

Bayer D.H.

SynLab

Douglas

Senvion SE

ista

Springer

MauserCABB

GEA

5German Private Equity Deal Survey 2017HY1 Activities in Germany at a glance |

A decrease in volume and value of PE investments could be observed due to the absence of multi-billion EUR transactions in 2017HY1. However, the market was driven by numerous small and midsized deals, resulting in a retention of PE investment volume at a very high level

Key Statements

• Primary PE transactions decreased by EUR 6.6bn compared to 2017HY2, mainly due to the absence of large carve-out transactions in 2017HY1. Secondaries volume decreased significantly by 27%

• Following the long-term trend, prices for primary and secondary investments continued to grow, leading to a shift in PE’s investment strategies. As a result, we observed an increasing number of PE minority investments e.g. EQT Partners AB acquired a 20% stake in Otto Bock Healthcare

• On an LTM basis, primary buyouts reached the highest value since June 2007 with EUR 21.1bn, backed by a strong activity in 2016HY2

Development of PE investments and secondary investments

120

100

0

Volume of transactions

PE investments (value) Secondary PE investments (value) PE investments (volume) Secondary PE investments (volume)

12

6

4

2

0

8

2013HY1 2013HY2 2014HY1 2014HY2 2015HY1 2015HY2 2016HY1

20

40

80

EUR bn

2016HY2 2017HY2

10

60

6 | German Private Equity Deal Survey 2017HY1 Activities in Germany at a glance

M&A activity in value terms increased strongly in 2017HY1. Five M&A deals in the German market were valued at EUR 1bn or above representing the consistently high demand for targets from strategic investors

Key Statements

• The graph shows the development of the German M&A market (i.e. non-PE investments) compared to PE investments

• Compared to the first-half of 2016, the value and volume of strategic takeovers increased significantly

• The acquisition of Wirtgen Group Holding GmbH by Deere & Company for EUR 4.6bn and the acquisition of Hamburg Südamerikanische Dampfschifffahrts-Gesellschaft KG by Maersk A/S (Maersk Line) for EUR 3.7bn were the largest M&A deals in 2017HY1

• Acquisitions of German targets by Chinese strategic investors rebounded in 2017HY1. Further, acquisitions by US based strategic investors quadrupled to EUR 7.15bn supported by the stable economic development in Germany and increasing investment risks in other geographic areas

Development of M&A transactions

0

5

10

15

20

25

30

35

40

2013HY1 2013HY2 2014HY1 2014HY2 2015HY1 2015HY2 2016HY1 2016HY2 2017HY1

WincorVNG

Getrag

Tank & Rast

Armacell

Disclosed value of PE investments Disclosed value of non-PE investments

RWE

TenneT

Eplus

CelesioAG

ScoutMauser

GEA

Median

DO Deutsche Office

Südewo

KaufhofGSW

Bosch

SAS

DouglasSynLab

Bayer D. H.Senvion SE

EUR bn

Flint

WILD Flavors

Bilfinger

WMF

Chemetall

Kuka

Airbus

XellaInternational

Atotech

Office FirstAcetow

BSNMedicalCarl Zeiss SMT

Wirtgen

Drillisch AG

Biotest AGAdam Opel AG

HH Dampf-Schifffahrt

7German Private Equity Deal Survey 2017HY1 Activities in Germany at a glance |

LTM June 2017 PE deal value was the highest since LTM Dec 2007. Based on a strong second half of the year 2016, 216 deals were signed in LTM June 2017, valued at more than EUR 21.1bn

Key Statements

• The graph pictures the historical development of PE investments by value and volume on an LTM basis

• The value of PE investments increased from EUR 13.5bn in LTM June 2016 to EUR 21.1bn in LTM June 2017. Also, the volume of PE investments in LTM June 2017 exceeded all previous periods since 2007

• The increase in value and volume for LTM June 2016 was mainly due to an extraordinary level of acquisition activity in 2016HY2. Further, high cash reserves of PE funds and stable economic growth in Germany fostered demand for targets in Germany

PE investments by value and volume

25

20

5

0

190

210

230

150

130

90

Value of PE investments

Volume of transactions

Volume of PE investments

110

LTMDec

2009

LTMJun

2010

LTMDec

2010

LTMJun

2011

LTMDec

2011

LTMJun

2012

LTMDec

2012

LTMJun

2013

LTMDec

2013

LTMJun

2014

LTMDec

2014

LTMJun

2015

LTMDec

2015

EUR bn

LTMJun

2016

15

10

170

LTMDec

2016

LTMJun

2017

8 | German Private Equity Deal Survey 2017HY1 Activities in Germany at a glance

Activity by US-based PE investors increased strongly in terms of value and volume, whereas activity of domestic PE investors remained stable on a LTM June 2017 base

Key Statements

• The adjacent graph shows the volume and value development of PE transactions considering the investors’ country of origin

• Increasing competition for small and midsized-deals was driven by US-based investors mainly due to the absence of large opportunities

• Deal value for US-based investors almost tripled (+EUR 9.8bn) in LTM June 2017 backed by a strong activity in 2016HY2, whereas the volume remained stable. The value of investments made by multinational syndicates declined after two consecutive highs in terms of deal value

• The largest disclosed transaction in 2017HY1, which was signed by a foreign investors, was the acquisition of a 20% stake in Otto Bock Healthcare by Sweden-based EQT for a deal value of EUR 0.61bn

Development of PE investments according to the origin country of investors

14

16

12

10

6

2

0

90

100

60

40

20

0LTM June 2012 LTM June 2013 LTM June 2014 LTM June 2015 LTM June 2016

Volume of transactions

Germany Multinational syndicateMultinational syndicateGermany

UK USAUSAUK

10

30

50

70

80

EUR bn

LTM June 2017

4

8

9German Private Equity Deal Survey 2017HY1 Activities in Germany at a glance |

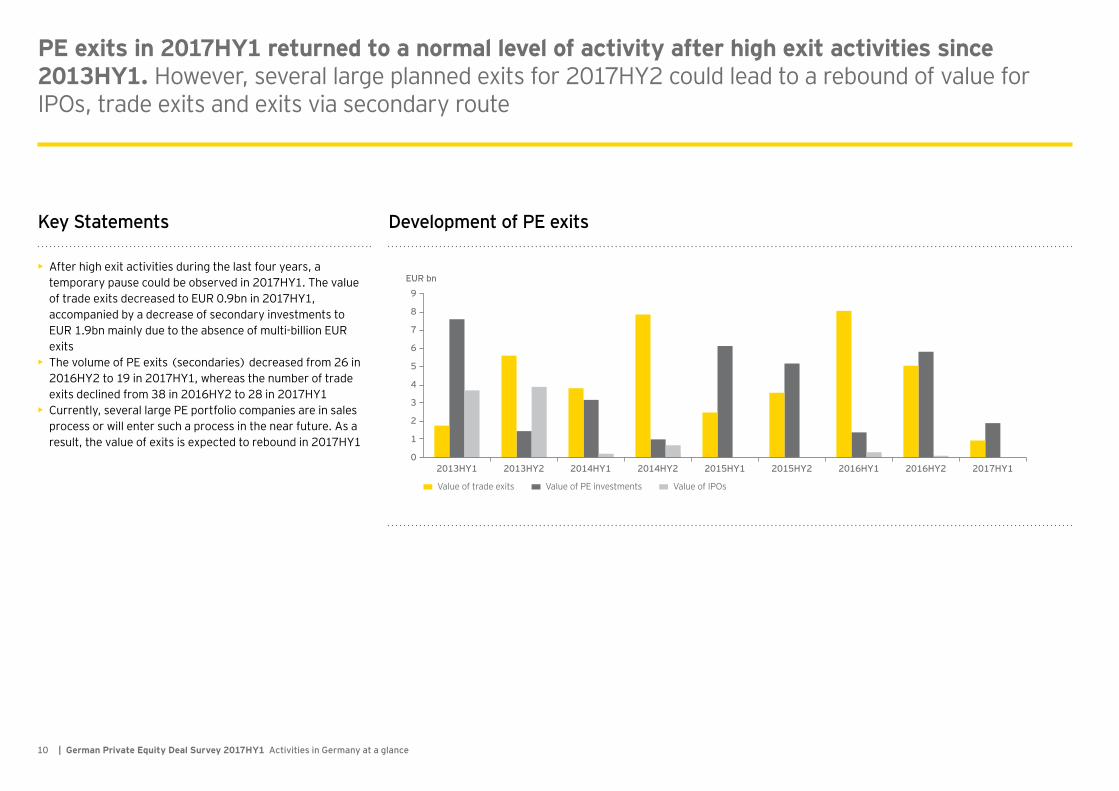

PE exits in 2017HY1 returned to a normal level of activity after high exit activities since 2013HY1. However, several large planned exits for 2017HY2 could lead to a rebound of value for IPOs, trade exits and exits via secondary route

Key Statements

• After high exit activities during the last four years, a temporary pause could be observed in 2017HY1. The value of trade exits decreased to EUR 0.9bn in 2017HY1, accompanied by a decrease of secondary investments to EUR 1.9bn mainly due to the absence of multi-billion EUR exits

• The volume of PE exits (secondaries) decreased from 26 in 2016HY2 to 19 in 2017HY1, whereas the number of trade exits declined from 38 in 2016HY2 to 28 in 2017HY1

• Currently, several large PE portfolio companies are in sales process or will enter such a process in the near future. As a result, the value of exits is expected to rebound in 2017HY1

Development of PE exits

9

7

6

4

2

0

1

3

5

8

2013HY1 2013HY2 2014HY1 2014HY2 2015HY1 2015HY2 2016HY1

Value of trade exits Value of PE investments Value of IPOs

EUR bn

2016HY2 2017HY1

10 | German Private Equity Deal Survey 2017HY1 Activities in Germany at a glance

Average PE portfolio holding period remained broadly stable since 2013. Following the consistent trend since 2015HY1, the average holding period remains on a level of 72 months on average in 2017HY1

Key Statements

• The graph shows the development of the average holding period for PE portfolio companies (exited) compared to the number of exits in the respective period

• Average holding period for portfolio companies remained stable at 72 months in 2016HY2 and 2017HY1 respectively

• The increasing average holding period is in line with the increasing long term focus of PEs on creating sustainable growth and value

• The total number of exits decreased from 64 in 2016HY2 to 47 exits in 2017HY1 due to some temporary effects and proposed shift of sales processes to 2017HY2

Development of average holding period of PE portfolio companies

70

30

10

0

Avg. Holding period (months) # Exits

2013HY1 2013HY2 2014HY1 2014HY2 2015HY1 2015HY2 2016HY1

20

40

months

2016HY2 2017HY1

50

60

90

70

60

40

20

0

10

30

50

80

# exits

11German Private Equity Deal Survey 2017HY1 Activities in Germany at a glance |

Special: FIDS – Compliance Due Diligence Services

12 | German Private Equity Deal Survey 2017HY1 Activities in Germany at a glance

Today’s businesses are operating in an uncertain economic environment

„ I am convinced there are only two types of companies: those that have been hacked and those that will be.” Robert Mueller (Former FBI Director)

44%

62%86%

report increasing level of concern over

“bribery and corruption risk.”(EY Global FDA Survey 2016)

report increasing level of concern over „cyber breach

or insider threat.“(EY Global FDA Survey 2016)

say their cybersecurity function does not fully meet their organization’s needs

(EY GISS 2016 – 17)

13German Private Equity Deal Survey 2017HY1 Activities in Germany at a glance |

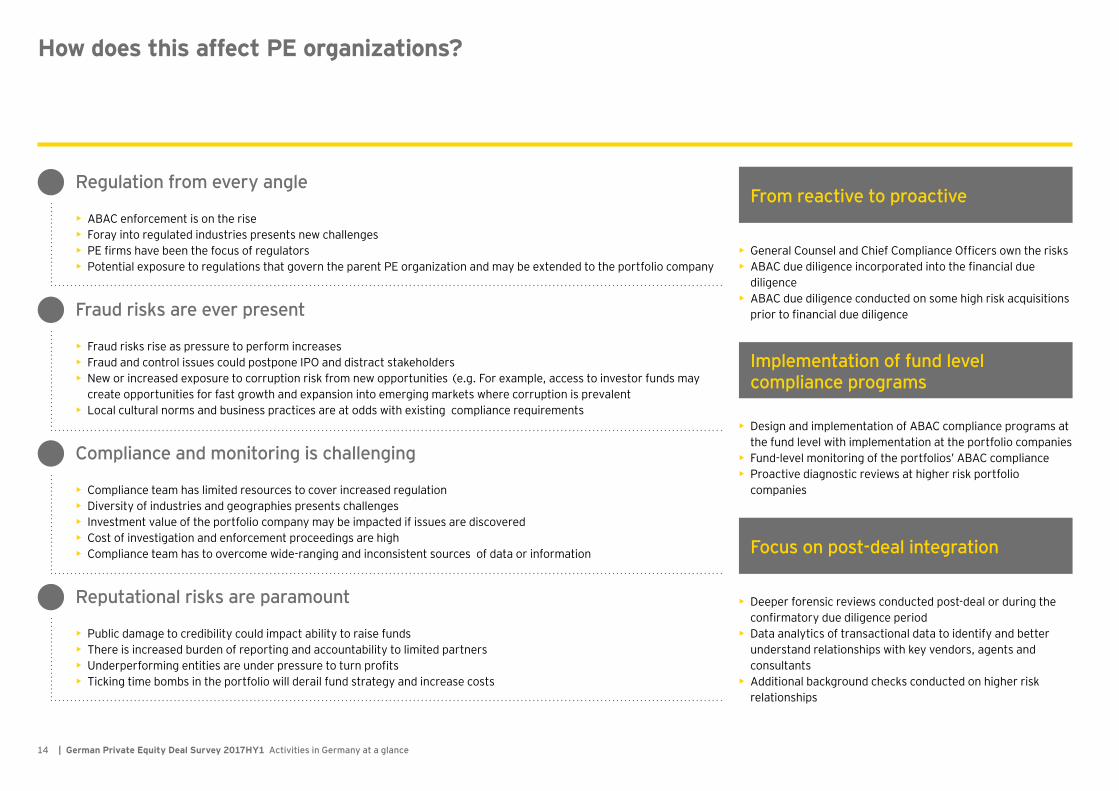

How does this affect PE organizations?

• ABAC enforcement is on the rise• Foray into regulated industries presents new challenges• PE firms have been the focus of regulators• Potential exposure to regulations that govern the parent PE organization and may be extended to the portfolio company

• Fraud risks rise as pressure to perform increases• Fraud and control issues could postpone IPO and distract stakeholders• New or increased exposure to corruption risk from new opportunities (e.g. For example, access to investor funds may

create opportunities for fast growth and expansion into emerging markets where corruption is prevalent• Local cultural norms and business practices are at odds with existing compliance requirements

• Compliance team has limited resources to cover increased regulation• Diversity of industries and geographies presents challenges• Investment value of the portfolio company may be impacted if issues are discovered• Cost of investigation and enforcement proceedings are high• Compliance team has to overcome wide-ranging and inconsistent sources of data or information

• Public damage to credibility could impact ability to raise funds • There is increased burden of reporting and accountability to limited partners• Underperforming entities are under pressure to turn profits • Ticking time bombs in the portfolio will derail fund strategy and increase costs

• General Counsel and Chief Compliance Officers own the risks• ABAC due diligence incorporated into the financial due

diligence• ABAC due diligence conducted on some high risk acquisitions

prior to financial due diligence

• Design and implementation of ABAC compliance programs at the fund level with implementation at the portfolio companies

• Fund-level monitoring of the portfolios’ ABAC compliance• Proactive diagnostic reviews at higher risk portfolio

companies

• Deeper forensic reviews conducted post-deal or during the confirmatory due diligence period

• Data analytics of transactional data to identify and better understand relationships with key vendors, agents and consultants

• Additional background checks conducted on higher risk relationships

Implementation of fund level compliance programs

Focus on post-deal integration

From reactive to proactiveRegulation from every angle

Fraud risks are ever present

Compliance and monitoring is challenging

Reputational risks are paramount

14 | German Private Equity Deal Survey 2017HY1 Activities in Germany at a glance

Transaction related to FIDS services

Many transactions are followed by significant challenges that may include the identification of potential fraud, compliance or disclosure issues that can harm business profitability and pose potential liability. Addressing this universe of risks requires in-depth knowledge of fraud and corruption; highly specialized investigative, dispute and industry experience; and a thorough understanding of the concerns and needs of each party to a transaction.

We have developed a set of solutions that provides integrity diligence and compliance due diligence support, investigative, anti-fraud, and forensic technology support in the early stages, during and after signing and closing, a broad spectrum of compliance advisory during integration and value creation phase plus overall the services and solution portfolio of Fraud Investigation & Dispute Services/Compliance Management portfolio.

Pre-transaction Post-transactionSigning & Closing

• Fraud-risk assessment based on target’s sector and/or business model

• Target Integrity Checks: preliminary integrity diligence of related parties and/or top-management (open source background check)

• Forensic data analysis of Financial and ERP data to verify financial DD or KPI for earn out

• Document reviews• Forensic interviews• Background checks• Forensic data freeze• In-depth data analytics with focus on ERP data, e.g.:

• Anti-Bribery, Anti-Corruption analytics• Analysis of transactions with respect to Asset

Misappropriations• Check for patterns of Financial Statement Fraud• Intercompany analytics

• Consultancy on the development of an anti-corruption compliance program or integration support

• Support with the implementation of IT-based continuous monitoring solutions

• Investigation of selected issues, i.e. cartel involvement based on forensic tool set:• Interviews• Email-Review• Compliance-Audit• In-depth data analysis of key issues from forensic

look back and identified red flags• Detailed review of high-risk transactions and

supporting documents

• Initial cyber risk assessment• Forensic data analytics and other technology-

enhanced electronic-data review• Data Freeze: Preserving valuable data

• Compliance Interviews• Data room review (compliance focused)• Compliance–questionnaire – assessment on response• Pre-signing and anti-corruption analytics• Analysis of relevant contract terms, definitions,

schedules and construction of accounting mechanisms• Antitrust Discovery Services, including high-volume,

time-sensitive electronic data review capabilities

Strategic and pre-transaction planning Post-closing activities – Integrity Assessment & post-closing analytics

Negotiation and execution

Post-acquisition / Transaction Effectiveness

Follow-up activities – Investigation, Anti-Fraud & Cyber

Forensic Analytics & Cyber

Integrity & Compliance Due Diligence activities

Many transactions are followed by significant challenges that may include the identification of potential fraud, compliance or disclosure issues that can harm business profitability and pose potential liability. Addressing this universe of risks requires in-depth knowledge of fraud and corruption; highly specialized investigative, dispute and industry experience; and a thorough understanding of the concerns and needs of each party to a transaction.

We have developed a set of solutions that provides integrity diligence and compliance due diligence support, investigative, anti-fraud, and forensic technology support in the early stages, during and after signing and closing, a broad spectrum of compliance advisory during integration and value creation phase plus overall the services and solution portfolio of Fraud Investigation & Dispute Services/Compliance Management portfolio.

15German Private Equity Deal Survey 2017HY1 Activities in Germany at a glance |

Cyber Due Diligence

In the ever-changing environment, sophisticated cyber security is vital to a company‘s success. Before a merger or an acquisition, a thorough network examination is essential for both sides to detect and identify any network vulnerabilities, and accurately evaluate any potential risk as data may be gone in seconds and could never be recovered. Data freeze is a crucial step to maintain data at a particular moment in order to capture and preserve the data for future actions. Truth is deliberately hidden behind the scenes.

A cyber investigation could effectively protect both sides under a merger or an acquisition by providing a clearer picture or disclosing facts that might greatly impact the planned transaction. The General Data Protection Regulation (GDPR) will come into force in May 2018, which aims to protect all EU citizens from privacy and data breaches. Companies and organizations under merger or acquisition have to be prepared in order to meet the requirements of GDPR.

• Sample check on network health• On-site incident response to cyber attacks • Diagnosis and analysis on live network traffic• Network vulnerability and weaknesses identification

„Enabling cyber investigation, revealing hidden truth“

„Preserving valuable data, surviving legal possibilities“

„Identifying network vulnerability, safeguarding company‘s assets“

„Ensuring data protection, reducing company‘s risk“

GDPRReadiness

Assessment

Trainingto data

handling personnel

Penetrationtesting on

user accountpermissions

Incident Response (IR)

service partnership

Advice ondeveloping

IR frameworkand policies

Store securely in EY evidencevault

Identify relevant data source from data pool

Ensure data remains unaltered

Maintain chain of custody throughout the acquisition

Make forensic images of data, ensuring completeness and integrity

Make ready for possible investigation

DataFreeze

Identify

Acquire

PreserveStore

Deleted data retrieval and password cracking

Data culling, extraction, processing and hosting

IT Forensicanalysis on computers and mobiledevices

Report of findings, professional statement and expert witness in court

16 | German Private Equity Deal Survey 2017HY1 Activities in Germany at a glance

17German Private Equity Deal Survey 2017HY1 Activities in Germany at a glance |

SourcesSources The involvement of EY in PE investments

MergermarketThomson One UnquoteBloombergDeutsche Börse

• EY’s Transaction Advisory Services has over 9,500 professionals in 95 countries and approximately 1,100 dedicated people working for our Transaction Advisory Services team in our sub area GSA (Germany, Switzerland, Austria).

• Our success is based on working together in industry aligned teams. Our experienced global Transaction Advisory team is actively involved throughout the world in transactions among Private Equity houses and corporates. These transactions include acquisitions, divestitures and financings. Managing this process is a complex exercise that requires an acute awareness of the confidential nature of these types of transactions: leveraging a global network of Private Equity advisers and industry specialists with a deep understanding of the motivation, pricing and market dynamics of their respective industry sectors.

• EY employs a broad range of transaction professionals who advise on financial and tax due diligence, tax structuring, transaction integration as well as IT, pensions and operational due diligence.

18 | German Private Equity Deal Survey 2017HY1 Activities in Germany at a glance

19German Private Equity Deal Survey 2015HY2 Activities in Germany at a glance |

Alexander Kron Managing Partner GSA Transaction Advisory Services Tel: +49 89 14331 17452 [email protected]

German Private Equity Deal Survey

Fraud Investigation & Dispute Services

Michael Kunz Market Segment Leader Private Equity GSATransaction Tax Tel: +49 6196 996 26253 [email protected]

Wolfgang TaudtePartnerTransaction Advisory ServicesTel: +49 6196 996 [email protected]

Bodo MesekePartnerBusiness Integrity & Corporate Compliance Tel: +49 6196 996 22174 [email protected]

Christian HackoberSenior ConsultantTransaction Advisory ServicesTel: +49 6196 996 [email protected]

Christian MuthPartnerBusiness Integrity & Corporate Compliance Tel: +49 6196 996 [email protected]

Contacts

EY | Assurance | Tax | Transactions | Advisory

About the global EY organizationThe global EY organization is a leader in assurance, tax, transaction and advisory services. We leverage our experience, knowledge and services to help build trust and confidence in the capital markets and in economies the world over. We are ideally equipped for this task – with well trained employees, strong teams, excellent services and outstanding client relations. Our global purpose is to drive progress and make a difference by building a better working world – for our people, for our clients and for our communities.

The global EY organization refers to all member firms of Ernst & Young Global Limited (EYG). Each EYG member firm is a separate legal entity and has no liability for another such entity’s acts or omissions. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information, please visit www.ey.com.

In Germany, EY has 21 locations. In this publication, “EY” and “we” refer to all German member firms of Ernst & Young Global Limited.

© 2017 Ernst & Young GmbH WirtschaftsprüfungsgesellschaftAll Rights Reserved.

GSA Agency SKN 1707-068ED None

This publication contains information in summary form and is therefore intended for general guidance only. Although prepared with utmost care this publication is not intended to be a substitute for detailed research or the exercise of professional judgment. Therefore no liability for correctness, completeness and/or currentness will be assumed. It is solely the responsibility of the readers to decide whether and in what form the information made available is relevant for their purposes. Neither Ernst & Young GmbH Wirtschaftsprüfungsgesellschaft nor any other member of the global EY organization can accept any responsibility. On any specific matter, reference should be made to the appropriate advisor.

www.de.ey.com

![Lecture – 3 Dr. Zahoor Ali Shaikh 1. What is Anemia? Anemia means - Decreased hemoglobin - Decreased RBC count - Decreased Hematocrit [PCV] Therefore,](https://static.fdocuments.in/doc/165x107/56649c9e5503460f9495e870/lecture-3-dr-zahoor-ali-shaikh-1-what-is-anemia-anemia-means-decreased.jpg)