Gerling Global Financial Products Pricing Structured Finance, Project Finance and Credit Enhancement...

30

Gerling Global Financial Products Pricing Structured Finance, Project Finance and Credit Enhancement Paul R. Hussian, FCAS Seminar on Reinsurance June 15, 2000

-

date post

21-Dec-2015 -

Category

Documents

-

view

215 -

download

0

Transcript of Gerling Global Financial Products Pricing Structured Finance, Project Finance and Credit Enhancement...

Gerling Global Financial Products

Pricing Structured Finance, Project Financeand Credit Enhancement

Paul R. Hussian, FCAS

Seminar on Reinsurance

June 15, 2000

Gerling Global Financial Products

Transaction Examples

• Trade Receivables

• Debt pools: Bonds (CBO), Bank Loans (CLO)

• Entertainment: Film Receivables

• Real estate finance: Commercial and residential mortgages (MBS)

• ...

Gerling Global Financial Products

Corporate Debt Ratings

Moody's S&P

Aaa AAAAa1 AA+Aa2 AAAa3 AA-A1 A+A2 AA3 A-

Baa1 BBB+Baa2 BBBBaa3 BBB-Ba1 BB+Ba2 BBBa3 BB-B1 B+B2 BB3 B-

Caa CCC

* Ratings reflect both frequency and severity of default

Gerling Global Financial Products

Structure

Assets(Collateral)

Receivables

Bonds,Corp Loans,Mortgages

Films

Real Estate

CashFlow

Aaa

Tranches

Senior 1

Senior 2

Mezzanine

Equity

Ba3

NR

Aa2

(Insurer)

Pari Passu

Equity

Unwrapped Notes

Insurer

Aa2 Aa2

NR

Structure 1 Structure 2

Gerling Global Financial Products

Two Pricing Perspectives

• Actuarial/Insurance

– premium

• Capital Markets

– yield spread: over Treasuries/LIBOR

Gerling Global Financial Products

Actuarial/Insurance Pricing

• Identify assets/cash flows

• Identify risk(s)

• Gather data

• Build cash flow model

• Run cash flows through deal structure

• Determine Premium, Profit, ROE

Gerling Global Financial Products

Assets / Cash Flows

• Receivables Collection cycle

• CBO/CLO Pools of debt (bonds, bank loans)

• Entertainment Film receipts

• Real estate Commercial/residential property

Gerling Global Financial Products

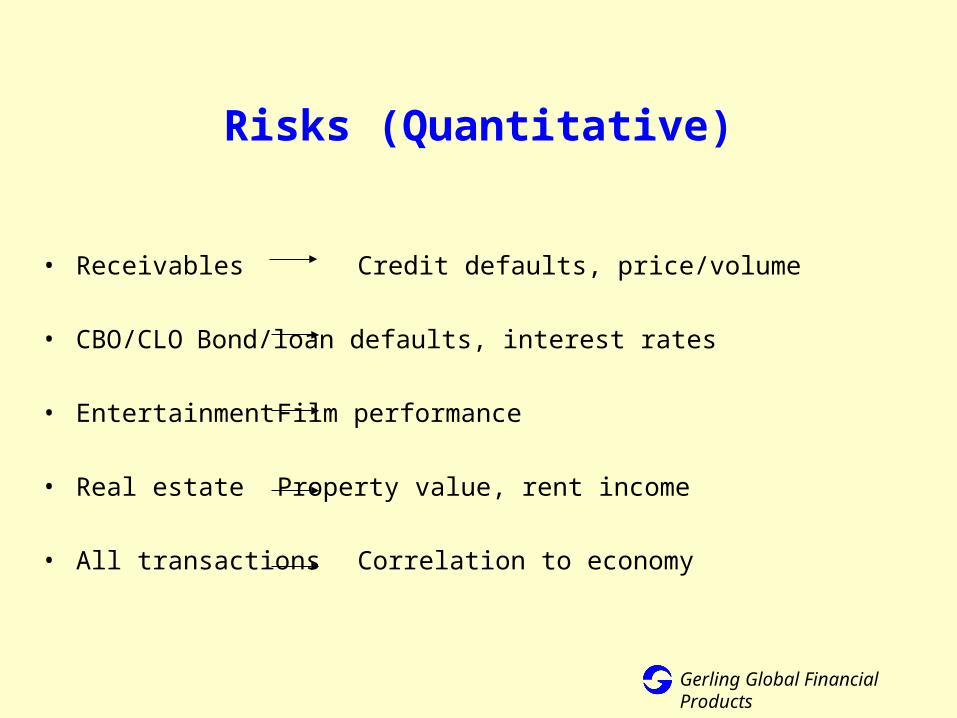

Risks (Quantitative)

• Receivables Credit defaults, price/volume

• CBO/CLO Bond/loan defaults, interest rates

• Entertainment Film performance

• Real estate Property value, rent income

• All transactions Correlation to economy

Gerling Global Financial Products

Data Sources

• Commodities Commodities futures exchange, Bloomberg,

company

• CBO/CLO Moody’s, S&P, sponsoring bank/company

• Entertainment MPAA, company

• Real estate Company, FHA, FDIC, private industry study

• All transactions Offering Memorandum

Gerling Global Financial Products

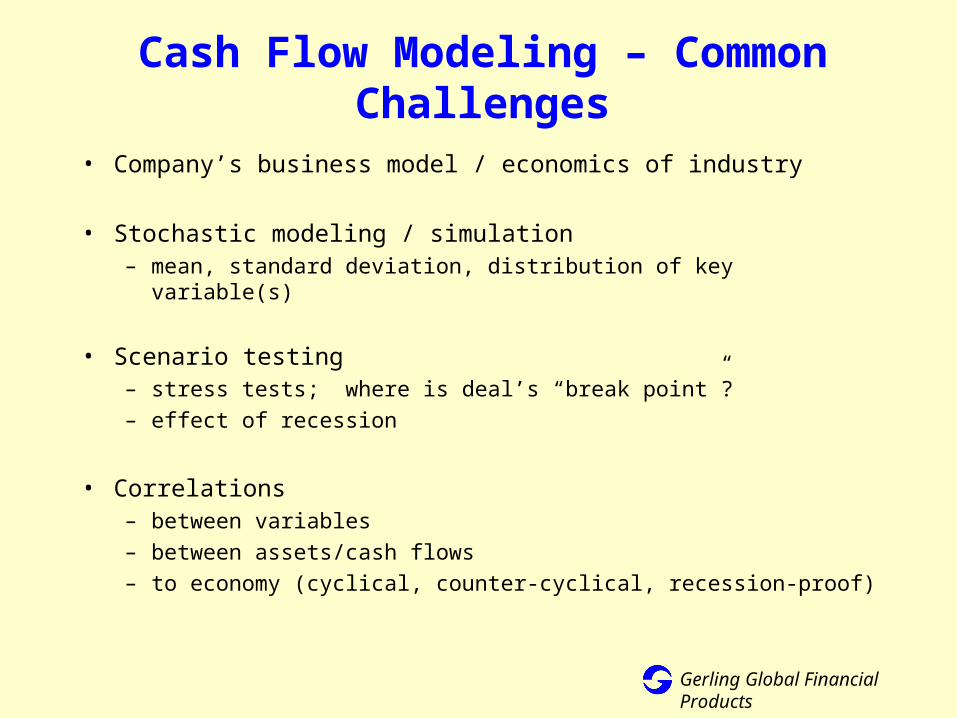

Cash Flow Modeling – Common Challenges

• Company’s business model / economics of industry

• Stochastic modeling / simulation– mean, standard deviation, distribution of key variable(s)

• Scenario testing– stress tests; where is deal’s “break point”?

– effect of recession

• Correlations– between variables

– between assets/cash flows

– to economy (cyclical, counter-cyclical, recession-proof)

Gerling Global Financial Products

Receivables - Cash Flows

• Credit defaults on receivables

– historical ratio: defaults receivables

– strength of obligors

• Price/volume of commodity being produced

– range of price fluctuation

– effect of recession on price, volume

– obligor concentration risk

Gerling Global Financial Products

Sample Receivables Loss Data

1.0

2.0

3.0

4.0

5.0

Pool Origination Date

% T

ota

l Lif

eti

me

Lo

ss

es

Historically 3%, stable

Historically 3%,

volatile

Increasing Loss

Trend

Gerling Global Financial Products

Receivables – Sample Average Monthly Price Data (Heavy Crude Oil)

$5

$10

$15

$20

$25

Jan-

91

Jul-9

1

Jan-

92

Jul-9

2

Jan-

93

Jul-9

3

Jan-

94

Jul-9

4

Jan-

95

Jul-9

5

Jan-

96

Jul-9

6

Jan-

97

Jul-9

7

Jan-

98

Jul-9

8

Jan-

99

Jul-9

9

US

$/ba

rrel

Gerling Global Financial Products

CBO/CLO – Cash Flows(Default Rates)

• Default Rate (frequency) = % of bonds/loans defaulting

– Annual, multi-year

• Moody’s/S&P credit ratings of bonds/loans in portfolio (Aaa, Aa1, …)

• Correlation between bonds/loans

– Diversity Score: translate portfolio into homogeneous, independent debt

securities

• Binomial distribution

Gerling Global Financial Products

CBO/CLO – Cash Flows (Severity)

• Severity = 1 - Recovery Rate

• Recovery Rate = post-default market value par value

• Moody’s/S&P credit ratings of portfolio notes (Aaa, Aa1, …)

• Normal, Lognormal distribution

• Correlation between frequency, severity

• Loss rate = Default rate x Severity

Gerling Global Financial Products

One-Year Default Rates by Year and Rating

Aaa

Aa

A

Baa

Ba

B

0.00

5.00

10.00

15.00

20.00

25.00

Defa

ult

Rate

%

Year

Gerling Global Financial Products

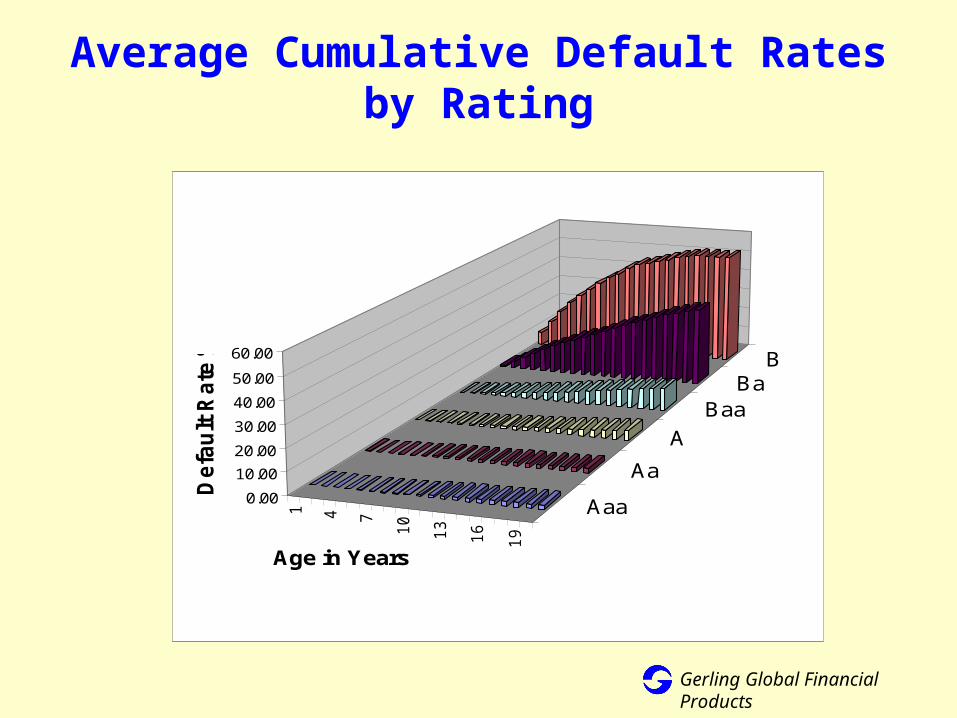

Average Cumulative Default Rates by Rating

1 4 7

10

13

16

19

Aaa

Aa

A

BaaBa

B

0.00

10.00

20.00

30.00

40.00

50.00

60.00

Defa

ult

Rate

%

Age in Years

Gerling Global Financial Products

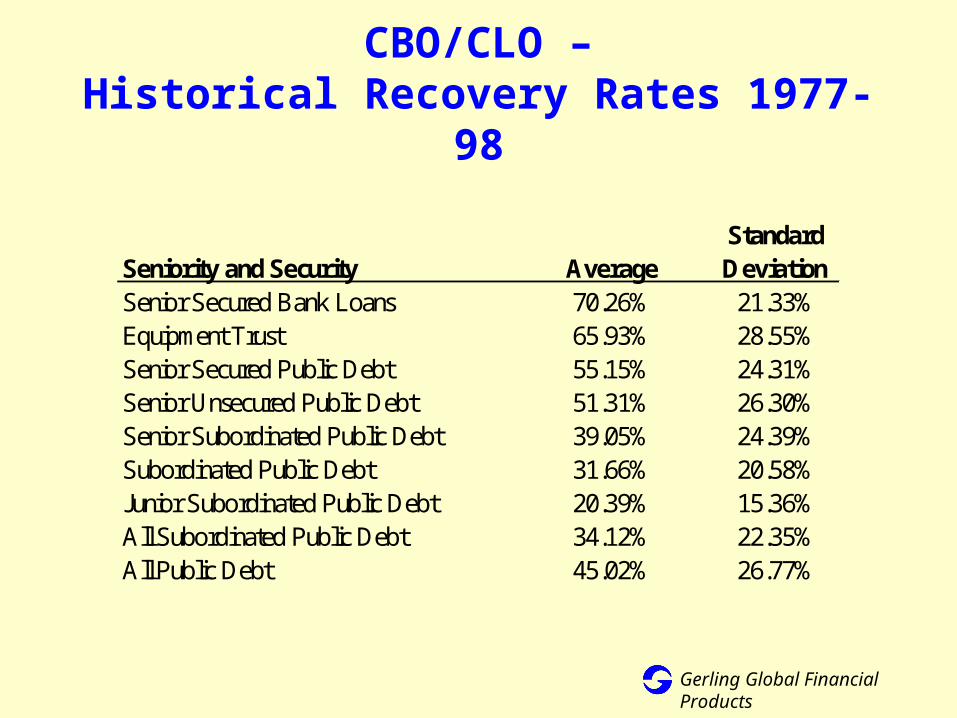

CBO/CLO –Historical Recovery Rates 1977-98

Seniority and Security AverageStandard Deviation

Senior Secured Bank Loans 70.26% 21.33%Equipment Trust 65.93% 28.55%Senior Secured Public Debt 55.15% 24.31%Senior Unsecured Public Debt 51.31% 26.30%Senior Subordinated Public Debt 39.05% 24.39%Subordinated Public Debt 31.66% 20.58%Junior Subordinated Public Debt 20.39% 15.36%All Subordinated Public Debt 34.12% 22.35%All Public Debt 45.02% 26.77%

Gerling Global Financial Products

CBO/CLO – Moody’s Diversity Score

• Avg default rate = p, Diversity score = n, Recovery rate = r– p = weighted avg of individual bond default rates

• n selected to equate loss variance

• Decreasing n increasing volatility & correlation– binomial C.V. =

– n depends on industry concentration

• S&P method: increase p with industry concentration, assume independence

np

p1

Gerling Global Financial Products

CBO/CLO - Example

# bonds = 5par value = 60,000,000

p = 5.0%n = 3 r = 50%

# of BinomialDefaults Prob Loss

0 85.7375% - 1 13.5375% 10,000,000 2 0.7125% 20,000,000 3 0.0125% 30,000,000

Expec Loss = 1,500,000 Loss Rate = 2.5%

Gerling Global Financial Products

Entertainment – Cash Flows (Film Co.)

• Coverage ratio = film revenue production cost– mean

– standard deviation

• Box office, licensing, pay-per-view, international

• Film revenue stream

• Correlation between films

Gerling Global Financial Products

Real Estate – Cash Flows

• Occupancy rates

• Average rents

• Capital structure (debt, equity)

• Property value

– cash flow discount rate

• Mortgages unrated, use industry data (FHA, FDIC)

• Strong correlation to economy

Gerling Global Financial Products

Modeling Deal Structure

• Tranched (layered) vs Syndicated (pari passu) securities

• Cash flow waterfall

• Equity, subordination structure

• Early amortization triggers

• Indemnification provisions

• Floating rates

• Impact on insurer’s profit & risk

Gerling Global Financial Products

Capital Markets Pricing

• Premium vs. yield spread between unwrapped notes and insurer credit rating

• Insurance vs. levered investment in unwrapped securities

(insurer = investor)

Gerling Global Financial Products

Current Spreads Over Treasuries (Financials)

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

8.00%

9.00%

Aaa

Aa1

Aa2

Aa3 A1 A2 A3

Baa1

Baa2

Baa3 Ba

1

Ba2

Ba3 B1 B2 B3 C

aa

3-yr

5-yr

10-yr

Investment Grade

Sub-Inv Grade

Gerling Global Financial Products

Example

5-yr bond: par value = $100M

insurer rating = Aa1 145 b.p. over T

unwrapped notes = Ba3 415 b.p.

over T

insurer premium = (415 – 145) b.p. x $100M =

$2.7M/yr

present value = $10.1M

Gerling Global Financial Products

Example

Levered Investment: Insurance:(1) (2) (3) (4)=(2)-(3) (1) (2) (3) (4)=(2)+(3)

(Ba3) (Aa1) (Aa1) (Ba3)Bond Insurer BondO/S Paid to Debt Insurer O/S Paid to Insurer Total

Year Principal Bond Service Profit Year Principal Bond Premium Paid0 100 0 1001 100 4.15 1.45 2.70 1 100 1.45 2.70 4.152 100 4.15 1.45 2.70 2 100 1.45 2.70 4.153 100 4.15 1.45 2.70 3 100 1.45 2.70 4.154 100 4.15 1.45 2.70 4 100 1.45 2.70 4.155 0 4.15 1.45 2.70 5 0 1.45 2.70 4.15

PV Profit--> $10.07 PV Profit--> $10.07

Aa1 spread = 1.45%Ba3 spread = 4.15%T = 6.50%

In $ millions

Gerling Global Financial Products

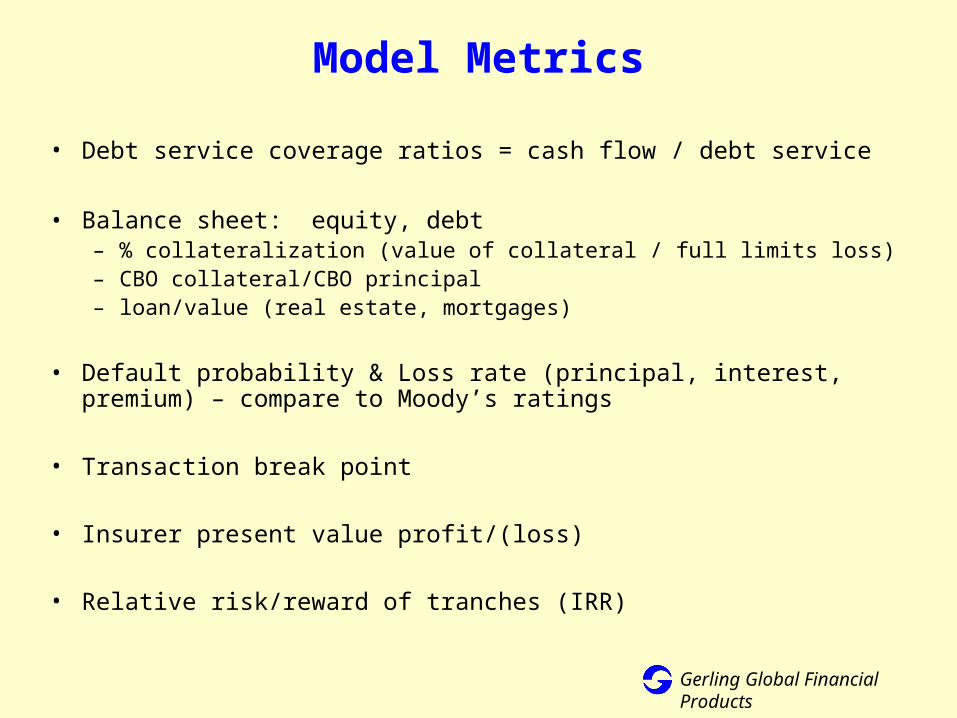

Model Metrics

• Debt service coverage ratios = cash flow / debt service

• Balance sheet: equity, debt– % collateralization (value of collateral / full limits loss)– CBO collateral/CBO principal– loan/value (real estate, mortgages)

• Default probability & Loss rate (principal, interest, premium) – compare to Moody’s ratings

• Transaction break point

• Insurer present value profit/(loss)

• Relative risk/reward of tranches (IRR)

Gerling Global Financial Products

CBO Example

p = 24.5% T = 6.5%r = 50.0% Expenses = 1.00%s.d. (r) = 25.6% Insurer Prem = 2.25%Maturity = 5 yrs Insurer Rating = Aa2

CashFlow

Aaa

Senior

CBO

3.50% + T

0.60% + T

$385 mm

$65 mm

$50 mmEquity

NR

Mezzanine(Insurer)

Ba2

Assets(Collateral)

50 Hi-Yield Bonds"Junk"

Avg Rating =

B1

Yield =4.10% + T

Par =$500 mm

Diversity = 30

Gerling Global Financial Products

Model Output

AllSenior Mezz Equity Tranches

Loss Rate 0.002% 4.238% 46.486% 10.179%

Insurer Expec Profit NA $2,789 $2,770 ($15,161)

Insurer ROE NA 18.0% 35.5% -17.4%

Insurer Loss Prob NA 16.5% 41.0% 77.4%

Rating Aaa Ba2 NR B1

Offered Spreads 0.60% 3.50% - 4.10%

Market Spreads 0.30%-0.60% 4.50%-5.00% - 4.00%-6.00%

All figures on present value basis.Results from 5000 iterations.In $000s.