GENEVA - UNECECNG price (1976-85) • Incentives/ subsidies continues • Funding for refuelling...

39

mm/y ©ENGVA, 2004 EMERGING MODELS of NGV MARKET DEVELOPMENT United Nations Working Party on Gas 20 January 2005 Dr. Jeffrey M. Seisler Executive Director GENEVA GENEVA

Transcript of GENEVA - UNECECNG price (1976-85) • Incentives/ subsidies continues • Funding for refuelling...

mm/y ©ENGVA, 2004

EMERGING MODELS of NGV MARKET DEVELOPMENT

United NationsWorking Party on Gas

20 January 2005Dr. Jeffrey M. Seisler

Executive Director

GENEVAGENEVA

mm/y ©ENGVA, 2004

GLOBAL NGV MARKET

mm/y ©ENGVA, 2004

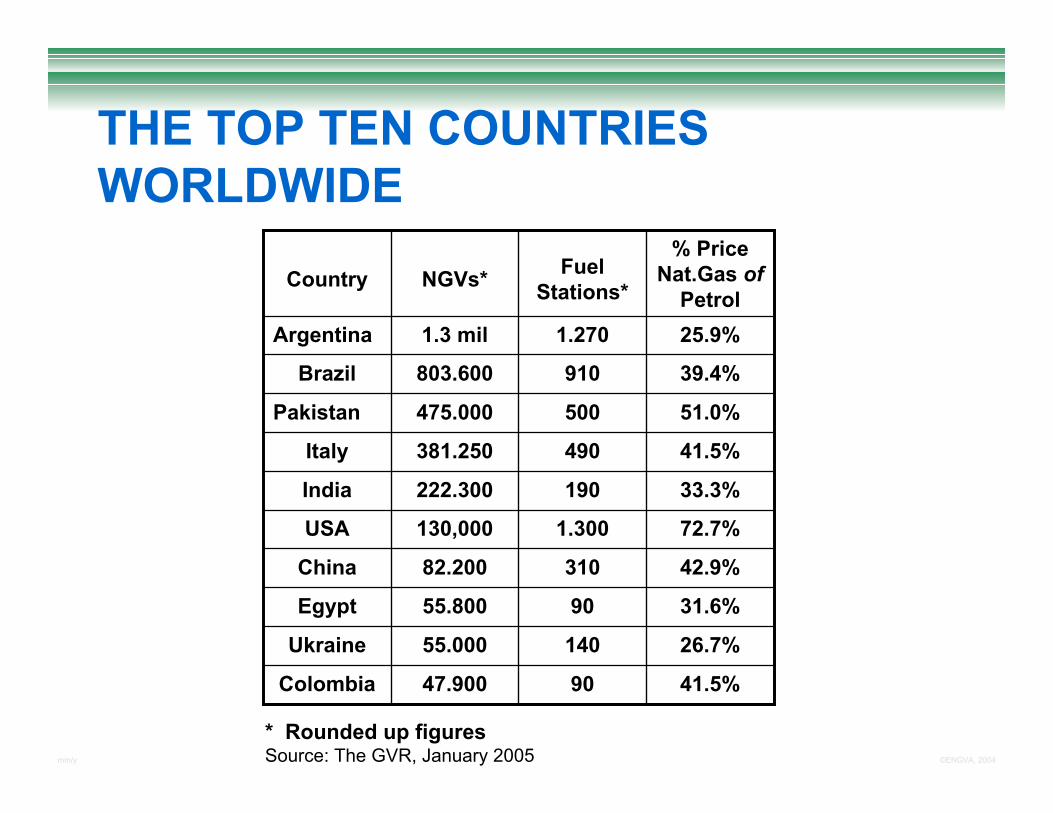

THE TOP TEN COUNTRIES WORLDWIDE

26.7%14055.000Ukraine

41.5%9047.900Colombia

31.6%9055.800Egypt

42.9%31082.200China

72.7%1.300130,000USA

33.3%190222.300India

41.5%490381.250Italy

51.0%500475.000Pakistan

39.4%910803.600Brazil

25.9%1.2701.3 milArgentina

% Price Nat.Gas of

PetrolFuel

Stations*NGVs*Country

January 2004 * Rounded up figuresSource: The GVR, January 2005

mm/y ©ENGVA, 2004

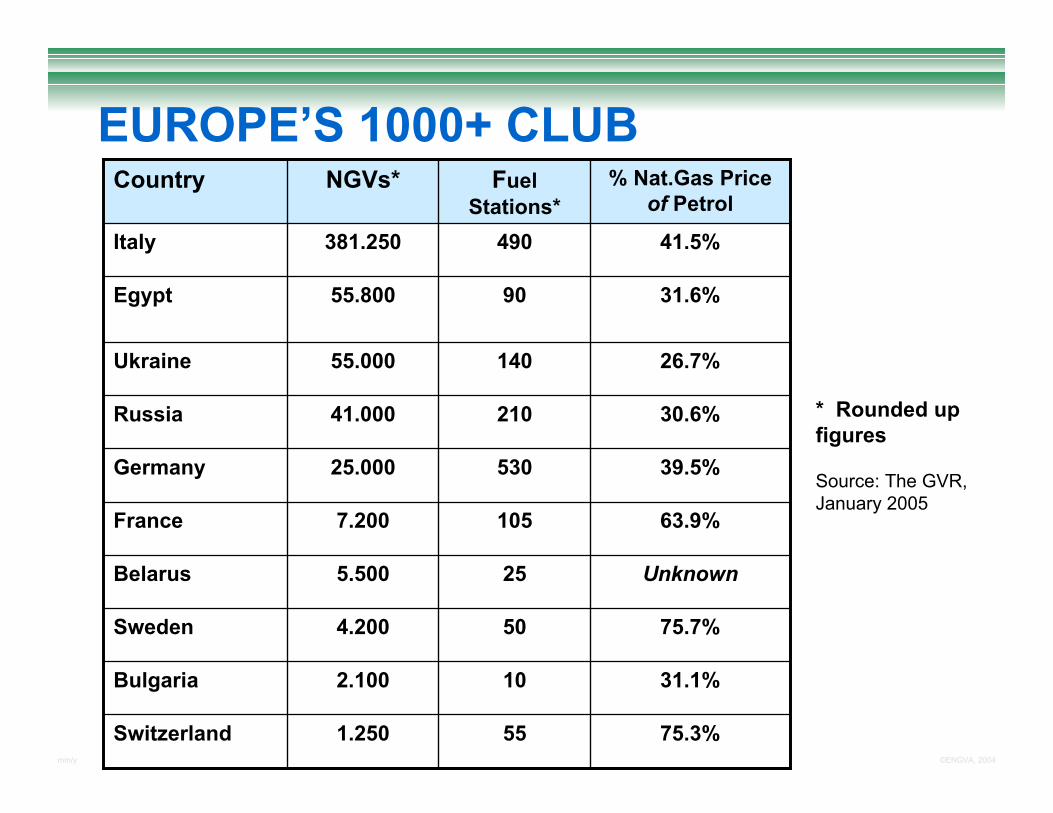

EUROPE’S 1000+ CLUB

26.7%14055.000Ukraine

31.1%102.100Bulgaria

75.3%551.250Switzerland

75.7%504.200Sweden

Unknown255.500Belarus

63.9%1057.200France

39.5%53025.000Germany

30.6%21041.000Russia

31.6%9055.800Egypt

41.5%490381.250Italy

% Nat.Gas Price of Petrol

Fuel Stations*

NGVs*Country

* Rounded up figures

Source: The GVR, January 2005

mm/y ©ENGVA, 2004

EUROPEAN COUNTRY MODELS

mm/y ©ENGVA, 2004

GOVERNMENT- STAKEHOLDERPARTNERSHIPS & POLICIES• Some national governments support NGVs

using ‘compacts’ with stakeholders– France– Germany– Italy– UK

• Other models & policies of government support are emerging– Sweden– Switzerland, etc

mm/y ©ENGVA, 2004

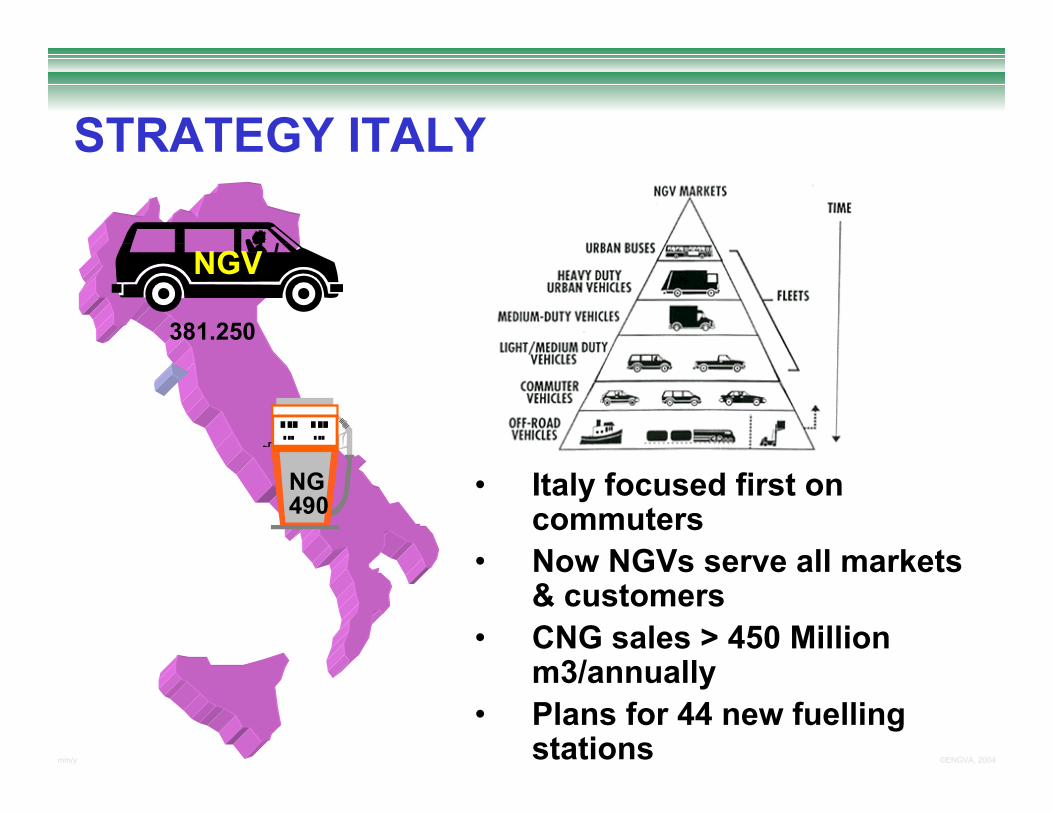

STRATEGY ITALY

• Italy focused first on commuters

• Now NGVs serve all markets & customers

• CNG sales > 450 Million m3/annually

• Plans for 44 new fuelling stations

NGV

NG

381.250

490

mm/y ©ENGVA, 2004

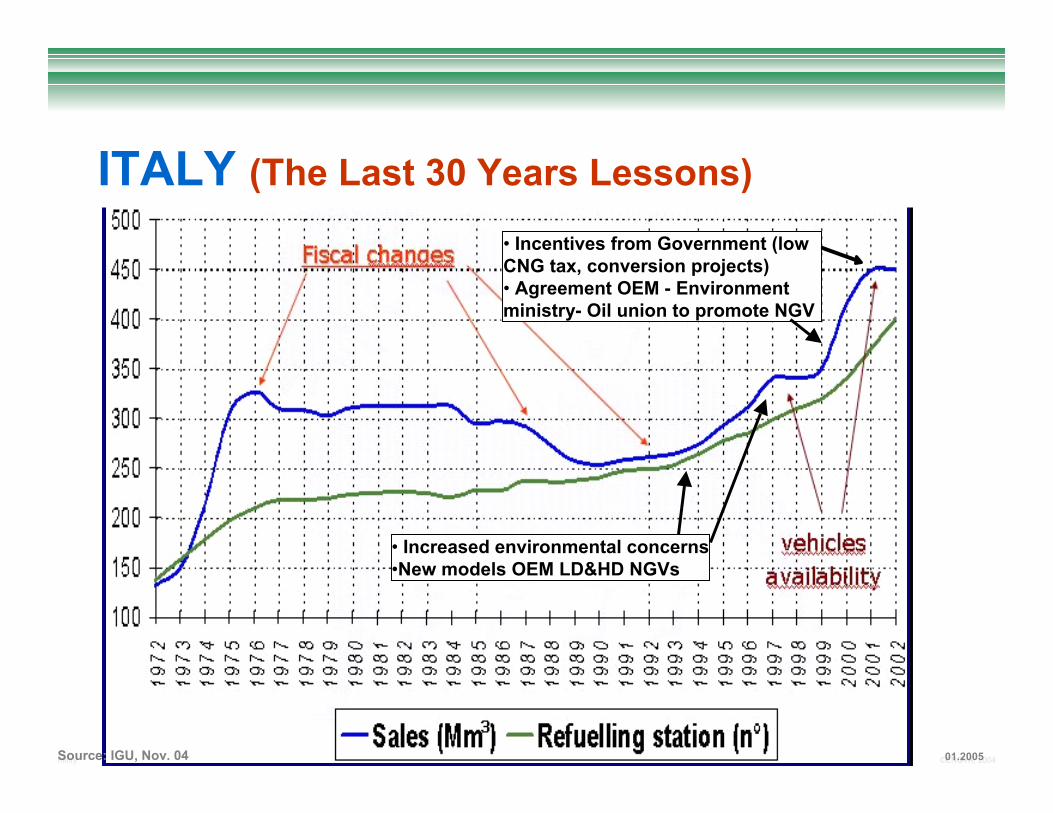

ITALY (The Last 30 Years Lessons)

• Increased environmental concerns•New models OEM LD&HD NGVs

• Incentives from Government (low CNG tax, conversion projects)• Agreement OEM - Environment ministry- Oil union to promote NGV

Source: IGU, Nov. 04 01.2005

mm/y ©ENGVA, 2004

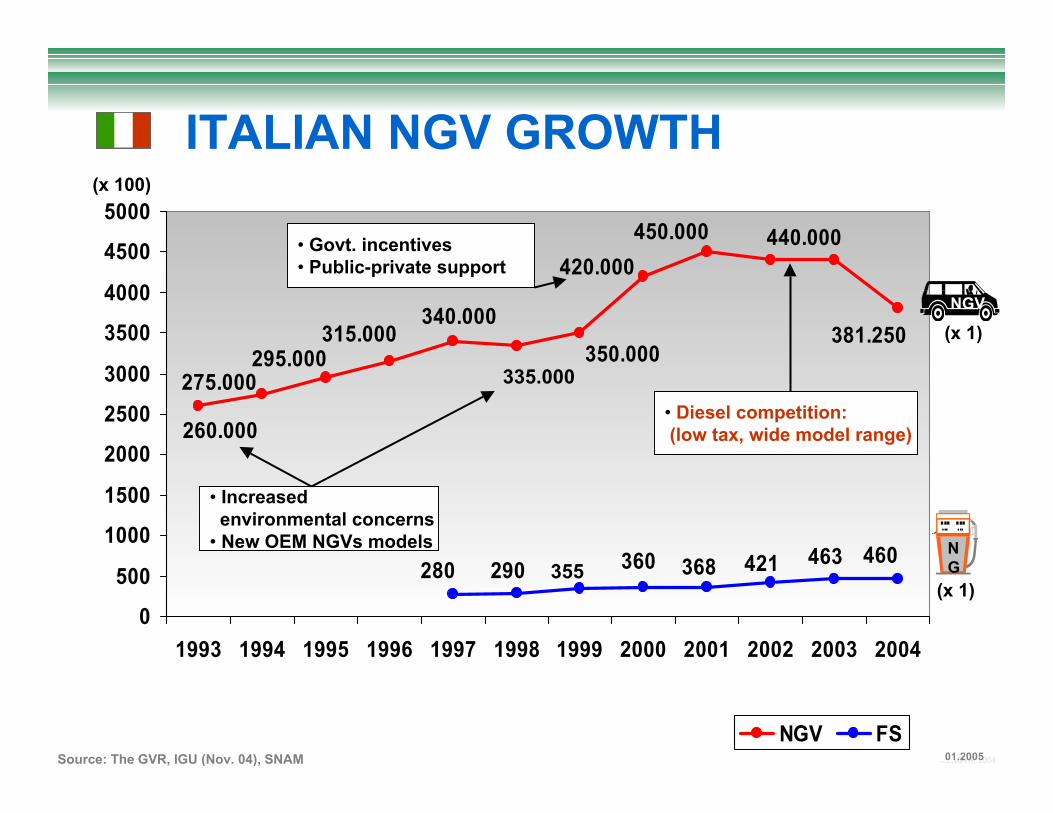

ITALIAN NGV GROWTH

440.000

381.250

275.000

260.000

295.000

450.000

340.000315.000

350.000

420.000

460463368360280 290 421

0

500

1000

1500

2000

2500

3000

3500

4000

4500

5000

1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

NGV FS

355

NGV

(x 1)

NG

(x 1)

Source: The GVR, IGU (Nov. 04), SNAM 01.2005

(x 100)

335.000

• Increased environmental concerns

• New OEM NGVs models

• Govt. incentives• Public-private support

• Diesel competition: (low tax, wide model range)

mm/y ©ENGVA, 2004

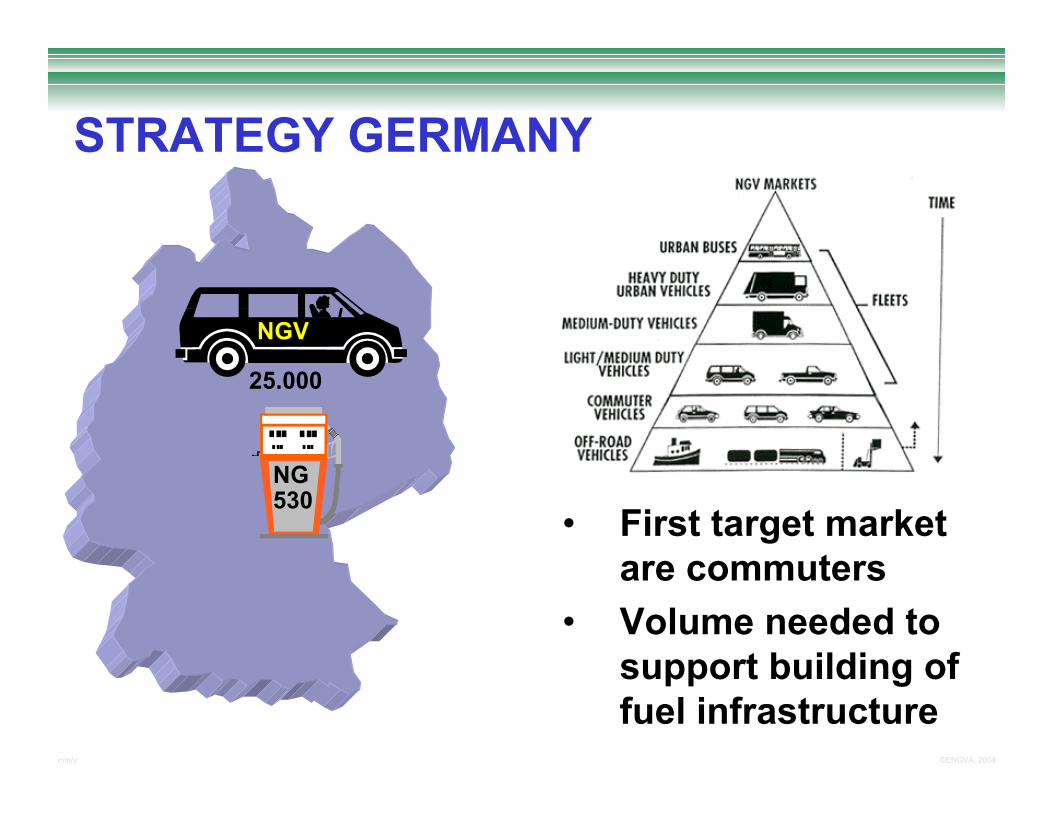

STRATEGY GERMANY

• First target market are commuters

• Volume needed to support building of fuel infrastructure

NGV

NG

25.000

530

mm/y ©ENGVA, 2004

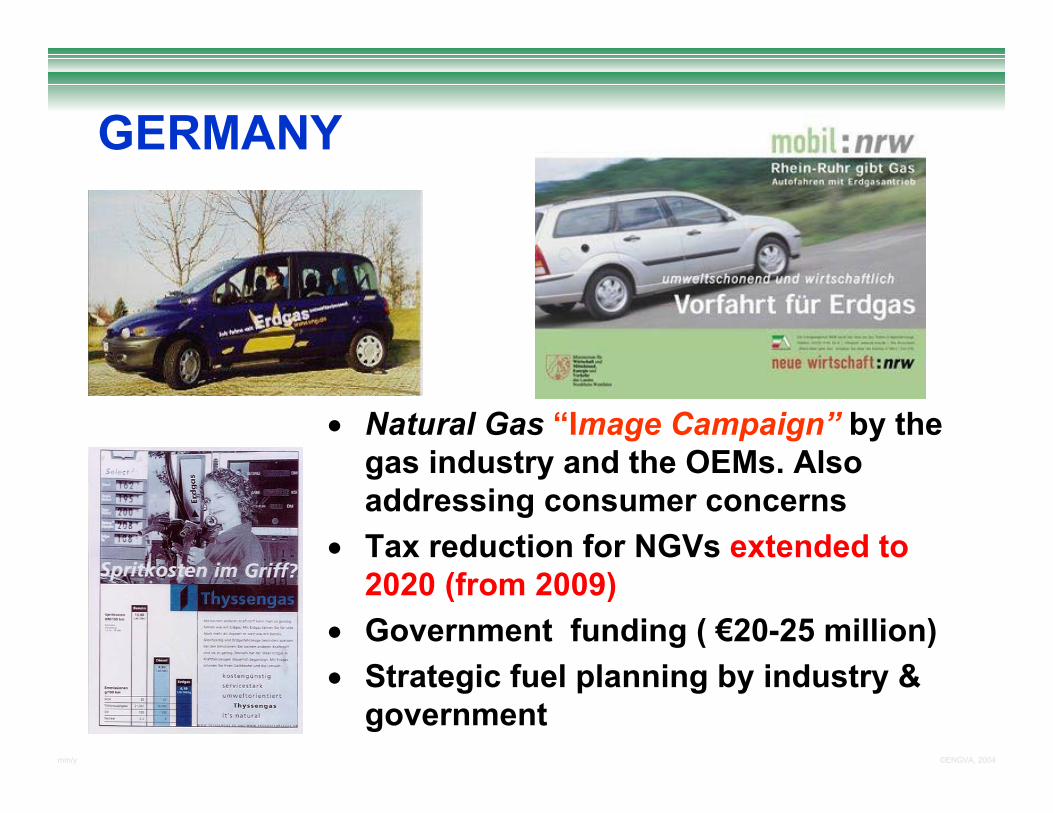

• Natural Gas “Image Campaign” by the gas industry and the OEMs. Also addressing consumer concerns

• Tax reduction for NGVs extended to 2020 (from 2009)

• Government funding ( €20-25 million)• Strategic fuel planning by industry &

government

GERMANY

mm/y ©ENGVA, 2004

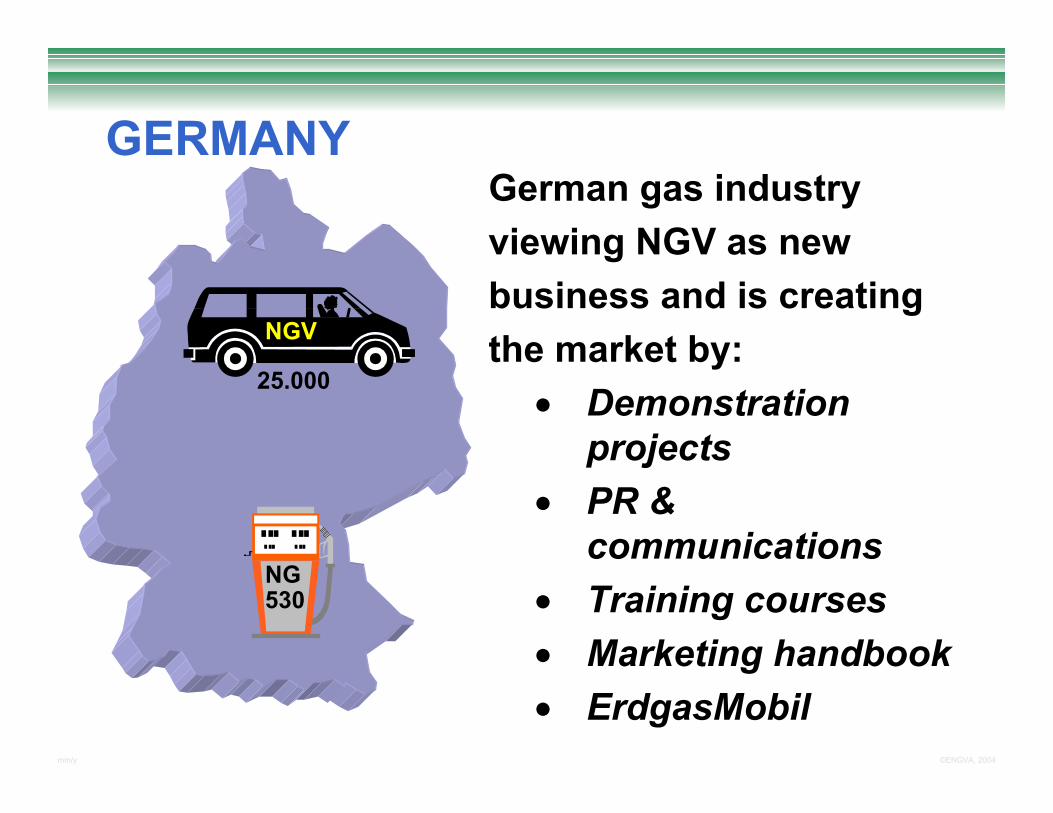

GERMANYGerman gas industryviewing NGV as newbusiness and is creating the market by:

• Demonstration projects

• PR & communications

• Training courses• Marketing handbook• ErdgasMobil

NGV

NG

25.000

530

mm/y ©ENGVA, 2004

GERMANY NGV GROWTH25.000

19.400

11.000

15.000

7.500

5.5004.200

3.0002.0001.000400

120100

80

250

190

14065

5035

530

390

0

5000

10000

15000

20000

25000

30000

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 20040

50

100

150

200

250

300

350

400

450

500

550

600

Number of natural gas vehicles Number of fuelling stations

NGV

(x 1)

NG

(x 1)

Source: IGU, Nov. 04 01.2005

• Reduced mineral oiltax (up to 2009)

• Political funding•1st OEM NGV (BMW)

• Increase oil prices• Sales incentives (OEM & gas industry)

• Establish ErdgasMobil (by gas & oil companies)

• Target 1.000 CNG stations• Fuel tax extension to 2020• More OEM NGVs

• More OEM NGV models• 1st NGVs with under floorgas tank

• Wide NG(V) campaign(public-private sectors)

mm/y ©ENGVA, 2004

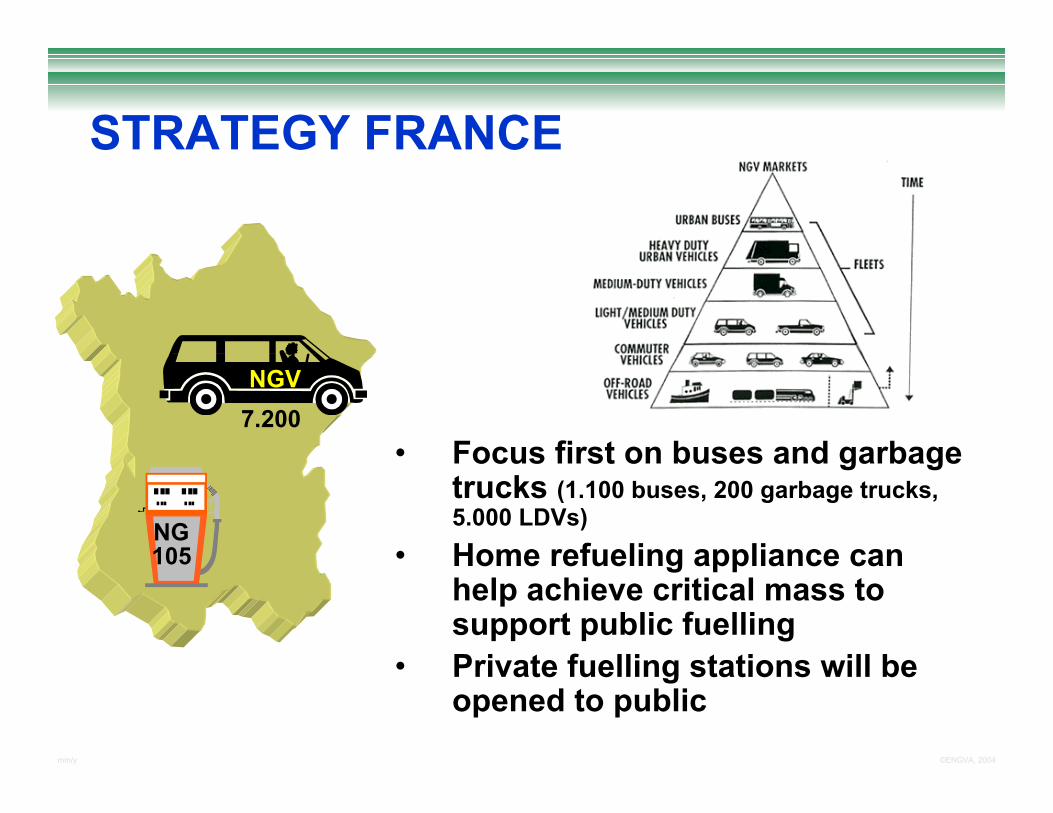

• Focus first on buses and garbage trucks (1.100 buses, 200 garbage trucks, 5.000 LDVs)

• Home refueling appliance can help achieve critical mass to support public fuelling

• Private fuelling stations will be opened to public

NGV7.200

NG105

STRATEGY FRANCE

mm/y ©ENGVA, 2004

FRANCE GROWTH MARKET

Strasbourg, France

Gaz de France fleet 3,500 NGVs & growing.

Largest gas company fleet in Europe

New! Fuelmaker:

“Phill”

20 municipalities have NGV bus fleets

mm/y ©ENGVA, 2004

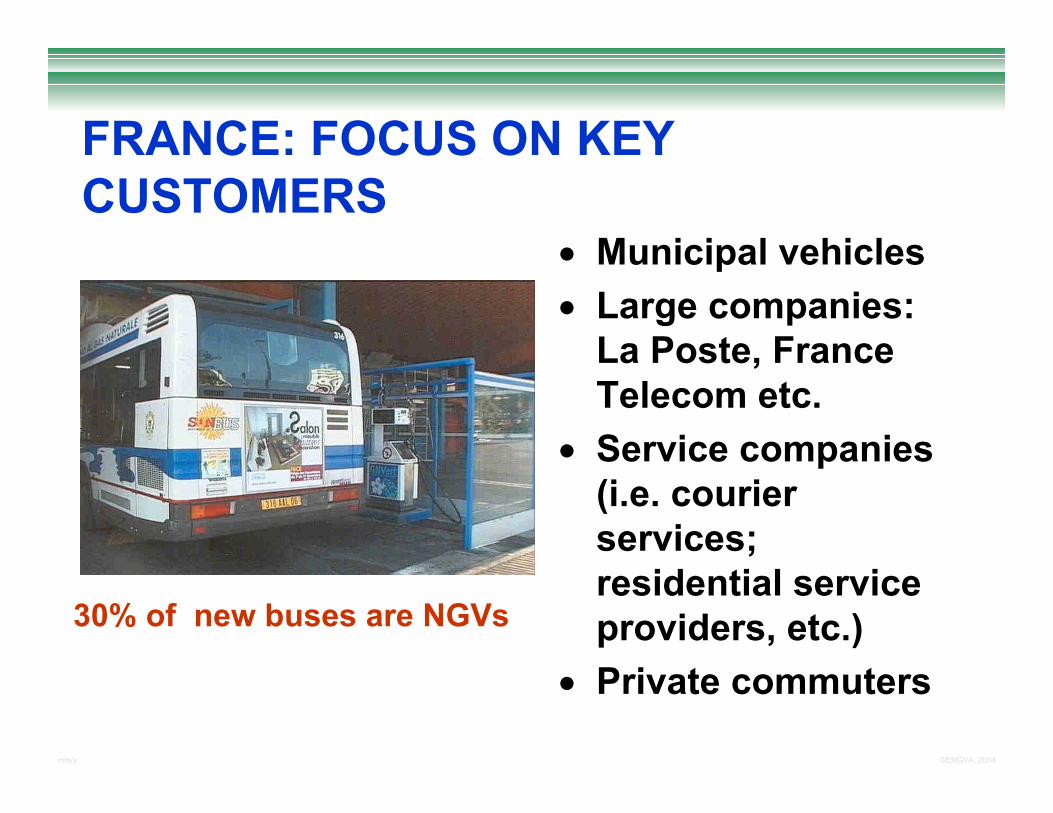

FRANCE: FOCUS ON KEY CUSTOMERS

• Municipal vehicles• Large companies:

La Poste, France Telecom etc.

• Service companies (i.e. courier services; residential service providers, etc.)

• Private commuters

30% of new buses are NGVs

mm/y ©ENGVA, 2004

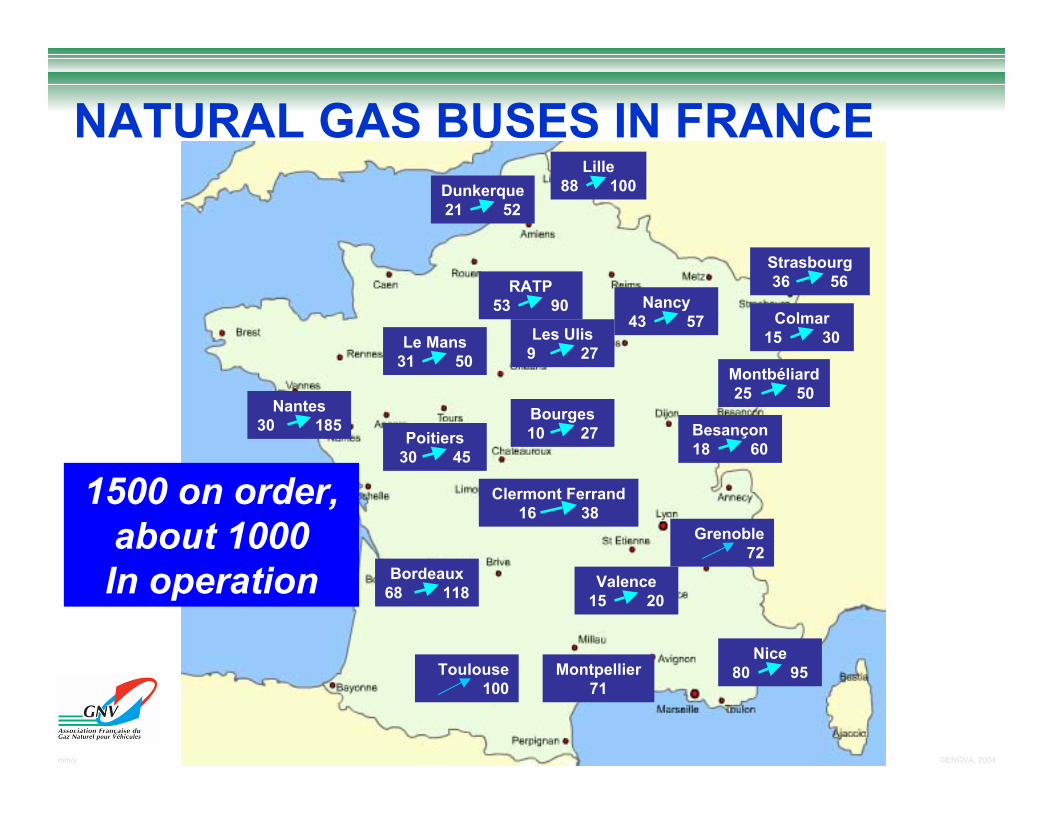

Strasbourg 36 56

Lille 88 100

Montbéliard 25 50

NATURAL GAS BUSES IN FRANCE

Le Mans 31 50

Nantes 30 185

Poitiers 30 45

Bordeaux 68 118

Clermont Ferrand 16 38

RATP 53 90

Les Ulis 9 27

Nancy 43 57

Dunkerque 21 52

Colmar 15 30

Besançon 18 60

Bourges 10 27

Valence 15 20

Grenoble 72

Toulouse 100

1500 on order,about 1000In operation

Nice 80 95Montpellier

71

mm/y ©ENGVA, 2004

• Governmental Support• Strong Gas industry support• OEMs producing NGVs• CNG price = -34% of petrol price

= -16% of diesel price Challenge

MARKET CONDITIONS

mm/y ©ENGVA, 2004

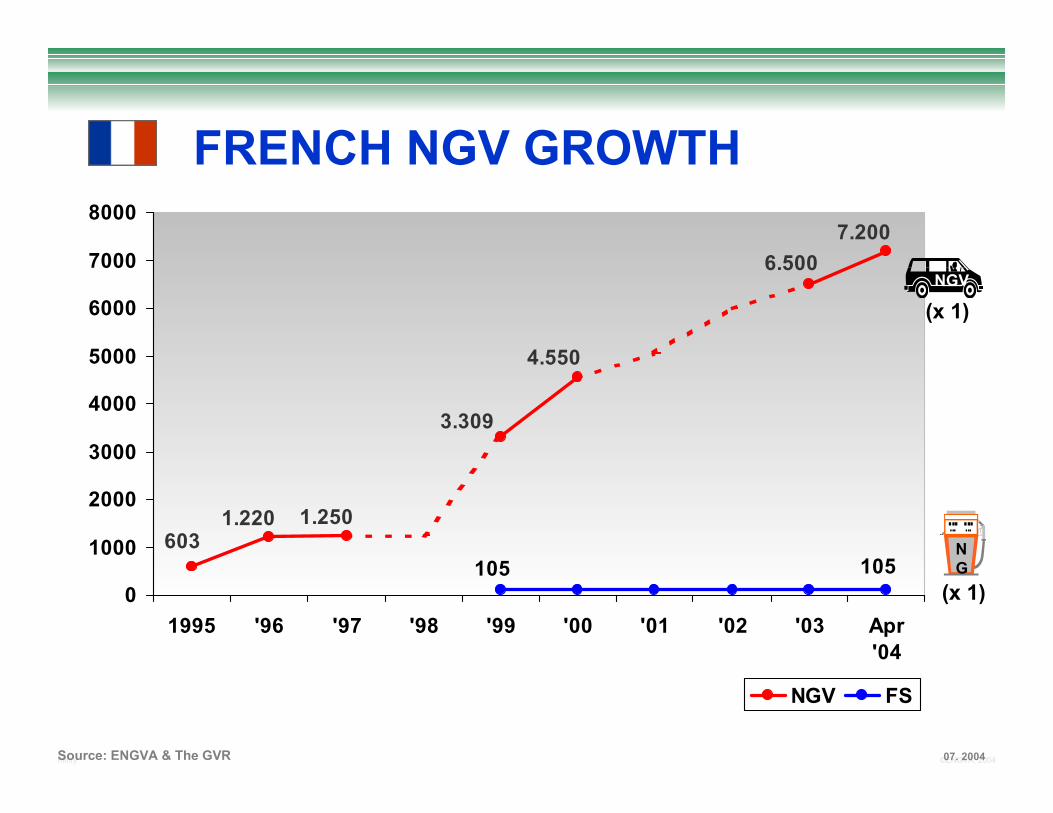

FRENCH NGV GROWTH

4.550

3.309

7.2006.500

1.250603

1.220

1051050

1000

2000

3000

4000

5000

6000

7000

8000

1995 '96 '97 '98 '99 '00 '01 '02 '03 Apr'04

NGV FS

NGV

(x 1)

NG

(x 1)

Source: ENGVA & The GVR 07. 2004

mm/y ©ENGVA, 2004

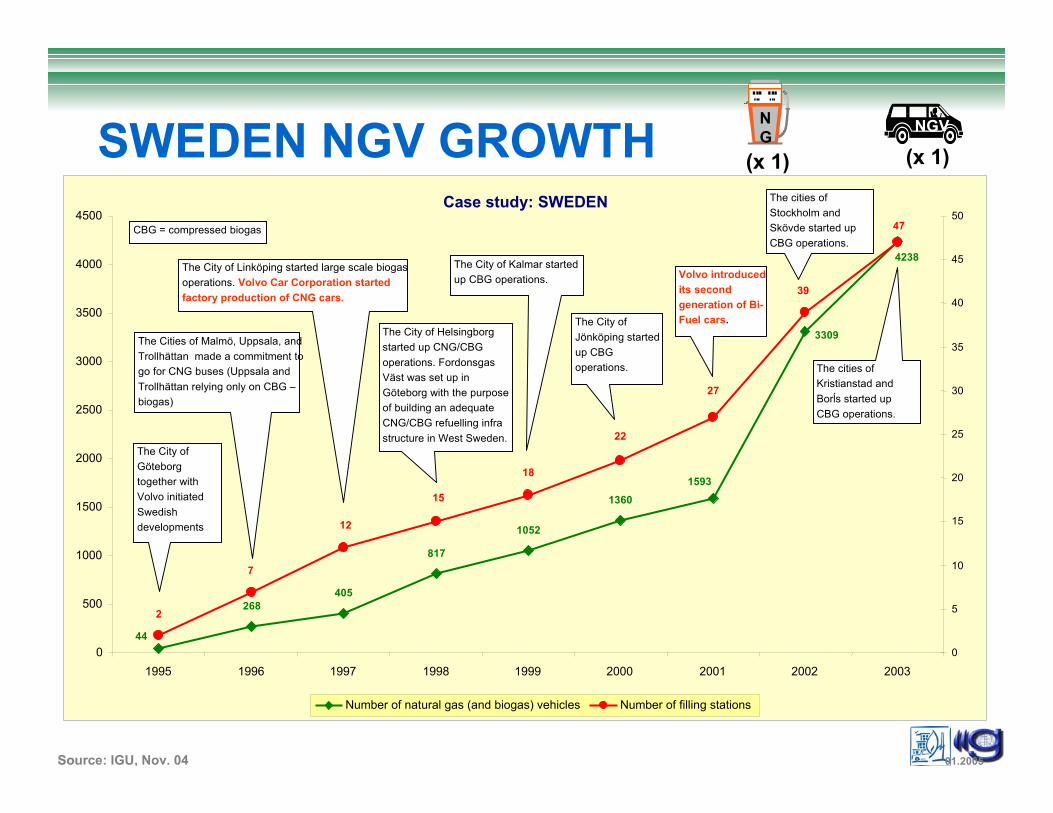

SWEDEN NGV GROWTH NGV

(x 1)

NG

(x 1)

Source: IGU, Nov. 04 01.2005

Case study: SWEDEN

268405

817

1052

13601593

4238

3309

44

2

7

12

27

39

47

15

18

22

0

500

1000

1500

2000

2500

3000

3500

4000

4500

1995 1996 1997 1998 1999 2000 2001 2002 20030

5

10

15

20

25

30

35

40

45

50

Number of natural gas (and biogas) vehicles Number of filling stations

The City of Göteborg together with Volvo initiated Swedish developments

CBG = compressed biogas

The Cities of Malmö, Uppsala, and Trollhättan made a commitment to go for CNG buses (Uppsala and Trollhättan relying only on CBG –biogas)

The City of Linköping started large scale biogas operations. Volvo Car Corporation started factory production of CNG cars.

The City of Helsingborg started up CNG/CBG operations. Fordonsgas Väst was set up in Göteborg with the purpose of building an adequate CNG/CBG refuelling infra structure in West Sweden.

The City of Kalmar started up CBG operations.

The City of Jönköping started up CBG operations.

Volvo introduced its second generation of Bi-Fuel cars.

The cities of Stockholm and Skövde started up CBG operations.

The cities of Kristianstad and Borĺs started up CBG operations.

mm/y ©ENGVA, 2004

SELECTED COUNTRY MODELS

MIDDLE EAST&

JAPAN

mm/y ©ENGVA, 2004

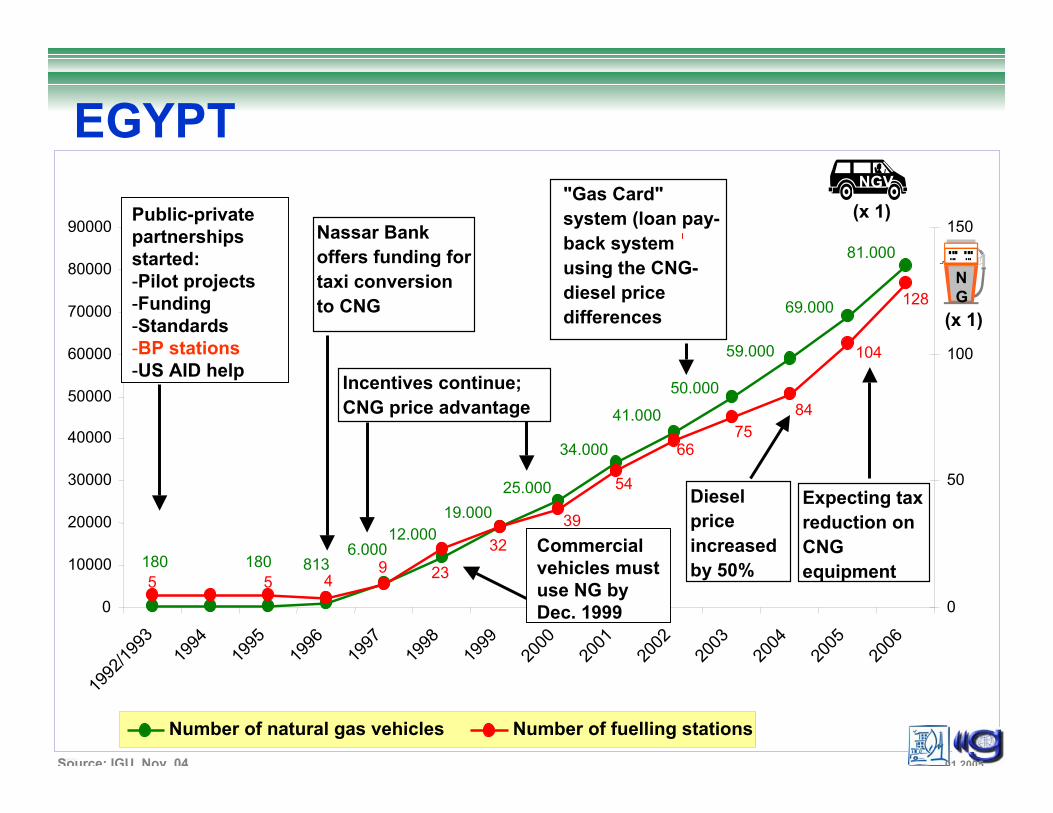

EGYPT

50.000

34.000

59.000

69.000

81.000

41.000

25.00019.000

12.0006.000

813180180

84

66

5 5

3239

54

49 23

128

104

75

0

10000

20000

30000

40000

50000

60000

70000

80000

90000

1992

/1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

0

50

100

150

Number of natural gas vehicles Number of fuelling stations

Nassar Bank offers funding for taxi conversion to CNG

Incentives continue;CNG price advantage

"Gas Card" system (loan pay-back system using the CNG-diesel price differences

Diesel price increased by 50%

Expecting tax reduction on CNG equipment

Public-private partnerships started:-Pilot projects-Funding-Standards-BP stations-US AID help

Commercial vehicles must use NG by Dec. 1999

NGV

(x 1)

NG

(x 1)

Source: IGU Nov 04 01 2005

mm/y ©ENGVA, 2004

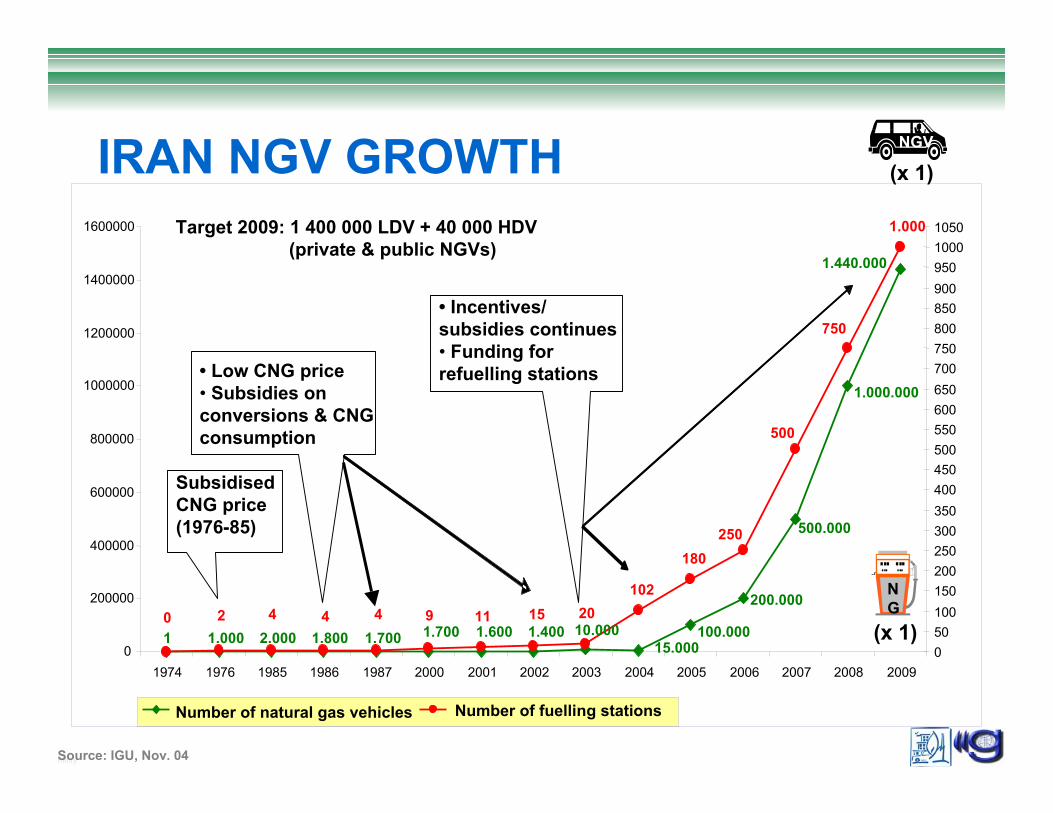

IRAN NGV GROWTH

1 1.000 2.000 1.800 1.700 1.700 1.600 1.400 10.00015.000

100.000

200.000

500.000

1.000.000

1.440.000

102

180250

500

750

1.000

0 2 4 11 15 204 4 9

0

200000

400000

600000

800000

1000000

1200000

1400000

1600000

1974 1976 1985 1986 1987 2000 2001 2002 2003 2004 2005 2006 2007 2008 200905010015020025030035040045050055060065070075080085090095010001050

Number of natural gas vehicles Number of fuelling stations

SubsidisedCNG price(1976-85)

• Incentives/ subsidies continues• Funding for refuelling stations

Target 2009: 1 400 000 LDV + 40 000 HDV(private & public NGVs)

Source: IGU, Nov. 04 01.2005

• Low CNG price• Subsidies on conversions & CNG consumption

NGV

(x 1)

NG

(x 1)

mm/y ©ENGVA, 2004

Vehicle growth scenario.2000Vehicle growth scenario.2000--20202020

5000000

10000000

15000000

20000000

25000000

30000000

35000000

0

2000

2005

2010

2015

2020

lowgrowth,(EIA)

mediumgrowth

high growth

Vehicle growth prognoses for Iran

mm/y ©ENGVA, 2004

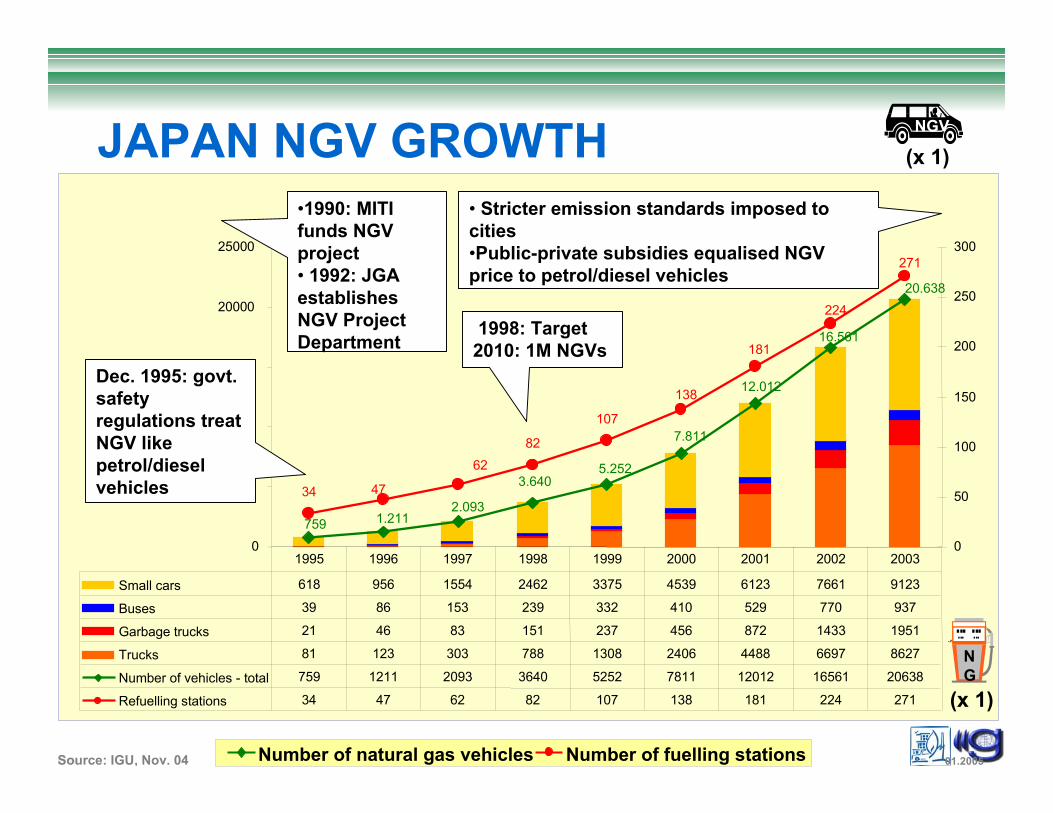

3.640

12.012

7.811

5.252

2.0931.211759

20.638

16.561

34

82

107

62

47

138

181

271

224

0

5000

10000

15000

20000

25000

0

50

100

150

200

250

300

Small cars 618 956 1554 2462 3375 4539 6123 7661 9123

Buses 39 86 153 239 332 410 529 770 937

Garbage trucks 21 46 83 151 237 456 872 1433 1951

Trucks 81 123 303 788 1308 2406 4488 6697 8627

Number of vehicles - total 759 1211 2093 3640 5252 7811 12012 16561 20638

Refuelling stations 34 47 62 82 107

JAPAN NGV GROWTH

Number of natural gas vehicles Number of fuelling stations

NGV

(x 1)

NG

(x 1)

Source: IGU, Nov. 04 01.2005

138 181 224 271

1995 1996 1997 1998 1999 2000 2001 2002 2003

•1990: MITI funds NGV project• 1992: JGA establishes NGV Project Department

• Stricter emission standards imposed to cities•Public-private subsidies equalised NGV price to petrol/diesel vehicles

Dec. 1995: govt. safety regulations treat NGV like petrol/diesel vehicles

1998: Target 2010: 1M NGVs

mm/y ©ENGVA, 2004

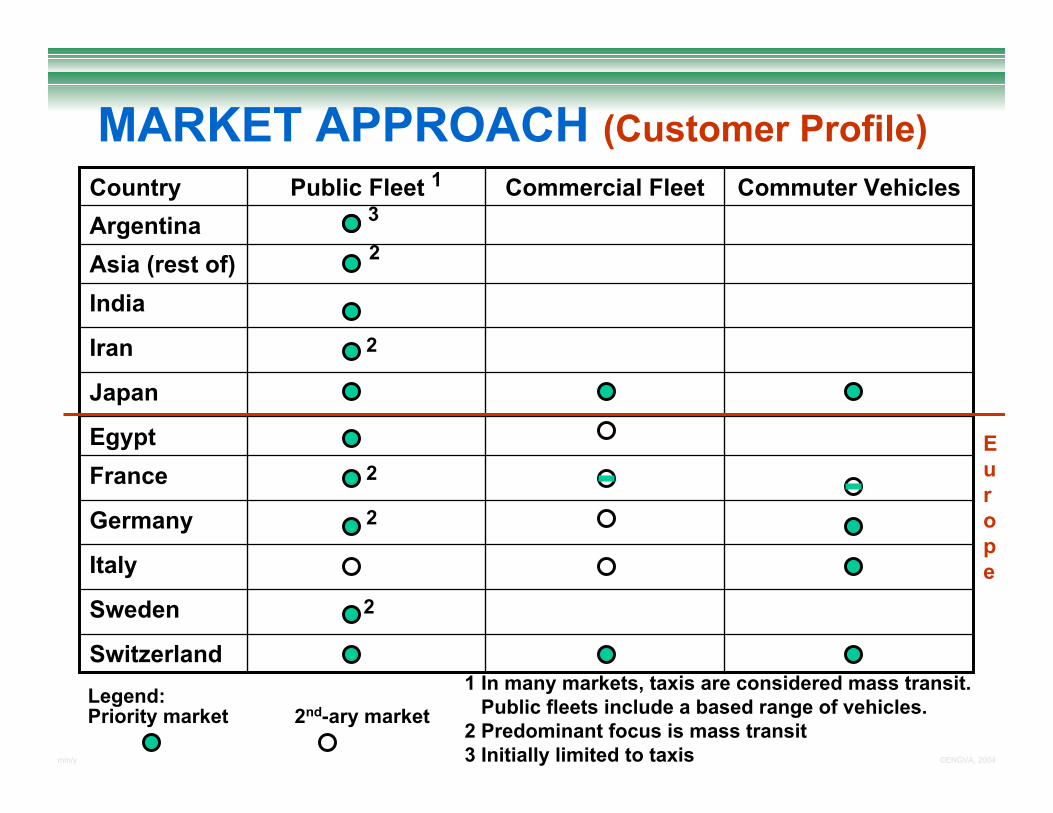

MARKET APPROACH (Customer Profile)

Egypt

2Sweden

Switzerland

Italy

2Germany

2France

Japan

2Iran

India

2Asia (rest of)

3ArgentinaCommuter VehiclesCommercial FleetPublic Fleet 1Country

January 2004

1 In many markets, taxis are considered mass transit. Public fleets include a based range of vehicles.

2 Predominant focus is mass transit3 Initially limited to taxis

Europe

Legend: Priority market 2nd-ary market

mm/y ©ENGVA, 2004

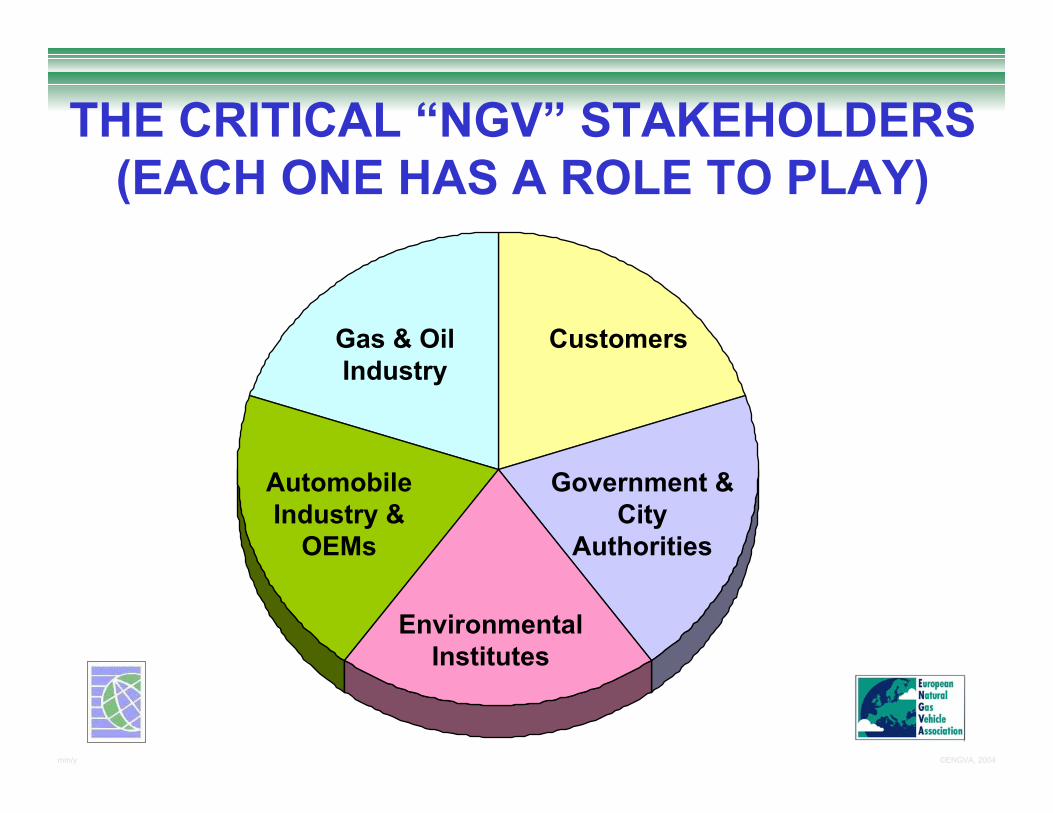

THE CRITICAL “NGV” STAKEHOLDERS (EACH ONE HAS A ROLE TO PLAY)

Gas & Oil Industry

Customers

Government & City

Authorities

Environmental Institutes

Automobile Industry &

OEMs

mm/y ©ENGVA, 2004

THE INVOLVEMENT OF GOVERNMENT IS ESSENTIAL*(Strategies Supported by Specific Actions!)

• Create incentives (financial & others)• Enforce mandates (but with incentives)• Develop standards• Fund research & development• Leadership by example• PR & communications

* What’s good for one alternative fuel is good for them all!

mm/y ©ENGVA, 2004

WHAT WE CAN LEARN FROM COUNTRY EXPERIENCES

• Policies MUST be balanced between carrots & sticks (incentives & mandates)

• Policies MUST be consistent over time (vision, strategy & focus)

• Incremental, transitional actions are required; not “knee jerk”, reactive policies

• Pro-active is better than re-active

mm/y ©ENGVA, 2004

THE SENSIBLE POLICY APPROACH TO NGV INCENTIVES

• Incentives should be based upon the environmental quality of the fuels AND the technologies

• Incentives should be based upon market share achieved over time

• Alternatively, incentives should be lowered slowly over time, and not based upon a single end-date

mm/y ©ENGVA, 2004

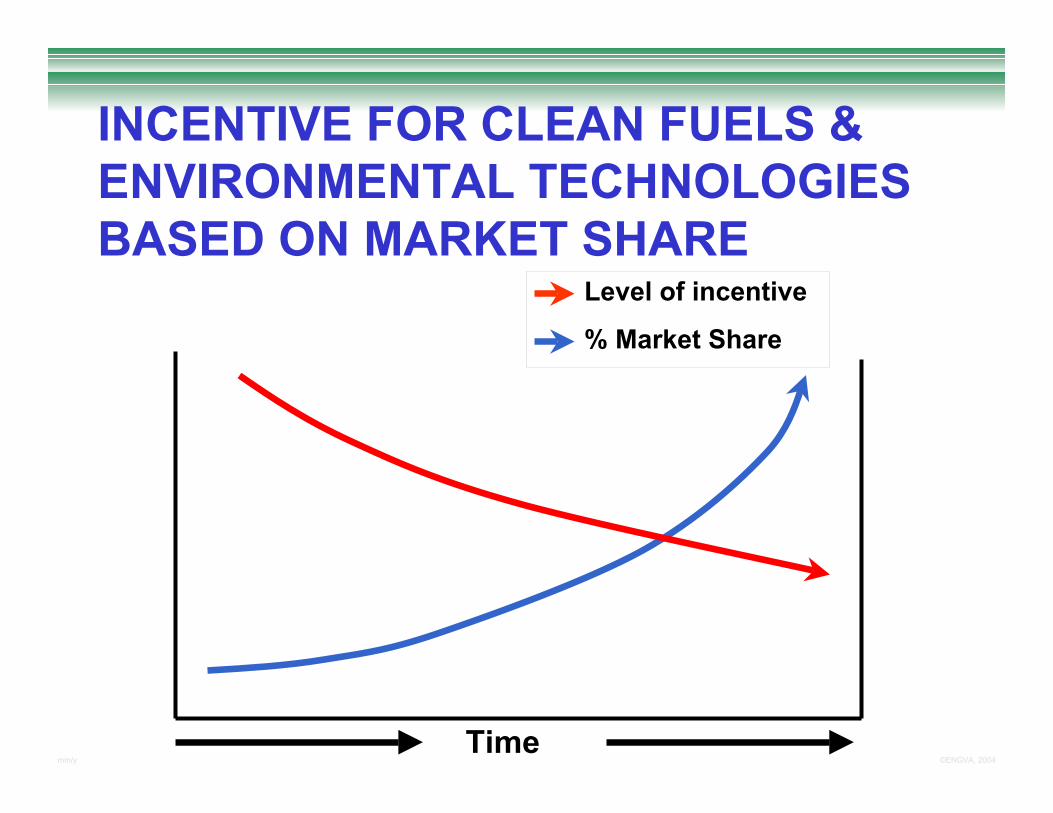

INCENTIVE FOR CLEAN FUELS & ENVIRONMENTAL TECHNOLOGIES BASED ON MARKET SHARE

Level of incentive

% Market Share

Time

mm/y ©ENGVA, 2004

IN CONCLUSION• There are no fuel panaceas.• NGVs, even with issues of fuel storage

and infrastructure development remain a fuel of choice (environment & energy security).

• More people have to be informed of its potential, the benefits, and of the contribution to improved air quality and energy security.

• Not easy market…but valuable in pursuing! It takes a long time…to be sustainable.

• Hydrogen link to the future is important!

mm/y ©ENGVA, 2004

UNITED NATIONS INITIATIVES 2005

• World harmonisation of gaseous fuel & vehicle standards (with ISO & UN)

• Road signage for cng fuelling stations (WP1 Traffic Safety)

• On-going amendments and harmonisation of standards(WP.29 & GRPE)

mm/y ©ENGVA, 2004

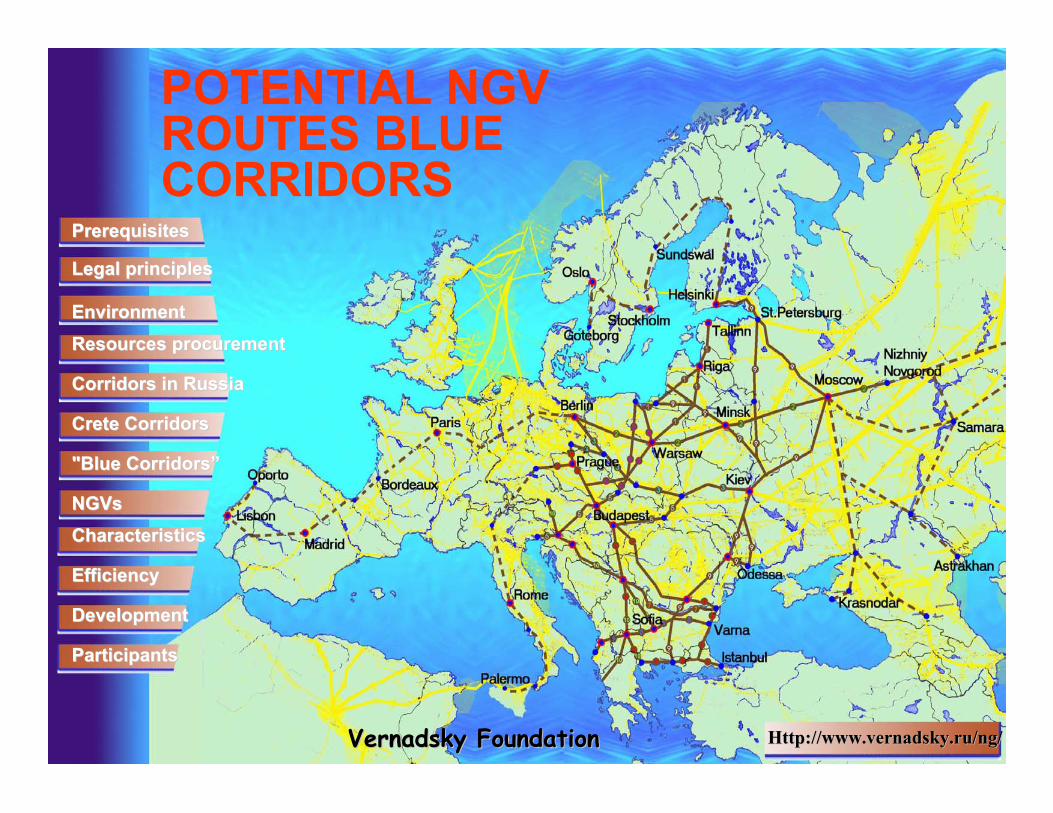

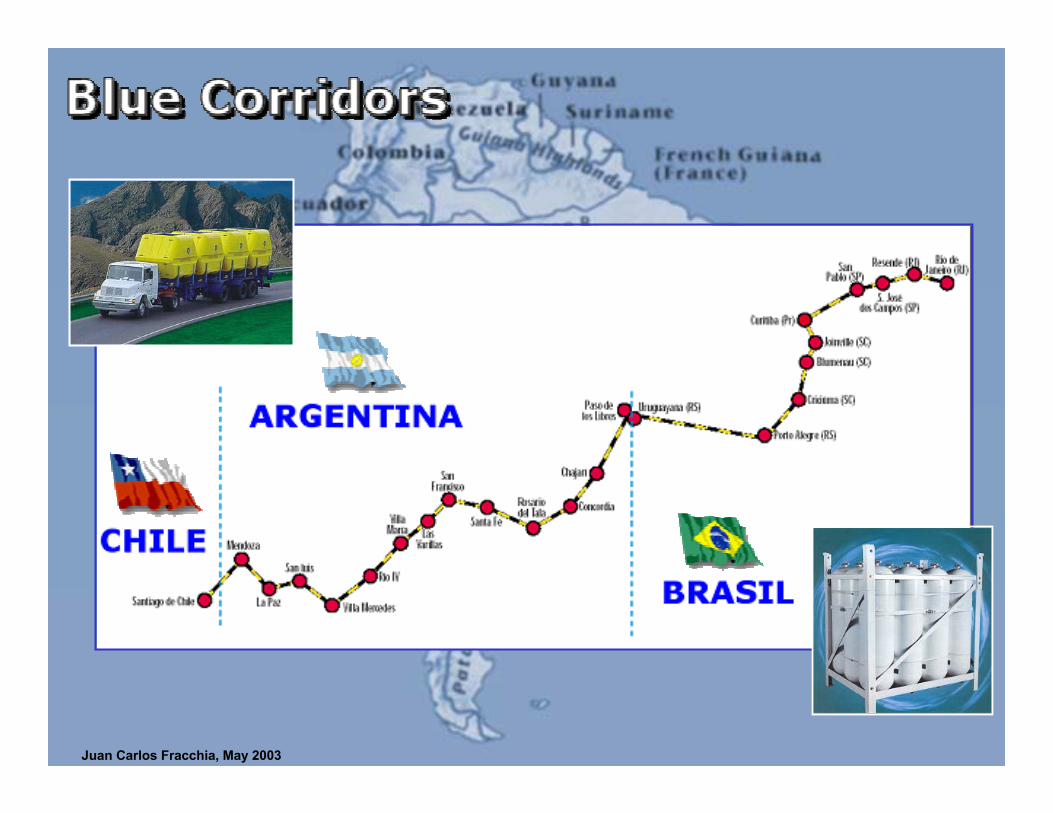

POTENTIAL NGV ROUTES BLUE CORRIDORS

Http://www.vernadsky.ru/ng/Http://www.vernadsky.ru/ng/

PrerequisitesPrerequisites

Legal principlesLegal principles

Environment Environment

Resources procurementResources procurement

Corridors in RussiaCorridors in Russia

CharacteristicsCharacteristics

EfficiencyEfficiency

DevelopmentDevelopment

ParticipantsParticipants

"Blue Corridors”"Blue Corridors”

NGVsNGVs

Crete CorridorsCrete Corridors

VernadskyVernadsky FoundationFoundation

mm/y ©ENGVA, 2004Juan Carlos Fracchia, May 2003

mm/y ©ENGVA, 2004

VISIT THE ASSOCIATION WEBSITES!!!

• www.iangv.org.nz

• www.engva.org

• www.ngvc.org

mm/y ©ENGVA, 2004

• In conjunction with the World Fair of Natural Gas & Hydrogen Vehicles (with The GVR magazine)

• June 8-10 Conference• June 9-12 Vehicle Fair• Bolzano (Bozen), Italy

A PROFITABLE €NVIRONMENT FOR NGVs

ENGVA 11th Annual ConferenceJune 2005

mm/y ©ENGVA, 2004

23rd WORLD GAS CONFERENCE

Anyone interested in participating in this Study Group 5.3. Natural Gas for Vehicles: Global Opportunities for Natural Gas as a Transportation Fuel for Today and Tomorrow, please contact [email protected] or [email protected]

mm/y ©ENGVA, 2004

EMERGING MODELS of NGV MARKET DEVELOPMENT

United NationsWorking Party on Gas

20 January 2005Dr. Jeffrey M. Seisler

Executive Director

GENEVAGENEVA