Gaming Expansion in New Jersey - · PDF fileGaming Expansion in New Jersey January 2016 i |...

115

Gaming Expansion in New Jersey Assessing the Impacts on the Atlantic City Region Prepared At The Request Of: Resorts Casino Hotel, Atlantic City, NJ Prepared By: Morowitz Gaming Advisors, LLC & Global Gaming & Hospitality, LLC January 22, 2016

Transcript of Gaming Expansion in New Jersey - · PDF fileGaming Expansion in New Jersey January 2016 i |...

Gaming Expansion in New Jersey

Assessing the Impacts on the Atlantic City Region

Prepared At The Request Of: Resorts Casino Hotel, Atlantic City, NJ

Prepared By:

Morowitz Gaming Advisors, LLC & Global Gaming & Hospitality, LLC

January 22, 2016

Gaming Expansion in New Jersey January 2016

i | P a g e

This Economic Impact Assessment and Financial Analysis (the “Report”) has been prepared by Morowitz Gaming Advisors, LLC and Global Gaming & Hospitality LLC (collectively hereinafter referred to as “GGH” or the “Advisors”), including its subsidiaries, affiliates, and independent contractors, which include Leisure Dynamics Research, LLC, at the request of Resorts Casino Hotel (the “Company”). The sole purpose of the Report is to assess the impacts of gaming expansion in northern New Jersey on the gaming industry and economies of the Atlantic City region and State of New Jersey. This Report does not purport to contain information that a prospective interested party may rely upon to evaluate any investment related to a potential transaction involving anything associated with Atlantic City. This Report has been prepared for informational purposes only. All information set forth in this Report has been prepared by GGH based upon information furnished by various third‐party sources. GGH does not assume any responsibility for such information, including the estimates and projections of future financial and operating performance of any of the companies or entities mentioned in this report, if any, and other forward‐looking statements, or of any additional evaluation material made available in connection with any further investigation of the market or the impacts of northern New Jersey gaming expansion. Any estimates, projections and forward‐looking statements contained herein have been prepared and based on information currently available to GGH and involve subjective assumptions, judgments and analyses, which may or may not be correct. GGH or the Company undertake no obligation to update any such estimates, projections or forward‐looking statements or to provide access to any additional information. Neither GGH nor the Company make any express or implied representation or warranty as to the accuracy or completeness of the information contained in, or for any omissions from, the Report or any additional evaluation material made available in connection with any further investigation of the impacts of northern New Jersey gaming expansion. Each of GGH and the Company expressly disclaims any and all liability which may be based on such information, errors therein or omissions therefrom. .

Neither the receipt of this Report by any person nor any information contained herein or supplied herewith or subsequently communicated to any person in connection herewith is to be taken as providing legal, tax, accounting, or investment advice by GGH to any such person. Further, the information contained herein, as well as any other communications or information provided by GGH is not intended to be, and shall not be regarded or construed as, a recommendation to participate in a transaction or to make any investment. GGH does not provide tax, legal or accounting advice. You should conduct a thorough and independent review of the legal, tax and accounting aspects of any information contained in this report and an independent assessment of the merits of pursuing a transaction related to Atlantic City or the potential northern New Jersey gaming expansion and should consult your own professional advisors in light of your particular circumstances.

This Report does not constitute a solicitation of funds, an offer to sell a financial interest in the Company or anything else related to the potential northern New Jersey gaming expansion or any other entity, or an offer to accept any proposal, nor does it constitute an offer to sell, or a solicitation of offers to buy, securities of the Company or any other entity. In furnishing this Report, neither GGH nor the Company undertake any obligation to provide the recipient with access to any evaluation material. This Report shall neither be deemed an indication of the state of affairs of the Company or other casinos or businesses in New Jersey nor constitute an indication that there has been no change in the business affairs of the Company or New Jersey since the date hereof or since the dates as of which information is provided herein.

All communications, inquiries and requests for information relating to this Report should be addressed directly to GGH at the contact information listed below.

Gaming Expansion in New Jersey January 2016

ii | P a g e

GGH Contact Information:

Cory Morowitz Morowitz Gaming Advisors, LLC Chairman & Managing Member

Michael S. Kim Global Gaming & Hospitality LLC Managing Partner, New York

248 South New York Road

Galloway, NJ 8205 T 609.652.6472 F 609.652.6473

299 Park Avenue, 6th Floor New York, NY 10171 T 646.719.1096 F 702.823.1926

www.morowitzgaming.com www.gghsp.com

Gaming Expansion in New Jersey January 2016

iii | P a g e

Gaming Expansion in New Jersey – Impacts on Atlantic City Region

TABLE OF CONTENTS

I. EXECUTIVE SUMMARY ................................................................................... 4

II. BACKGROUND, METHODOLOGY & SIGNIFICANT ASSUMPTIONS .................. 7

III. ATLANTIC CITY – AN EVOLVING GAMING MARKET ..................................... 10

IV. THE REGIONAL ECONOMY ........................................................................... 24

V. THE FUTURE OF ATLANTIC CITY WITHOUT NEW JERSEY EXPANSION .......... 43

VI. NON‐GAMING AND CONVENTIONS ............................................................. 59

VII. THE IMPACT OF NORTH JERSEY GAMING EXPANSION ON ATLANTIC CITY

CASINOS ....................................................................................................... 65

VIII. THE FLOW THROUGH IMPACTS TO THE REGION FROM NORTH JERSEY

GAMING EXPANSION ................................................................................... 82

IX. LIMITING CONDITIONS .............................................................................. 109

X. APPENDIX – ABOUT THE AUTHORS OF THIS REPORT ................................ 110

Gaming Expansion in New Jersey January 2016

4 | P a g e

I. EXECUTIVE SUMMARY The State of New Jersey is considering the expansion of casino gaming into northern New Jersey. Recent proposed legislation calls for no more than two casinos, each to be located in a different county in municipalities more than 72 miles from Atlantic City. This expansion comes at a time that Atlantic City’s gaming industry, after several years of decline owing to an increasingly competitive northeast gaming market, is finally finding its footing. Atlantic City has right sized its gaming industry, is in the middle of several strategic investments and despite potential new out‐of‐state competition, has stabilized and is poised for new growth. Expansion of gaming to Northern New Jersey could jeopardize Atlantic City’s recovery and negatively impact not only the gaming industry, but the entire region. GGH (Morowitz Gaming Advisors and Global Gaming & Hospitality) was requested by Resorts Casino Hotel (the “Company”) to prepare an analysis of the expansion of gaming in New Jersey. Specifically, GGH analyzed the impact of two large scale casino investments in northern New Jersey on the competitive environment impacting New Jersey and Atlantic City and quantified the potential impacts on the casinos in Atlantic City and the overall economy of the Atlantic City region. We did not analyze or quantify the offsetting economic impacts of casino expansion in northern New Jersey because there is simply not enough detail in the proposed legislation to determine those impacts. This analysis therefore focuses solely on the impacts to the Atlantic City region. Our analysis and conclusions are based on a number of analytical techniques including an in depth qualitative and quantitative analysis of the trends through the date of this report impacting the gaming industry in Atlantic City as well as governmental spending and trends in the region. Our analysis also relies on the development and utilization of a gravity model, which is a modeling technique used throughout the gaming industry to measure the impacts of new gaming supply on existing competitors and the market as a whole. Atlantic County has grown significantly during the casino era in terms of population and almost all of that growth has been confined to the municipalities and towns in the mainland communities surrounding Atlantic City. This growth was catalyzed and supported by the gaming industry and necessitated much in the way of infrastructure to support this growth including roads, schools and government services. As the industry has contracted, the area has come under considerable stress. As of September 2015, the casino industry generated $2.6 billion of net revenue, $404 million of EBITDA, employed 24,431 employees, over $590 million in wages (not including tips) and was paying approximately $381 million in State and local taxes (including property taxes). On a pro forma basis, those amounts are expected to decline marginally with the opening of new out‐of‐state competitors anticipated in Pennsylvania, Maryland, New York and Massachusetts to $2.45 billion of gaming revenue, $356 million of EBITDA, 23,029 employees, $557 million in wages and $363 million in taxes. At this point, due to saturation of the U.S. market, it is highly unlikely that

Gaming Expansion in New Jersey January 2016

5 | P a g e

there will be additional out‐of‐state expansion and the Atlantic City casino industry should stabilize and even potentially grow. However, if casinos expand to northern New Jersey, Atlantic City’s casino industry will contract significantly, losing net revenue ranging from $624 million to $1.4 billion with industry EBITDA declining to anywhere from $162 million to $195 million. However, the more likely result is that anywhere from three to five casinos will close, causing a spiral downward with net revenues declining by a range of $1.0 billion to $1.4 billion, EBITDA declining by between $162 million and $170 million, employment declining by between 11,800 and 15,000, wages (not including tips) declining by between $285 million and $365 million and industry tax payments declining by between $128 million and $158 million.

Impacts of North Jersey Expansion on Atlantic City Casinos

Based on our analysis we have concluded that the expansion of gaming in northern New Jersey will have significant and far reaching impacts on the Atlantic City region. The major impacts are summarized as follows:

Gaming revenue declines of $691 million to $1.4 billion

Three to five additional casino closures

Total job losses to the region ranging from 23,000 to 30,000 and regional unemployment rates of 25% to 30%

Foreclosure rates (already among the highest in the nation) increasing significantly

Lost regional and state economic output of $1.5 billion to $2.0 billion

Potential increases in New Jersey State transitional and school subsidies to municipalities and school districts of $134 million to $367 million

Reductions in Atlantic City Expressway tolls of $11 to $15 million

Reductions in state tax payments by Atlantic City casinos of $86 million to $111 million

Potential for $100 million of reduced spending at Boardwalk based small businesses

(in 000's except Employees TTM 9/15 Baseline No Closures 3 Closures Impact % 4 Closures Impact % 5 Closures Impact %

Revenues

Gaming 2,474,066$ 2,285,898$ 1,594,254$ 1,194,844$ (1,091,055)$ (47.7%) 1,006,471$ (1,279,427)$ (56.0%) 856,580$ (1,429,318)$ (62.5%)

Non‐gaming 999,387 964,683 790,253 641,193 (323,490) (33.5%) 562,394 (402,289) (41.7%) 521,453 (443,230) (45.9%)

Gross Revenue 3,473,453 3,250,581 2,384,507 1,836,037 (1,414,544) (43.5%) 1,568,865 (1,681,716) (51.7%) 1,378,034 (1,872,548) (57.6%)

Promo 860,232 797,443 556,161 406,222 (391,221) (49.1%) 352,985 (444,458) (55.7%) 302,595 (494,848) (62.1%)

Net Revenue 2,613,221 2,453,138 1,828,346 1,429,815 (1,023,323) (41.7%) 1,215,880 (1,237,259) (50.4%) 1,075,439 (1,377,700) (56.2%)

EBITDA 404,545 356,226 161,108 186,283 (169,943) (47.7%) 186,529 (169,697) (47.6%) 193,942 (162,284) (45.6%)

% Margin 15.5% 14.5% 8.8% 13.0% (1.5%) (10.3%) 15.3% 0.8% 5.6% 18.0% 3.5% 24.2%

Gaming as % of Gross 71.2% 70.3% 66.9% 65.1% (5.2%) (7.5%) 64.2% (6.2%) (8.8%) 62.2% (8.2%) (11.6%)

Occupancy 80.9% 81.6% 80.3% 85.5% 3.9% 4.7% 88.6% 7.0% 8.6% 90.4% 8.8% 10.8%

ADR 102.37$ 102.26$ 96.95$ 107.79$ 5.52$ 5.4% 113.93$ 11.67$ 11.4% 120.65$ 18.39$ 18.0%

# of Employees 24,431 23,029 16,318 11,205 (11,824) (51.3%) 9,353 (13,676) (59.4%) 7,990 (15,039) (65.3%)

Salaries & Wages 590,710$ 556,675$ 394,907$ 271,619$ (285,056)$ (51.2%) 227,341$ (329,334)$ (59.2%) 192,156$ (364,520)$ (65.5%)

Average Salary 24.18 24.17 24.20 24.24 0.07 0.3% 24.31 0.13 0.6% 24.05 (0.12) (0.5%)

Taxes

Gaming Tax 175,322$ 165,667$ 117,720$ 90,740$ (74,927)$ (45.2%) 78,082$ (87,585)$ (52.9%) 67,883$ (97,784)$ (59.0%)

CRDA Fee 19,390 28,574 19,928 14,936 (13,638) (47.7%) 12,581 (15,993) (56.0%) 10,707 (17,866) (62.5%)

Property Tax 151,162 124,979 90,000 90,000 (34,979) (28.0%) 90,000 (34,979) (28.0%) 90,000 (34,979) (28.0%)

Parking Fee 3,620 3,344 2,332 1,748 (1,596) (47.7%) 1,473 (1,872) (56.0%) 1,253 (2,091) (62.5%)

Room Fee 11,897 11,997 11,809 8,706 (3,290) (27.4%) 7,009 (4,988) (41.6%) 6,433 (5,564) (46.4%)

Total 361,391$ 334,561$ 241,789$ 206,130$ (128,430)$ (38.4%) 189,144$ (145,416)$ (43.5%) 176,276$ (158,284)$ (47.3%)

Gaming Expansion in New Jersey January 2016

6 | P a g e

These impacts are summarized in the following tables.

Summary of Regional Impacts on Jobs, Income and Economic Output

Job Losses Income Loss

Loss in Economic Output Unemployment Rate

Direct Casino Impacts 12,500 to 16,000 jobs

$372 million to $490 million

Vendor Impacts 5,000 to 7,000

jobs

$185 million to $242 million

Total Regional Economic Impact from Casino 17,500 to 23,000

$556 million to $733 million

$664 million to $888 million 20% to 25%

Spending Outside Casinos 5,600 to 7,300

$153 million to $201 million

$364 million to $477 million

Total Regional Economic Impact with Casinos and Boardwalk

23,000 to 30,000

$709 million to $934 million

$1.0 billion to $1.36 billion 25% to 30%

Summary of Direct Casino Toll and Tax Related Impacts

SJTA Tolls Gaming Revenue Tax Luxury Tax Room Tax Parking Tax

Total Impact $11.4 million to $14.9 million

$75 million to $98 million

$5.6 million

$3.3 million to $5.6 million

$1.6 million to $2.1 million

Summary of Potential Government Impacts

Transitional Aid Range School Aid Range Total

Government Impacts $31 million to $54 million $103 million to $313

million $134 million to $367 million Annually

Potential Reduced Economic Output Beyond Atlantic County Region

Decline in Economic Output Outside Atlantic County

Annual Impact Per Non‐Atlantic County

Resident

Multiplier Impacts of Atlantic City Economic Decline to Rest of State $275 million to $369 million $32 to $43

Direct, Indirect and Induced Impacts of Vendor Spending Declines Outside of Atlantic County $185 million $21

Total Decline Outside Atlantic County $460 million to $554 million $53 to $64

Our analysis, methodology and conclusions are detailed in the accompanying report and economic impact study and magnify the importance of studying the overall impact of gaming expansion in New Jersey. The key issue is that casinos in northern New Jersey will not just impact Atlantic City. They will impact the wellbeing of an entire region of the State of New Jersey. In the absence of other significant economic catalysts, the Atlantic County region could become a significant and permanent ward of the state of New Jersey.

Gaming Expansion in New Jersey January 2016

7 | P a g e

II. BACKGROUND, METHODOLOGY & SIGNIFICANT ASSUMPTIONS

Background The State of New Jersey is considering the expansion of casino gaming into northern New Jersey. Recent proposed legislation calls for no more than two casinos, each to be located in a different county in municipalities more than 72 miles from Atlantic City. Potential locations include Bergen County and Hudson County. Gaming in northern New Jersey carries risks for the gaming industry in Atlantic City and will impact revenues and profitability. The issue facing New Jersey is not so much the impact on the individual casino operators. Rather, it is the potential impact on an entire region. The greater Atlantic City region is already in crisis. The regional workforce has already shed almost 13,000 jobs since 2007 (approximately 9%) representing over $500 million of economic output for a region in dire need. This has resulted in unemployment still hovering near 9% and a foreclosure rate over 4 times the national average (and among the highest in the country). This is not just an Atlantic City issue, it is an issue that impacts the entire region including the towns surrounding Atlantic City. Interestingly, the gaming industry in Atlantic City is finally finding its footing. The Atlantic City casinos are gaining profitability and the tourism economy of the city is diversifying. Gaming expansion into northern New Jersey will negatively impact this recovery. GGH was requested by Resorts Casino Hotel (the “Company”) to prepare an analysis of the expansion of gaming in New Jersey. Specifically, GGH analyzed the impact of two large scale casino investments in northern New Jersey on the competitive environment impacting New Jersey and Atlantic City and quantified the potential impacts on the casinos in Atlantic City and the overall economy of the Atlantic City region. We did not analyze or quantify the offsetting economic impacts of casino expansion in northern New Jersey because there is simply not enough detail in the proposed legislation to determine those impacts. For instance, it is unknown exactly where the casinos will be located, what the tax rate will be, what kind of amenities they will have, their total investment or other details that would be required to develop a fulsome analysis of the positive impacts. Therefore, this analysis focuses specifically on the impacts of adding two large scale casinos to northern New Jersey to the Atlantic City casino industry and the regional economy. Methodology

Our conclusions are based on the following analyses and tasks.

Assessed the market for casino gaming in New Jersey in order to provide an assessment of the impacts of proposed new casinos in Northern New Jersey on the economy of the Atlantic City region.

Interviewed regional business and government officials including officials from Atlantic City, Egg Harbor Township, Galloway Township and Atlantic County.

Gaming Expansion in New Jersey January 2016

8 | P a g e

Evaluated the Atlantic City gaming and entertainment market, its evolution and current trends, and developed a baseline of potential future gaming revenue, other revenue, and casino profitability (“Baseline Scenario”). Our analysis included the development of a regional gravity model calibrated to current gaming revenues and other econometric models and trend analyses of current casino based‐gaming revenues.

Provided qualitative and quantitative analyses of the Atlantic City gaming industry and analysis of its current financial health and likely future if gaming is not expanded in New Jersey. This included applying the gravity model and trend models to a future scenario without expanded gaming in New Jersey.

Quantified the impact on the Atlantic City gaming market (using the gravity model methodology) if gaming expands to Northern New Jersey.

Analyzed and quantified the potential revenue and resulting profitability impacts on Atlantic City casinos and the likelihood of additional casino closures.

Analyzed the prior impact of casino closures on the greater Atlantic City region including the impacts on regional macroeconomic factors such as employment, real estate values (including property tax revenue trends), foreclosure rates, and other economic statistics.

Qualitatively and quantitatively analyzed the flow through economic impacts on the Atlantic City regional economy (including both Atlantic City individually and the surrounding towns and county) of additional potential casino closures including the following:

a. Employment and unemployment b. Regional Economic Output and Impacts on the rest of New Jersey c. Foreclosure rates d. Regional tax generation

Assumptions

The following assumptions are an integral part of this study:

While the final form of legislation is at this time unknown, this study assumes there will be two casinos in northern New Jersey. For purposes of our analyses, we assumed the casinos would be located in Bergen County and Hudson County. However, as the report will show, any location in New Jersey within a 90 to 180 minute drive of Atlantic City will have a significant negative impact on Atlantic City.

The casinos in northern New Jersey would each have up to 5,000 gaming positions, significant non‐gaming amenities such as hotels, retail, dining and entertainment and over $1 billion of investment.

The tax rate applied to casino revenues in northern New Jersey is unknown at this time but it is assumed it will be similar to those proposed for resort casinos in New York and Massachusetts.

Both properties will:

o Have management personnel with extensive experience operating comparable casino and resort operations

Gaming Expansion in New Jersey January 2016

9 | P a g e

o Utilize comprehensive accounting and gaming control systems capable of providing management with accurate and timely performance data

o Be properly maintained and annual capital expenditures required to keep them at a competitive level will be made

o Develop a marketing and advertising campaign and a promotional plan to ensure adequate patronage from local and regional customers

Gaming Expansion in New Jersey January 2016

10 | P a g e

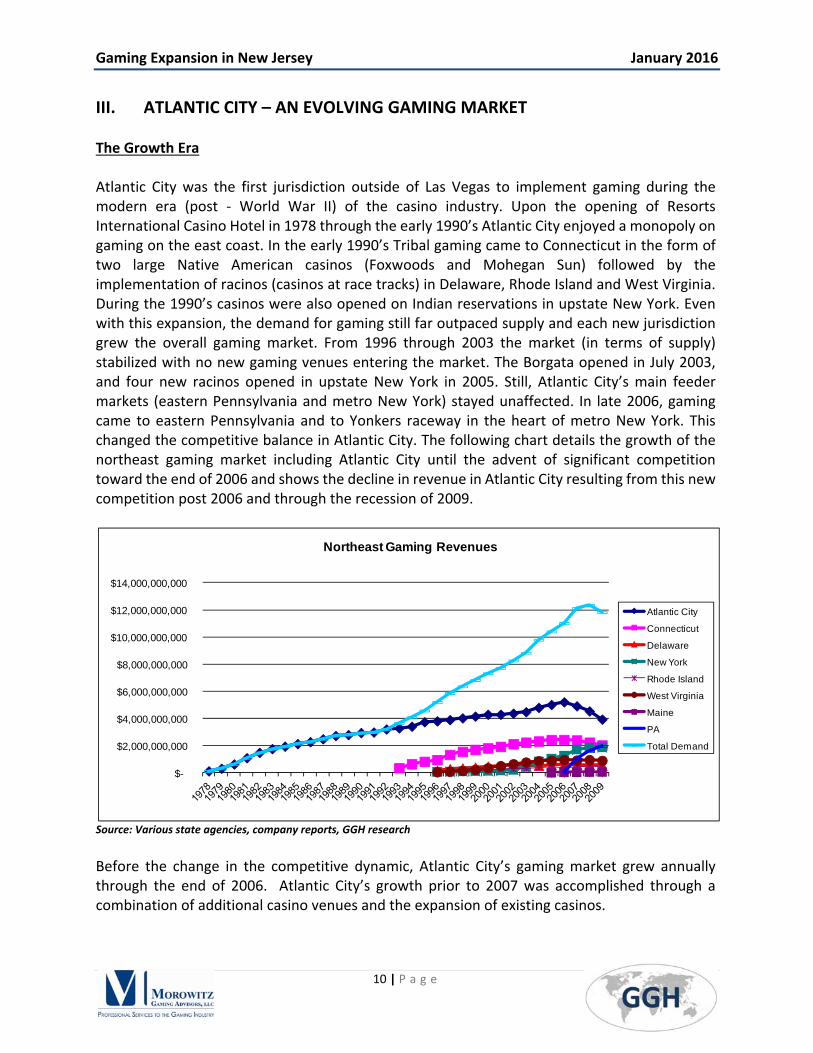

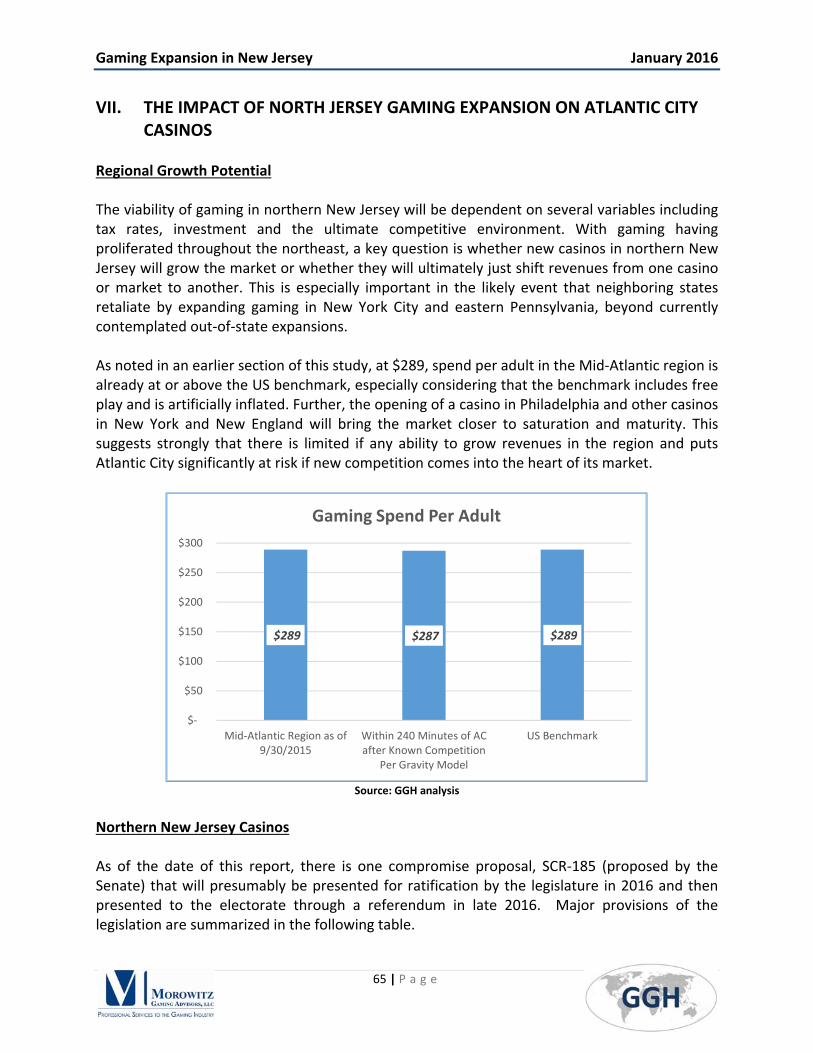

III. ATLANTIC CITY – AN EVOLVING GAMING MARKET The Growth Era Atlantic City was the first jurisdiction outside of Las Vegas to implement gaming during the modern era (post ‐ World War II) of the casino industry. Upon the opening of Resorts International Casino Hotel in 1978 through the early 1990’s Atlantic City enjoyed a monopoly on gaming on the east coast. In the early 1990’s Tribal gaming came to Connecticut in the form of two large Native American casinos (Foxwoods and Mohegan Sun) followed by the implementation of racinos (casinos at race tracks) in Delaware, Rhode Island and West Virginia. During the 1990’s casinos were also opened on Indian reservations in upstate New York. Even with this expansion, the demand for gaming still far outpaced supply and each new jurisdiction grew the overall gaming market. From 1996 through 2003 the market (in terms of supply) stabilized with no new gaming venues entering the market. The Borgata opened in July 2003, and four new racinos opened in upstate New York in 2005. Still, Atlantic City’s main feeder markets (eastern Pennsylvania and metro New York) stayed unaffected. In late 2006, gaming came to eastern Pennsylvania and to Yonkers raceway in the heart of metro New York. This changed the competitive balance in Atlantic City. The following chart details the growth of the northeast gaming market including Atlantic City until the advent of significant competition toward the end of 2006 and shows the decline in revenue in Atlantic City resulting from this new competition post 2006 and through the recession of 2009.

Source: Various state agencies, company reports, GGH research

Before the change in the competitive dynamic, Atlantic City’s gaming market grew annually through the end of 2006. Atlantic City’s growth prior to 2007 was accomplished through a combination of additional casino venues and the expansion of existing casinos.

$-

$2,000,000,000

$4,000,000,000

$6,000,000,000

$8,000,000,000

$10,000,000,000

$12,000,000,000

$14,000,000,000

Northeast Gaming Revenues

Atlantic City

Connecticut

Delaware

New York

Rhode Island

West Virginia

Maine

PA

Total Demand

Gaming Expansion in New Jersey January 2016

11 | P a g e

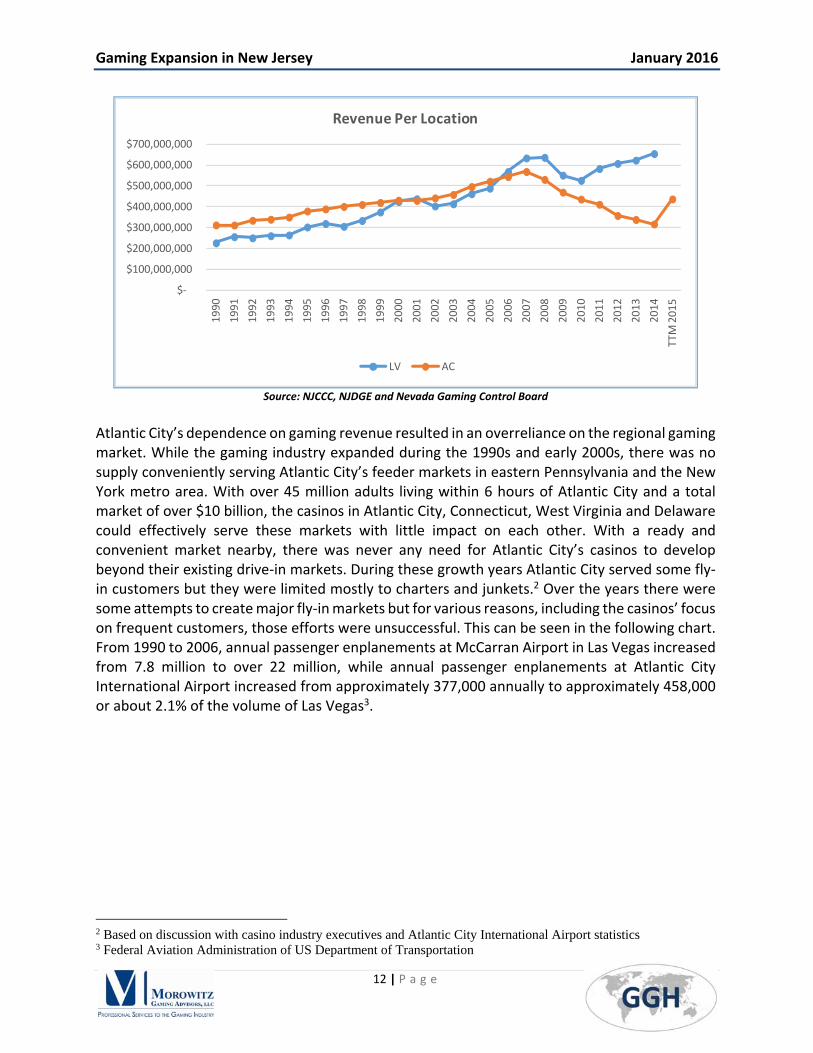

During this period of continuous gaming growth, a combination of factors including, but not limited to regulatory constraints, inertia and a lack of competition resulted in the industry looking inward and a focus on high frequency gamers took hold. While Las Vegas was diversifying its business and non‐gaming was becoming a larger part of its revenue base1, Atlantic City remained dependent on gaming revenue. We can see this dichotomy in the following chart. Atlantic City realized over 80% of its revenues from gaming throughout the 1990s and up to the mid‐2000s before seeing that percentage decline to around 70%. During this period, large Las Vegas Strip properties became less reliant on gaming revenues as their percentage of total revenues declined from 57% in 1990 to 37% in 2015.

Source: NJCCC, NJDGE and Nevada Gaming Control Board

Interestingly, Atlantic City and Las Vegas Strip revenue per property rose in lockstep with each other until 2007. This is when Atlantic City’s reliance on gaming became apparent. As a result of several years of investment and diversification, Las Vegas casinos continued on an upward trajectory (aside from a recession induced trough). Atlantic City casinos however saw their average revenues decline to $317 million per casino before heading upward in 2015 (with less casinos) to $437 million. Coupled with the increase in the percentage of non‐gaming revenue, this indicates a strategic shift is occurring in Atlantic City.

1 Based on study of Las Vegas Strip large property ($72 million and over gaming revenues) and profit and loss statements included in Nevada Gaming Abstract (Nevada Gaming Control Board publication)

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

90.0%

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

TTM 2015

Gaming as % of Total Revenue

LV % Gaming AC % Gaming

Gaming Expansion in New Jersey January 2016

12 | P a g e

Source: NJCCC, NJDGE and Nevada Gaming Control Board

Atlantic City’s dependence on gaming revenue resulted in an overreliance on the regional gaming market. While the gaming industry expanded during the 1990s and early 2000s, there was no supply conveniently serving Atlantic City’s feeder markets in eastern Pennsylvania and the New York metro area. With over 45 million adults living within 6 hours of Atlantic City and a total market of over $10 billion, the casinos in Atlantic City, Connecticut, West Virginia and Delaware could effectively serve these markets with little impact on each other. With a ready and convenient market nearby, there was never any need for Atlantic City’s casinos to develop beyond their existing drive‐in markets. During these growth years Atlantic City served some fly‐in customers but they were limited mostly to charters and junkets.2 Over the years there were some attempts to create major fly‐in markets but for various reasons, including the casinos’ focus on frequent customers, those efforts were unsuccessful. This can be seen in the following chart. From 1990 to 2006, annual passenger enplanements at McCarran Airport in Las Vegas increased from 7.8 million to over 22 million, while annual passenger enplanements at Atlantic City International Airport increased from approximately 377,000 annually to approximately 458,000 or about 2.1% of the volume of Las Vegas3.

2 Based on discussion with casino industry executives and Atlantic City International Airport statistics 3 Federal Aviation Administration of US Department of Transportation

$‐

$100,000,000

$200,000,000

$300,000,000

$400,000,000

$500,000,000

$600,000,000

$700,000,000

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

TTM 2015

Revenue Per Location

LV AC

Gaming Expansion in New Jersey January 2016

13 | P a g e

Source: Federal Aviation Administration of US Department of Transportation

Despite this lack of air service and reliance on a regional market, Atlantic City’s casinos flourished. From 1990 through 2006 industry Earnings Before Interest, Taxes, Depreciation and Amortization (EBITDA) increased from $500 million to $1.2 billion4, a compound annual growth rate (CAGR) of 5.7%.

Source: NJCCC

In 2006, competition loomed in Atlantic City’s feeder markets. New gaming legislation and expansion would bring casino gaming to eastern Pennsylvania and the New York metro market. At the time, the general consensus was that Atlantic City would survive this onslaught because high tax rates in the new jurisdictions would limit investment in those new casinos. However,

4 Atlantic City casinos industry quarterly reports and individual casinos quarterly reports supplies by NJ Casino Control Commission (NJCCC)

‐

5,000,000

10,000,000

15,000,000

20,000,000

25,000,000

Passenger Emplanements

Atlantic City Las Vegas

$‐

$0.2

$0.4

$0.6

$0.8

$1.0

$1.2

$1.4

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

Atlantic City 1990‐2006 ‐ EBITDA Trends ($ Billion)

Gaming Expansion in New Jersey January 2016

14 | P a g e

despite significant investment in Atlantic City, the casinos there were still dependent on convenience oriented, high frequency gamers and those gamers would switch their allegiance to more conveniently located competitors. Atlantic City was thus unprepared for the changing dynamics of a newly competitive market. Competition and Decline Competition in the northeast heated up in 2006 and 2007 with the expansion of gaming in Pennsylvania and New York. During this period casinos opened along the border in Pennsylvania in Chester, Philadelphia, Bensalem, Bethlehem, Mount Airy and Scranton – Wilkes Barre. In New York during the same period a racino opened at Yonkers Raceway just north of New York City, followed by another in 2011 at Aqueduct Racetrack (now Resorts World) in Queens. Casinos also opened in Maryland in 2012 through 2014. This new competition in Atlantic City’s previously underserved feeder markets effectively encircled Atlantic City and combined with Atlantic City’s focus on high frequency gaming customers, caused the industry to decline.

New Casinos Impacting Atlantic City 2007‐2014

The timeline on the following page depicts the downward trend of Atlantic City gaming revenues as various events occurred starting in 20075.

5 Based on GGH/MGA analysis of news archives, gaming regulatory filings, proprietary database, company news releases and company public filings

Gaming Expansion in New Jersey January 2016

15 | P a g e

Timeline of Events Impacting Atlantic City and Gaming Revenue by Year

Developments

EconomyFinancial markets turn negative mid

2007

Lehman Brothers Bankruptcy Sep '08

Small recoveryRecovery Continues

AC

Casinos close for three days for

budget impasse in Jul '06

Harrahs Pool and major expansion opens in Spring; Borgata opens

Water Club Jun '08; Taj Mahal hotel

tow er opens in Q4

Resorts sale closes Dec '10

Landry's acquires Trump Marina May '11; Casinos close for three days in

August for Hurricane Irene

Casinos close for 5 days due to

Hurricane Sandy Oct. 2012; Revel opens Apr '12

Online Gambling Nov '13

Four casinos close in 2014:

Atlantic Club Jan; Show boat Aug; Plaza and Revel

Sep

NYYonkers opens Oct

'06

Yonkers expands to 5,000 slots by

end of Mar

Resorts World opens Oct '11

Resorts World expands to 5,000 slots by Jan '12

PA

Mohegan Pocono opens Nov '06;

Phila. Park opens Dec '06

Harrahs Chester opens Jan '07; Mt Airy opens Oct '07

Mohegan opens permanent facility Aug '08; Penn Nat'l

opens Feb '08

Sands Bethlehem opens May '09

Phila.Park opens permanent facility

Jan '10; Table Games Jul '10;

SugarHouse opens Sep '10

Sands Bethlehem opens hotel May

'11

Valley Forge opens Mar '12

Mohegan Pocono opens new hotel

CT

Foxw oods MGM opens May '08;

Mohegan expansion opens in

Sep '08;

DESports Wagering

Sep '09Table Games Jun

'10Online Gambling

MDHollyw ood

Perryville opens Sep '10

Ocean Dow ns opens Jan '11

Live! opens Jun '12Perryville and Live! offer table games

Mar/Apr '13

Horseshoe opens Aug '14

$5,018,276,523$5,217,877,474

$4,920,786,970

$4,545,235,597

$3,943,171,237

$3,564,330,358$3,317,720,532

$3,051,335,548$2,862,068,918

$2,619,250,906$2,425,177,507

$0

$1,000,000,000

$2,000,000,000

$3,000,000,000

$4,000,000,000

$5,000,000,000

$6,000,000,000

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 TTM Sep '15

Atlantic City Gaming Revenues

Gaming Expansion in New Jersey January 2016

16 | P a g e

From 2006 through 2013, gaming industry net revenues declined from $5.1 billion to $3.0 billion while industry operating profits (EBITDA) declined from $1.2 billion to $0.1 billion during the same period. As a result, and despite the opening of Revel casino in 2012, several casinos closed in 2014 (Atlantic Club, Showboat, Revel and Trump Plaza), leading to further revenue declines, down to $2.6 billion as of September 2015. However, the closure of those casinos in 2014 led to the right sizing of the industry and profits have recovered from their low of $83.9 million in 2013, to $183.5 million in 2014 and $400.5 million for the trailing twelve months ended September 2015. The right sizing of the industry and increased profits clearly indicates the industry has stabilized.

Source: NJDGE, GGH analysis

Stabilization The trend in profits by individual casinos reveals how the industry has stabilized and is trending upward. Since the industry’s nadir in 2013 when EBITDA hit $83.9 million, EBITDA has recovered to $400.5 million. Essentially, the weakest casinos have closed, taking their losses with them. What is left are eight casinos who are beginning to re‐invest and diversify their revenue and are on a significantly positive trajectory, as well as two purely digital companies in start‐up mode that are heading toward profitability. Only the Taj Mahal is operating at negative EBITDA and that is principally due to its ongoing bankruptcy and labor issues that presumably will be resolved once they emerge from bankruptcy and new leadership takes control. The table below depicts EBITDA by casino from 2013 through the most recent twelve month period ending in September of 2015. EBITDA at remaining casinos (those still open) rose by $147.9 million since the end of 2014 and $173.9 million since 2013. All land based casinos6 (except the Taj Mahal) saw increases since 2013.7

6 Caesars Interactive and Resorts Digital have no land based operations 7 Individual company results also impacted by real estate tax appeals and refunds, some of which may be non-recurring.

$1.2

$1.1

$0.8

$0.6

$0.4 $0.3

$0.2 $0.1

$0.2

$0.4

$‐

$1.0

$2.0

$3.0

$4.0

$5.0

$6.0

$‐

$0.2

$0.4

$0.6

$0.8

$1.0

$1.2

$1.4

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Net Reven

ue

EBITDA

Atlantic City Casino IndustryNet Revenue and EBITDA Trend ($Billion)

EBITDA Net Revenue

Gaming Expansion in New Jersey January 2016

17 | P a g e

Atlantic City Casinos – EBITDA Trends ($ Million)

Source: NJDGE and GGH analysis, Resorts Digital still in start‐up mode

At $400 million, industry EBITDA is at its highest point since before 2010 and is trending upward.

Source: NJDGE and GGH analysis

The improvement in industry profitability can be explained by several factors. First, the market has right sized. In 2014, there simply was too much capacity for the market as it is currently configured. Atlantic City’s casinos are undergoing fundamental change. Whereby the industry was previously laser focused on high frequency casino gamers, it is now evolving into one more

2013 2014

TTM Sept

2015

Change

from 2013

%

Change

from

2013

Change

from 2014

%

Change

from

2014

Bally's 4,968$ (6,722)$ 13,326$ 8,358$ 168.2% 20,048$ 298.2%

Borgata 119,413$ 156,076$ 194,319$ 74,906$ 62.7% 38,243$ 24.5%

Caesars 41,015$ 32,045$ 56,300$ 15,285$ 37.3% 24,255$ 75.7%

Caesars Interactive (1,534)$ (13,297)$ 914$ 2,448$ 159.6% 14,211$ 106.9%

Golden Nugget (10,886)$ 2,256$ 18,449$ 29,335$ 269.5% 16,193$ 717.8%

Harrah's 55,711$ 47,276$ 82,413$ 26,702$ 47.9% 35,137$ 74.3%

Resorts (12,625)$ 517$ 9,703$ 22,328$ 176.9% 9,186$ 1776.8%

Resort's Digital ‐$ (1,664)$ (4,925)$ (4,925)$ N/A (3,261)$ N/A

Tropicana 17,555$ 52,224$ 35,442$ 17,887$ 101.9% (16,782)$ ‐32.1%

Taj Mahal 13,016$ (16,048)$ (5,407)$ (18,423)$ ‐141.5% 10,641$ 66.3%

ACH (13,295)$ (1,853)$ ‐$ 13,295$ 100.0% 1,853$ 100.0%

Showboat 13,769$ (2,492)$ ‐$ (13,769)$ ‐100.0% 2,492$ ‐100.0%

Trump Plaza (11,763)$ (15,118)$ ‐$ 11,763$ 100.0% 15,118$ 100.0%

Revel (131,428)$ (49,747)$ ‐$ 131,428$ 100.0% 49,747$ 100.0%

Total All Casinos 83,916$ 183,453$ 400,534$ 316,618$ 377.3% 217,081$ 118.3%

Remaining Casinos 226,633$ 252,663$ 400,534$ 173,901$ 76.7% 147,871$ 58.5%

Former Casinos (142,717)$ (69,210)$ ‐$ 142,717$ 100.0% 69,210$ 100.0%

$1.2 $1.1

$0.8

$0.6

$0.4 $0.3

$0.2 $0.1

$0.2

$0.4

$‐

$0.2

$0.4

$0.6

$0.8

$1.0

$1.2

$1.4

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

EBITDA

Atlantic City Casino Industry EBITDA Trend ($Billion)

EBITDA

Gaming Expansion in New Jersey January 2016

18 | P a g e

like that of Las Vegas or even Reno where non‐gaming revenues are over 51%, more diversified and more reliant on non‐gaming and entertainment to drive profitability. Second and along these lines, the remaining casinos have made several investments in non‐gaming amenities to enhance their facilities and appeal to a more diverse audience. Recent investments include the following:

Resorts Casino Hotel invested in a Margaritaville themed destination dining and entertainment facility, added several quick serve dining options, added conference space and upgraded its rooms, casino floor and public areas.

The Borgata developed an outdoor entertainment facility and is improving its nightlife offering.

The Tropicana added a high end health club, improved its boardwalk retail offering and façade, added a high tech light show and improved its room product.

Harrah’s added a 100,000 square‐foot meeting space expansion including two 50,000 square‐foot ballrooms. The conference center has been deemed the largest hotel‐conference center complex from Baltimore to Boston and will expand Atlantic City’s meeting and convention market.

The Golden Nugget received approval to add two luxury suites that should draw high end gamers from its other properties, allow it to expand its entertainment offerings and attract higher end acts and act as a mid‐week meeting space and hospitality space to attract additional meetings to the property.

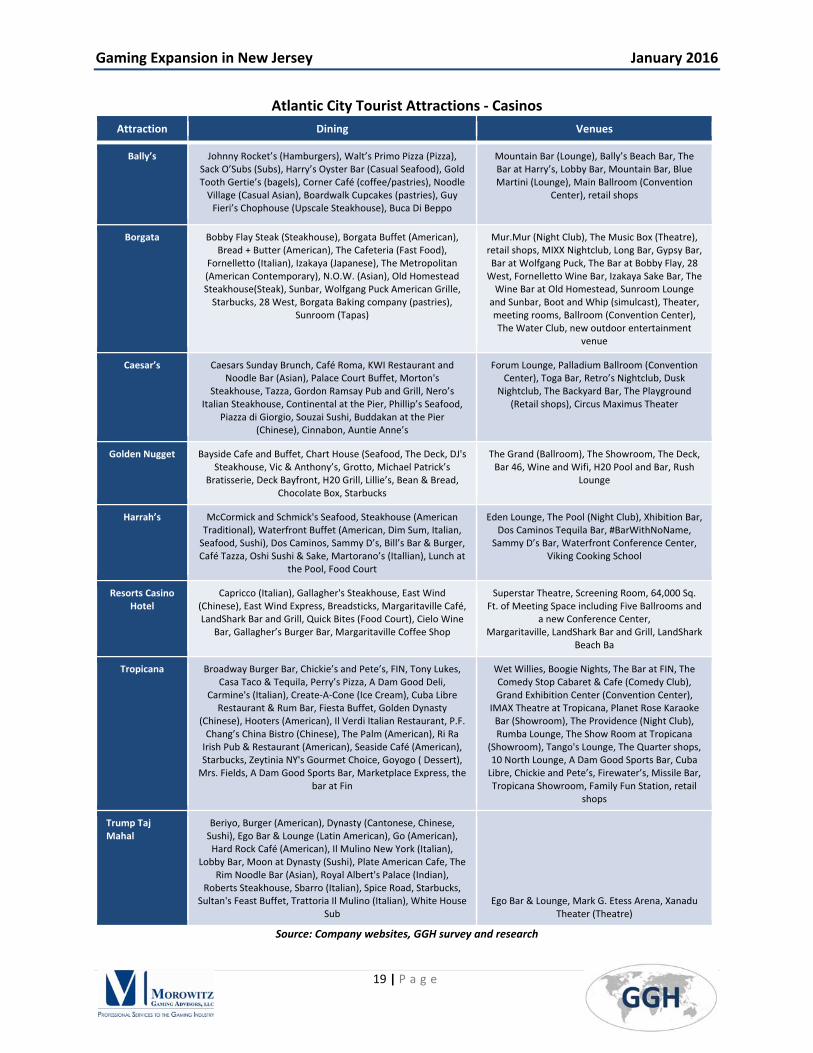

Finally, the City’s non‐gaming offerings have made Atlantic City a true destination resort. The City offers a critical mass of attractions that together lead to over 23 million visitors annually. The following table lists the non‐gaming offerings at Atlantic City casinos.

Gaming Expansion in New Jersey January 2016

19 | P a g e

Atlantic City Tourist Attractions ‐ Casinos

Attraction Dining Venues

Bally’s Johnny Rocket’s (Hamburgers), Walt’s Primo Pizza (Pizza), Sack O’Subs (Subs), Harry’s Oyster Bar (Casual Seafood), Gold Tooth Gertie’s (bagels), Corner Café (coffee/pastries), Noodle Village (Casual Asian), Boardwalk Cupcakes (pastries), Guy Fieri’s Chophouse (Upscale Steakhouse), Buca Di Beppo

Mountain Bar (Lounge), Bally’s Beach Bar, The Bar at Harry’s, Lobby Bar, Mountain Bar, Blue Martini (Lounge), Main Ballroom (Convention

Center), retail shops

Borgata Bobby Flay Steak (Steakhouse), Borgata Buffet (American), Bread + Butter (American), The Cafeteria (Fast Food),

Fornelletto (Italian), Izakaya (Japanese), The Metropolitan (American Contemporary), N.O.W. (Asian), Old Homestead Steakhouse(Steak), Sunbar, Wolfgang Puck American Grille, Starbucks, 28 West, Borgata Baking company (pastries),

Sunroom (Tapas)

Mur.Mur (Night Club), The Music Box (Theatre), retail shops, MIXX Nightclub, Long Bar, Gypsy Bar, Bar at Wolfgang Puck, The Bar at Bobby Flay, 28 West, Fornelletto Wine Bar, Izakaya Sake Bar, The Wine Bar at Old Homestead, Sunroom Lounge and Sunbar, Boot and Whip (simulcast), Theater, meeting rooms, Ballroom (Convention Center), The Water Club, new outdoor entertainment

venue

Caesar’s Caesars Sunday Brunch, Café Roma, KWI Restaurant and Noodle Bar (Asian), Palace Court Buffet, Morton's

Steakhouse, Tazza, Gordon Ramsay Pub and Grill, Nero’s Italian Steakhouse, Continental at the Pier, Phillip’s Seafood,

Piazza di Giorgio, Souzai Sushi, Buddakan at the Pier (Chinese), Cinnabon, Auntie Anne’s

Forum Lounge, Palladium Ballroom (Convention Center), Toga Bar, Retro’s Nightclub, Dusk

Nightclub, The Backyard Bar, The Playground (Retail shops), Circus Maximus Theater

Golden Nugget Bayside Cafe and Buffet, Chart House (Seafood, The Deck, DJ's Steakhouse, Vic & Anthony’s, Grotto, Michael Patrick’s

Bratisserie, Deck Bayfront, H20 Grill, Lillie’s, Bean & Bread, Chocolate Box, Starbucks

The Grand (Ballroom), The Showroom, The Deck, Bar 46, Wine and Wifi, H20 Pool and Bar, Rush

Lounge

Harrah’s McCormick and Schmick's Seafood, Steakhouse (American Traditional), Waterfront Buffet (American, Dim Sum, Italian, Seafood, Sushi), Dos Caminos, Sammy D’s, Bill’s Bar & Burger, Café Tazza, Oshi Sushi & Sake, Martorano’s (Itallian), Lunch at

the Pool, Food Court

Eden Lounge, The Pool (Night Club), Xhibition Bar, Dos Caminos Tequila Bar, #BarWithNoName,

Sammy D’s Bar, Waterfront Conference Center, Viking Cooking School

Resorts Casino Hotel

Capricco (Italian), Gallagher's Steakhouse, East Wind (Chinese), East Wind Express, Breadsticks, Margaritaville Café, LandShark Bar and Grill, Quick Bites (Food Court), Cielo Wine

Bar, Gallagher’s Burger Bar, Margaritaville Coffee Shop

Superstar Theatre, Screening Room, 64,000 Sq. Ft. of Meeting Space including Five Ballrooms and

a new Conference Center, Margaritaville, LandShark Bar and Grill, LandShark

Beach Ba

Tropicana Broadway Burger Bar, Chickie’s and Pete’s, FIN, Tony Lukes, Casa Taco & Tequila, Perry’s Pizza, A Dam Good Deli,

Carmine's (Italian), Create‐A‐Cone (Ice Cream), Cuba Libre Restaurant & Rum Bar, Fiesta Buffet, Golden Dynasty

(Chinese), Hooters (American), Il Verdi Italian Restaurant, P.F. Chang’s China Bistro (Chinese), The Palm (American), Ri Ra Irish Pub & Restaurant (American), Seaside Café (American), Starbucks, Zeytinia NY's Gourmet Choice, Goyogo ( Dessert), Mrs. Fields, A Dam Good Sports Bar, Marketplace Express, the

bar at Fin

Wet Willies, Boogie Nights, The Bar at FIN, The Comedy Stop Cabaret & Cafe (Comedy Club), Grand Exhibition Center (Convention Center),

IMAX Theatre at Tropicana, Planet Rose Karaoke Bar (Showroom), The Providence (Night Club), Rumba Lounge, The Show Room at Tropicana

(Showroom), Tango's Lounge, The Quarter shops, 10 North Lounge, A Dam Good Sports Bar, Cuba Libre, Chickie and Pete’s, Firewater’s, Missile Bar, Tropicana Showroom, Family Fun Station, retail

shops

Trump Taj Mahal

Beriyo, Burger (American), Dynasty (Cantonese, Chinese, Sushi), Ego Bar & Lounge (Latin American), Go (American), Hard Rock Café (American), Il Mulino New York (Italian),

Lobby Bar, Moon at Dynasty (Sushi), Plate American Cafe, The Rim Noodle Bar (Asian), Royal Albert's Palace (Indian),

Roberts Steakhouse, Sbarro (Italian), Spice Road, Starbucks, Sultan's Feast Buffet, Trattoria Il Mulino (Italian), White House

Sub Ego Bar & Lounge, Mark G. Etess Arena, Xanadu

Theater (Theatre)

Source: Company websites, GGH survey and research

Gaming Expansion in New Jersey January 2016

20 | P a g e

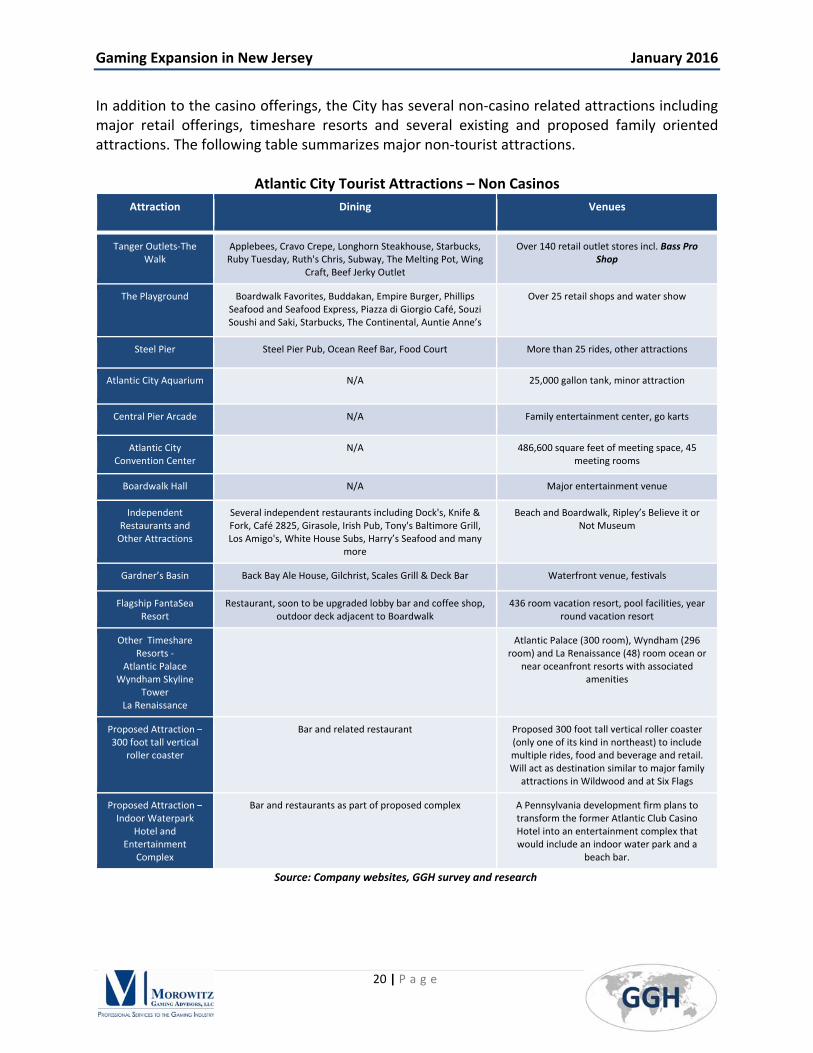

In addition to the casino offerings, the City has several non‐casino related attractions including major retail offerings, timeshare resorts and several existing and proposed family oriented attractions. The following table summarizes major non‐tourist attractions.

Atlantic City Tourist Attractions – Non Casinos

Attraction Dining Venues

Tanger Outlets‐The Walk

Applebees, Cravo Crepe, Longhorn Steakhouse, Starbucks, Ruby Tuesday, Ruth's Chris, Subway, The Melting Pot, Wing

Craft, Beef Jerky Outlet

Over 140 retail outlet stores incl. Bass Pro Shop

The Playground Boardwalk Favorites, Buddakan, Empire Burger, Phillips Seafood and Seafood Express, Piazza di Giorgio Café, Souzi Soushi and Saki, Starbucks, The Continental, Auntie Anne’s

Over 25 retail shops and water show

Steel Pier Steel Pier Pub, Ocean Reef Bar, Food Court More than 25 rides, other attractions

Atlantic City Aquarium N/A 25,000 gallon tank, minor attraction

Central Pier Arcade N/A Family entertainment center, go karts

Atlantic City Convention Center

N/A 486,600 square feet of meeting space, 45 meeting rooms

Boardwalk Hall N/A Major entertainment venue

Independent Restaurants and Other Attractions

Several independent restaurants including Dock's, Knife & Fork, Café 2825, Girasole, Irish Pub, Tony's Baltimore Grill, Los Amigo's, White House Subs, Harry’s Seafood and many

more

Beach and Boardwalk, Ripley’s Believe it or Not Museum

Gardner’s Basin Back Bay Ale House, Gilchrist, Scales Grill & Deck Bar Waterfront venue, festivals

Flagship FantaSea Resort

Restaurant, soon to be upgraded lobby bar and coffee shop, outdoor deck adjacent to Boardwalk

436 room vacation resort, pool facilities, year round vacation resort

Other Timeshare Resorts ‐

Atlantic Palace Wyndham Skyline

Tower La Renaissance

Atlantic Palace (300 room), Wyndham (296 room) and La Renaissance (48) room ocean or

near oceanfront resorts with associated amenities

Proposed Attraction – 300 foot tall vertical

roller coaster

Bar and related restaurant Proposed 300 foot tall vertical roller coaster (only one of its kind in northeast) to include multiple rides, food and beverage and retail. Will act as destination similar to major family

attractions in Wildwood and at Six Flags

Proposed Attraction – Indoor Waterpark

Hotel and Entertainment

Complex

Bar and restaurants as part of proposed complex A Pennsylvania development firm plans to transform the former Atlantic Club Casino Hotel into an entertainment complex that would include an indoor water park and a

beach bar.

Source: Company websites, GGH survey and research

Gaming Expansion in New Jersey January 2016

21 | P a g e

The strategic shift from gaming centric to a tourist destination coupled with the non‐casino offerings is fundamentally changing the visitor profile of Atlantic City. The following table summarizes the visitor profile in 2013 vs. 2004. It shows how the primary purpose of visiting Atlantic City has shifted from gaming to more of a leisure orientation. In 2004, 85% of visitors to Atlantic City reported gambling as the primary purpose of their trip. As of 2013 that percentage had declined to 27% and had been replaced mostly by people looking for a getaway or visiting friends and family8.

Source: ACCVA, Stockton University

Atlantic City’s Gaming Industry Today Atlantic City’s casinos today are a $3.5 billion industry (gross revenue), featuring 13,424 hotel rooms and employing over 23,750 people in a region with total employment of 133,0009, with total wages (not including tips) of over $590 million10. The Atlantic City casinos spent over $1.2 billion on goods and services in 2014, approximately 41% of which was spent in Atlantic County and 58% in New Jersey. The casinos collectively have taxable value of $3.9 billion (54% of the City’s ratable base)11. Despite their decline, they remain the most viable and important industry in the region. As of September 30, 2015 the industry earned operating profits of $523.0 million and EBITDA of $400.5 million, up from $339.5 million and $183.5 million respectively at the end of 2014.

8 Visitor surveys for 2004 and 2013 were completed by two different entities and reporting categories are slightly different. Although the methodology for these two surveys was somewhat different, potentially inflating the percentage in 2003, the essential point remains; the core reason for visiting Atlantic City is changing. 9 Bureau of Labor Statistics data for Atlantic City‐Hammonton MSA as of September 2015 10 Estimate based on 2014 data at remaining casinos. Tips by casino operator estimates adds another 15% or approximately $90 million. 11 GGH research and information gleaned from Atlantic City 2015 – Series A Bond Offering Memorandum

0% 10% 20% 30% 40% 50% 60% 70% 80% 90%

Other

Visit friends/Family

Special Event

Vacation/Getaway

Gamble

Business Meeting

Conv/Trade Show

Visitor Profile Survey ‐ Primary Purpose of Trip

2004 2013

Gaming Expansion in New Jersey January 2016

22 | P a g e

Key Atlantic City Statistics ($000)

Source: NJDGE and GGH research

While the gaming industry has declined, it remains vibrant and is still a vital part of the local economy. It accounts for approximately 60% of the leisure and hospitality employment base12 with jobs that are generally considered well paying for the area and in most cases include benefits. The leisure and hospitality industry is the largest employment segment for the Atlantic City‐Hammonton MSA (which covers all of Atlantic County as defined by the Bureau of Labor Statistics), representing approximately 30% of all employment.

12 Based on Bureau of Labor Statistics data for Atlantic City‐Hammonton MSA employment by industry

2014 TTM Sept 2015

Revenue:

Casino 2,669,976$ 2,497,703$

Rooms 472,409 405,931

Food and Beverage 485,210 442,782

Other 180,383 152,377

Total Revenue 3,807,978$ 3,498,793$

Less: Promotional Allowances 982,382 862,164

Net Revenue 2,825,596$ 2,636,629$

Costs and Expenses:

Casino 1,163,855 1,048,804

Rooms, Food & Beverage 344,793 292,943

General, Administrative & Other 977,479 771,911

Total Costs and Expenses 2,486,127$ 2,113,658$

Gross Operating Profit 339,469$ 522,971$

Industry EBITDA 183,453$ 400,534$

Total Employees 28,259 23,753 1

Wages and Salaries 684,032$ 591,000$ 2

1 Based on November employment report

2 Estimate based on 2014 wages at remaining casinos

39.8

23.6

21.7

19.2

9.9

6.3

5.6

3.8

2.2

0.7

‐ 5.0 10.0 15.0 20.0 25.0 30.0 35.0 40.0 45.0

Leisure and Hospitality

Government

Trade, Transportation, and Utilities

Education and Health Services

Professional and Business Services

Other Services

Mining, Logging, and Construction

Financial Activities

Manufacturing

Information

ATLANTIC CITY‐HAMMONTON MSA EMPLOYMENT BY INDUSTRY (000)

Gaming Expansion in New Jersey January 2016

23 | P a g e

Source: Bureau of Labor Statistics

Source: Bureau of Labor Statistics

This is a defining moment for Atlantic City, its gaming industry and the region. Atlantic City is changing. Through its various phases (growth, decline and stabilization) it is evolving from a gaming centric city to a multi‐faceted entertainment destination, with gaming as a crucial part of its appeal. After several years of turmoil the gaming industry has stabilized, and it remains the largest regional employer. The industry has rightsized and has made crucial investments to reposition itself. This repositioning appears to be working as profits have increased and are trending upward. The single most important issue facing the region is whether this industry will be allowed to continue its recovery.

Gaming Expansion in New Jersey January 2016

24 | P a g e

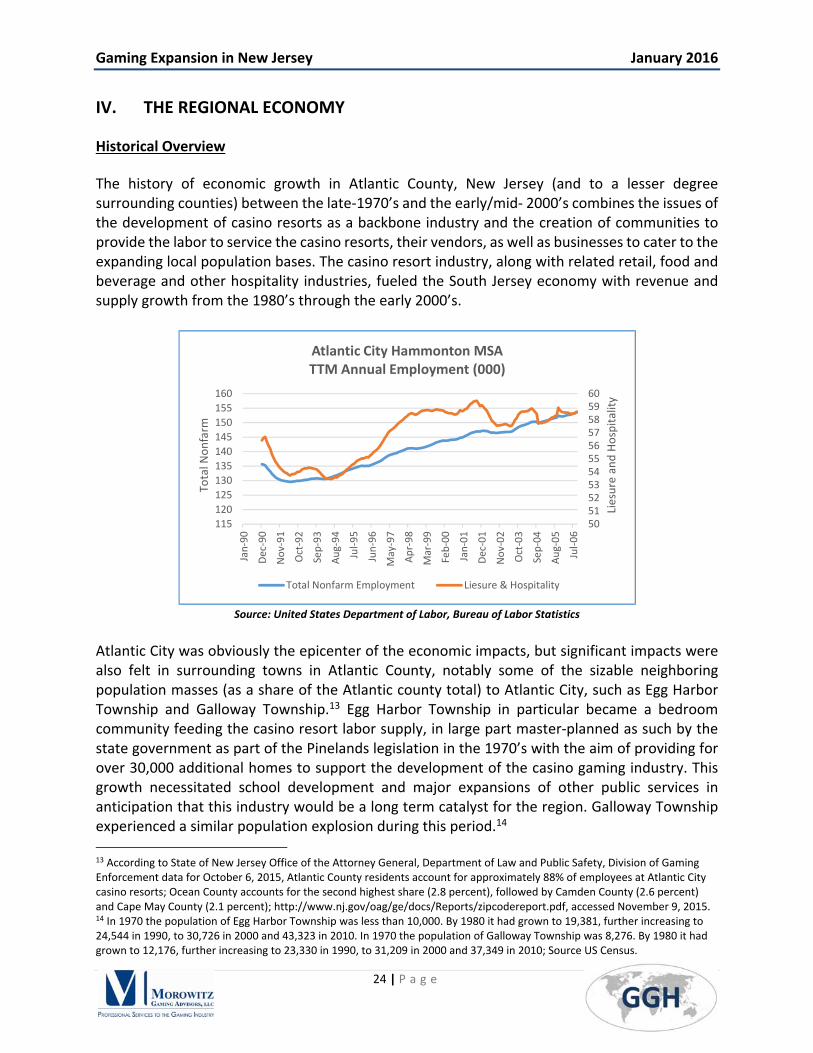

IV. THE REGIONAL ECONOMY

Historical Overview

The history of economic growth in Atlantic County, New Jersey (and to a lesser degree surrounding counties) between the late‐1970’s and the early/mid‐ 2000’s combines the issues of the development of casino resorts as a backbone industry and the creation of communities to provide the labor to service the casino resorts, their vendors, as well as businesses to cater to the expanding local population bases. The casino resort industry, along with related retail, food and beverage and other hospitality industries, fueled the South Jersey economy with revenue and supply growth from the 1980’s through the early 2000’s.

Source: United States Department of Labor, Bureau of Labor Statistics

Atlantic City was obviously the epicenter of the economic impacts, but significant impacts were also felt in surrounding towns in Atlantic County, notably some of the sizable neighboring population masses (as a share of the Atlantic county total) to Atlantic City, such as Egg Harbor Township and Galloway Township.13 Egg Harbor Township in particular became a bedroom community feeding the casino resort labor supply, in large part master‐planned as such by the state government as part of the Pinelands legislation in the 1970’s with the aim of providing for over 30,000 additional homes to support the development of the casino gaming industry. This growth necessitated school development and major expansions of other public services in anticipation that this industry would be a long term catalyst for the region. Galloway Township experienced a similar population explosion during this period.14

13 According to State of New Jersey Office of the Attorney General, Department of Law and Public Safety, Division of Gaming Enforcement data for October 6, 2015, Atlantic County residents account for approximately 88% of employees at Atlantic City casino resorts; Ocean County accounts for the second highest share (2.8 percent), followed by Camden County (2.6 percent) and Cape May County (2.1 percent); http://www.nj.gov/oag/ge/docs/Reports/zipcodereport.pdf, accessed November 9, 2015. 14 In 1970 the population of Egg Harbor Township was less than 10,000. By 1980 it had grown to 19,381, further increasing to 24,544 in 1990, to 30,726 in 2000 and 43,323 in 2010. In 1970 the population of Galloway Township was 8,276. By 1980 it had grown to 12,176, further increasing to 23,330 in 1990, to 31,209 in 2000 and 37,349 in 2010; Source US Census.

5051525354555657585960

115

120

125

130

135

140

145

150

155

160

Jan‐90

Dec‐90

Nov‐91

Oct‐92

Sep‐93

Aug‐94

Jul‐95

Jun‐96

May‐97

Apr‐98

Mar‐99

Feb‐00

Jan‐01

Dec‐01

Nov‐02

Oct‐03

Sep‐04

Aug‐05

Jul‐06

Liesure and Hospitality

Total N

onfarm

Atlantic City Hammonton MSA TTM Annual Employment (000)

Total Nonfarm Employment Liesure & Hospitality

Gaming Expansion in New Jersey January 2016

25 | P a g e

The increased competition from out of state casinos documented in the prior section of this report has led to market saturation, resulting in a sharp gaming revenue and patronage decline for casinos in Atlantic City, as well as revenues and patronage for affiliated hospitality industries. The sustained decline led to the closure of four Atlantic City casino resorts in 2014, as well as many other businesses outside of the casino resort establishments, as fewer gamer visits equates to a decline in tourist dollars being spent throughout the economy. Industries providing services to the casino resorts have also suffered as their client base has shrunk with the casino resort closures. Additionally, the casino hotel workforce in the region has declined by more than 20,000 since 2005, meaning that there has been a significant decline in regional consumer spending outside of the resort environment as well, along with pressure on the housing market that has resulted in/from Atlantic County having one of the highest foreclosure rate in the country.15

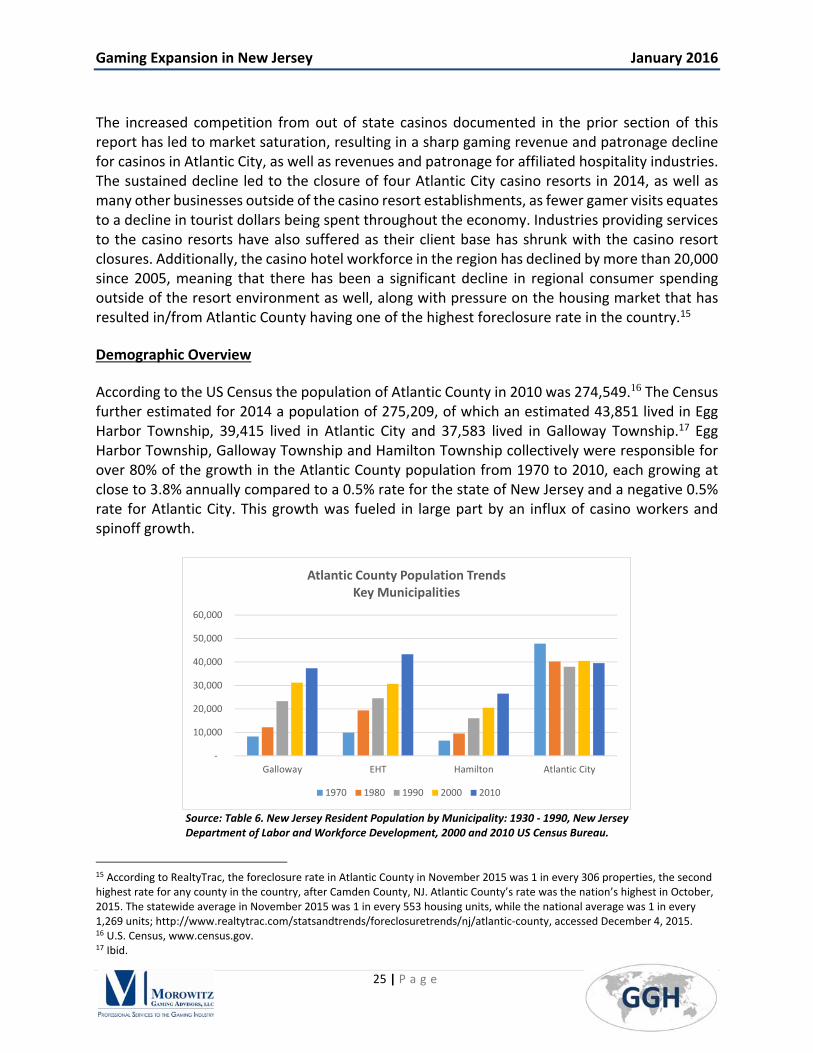

Demographic Overview

According to the US Census the population of Atlantic County in 2010 was 274,549.16 The Census further estimated for 2014 a population of 275,209, of which an estimated 43,851 lived in Egg Harbor Township, 39,415 lived in Atlantic City and 37,583 lived in Galloway Township.17 Egg Harbor Township, Galloway Township and Hamilton Township collectively were responsible for over 80% of the growth in the Atlantic County population from 1970 to 2010, each growing at close to 3.8% annually compared to a 0.5% rate for the state of New Jersey and a negative 0.5% rate for Atlantic City. This growth was fueled in large part by an influx of casino workers and spinoff growth.

Source: Table 6. New Jersey Resident Population by Municipality: 1930 ‐ 1990, New Jersey Department of Labor and Workforce Development, 2000 and 2010 US Census Bureau.

15 According to RealtyTrac, the foreclosure rate in Atlantic County in November 2015 was 1 in every 306 properties, the second highest rate for any county in the country, after Camden County, NJ. Atlantic County’s rate was the nation’s highest in October, 2015. The statewide average in November 2015 was 1 in every 553 housing units, while the national average was 1 in every 1,269 units; http://www.realtytrac.com/statsandtrends/foreclosuretrends/nj/atlantic‐county, accessed December 4, 2015. 16 U.S. Census, www.census.gov. 17 Ibid.

‐

10,000

20,000

30,000

40,000

50,000

60,000

Galloway EHT Hamilton Atlantic City

Atlantic County Population Trends Key Municipalities

1970 1980 1990 2000 2010

Gaming Expansion in New Jersey January 2016

26 | P a g e

A notable assumption by the US Census between 2010 and 2014 for Atlantic County, as well as each of these four jurisdictions within Atlantic County (as can be surmised by the 2010 and 2014 figures), was that population growth was relatively flat between 2010 and 2014 despite the continued economic decline. It is worth noting that the 2014 figures would not capture the impact of the September closures of three casino resorts, or possibly the early‐2014 closure of the Atlantic Club Casino. Those that lost their jobs late in the year likely would not have immediately relocated, or would have been recognized by Census estimators as being a source of potential mass exodus, which appears to have been occurring given the fact that the industry and overall macroeconomic downturn resulted in foreclosure rates in these communities that are amongst the highest in the country. Some former casino resort employees (or others in Atlantic County that have lost their jobs) have left as a result of having their homes foreclosed on or have found job opportunities elsewhere, but many others remain in the area despite losing their jobs, as the prospect of selling one’s home is unattractive when faced with a glut of foreclosed‐upon homes for sale in the market at depressed prices. As a result, regional unemployment rates are much higher than they were prior to the recession, while statewide the unemployment rate is back down to 2008 levels. The size of the Atlantic County and city/township labor forces are smaller than they were prior to the casino‐resort closures, but have not nearly declined at the same level as the regional hospitality industry job decline. Regional unemployment can best be defined as structural, i.e. these former hospitality industry employees may need to learn new skills to find good, new jobs, which could be especially difficult and long‐term as a result of there being few regional developed industry alternatives to transition to. For example, the remaining major employers in Galloway Township and Egg Harbor Township are Stockton University and the Atlanticare Regional Medical Center, neither of which are easy job transitions for people whose work experience has been in the hospitality industry. Similarly, major non‐casino resort employers in Atlantic City include the Atlanticare hospital complex or at The Tanger Outlets, which are large‐scale retail venues along Atlantic Avenue. These retail jobs are the ones that are the easiest transition for those with the skill set of former casino‐resort workers, but they are also at close to minimum wage, much lower than they, on average, historically earned. Based on the US Census’ County Business Patterns data from 2011 to 2013 for the Atlantic City‐Hammonton MSA, it is evident that this is where much of the transition has been, as retail trade has been the largest sector demonstrating employment growth in the metropolitan area (the Census has a lengthy lag in preparing data, as it is currently only available through 2013).18

Further examination of comparative unemployment rates, as well as the hospitality industry’s share of employment declines, will be addressed later in this analysis. The prospect of additional hospitality industry job declines in the face of additional competition, and its other macroeconomic implications, will also be addressed.

18 County Business Patterns, http://censtats.census.gov/cgi‐bin/msanaic/msasect.pl

Gaming Expansion in New Jersey January 2016

27 | P a g e

Macroeconomic and Microeconomic Labor Overviews

Casino Resort Employment Overview

Employment at casino resorts in Atlantic City peaked during the period from 1992 to 2005, generally being in the range of 44,000 to 49,000 employees, declining slightly during the latter years as technology made slot operations more efficient.19 Competitive factors that drove the Atlantic City market downturn brought the employment total down below 40,000 in 2008 and below 35,000 in 2010.20 As a result of the closure of the Atlantic Club in January 2014 and Revel, Showboat and Trump Plaza in September 2014 the total has fallen to less than 24,000, approximately half of the peak total.21

Casino Resort Employment, 2004‐2015

Year Casino employees

2004 year end 45,501

2005 year end 44,542

2006 year end 42,456

2007 year end 40,788

2008 year end 38,585

2009 year end 36,377

2010 year end 34,145

2011 year end 32,827

2012 year end 34,698

2013 year end 32,427

2014 year end 24,817

LTM average (12/2014‐11/2015) 24,314

2015 November 23,764

Source: http://www.nj.gov/oag/ge/employee_licensing.html and NJ Casino Control Commission. The 2014 year‐end figure includes 104 employees at Revel and 26 employees at Trump Plaza, despite both no longer being operational. Similarly, the November 2015 total includes 20 employees at Trump Plaza.

The current (November 2015) employment figures total 23,744 for the remaining eight casinos and are as follows:

Current Casino Employee Figures (November 2015)

Casino Employment

Bally's AC 2,653

Borgata 5,805

Caesars 2,911

Golden Nugget 2,141

Harrah's Marina 3,314

Resorts Casino Hotel 1,823

19 State of New Jersey Casino Control Commission; http://www.state.nj.us/casinos/financia/histori/, accessed November 9, 2015. 20 Ibid. 21 State of New Jersey Office of the Attorney General, Department of Law and Public Safety, Division of Gaming Enforcement; http://www.nj.gov/oag/ge/casinohotelempfigures.html, accessed December 15, 2015.

Gaming Expansion in New Jersey January 2016

28 | P a g e

Tropicana 2,846

Trump Taj Mahal 2,251 Source: State of New Jersey Office of the Attorney General, Division of Gaming Enforcement casino hotel employment figures; http://www.nj.gov/oag/ge/casinohotelempfigures.html. Note: the reported totals do not differentiate between full‐time and part‐time employment.

At present approximately 88% of the Atlantic City casino resort employees reside in Atlantic County, or nearly 21,000 employees.22 Ocean County provides the next largest share, approximately 2.8% of the total (667 employees), followed by Camden County with approximately 2.6% (613 employees) and Cape May County with 2.1% (500 employees).23 The nearly 21,000 jobs in Atlantic County is a significant percentage of the Atlantic County labor force (132,457, as of the third quarter 2015) and employed population (121,308, as of the third quarter 2015), such that any sizable industry layoff in the future will have significant ripple effects on regional consumer spending.24 These ripple effects also are a function of changes in vendor spending by the casino resorts, as any cutback in casino resort spending may result in a decline in revenues by Atlantic County‐based vendors. We provide later in this analysis the historical relationships between casino closures and overall economic activity in Atlantic County, demonstrating that it is not just the Atlantic City casino industry that is at risk if casinos are added in North Jersey, but the entirety of an already fragile South Jersey economy.

State and Atlantic County Labor Overview Atlantic County has a labor force of approximately 132,000, down from over 140,000 a decade ago.25 Atlantic City, Egg Harbor Township and Galloway Township are the major population centers in Atlantic County, each accounting for between 16,000 and 22,000 labor force participants. However, that still amounts to nearly 80,000 persons residing elsewhere in Atlantic County. The labor force in Atlantic City is slowly declining, but reached 16,032 in September, 2015, its lowest monthly total in over 25 years (data was only available for the last 25 years).26

22 State of New Jersey, Office of the Attorney General, Division of Gaming Enforcement, as at October 6, 2015; http://www.nj.gov/oag/ge/docs/Reports/zipcodereport.pdf, accessed December 15, 2015. We note that this is a slightly higher percentage than the reported share of those employed in Atlantic County in all industries also being from within the county (based on Census estimates from 2009‐2013) – according to the US Census Bureau Local Employment Dynamics approximately 80% of those employed in Atlantic County also lived there, followed by Cape May County at 4.4%.

23 Ibid. 24 U.S. Bureau of Labor Statistics non‐seasonally adjusted data, from economagic.com. 25 U.S. Bureau of Labor Statistics 26 Ibid.

Gaming Expansion in New Jersey January 2016

29 | P a g e

Source: U.S. Bureau of Labor Statistics

As noted in the preceding paragraph, casino resort employment has fallen from approximately 45,000 a decade ago to less than 24,000 in 2015. The middle years of this decline coincided with the largest macroeconomic downturn in several generations, but clearly the trajectory here has not corrected itself in concert with the macroeconomic recovery. As demonstrated in the following chart, regional unemployment rates were generally close to statewide unemployment rates before the increased competition and recession, but now average approximately 2% more than the statewide rate. The exception is Atlantic City, where the unemployment rate in the mid‐2000s was approximately 3 to 4% greater than the statewide average. The gap grew during the recession, after which the differential grew to approximately 7% during the summer months and 10% during the winter months.

State, Atlantic County and Local Unemployment Rates

Source: U.S. Bureau of Labor Statistics. Note: State data is seasonally adjusted; County, City and Township data

is not seasonally adjusted.

‐

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

Quarterly Labor Force Totals

Atl County Other Atlantic City Egg Harbor Twp Galloway Twp

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

18.0%

20.0%

Quarterly Unemployment Rates

State Atl County Atl City Egg Harbor Galloway

Gaming Expansion in New Jersey January 2016

30 | P a g e

Due to the fact that there was some economic recovery from 2010 to 2015, it is not possible to graphically depict a clear relationship between the casino resort job losses and the regional employment level impacts on a broader macroeconomic level. Some of those who have lost their casino jobs or casino service jobs have moved to other regions, some have changed careers and moved into other industries, some work in other regions and some no longer work. But with otherwise macroeconomic stability, any new job losses attributable to casino closures or downsizing may not be as easily transitioned into alternative employment as they had during the macroeconomic recovery years. Regional Public Finance and Public Service The regional governments, at both the Atlantic County level and for the municipalities, primarily are funded through property taxes. The majority of these taxes are then spent on schools, along with public works, public safety, health insurance and other fringe benefits (including pensions), municipal bond debt service and public assistance programs. According to the Atlantic County Administration, approximately 40% of Atlantic County residents receive some sort of public assistance. Public school enrolments have not changed significantly over the past decade, but the cost per student has steadily increased as a result of keeping student/teacher ratios consistent and an increasing percentage of students receiving subsidized meals. Health insurance costs are also rapidly increasing, at a much higher rate than the 2% ceiling on tax revenue growth, such that fringe benefits account for an increasing percentage of municipal budgets. The economic downturn has also resulted in a high, and continuously growing, share of the population relying on public assistance. As a result, there has been a need to cut back on other services, freeze salaries or downsize other departments, in order to maintain balanced budgets. Moreover, as a result of new assessment levels for casinos, homeowners and other commercial businesses are experiencing increasing tax bills, providing a disincentive to bring business to the area and for homeowners to stay in the area. This has a snowball effect, as outward migration of residents and businesses simply means higher taxes for those that remain. And those that do remain are experiencing cutbacks in the provision of public services. The situation therefore is already bad for governments and taxpayers. If the economy faces a further downturn with the closure of additional casinos and/or large‐scale labor cutbacks, it is unclear how the municipal governments can continue to function. The current proposed legislation (and potential referendum to voters) suggests that some portion of gaming taxes from north Jersey casinos would provide some public finance assistance to Atlantic City. But as we note below, as well as from the demographic overview above, Atlantic County and Atlantic City’s neighboring townships are directly impacted by anything that happens to the Atlantic City economy. At present these jurisdictions are excluded in the proposed legislation from receiving any support. The following section provides some detail on the financial health of the Atlantic County and municipal governments analyzed for this report.

Gaming Expansion in New Jersey January 2016

31 | P a g e

Atlantic County Atlantic County operates on an approximate $200 million annual budget, not including dedicated tax programs for public health and libraries. From 2010 to 2015 County expenditures have increased at a compound average annual growth rate of 1.3%. Tax revenues have increased at an annual rate of 1.9% during this period, as revenues from other sources, along with surplus funds, have declined over the past six years. Notable changes in the budget have been increased costs for Law and Public Safety for the past two years and rising insurance and pension costs (fringe benefits). In order to annually increase tax revenues it has been necessary to increase the property tax millage rates, increasing the burden on residents and small commercial businesses. The anticipated PILOT tax program for the casino resorts will likely mean a fixed ceiling (adjusted upward by 2% annually) on the taxes paid by the casino resorts, but they could also pay as much as $30 million less if new North Jersey competition arises, further eroding Atlantic City’s Gross Gaming Revenue, one of the factors which determines the amount Atlantic City casinos are required to contribute to the PILOT program each year. In that event, Atlantic County would have to figure a way to make up the budget shortfall by raising taxes on homeowners and other businesses, which currently only makes up a fraction of the revenues received. As a result, there would likely need to be some combination of major spending cuts and tax hikes.

Gaming Expansion in New Jersey January 2016

32 | P a g e

Atlantic County Budget Summaries, 2010‐2015 Atlantic County Budget 2010 2011 2012 2013 2014 2015 CAGR

Total Expenditures $188,750,380 $190,739,294 $194,091,547 $193,837,030 $196,133,473 $201,101,721 1.3%

Support Services $7,988,826 $8,118,833 $7,905,316 $8,053,372 $8,090,263 $7,892,680 ‐0.2%

Direct Services (Planning, Public Works and Human Services)

$29,125,914 $29,001,744 $29,451,468 $29,935,975 $30,343,209 $30,623,158 1.0%

Law & Public Safety $50,378,024 $50,603,828 $50,470,724 $50,729,349 $52,537,721 $54,485,708 1.6%

State Programs $10,894,786 $10,737,696 $11,184,142 $10,968,367 $11,173,711 $11,736,860 1.5%

Fringe Benefits $42,364,809 $44,327,067 $45,710,670 $45,697,012 $46,597,055 $47,565,526 2.3%

Group Insurance* $21,614,556 $21,900,000 $22,853,600 $23,822,000 $23,909,242 $24,376,814 2.4%

Educational Institutions $12,562,000 $12,701,620 $12,790,258 $13,093,764 $13,088,393 $13,091,393 0.8%

State Mandates $2,843,779 $2,987,376 $2,965,150 $3,081,042 $2,636,698 $3,134,697 2.0%

Debt Service $21,780,607 $21,780,823 $21,770,714 $21,770,962 $21,770,962 $21,850,962 0.1%

Major Accounts $8,108,324 $8,277,092 $8,641,288 $8,697,271 $7,835,871 $8,652,583 1.3%

Grants $2,703,311 $2,203,216 $3,201,817 $1,809,916 $2,059,590 $2,068,154 ‐5.2%

Total Revenues $188,750,380 $190,739,294 $194,091,547 $193,837,030 $196,133,473 $201,101,721 1.3%

County Taxes $146,224,156 $149,777,167 $152,745,744 $155,598,082 $156,500,165 $160,646,006 1.9%

Surplus $7,722,000 $7,752,000 $7,743,000 $7,155,000 $7,644,000 $7,474,000 ‐0.7%

General Revenues $34,804,224 $33,210,127 $33,602,803 $31,083,948 $31,989,307 $32,981,714 ‐1.1%

Dedicated Tax Programs Public Health Expenditure $9,584,769 $9,267,534 $9,192,750 $9,078,592 $9,157,135 $9,188,080 ‐0.8%

Public Health Revenues Surplus $577,000 $500,000 $600,000 $550,000 $609,000 $700,000 3.9%

Anticipated Revenues $2,813,314 $2,410,584 $2,283,207 $2,328,123 $2,306,055 $2,314,913 ‐3.8%

Public Health Tax $6,194,455 $6,356,950 $6,309,543 $6,200,469 $6,242,080 $6,173,167 ‐0.1%

Library Expenditures $9,363,043 $9,344,927 $8,953,635 $8,979,000 $8,943,180 $8,679,189 ‐1.5%

Library Revenues Surplus $1,300,000 $1,200,000 $982,000 $1,075,000 $1,075,000 $1,042,008 ‐4.3%

Library Tax $8,063,043 $8,144,927 $7,971,635 $7,904,000 $7,868,180 $7,637,181 ‐1.1%

Source: Atlantic County Annual Budget Summaries, http://www.aclink.org/Budget/index.asp. * Group insurance figure provided as a major component of Fringe.

Gaming Expansion in New Jersey January 2016

33 | P a g e

One of the major challenges facing Atlantic County is that it currently has one of the highest foreclosure rates in the country, with approximately 1 in every 306 housing units in foreclosure. This may make some population estimates unreliable, as residents have been forced out of their homes, with the only reliable measures of inter‐Census populations being school student populations and senior subsidies – in between (the working age population) it is likely that the population has fallen below Census estimates given the increasing number of foreclosures. The chart below depicts foreclosure rates (in percentage terms) for National, New Jersey, Atlantic City, Atlantic County, Absecon/Galloway and Egg Harbor Township and shows the concentration of foreclosure activity in surrounding towns where rates are as much as five times the national average and over two times the New Jersey average.

Source: RealtyTrac; http://www.realtytrac.com/statsandtrends/