Gaap-uccino 1.5 - Part I of III - Final

39

GAAP-uccino V ersion 1.5 Part I of III February 1, 2012

-

Upload

mistervigilante -

Category

Documents

-

view

218 -

download

0

Transcript of Gaap-uccino 1.5 - Part I of III - Final

8/3/2019 Gaap-uccino 1.5 - Part I of III - Final

http://slidepdf.com/reader/full/gaap-uccino-15-part-i-of-iii-final 1/39

GAAP-uccino Version 1.5Part I of III

February 1, 2012

8/3/2019 Gaap-uccino 1.5 - Part I of III - Final

http://slidepdf.com/reader/full/gaap-uccino-15-part-i-of-iii-final 2/39

DisclaimerTHESE MATERIALS SHALL NOT CONSTITUTE AN OFFER TO SELL OR THE SOLICITATION OF AN OFFER TO BUY

ANY INTERESTS IN LONGSHORTTRADER OR ANY OF ITS AFFILIATES. SUCH AN OFFER TO SELL OR

SOLICITATION OF AN OFFER TO BUY INTERESTS MAY ONLY BE MADE PURSUANT TO A DEFINITIVE

SUBSCRIPTION AGREEMENT BETWEEN LONGSHORTTRADER AND AN INVESTOR.

The information contained herein reflects the view of longshorttrader (“LST”) as of the date of publication.

This presentation was not prepared by Greenlight Capital. These views are subject to change without notice

at any time subsequent to the date of issue. LST has no economic interest in the price movement of the

securities discussed in this presentation, but LST’s economic interest is subject to change without notice. All

information provided in this presentation is for informational purposes only and should not be deemed as

investment advice or a recommendation to purchase or sell any specific security. While the information

presented herein is believed to be reliable, no representation or warranty is made concerning the accuracy

of any data presented. In addition, there can be no guarantee that any projection, forecast or opinion in this

presentation will be realized. All trade names, trade marks, service marks, and logos herein are the propertyof their respective owners who retain all proprietary rights over their use. This presentation is confidential

and may not be reproduced without prior written permission from LST.

2

8/3/2019 Gaap-uccino 1.5 - Part I of III - Final

http://slidepdf.com/reader/full/gaap-uccino-15-part-i-of-iii-final 3/39

Table of Contents

• Introduction

• Summary

• The CFO Should Resign

• Threats to the Razor/Blade Myth

• Parallels to Sino-Forest

• Price Target

3

8/3/2019 Gaap-uccino 1.5 - Part I of III - Final

http://slidepdf.com/reader/full/gaap-uccino-15-part-i-of-iii-final 4/39

Introduction

4

8/3/2019 Gaap-uccino 1.5 - Part I of III - Final

http://slidepdf.com/reader/full/gaap-uccino-15-part-i-of-iii-final 5/39

Introduction

• Green Mountain Coffee Roasters’ (GMCR) stock was and remains

one of the best performing stocks trading on the NASDAQ.

$0.00

$5.00

$10.00

$15.00

$20.00

$25.00

$30.00

$35.00

$40.00

$45.00

$50.00

$55.00

$60.00

$65.00

$70.00

$75.00

$80.00

$85.00

$90.00

$95.00

$100.00

$105.00

$110.00

$115.00

$120.00

1/3/2006 1/3/2007 1/3/2008 1/3/2009 1/3/2010 1/3/2011 1/3/2012

GMCR Daily Stock Price- 2006-Present

5

8/3/2019 Gaap-uccino 1.5 - Part I of III - Final

http://slidepdf.com/reader/full/gaap-uccino-15-part-i-of-iii-final 6/39

Introduction

• Compare GAAP earnings (i.e. paper profits) vs economic earnings vs

the stock; you see conflicting stories. This got the critics’ attention.

-

-$1,150,000

-$1,100,000

-$1,050,000

-$1,000,000

-$950,000

-$900,000

-$850,000

-$800,000

-$750,000

-$700,000

-$650,000

-$600,000

-$550,000

-$500,000

-$450,000

-$400,000

-$350,000

-$300,000

-$250,000

-$200,000

-$150,000

-$100,000

-$50,000

$0

$50,000

$100,000

$150,000

$200,000

$250,000

$300,000

2006 2007 2008 2009 2010 2011

Free Cash Flow - All Inclusive

Free Cash flow ex Acquisitions

GAAP Earnings

Free Cash Flow - Proxy for Economic Earnings

Even as

economic/cash

earnings

decreased at an

accelerating rate

Accounting, paper earnings increased…

6Sources: GMCR 10Ks, Thomson Reuters

8/3/2019 Gaap-uccino 1.5 - Part I of III - Final

http://slidepdf.com/reader/full/gaap-uccino-15-part-i-of-iii-final 7/39

Introduction

• GMCR critics include an all-star lineup of accounting/fraud experts

(with many more):

David Einhorn – Allied Capital, Lehman Brothers, Office Depot

Howard Schilit/CFRA – Author of “Financial Shenanigans”

Sam Antar – Crazy Eddie, Overstock.com,

Edward Ketch/Anthony Catanach – Accounting experts, Professors.

The Warrior – One of the greatest financial/accounting fraud experts.

Uncovered various frauds during the dot-com and subprime bubbles

7

8/3/2019 Gaap-uccino 1.5 - Part I of III - Final

http://slidepdf.com/reader/full/gaap-uccino-15-part-i-of-iii-final 8/39

Introduction

• These experts’ (crime fighters) many concerns sound asif they come straight out of a Harvard Business SchoolCase Study: Accounting/Fraud Issues: Overstating Revenue,

Understating Expenses, Capitalizing Expenses, Channel

Stuffing, etc. all to meet Wall Street Estimates Improper Conduct/Violation of Laws: Violations of

Regulation FD, Insider Trading, Securities Fraud, Peculiarrelationship with quasi-captive distributor, etc.

Fundamental Problems: Zero cash flow since Keurig

Acquisition, 100% dependent on external capital, Abysmalearnings quality, reliance on acquisitions to meet/beatexpectations, Reduced/changing transparency of operatingmetrics, Patent expiration, etc.

8Sources: GAAP-ucino by Greenlight Capital, Sam Antar's blog, Grumpy Old Accountant's blog, & sources citing Howard Schilit

8/3/2019 Gaap-uccino 1.5 - Part I of III - Final

http://slidepdf.com/reader/full/gaap-uccino-15-part-i-of-iii-final 9/39

Summary

• Yet there is even more to the story… GMCR Executives have repeatedly lied and mislead; In

particular, CFO Frances Rathke has misrepresented her CPACredentials for at least 8 years. This appears to be aviolation of Vermont law. Rathke even tried to cover this

up recently. The CFO needs to go. A

A

A

A

A A

A

9Source: http://license.reg.state.ma.us/

8/3/2019 Gaap-uccino 1.5 - Part I of III - Final

http://slidepdf.com/reader/full/gaap-uccino-15-part-i-of-iii-final 10/39

Summary

• The Razor/Razor blade Myth Is Under Threat The rising popularity of Reusable K-Cups (such as Ekobrew & Solofill),

replaces the need for k-cups.

Ekobrew and Solofill offer customers a ‘win-win’ – they can drinkhigher quality coffee, for a fraction of the price.

One Ekobrew/Solofill can save a user between $137 - $343 per year,

and on average, $250 per year. This can easily cost GMCR $100s of millions in revenue, and render the business even more unprofitable.

At best (for GMCR), the Ekobrew and Solofill complicate the ‘razor /razor blade model’ and growth trajectory.

A

A

A

A

a

10Sources: LST estimates

8/3/2019 Gaap-uccino 1.5 - Part I of III - Final

http://slidepdf.com/reader/full/gaap-uccino-15-part-i-of-iii-final 11/39

Summary

• Initial Price Target is $15.00/share…then single digits GMCR stock may look reasonably priced, if you trust the

numbers AND believe its high growth continues indefinitely.

However, GAAP Net income does not reflect economic income. Iestimate GMCR’s true net income is closer to ~$60-$120 million.

Once earnings decline, stock has no support until single digits.Note that Research In Motion (RIMM) stock peaked years beforerevenue and earnings did.

• Eerie Similarities to Sino-Forest The economic, accounting, and behavioral similarities between

Sino-Forest and GMCR are disturbing.

The two biggest reasons the market has yet to punish GMCR asseverely as it did Sino-Forest, are GMCR is an Americanbusiness, and its products are visible. Unfortunately, thesereasons provide a false wall of security. Investors/traders equatethe popularity of the product with “there is no fraud.”

11Sources: LST estimates, GMCR 10Ks &

10Qs, Muddy Waters Research

8/3/2019 Gaap-uccino 1.5 - Part I of III - Final

http://slidepdf.com/reader/full/gaap-uccino-15-part-i-of-iii-final 12/39

The CFO Should Resign

12

8/3/2019 Gaap-uccino 1.5 - Part I of III - Final

http://slidepdf.com/reader/full/gaap-uccino-15-part-i-of-iii-final 13/39

The CFO Should Resign

• GMCR Management made some bold claims last quarter to addressEinhorn and the crimefighters’ concerns: “Ultimately, our best response is continuing to run our business with

the utmost of integrity ”

“Those who know this Company and the individuals that cometogether to make our success possible, know how much we value

integrity and respect ” “Though disappointing, we take the recent allegations of misconduct

seriously. Our audit committee has reviewed the allegations and weare confident there is no misconduct. There is no wrongdoing”

• Contrary to the above statements, there is in fact, wrong-doing.

Chief Financial Officer (CFO) Frances Rathke has been FALSELYclaiming to be a Certified Public Accountant (CPA) since first joiningthe company in 2003; She’s been lying for at least 8 years. It wouldappear this violates Vermont law. Rathke should resignimmediately, especially given the many more serious allegations.

13Sources: GMCR Q4 2011 Earnings Call

8/3/2019 Gaap-uccino 1.5 - Part I of III - Final

http://slidepdf.com/reader/full/gaap-uccino-15-part-i-of-iii-final 14/39

The CFO Should Resign

• GMCR Chief Financial Officer (CFO) Frances RathkeClaims to be a Certified Public Accountant (CPA) in 6out of 9 SEC 10K filings. Each 10K states: “Frances G. Rathke has served as Chief Financial Officer of the Company since

October 2003, and as Interim Chief Financial Officer of our Company sinceApril 2003. Prior to that, Ms. Rathke worked as a financial consultant with

various food manufacturers and food retailers from September 2000 to April2003. One of these consulting assignments included the position of InterimChief Financial Officer for Wild Oats Markets, Inc., a supermarket chain, fromJuly 2001 to December 2001. Prior to this, Ms. Rathke served as Chief Financial Officer for Ben & Jerry’s Homemade, Inc., an ice creammanufacturer, from April 1989 to August 2000. From September 1982 toMarch 1989, Ms. Rathke practiced public accounting and auditing withCoopers & Lybrand LLC, and is a certified public accountant.”

14Sources: GMCR 10K 2003 - 2011

8/3/2019 Gaap-uccino 1.5 - Part I of III - Final

http://slidepdf.com/reader/full/gaap-uccino-15-part-i-of-iii-final 15/39

The CFO Should Resign

• In addition to falsely claiming to be a Certified Public Accountant, Rathke in the10Ks certifies pursuant to SECTION 302 OF THE SARBANES-OXLEY ACT OF 2002:

“I, Frances G. Rathke, Chief Financial Officer, certify that:

1. I have reviewed this annual report on Form 10-K of Green MountainCoffee Roasters, Inc.;

2. Based on my knowledge, this report does not contain any untruestatement of a material fact or omit to state a material fact necessary to

make the statements made, in light of the circumstances under whichsuch statements were made, not misleading with respect to the periodcovered by this report “

Did Rathke “review” ANY of the 10Ks? Based on her knowledge, it’s hard tobelieve she was not fully aware that these were untrue statements.

If Rathke has been inflating her credentials for the last 9 years, is it a stretch tosay that GMCR is overstating its revenues and earnings as well?

15Sources: GMCR 10Ks

8/3/2019 Gaap-uccino 1.5 - Part I of III - Final

http://slidepdf.com/reader/full/gaap-uccino-15-part-i-of-iii-final 16/39

The CFO Should Resign

• GMCR’s website also falsely claimed Rathke is a CPA, as recently as

Friday, December 2nd, 2011 (as shown below):

16Sources: GMCR website as of 12/2/2011 4 pm

EST

8/3/2019 Gaap-uccino 1.5 - Part I of III - Final

http://slidepdf.com/reader/full/gaap-uccino-15-part-i-of-iii-final 17/39

The CFO Should Resign

• On the evening of Friday, December 2nd, 2011, Sam Antar

tweeted (time-stamped in the image):

17Sources: http://www.twitter.com/samantar

8/3/2019 Gaap-uccino 1.5 - Part I of III - Final

http://slidepdf.com/reader/full/gaap-uccino-15-part-i-of-iii-final 18/39

The CFO Should Resign

• Sam Antar continued:

18Sources: http://www.twitter.com/samantar

8/3/2019 Gaap-uccino 1.5 - Part I of III - Final

http://slidepdf.com/reader/full/gaap-uccino-15-part-i-of-iii-final 19/39

The CFO Should Resign•

A simple license check confirms Rathke is not a CPA… it expired in 1993• As if to remove all doubt, GMCR’s website modified Rathke’s bio within 2-3

hours of Sam Antar’s late, Friday night tweets.

19Sources: GMCR website,

http://license.reg.state.ma.us

8/3/2019 Gaap-uccino 1.5 - Part I of III - Final

http://slidepdf.com/reader/full/gaap-uccino-15-part-i-of-iii-final 20/39

The CFO Should Resign

• The Vermont Statutes Online, Title 26: Professions and Occupations,Chapter 1: Accountants, under § 14. Prohibitions (b) states: “No individual person may use the title "certified public accountant," "CPA,"

"registered public accountant," "RPA," or "auditor" or any other title tending toindicate that he is a public accountant, unless he is licensed as a publicaccountant under this chapter or is an individual with practice privileges set forth under section 74c of this title.”

Section 74c ‘substantial equivalency’ doesn’t seem to excuse Rathke.• CFO Fran Rathke has been using the title “certified public accountant” and

“CPA” for at least the last 8-9 years. Were it not for Sam Antar, GMCR and Rathke would’ve continued this charade.

What’s equally, if not more disturbing, is that GMCR has attempted to cover-up this lie, in hopes that no one knows or cares.

Unfortunately, as the next two pages show, Rathke is not the first C-Levelexecutive to lie. Nearly all CEOs who lied in the past resigned; Rathke shouldas well, or at the very least, be forced to forfeit compensation.

20Sources: The Vermont Statutes Online -

http://www.leg.state.vt.us/statutes/fullchapter.cfm?Title=26&Chapter=001

8/3/2019 Gaap-uccino 1.5 - Part I of III - Final

http://slidepdf.com/reader/full/gaap-uccino-15-part-i-of-iii-final 21/39

The CFO Should Resign

• Ronald Zarrella, Bausch & Lomb CEO Zarrella falsely claimed an MBA from New York University's Stern

School of Business. He attended the program from 1972-76, but neverearned his MBA. His claim was never checked by his prior employers.

He was forced to forfeit $1.1 million from a bonus that could'vepotentially reached $1.65 million. Zarrella remained employed with

Bausch & Lomb, who said he brought too much value to the companyand its shareholders to fire him completely.

• Kenneth Lonchar, chief financial officer of Veritas software

Lonchar fabricated his education, saying he earned an accountingdegree from Arizona State University and was a Stanford MBAgraduate -- in reality, all he had was an undergraduate degree fromIdaho State University.

Lonchar resigned and Veritas stock investors responded -- thecompany's stock price fell about 16 percent.

21Sources: "Infamous Resume Lies" by Rachel Zupek - http://msn.careerbuilder.com/Article/MSN-

1154-Cover-Letters-Resumes-Infamous-R%C3%A9sum%C3%A9-Lies/

8/3/2019 Gaap-uccino 1.5 - Part I of III - Final

http://slidepdf.com/reader/full/gaap-uccino-15-part-i-of-iii-final 22/39

The CFO Should Resign

• Jeff Papows, chief executive officer of Lotus Corporation In 1999, The Wall Street Journal discovered Papows exaggerated his

military record (he was a lieutenant not a captain), feigned hiseducation (he doesn't have a Ph.D. from Pepperdine University) andclaimed he was an orphan (his parents are alive and well).

Papows resigned after his exaggerations were exposed at the same

time as a sexual discrimination allegation from a former Lotusemployee against him.

• Dave Edmondson, chief executive of RadioShack

Edmondson falsified his résumé by claiming to have a degree inpsychology from Pacific Coast Baptist College in California (though theschool doesn't offer a psychology program), along with a degree intheology from the same unaccredited college.

Like the others, Edmondson admitted his false claims and resigned.

22Sources: "Infamous Resume Lies" by Rachel Zupek - http://msn.careerbuilder.com/Article/MSN-

1154-Cover-Letters-Resumes-Infamous-R%C3%A9sum%C3%A9-Lies/

8/3/2019 Gaap-uccino 1.5 - Part I of III - Final

http://slidepdf.com/reader/full/gaap-uccino-15-part-i-of-iii-final 23/39

The CFO Should Resign

• GMCR ‘Code of Ethics’ The Code of Ethics in brief askseach employee to: “Maintain accurate records and report any unethical

behavior

“Comply with all laws, rules, and regulatory requirements”

“Avoid conflicts of interest and refrain from any appearance of impropriety”

• CFO Fran Rathke and the Company has chronicallyviolated the above: Maintained false records of CPA credential

Most likely did not comply with laws and rules related toproper use of CPA designation

Increased the appearance of impropriety by trying tosweep this false claim under the rug

23Sources: GMCR website

8/3/2019 Gaap-uccino 1.5 - Part I of III - Final

http://slidepdf.com/reader/full/gaap-uccino-15-part-i-of-iii-final 24/39

Threats to the Razor / Razor

Blade Myth

24

8/3/2019 Gaap-uccino 1.5 - Part I of III - Final

http://slidepdf.com/reader/full/gaap-uccino-15-part-i-of-iii-final 25/39

Threats to the Razor/Blade Myth

• The Rising Popularity of Reusable K-Cups RaisesDoubts about the Razor/Razor blade Model: GMCR claims “Sell the brewer at or near cost & Sell the K-

cup at a high margin, just like a ‘razor, razor blade’ model.”

Reusable k-cups, such as Ekobrew & Solofill, reduces the

need for k-cups. Their popularity may keep the Keurigplatform relevant, but render the business unprofitable.

The problem for GMCR is that Ekobrew & Solofill offerconsumers a compelling alternative to k-cups, as they canenjoy fresher, higher quality, BPA-free coffee, for a fractionof the cost of a k-cup.

Consumers will (rightfully) wonder: why pay high prices for(at best) mediocre coffee, when they can pay low pricesfor premium coffee by using Ekobrew or Solofill?

25Sources: Various GMCR presentations and LST estimates

8/3/2019 Gaap-uccino 1.5 - Part I of III - Final

http://slidepdf.com/reader/full/gaap-uccino-15-part-i-of-iii-final 26/39

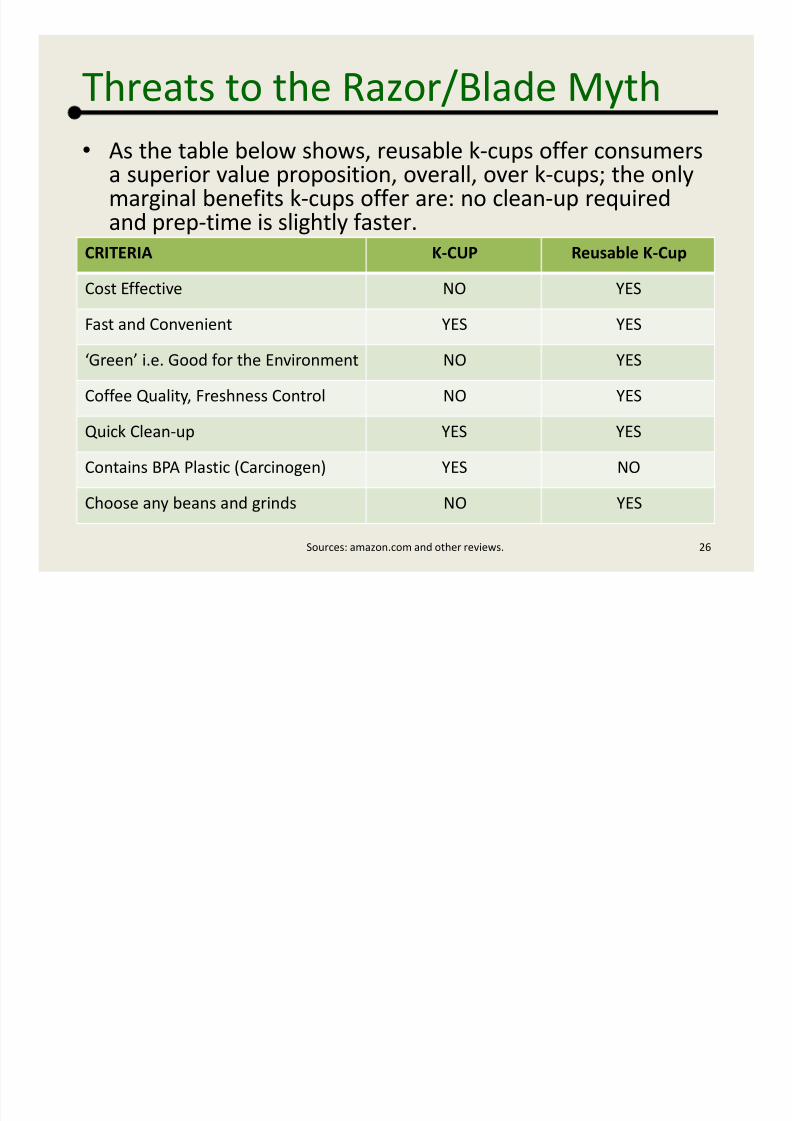

Threats to the Razor/Blade Myth

• As the table below shows, reusable k-cups offer consumersa superior value proposition, overall, over k-cups; the onlymarginal benefits k-cups offer are: no clean-up requiredand prep-time is slightly faster.

• A

• A• A

• A

• A

• A

• A

• A

• :

CRITERIA K-CUP Reusable K-Cup

Cost Effective NO YES

Fast and Convenient YES YES

‘Green’ i.e. Good for the Environment NO YES

Coffee Quality, Freshness Control NO YES

Quick Clean-up YES YES

Contains BPA Plastic (Carcinogen) YES NO

Choose any beans and grinds NO YES

26Sources: amazon.com and other reviews.

8/3/2019 Gaap-uccino 1.5 - Part I of III - Final

http://slidepdf.com/reader/full/gaap-uccino-15-part-i-of-iii-final 27/39

Threats to the Razor/Blade Myth

• GMCR has its own reusable k-cup…and the marketplace

speaketh

Reviews for the Keurig-branded product are noticeably weaker

compared against Ekobrew or Solofill

“ A must-have, but very poorly made…These things last us about 2-3

months max. They are so poorly made that they seem designed to

break after a certain time period. I have gone through three so far” a

review written on April 21, 2007. 302 of 324 customers found this

review helpful. It is considered ‘the most helpful critical review ’AMAZON.COM REVIEWs as 1/31/2012

Ekobrew Solofill

Keurig

My K-cup5 574 411 344

4 109 163 169

3 55 88 116

2 75 60 107

1 101 113 233

TOTAL 914 835 969

Average Review 4.07 3.84 3.29

27

Sources: Amazon.com

8/3/2019 Gaap-uccino 1.5 - Part I of III - Final

http://slidepdf.com/reader/full/gaap-uccino-15-part-i-of-iii-final 28/39

Threats to the Razor/Blade Myth

• Ekobrew is the newest product & appears the most promising

Ekobrew launched ~2 quarters ago, yet it is sold at Costco, and already

ranked #3 best seller in ‘Grocery & Gourmet Foods’ at Amazon.com.

Nearly all anecdotal accounts suggest Ekobrew has accomplished what

the others have failed: deliver a strong cup of coffee. All indicators

suggest they are selling like hot cakes.

Compatible with nearly all 26 Keurig, Cuisinart, Breville, and Mr. Coffee

brewers (B30 Mini, B130, B150, B155, B3000 currently incompatible).

28Sources: Costco, Amazon, & industry insiders

8/3/2019 Gaap-uccino 1.5 - Part I of III - Final

http://slidepdf.com/reader/full/gaap-uccino-15-part-i-of-iii-final 29/39

Threats to the Razor/Blade Myth

• The Reusable K-cups Can Easily Save ConsumersHundreds of Millions of $ a year:

Buying an Ekobrew or Solofill and a 1-3 pound bag of premium drip coffee already leaves you with a positive ROIvs. buying equivalent # of servings of k-cups

While this is great news for consumers, who get more forless, this is bad news for GMCR

I estimate one reusable k-cup user saves between $137 -$343 a year, and on average $250, depending on how

often the Ekobrew/Solofill is used. If there are 1,000,000-2,000,000 reusable k-cup users,

that’s around $150-$600 million in savings for consumers,and $150-$600 million in lost k-cup revenue for GMCR

29Sources: LST estimates

8/3/2019 Gaap-uccino 1.5 - Part I of III - Final

http://slidepdf.com/reader/full/gaap-uccino-15-part-i-of-iii-final 30/39

Threats to the Razor/Blade Myth

• The table below summarizes how much money reusable k-cup

filter users can save collectively, depending on: (1) how many

users there are and (2) How frequently they use them

• The below analysis assumes a k-cup costs $0.66 and that a

household consumes 1,040 coffee servings per year

Cost Savings from Reusable Filter Adoption (in thousands of $)

Reusable Filters Users (in thousands)

250 500 750 1,000 1,250 1,500 1,750 2,000 2,250 2,500

20% 34,320$ 68,640$ 102,960$ 137,280$ 171,600$ 205,920$ 240,240$ 274,560$ 308,880$ 343,200$

25% 42,900$ 85,800$ 128,700$ 171,600$ 214,500$ 257,400$ 300,300$ 343,200$ 386,100$ 429,000$

% of coffee 30% 51,480$ 102,960$ 154,440$ 205,920$ 257,400$ 308,880$ 360,360$ 411,840$ 463,320$ 514,800$served using 35% 60,060$ 120,120$ 180,180$ 240,240$ 300,300$ 360,360$ 420,420$ 480,480$ 540,540$ 600,600$

reuseable filters 40% 68,640$ 137,280$ 205,920$ 274,560$ 343,200$ 411,840$ 480,480$ 549,120$ 617,760$ 686,400$

45% 77,220$ 154,440$ 231,660$ 308,880$ 386,100$ 463,320$ 540,540$ 617,760$ 694,980$ 772,200$

50% 85,800$ 171,600$ 257,400$ 343,200$ 429,000$ 514,800$ 600,600$ 686,400$ 772,200$ 858,000$

30Sources: LST estimates

8/3/2019 Gaap-uccino 1.5 - Part I of III - Final

http://slidepdf.com/reader/full/gaap-uccino-15-part-i-of-iii-final 31/39

Threats to the Razor/Blade Myth

• Popularity of the reusable k-cup filters may directly save

consumers hundreds of millions of $ and cost GMCR the same

amount annually. That’s at least 10%-20% of 2011 revenue.

• Reusable k-cup popularity may lead consumers to question

the keurig brewer’s value proposition. Their popularitypressures GMCR profitability in the short term, viability in the

longer term.

• What were to happen if a competing single-serve coffee

brewer that directly uses coffee grinds instead of k-cups, were

to gain traction among customers? It seems that themarketplace beckons for a solution that delivers higher quality

coffee for a lower price.

31Sources: LST estimates

8/3/2019 Gaap-uccino 1.5 - Part I of III - Final

http://slidepdf.com/reader/full/gaap-uccino-15-part-i-of-iii-final 32/39

Parallels to Sino-Forest

32

8/3/2019 Gaap-uccino 1.5 - Part I of III - Final

http://slidepdf.com/reader/full/gaap-uccino-15-part-i-of-iii-final 33/39

Parallels to Sino-Forest

• Both GMCR and Sino-Forest have made claims denying wrong-doing: “I would like to say that there are no inaccuracies in our corporate reports,

filings or audited financial statements.” Allen Chan, Former CEO, Chairman,and Founder of Sino-Forest June 14, 2011 Earnings Call.

“We can categorically say Sino-Forest is not the ‘near total fraud’ and ‘Ponzischeme’ as alleged by Muddy Waters. I am pleased that the independentcommittee has been able to refute the substance of the allegations made in

the Muddy Waters report," said Judson Martin, vice-chair & CEO, November15, 2011.

“Embattled Sino-Forest Corp. is warning that its historic financial statementsand audit reports should not be relied upon.” – January 12, 2012, The Globeand Mail.

“We are confident there is no misconduct, there is no wrongdoing.” LarryBlanford, CEO of GMCR Q4 Earnings

"The audit committee, with the assistance of counsel and a forensicaccounting firm, completed its investigation of accounting practices at thecompany in December 2010,“ Suzanne Dulong GMCR spokeswoman toldReuters on December 20, 2011…even as there are new allegations of misconduct in 2011, NOT 2010.

33Sources: Sino-Forest earnings, press releases, The Global & Mail,

GMCR earnings, & reuters

8/3/2019 Gaap-uccino 1.5 - Part I of III - Final

http://slidepdf.com/reader/full/gaap-uccino-15-part-i-of-iii-final 34/39

Parallels to Sino-Forest

• M Block & Sons

• Rapid, smooth growth

• No Free cash flow

• Sweeping denials• aa fulfillment partner,

administrator

• ArtificialIntermediaries

• Rapid, smooth growth

•

No Free cash Flow• Sweeping denials

• Last paragraph of mitch the snitch

CATEGORY GMCR Sino-Forest

Shady ‘Intermediaries’ YES YES

Smooth revenue + earnings growth YES YES

Free Cash Flow No No

Glaring FCF vs. Earnings Discrepancy YES YES

Dependence on External Capital YES YES

Questionable Capex Spending YES YES

Prominent Short Seller Exposed Fraud YES YES

Numerous ‘minor’ errors in filings YES YES

Growth via Aggressive Acquisitions YES YES

34Sources: LST estimates, Muddy Waters Research, Greenlight Capital, Sam Antar, The Grumpy Old Accountants Blog,

Sino-Forest filings, GMCR filings

8/3/2019 Gaap-uccino 1.5 - Part I of III - Final

http://slidepdf.com/reader/full/gaap-uccino-15-part-i-of-iii-final 35/39

Parallels to Sino-Forest (cont’d)

• M Block & Sons

• Rapid, smooth growth

• No Free cash flow

• Sweeping denials• aa fulfillment partner,

administrator

• ArtificialIntermediaries

• Rapid, smooth growth

•

No Free cash Flow• Sweeping denials

• Last paragraph of mitch the snitch

CATEGORY GMCR Sino-Forest

Revenue + Earnings Overstatements YES YES

Ties between execs & auditor YES YES

Questionable Audit Committee YES YES

Deep Ties with Chairman/Founder YES YES

Sweeping Denial of Fraud Allegations YES YES

Conflicted Wall Street Enablers YES YES

Profitability as Reported is Doubtful YES YES

Voluntary ‘Independent’ Investigation YES YES

Stock prices appreciated 10x-20x YES YES

35Sources: LST estimates, Muddy Waters Research, Greenlight Capital, Sam Antar, The Grumpy Old Accountants Blog,

Sino-Forest filings, GMCR filings

8/3/2019 Gaap-uccino 1.5 - Part I of III - Final

http://slidepdf.com/reader/full/gaap-uccino-15-part-i-of-iii-final 36/39

Price Target

36

8/3/2019 Gaap-uccino 1.5 - Part I of III - Final

http://slidepdf.com/reader/full/gaap-uccino-15-part-i-of-iii-final 37/39

Price Target

• GMCR’s CFO Cannot Be Trusted, its numbers cannot be trusted GMCR CFO has lied about her credentials before, during, and after serious

allegations of financial/accounting shenanigans were made and leftunresolved; the CFO, who acts as the chief steward of financial reporting,cannot be trusted.

If the CFO cannot be trusted, especially given the nature of allegations,GMCR’s numbers cannot be trusted.

If GMCR’s numbers – revenue, earnings, etc. – cannot be trusted, valuationmetrics derived off them, such as PE, PEG, etc. ratios, are meaningless.

• Working off Statement of Cash Flows, assuming cash balances are valid Let’s assume that GMCR’s financial shenanigans is limited to overstating

revenue, understating expenses, and/or capitalizing expenses. That is, let’sassume there is no cash balance related fraud. I speculate that a decent proxy for true earnings, looking past the shenanigans, is going

to be cash from operating activities less depreciation (where depreciation is a proxy formaintenance/recurring capex)

2009’s CFFO less depreciation is roughly $15 million. In 2010 and 2011 this calculationleads to negative numbers. For the sake of being generous, I will ignore this andspeculate that true earnings in 2011 was roughly 4x that of 2009 (revenue increased3.4x, so I’m granting some operating leverage). I arrive at $60 million as an estimate fortrue earnings for fiscal year 2011.

37Sources: GMCR 10Ks & 10Qs, and LST

estimates

8/3/2019 Gaap-uccino 1.5 - Part I of III - Final

http://slidepdf.com/reader/full/gaap-uccino-15-part-i-of-iii-final 38/39

8/3/2019 Gaap-uccino 1.5 - Part I of III - Final

http://slidepdf.com/reader/full/gaap-uccino-15-part-i-of-iii-final 39/39

To Be Continued in Part II

39