FUNDING HIGHER EDUCATION Rohidin, Taufiq Damarjati David Greenaway and Michelle Haynes.

20

FUNDING HIGHER EDUCATION Rohidin, Taufiq Damarjati David Greenaway and Michelle Haynes

-

Upload

justin-jefferson -

Category

Documents

-

view

216 -

download

0

Transcript of FUNDING HIGHER EDUCATION Rohidin, Taufiq Damarjati David Greenaway and Michelle Haynes.

FUNDING HIGHER EDUCATION

Rohidin, Taufiq Damarjati

David Greenaway and Michelle Haynes

INTRODUCTION

Over the last 20 years of the 20th century there was a remarkable increase in participation in higher education in a number of OECD and non-OECD countries

In the case of the former, this was partly demand-driven, with key factors being increased female participation and increasing private rates of return to a first degree.

In some countries, it was also supply-driven, with policy initiatives to increase the number of universities and increase publicly funded places to support development of the ‘knowledge-based economy’.

INTRODUCTION (2)

One of the key debates triggered by increased participation is how to pay for it.

Governments have become less capable of financing higher education expansion owing to increased competition for public funds. This has triggered two questions: should the beneficiaries of higher education make

a larger contribution to the costs of provision and, if the answer to this question is ‘yes’, how

and when should they make that contribution?

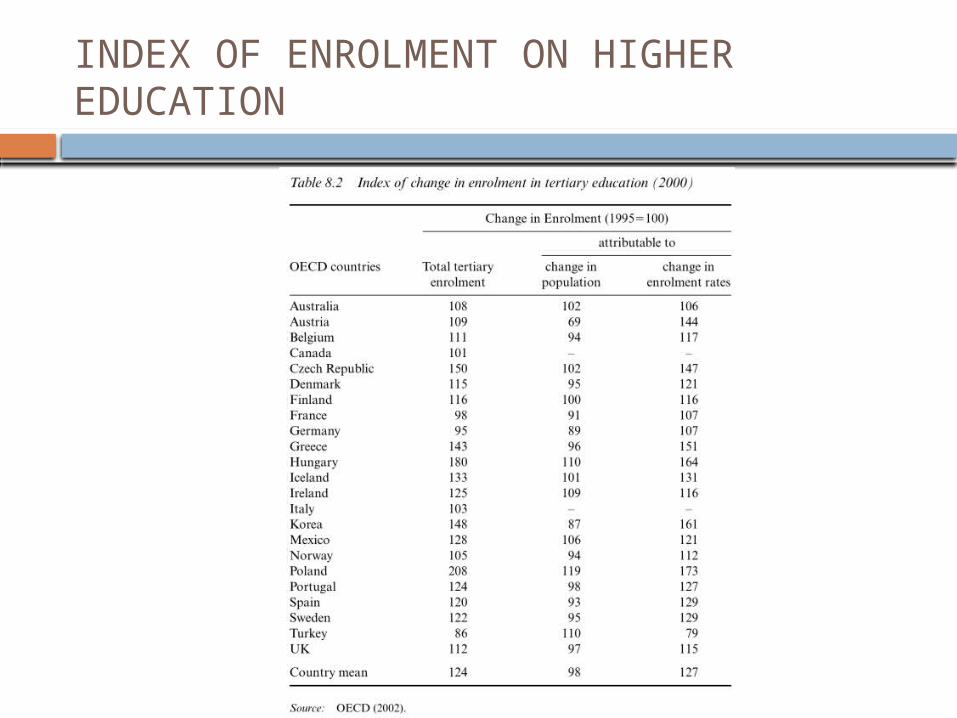

INDEX OF ENROLMENT ON HIGHER EDUCATION

PARTICIPATION ON HIGHER EDUCATION

Type B = Further Education (Setara Politeknik)

Type A = Higher Education (Setara Universitas)

PARTICIPATION BY GENDER

PARTICIPATION BY ENROLMENT MODE

PARTICIPATION BY AGE

COMPLETION RATE

PUBLIC AND PRIVATE FUNDING

EXPENDITURE PER STUDENT

PUBLIC EXPENDITURE ON EDUCATION

WHO SHOULD PAY FOR HIGHER EDUCATION

Private sector?

WHO SHOULD PAY FOR HIGHER EDUCATION (2)

Socio Cultural sector?

ALTERNATIVE FUNDING OPTION Increased taxpayer contributions via

enhanced grant allocations Introduction of a graduate tax Education vouchers Deregulation of fees Income-contingent loans Fees, loans and widening participation

RECENT DEVELOPMENT

Australia HECS (Higher Education Contribution Schema)

a charge of $A1800 (in 1989 terms) pro-rated by course load, butwith no variation by discipline;

on enrolment students could choose to incur the debt, to be repaid through the tax system depending on personal income; or

students could avoid the debt by paying up-front, which was associated with a discount of 15 per cent (later increased to 25 percent);

those students choosing to pay later faced no repayment obligation unless their personal taxable income exceeded the average income of Australians working for pay (about $A30 000 per annum, in 1989 terms);

at the first income threshold of repayment a former student’s obligation was 2 per cent of income, with repayments increasing in percentage terms above the threshold; and

HECS could be paid up-front with a discount,but there was no additional interest rate, although the debt and the repayment thresholds were (and remain) indexed to the CPI.

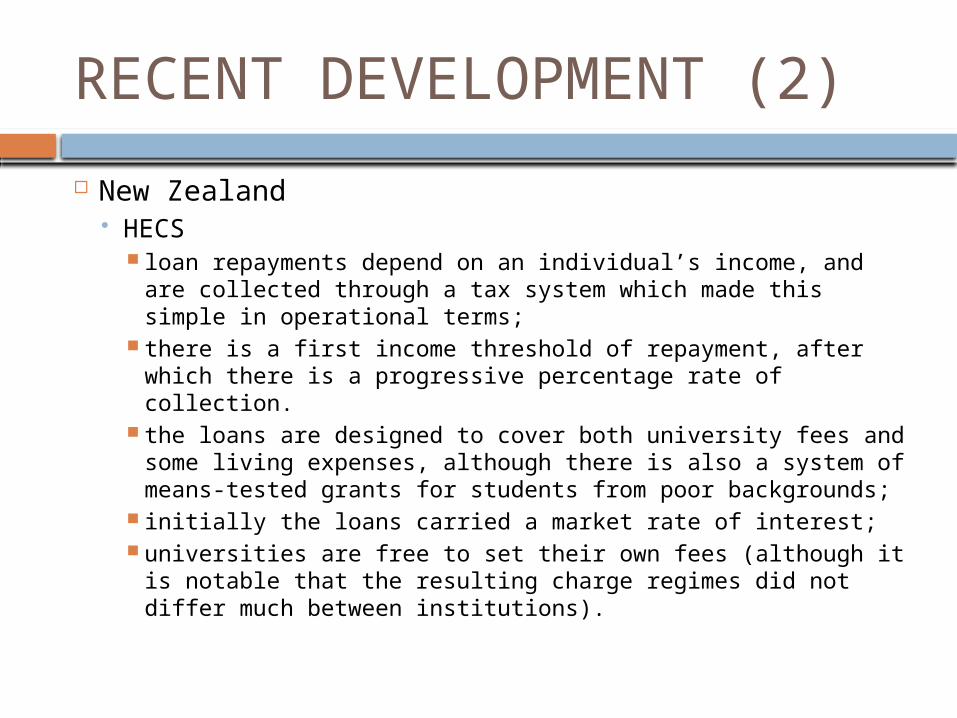

RECENT DEVELOPMENT (2)

New Zealand HECS

loan repayments depend on an individual’s income, and are collected through a tax system which made this simple in operational terms;

there is a first income threshold of repayment, after which there is a progressive percentage rate of collection.

the loans are designed to cover both university fees and some living expenses, although there is also a system of means-tested grants for students from poor backgrounds;

initially the loans carried a market rate of interest; universities are free to set their own fees (although it is

notable that the resulting charge regimes did not differ much between institutions).

RECENT DEVELOPMENT (3)

United Kingdom HECS

a uniform charge of about 25 per cent of average course costs;

the charge to take the form of a debt, with loan recovery to be contingent on income and collected through the tax system;

the debt to be adjusted over time, but with less than the market rate of interest charged on loans; and

revenue from the scheme to flow to the Internal Revenue.

CONCLUSION

the evidence on private and social rates of return provides a strong case or beneficiaries making a greater contribution than at present in many countries.

greater reliance on deferred fees repaid through an income-contingent loan system was potentially the most effective and efficient mechanism available

option of funding via deferred payments is likely to become more common.

TERIMA KASIH