FUMA- Doug Humberstone (LMA), Paul Miller (Berkley)

29

Joint Rig Committee SO, WHAT IS THIS “FUMA” THING THAT YOU ARE HEARING ABOUT ??? Paul Millen Underwriter , Berkley Offshore Underwriting Managers Doug Humberstone Underwriting and Claims Manager, Lloyd’s Market Association on behalf of MARIN 32 nd JIP Week 26 th March 2014

description

Join Rig Comittee

Transcript of FUMA- Doug Humberstone (LMA), Paul Miller (Berkley)

Joint Rig Committee

SO, WHAT IS THIS “FUMA” THING THAT YOU

ARE HEARING ABOUT ???

Paul Millen

Underwriter , Berkley Offshore Underwriting Managers

Doug Humberstone

Underwriting and Claims Manager, Lloyd’s Market Association

on behalf of

MARIN 32nd JIP Week

26th March 2014

JOINT RIG COMMITTEE - What is it?

An elected body of Marine Energy 14

underwriters drawn from:

• the Lloyd’s Market Association

• the International Underwriting

Association.

Joint Rig Committee – Terms of Reference

A forum for the London Marine Energy Market which:

• Discusses common issues or concerns.

• Promotes the best principles and practice of Marine Energy Insurance

• Initiates projects or sub-groups where appropriate to address specific issues.

• Supports the LMA’s provision of advice, information and technical services to the Marine Energy Insurance Community.

• Communicates with Marine Energy Insurers on issues including the its ongoing work and that of its sub-committees and working parties.

A CORE PROPOSITION OF UPSTREAM ENERGY INSURERS

Marine Energy Insurers seek to understand , support and,

where possible, add value to their Assured’s existing

Risk Management and Risk Reduction processes.

HOW DO WE DO THIS?

• Through third-party application of defined Survey and Assessment processes

• For Example • Construction Marine Warranty Survey

• Construction Yard Audits

• Drilling Well Plan Review

• Drilling Rigs Move Surveys

• Vessels Towage Surveys

• Constructive and informative processes of mutual benefit

WHY WERE THESE PROCESSES CREATED?

• A wish to understand ever-changing technology / risk

profiles

• Enable Insurers to deliver better products

• A response to recent events

HOW WERE THEY CREATED?

Consultation between:

• The Joint Rig Committee

• Industry experts (third-party engineers / surveyors)

• Industry bodies / associations

To ensure they are:

• Reasonable

• Relevant

• Practical

• Value Adding

SO WHAT ABOUT MOORING INTEGRITY?

• Insurers had relied on Classification Societies and

Operators to ensure system integrity.

• The JRC mandated the Engineering Sub-committee to

investigate the need for & development of a formal

process for the assessment of Mooring Systems

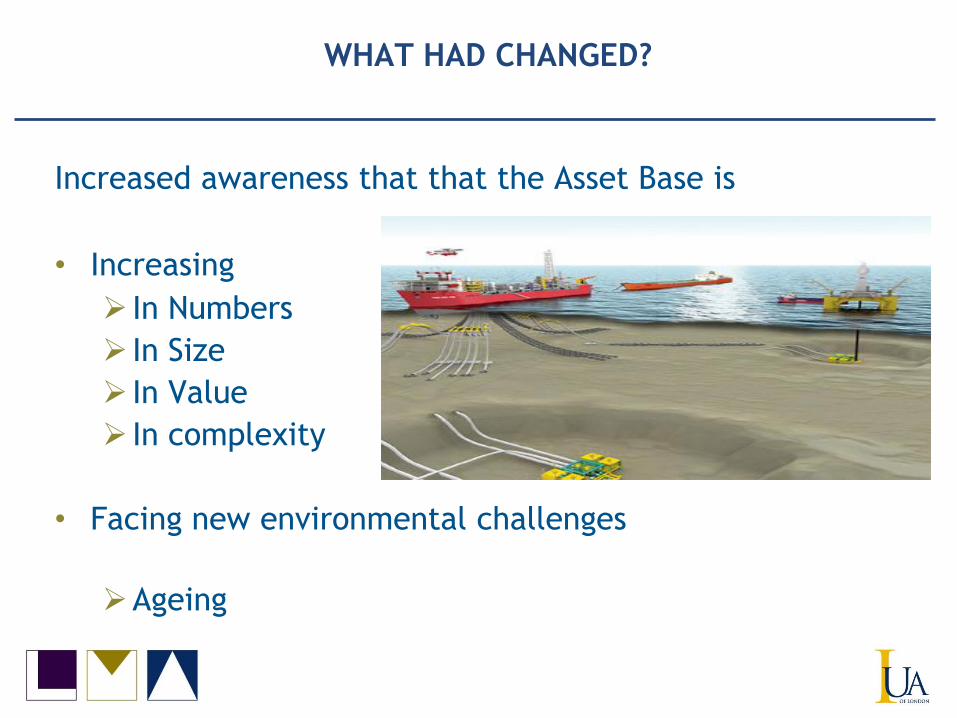

WHAT HAD CHANGED?

Increased awareness that that the Asset Base is

• Increasing

In Numbers

In Size

In Value

In complexity

• Facing new environmental challenges

Ageing

WHAT HAD CHANGED?

Awareness of :

Increasing frequency of

• General Mooring System failures

• Premature failures

Increasing quantum of Insured Losses

WHAT HAD CHANGED?

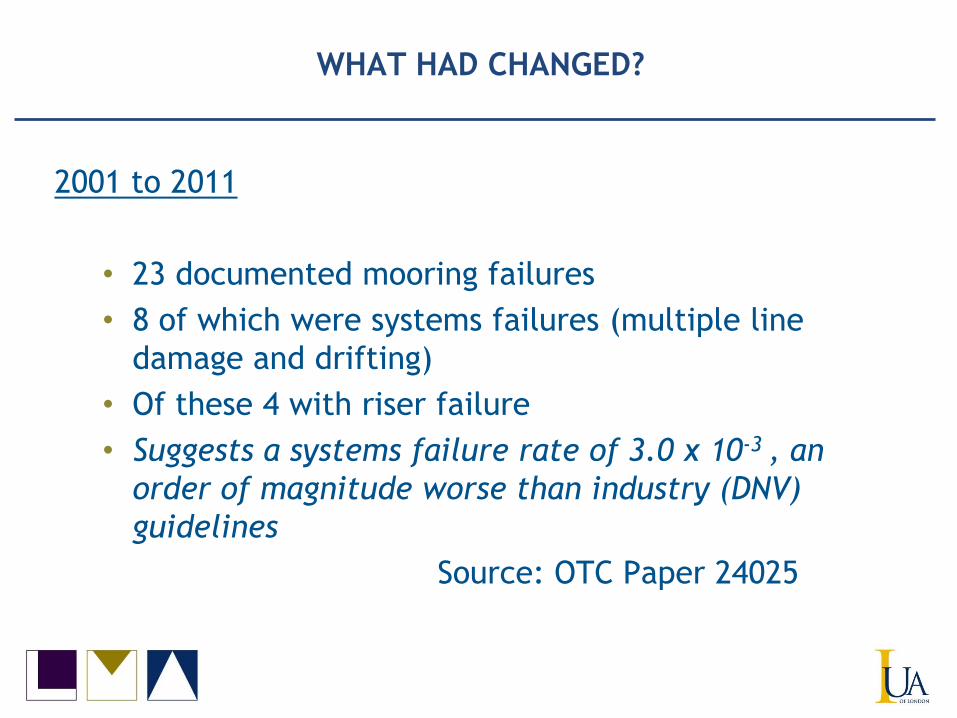

2001 to 2011

• 23 documented mooring failures

• 8 of which were systems failures (multiple line

damage and drifting)

• Of these 4 with riser failure

• Suggests a systems failure rate of 3.0 x 10-3 , an

order of magnitude worse than industry (DNV)

guidelines

Source: OTC Paper 24025

WHAT HAD CHANGED?

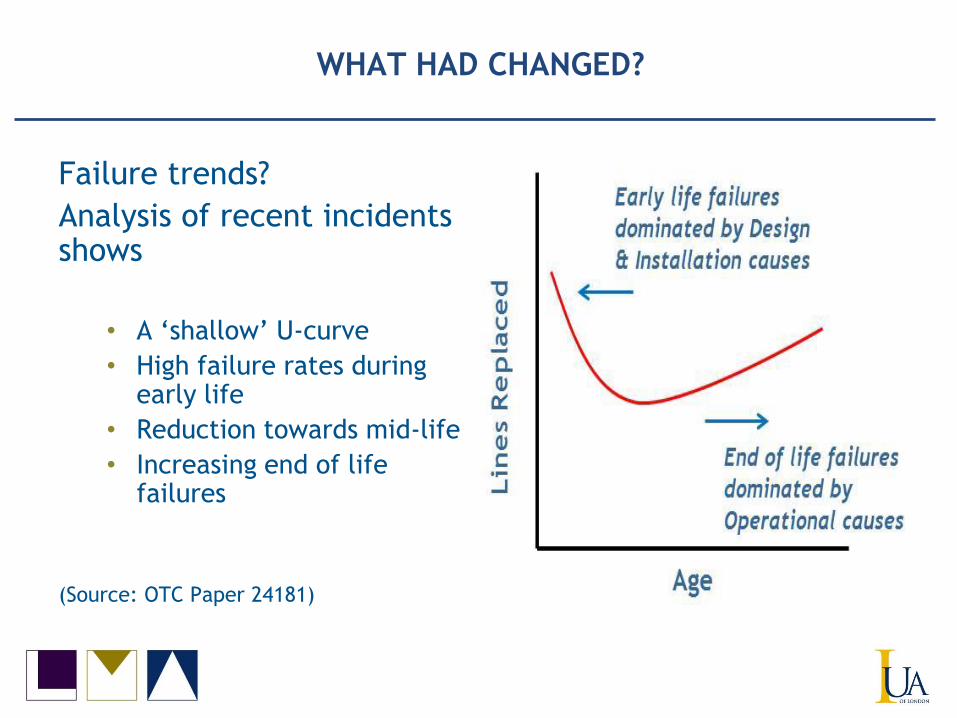

Failure trends?

Analysis of recent incidents shows

• A ‘shallow’ U-curve

• High failure rates during early life

• Reduction towards mid-life

• Increasing end of life failures

(Source: OTC Paper 24181)

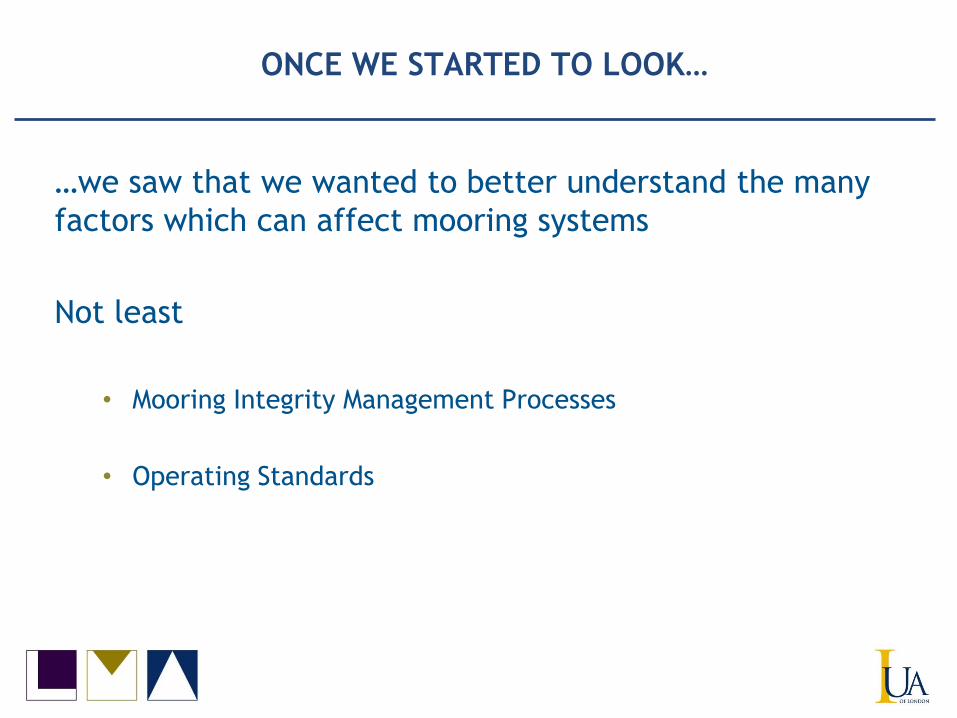

ONCE WE STARTED TO LOOK…

…we saw that we wanted to better understand the many

factors which can affect mooring systems

Not least

• Mooring Integrity Management Processes

• Operating Standards

AND…

Lifetime Extension Processes

Classification Societies

Uninspected ‘Desk Top’ class extensions

Inconsistency of Rules

Variable application of own rules

Variable Capability

UNDERWRITERS CONCLUSIONS

• There were gaps in our understanding

• Operating and Maintenance standards are variable

• Class is variable

• Be better informed…and promote risk reduction for

Insurers and Assureds alike.

• A formalised Assessment Process was the best way

forward

ESTABLISHING THE CORE VALUES OF THE NEW PROCESS

IT SHOULD BE:

• Inclusive and promote dialogue with assureds)

• Discretionary or voluntary

• Flexible / risk appropriate

• Relevant / standards-based

• An underwriting tool

• Value-adding for assureds

ESTABLISHING THE CORE VALUES OF THE NEW PROCESS

It should generally enhance understanding of the

• Various types of mooring systems and the differing

associated risk

• Various international codes for mooring system

design and operation , installation and integrity

management

• Lifetime Extension process

• Condition, operational experience and integrity

management of specific systems

• Suitability, pre-installation, of a specific system

HOW WAS IT DRAFTED?

We followed well-trodden , proven paths

A document structured consistently with other JRC survey

documents e.g. CAR MWS / Well Plan

• Guidance Notes

• Endorsement

• Code of Practice

• Workscopes

HOW WAS IT DRAFTED?

Consideration was given to known

• International Standards

• Design Codes

• Codes of Practice

• Operation Codes

• Integrity Management Systems

• Industry Best Practice

• Defined Safe Operating Limits

Drafting and Consultation

JRC

Oil & Gas UK (including Mooring Integrity

working group

3rd party Engineers

MWS

JRC Engineering Sub Committee

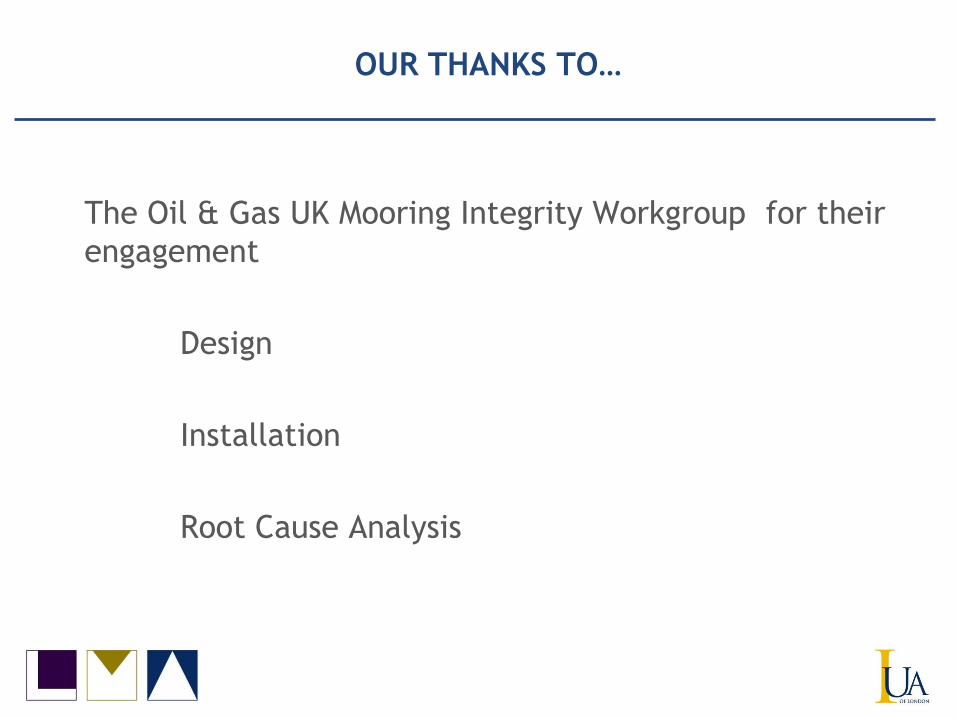

OUR THANKS TO…

The Oil & Gas UK Mooring Integrity Workgroup for their

engagement

Design

Installation

Root Cause Analysis

AND THEN…

The JRC Engineering Sub-Committee delivered

its process for

Floating Unit Mooring Assessment

“FUMA”

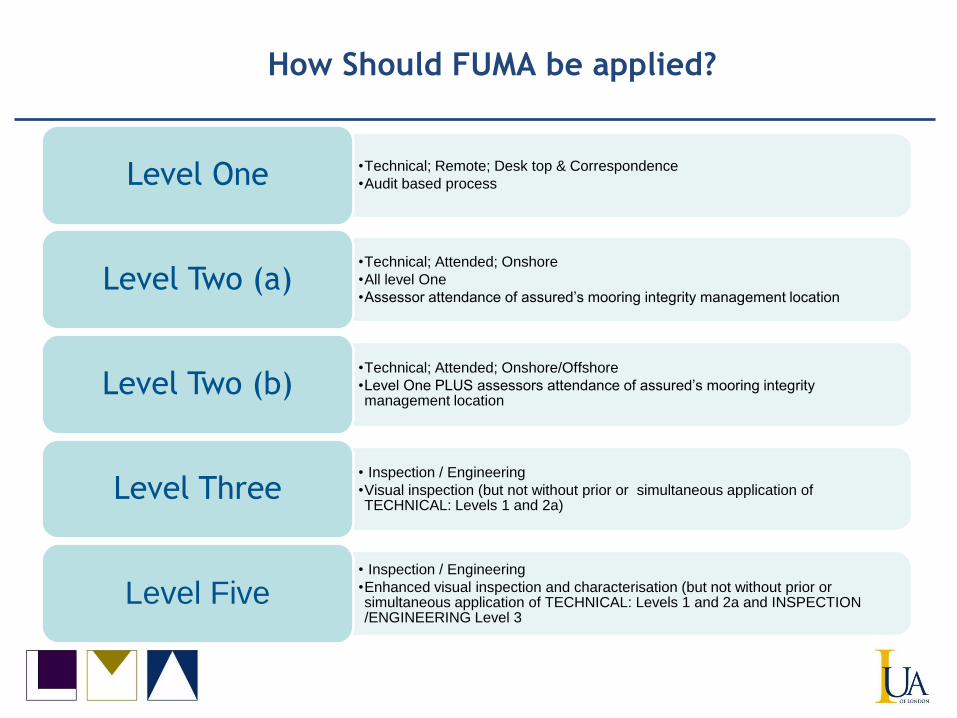

HOW SHOULD FUMA BE APPLIED?

Intended for use with Moored Floating Units OTHER THAN MODU’s

Application is Discretionary and/or Voluntary

There is an INITIAL SCREENING PROCESS (ISP) which may indicate FUMA is NOT REQUIRED

If ISP indicates need for FUMA application it is a ‘tiered’ process

‘Technical’ or ‘Physical’

‘Remote’ or ‘Attended’

How Should FUMA be applied?

•Technical; Remote; Desk top & Correspondence

•Audit based process Level One

•Technical; Attended; Onshore

•All level One

•Assessor attendance of assured’s mooring integrity management location Level Two (a)

•Technical; Attended; Onshore/Offshore

•Level One PLUS assessors attendance of assured’s mooring integrity management location

Level Two (b)

• Inspection / Engineering

•Visual inspection (but not without prior or simultaneous application of TECHNICAL: Levels 1 and 2a)

Level Three

• Inspection / Engineering

•Enhanced visual inspection and characterisation (but not without prior or simultaneous application of TECHNICAL: Levels 1 and 2a and INSPECTION /ENGINEERING Level 3

Level Five

HOW SHOULD FUMA BE APPLIED?

Mooring Assessors ; Selection and Appointment

• Any party(ies) on which Insurers and Assureds may mutually agree

• Insurers to propose (wherever possible) a panel of potential Assessors

• Assured to select its preferred Assessor from the proposed panel

Assessors may include

• An Insurer’s internal engineering capability

• A third-party e.g. a Marine Warranty Surveyor or a specialist engineer

AND THEN…

• The workscope is applied

• The Assessor delivers its findings to the Assured and

the Insurers

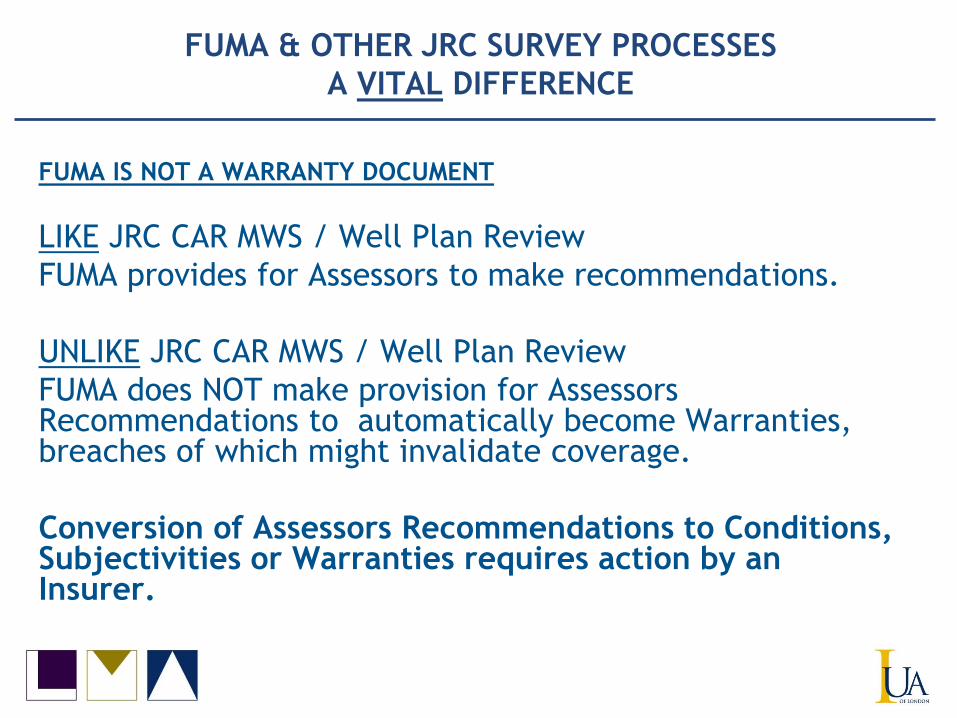

FUMA & OTHER JRC SURVEY PROCESSES

A VITAL DIFFERENCE

FUMA IS NOT A WARRANTY DOCUMENT

LIKE JRC CAR MWS / Well Plan Review

FUMA provides for Assessors to make recommendations.

UNLIKE JRC CAR MWS / Well Plan Review

FUMA does NOT make provision for Assessors Recommendations to automatically become Warranties, breaches of which might invalidate coverage.

Conversion of Assessors Recommendations to Conditions, Subjectivities or Warranties requires action by an Insurer.

And Finally…

We seek to UNDERSTAND but NOT to DICTATE

We believe our Risk Survey / Assessment

processes add value in other categories of risk

We believe the same can be true for Mooring

System Integrity Management

www.lmalloyds.com/underwriting/jrc

Thanks for your attention and