FP Standard - Spring 2015

16

FPStandard SPRING 2015 ISSUE 11 IDEAS THOUGHTS AND TRENDS IN THE FINANCIAL PLANNING PROFESSION P 1 FPSC.CA On My Mind: Why We Do What We Do P 2 Clients Trust What They See: Display Your Full Value with Winning Body Language P 6 Professionals Must Always Be Watchful for Potential Conflicts of Interest P 8 Unified Standards for the Canadian Financial Planning Profession

-

Upload

financial-planning-standards-council -

Category

Economy & Finance

-

view

61 -

download

2

Transcript of FP Standard - Spring 2015

FPStandard SPRING 2015

ISSUE 11

I D E A S T H O U G H T S A N D T R E N D S I N T H E F I N A N C I A L P L A N N I N G P R O F E S S I O N

P 1

FPSC.CA

On My Mind: Why We Do What We Do

P 2

Clients Trust What They See:Display Your Full Value

with Winning Body Language

P 6

Professionals Must Always Be Watchful for Potential

Conflicts of Interest

P 8

Unified Standards for the Canadian Financial

Planning Profession

902-375 University Avenue Toronto, Ontario M5G 2J5

Telephone: 416 593 8587 Toll-Free: 1 800 305 9886

Email: [email protected] Website: fpsc.ca

Twitter: @FPSC_Canada

Facebook: FPSC.Canada

LinkedIn: company/Financial-Planning-Standards-Council

YouTube: FPVision2020

CFP®, Certified finanCial Planner® and are certification trademarks owned outside the U.S. by Financial Planning Standards Board Ltd. (FPSB). Financial Planning Standards Council is the marks licensing authority for the CFP marks in Canada, through agreement with FPSB. All other ® are registered trademarks of FPSC, unless indicated. © 2015 Financial Planning Standards Council. All rights reserved.

A NATIONAL SURVEY CONDUCTED ON BEHALF OF FINANCIAL PLANNING STANDARDS COUNCIL (FPSC) HAS FOUND THAT MONEY IS THE LEADING SOURCE OF STRESS AMONG CANADIANS, SIGNIFICANTLY MORE THAN WORK, PERSONAL HEALTH AND RELATIONSHIPS.

ACCORDING TO THE SURVEY, FINANCIAL STRESS IS DRIVING CANADIANS TO LOSE SLEEP, RECONSIDER PAST FINANCIAL DECISIONS, ARGUE WITH PARTNERS AND LIE TO FAMILY AND FRIENDS ABOUT PERSONAL FINANCES. HIGHLIGHTS FROM THE SURVEY ON FINANCIAL STRESS ARE AVAILABLE AT FPSC.CA/VALUE-FINANCIAL-PLANNING/HOW-IS-FINANCIAL-STRESS-AFFECTING-CANADIANS.

51 45

#1

4 in 10

% % OF WOMEN LOSE SLEEP OVER FINANCIAL WORRIES, WHILE 40% OF MEN CLAIM THE SAME.

MONEY IS THE NUMBER ONE STRESS FACTOR AMONG CANADIANS OF ALL DEMOGRAPHICS AND GEOGRAPHICAL REGIONS.

The survey was conducted by Leger and included more than 1,000 Canadians (excluding Quebec) between September 26 and October 1, 2014. It has a margin of error of +/- 2.5%, 19 times out of 20.

OF CANADIANS ARE EMBARRASSED ABOUT THEIR LACK OF CONTROL OVER FINANCES.

PEOPLE IN RELATIONSHIPS WITH SHARED FINANCES ARGUE REGULARLY OVER FINANCES.

87% OF CANADIANS WISH THEY HAD MADE BETTER FINANCIAL DECISIONS EARLIER IN LIFE.

BY THE NUMBERS

MONEY IS THE LEADING SOURCE OF STRESS FOR CANADIANS

SPRING 2015 – 1

ON MY MIND

WHY WE DO WHAT WE DO

There is no question that we live in an age of information sharing and unprecedented transparency. The past decade has seen explosive growth in the number and popularity of the online communities and social networks that provide an avenue for millions of Canadians to share the many details of their lives, thoughts and opinions. An August 13, 2013 headline in the National Post noted that “More Canadians use Facebook daily than anywhere else in the world”. In fact, at that time the Post reported that “More than 19 million Canadians were logging onto Facebook at least once every month — that’s more than half the population — while 14 million check their newsfeed every single day…”.

As Canadians, we talk about what and where we eat and what’s hot on Netflix; we offer cures for what would have once been embarrassing ailments; and much more. It seems like there are no longer any topics too intimate or too private to share — except perhaps one.

Most Canadians draw the line when it comes to discussing their personal finances — in this age of über-communications, money may be considered the last vestige of taboo subjects for Canadians. Divulging details of our finances has enjoyed an unrivalled tenure on the ever-shrinking list of “taboo topics”.

We don’t tell or ask each other how much we earn or what we owe. Most of us can only guess how much money our parents have saved . As Canadians, we take the “personal” in “personal finance”

seriously. It’s one of the few things that we all care about, but very very few of us feel comfortable talking about.

It’s private.

However, we know through empirical evidence that when Canadians sit down across from a CFP® professional and bare all, they are likely to reap substantial financial and emotional benefit. The Value of Financial Planning study – commissioned by FPSC and financially supported by the Financial Planning Foundation – revealed that Canadians with comprehensive financial plans feel that their financial goals and retirement plans are more on track, their ability to save has improved, and that they are more confident they can handle the inevitable bumps in life. Further, those working with a CFP professional universally report more positive feelings regarding their personal finances and their financial futures.

But Canadians will never realize these advantages unless they are satisfied they can trust a true financial professional with information related to their most intimate and personal matters – their financial affairs.

That is why we do what we do. Canadians must know they can trust financial planners to help them achieve financial well-being, and financial planners must be worthy of that trust.

Canadians need to trust that those financial planners who have earned the CFP® designation have met internationally recognized standards of knowledge, skills

Cary List CA, CPA, CFP®

President & CEO, FPSC

Cary leads FPSC as the premier standards-setter for the financial planning profession in Canada. He has spent most of the past decade working to ensure that CFP certification is recognized as the standard for financial planning and to see financial planning recognized in law as a distinct profession.

and abilities and are accountable for and abide by a code of ethics that prescribes their duty to act with the due prudence of a professional and to put their clients’ interests before all others.

FPSC attests to the fact that those who complete CFP certification have undertaken an extensive approved education program, passed rigorous national exams, and obtained a minimum of three years’ qualifying work experience. To remain certified, CFP professionals must undertake continuous professional development and agree to adhere to FPSC’s Standards of Professional Responsibility for CFP Professionals.

It is not easy to become a Certified finanCial Planner® professional, nor should it be…why should Canadians settle for less?

Money. It’s time we talked about it. With the right professional.

SPRING 2015 – 2

BY MARK BOWDEN

As a financial planner, chances are you have to present to your current and prospective clients more than just now and again. Whether it is to deliver a plan, or to speak to one or many in order to win new business, getting your ideas heard and trusted is essential if you are to stand out from the crowd.

For you to have the most positive impact, here are my top body language tips for speaking in front of any audience any time and in a way that wins trust immediately.

PUT YOUR BODY ON DISPLAYWhen speaking at a conference, have a lavaliere or handheld mic and step away from the podium. If sitting with a client, pull your chair back from the table — in short, display more of your body to your audience. Your audience's instinctual 'reptilian' brain needs to see your body and your body language to decide what they think your intentions and feelings are towards them.

SPEAK FROM YOUR BELLYPlace your hands in what I have trademarked the TRUTHPLANE®, the horizontal plane that extends 180 degrees out of your navel area. Bringing the audience's unconscious attention to this vulnerable area of your body makes them feel that you are very confident. By assuming this physicality, you will feel confident too.

SHOW YOUR HANDSShow your palms open with nothing in your hands to let others know that you mean no harm and are speaking for their benefit. This is a universally recognised 'friendly' gesture.

HANG OUT... CHECK OUTAvoid dangling your hands by your sides when giving important messages. It gives your voice a depressing or sleepy downward intonation, and makes you look unconfident.

ATTRACT RECOGNITIONKeep your gestures symmetrical. The brain understands symmetry in the body more easily than asymmetry, and we find it more appealing.

REVEAL, NOT CONCEALAvoid having your hands at mouth level when speaking, for example when sitting at a table with your chin in your hands. We lip-read more than we think, and when the picture of the words is taken away, it becomes harder to verify the language. The audience will perceive or create negative feelings about the speaker's intentions — in the absence of the nonverbal information.

MOVE COMPLEX TO CLEARWhen giving a complex message, avoid complex movement — so no fiddling with your pen! It is hard for the brain to decode complex verbal language when it is concentrating on complex nonverbal behaviour.

CLIENTS TRUST WHAT THEY SEE

DISPLAY YOUR FULL VALUE WITH WINNING BODY LANGUAGE

STOP READING AND START LEADINGDon't try to read other people's body language consciously. Generally, most of us stand little more than a 50/50 chance of getting it right. Instead, concentrate on influencing your audience to mirror your simple and positive nonverbal behaviour, and they will be extremely likely to trust and engage with you every time you communicate.

Mark Bowden is a body language and behavior expert and the creator of TRUTHPLANE®, a communication training company and unique methodology for anyone who has to communicate with impact. Mark travels all over the world giving keynote speeches and training groups. His clients include leading businesspeople, teams, and politicians, presidents and CEOs of Fortune 500 companies and current Prime Ministers of G8 powers. His 3 books are the bestselling Winning Body Language, Winning Body Language for Sales Professionals, and Tame the Primitive Brain – 28 Ways in 28 Days to Manage the Most Impulsive Behaviors at Work. Mark is particularly honored to now be in the TED community, having spoken on the main stage at TEDx Toronto. He is a regular contributor to TV shows, and you can see him currently on CTV’s daily talk show The Social as the resident body language expert. Mark is voted #1 in the World’s Top 30 Body Language Professionals for 2014 by GlobalGurus.org.

SPRING 2015 – 3

LOOK FOR THIS SYMBOL

For more information visit:fpsc.ca/approved-ce-credits

as Assurance of FPSC®-Approved CE Activities and CE Credits.

ASSESSED.

APPROVED.

ASSURED.

Academy of Financial Divorce Specialists

Advisor.ca/Rogers Publishing Ltd.

Age-Friendly Business

Agenomics

AGF Investments Inc.

Aston Hill Asset Management Inc.

Bachrach & Associates Inc.

Bridgehouse Asset Managers

Bruce Etherington & Associates

Business Career College Corp.

Business Families Foundation

Canadian Anti-Money Laundering Institute

CICEA

Canadian Securities Institute

Capital R Consulting

CDSPI Advisory Services Inc.

CE-credits.ca

CE Network Inc.

CGA Canada PD Net

CI Investments

CIBC Asset Management Inc.

Clear Path Media

CLIFE Inc.

Convention Business Travel

Dalhousie University - MBA

Damian Borges

Dynamic Funds

ERAssure - Estate Risk Protection Plan Inc.

ES Computer Training

Exam Success

Foran Financial Institute

Gobeil & Associates

Gordon B Lang and Associates Inc.

HAHN Investment Stewards & Company Inc.

Harrison Pensa LLP

iA Financial Group

IFSE Institute

ILS Learning Corporation

Independent Financial Brokers of Canada

Ingle International/ Imagine Financial Ltd.

Institute for Divorce Financial Analysts

Institute of Advanced Financial Planners

INTEGRIS Pension Management Corp.

Invesco Canada Ltd.

Ivey Business School

Jarislowsky Fraser Limited

Knowledge Bureau

Knowledge First Financial

Learning Partner

Louis Jolicoeur

Mackenzie Investments

Manulife

McCague Borlack LLP

MD Management

MedAxio Insurance Medical Services

Mindpath Financial Conferences

My Money Mindset

National Exempt Market Association

NPC Data Guard

Oliver's Learning

Pacific Business & Law Institute

Parley Consulting

FPSC CE Approval ProgramPhoenix Coaching Works Inc.

Practical Management of Canada

Private Capital Markets Association of Canada

Radius Financial Education

Responsible Investment Association

SaskWorks Venture Fund Inc.

Seminar Partners

Skillsoft Corporation

Smarten Up Institute

STEP Canada

Tabuchi Law Offices

TEN STAR Financial Services

The Canadian Institute of Financial Planners

The Heritage Institute Canada

The Money Finder

Vancouver Dementia Care Consulting

Vision Systems Corp.

Wardell

Worldsource Wealth Management

SPRING 2015 – 4

BY BOB VERES

COMPETITIVE EVOLUTION

INSIDE INFORMATION

We’re all hearing a lot of hand-wringing discussion about the robo-competition—the new online advice platforms that offer automated investment portfolios at a very low cost. In articles and hallway conversations, the so-called robo-advisors are described as a serious threat to the revenue model of the profession.

What we tend to forget is that the profession has faced down a number of mortal threats in the past, and each time has emerged stronger through positive evolution. When the personal finance magazines seemed to be giving away the advice that advisors were charging for, the profession evolved from the sales of thick financial plans to ongoing planning, and the assets under management (AUM) business model was born. When discount brokerage firms began running ads questioning why anyone would work with an expensive financial advisor when they could trade stocks on their own, advisors began recommending portfolios created according to the principles of modern portfolio theory, and offered alpha-enhancing services like disciplined rebalancing, tax-loss harvesting and a buy-and-hold ethos.

In response to the robo-competition, I expect to see a similar evolutionary shift for the better. The new competition is helping advisors recognize what most of us knew all along: that their competitive advantage is, and will always be, the personal service and customized advice they provide.

There will be two parts to the evolution. First, advisors will find new ways to maximize the time they spend face-to-face with clients. They will start to automate back office chores like rebalancing, data entry and portfolio reporting—which can be handled by computers more efficiently than by humans. With this additional free time, they’ll develop new, better service packages. The profession is already starting to embrace a more customized advice model which is sometimes called “life planning”. Instead of creating financial plans for clients, advisors will begin co-creating them over multiple meetings that allow more time to explore goals in greater depth. They’ll let clients take the wheel of the planning software and explore their financial futures.

Recently, I’ve seen advisors beginning to offer “netweaving” services, where they collect, from their clients, the names of local service providers who have provided outstanding service. Whenever a client wants someone to fix their plumbing or their computer, or remodel their kitchen, they go to their advisor for a recommendation. The advisor becomes an important information and referral hub in the community! The profession will not only survive this latest challenge; it will become better as a result of it. After all, it’s done it before.

Bob Veres is publisher of Inside Information, the leading information resource for financial advisors and planners in the U.S. market and was a guest speaker at the 2014 FPSC CFP® Professional Symposium held during Financial Planning Week in November. For a free 3-month trial of his service, go to bobveres.com/amember/signup/trial and insert coupon code FPSC2015.

SPRING 2015 – 5

BY STEPHEN ROTSTEIN, LL.B. FPSC VP, POLICY & REGULATORY AFFAIRS & GENERAL COUNSEL

INTRODUCING THE

FPSC PUBLIC POLICY AMBASSADOR PROGRAM

In the Fall of 2014, FPSC announced that it would be launching a new grassroots program for CFP professionals: the Public Policy Ambassador Program.

Inspired by the adage that “all politics is local”, the goal is to assist CFP professionals to educate their local elected representative on issues that affect the public, including the current absence of necessary safeguards for individuals seeking the services of a financial planner.

An initial call for volunteers went out in the late autumn of 2014, attracting over 80 individuals who indicated their interest in participating. In order to become a Public Policy Ambassador, CFP professionals must

take part in a training session offered via webinar. Over 40 individuals participated earlier this year in our initial training session, and a second session is scheduled to be delivered this fall.

In the few short months since the training webinar took place, CFP professionals have already begun to set up and hold meetings with their elected officials, promoting the need to restrict the title “financial planner” to only those who have met unified standards of competence, practice and ethics, with the CFP designation at the forefront of these standards.

As the Public Policy Ambassador Program continues to grow, FPSC will gather

feedback from Ambassadors and provide additional materials and resources to assist with their advocacy efforts.

If you are interested in learning more about the Public Policy Ambassador Program, or about how to participate, please email us at [email protected].

A MATTER OF TRUST:

PROTECTING CANADIANS’ FINANCIAL FUTURES

Studies have clearly demonstrated that Canadians are not getting the financial planning help they need, from qualified, professional financial planners. This is partially the result of a lack of understanding of how to identify a qualified financial planner and of what they should expect of a financial planner and/or a financial plan. Today’s unregulated financial planning environment leaves consumers vulnerable and at risk of receiving advice from individuals holding themselves out as financial planners but who have not had to meet any qualifications based on accepted, unified standards of ethics, competence and practice.

We need to ensure that consumers are appropriately served and protected by

qualified and competent financial planners. Clear, singular standards of competence, ethics and practice must be accepted and permitted to be enforced by provincial governments.

The solution proposed by the Financial Planning Coaltion is simple – codify in law the professional certification structure, governance and oversight mechanisms that already exist in practice, but that are currently voluntary for the 22,000 financial planners licensed or certified through IQPF and FPSC in Canada, and make them a requirement for all who wish to claim financial planning as their own.

Members of the Financial Planning Coalition are working to ensure that this message

is received by all levels of government, throughout Canada.

About the Financial Planning Coalition: The Financial Planning Coalition was formed in 2009 to establish a framework for a profession for those holding themselves out as financial planners. The Coalition advocates for the official recognition of financial planning as a distinct profession that will best serve the interests of Canadians. Members include the Canadian Institute of Financial Planners (CIFPs), Financial Planning Standards Council (FPSC), the Institute of Advanced Financial Planners (IAFP) and the Institut québécois de planification financière (IQPF).

Canadians must be able to trust financial planners to help them achieve financial well-being.

SPRING 2015 – 6

MARK BOWDEN

BY DAMIENNE LEBRUN-REID, LL.B.FPSC DIRECTOR, STANDARDS AND ENFORCEMENT

CONFLICTS OF INTEREST

PROFESSIONALS MUST ALWAYS BE WATCHFUL FOR POTENTIAL CONFLICTS OF INTEREST

CFP professionals must always place their client’s interests ahead of their own; the Client First Principle is the first principle of the FPSC® Code of Ethics. Despite the importance of this principle to the profession, CFP professionals, like many others, continue to struggle to identify and manage potential and realized conflicts of interest.

The Standards of Professional Responsibility require CFP professionals to be objective when providing services to clients and to maintain confidentiality of client information. Rules 8 and 9 of the FPSC® Rules of Conduct directly address disclosure of conflicts and require that likely conflicts be disclosed in writing to the client on an ongoing basis.

This article explores common sources of conflicts of interest and provides best practice tips for anticipating and managing conflicts.

Be Watchful for Potential Conflicts of Interest

You will encounter situations that involve inherent conflicts of interest, for example, where you represent spouses, members of the same family or business partners. When they first retain you, a couple’s interests and financial goals are likely aligned; however, the potential for a conflict to arise

is undeniable. It may well be that you can act for a couple as long as their financial objectives remain aligned, but you should alert your clients (and remind yourself) that there may come a time when you can no longer act for both parties.

Taking steps in the early stages of a client relationship to anticipate and plan for future conflicts is in your best interest and your clients’ best interests. Document the steps you take to identify potential and actual conflicts, and your discussions with your clients.

Taking it a Step Further – Best Practice

The public expects more from professionals. Best practice suggests that in addition to identifying and disclosing likely conflicts, CFP professionals should decline to act for a client where a conflict of interest exists or is likely to materialize and where the conflict cannot be mitigated. You should:

1. Decline to act where there is an existing conflict of interest:

a. Between you and your client; and/or

b. Among your clients in the case of a joint engagement; and

2. Advise your clients that you may not be able to continue to provide services to them if a conflict of interest materializes in the future.

It is always better to be proactive than reactive.

When considering whether you should accept an engagement or continue in an existing engagement, you should ask yourself if the duties you owe your client may be negatively impacted if you continue with the engagement.

Consider whether you, your employer or your business partners have a personal interest in your client’s affairs. Is there a risk that your professional duties to your client may be adversely affected by your own interests or by your duty to another client or to a third person? If the answer is yes, there is a conflict of interest.

Do not ignore conflicts of interest. Addressing them head-on is both professionally prudent and consistent with good client-relationship development and management practices.

SPRING 2015 – 7

REPORTS ON FPSC DISCIPLINARY ACTIONS

Where CFP professionals have been found by a Hearing Panel to have breached the standards for the profession as established by FPSC, the Hearing Panel may impose disciplinary sanctions ranging from a letter of admonishment to permanent revocation of the right to use the CFP marks. FPSC makes all Hearing Panel decisions public, in part, by publishing a report on our website.

For FPSC Level 1™ certificants in Financial Planning, disciplinary sanctions can range from a letter of admonishment to expulsion from the FPSC Level 1 Certificant program (thereby preventing them from using the FPSC Level 1 marks and from obtaining CFP certification).

The following individual has recently received admonishment:

• Cloth, M. Jason (Markham, ON)

On July 9, 2014 FPSC’s Disciplinary Hearing Panel of the Enforcement Policy Committee considered the matter of Financial Planning Standards Council and Jason M. Cloth, CFP®.

By way of unanimous decision dated August 7, 2014, the Hearing Panel found that Mr. Cloth breached Rules 101, 202 and 702 of the FPSC® Code of Ethics (the Code).

Mr. Cloth appealed the Hearing Panel’s decision. By way of Order dated October 30, 2014, the Appeal Panel allowed the Appeal in part and upheld the following findings of the Hearing Panel:

i. Mr. Cloth breached Rule 101 of the Code by failing to properly explain and illustrate to his client the cost of the product over the client’s life expectancy or for the time period the insurance was to be in force;

ii. Mr. Cloth breached Rule 202 of the Code by failing to act in the interests of his client by allowing a provision of the policy that was significant and important to the client — the Cost of Insurance — to be changed from Level to Yearly Renewable without making the necessary and adequate disclosure and without the client's proper authorization; and

iii. Mr. Cloth breached Rule 702 of the Code by failing to implement only those recommendations that were suitable for the client, by not sufficiently explaining to the client the details of the insurance product, the effects of changes made to the insurance, and by failing to confirm the client's understanding of the product purchased by periodically reviewing it with the client.

Mr. Cloth was issued a Letter of Admonishment, and his right to use the CFP certification marks has been suspended for one (1) year until November 6, 2015.

PRINCIPLES OF CFP PROFESSIONAL CODE OF ETHICS:

• Put Client Interests First

• Act With Integrity

• Be Objective

• Maintain Competence

• Be Fair & Open

• Maintain Confidentiality

• Act Diligently

• Be Professional

For a full description of the Code, visit FPSC.ca

SPRING 2015 – 8

UNIFIED STANDARDS FOR THE CANADIAN FINANCIAL PLANNING PROFESSIONFPSC and the Institut québécois de planification financière (IQPF), the two organizations that establish and maintain standards for the financial planning profession in Canada, have for the first time come together to establish a unified set of financial planning standards.

With the Canadian Financial Planning Definitions, Standards & Competencies, FPSC and IQPF establish a unified code of ethics and a common set of practice standards by which individuals holding the F.Pl. diploma and CFP® designation must abide. They also define the ethical and performance standards that clients should expect from a professional relationship.

“We’ve achieved unprecedented consensus within the financial planning profession to unify standards that will help give Canadians clarity and confidence when engaging a qualified financial planner,” says Cary List, President and CEO of FPSC. “Together we will use this as a foundation to elevate financial planning as a distinct professional practice in Canada; one that holds itself to the highest possible standards of ethics and performance.”

“This is a milestone for the financial planning profession,” says Jocelyne Houle-LeSarge, President and CEO of IQPF. “This publication plays an important role in driving consistency across the financial planning profession by specifying unified standards for those practicing within it. It further acts as a resource to the industry firms, financial planning educators, other key industry partners and the Canadian public at large.”

Recent research by the Financial Planning Coalition* reveals the significant need for clarity around standards. The survey found that while most Canadians feel they have insufficient knowledge to adequately

plan their financial future, they are also unaware of the lack of mandatory standards for financial planners throughout most of Canada.

The research found that two-thirds of Canadians feel they need help planning their financial futures, but most are unaware of the lack of regulatory standards for financial planners throughout most of Canada. Fewer than half of respondents (49 per cent) know there is a difference between a financial planner and a financial advisor, while almost half (44 per cent) believe there are regulatory standards in place for financial planners.

In unifying financial planning standards, FPSC and IQPF have clearly defined what “financial planning”, a “financial planner” and a “financial plan” really mean. These definitions and standards emphasize objectivity; confidentiality; ethics and client interest first; a deep understanding of the financial needs, goals and aspirations of the client; and a high level of competence as essential characteristics of all financial planners. Critically, the organizations stipulate that a true financial planner must be appropriately qualified and agree to be accountable to professional oversight and to putting their clients’ interests first.

The Canadian standards for financial planning are consistent with the highest professional standards in financial planning internationally, through association with the Financial Planning Standards Board (FPSB), which represents standards for over 150,000 financial planners worldwide.

*Members of the Financial Planning Coalition include Financial Planning Standards Council (FPSC), Institut québécois de planification financière (IQPF), the Canadian Institute of Financial Planners (CIFPs) and the Institute of Advanced Financial Planners (IAFP).

Financial Planning Standards Council

Financial Planning Standards Council (FPSC®) is a not-for-profit organization which develops, promotes and enforces professional standards in financial planning through Certified finanCial Planner® certification. FPSC’s purpose is to instill confidence in the financial planning profession. As a standards-setting and certification body, FPSC ensures CFP® professionals and FPSC Level 1™ Certificants in Financial Planning meet appropriate standards of competence and professionalism through rigorous requirements of education, examination, experience and ethics. More information is at www.fpsc.ca.

The Institut québécois de planification financière

The Institut québécois de planification financière (IQPF) is the only organization in Quebec authorized to grant financial planning diplomas and to establish rules concerning the ongoing professional development of professional financial planners. Only professionals recognized by the Institut québécois de planification financière are authorized to use the title of Financial Planner (F.Pl.) in Quebec.The IQPF is also the only organization in the province entirely dedicated and reserved forfinancial planners.

CARY LIST, CA, CPA, CFP®

PRESIDENT & CEO, FPSCJOCELYNE HOULE-LESARGE,PRESIDENT & CEO, IQPF

SPRING 2015 – 9

BECOMING A CERTIFIED NECESSITY™

Financial planners are in demand now and will be even more in the future. Helping people plan for their future financially isn’t just a way to make a living. It’s a way to make a difference. When you become a Certified finanCial Planner® professional, you have the opportunity to give clients peace of mind and a true road map to their financial well-being. CFP certification represents the standard for the profession, demanding the highest level of competence, ethics and practice. Below is a depiction of the path to CFP certification. For more information on the specific steps, be sure to read page 10 of this publication.

SPRING 2015 – 10

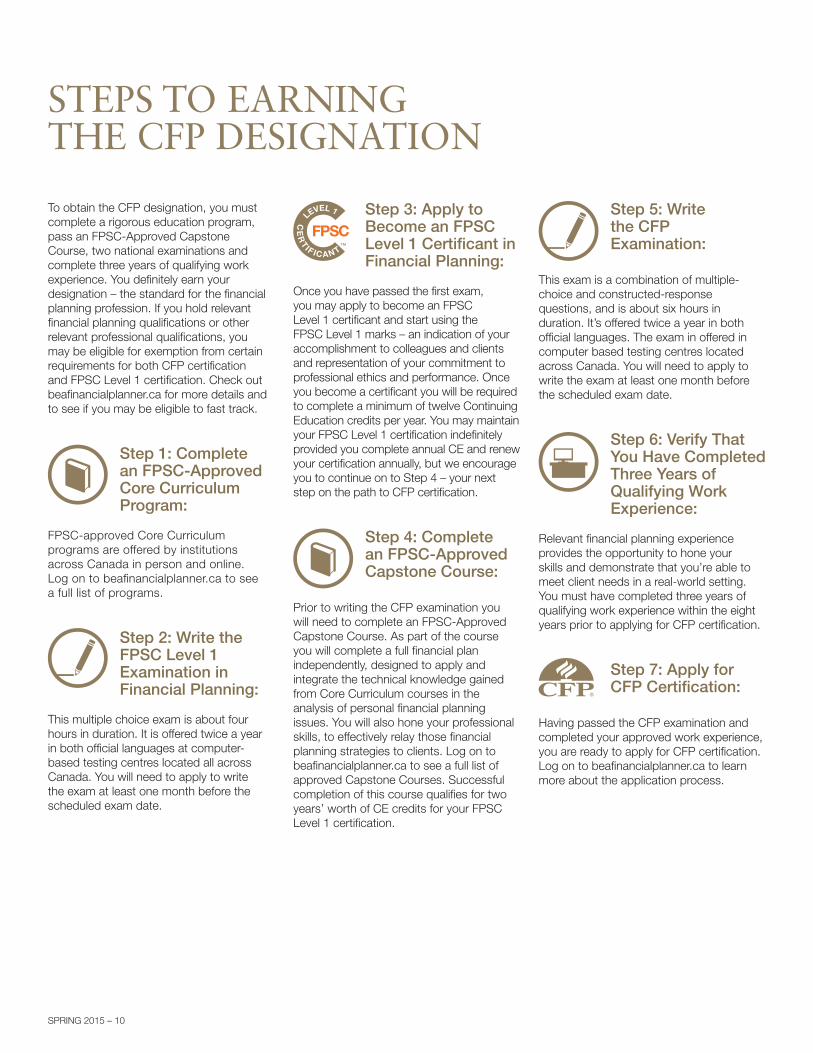

STEPS TO EARNING THE CFP DESIGNATION

To obtain the CFP designation, you must complete a rigorous education program, pass an FPSC-Approved Capstone Course, two national examinations and complete three years of qualifying work experience. You definitely earn your designation – the standard for the financial planning profession. If you hold relevant financial planning qualifications or other relevant professional qualifications, you may be eligible for exemption from certain requirements for both CFP certification and FPSC Level 1 certification. Check out beafinancialplanner.ca for more details and to see if you may be eligible to fast track.

Step 1: Complete an FPSC-ApprovedCore Curriculum Program:

FPSC-approved Core Curriculum programs are offered by institutions across Canada in person and online. Log on to beafinancialplanner.ca to see a full list of programs.

Step 2: Write the FPSC Level 1 Examination in Financial Planning:

This multiple choice exam is about four hours in duration. It is offered twice a year in both official languages at computer-based testing centres located all across Canada. You will need to apply to write the exam at least one month before the scheduled exam date.

Step 3: Apply to Become an FPSC Level 1 Certificant in Financial Planning:

Once you have passed the first exam, you may apply to become an FPSC Level 1 certificant and start using the FPSC Level 1 marks – an indication of your accomplishment to colleagues and clients and representation of your commitment to professional ethics and performance. Once you become a certificant you will be required to complete a minimum of twelve Continuing Education credits per year. You may maintain your FPSC Level 1 certification indefinitely provided you complete annual CE and renew your certification annually, but we encourage you to continue on to Step 4 – your next step on the path to CFP certification.

Step 4: Complete an FPSC-Approved Capstone Course:

Prior to writing the CFP examination you will need to complete an FPSC-Approved Capstone Course. As part of the course you will complete a full financial plan independently, designed to apply and integrate the technical knowledge gained from Core Curriculum courses in the analysis of personal financial planning issues. You will also hone your professional skills, to effectively relay those financial planning strategies to clients. Log on to beafinancialplanner.ca to see a full list of approved Capstone Courses. Successful completion of this course qualifies for two years’ worth of CE credits for your FPSC Level 1 certification.

Step 5: Write the CFP Examination:

This exam is a combination of multiple-choice and constructed-response questions, and is about six hours in duration. It’s offered twice a year in both official languages. The exam in offered in computer based testing centres located across Canada. You will need to apply to write the exam at least one month before the scheduled exam date.

Step 6: Verify That You Have Completed Three Years of Qualifying Work Experience:

Relevant financial planning experience provides the opportunity to hone your skills and demonstrate that you’re able to meet client needs in a real-world setting. You must have completed three years of qualifying work experience within the eight years prior to applying for CFP certification.

Step 7: Apply for CFP Certification:

Having passed the CFP examination and completed your approved work experience, you are ready to apply for CFP certification. Log on to beafinancialplanner.ca to learn more about the application process.

SPRING 2015 – 11

STUDY TIPS FROM PRESIDENT’S LIST WINNERS

CANADA’S TOP CFP EXAMINATION CANDIDATES SHARE THEIR ADVICE R. PAUL THORNE

DARTMOUTH, NOVA SCOTIA1ST PLACE PRESIDENT’S LIST RECIPIENTNOVEMBER 2014

GREG BALDWINTORONTO, ONTARIO1ST PLACE PRESIDENT’S LIST RECIPIENTJUNE 2014

FPSC’s President’s List recognizes the top three candidates from across Canada who have earned the highest marks on the CFP examination, the final exam on the path to CFP certification.

Here, the first place President’s List recipients from the 2014 CFP examinations share study tips for exam candidates, their experiences along the path to CFP certification and the benefits of being a CFP professional.

Q: How do you feel about being named a President’s List recipient?

Greg: It was quite an honour – definitely a confidence booster in my dealings with clients.

Paul: It was a complete surprise, because it’s not an easy exam and it’s hard to know how you did when you walk out of it.

Q: What do you think were the key factors for your success in the exam?

Paul: I made sure I bought and prepared with the FPSC Practice Exam. You can’t beat it to help you get comfortable with the software, familiarize yourself with how the questions are asked, and learn what to expect on the exam. I also attended FPSC’s exam preparation webinar to find out what other resources were available.

Q: What is your best study tip?

Greg: When you come across a topic you are struggling to understand, write it down in a notebook with all the details. I thought of this as a ‘What I didn’t know list’. Taking extra time to study the areas you find difficult will give you more confidence going in to the exam.

Q: What advice would you give to other candidates preparing for the exam?

Greg: Everyone struggles with time management challenges, especially when you’re already working in the industry. It’s not so much about finding the time, but prioritizing it. Studying will never seem as pressing as an important client meeting or other work commitment, so you need to schedule the preparation time and stick to it.

Q: Now that you have the CFP designation, do you feel you’re perceived differently?

Greg: There’s definitely a change in the way clients perceive you – they have more confidence in your knowledge. There are countless people calling themselves financial advisors, but I’m part of the small percentage in Canada with the CFP designation who are truly professional financial planners.

Q: How has obtaining the CFP designation improved your career prospects?

Paul: Having the CFP certification provides you with an invaluable base set of knowledge that gives you the ability to be comfortable in any number of different client situations. You can’t compare the comprehensive knowledge you gain from the CFP designation to anything else that’s out there.

Q: What is the most rewarding part of your role as a CFP professional?

Greg: As a CFP professional, I have the opportunity to have a significant impact on people’s lives by making them feel more confident about where they are financially. At the end of the day, my ultimate goal is to improve my clients’ well-being.

TOP 10 STUDY TIPS FROM 2014’S HIGHEST SCORERS

1. Prepare with FPSC’s Practice Exam to get familiar with the software and types of questions.

2. Schedule time for studying and stick to it.

3. Keep a ‘What I didn’t know’ list of notes about topics you find challenging.

4. Attend FPSC’s exam preparation webinar.

5. Consider an exam preparation course.

6. Answer the question and explain why that’s the answer – details and process are important.

7. Remember that there is more than one way to answer a question.

8. If you work in the financial industry, take advantage of your day-to-day work to help integrate the information you need to learn.

9. Don’t take the exam lightly – be prepared.

10. Ask your employer how they can help to support you as you work toward your CFP designation.

SPRING 2015 – 12

WHAT’S HAPPENING@ FPSC_CANADA 2015

JUN 05 CFP examination and FPSC Level 1TM Examination in Financial Planning are held at various locations across Canada. You must register at least one month prior to the exam.

JUN 08-11 Technical Knowledge Content Development session with CFP professional volunteers in Ottawa, ON.

JUL Results of the June 2015 CFP examination and FPSC Level 1 Examination in Financial Planning are made available.

JUL 20-24 Item writing workshops with CFP professional volunteers in Montebello, QC.

AUG 10-13 Technical Knowledge Content Development session with CFP professional volunteers in Winnipeg, MB.

SEP CFP Professional Ambassadors head back into Core Curriculum classrooms across the country to educate students on the value of the CFP designation. To book an Ambassador for your school, email [email protected].

OCT 19-22 Technical Knowledge Content Development session with CFP professional volunteers in Toronto, ON.

OCT& NOV FPSC’s national consumer awareness campaign begins – watch for news on where to see our television commercials.

NOV 15-21 7th Annual Financial Planning Week takes place across Canada. Visit fpsc.ca/about-fpw.

NOV 16 The Globe and Mail special report on Financial Planning is published. To reserve space, contact Richard Deacon, National Business Development Manager, The Globe and Mail at [email protected] or 604 631 6636.

NOV 17Celebration of the Profession Reception and Dinner at the Old Mill Inn in Toronto in conjunction with Financial Planning Week. Hosted by comedian Judy Croon, it’s going to be a fabulous evening. Seats can be reserved in September.

NOV 18Special Breakfast CE Session on Ethics at the Old Mill Inn in Toronto. Facilitated by FPSC’s Director, Enforcement alongside panelists Cary List, President & CEO, FPSC and ethics expert Rod Burylo. Tickets go on sale in September.

NOV 18CFP professionals gather for a full day of Continuing Education at the 2015 Toronto CFP Professional Symposium at the Old Mill Inn. This year’s theme is “Trust Matters”, with a lineup of amazing speakers and a keynote address from Scott Stratten: Un-marketing 101. Be sure to reserve your seat when they go on sale in September.

NOV 20Special Breakfast CE Session on Ethics at the Pan Pacific Hotel in Vancouver. Facilitated by FPSC’s Director, Enforcement alongside panelists Cary List, President & CEO, FPSC and ethics expert Rod Burylo. Tickets go on sale in September.

NOV 20CFP professionals gather for a full day of Continuing Education at the 2015 Vancouver CFP Professional Symposium at the Pan Pacific Hotel. This year’s theme is “Trust Matters”, with a lineup of amazing speakers and a keynote address from Scott Stratten: Un-marketing 101. Be sure to reserve your seat when they go on sale in September.

NOV 23-27 Item writing workshops with CFP professional volunteers in Niagara-on-the-Lake, ON.

NOV 27 The winter administration of the CFP examination and FPSC Level 1 Examination in Financial Planning is held at various locations across Canada. You must register at least one month prior to the exam.

The Financial Planning Foundation is a charitable organization that is committed to developing and promoting financial planning research and education for the benefit of financial and allied professionals, education providers and the Canadian public.

YOU CAN HELP SHAPETHE CANADIAN FINANCIALPLANNING LANDSCAPE

Support the Foundation today.fpfoundation.ca

TM

CFP®, Certified finanCial Planner® and are certification trademarks owned outside the U.S. by Financial Planning Standards Board Ltd. (FPSB). Financial Planning Standards Council is the marks licensing authority for the CFP marks in Canada, through agreement with FPSB. All other ® are registered trademarks of FPSC, unless indicated. ©2015 Financial Planning Standards Council. All rights reserved.

FSC printing logo here

Become aCertified Necessity. Helping people plan for their future financially isn't just a way to make a living. It’s a way to make a difference. When you become a Certified finanCial Planner® professional you have the opportunity to give clients peace of mind. Research shows that Canadians who work with a CFP®

professional feel their financial goals and retirement plans are more on track, their ability to save has improved, and they’re more confident they can handle the inevitable bumps in life.

Learn how to earn the CFP designation. It’s the industry gold standard in financial planning—don’t settle for less.

To learn more about CFP certification visit beafinancialplanner.ca