Forex Market _2

18

FOREIGN EXCHANGE RATES Basic calculation-cont….

-

Upload

emad-tabassam -

Category

Documents

-

view

224 -

download

0

Transcript of Forex Market _2

8/3/2019 Forex Market _2

http://slidepdf.com/reader/full/forex-market-2 1/18

FOREIGN EXCHANGE RATES

Basic calculation-cont….

8/3/2019 Forex Market _2

http://slidepdf.com/reader/full/forex-market-2 2/18

FOREIGN CURRENCY

Basis Point

1 cent = 100 basis points

For example $/£ 1.8525. This means that there is one dollar, 85 cents and 25 basis

points to the pound or there is one dollar and 851/4 cents to the pound

Illustration $/£ 1.8645

Narrate the exchange rate in terms of basis points

Illustration $/£ 1.0550

Narrate the exchange in terms of basis points

As cent represents one hundredth of a dollar

So basis point represents one-hundredth of a cent

1 dollar = 100 cents

There is one Dollar, 86 cents and 45 basis points to the pound

There is one Dollar, 5 cents and 50 basis point to the pound

8/3/2019 Forex Market _2

http://slidepdf.com/reader/full/forex-market-2 3/18

INVERTING EXCHANGE RATES:

If you are given a middle rate: $/£ 1.5385, this indicates that

$1.5385=pound 1. Notice that the exchange rate can be found from the

inversion of the $/£ exchange rate.

Illustration

If exchange rate: $/£ 1.5240; andY/£ 235.20

Determine

Exchange rate Y/$

SolutionY/$ = 235.20 = 154.33

1.5240

Thus £/$ = 1/1.5385 = 0.6500 In other words £ 0.6500 (or 65 p) = $1

8/3/2019 Forex Market _2

http://slidepdf.com/reader/full/forex-market-2 4/18

Illustration 2

If exchange rate: DM/£ 2.5150; and

PTE/£ 205.80

DetermineExchange rate PTE/DM

Illustration 3If exchange rate: Y/$ 154.33; and

Y/£ 235.20

Determine

Exchange rate £/$

Solution 2 PTE/DM = 205.80 = 81.83

2.5150

Solution 3 £/$ = 154.33 = 0.6562

235.20

8/3/2019 Forex Market _2

http://slidepdf.com/reader/full/forex-market-2 5/18

Illustration 4

If exchange rate: SFF/£ 4.3510; and

$/SFF 0.4450

DetermineExchange rate $/£

However, be careful if you wish to turn exchange rate around in this way and you

are given a buying and selling rate. Not only should you take the inverse of each,but also switch each around s follows:

Solution 4 $/£ =0.4450 * 43510 = 1.9362

£/$ 0.6734 0.6748

$/ £ 1.482 1.485

£/$ 1 11.485 1.482

8/3/2019 Forex Market _2

http://slidepdf.com/reader/full/forex-market-2 6/18

Illustration 6

If exchange rate: Rs./$ 55 – 58 ; and

Rs./Y 0.4852 – 0.4910

DetermineExchange rate $/Y

$/Y 0.008365 0.008926

$/Rs. 0.1724 0.01818

Rs./Y 0.4852 0.491

Rs./$ 55 58

Rs./$ 1 1

58 55

8/3/2019 Forex Market _2

http://slidepdf.com/reader/full/forex-market-2 7/18

Illustration 6

SOLUTION

Y/$ 153.8663 154.6649

Y/£ 234.8 235.4

If exchange rate: $/£ 1.522 – 1.526 ; and

Y./£ 234.8 – 235.4

DetermineExchange rate Y/$

Illustration 6

$/£ 1.522 1.526

1 1

£/$ 1.526 1.522

8/3/2019 Forex Market _2

http://slidepdf.com/reader/full/forex-market-2 8/18

Spot Market

Is where you can buy and sell currencies for immediate (i.e. on the

spot) exchange or delivery.

Forward MarketIs where you can arrange a deal now to buy or sell a specific amount of

currency at a specific rate of exchange (the forward rate) for exchange/delivery

on a specific future date (the forward date).

Although spot markets exist for most of the world’s currencies, for many of the more minor currencies there is no forward market, because there is

insufficient demand.

The four major trading currencies in the world are the US$, £, Y and DM and

the forward market amongst these currencies can stretch up to 10 years

forward.

Standard periods of time forward are one month, three months and these rates

and together with the spot rate are instantly available. Other forward rates such

as the 84 days forward rate have to be specially quoted by the bankers.

8/3/2019 Forex Market _2

http://slidepdf.com/reader/full/forex-market-2 9/18

Spot and forward rates may be given as follows:

$/pound spot 1.5840 – 1.5860

However it is more likely that instead of being given the forward rates like

this you are given them as a rate of discount on the spot rate:

Three months forward 6.85c – 7.00 c discount

$/pound spot 1.5840 – 1.5860

$/pound one month forward 1.6290 – 1.6335

$/pound three months forward 1.6525 – 1.6560

One month forward 4.50 c – 4.75 c discount

8/3/2019 Forex Market _2

http://slidepdf.com/reader/full/forex-market-2 10/18

Therefore:

Spot 1.5840 – 1.5860

1 month forward 1.6290 – 1.6335

3 months forward 1.6525 - 1.6560

To obtain the actual forward rate, you add the discount to spot rate

Add discount 0.0450 – 0.0475

And

Spot 1.5840 – 1.5860

Add discount 0.0685 - 0.0700

8/3/2019 Forex Market _2

http://slidepdf.com/reader/full/forex-market-2 11/18

Putting this more technically, the $ is weakening or depreciating against thePound. It is becoming less valuable. (And Pound therefore is appreciating )

More generally, If forward rates are at a discount, the first currently is

depreciating against the second currency is your pair of currencies.

If you want to buy $/Pound spot, for every 1 Pound you would receive$1.5840, but if you bought $ for 3 months/ forward delivery you get $ 1.6525

for every 1 Pound.

Thus in the forward markets, the $ is becoming cheaper to buy.

NOTE

When

Forward rates are at discount to the spot ratesForward rates > Spot rates

To illustrate further

8/3/2019 Forex Market _2

http://slidepdf.com/reader/full/forex-market-2 12/18

this signifies that the first currency is appreciating against the second of the pair of

currencies.

When

Forward rates < Spot rates

Forward rates are at Premium to the spot rates

When forward rates are quoted at a premium, we subtract the premium

from the spot rate to find the forward rate.

Therefore Whenever forward rates are smaller numbers than spot rates,

the forward rates are at a premium

And

8/3/2019 Forex Market _2

http://slidepdf.com/reader/full/forex-market-2 13/18

Illustration 7$/pound spot 1.8420 1.8260

1 month forward 0.85 c 0.75 c Premium

Determine one month forward rate

Solution

1 month forward 1.8335 1.8185

The $ is becoming more valuable, it is appreciating against Pound. Every 1 Pound

buys you $ 1.8420 at spot, but only buys you $1.18335 in one month’s time.

Spot 1.8420 - 1.8260

- premium 85 - 75

8/3/2019 Forex Market _2

http://slidepdf.com/reader/full/forex-market-2 14/18

Illustration 8$/pound spot 1.5210

12 months forward 8.65 c Discount

Determine Twelve months forward rate

Solution

+ discount 0.0865

Spot rate $/£ 1.5210

12 months forward rate 1.6075

8/3/2019 Forex Market _2

http://slidepdf.com/reader/full/forex-market-2 15/18

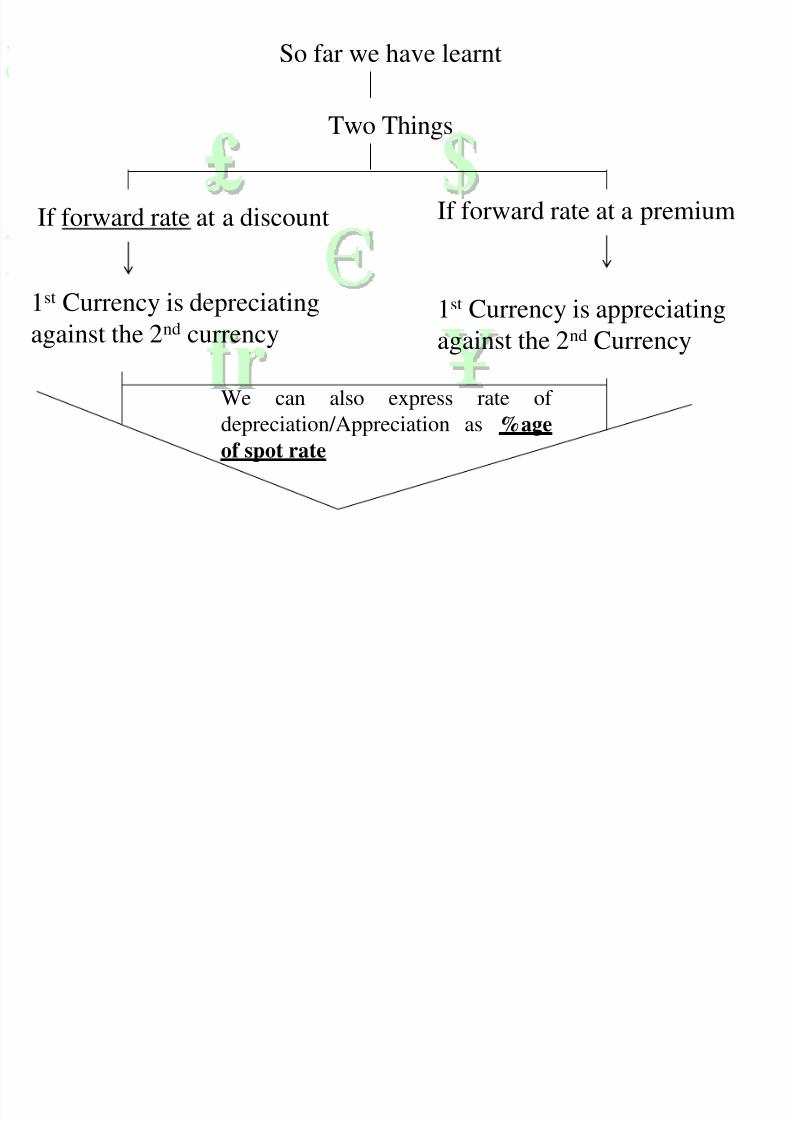

So far we have learnt

Two Things

If forward rate at a discount

1st Currency is depreciating

against the 2nd currency

If forward rate at a premium

1st Currency is appreciating

against the 2nd Currency

We can also express rate of

depreciation/Appreciation as %ageof spot rate

8/3/2019 Forex Market _2

http://slidepdf.com/reader/full/forex-market-2 16/18

For Example$/pound spot 1.5210

12 months forward 8.65 c Discount

Determine Twelve months forward rate

Rate of Depreciation = Discount x 100%= 0.0865 x 100%=5.69%

Spot rate 1.5210

Which indicate (as it is a discount) that a forward rate represents a 5.69%

depreciation of the $ on the spot rate. As a result, the forward rate can be

calculated as:

Forward rate = spot rate x (1+ rate of depreciation)

12 month forward = 1.5210 x (1 + 0.0569) = 1.6075

8/3/2019 Forex Market _2

http://slidepdf.com/reader/full/forex-market-2 17/18

Illustration 9$/pound spot 1.6580

12 months forward 5c PremiumDetermine Twelve months forward rate

Solution 9

Therefore the forward rate represents a 3% appreciation in the $ giving

12 Months forward rate $/£ = 1.6580* (1 – 0.03) = $ 1.6083

Similarly

Rate of Appreciation = Premium x 100% = x %

Spot rateForward rate = Spot rate x (1 – rate of appreciation)

Rate of Appreciation= 0.05 = 0.03 or 3%

1.6580

8/3/2019 Forex Market _2

http://slidepdf.com/reader/full/forex-market-2 18/18

Illustration 10Suppose you are told that $/pound Spot is 1.5345 and the $ is expected to

depreciate by 5% per year over the next two years and thereafter appreciate

by 7% per year.

Required

Calculate the forward rates for the next 5 years.

SolutionOne year forward $1.5345 * (1+ 0.05) = $1.6112

Two years forward $1.6112 * (1 + 0.05) = $ 1.6918

Three year forward $1.6918 * (1- 0.07) = $ 1.5734

Four year forward $ 1.5734 * (1 - 0.07) = $ 1.4632

Five year forward $ 1.4632 * (1 – 0.07) = $ 1.3608