Forest Carbon Aggregation - EPRIeea.epri.com/pdf/ghg-offset-policy-dialogue/... · Forest Carbon...

17

Forest Carbon Aggregation Looking back, looking forward EPRI Offsets Workshop #12, March 15, 2012 The views expressed in this presentation are the views of the author and do not necessarily represent the position of any author and do not necessarily represent the position of any New Forests corporate entity. Contact: Brian Shillinglaw N F tI New Forests Inc. (415) 321 3305 bshillinglaw@newforests‐us.com

Transcript of Forest Carbon Aggregation - EPRIeea.epri.com/pdf/ghg-offset-policy-dialogue/... · Forest Carbon...

Forest Carbon AggregationLooking back, looking forward

EPRI Offsets Workshop #12, March 15, 2012

The views expressed in this presentation are the views of the author and do not necessarily represent the position of anyauthor and do not necessarily represent the position of any New Forests corporate entity.

Contact:Brian ShillinglawN F t INew Forests Inc.(415) 321 3305bshillinglaw@newforests‐us.com

Outline

1 Introd ction to Ne Forests1. Introduction to New Forests

2. Aggregation: why bother?

3. New Forests’ experience to date

4. Two core models for carbon aggregation

5 Suggestions for the path forward5. Suggestions for the path forward

Slide 2

About New Forests3

Global real asset manager. New Forests manages over USD $1 billion ing g $capital for investments in sustainable timber and associated environmentalmarkets, such as carbon, biodiversity and water. Headquartered in Sydney,with offices in San Francisco and Singapore.

Forest carbon offset expertise. New Forests has participated as a stakeholderand investor in the development and implementation of forest carbon offsetmarkets and cap and trade systems in multiple countries for over six years.

Projects developed for the California market. We have invested in forestProjects developed for the California market. We have invested in forestcarbon offset projects for the California market through two fund vehicles andare developing projects on over 71,000 acres.

Slide 3

Aggregation: why bother? Western Climate Initiative policy.

75% of U.S. private forestland is in small holdings of <5,000 acres.

It’s where the carbon is.

Slide 4 Source: http://www.nrs.fs.fed.us/pubs/gtr/gtr_wo78.pdf; New Forests analysis

New Forests & Forest Carbon Aggregation

CAR aggregation stakeholder committee (2010)CAR aggregation stakeholder committee (2010)

Forest Carbon Partners, L.P. Launched in 2011 Launched in 2011 Finances and develops projects with family forest owners and Native American tribes

11,500 acres of projects under development at present, expect 17,000 this quarter

Will aggregate projects if aggregation rules adopted by ARB

Slide 5

Aggregation Value Proposition

For landownersFor landowners Project finance, project management, credit sales management, market access (high volume sales), potentially reduced costs via CAR aggregation rules

For compliance buyers Portfolio diversification – reduced delivery risk Scalable supply relationship One counterparty, one point of sale Charismatic carbon

Slide 6

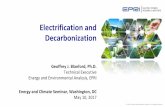

Aggregation Challenges

Key challenges in aggregating forest projects:Key challenges in aggregating forest projects: Skepticism of landowners in early stage of system Origination costs Origination costs Credit yield estimation in low‐data environment Low percentage of projects pencil out at current costs p g p j pand expected near‐term carbon prices Inventory and verification costs are key

Managing credit invalidation risk

Slide 7

Outline

1 Introd ction to Ne Forests1. Introduction to New Forests

2. Aggregation: why bother?

3. New Forests’ experience to date

4. Two core models for carbon aggregation

5 Suggestions for the path forward5. Suggestions for the path forward

Slide 8

Models of Aggregation

1. Project‐centric: aggregator as service provider1. Project centric: aggregator as service provider Example: CAR forest carbon aggregation rules Baseline, additionality, MRV, permanence assessed Baseline, additionality, MRV, permanence assessed

and enforced at project level Aggregation reduces MRV costs – quantification and

verification

2. Aggregate‐centric: aggregator as project owner Permanence, MRV, and potentially baseline and

ddi i li d l ladditionality assessed at aggregate level

Slide 9

Two Approaches to the Key Aggregation Issues

#1: Project‐centric #2: Aggregate‐centric

Temporal dispersion Feasible FeasibleTemporal dispersion Feasible Feasible

Geographical dispersion Feasible Feasible

Additionality Measured at project level Measured at project orAdditionality Measured at project level Measured at project or aggregate level

Risk allocation Project‐focused Aggregator‐focused

Quantification Project‐focused with cost savings from aggregation

Either project or aggregate‐focused

MRV Project‐focused, with cost Aggregate‐focusedsavings from aggregation

Permanence Project (default liability) Aggregator (default liability)

Invalidation liability Project (default liability) Aggregator (default liability)

Slide 10

Invalidation liability Project (default liability) Aggregator (default liability)

Forest Carbon Aggregation in Compliance Markets

Permanence and invalidation liability are key.Permanence and invalidation liability are key. Integrity of the cap requires strong assurance that MRV is accurate and permanence is maintained.

Market participants prefer aggregation model #2:p p p gg g Permanence and invalidation liability most efficiently managed by aggregator.

Landowners can more easily enter and exit. Aggregator can more easily manage invalidation li bili i h l f li f ff iliability with large portfolio of offset instruments.

Slide 11

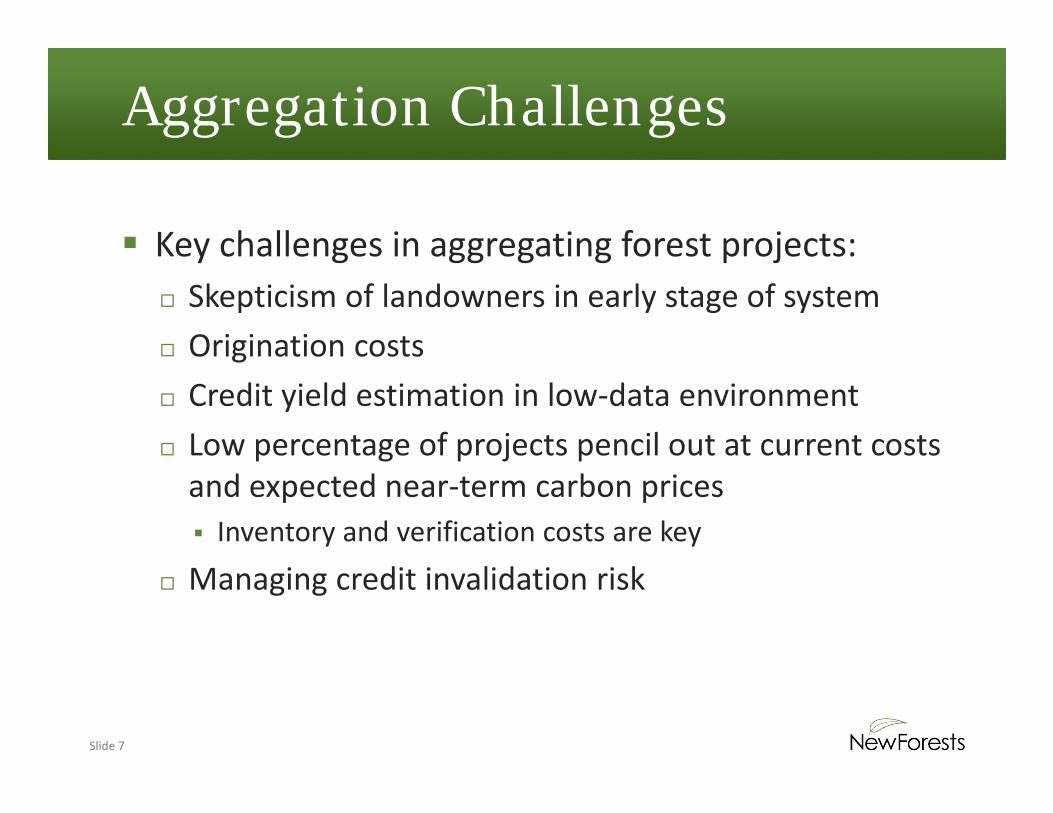

Forest Carbon Aggregation in Compliance Markets

Regulator concerns about aggregation model #2 inRegulator concerns about aggregation model #2 in sequestration project context: Compliance market regulators have historically p g yexpressed some concern about default assignment of permanence and credit invalidation liability to a

j t d l t ti titproject developer or corporate aggregation entity.

H d f ll t t t j tHow do we carefully structure true project aggregation in compliance markets to adequately

ensure permanence and credit quality?ensure permanence and credit quality?

Slide 12

Outline

1 Introd ction to Ne Forests1. Introduction to New Forests

2. Aggregation: why bother?

3. New Forests’ experience to date

4. Two core models for carbon aggregation

5 Suggestions for the path forward5. Suggestions for the path forward

Slide 13

A path forward with two tracks

Both models of aggregation should be available in gg gcompliance markets.

Track #1. Compliance market adoption of aggregation model #1. e.g. CAR forest carbon aggregation rules

T k #2 L i h f d i Track #2. Laying the foundation to support compliance market adoption of aggregation model #2#2.

Slide 14

A path forward with two tracks

One approach to enabling aggregation model #2 in the pp g gg gcompliance market sequestration project context: Legislative adoption of a terrestrial carbon property right at the state

level (technically: a new type of negative easement in gross)level (technically: a new type of negative easement in gross)

Require aggregators to hold such a carbon property right on all projects

I th t f t b k t di l ti i h In the event of aggregator bankruptcy or dissolution, require such carbon property rights to escheat to the state.

Aggregator thereby becomes project owner after acquiring rights from landowner.

Strong assurance of recovery in the event of intentional reversal of obligated carbon or credit invalidationreversal of obligated carbon or credit invalidation.

Slide 15

Summary

New Forests is actively engaged in financing and aggregating forest b j t f th C lif i li k tcarbon projects for the California compliance market.

Aggregation is critical to organizing adequate offset supply and in the forest carbon context leads to strong environmental and social co‐benefitsco‐benefits.

Aggregation delivers significant economic value to landowners and to compliance offset purchasers.

There are two core models of carbon project aggregation: project‐ There are two core models of carbon project aggregation: project‐centric and aggregator‐centric.

Many market participants prefer an aggregator‐centric model. Recommendation: compliance markets enable both aggregation Recommendation: compliance markets enable both aggregation

models for sequestration carbon projects. An aggregator‐centric model may be facilitated by the legislative adoption of a forest carbon property right.

Slide 16

www newforests com auwww.newforests.com.au