FOR PM 3: 2 7 - Stanford...

94

IN THE UNITED STATES DISTRICT COURT FOR THE' L " F C i NORTHERN DISTRICT OF ALABAMA 00 JUN IS PM 3: 2 7 SOUTHERN DIVISIO N STATE OF WISCONSIN INVESTMENT N .D . OF ~~•L a. `AMA BOARD, KENNETH D . BUSH , EDWARD E . EUBANK, JR., JOHN MICHAEL, et al., suing on behalf of themselves and all others similarly situated, JURY TRIAL DEMANDED Plaintiffs, vs. CV 99-BU-3097-S and HAROLD RUTTENBERG ; CV 99-BU-3129-S ERIC L . TYRA ; PETER BERMAN COOPER EVANS ; PATRICK LLOYD ; DON-ALLEN RUTTENBERG ; MICHAEL LAZARUS ; HELEN ROCKEY ; SCOTT C . WYNNE ; RANDALL L. HAINES ; ADAM GILBURNE ; DELOITTE & TOUCHE LLP ; STEVEN H . BARRY ; and KAREN BAKER, Defendants . CONSOLIDATED CLASS ACTION COMPLAINT Plaintiffs, by their undersigned counsel, for their Consolidated Class Action Complaint, o n their own behalf and as representatives of those similarly situated, upon personal knowledge as to themselves and their own acts, and based upon the investigation by their counsel which has included review and analysis of public statements, publicly-filed documents, press releases and news articles, analysts' statements, interviews of persons knowledgeable of the facts stated herein, and relevant accounting rules and related literature, allege as follows :

-

Upload

nguyennguyet -

Category

Documents

-

view

214 -

download

0

Transcript of FOR PM 3: 2 7 - Stanford...

IN THE UNITED STATES DISTRICT COURT FOR THE' L" F CiNORTHERN DISTRICT OF ALABAMA 00 JUN IS PM 3: 2 7

SOUTHERN DIVISION

STATE OF WISCONSIN INVESTMENT N .D. OF ~~•L a. `AMABOARD, KENNETH D . BUSH,EDWARD E. EUBANK, JR., JOHNMICHAEL, et al., suing on behalf ofthemselves and all others similarly situated,

JURY TRIAL DEMANDEDPlaintiffs,

vs. CV 99-BU-3097-Sand

HAROLD RUTTENBERG; CV 99-BU-3129-SERIC L . TYRA ;PETER BERMANCOOPER EVANS ;PATRICK LLOYD ;DON-ALLEN RUTTENBERG ;MICHAEL LAZARUS ;HELEN ROCKEY ;SCOTT C . WYNNE ;RANDALL L. HAINES ;ADAM GILBURNE ;DELOITTE & TOUCHE LLP ;STEVEN H. BARRY ; andKAREN BAKER,

Defendants .

CONSOLIDATED CLASS ACTION COMPLAINT

Plaintiffs, by their undersigned counsel, for their Consolidated Class Action Complaint, o n

their own behalf and as representatives of those similarly situated, upon personal knowledge as to

themselves and their own acts, and based upon the investigation by their counsel which has included

review and analysis of public statements, publicly-filed documents, press releases and news articles,

analysts' statements, interviews of persons knowledgeable of the facts stated herein, and relevant

accounting rules and related literature, allege as follows :

NATURE OF THE ACTION

1 . This is a securities class action on behalf of all persons and entities (other than

Defendants and affiliated persons as defined in paragraph 37 below) who purchased common stock

of Just For Feet, Inc . ("Just For Feet" or the "Company") between May 5, 1997 and November 1,

1999 (the "Class Period") and who have suffered a loss .

2 . During the Class Period, defendants Harold Ruttenberg, Eric Tyra, Scott Wynne and

Deloitte & Touche, L .L.P . ("Deloitte"), with the knowledge, assistance and participation of the other

defendants, orchestrated a scheme to defraud public shareholders and purchasers of Just For Feet

securities. In sum, the scheme entailed publishing fraudulent and false financial statements for Just

For Feet for a minimum of three fiscal years, that materially overstated sales, profits and income ;

understated costs ; overstated accounts receivable, inventories, equipment, fixed assets and

stockholders' equity ; and understated significant liabilities . The scheme also included the

concealment of the material omitted facts described herein .

3 . The fraud concerns at least nine specific areas of accounting gimmicks, including :

(1) creating a fraudulent kickback scheme from its advertising agency in order to increase revenues ;

(2) creating false billings and receivables for booth assets donated by shoe manufacturers ; (3)

creating other false vendor billings and receivables ; (4) failing to write off bad debt; (5) failing to

book required loss reserves ; (6) understating its cost of sales through the improper use of acquisition

accounting ; (7) improperly capitalizing inventory costs and expenses that should have been reported

as current operating expenses ; (8) overstating ending inventory by not accounting or reserving for

obsolete or missing inventory and by arbitrarily writing up the costs of inventory that was transferred

between stores or divisions ; (9) overstating earnings and understating liabilities by improperly

2

accounting for leaseholds. In addition, Just for Feet knowingly maintained woefully inadequate

accounting and inventory control systems .

4 . Through the use of false and fraudulent financial statements, Just For Feet was able

to convey the appearance of a profitable operating company when, in reality, Just For Feet was not

a viable concern . In fact, Just For Feet was principally supported by its credit lines which were only

available to it because of its fraudulently prepared financial statements.

5 . As a result of this fraud, the market prices of Just For Feet common stock (which

ranged from a high of $29 .00 per share during the Class Period to a low of $1 .25 per share) were

materially and artificially inflated throughout the Class Period .

6 . On November 2, 1999, Just For Feet announced its intention of seeking Chapter 1 1

bankruptcy protection . Public statements made by Just For Feet's president, Helen Rockey, indicate

that Just For Feet had intended to file for Chapter 11 protection eight weeks earlier, but decided to

complete a new revolving credit facility first . Nevertheless, the Defendants allowed investors to

continue trading Just For Feet securities, knowing that the common stock would be rendered

worthless in the near term by the Defendants' actions .

7 . At all times relevant to the Class Period, Deloitte served as independent auditors fo r

Just For Feet 's financial statements and issued unqualified opinions stating that they had performed

their duties in accord ance with Generally Accepted Auditing Standards ("GAAS") and that the

financial statements fairly presented the financial position and results of operations of Just for Feet

in accordance with Generally Accepted Accounting P rinciples ("GAAP") . In failing to recognize

and/or repo rt Just For Feet ' s false and fraudulent statements which materially overstated Just For

Feet's sales , profits and income, Deloi tte breached its duty to the shareholders . Deloitte ' s failure to

comply with GAAP and GAAS was knowing, intentional and fraudulent .

JURISDICTION AND VENU E

8 . This Court has jurisdiction of this action pursuant to Section 27 of the Securities

Exchange Act of 1934 (the "Exchange Act"), 15 U .S .C . § 78aa ; 28 U .S .C . §§ 1331 and 1337; and

pursuant to principles of supplemental jurisdiction, 28 U .S .C . § 1367 .

9 . The claims herein arise under Section 10(b) of the Exchange Act, 15 U .S .C . § 78j(b)

and Rule 10b-5, 17 C.F .R. 240.10b-5, promulgated thereunder by the Securities and Exchange

Commission (the "SEC"); Section 18 of the Exchange Act, 15 U .S .C. § 78r; Section 20(a) of the

Exchange Act, 15 U.S .C . § 78t(a) ; and state law fraud and professional negligence .

10. Venue is proper in this District pursuant to Section 27 ofthe Exchange Act, 15 U.S .C .

§ 78aa, and 28 U.S .C. § 1391(b) . Many of the acts comprising the violations of law complained of

herein, including devising and carrying out of the wrongful financial reporting schemes, and the

preparation and dissemination to the investing public of materially false and misleading financial

statements, reports to stockholders, press releases, and other information, occurred in this District .

At all relevant times, the executive offices of Just For Feet were located at 7400 Cahaba Valley

Road, Birmingham, Alabama 35242, and the majority ofits officers and directors who are defendants

herein resided in this District . At all relevant times, Deloitte maintained an office in this District .

In addition, each of the Defendants transacted business in this District .

11 . In connection with the acts, conduct, combination and course of conduct alleged in

this Complaint, the Defendants directly and indirectly used the means and instrumentalities o f

4

interstate commerce, including the United States mails and interstate telephone communications, an d

the facilities of the national securities markets .

THE PARTIES

Plaintiffs

12 . Lead Plaintiff STATE OF WISCONSIN INVESTMENT BOARD ("SWIB") acts

in a fiduciary capacity as investment manager for the Wisconsin Public Employee Retirement

System. During the Class Period, SWIB purchased 4,163,000 shares of Just For Feet common stock

for an aggregate amount of $53,353,413 .04 and retained 2,391,000 shares of Just For Feet common

stock through the end of the Class Period .

13 . Lead Plaintiff KENNETH D. BUSH is an individual who purchased 23,200 shares

of Just For Feet common stock during the Class Period for an aggregate amount of $304,382, an d

retained all of those shares through the end of the Class Period.

14. Lead Plaintiff EDWARD E . EUBANK, JR. is an individual who purchased 15,67 8

shares of Just For Feet common stock during the Class Period for an aggregate amount of $179,719 ,

and retained 8,900 of those shares through the end of the Class Period .

15. Lead Plaintiff JOHN MICHAEL is an individual who purchased 116,800 shares of

Just For Feet common stock during the Class Period for an aggregate amount of $700,261, and

retained 20,200 shares of Just For Feet common stock through the end of the Class Period .

Defendants

16. Defendant HAROLD RUTTENBERG ("Ruttenberg"), who resides in this District ,

was at all times relevant to the Class Period, Chairman of the Board , President, Chief Executive

Officer, and/or a Director of the Company . According to the Company ' s 1999 proxy statement, as

of April 12, 1999 , Ruttenberg beneficially owned as much as 5,439,730 shares of Just For Feet

stock, or approximately 17 .4% of the total then outstanding shares of the Company . Furthermore,

during the Class Period, while in possession of material, adverse inside information and perpetrating

a fraud, Ruttenberg sold 413,850 shares of Just For Feet common stock on or about May 8, 1998,

and realized proceeds of approximately $5,897,362 .50, as described more fully below. Ruttenberg

signed each of the Company's Reports on Form 10-K and Form 10-Q, Annual Reports, Proxy

Statements and Letters to Shareholders issued during the Class Period, with the exception of the

Report on Form 10-Q that was filed with the SEC on September 27, 1999 . At all relevant times,

Ruttenberg was aware of, and actively and willingly participated in, the fraud at Just For Feet .

17. Defendant ERIC L. TYRA ("Tyra"), who resides in this District, is a former partner

of Deloitte who, at all times relevant to the Class Period, was the Executive Vice President, Chief

Financial Officer and a director of the Company . According to the Company's 1999 proxy

statement, as of April 12, 1999, Tyra beneficially owned as much as 92,000 shares of Just For Feet

stock . Tyra signed each of the Company's Reports on Form 10-K and the letters to shareholders

issued in connection with the Company's Annual Reports for the fiscal years ended January 1998

and January 1999, as well as each of the Company's Reports on Form 10-Q that were issued during

the Class Period, with the exception of the Report on Form 10-Q that was issued on September 27,

1999. At all relevant times, Tyra was aware of, and actively and willingly participated in, the fraud

at Just For Feet.

18 . Defendant PETER BERMAN ("Berman"), who resides in this District, was Just For

Feet's Controller and a financial officer of the Company at all times relevant to the Class Period .

Berman, along with Tyra and Ruttenberg, participated in the fraudulent reporting of Just For Feet's

financial condition . Bermanwas responsible for all accounting and data processing activities by Just

For Feet .

19 . Defendant COOPER EVANS ("Evans"), who resides in this District , was Just For

Feet's Director of Financial Reporting at all times relevant to the Class Pe riod. Evans, along with

Berman, Tyra and Ruttenberg , participated in the fraudulent report ing of Just For Feet 's financial

condition . Evans was responsible for all financial data repo rted to third parties .

20. Defendant PATRICK LLOYD ("Lloyd"), who resides in this District, was

Accounting M anager of Just For Feet at all times relev ant to the Class Period. Lloyd, along with

Berman, Tyra and Ruttenberg , part icipated in the fraudulent report ing of Just For Feet's financial

condition. Lloyd was responsible for all financial data reported to third part ies.

21 . Defendant MICHAEL LAZARUS ("Lazarus") was a director and a member of the

Audit Committee of the Board of Directors of Just For Feet during the Class Period . As a director,

Lazarus was responsible for supervision of the entire business and affairs of the Company and the

activities of the individual defendant officers named herein as defendants, and for supervision of the

Company' s financial reporting . Lazarus was a member of the Audit Committee and as such ha d

special responsibilities for recommending the Company' s outside auditors, reviewing with those

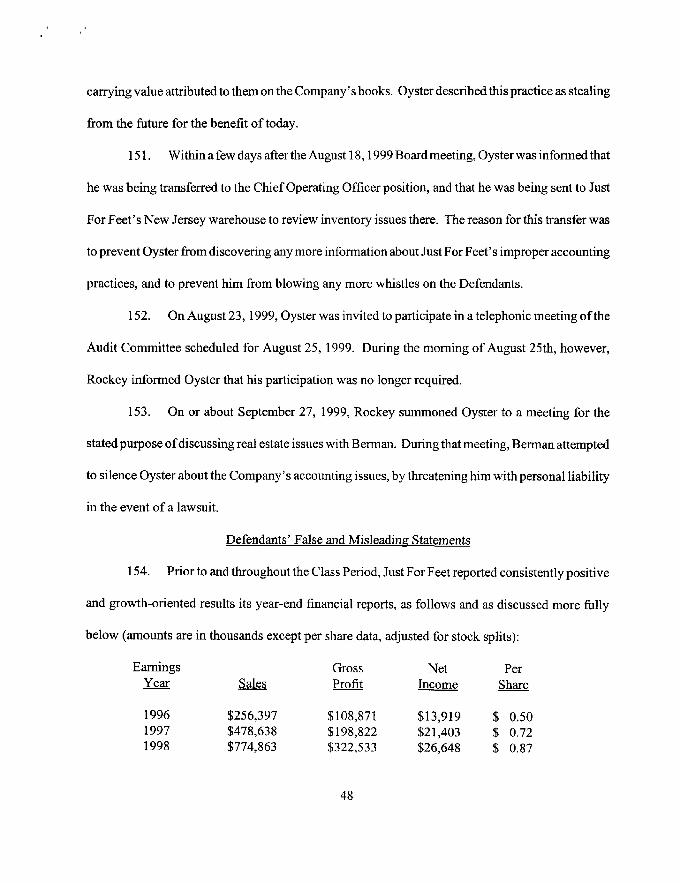

auditors the scope and results of Company audits, monitoring the Company's financial and control

procedures, monitoring non-audit services of the auditors, familiarizing himself with the financial

reports and accounting issues facing Just For Feet, and reviewing all conflicts of interest. Lazarus

signed the Reports on Form 10-K filed with the SEC for fiscal years ended January 1998 and Januar y

7

1999. By no later than July 3, 1999, Lazarus was aware of the fraud at Just For Feet but took no

action to remedy it or warn the investing public about the fraud .

22. Defendant RANDALL L . HAINES ("Haines"), who resides in this District, was a

director and a member of the Audit Committee of the Board of Directors of Just For Feet during the

Class Period. Haines was also the president of Compass Bank-Birmingham, one of Just For Feet's

principal lenders, during the Class Period . As president of Compass Bank, Haines helped to arrange

the loan syndicate which was the major source of Just For Feet's credit ; arranged for Compass to

serve as documentation agent for the syndicate ; and arranged for Compass to serve as an issuing

lender for the Company's letters of credit backed by the loan syndicate . As a director of Just For

Feet, Haines was responsible for supervision of the entire business and affairs of the Company and

the activities of the individual defendant officers named herein as defendants, and for supervision

of the Company' s financial reporting . Haines was a member of the Audit Committee and as suc h

had special responsibilities for recommending the Company ' s outside auditors, reviewing with those

auditors the scope and results of Company audits, monitoring the Company's financial and control

procedures, monitoring non-audit services of the auditors, familiarizing himself with the financial

reports and accounting issues facing Just For Feet, and reviewing all conflicts of interest. Haines

signed the Reports on Form 10-K filed with the SEC for the fiscal years ended January 1998 and

January 1999 . By no later than August 18, 1999, Haines was aware of the fraud at Just For Feet but

took no action to remedy it or warn the investing public about the fraud . Instead, Haines kept quiet

about the fraud, allowing the Company to successfully complete a private offering in the spring of

1999 of approximately $200 million of senior subordinated notes, which directly benefitted Compass

Bank (of which Haines was president) because the proceeds of the offering were used to repay

outstanding loans from Compass Bank to Just For Feet .

23. Defendant HELEN ROCKEY ("Rockey"), who resides in this District, was

appointed president of Just For Feet in March 1999, and was elected a director of the Company on

June 1, 1999. She was responsible for supervision of the entire business and affairs of the Company

and the activities of the individual defendant officers named herein as defendants, and for

supervision of the Company's financial reporting . By no later than June 1999, Rockey was aware

of the fraud at Just for Feet but took no action to remedy it or to warn the investing public . Instead,

as alleged herein, she took steps to cover up the fraud . Rockey signed the Company's Report on

Form 10-Q filed with the SEC for the three-month period ended July 31, 1999 .

24. Defendant SCOTT C. WYNNE ("Wynne"), was an officer and employee of th e

Company throughout the Class Period . Since 1990, Wynne has served as Operations Manager of

the Company, and has been responsible for inventory control, distribution, management information

systems, and traffic . Wynne was elected Vice President - Store Operations in 1994, corporate

Secretary in 1995, and Vice President - Operations in February 1997 . At all relevant times, Wynne

knew about and actively directed and participated in the fraud at Just For Feet, including the

improper manipulation and falsification of inventory and accounting data .

25 . Defendant DON-ALLEN RUTTENBERG ("Don-Allen"), an officer and employee

of the Company for the past twelve years, is the son of Defendant Harold Ruttenberg, a member of

the Ruttenberg family controlling group of stockholders, a Vice President of the Company, and the

holder of 129,818 shares of the Company's common stock as of April 12, 1999 . From February

9

1997 through February 1999, Don-Allen was the Company's Executive Vice President ofNew Store

Development . At all relevant times, Don-Allen was aware of, and actively participated in, the fraud

at Just For Feet.

26. Defendant ADAM GILBURNE ("Gilburne") has served as Executive Vice President

of the Company and President-Superstore Division since August 1997 . Gilburne was aware of, and

actively participated in, the inventory accounting frauds that were occurring at Just For Feet.

27. Defendant DELOITTE is an international accounting firm with offices located in

various cities throughout the world, including a location at 417 Twentieth Street North, Suite 10000 ,

Birmingham, Alabama . At all times relevant to the Class Period, Deloitte's Birmingham office

served as the auditors of Just For Feet . Upon information and belief, Just For Feet was one of the

largest clients of Deloitte's Birmingham office, accounting for a substantial percentage of that

office's revenues in 1998 and 1999 .

28. As Just For Feet's independent outside auditors, Deloitte assisted in the preparation

of Just For Feet's annual and quarterly financial statements, reviewed those fin ancial statements and

the text that accompanied them in the Company' s SEC filings, and audited the annual financial

statements and certified that they were prepared in compli ance with GAAP . Deloitte was also

responsible for, among other things , examining Just For Feet 's system of inte rnal controls to identify

any material weaknesses or reportable conditions which might impact the accuracy or reliability of

the Company ' s financial statements . Deloi tte was required to perform its audit se rvices according

to GAAS, which included Statements on Auditing St andards ("SAS") issued by the American

Institute of Certified Public Account ants ("AICPA"), and to issue an unquali fied opinion only if Just

For Feet's financial statements were fairly presented in accord ance with GAAP .

10

29. Deloitte issued unqualified auditors' opinions on the financial statements of Just For

Feet for the fiscal years ended January 1998 and 1999, which were, with Deloitte's knowledge and

approval, included in Just For Feet's Reports on Form 10-K filed with the SEC and Just For Feet's

Annual Reports, all of which were publicly disseminated to members of the Class . In failing to

recognize and/or report the false and fraudulent misrepresentations in Just For Feet's financial

statements, Deloitte breached its duties to the shareholders, and either recklessly or fraudulently

failed to comply with GAAP and GAAS .

30. Defendant STEVEN H. BARRY ("Barry"), who resides in this District, was at al l

times relevant to this Class Period the Managing Partner of Deloitte's Birmingham office and the

audit partner on the Deloitte audit of Just For Feet. As such, Barry knew or should have known

(based, inter alia, on his extensive contacts with Company officers and personnel, his responsibility

under GAAS for the audit evaluation of Just For Feet's internal controls and accounting methods,

and his firm's audits of Just For Feet's financial statements, and his review and supervision related

to those audits) of the material fraudulent misrepresentations in Just For Feet's financial statements .

Barry either recklessly or intentionally failed to comply with GAAS in discharging his duties . Had

he complied with his professional responsibilities, he would have : (1) immediately alerted the

Company's Board of Directors and shareholders that Just For Feet's financial statements were

materially false and misleading due to materially overstated sales, profits, income, accounts

receivable, inventories, equipment, fixed assets, and stockholders' equity, and materially understated

costs and liabilities ; (2) refused to issue an unqualified opinion; and (3) depending upon the Board's

actions, taken appropriate action.

11

31 . Defendant, KAREN BAKER ("Baker"), who resides in this District, was Deloitte's

Senior Manager assigned to the audit of Just For Feet from at least June 1997 through the end of the

Class Period. As Senior Manager for the Deloitte audits, Baker knew or should have known (based,

inter alia, on her extensive contacts with Company officers and personnel, her responsibility under

GAAS for the audit evaluation of Just For Feet's internal controls and accounting methods, her

review and supervision related to the audit of Just for Feet's financial statements, and her audit,

examination and testing of Just For Feet's financial statements) of the material fraudulent

misrepresentations in Just For Feet's financial statements . Baker either recklessly or intentionally

failed to comply with GAAS in discharging her duties . Had she complied with her professional

responsibilities, she would have : (1) immediately alerted the Company's Board of Directors and

shareholders that Just For Feet's financial statements were materially false and misleading due to

materially overstated sales, profits, income, accounts receivable, inventories, equipment, fixed assets,

and stockholders' equity, and materially understated costs and liabilities ; (2) refused to issue an

unqualified opinion; and (3) depending on the Board's actions, taken appropriate action .

32. Defendants Ruttenberg, Tyra, Wynne and Don-Allen, by virtue of their stoc k

ownership and/or positions of knowledge, control and influence, were controlling persons (or

members of a control group) of Just For Feet, within the meaning of Section 20(a) of the Exchange

Act ("Control Person Defendants") . Because of their positions of control and authority, they were

able to review and control the contents and cause the issuance of the various financial reports,

financial statements, press releases and SEC filings of the Company, and had the power and authority

to cause Just for Feet to engage in the conduct herein described . These Control Person Defendants

had a duty to promptly disseminate accurate and truthful information with respect to the Company' s

12

operations, financial condition, earnings and profitability and future business prospects so that the

market related to Just For Feet would be based on timely, truthful and accurate information .

Non-Defendant Co-Conspirators

33. DAVID HERSKOVITS ("Herskovits"), is Deloitte's retail partner expert, and wa s

fully aware of the fraud that was taking place at Just For Feet but did nothing to alert the Board o f

Directors or the shareholders of the fraud .

34. JAY SWARTZ ("Swartz") is a partner in the Atlanta law firm of Smith, Gambrell

& Russell, LLP, who represented Just For Feet in securities matters and was fully aware of the

accounting fraud that was taking place at Just For Feet . He continued to supply legal counsel on

securities matters to Just For Feet, including the drafting of portions of the Company's Reports on

Form 10-K for the fiscal years ended January 31, 1998 and January 30, 1999, even though he knew

of the fraud .

35. JOHN A. BERG ("Berg") was elected a director of the Company on June 1, 1999 .

As a director, Berg was responsible for supervision ofthe entire business and affairs ofthe Company

and the activities of the individual defendant officers named herein as defend ants, and for

superv ision of the Company' s financial repo rt ing . Berg took no action to remedy the fraud at Just

For Feet or to warn the investing public about the fraud . Berg signed the Report on Form 10-Q filed

with the SEC for the three -month period ended July 31, 1999 .

36 . ROBERT WABLER ("Wabler") was the Chief Financial Officer of Just For Feet

until April 1997 . During his employment, Wabler was aware of, and actively participated in, the

fraud at Just For Feet .

13

PLAINTIFFS ' CLASS ALLEGATION S

The Class

37. Plaintiffs bring this action as a class action pursuant to Rule 23 of the Federal Rules

of Civil Procedure on behalf of all persons and entities who purchased Just For Feet common stock

during the Class Period and who suffered damages as a result of their purchases (the "Class") .

Excluded from the Class are ( 1) Defendants , (2) members of the families of Defendants , (3) the

subsidiaries or affiliates of any Defendant, (4) any person or entity who is a shareholder , partner,

officer, director, employee or controlling person of any Defendant, (5) any entity in which any

Defendant has a controlling interest, and (6) the legal representatives , heirs, successors or assigns

of any such excluded person .

38. The members of the Class are so numerous that joinder of all members i s

impracticable. As of September 15, 1999 Just For Feet had approximately 31,210,980 shares of

common stock outstanding. Because of the common practice of publicly traded stock being held in

"street name," it is likely that the number of beneficial owners and purchasers of Just For Feet stock

during the Class Period is in the thousands . Throughout the Class Period, the stock was actively

traded on NASDAQ's National Market System, an efficient and open market, under the symbol

"FEET . "

39. Plaintiffs' claims are typical of the claims of the members of the Class . Plaintiffs will

fairly and adequately protect the interest of the members of the Class and have retained counsel

competent and experienced in class and securities litigation. Plaintiffs have no interests that are

adverse or antagonistic to the Class .

14

40. A class action is superior to other available methods for the fair and efficien t

adjudication of this controversy. Since the damages suffered by many individual Class members

maybe relatively small, the expense and burden of individual litigation makes it virtually impossibl e

for the Class members individually to seek redress for the wrongful conduct alleged .

41 . Common questions of law and fact exist as to all members of the Class, and

predominate over any questions affecting solely individual members of the Class. Among the

questions of law and fact common to the Class are :

(a) Whether the federal securities laws and/ or state law were violated by Defendants' acts

as alleged herein;

(b) Whether the documents, releases, and statements disseminated to the investing publi c

and the shareholders during the Class Period omitted and/or misrepresented material facts about th e

business affairs, financial condition and future prospects of Just For Feet as particularized herein ;

(c) Whether Defendants acted willfully or recklessly in omitting to state and/o r

misrepresenting material facts about the financial condition, profitability and future prospects ofJust

For Feet;

(d) Whether the market prices of the Just For Feet common stock during the Class Perio d

were artificially inflated due to the nondisclosures an d/or misrepresentations complained of herein;

and

(e) Whether the members of the Class have sustained damages, and, if so, what is th e

proper measure thereof.

42. Plaintiffs know ofno difficulty which will be encountered in the management of thi s

litigation which would preclude its maintenance as a class action.

15

43 . The names and addresses of the record owners of the shares of Just For Feet commo n

stock purchased during the Class Period are available from the Company's transfer agent(s) . Notice

can be provided to such record owners by first class mail.

FACTS

44. In order to materially overstate the Company's financial results and thereby

encourage investors to purchase Just For Feet securities, Defendants employed a number o f

accounting man ipulations , including :

a. creating fraudulent billing and kickback schemes from Just For Feet's advertising

agency in order to increase revenue ;

b. creating false billings and receivables for fixed assets donated by shoe manufacturers ;

c . creating false vendor billings and receivables ;

d. failing to write off bad debt;

C . failing to book required reserves for sales promotions and barter transactions ;

f. understating its cost of sales through the improper use of acquisition accounting ;

g . improperly capitalizing expenses that should have been reported as current operatin g

expenses ;

h. overstating ending inventory by not accounting or reserving for obsolete or missing

inventory, and by arbitrarily writing up the costs of inventory when it was transferred

between stores and divisions ;

i . improperly accounting for leaseholds in order to increase earnings and decrease

liabilities ; and

j . knowingly maintaining a woefully inadequate accounting system .

16

45 . The Company' s scheme to falsify its financial statements was concocted and initiated

primarily by Ruttenberg and Wynne, and was implemented and facilitated by the Company's internal

financial and accounting staff, and its outside auditors, Deloitte, Baker and Barry .

46. The fraud at Just For Feet was well known among the Company 's management even

before the Class Period began . On March 6, 1997, Just For Feet's controller, Anthony Lones

("Lones") met with the Company's outside securities counsel, Swartz, and presented Swartz with

a list of accounting irregularities and problems at Just For Feet which amounted to about $5 million

in improper accounting entries or, as they were referred to internally at Just For Feet, "bads ." Lones

had similar conversations with Barry and Baker of Deloitte in early 1997 . In fact, Lones had a pre-

existing relationship with Barry because they had worked together at Deloitte for several years, and

Lones repeatedly informed Barry and Deloitte of his concerns about Just For Feet's accounting

methods and internal controls throughout the Class Period .

47 . Tyra joined Just For Feet as its Chief Financial Officer in May 1997, and on June 27,

1997, he met with Lones and Evans for the purpose of being briefed about open accounting and

internal control issues at Just For Feet . During that meeting, Tyra was informed of accounting

irregularities at the Company, including inaccurate and false accounting for Just For Feet's accounts

receivable, inventory capitalization and inventory discount accounting methods . In this meeting,

Tyra was informed, among other things, that Just For Feet overstated its revenue, and/or understate d

its expenses by falsely accruing revenue and accounts receivable for : (a) fictitious rebates from

vendors providing advertising services ; (b) various shoe vendors for sharing of expenses for store

fixtures and opening costs ; (c) cooperative advertising monies from its vendors ; and (d) bulk sales

occurring after the end of fiscal periods which were improperly allocated out to stores for those

17

periods to provide the illusion that those stores' sales had increased since the prior year . Rather than

rectifying these improper practices, Tyra (who had been granted numerous options to purchase Just

For Feet stock on May 1, 1997) became an active participant in the fraud at Just For Feet .

48 . Likewise, shortly after Rockey joined Just For Feet as its President in March 1999,

she was specifically informed of a number of fraudulent and improper accounting practices at Just

For Feet . For example on July 7, 1999, Berman wrote a "confidential" memo to Rockey in whic h

he recommended that the Company make a number of accounting adjustments if they had "the

opportunity to clean up our balance sheet at the end of [the quarter ended July 31, 1999] and not

carry forward problems into the future ." Many of those proposed adjustments related directly to

improper accounting practices alleged in this Complaint, including the need to establish reserves for

uncollectible receivables for co-op advertising and CheckCare claims, and the need to accrue an

obsolescence reserve for future special sales . Berman went on to say that the issues identified in his

memo had "in the past . . . been treated rather aggressively at [Just For Feet]" and that "[i]f we are

trying to do the right thing for the business in the future, we need to discuss taking our punishment

today ." Rockey did nothing to correct these problems and, as discussed below, took action to cover

them up instead .

Fraudulent Rebates from Advertising Agency For Sales Promotion s

49. At the June 27, 1997 meeting among Tyra, Evans and Lones, Tyra was informed that

Just For Feet had engaged in a scheme to inflate its revenues and "pay down" bogus receivables by

having its advertising agency Rogers Advertising ("Rogers") substantially overcharge for production

of commercials . Rogers, where Ruttenberg's daughter is employed, would then kick back or credit

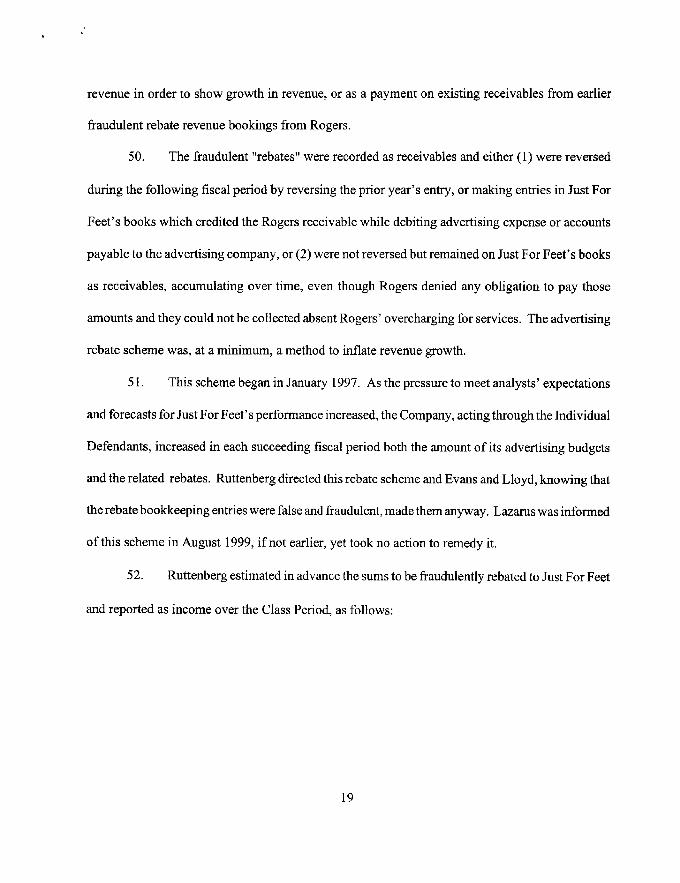

most of the overpayment to Just For Feet, and Just For Feet would book that payment as rebat e

18

revenue in order to show growth in revenue , or as a payment on existing receivables from earlier

fraudulent rebate revenue bookings from Rogers .

50. The fraudulent "rebates " were recorded as receivables and either ( 1) were reversed

during the following fiscal pe riod by reversing the prior year 's entry, or making ent ries in Just For

Feet ' s books which credited the Rogers receivable while debiting advert ising expense or accounts

payable to the advertising company, or (2) were not reversed but remained on Just For Feet 's books

as receivables , accumulating over time, even though Rogers denied any obligation to pay those

amounts and they could not be collected absent Rogers' overcharging for se rv ices . The adve rtising

rebate scheme w as, at a minimum , a method to inflate revenue growth.

51 . This scheme began in January 1997 . As the pressure to meet analysts' expectation s

and forecasts for Just For Feet's performance increased, the Company, acting through the Individual

Defendants, increased in each succeeding fiscal period both the amount of its advertising budgets

and the related rebates . Ruttenberg directed this rebate scheme and Evans and Lloyd, knowing that

the rebate bookkeeping entries were false and fraudulent, made them anyway . Lazarus was informed

of this scheme in August 1999, if not earlier, yet took no action to remedy it .

52. Ruttenberg estimated in advance the sums to be fraudulently rebated to Just For Feet

and reported as income over the Class Period, as follows :

19

BILLINGSGROSS

AMOUNT PURPORTE DBY GROSS PROFIT

PURPORTEDLY REBATE TO

YEARROGERS

COMMISSIONSEXPENSES TO RETAINED BY JUST FOR

TO JUSTROGERS

ROGERS FEETFOR FEET

1997 $20,000,000 $3,000,000 $822,000 $2,178,000 $806,000 $1,372,00 0

1998 $30,000,000 $4,500,000 $1,126,000 $3,374,000 $1,104,000 $2,270,00 0

1999 $45,000,000 $6,750,000 $1,543,000 $5,207,000 $1,512,000 $3,695,00 0

2000 $60,000,000 $9,000,000 $2,114,000 $6,886,000 $2,071,000 $4,815,00 0

53 . As time passed , however, the actual "rebates" exceeded these estimates . By August

of 1999, the fraudulent "rebates" from Rogers had grown to approximately $ 7 .5 million. In the

quarter ended July 31, 1999 alone , Just For Feet booked $1 .5 million in "rebates" from Rogers .

54. This scheme and the repo rting implication of these false and misleading accounting

entries in Just For Feet ' s books and records were made known to Tyra, Baker, Barry and Herskovits

by Lones no later th an June 1997, but were allowed to continue throughout the Class Period .

55 . The existence ofthese accounting irregularities was also made known to Swa rtz, Just

For Feet ' s securi ties attorney, by Lones in April of 1997 .

56. On Monday morning, August 16, 1999, when con fronted by Just For Feet employee s

who were unaware of the existence of the rebate scheme, Reed Rogers, the President of Rogers

Advertising, readily admitted that he had been overcharging Just For Feet for advertising . He

admitted that four recent television advertising spots for the first quarter of 1999 should have been

invoiced at about $6,000 per television spot, rather than the $60,000 to $65,000 reflected in the

invoice . He went on to admit that he had been overcharging the company by $250,000 each month

and, when asked why, said that is what Ruttenberg and Gilburne had told him to do . He also added

that the approximately $7.5 million in accounts receivable attributed to it on Just For Feet's books

20

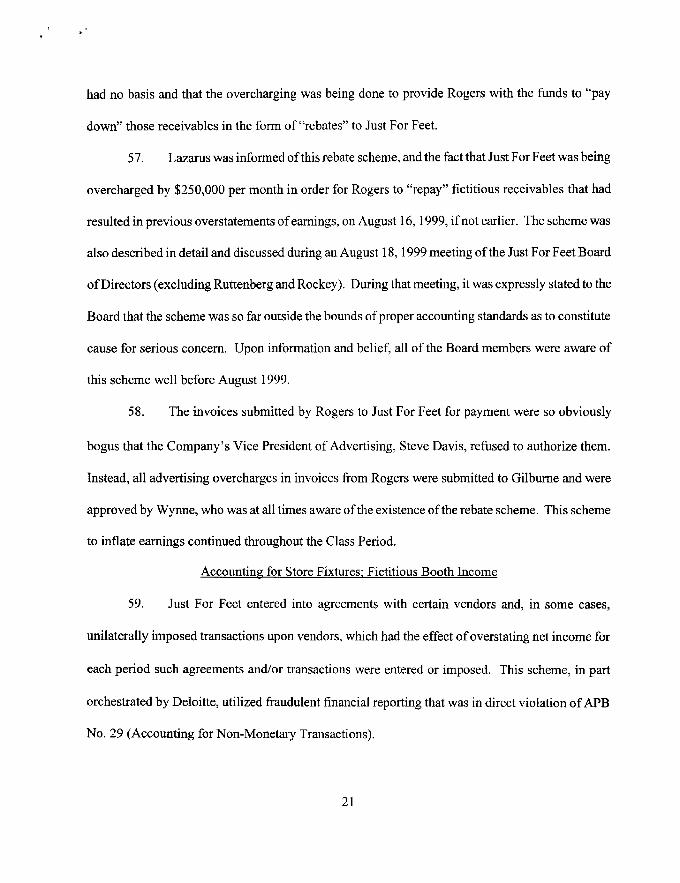

had no basis and that the overcharging was being done to provide Rogers with the funds to "pay

down" those receivables in the form of "rebates" to Just For Feet .

57 . Lazarus was informed of this rebate scheme, and the fact that Just For Feet was being

overcharged by $250,000 per month in order for Rogers to "repay" fictitious receivables that had

resulted in previous overstatements of earnings, on August 16, 1999, if not earlier . The scheme was

also described in detail and discussed during an August 18, 1999 meeting of the Just For Feet Board

of Directors (excluding Ruttenberg and Rockey) . During that meeting, it was expressly stated to the

Board that the scheme was so far outside the bounds of proper accounting standards as to constitute

cause for serious concern. Upon information and belief, all of the Board members were aware of

this scheme well before August 1999 .

58. The invoices submitted by Rogers to Just For Feet for payment were so obviousl y

bogus that the Company's Vice President of Advertising, Steve Davis, refused to authorize them .

Instead, all advertising overcharges in invoices from Rogers were submitted to Gilburne and were

approved by Wynne, who was at all times aware of the existence of the rebate scheme . This scheme

to inflate earnings continued throughout the Class Period .

Accounting for Store Fixtures, Fictitious Booth Incom e

59. Just For Feet entered into agreements with certain vendors and, in some cases,

unilaterally imposed transactions upon vendors, which had the effect of overstating net income for

each period such agreements and/or transactions were entered or imposed . This scheme, in part

orchestrated by Deloitte, utilized fraudulent financial reporting that was in direct violation of APB

No. 29 (Accounting for Non-Monetary Transactions) .

21

60. When Just For Feet opened a new store, shoe manufacturers desiring to exploit new

markets for sales of their products and to receive the advertising benefits associated with a grand

opening of a new retail outlet would donate creative and expensive displays, or booths, for their

products in an attempt to maximize sales of their products . Some manufacturers treat their booths

as their property which is placed at the retailer's site for the retailer's use in selling the

manufacturer's products, rather than as an outright gift . Some manufacturers' displays, like

Timberland's, cost as much as $30,000.

61 . In 1996, Just For Feet's then CFO, Wabler, with the knowledge of (and acting upon

the advice of) Deloitte, instituted an arrangement with shoe manufacturers by means of which Just

For Feet was to treat these promotional donations as income based upon a series of fictitious and

misleading "exchanges for value," which were nothing more than fraudulent book entries .

62 . Rather than have its vendors donate the fixtures or booths displaying their products

for use in new stores , which is the st andard industry practice, Just For Feet purpo rted to "buy" the

booths ( shelving, racks , partitions , lighting, displays , etc .) from the vendors, capitalize the "purchase

p rice " as an asset, and then "depreciate " the asset over time . Then , Just For Feet would require that

the vendors remit the purchase price back to Just For Feet in the form of credits for co-op adve rtising

(adve rtising by Just For Feet that also incorporates a vendor's products, and for which the vendor

agrees to share the advert ising cost) . Just For Feet immediately booked these co-op advertising

monies or credits as revenue , even though they had not been "earned " by the placement of co-op

advert isements .

22

63. Moreover, with the assist ance of Rogers, Just For Feet also inflated the cost of the

co-op advertising , to "earn" more co-op dollars and credits from the vendors, separate and apart from

the booth accounting scheme .

64. The booth accounting scheme allowed Just For Feet to recognize as income the valu e

of the booths in the current period, but defer the equal amount of cost (since it was a wash sale) to

subsequent periods (because the costs were capitalized rather than expensed), thereby inflating net

income. This allowed the Company to show income in the current quarter, but also caused the

Company to incur unnecessary tax liabilities . No rational business person would use such an

accounting scheme, which caused it to incur unnecessary income tax liability, unless it was trying

to boost reported revenues and deceive the investing public .

65 . In some cases, Just For Feet booked the value of shoe manufacturer' booths as assets

(including booths the manufacturers had not intended to donate), and booked co-op advertising

income from those manufacturers, without even consulting them . In an after-the-fact attempt to

justify some of these entries, in the summer of 1999, Don-Allen met separately with representatives

of Reebok and Timberland, two of the vendors who had provided booths at Just For Feet's new store

grand openings . Don-Allen told each of them that Just For Feet had accrued booth receivables on

its books and that Just For Feet wanted co-op advertising credits from their respective companies .

Reebok and Timberland refused Don-Allen's request . The representatives of Timberland (whose

auditing firm is Deloitte) replied that they would not be a part of Just For Feet's booth accounting

scheme .

66. More troubling still, during the course of Just For Feet's bankruptcy case at least one

other shoe manufacturer (Reebok) has disputed Just For Feet's title to the manufacturer's booths ,

23

claiming that the booths were simply on loan to Just For Feet and that Just For Feet had no right to

record them as assets on the Company's books .

67. As of January 30, 1999, Don-Allen needed more than $40 million in credits from

manufacturers in order to clear-up outstanding accounting issues from the fiscal years ended January

1997, 1998 and 1999, including issues relating to booth accounting and co-op advertising . Although

many of those "receivables" were in dispute, Just For Feet did not book any reserves.

68. During a telephone conversation initiated by Don-Allen following one of the

meetings described above, Wynne explained the booth accounting scheme and remarked that

Deloitte had suggested that Just For Feet employ it .

69 . Just For Feet opened or converted approximately twenty-five (25) new superstore s

in fiscal year ended January 1998, and approximately fifty (50) new or converted superstores in

fiscal year ended January 1999 . Just For Feet opened or converted approximately twenty (20) new

specialty stores in fiscal year ended January 1998, and approximately fifty (50) new or converted

speciality stores in fiscal year ended January 1999 .

70. For fiscal year ended January 1998, Just For Feet recognized approximately $20

million in booth income which it never received . Absent this accounting scheme, Just For Feet' s

repo rted pre-tax income of $34 .2 million for that fiscal year would have been reduced by 60% to

about $14.2 million . Absent the rest of Just For Feet's accounting manipulations, if its financial

statements had been prepared in accordance with GAAP , Just For Feet would have reported a

substantial loss for the year.

24

71 . For fiscal year ended January 1999, Just For Feet recognized approximately $2 2

million in booth income which it never received. Without the fraudulent booth income, Just Fo r

Feet's reported pre-tax income of $43 .3 million for that fiscal year would have been reduced b y

about 50% to about $21 .3 million . Absent the rest of Just For Feet 's accounting manipulations, if

its financial statements had been prepared in accordance with GAAP, Just For Feet would have

reported a substantial loss for the year .

72 . For the quarter ended July 31, 1999, Just For Feet recognized approximately $5 . 9

million in fraudulent booth income . Without the fraudulent booth income, Just for Feet's reporte d

pre-tax loss of approximately $42 million for that quarter would have been increased by about 14 %

to a loss of about $48 million .

73. The fraudulent accounting entries relating to the boothaccounting scheme were made

by, or directed by, Tyra, Berman, Lloyd and Evans . Barry, Baker and Deloitte were informed of the

existence of this scheme by members of Just For Feet's finance department, including Lones and

Evans, in January 1997, and they were well aware of the magnitude of the amounts involved . The

scheme continued to operate at levels that materially distorted and misstated operating results

throughout the Class Period .

74. In June 1999, Rockey was apprised of the nature and magnitude of the boot h

accounting issues and did nothing to remedy the problem .

75. The Board of Directors of Just For Feet was informed of this booth accountin g

scheme on August 19, 1999, if not earlier, and did nothing to remedy the problem

25

76. On or about August 25, 1999, Rockey instructed employees of Just For Feet not to

speak with the Company's Audit Committee any further about the booth accounting problem or the

magnitude of the problem .

False Billings and Receivable s

77. During the Class Period, Just For Feet's accounts receivable were materially

overstated as a result of billings to vendors that were either wholly fictitious or were not properly

adjusted to provide for uncollectible amounts . In addition to the false advertising rebates and booth

accounting schemes described above, these misleading billings and receivables were, in part, the

result of. (a) bulk sales of outdated inventory to liquidation companies ; (b) cost offsets resulting

from Reebok mis-shipments; (c) the existence of an old uncollectible credit receivable from KPR

Sports which dated back to 1995 but had not been written off; (d) a $58,736 .73 credit receivable

from GSV, Inc . of Atlanta, Georgia from which Just For Feet had purchased Store # 7 in 1994 ; and

(e) Just For Feet's improper accounting for co-op advertising . These false billings and receivables

were discussed by Lones, Tyra and Cooper on June 27, 1997 .

78 . During the fiscal years ended January 1997 and 1998, Just For Feet shipped out-dated

shoe inventory to ELF, a liquidation company . By agreement, ELF was to pay Just For Feet $6 .00

per pair of shoes . In 1997, however, Just For Feet began to book the sale and receivable from ELF

at $8 .00 per pair instead of $6 .00, even though ELF had not agreed to the price increase . These

arbitrary and uncollectible increases by Just For Feet were made for the sole purpose of increasing

sales and receivables on the Company's books, and resulted in the addition of $65,000 in unfounded

and fraudulent receivables and revenue on Just For Feet's financial statements . In addition, as of

January 31, 1997 and July 31, 1997, Just For Feet had booked receivables for shoes that were no t

26

even shipped to ELF until after those dates, in violation of Financial Accounting Standards ("FAS")

Statement No. 48 (Revenue Recognition) . These issues were discussed among Lones, Cooper and

Tyra on June 26, 1997, and were made known to Deloitte during 1997 .

79. Just for Feet booked false and inflated credits for merchandise that was returned to

vendors ("RTVs") . For example, Just For Feet would accept trade-ins of used shoes from customers,

which it claimed would be donated to charity . Instead of donating all of the used shoes to charity,

Just For Feet would clean some of them up and return them to the vendors in exchange for credits .

This scheme was concocted and directed by Wynne . At times, Just For Feet booked credits for as

much as $10,000 or $100,000 per pair of returned shoes . In all, Just For Feet had over booked about

$900,000 in vendor credits by July 31, 1997 . When Deloitte looked at the issue in June 1999, it

found that for the fourth quarter of 1998 and the first quarter of 1999, approximately $600,000 of

Just For Feet's RTVs (a full one-third to one-half of all its RTVs) were in dispute and lacked

supporting authorization numbers .

80 . Just For Feet improperly recognized sales revenues for merchandise that was given

away pursuant to the Company's giveaway promotions . For example, Just For Feet offered a

promotion whereby a customer would receive a free tote bag with the purchase of shoes . Just For

Feet accounted for each giveaway as a sale, booking sales revenue equal to the arbitrary sales value

of each tote bag given away in order to show revenue growth, and to fraudulently increase store sales

figures and comparable store sales growth rates .

81 . Just For Feet booked inflated and unrealistic estimates of vendor receivables,

including receivables relating to co-op advertising (whereby Just For Feet and vendors would share

joint advertising costs), at year-end 1997 and throughout the Class Period . These estimates of co-op

27

receivables, which were supplied to the Company's accounts receivable department by Gilburne,

lacked both economic substance and any supporting documentation, such as any agreements with

the advertising companies or vendors . Moreover, no one at Just For Feet or Deloitte made any effort

then or in subsequent periods to compare the Company's actual receipts with the estimated

receivables, in violation of GAAS (including Statement on Auditing Standards No . 67) .

82 . Any discussions with vendors who were included in the receivables claimed by Just

For Feet were conducted after the making of the accounting entries, if at all, and vendors frequently

rejected Just For Feet's proposed receivables as incorrect and/or improper .

83. The false entries to Just For Feet's accounting journals were made by Evans and

Lloyd at the direction of Tyra, based upon estimates made by Gilburne and Don-Allen . Upon

information and belief, Deloitte failed to pursue and obtain confirmations for these entries .

84 . These false vendor billings and receivables were known to Defendants throughout

the Class Period .

Failure To Write-OffBad Debt

85. Just For Feet also understated operating expenses and overstated accounts receivable

by at least $500,000 relating to uncollectible amounts from CheckCare, its check validation vendor.

86. In 1997, Ruttenberg, Wynne, Tyra, Gilburne, Barry, Baker, Herskovits and Deloitte

were aware that Just For Feet was faced with the prospect of having to record bad debt expense

approximating $1 .2 million as a result of having failed to follow the procedures mandated by Just

For Feet's agreement with CheckCare Systems when accepting customer checks as payment for

merchandise sold at the Company's stores .

28

87. CheckCare Systems' guarantee of customer checks could only be invoked if Just For

Feet and its sales personnel followed and documented certain carefully described procedures, such

as customer presentment of a valid state driver's license and telephone number .

88 . As a result of Just For Feet's failure to adhere to the CheckCare procedures, in June

1997, the Company was faced with the prospect of having to book approximately $1 .2 million in

losses for which it had established no reserves, contrary to FAS 5 (Accounting for Contingencies) .

On June 27, 1997, Lones discussed the prospects for having to book these losses with Tyra and

Evans in Tyra's offices at Just For Feet's corporate headquarters in Birmingham, Alabama.

89. Additionally, Lones discussed the existence of the $1 .2 million in prospective losses

stemming from Just For Feet's failure to follow the CheckCare procedures with the Company's in-

house and outside counsel, including Swartz, as early as March 6, 1997 . Just For Feet's counsel

advised that the Company did not have a likelihood of recovering these amounts from CheckCare .

90. During the Summer of 1997, prior to the close of Just For Feet's second quarter

ending July 31, 1997, Just For Feet wrote off approximately one-half of the $1 .2 million of

CheckCare losses . However, following a negative newspaper article, Tyra directed Lones and Evans

to cease all write-offs of bad debt losses for the stated reason that Just For Feet's earnings reports

had been negatively impacted . The CheckCare receivables which the Company's management

considered to be uncollectible approximated $600,000 on July 7, 1999 . The failure to take the

balance of the write-offs violated GAAP's requirements with respect to the timing and recognition

of losses . The effect of the write-off of these receivables as bad debt were known to Deloitte,

Ruttenberg, Baker, Tyra, Wynne, Evans and Barry, all of whom acquiesced in Just For Feet's efforts

to protect earnings by continuing to keep the remaining bad debts on the books at full value .

29

91 . During the quarter ended October 31, 1997, Just For Feet reversed a sales tax payment

in the amount of $60,000 relating to the CheckCare bad debt losses, adding $60,000 back to income,

even though the bad debt loss had not yet been written off. This reversal, which violated GAAP, was

made against the express advice of Lones .

Failure To Book Required Reserves For Sales Promotions

92. During the last weekend in April 1999, Just For Feet, which was desperately

attempting to increase its revenues through increased sales, embarked upon a special promotion for

the sale of its goods in its Super Stores Division . Under this program, Just For Feet's Super Stores

Division offered a dollar-for-dollar rebate program for purchases of goods at Just For Feet . For

example, if a purchaser of Just For Feet goods spent $50.00 in a Just For Feet superstore, that

purchaser was entitled to receive a $50 .00 credit on any goods purchased at any Just For Feet store

after June 18, 1999 . The rebate offer was good from June 18, 1999 through December 31, 1999 .

93. Just For Feet realized approximately $20 million from this sales promotion an d

booked that sum during the first quarter of 1999 . Notwithstanding that for every dollar realized as

a result of this sales promotion Just For Feet also incurred a liability after June 18, 1999, only twenty

percent (20%) of the $20 million received from this sales promotion was reserved as a future

liability, in violation of FAS 5 (Accounting for Loss Contingencies) because the redemption rate of

the coupons from this sales promotion was quantifiably in excess of 80% .

94. Additionally, the June 18, 1999 effective date for the rebate was intentionally set to

occur after Just For Feet had reported its first quarter results to the SEC . The effect of this scheme

was to inflate first quarter fiscal 1999 results at the expense of the Company's historically strongest

sales season in July and August (the back-to-school season) .

30

95. On May 25, 1999, the Company's management scheduled telephone conference calls

with securities analysts and other interested parties for the purpose of discussing the financial results

of the Company for the quarter ended April 30, 1999 . The Company was represented in that

conference by Ruttenberg, Tyra and Rockey .

96. In describing the first quarter 1999 Super Stores Division's "dollar-for-dollar" sales

promotion manipulation, Ruttenberg boasted that :

(a) The Company's core business, its Super Stores Division, continued to excee d

management 's expectations ;

(b) The Company's Super Stores Division continued to take market share and was the

most differentiated and best formula for winning business in this competitive

business ;

(c) The Company would continue to invest in the Super Stores concept to ensure that

they would be the most dominant retailer of the future ; and

(d) Industry conditions remained difficult and challenging, but the Super Stores Division

again demonstrated the ability to continue to take market share, as well a s

experienced positive same store sales growth for the twenty-second consecutiv e

quarter.

97 . Following Ruttenberg's presentation, Tyra described Just For Feet's financial result s

as follows :

(a) For the first quarter ended May 1, 1999, sales were approximately $221 million, u p

45 .5% versus the first quarter of last year; and

31

(b) Operating income for the first quarter was $12 .7 million, before interest and taxes,

up 26 .2% over the $10.1 million for the first quarter of last year .

Tyra never disclosed the dollar-for-dollar rebate program or the effect that such a program would

have on Just For Feet's future quarters . Nor did Tyra disclose that, if the Company had established

appropriate reserves of 80% rather than 20% of the potential $20 million liability in connection with

the program, the additional $12 million in reserves would have wiped out virtually all of the

quarter's $12 .7 million in operating income .

98. In the question and answer session which followed these presentations, Ms . Dana

Cohen, of Donaldson, Lufkin & Jenrette, asked about the first quarter "buy one get one free"

program and its impact on the first quarter results . Ruttenberg responded that the program was part

of the Company's inventory reduction plan, worked very well, was held for one weekend only and,

while business was very good over that period, the program was not significant and did not

materially impact first quarter results . Unbeknownst to the analysts and stockholders on the call,

these representations were false when made, and Ruttenberg, Tyra and Rockey knew of their falsity .

99. In response to a subsequent question by Mark Freidman of Merrill Lynch, Ruttenberg

stated: (a) Our inventories will be at peak at the end of July for our back-to-school season ; and (b)

We have no plans to be playing around with our back-to-school business . Ruttenberg made these

representations despite his knowledge that the first quarter "dollar-for-dollar," or "buy one get one

free" program would likely hurt the back-to-school season .

100 . The understatement for the Company's first quarter 1999 sales promotion was not the

only instance of failing to properly reserve against income . Just For Feet's hallmark sales promotion

was "Buy at Just For Feet, where the thirteenth pair is free ." In fact, Just For Feet held a registere d

32

trademark for the slogan "Where the 13`h pair is free ." The Company did not, at any time, make any

allowance or reserve for the free thirteenth pair of shoes, despite claiming to have 2 .4 million

families enrolled in the program. Nor did the Company establish reserves for the redemption of gift

certificates or coupons offering discounts to customers in connection with other sales promotions .

This failure to establish reserves violated FAS 5 .

101 . The Company's failure to book appropriate reserves for gift certificates, promotions

and coupons was known to Defendants throughout the Class Period, and at the very least was

disclosed to the Board of Directors in August 1999 .

Failure To Book Required Reserves For Barter Transaction s

102 . Just For Feet also failed to book reserves or impairments relating to its "sales" to

barter exchanges . From time to time during the Class Period, Just For Feet "sold" its aged inventory

to "barter groups" in return for credits for an equivalent value of services to be rendered in the future

by members of the barter group. Just For Feet booked the value of the barter group receivable at the

actual original cost of the merchandise, plus 14%. During the Class Period, Just For Feet booked

barter group receivables of at least $5 million .

103 . Because of the limited ability to use the barter dollars, and because services obtained

with barter dollars were at full retail price, the services to be received by Just For Feet were worth

substantially less than the value booked by Just For Feet for the barter receivable or asset . In fact,

Just For Feet used very few of its barter credits, because it found that it could negotiate better prices

and terms by paying for services in cash rather than barter credits . These facts were commonly

known to the Company's senior management, and were specifically disclosed to the Board of

Directors in August 1999, if not earlier .

33

104 . Whenever the Company and its senior management needed to show an increase in

gross profit, they dumped some of the Company' s aged and essentially worthless inventory off to

the barter groups and booked the original merchandise costs, which included the 14% inventory cos t

capitalization, at full value as a viable receivable .

Misuse of Acquisition Accounting

105 . In June of 1998, Just For Feet announced its acquisition of Sneaker Stadium .

Ruttenberg , Tyra and Berm an, with the active assist ance of Wynne, Evans and Lloyd, embarked o n

a scheme to inflate Just For Feet's earnings by the manipulation of the value of Sneaker Stadium

inventory .

106 . On the date of the acquisition of Sneaker Stadium, Tyra and Berman, with the activ e

assistance of Wynne, Evans and Lloyd, established an inventory reserve of $10,583,897 against an

inventory balance of $46,973,783, thus reducing the net value of the newly acquired Sneaker

Stadium inventory to $36,389,886, or 77.5% of cost.

107. Ruttenberg , Tyra and Berman acted in concert to hide Just For Feet's poor

performance by improper use of acquisition accounting entries relating to the Sneaker Stadiu m

acquisition. These included providing inventory reserves greatly in excess of justifiable amounts ,

then releasing rese rves as needed to allow the Company to continue to inflate earn ings .

108. Per the 10-Q for the quarter ended July 31, 1998 the Defendants caused the Comp any

to show an estimate of inventory value for the inventory acquired from Sneaker Stadium to be $36 . 4

million. In the 10-Q for the quarter ended October 31, 1998, the amount was adjusted downward

to $27 .6 million pursuant to an overreaching application of Accounting Principles Board ("APB")

34

Statement No. 16 and FAS 38, which permit a one-year period of allocation of purchase price . As

a result, the inventory was now valued at 59% of its cost on the Company's books .

109 . Just For Feet was adjusting inventory downward by increasing its acquisition-related

inventory reserve, with an offsetting increase to goodwill (which was being amortized over the

years, which itself was an overreaching application of APB 17) . The Defendants then recognized

profit on the future sale of the undervalued inventory, causing profit margins and net profits to be

overstated . This treatment effectively masked poor operational results by reducing average cost of

sales and increasing operating income by the amount of the excessive inventory reserve .

110 . As Just For Feet was faced with the prospect of failing to meet securities analysts '

expectations for the third quarter ending October 1998, Defendants Tyra and Berman, with the active

assist ance of Defendants Wynne, Evans and Lloyd, added an additional $8,802,522 to the Sneaker

Stadium inventory reserves . The effect of these arbitrary write-downs of Sneaker Stadium's

inventory was to decrease the cost of goods sold and thereby increase income and earnings . By

means of this manipulative device, Just For Feet was able to meet or exceed the earnings

expectations of securities analysts and thus maintain or support the market price for the shares of

common stock of Just For Feet .

111 . As January 30, 1999 (the end of the fiscal year) neared, Just For Feet was again face d

with a prospective failure to meet securities analysts' earnings expectations and forecasts . In order

to increase earnings and thereby fulfill market expectations, Just For Feet, acting through Tyra and

Berman, and with the active assistance and participation of Wynne, Evans and Lloyd, added an

additional $2,503,650 to the acquisition inventory reserves for the Sneaker Stadium inventory, whic h

35

had been acquired six months earlier, and thereby were able to decrease the cost of goods sold and

thus increase income and earnings .

112 . The use of this manipulation of the Sneaker Stadium inventory reserves, which was

not disclosed to the investing public, enabled Just For Feet to again meet the securities analysts'

earnings forecasts and expectations with the result that the market price of the Just For Feet shares

of common stock was artificially supported by means of these misleading manipulations .

113 . In all, Just For Feet reserved a total of $21,890,069 as acquisition inventory reserves

for the Sneaker Stadium transaction, or 46.6% of its originally booked inventory costs, most or all

of which was unjustified . This scheme to manipulate the inventory costs of the Sneaker Stadium

acquisition had the effect of increasing earnings by as much as $21,890,069, or nearly half of the

Company's reported pre-tax earnings of $43 .3 million .

114 . This scheme was directed by Tyra and Berman, with the active assistance of Wynne,

Evans and Lloyd, and with the knowledge and support of Ruttenberg, Barry, Baker and Deloitte .

Improper Capitalization of Inventory Cost s

115 . By the end of each fiscal year during the Class Period, Just For Feet overstated

inventory by improperly capitalizing operating costs which should have been expensed in the current

period . These costs included operating costs of the corporate headquarters and the stores'

administrative and sales costs in excess of the amounts properly allowable under GAAP . By use of

this device, Just For Feet reduced operating expense by moving tens of millions of dollars into asset

categories such as capitalized inventory costs, thereby overstating inventory and earnings . This

scheme, and its impact upon Just For Feet's reported income and earnings, were discussed among

Lones, Wynne, Barry and Baker in June and July of 1997 .

36

116 . Notwithstanding Lones' adamant insistence that the accounting methods employe d

by Just For Feet were improper and misleading, Wynne and Deloitte, acting through Baker an d

Barry, directed Lones to utilize an accounting methodology which resulted in an even highe r

inventory capitalization.

117 . Just For Feet's improper methods of inventory capitalization, which blatantly violate d

Accounting Research Bulletin ("ARB") 43 (Inventory Pricing), were discussed with Evans and Tyr a

on June 27, 1997 in Tyra's office at the headquarters on 7400 Cahaba Valley Road .

118 . In short, the inventory cost capitalization practices were extraordinary and vastl y

exceeded industry practice . At Just For Feet, the costs of the acquisition of goods was capitalized

at a rate of fourteen percent (14%), which substantially exceeded industry norms . For example, if

Just For Feet purchased a pair of shoes from Nike, it added certain overhead costs to that purchase

price, i.e., cost of personnel in the buying department, freight costs, etc . When Just For Feet

accounted for the purchase of that $30 .00 pair of shoes, it showed the value of that purchase as

$30 .00 x 14%, or $34 .20 .

119. Because Just For Feet utilized the first-in first-out ("FIFO") method of inventor y

accounting, rather than the more widely utilized dollar-value last-in first-out ("LIFO") retail method ,

these improperly capitalized expenses remained in inventory (and thus offthe income statement) fo r

several reporting periods .

120 . The effect of the use of the 14% figure was to materially decrease operating expense s

and consequently increase the earnings of Just For Feet throughout the Class Period . No disclosure

was made that Just For Feet was using a capitalization rate far in excess of industry norms .

37

Overstatement of Inventory Net Realizable Value

121 . By the end of each fiscal year during the Class Period , Just For Feet overstated

inventory by failing to calculate its invento ry in accordance with ARB 43 (Invento ry Pricing) . Just

For Feet failed to properly value invento ry using the lower of cost or market as required by GAAP,

and failing to adequately provide for obsolescence and inventory sh rinkage , also as required by

GAAP .

122. As of May 1, 1999, Just For Feet maintained invento ry reserves of only $400,000,

ludicrously low for fashion retail inventories valued at $458 million. Additionally, there existed no

inventory aging policy at Just For Feet because the information in the Just For Feet invento ry

accounting system was totally unreliable .

123 . Just For Feet regularly transferred its invento ry from division to division and store

to store to inflate the value of its inventory assets . When inventory was transferred from one

division or store to another division or store, it was booked on the records of Just For Feet as "new"

inventory . Thus, when the Just For Feet Specialty Stores Division, which catered to a particularized

market, could not sell inventory, it was transferred to the Super Stores Division, which catered to

an altogether different market, and was picked up on the Super Stores Division's books at the

Specialty Stores' carrying cost (including the old 14% add-on), plus an additional 14% of the already

marked-up value. During July and August 1999 alone, Just For Feet transferred $20 million in

inventory from its Specialty Stores to its Super Stores .

38

124 . In fact, the inventory transferred was frequently obsolete , out of date and, given the

differences in the markets served by the two divisions, was likely to be sold out of the Super Stores

at huge discounts, if at all .

125 . In 1998 and 1999, the inventories at the Specialty Stores consisted largely of outdated

materials, i . e ., 1996 Olympic warm-ups, Houston Oilers jackets, etc ., which had been purchased by

Don-Allen Ruttenberg . In the Just For Feet corporate headquarters, such purchases became known

as "Don Deals . "

126 . The New Jersey warehouse of Just For Feet, which serviced all the northeaster n

United States , was the dumping ground for goods purchased by Just For Feet in "Don Deals ."

Notwithstanding that Just For Feet 's management knew that the invento ry stored at the New Jersey

warehouse was vi rtually worthless, Just For Feet valued that invento ry at its "cost," which was

inflated by a factor of 14% because of Just For Feet's improper inventory cost capitalization

practices , all in violation of GAAP . Just For Feet carried no reserves with respect to this inventory .

127. Many of the "Don Deals" were inventory that was purchased at inflated prices

(frequently to compensate vendors for their pa rticipation in prior accounting schemes by Just For

Feet), and then marked for sale at deep discounts . For example , Don-Allen purchased Dr. Martens

sandals for $23 .00 per pair, but when they hit the sales floor they were immediately marked for sale

at only $ 9 .00 per pair . However, Just For Feet continued to carry the invento ry of sandals on its

books at $23 .00, so it could defer recognition of any loss until the sandals were actually sold, thus

enabling it to spread the loss over future periods . This practice of marking down p rices on the retail

side (the store shelves ) but not on the inventory side (the warehouse or backrooms of stores), was

a standard practice at Just For Feet , and is in violation of the GAAP requirement that inventories be

39

valued at the lower of cost or market value . This practice had a material impact on Just For Feet's

reported earnings throughout the Class Period .

128 . Just For Feet also did not properly account for market enhancement discounts

provided by vendors . When vendors provided cost reductions or markdowns to Just For Feet, Just

For Feet would nevertheless enter and/or maintain the value of the inventory on its books at the

original cost (which was more than Just For Feet had paid), and would immediately recognize

income equal to the difference between the original cost and the price paid, net of discounts . This

allowed Just For Feet to recognize a portion of the income from this inventory immediately upon

receipt of the inventory from the vendors rather than upon sale to customers, thereby increasing

income immediately rather than deferring that income until the inventory was eventually sold to

customers . Because much ofthis inventory was slow-moving or unattractive, the Company in effect

created phantom income rather than reserving for the loss such inventory would likely entail .

129 . As of June 1999, the inventory overstatement at Just For Feet's Specialty Stores ha d

grown to at least $20 million . On a companywide basis, as of July 1, 1999, Just For Feet was

carrying more than $53 million in aged and impaired goods (including Don Deals) on its books at

full cost . These inventory problems were known to most all senior managers at Just For Feet, as well

as to Deloitte, who had been told of the GAAP violations as early as June 1997 .

Improper Accounting For Leaseholds

130 . Just For Feet treated all of its store leases as operating leases, regardless of whether

circumstances existed that would have required them to be capitalized under GAAP . Many of Just

For Feet 's leaseholds were fitted with build-outs and other costly improvements , yet the costs of

those improvements were never capitalized . By failing to capitalize its leases and leasehol d

40