Foodservice Market Prospects - Food South Australia...

43

Foodservice Market Prospects Australia & South East Asia Food SA Summit 5th June 2012

Transcript of Foodservice Market Prospects - Food South Australia...

Foodservice Market Prospects

Australia & South East Asia

Food SA Summit

5th June 2012

BIS Foodservice

3

4

Three Available

Food & Beverage Markets

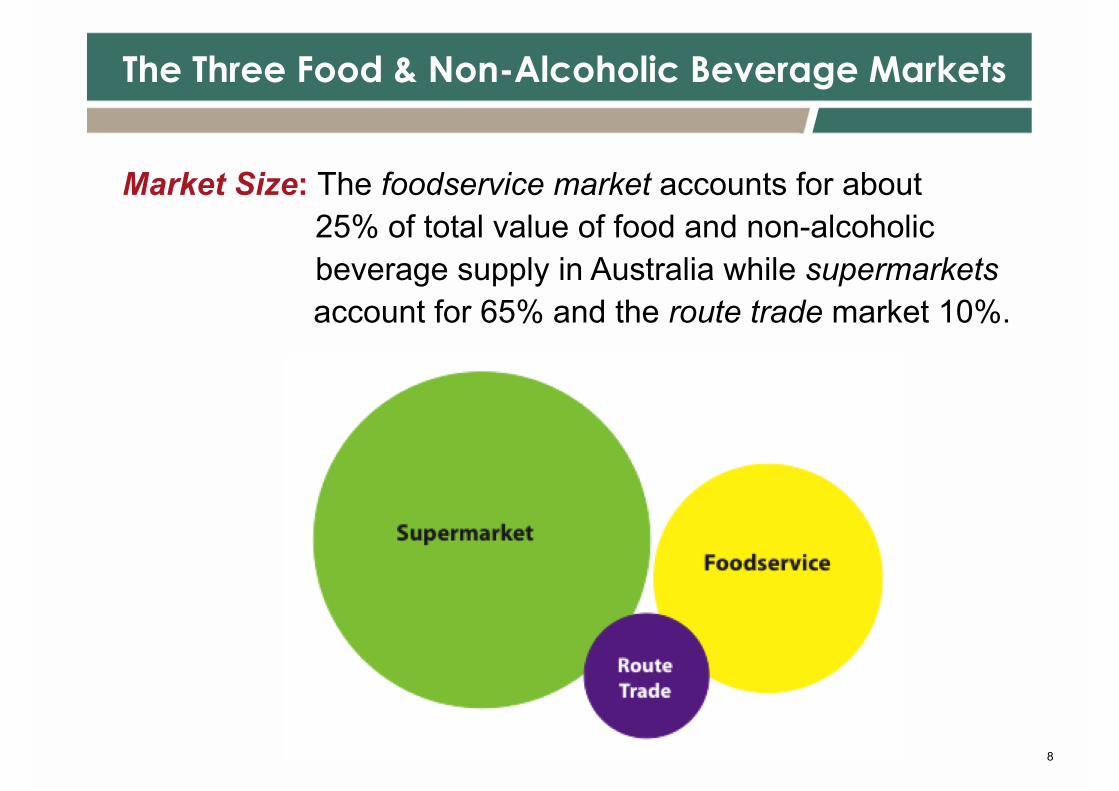

The Three Food & Non-Alcoholic Beverage Markets

8

Market Size: The foodservice market accounts for about

25% of total value of food and non-alcoholic

beverage supply in Australia while supermarkets

account for 65% and the route trade market 10%.

9

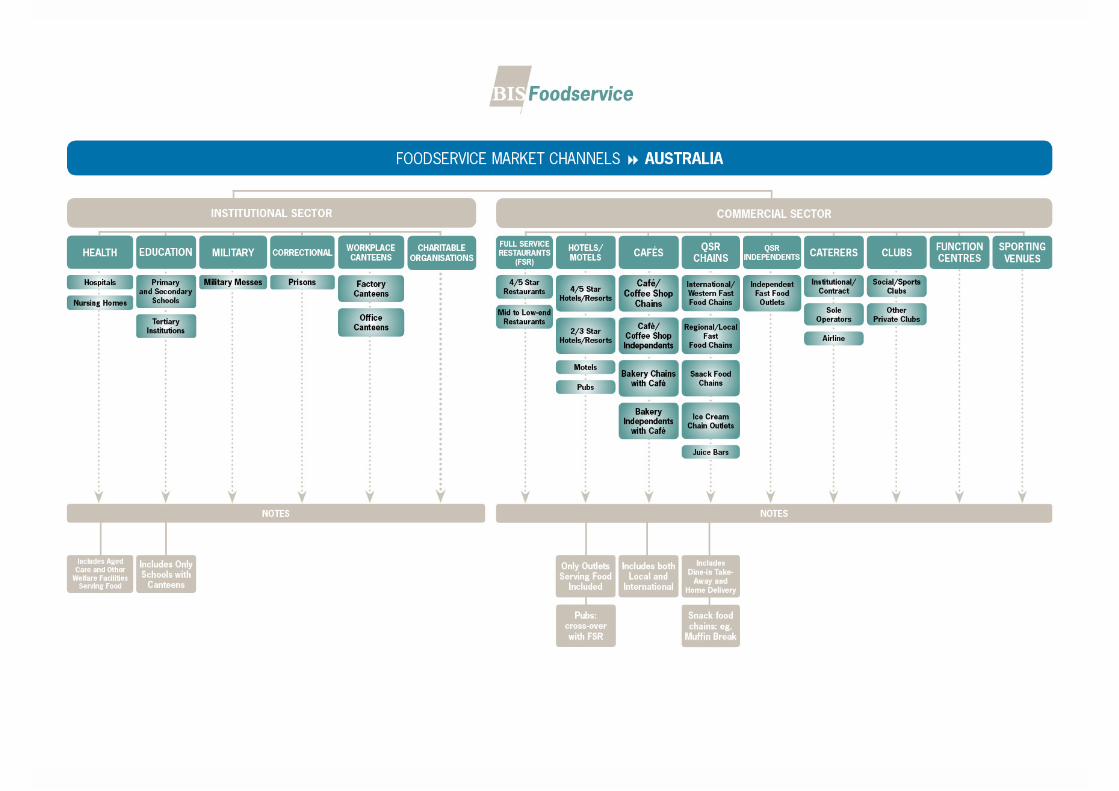

The Foodservice Market – Key Segments

Commercial Sector

Restaurants

Cafés

Fast Food (QSR) Chains & Independents

Institutional Sector

Nursing Homes

Schools

Workplace Canteens

10

The Australian

Foodservice Market

Australian Foodservice Market

The Australian Foodservice market is unique in its total

offering of various cuisine types and eating out experiences.

No other foodservice market offers a similar choice for the

consumers, and hence market opportunities for food and

beverage suppliers.

Over the past ten to fifteen years, Australians have made

eating out a way of life.

The Australian Foodservice market is today a developed

market where the foodservice consumer does not stop eating

out during economic downturns when consumer & business

confidence is low, but they trade down instead in their choice

of outlet.

12

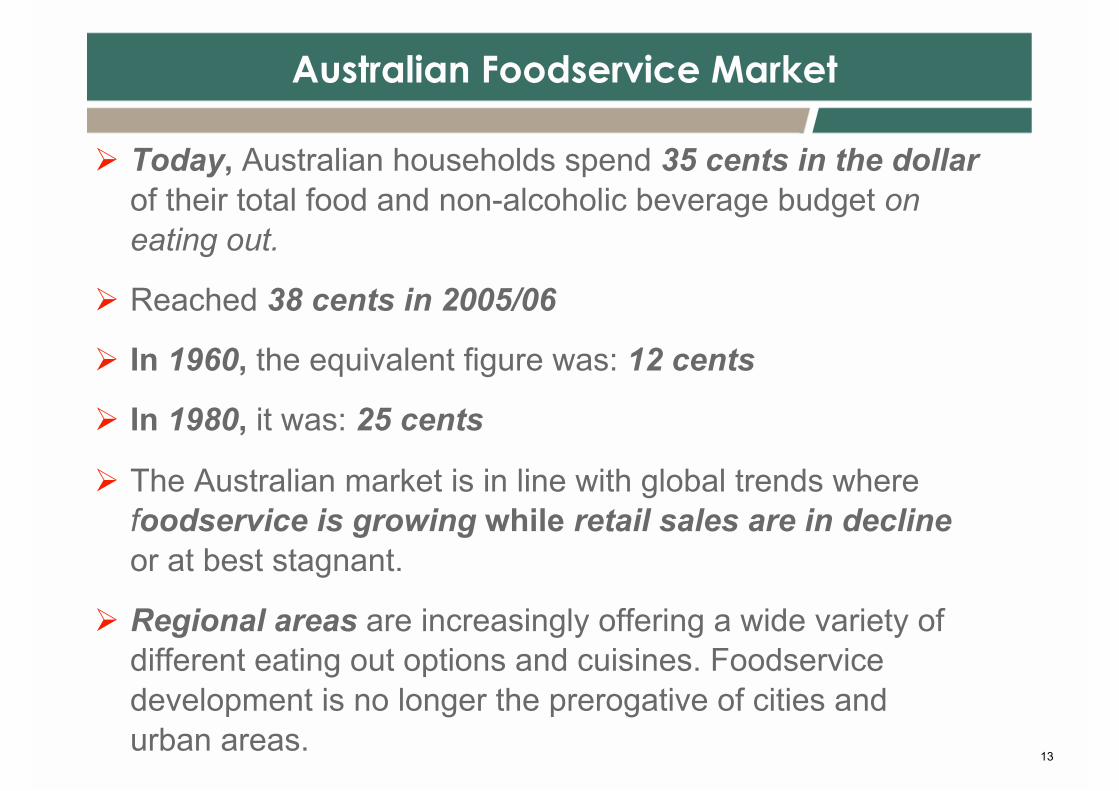

Australian Foodservice Market

Today, Australian households spend 35 cents in the dollar

of their total food and non-alcoholic beverage budget on

eating out.

Reached 38 cents in 2005/06

In 1960, the equivalent figure was: 12 cents

In 1980, it was: 25 cents

The Australian market is in line with global trends where

foodservice is growing while retail sales are in decline

or at best stagnant.

Regional areas are increasingly offering a wide variety of

different eating out options and cuisines. Foodservice

development is no longer the prerogative of cities and

urban areas. 13

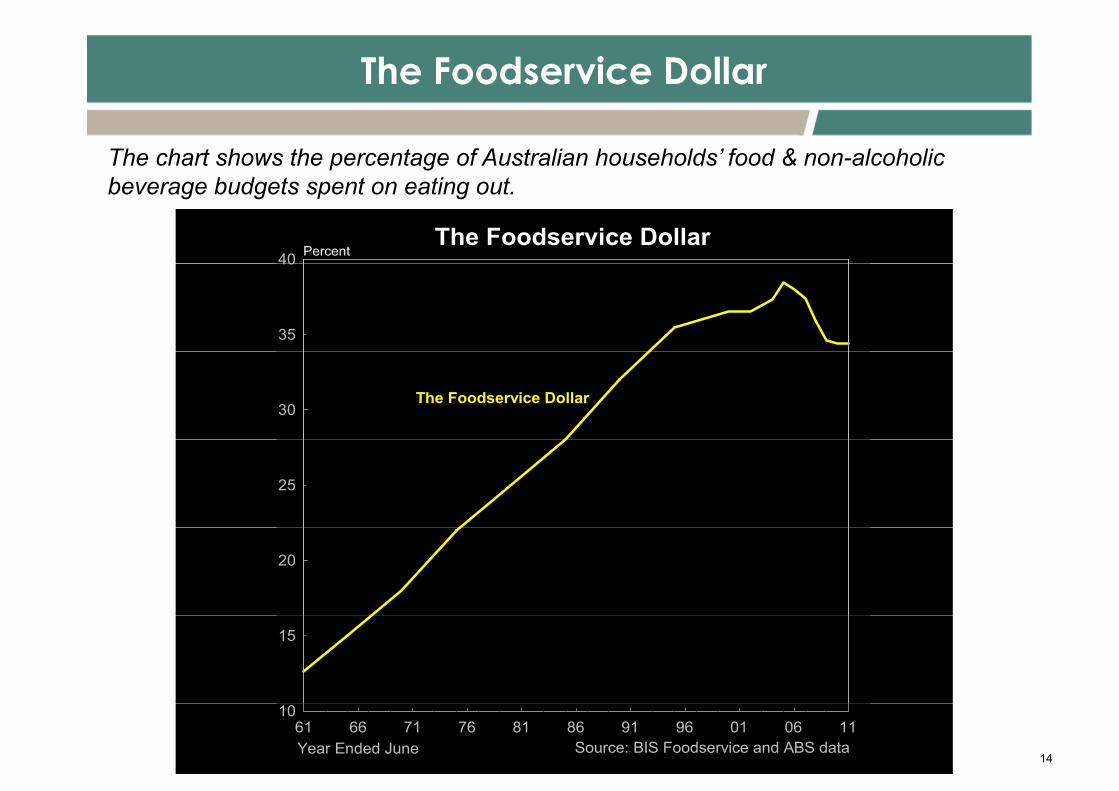

The Foodservice Dollar

The chart shows the percentage of Australian households’ food & non-alcoholic beverage budgets spent on eating out.

The Foodservice Dollar40 Percent

35

40

30The Foodservice Dollar

25

20

15

14

61 63 65 67 69 73 75 77 79 83 85 87 89 93 95 97 99 03 05 07 09 61 66 71 76 81 86 91 96 01 06 11 10

Source: BIS Foodservice and ABS dataYear Ended June

Australian Foodservice Market

Eating out in Australia is relatively affordable compared with other Western developed foodservice markets

Personal relationships still the hallmark of the foodservice market

The foodservice market is by nature international but with distinct national or local characteristics. Many similar world wide trends like the Italian Coffee & Café Culture

But caution when comparing markets

The Australian Foodservice Market = The Scandinavian Foodservice

Markets and not the US Foodservice Market

The Singaporean Foodservice Market South East Asian Markets 15

Foodservice Regions

South Australia

17

A strongly rooted food culture – the essence of the South Australian foodservice market

Always favoured own local produce and food products

Farmer’s markets are important institutions also for foodservice operators

Still a proud British and German food culture

National as well as international food trends and cuisines take a long time to get established in this foodservice region

Seasonal food offering

“South Australia is about regionalism in our own local produce”

New South Wales

Although Sydney centric, NSW has:

Many other large urban areas & cities

Wine districts

Holiday destinations

Thai, Japanese, Indian and of course, Chinese, are the more well known ethnic cuisines established in regional NSW, while Italian food is not counted as foreign

The R&G coffee culture is entrenched right throughout the state

Traditionally, NSW has a strong club culture

Sydney is a very cosmopolitan foodservice market – truly diverse and dynamic in its total offering

18

“New South Wales is a pulsating, ethnically diverse foodservice market”

Victoria

Foodservice in regional Victoria has been booming since

the beginning of last decade with more and more excellent

restaurants – particularly in the wine regions

Tourism is critically important to regional Victoria

Café culture started in Melbourne in the 1950s

Melbourne – an eclectic mix of cafés and restaurants as well as fine dining

19

“Melbourne is the coffee capital of Australia”

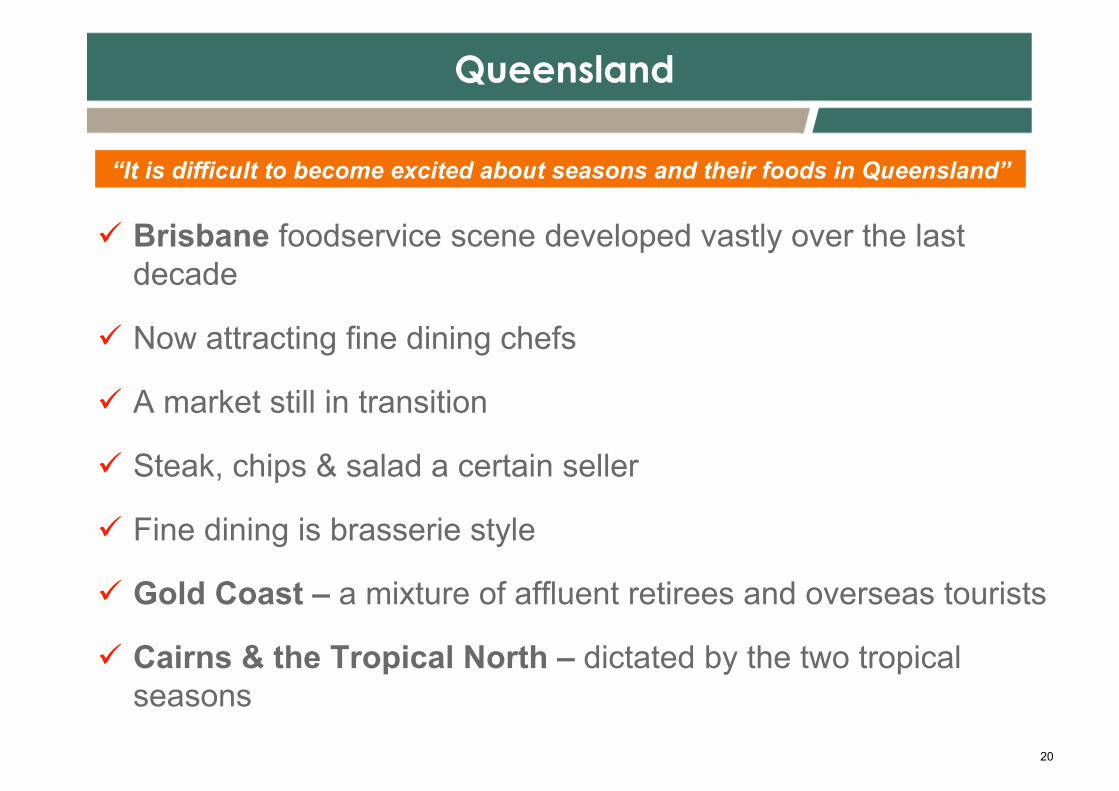

Queensland

Brisbane foodservice scene developed vastly over the last decade

Now attracting fine dining chefs

A market still in transition

Steak, chips & salad a certain seller

Fine dining is brasserie style

Gold Coast – a mixture of affluent retirees and overseas tourists

Cairns & the Tropical North – dictated by the two tropical seasons

20

“It is difficult to become excited about seasons and their foods in Queensland”

Western Australia

Many hundred operating mines

Significant growth in tourism

Opportunities for several channels in the foodservice

sector – in particular hotels, workplace canteens, cafés, restaurants, QSR, hospitals and caterers

Shortage of skilled back-of-house as well as front-of-house foodservice personnel opens up for opportunities in partly or fully prepared food products

North west of the state have problems with supply

21

“Although remote from the Eastern states, WA has huge potential for foodservice suppliers.”

Northern Territory

A strong economy due to large resources and infrastructure projects

Excellent setting for casual dining with an abundance of high quality restaurants and cafés

A strong club culture

A chronic shortage of foodservice staff

22

“The future looks bright for Darwin”

Foodservice Market Size

Foodservice Operatorsp

Foodservice Outlets

Total number of foodservice outlets: 74 196Total number of foodservice outlets: 74,196

Commercial outlets: 58,602

Institutional outlets: 15,594

Commercial Institutional

21%

S i 4 billi l ll79%

Serving 4.7 billion meals annually

24

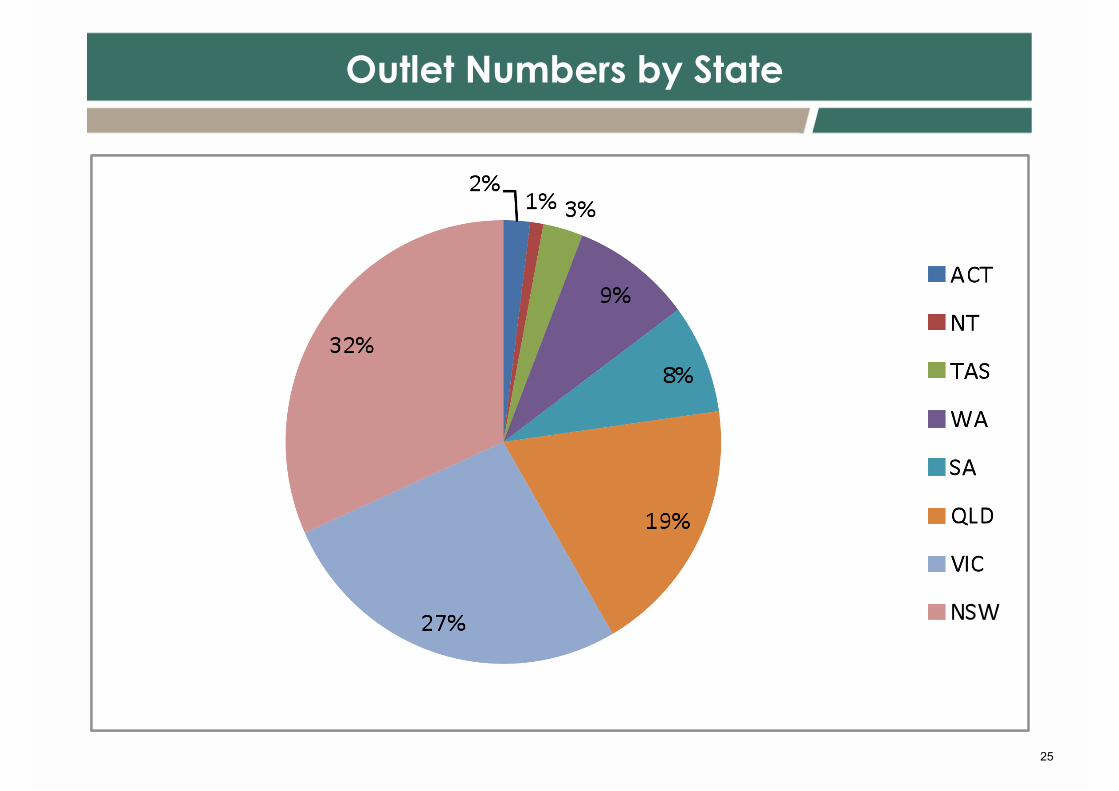

Outlet Numbers by State

25

Market Size

26

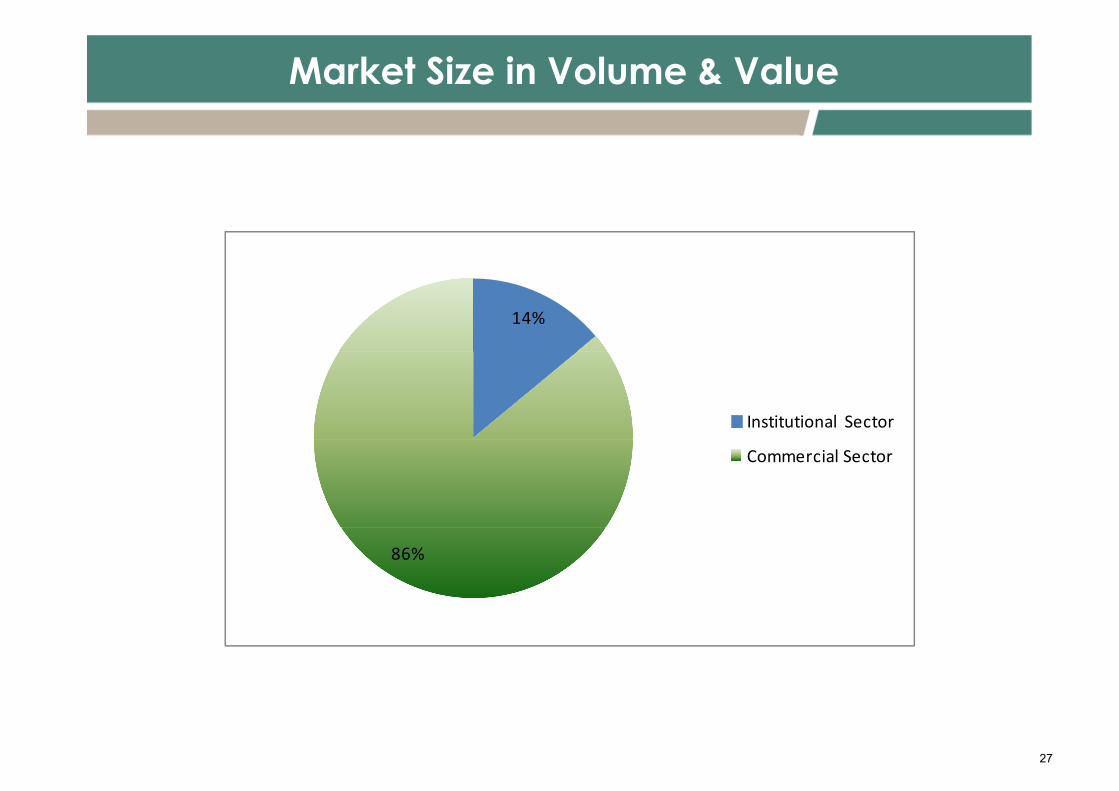

Foodservice Operators’ Purchase of Food

& Non-Alcoholic Beverages 2011

Total Market Size - Volume 2.8 Million Tons

Commercial Market Size - Volume 2.4 Million Tons

Institutional Market Size - Volume 400 Thousand Tons

Foodservice Operators’ Expenditure on

Food & Non-Alcoholic Beverages 2011

Total Market Size - Value A$15.6 Billion

Commercial Market Size - Value A$13.4 Billion

Institutional Market Size - Value A$2.2 Billion

Market Size in Volume & Value

14%

Institutional Sector

Commercial Sector

86%

27

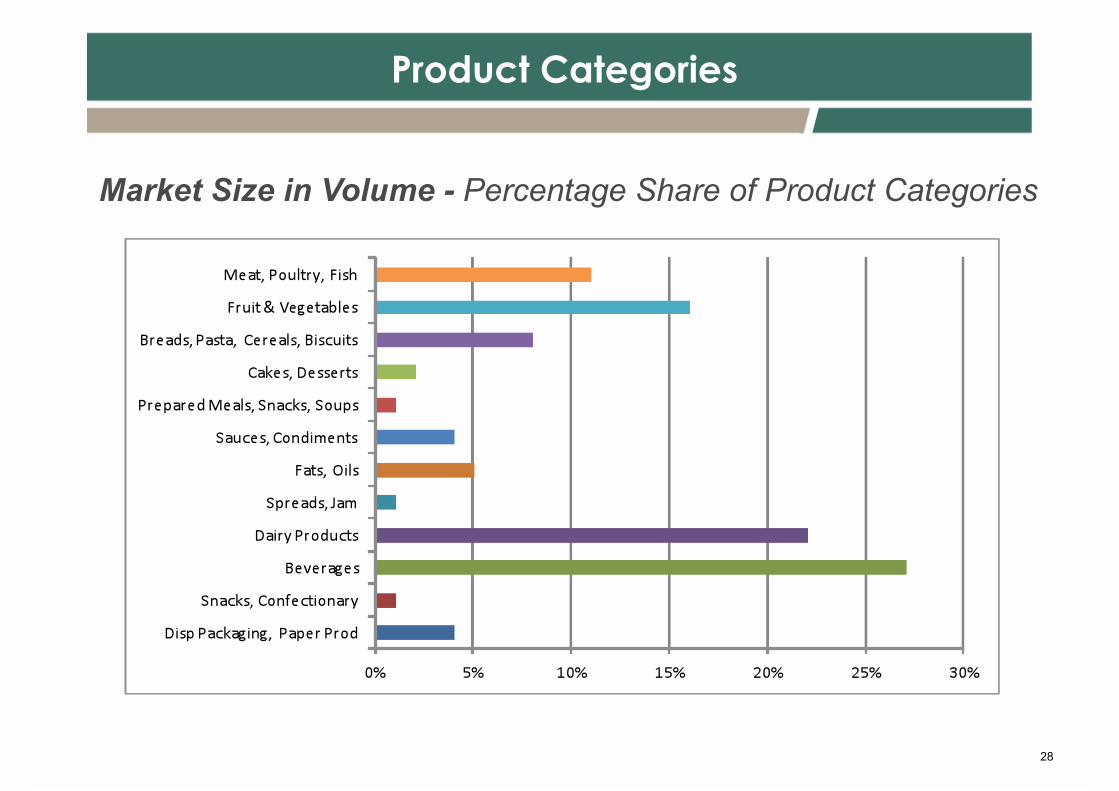

Product Categories

28

Market Size in Volume - Percentage Share of Product Categories

Opportunities

The foodservice market is extremely exciting and vibrant with

ample opportunities for all types of suppliers to find their areas

for growth

By nature the foodservice market offers far more opportunities

for developing distinct market approaches and niches

compared with the Australian food retailing scene where

fighting and paying for shelf space tend to be the main game

Increasing opportunities in the institutional foodservice sector

due to an ageing population. Already underserviced

29

Opportunities

Products:

partly or fully

pre-prepared

food products

portion control

gluten free

30

Innovation paramount – think foodservice, not retail!

Opportunitiespp

Healthy eating – also on the rise in foodservice

The winners in the commercial sector during the economic downturn have been: Lower end restaurants Clubs Fast Food chains

Espresso coffee is on the prise & rise – opens up for complimentary food products

31

Challengesg

Rising food costs ill b– still number one

concern among operators

Fragmented market Fragmented market

A continent

Distribution

32

Market Outlook

Any foodservice market is the first market or industry to be affected by an economic downturn.

But also one the first markets to rebound once the economy improves and consumer & business confidence returns.

Foodservice expenditure by consumers is discretionary spending but in Australia consumers are still eating out but they have traded down in their choice of outlet, they do not eat out as often and they do not spend as much each time.

Up until the beginning of the GFC, the Australian Foodservice market experienced solid growth year on year. This growth will pick up again once the general economy improves.

33

Worldwide Foodservice Markets

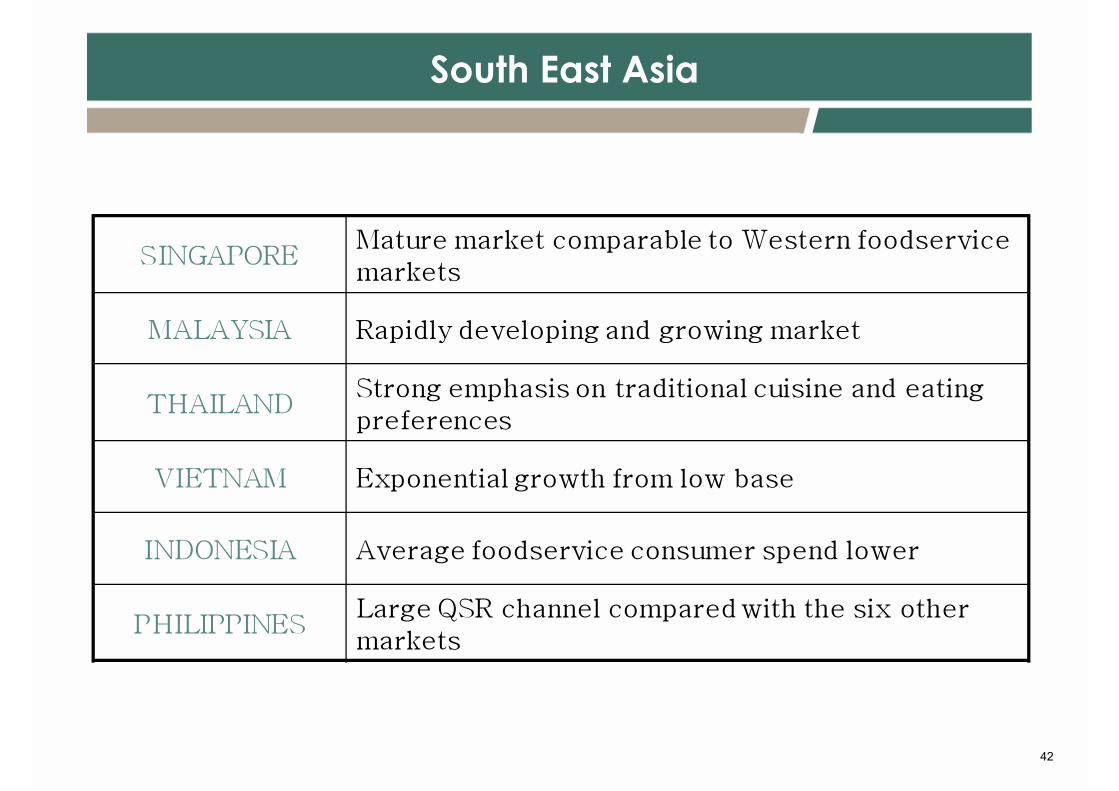

South East Asia

Six major markets – each with its own unique market characteristics:

Malaysia

Singapore

Thailand

Vietnam

Philippines

Indonesia

With a total population of 543 Million

37

South East Asia

38

1.3 million foodservice outlets

US$48 billion at consumer level

Street Dominates

39

South East Asia

Eating out of home a total way of life

All markets, except Singapore, are developing foodservice markets

Strong food cultures and traditional cuisines

40

South East Asia

Young populations and new family structures impacting the foodservice market

Rapid urbanisation impetus for foodservice

growth – particularly in the QSR channel

41

South East Asia

42