UAE Foodservice: The Future of Foodservice in the UAE to 2019 - SP.pdf · UAE Foodservice: The...

19

UAE Foodservice: The Future of Foodservice in the UAE to 2019 FS0012MR August 2015 Sample Pages Single User Price: US$3,200

Transcript of UAE Foodservice: The Future of Foodservice in the UAE to 2019 - SP.pdf · UAE Foodservice: The...

UAE Foodservice: The Future of Foodservice in the UAE to 2019

FS0012MR August 2015 Sample Pages

Single User Price: US$3,200

Summary • Rising obesity rates and related lifestyle diseases have encouraged Emirati consumers to shift their dietary habits towards

healthy foods. The fresh and healthy food trend will also fuel the growth of specific cuisines such as Japanese.

• The Restaurants will remain the dominant channel while the Retail will be the fastest growing channel.

• Low unemployment rates and rising disposable incomes will drive the increased frequency of eat-out occasions and home

deliveries of cooked meals.

• Out of the seven Profit channels, the Restaurants remains the dominant channel in terms of sales in 2014, driven by large

working population and growing tourist volume.

• Out of four Cost channels, Healthcare channel will fuel the growth of Cost Sector foodservice sales, driven by the growing

needs of Emiratis owing to increasing number of diseases associated with sedentary urban lifestyle.

Scope UAE Foodservice: The Future of Foodservice in the UAE to 2019 provides a detailed analysis of macro-economic factors and

the important trends within the market. The report offers detailed analysis of the market in terms of sales, outlets and

transactions. It also covers the major players in the market and regulatory scenario for the foodservice operators. Get access to:

• Macro-economic analyses and trends: GDP per capita, consumer price index, unemployment rate and age profile, which

impact the foodservice market. Consumer, operator and technology level trends are also covered.

• Foodservice market attractiveness: details and insights into the development of the foodservice sector from 2009-2019.

• Sector analysis: provides in-depth data on the valuation and development of both the profit and the cost sectors, details on the

number of outlets, transactions, average price, foodservice sales, sales per outlet, and transactions per outlet across nearly

50 sub-channels

• An overview of key players, together with insights such as number of outlets, business description and product profiles.

• Regulatory scenario insights for foodservice operators in the Emirati market

11/08/2015 3 8/11/2015 3 8/11/2015 3 8/11/2015 3

This report provides a top-level overview and detailed market and channel insights into the operating environment for

foodservice companies. It is an essential tool for companies active across the Emirati foodservice value chain, and for

new companies considering entering the market.

Macro Economic Analysis and Trends

To assess the impact of economic recession and recovery on foodservice market growth. It also identifies the major

trends at consumer, operator and technology level that will shape the foodservice market and will provide a clear

picture about the future opportunities that can be explored, resulting in revenue expansion.

Foodservice Market Attractiveness

To gain the confidence to make the correct business decisions based on a detailed analysis of the Emirati

Foodservice market. The report also provides historic (2009-2014) and forecast (2014-2019) view, with a special focus

on foodservice sales, outlets and transactions.

Sector Analysis- Profit Sector and Cost Sector

To have a thorough fact based analysis with information about value of the foodservice market across the channels

and sub-channels in both the sectors and the underlying factors that are driving the channel sales.

Competitive Landscape

Overview of key foodservice companies in the UAE with information about their business description, product profile

and number of outlets wherever available.

Reasons to buy this report

11/08/2015 4 8/11/2015 4 8/11/2015 4 8/11/2015 4

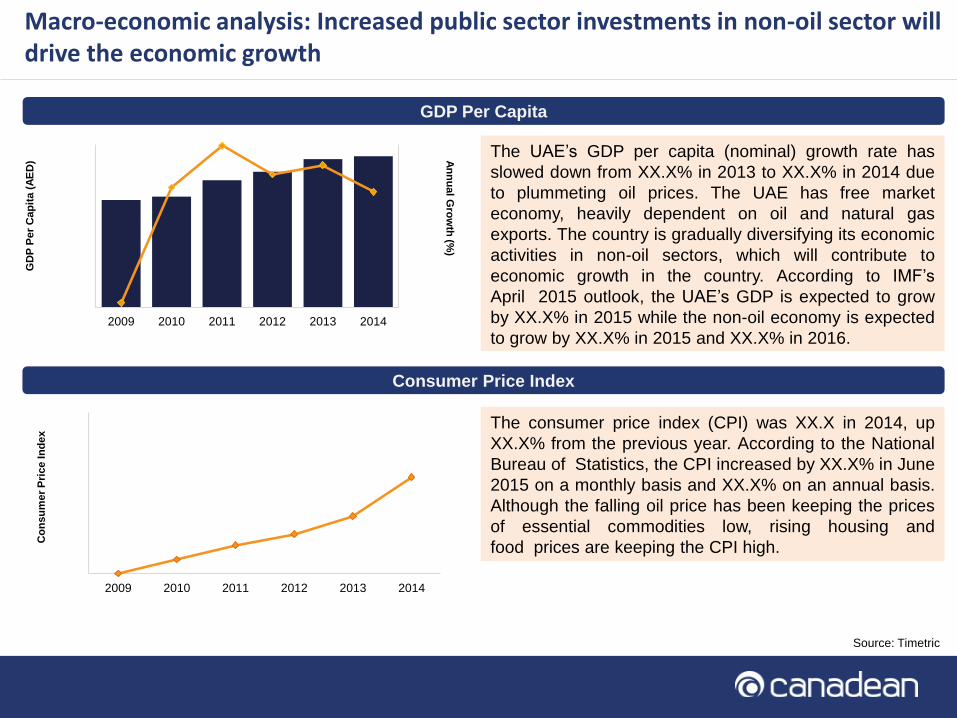

Macro-economic analysis: Increased public sector investments in non-oil sector will drive the economic growth

GDP Per Capita

Consumer Price Index

The UAE’s GDP per capita (nominal) growth rate has

slowed down from XX.X% in 2013 to XX.X% in 2014 due

to plummeting oil prices. The UAE has free market

economy, heavily dependent on oil and natural gas

exports. The country is gradually diversifying its economic

activities in non-oil sectors, which will contribute to

economic growth in the country. According to IMF’s

April 2015 outlook, the UAE’s GDP is expected to grow

by XX.X% in 2015 while the non-oil economy is expected

to grow by XX.X% in 2015 and XX.X% in 2016.

The consumer price index (CPI) was XX.X in 2014, up

XX.X% from the previous year. According to the National

Bureau of Statistics, the CPI increased by XX.X% in June

2015 on a monthly basis and XX.X% on an annual basis.

Although the falling oil price has been keeping the prices

of essential commodities low, rising housing and

food prices are keeping the CPI high.

Source: Timetric

-30%

-20%

-10%

0%

10%

0

10,000

20,000

30,000

40,000

50,000

2009 2010 2011 2012 2013 2014

An

nu

al G

row

th (%

)

GD

P P

er

Cap

ita (

AE

D)

100

102

104

106

108

110

2009 2010 2011 2012 2013 2014

Co

ns

um

er

Pri

ce In

de

x

11/08/2015 5 8/11/2015 5 8/11/2015 5 8/11/2015 5

Consumer Trends: Consumer awareness is leading to a shift in dietary habits

Shifting towards healthy eating habits

Rising obesity rates and related lifestyle diseases such as diabetes have

encouraged Emirati consumers to pay more attention towards their diet,

resulting in a shift in the dietary habits towards eating healthy foods. More

than 60% of the UAE residents (above 18 years old) are either

overweight or obese. Although the demand for healthy foods such as

organic/gluten-free foods is primarily driven by western expatriate

population in the UAE, recent health awareness promotions have led the

young Emiratis to gradually shift to healthy food options while dining out.

Major drivers contributing to the trend are:

• Easy access to organic foods- Despite low local production of

organic products, the demand for organic foods is growing in the

UAE. To meet the growing demand, some companies in collaboration

with local certified organic farmers are putting up weekly organic

markets such as the Ripe Food & Craft Market, and Organic Foods

and Cafe. The Ripe Food & Craft also delivers fruit boxes to

workplaces to promote healthy snacking habits among the UAE

consumers. Some of the markets also serve freshly prepared

breakfast including homemade breads and jams. Many restaurants

specializing in organic dishes are also opening in the country, popular

one include the Organic Foods & Café, the Taste Initiative, the Park

Hyatt, Kamat, Aryaas and Comptoir 102.

• Willingness to pay for healthy food- Most of the healthy foods

such as low-carb, organic and gluten-free are often associated with

premium prices. But growing disposable incomes of Emiratis and

rising awareness about healthy eating benefits are stimulating the

demand for high quality, fresh and organic foods. Emirati consumers

are willing to pay higher prices for certified organic food.

The farmer’s market at Jumeirah Emirates Towers,

Dubai serves freshly cooked breakfast in addition

to organic fruits, vegetables and other food

products.

Heading towards

healthy eating

Easy access to healthy foods

promoting healthy eating habits among

children

Affordability and willingness

11/08/2015 6 8/11/2015 6 8/11/2015 6 8/11/2015 6

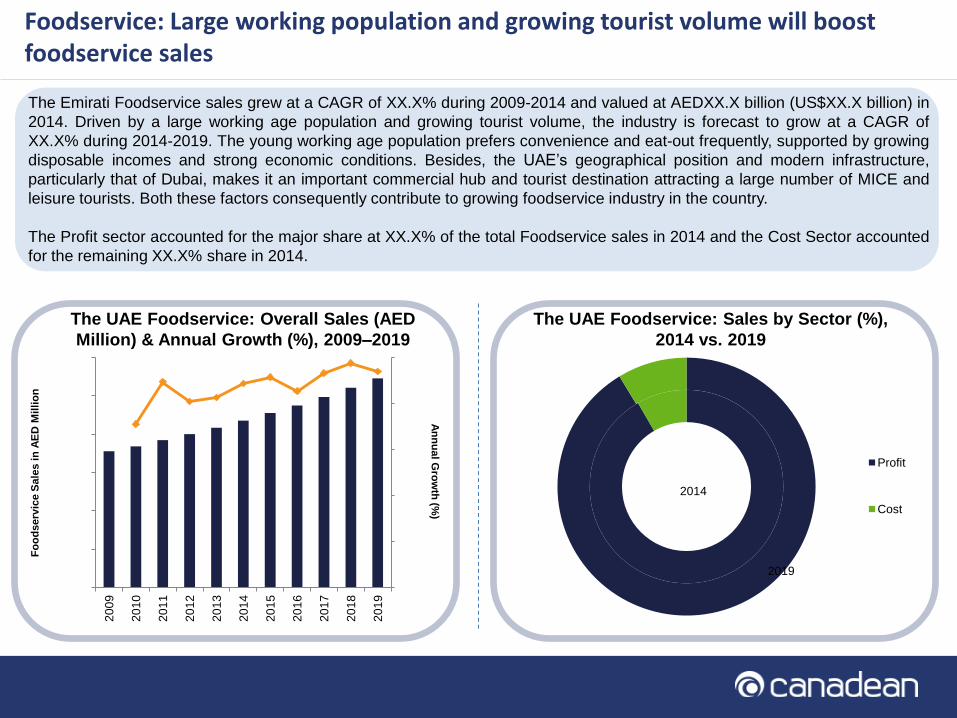

The Emirati Foodservice sales grew at a CAGR of XX.X% during 2009-2014 and valued at AEDXX.X billion (US$XX.X billion) in

2014. Driven by a large working age population and growing tourist volume, the industry is forecast to grow at a CAGR of

XX.X% during 2014-2019. The young working age population prefers convenience and eat-out frequently, supported by growing

disposable incomes and strong economic conditions. Besides, the UAE’s geographical position and modern infrastructure,

particularly that of Dubai, makes it an important commercial hub and tourist destination attracting a large number of MICE and

leisure tourists. Both these factors consequently contribute to growing foodservice industry in the country.

The Profit sector accounted for the major share at XX.X% of the total Foodservice sales in 2014 and the Cost Sector accounted

for the remaining XX.X% share in 2014.

Foodservice: Large working population and growing tourist volume will boost foodservice sales

The UAE Foodservice: Overall Sales (AED

Million) & Annual Growth (%), 2009–2019

The UAE Foodservice: Sales by Sector (%),

2014 vs. 2019

0%

1%

2%

3%

4%

5%

0

5,000

10,000

15,000

20,000

25,000

30,000

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

An

nu

al G

row

th (%

)

Fo

od

serv

ice S

ale

s in

AE

D M

illi

on

Profit

Cost

2019

2014

11/08/2015 7 8/11/2015 7 8/11/2015 7 8/11/2015 7

The Emirati Foodservice industry has grown steadily during 2009-2014. Restaurants is the dominant

Foodservice channel, accounting for XX.X% of the total foodservice sales in 2014. Increasing frequency of

eating-out and home deliveries of cooked meals will drive the Restaurants channel. Rapid development of the

retail sector, particularly in major the cities of Abu Dhabi, Sharjah, and Dubai, where consumers prefer to shop

in large malls, supermarkets, and hypermarkets will boost the Retail foodservice sales, which will be fastest

growing during 2014-2019.

Restaurants will remain the dominant channel while Retail will be the fastest growing channel

Bubble size = 2014 Sales

0%

2%

4%

6%

8%

0% 2% 4% 6% 8%

Sale

s in

AE

D M

illi

on

CA

GR

(%

) 2014

-2019

Sales in AED Million CAGR (%) 2009-2014

Comparative growth analysis by channels, 2009-2014 vs. 2014-2019

Restaurants

Accommodation

Workplace

Education

Retail

Leisure

Military & civil defense

Healthcare

Travel

Pub, club and bar

Welfare & services

11/08/2015 8 8/11/2015 8 8/11/2015 8 8/11/2015 8

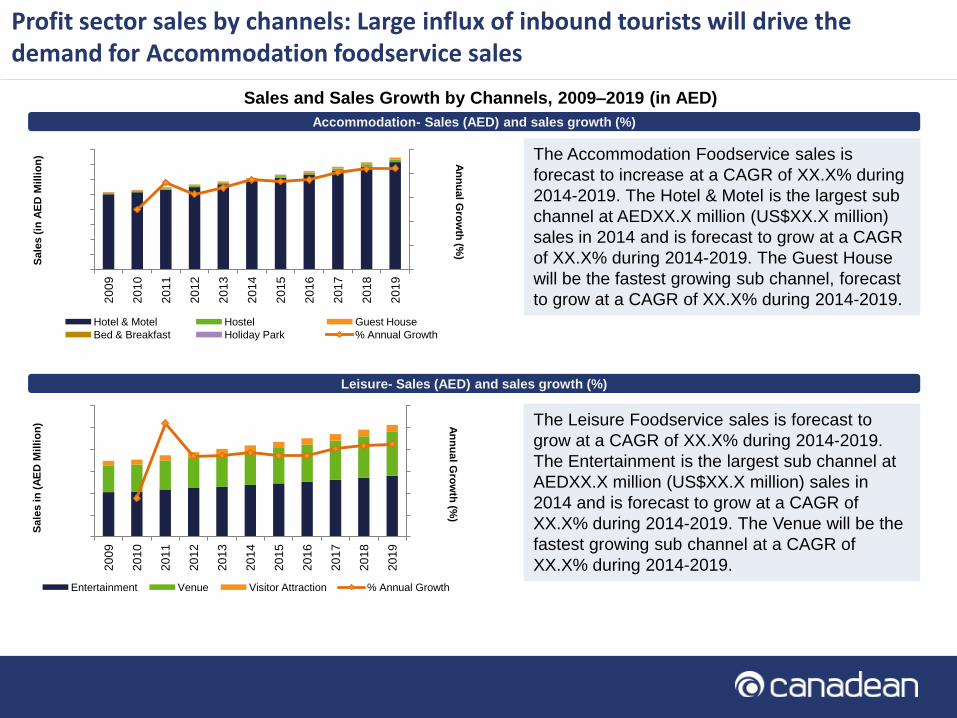

Profit sector sales by channels: Large influx of inbound tourists will drive the demand for Accommodation foodservice sales Accommodation- Sales (AED) and sales growth (%)

Sales and Sales Growth by Channels, 2009–2019 (in AED)

Leisure- Sales (AED) and sales growth (%)

The Accommodation Foodservice sales is

forecast to increase at a CAGR of XX.X% during

2014-2019. The Hotel & Motel is the largest sub

channel at AEDXX.X million (US$XX.X million)

sales in 2014 and is forecast to grow at a CAGR

of XX.X% during 2014-2019. The Guest House

will be the fastest growing sub channel, forecast

to grow at a CAGR of XX.X% during 2014-2019.

The Leisure Foodservice sales is forecast to

grow at a CAGR of XX.X% during 2014-2019.

The Entertainment is the largest sub channel at

AEDXX.X million (US$XX.X million) sales in

2014 and is forecast to grow at a CAGR of

XX.X% during 2014-2019. The Venue will be the

fastest growing sub channel at a CAGR of

XX.X% during 2014-2019.

0%

1%

2%

3%

4%

5%

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

An

nu

al G

row

th (%

)

Sale

s (

in A

ED

Mil

lio

n)

Hotel & Motel Hostel Guest House

Bed & Breakfast Holiday Park % Annual Growth

0%

1%

2%

3%

4%

5%

6%

0

100

200

300

400

500

600

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

An

nu

al G

row

th (%

)

Sa

les

in

(A

ED

Mil

lio

n)

Entertainment Venue Visitor Attraction % Annual Growth

11/08/2015 9 8/11/2015 9 8/11/2015 9 8/11/2015 9

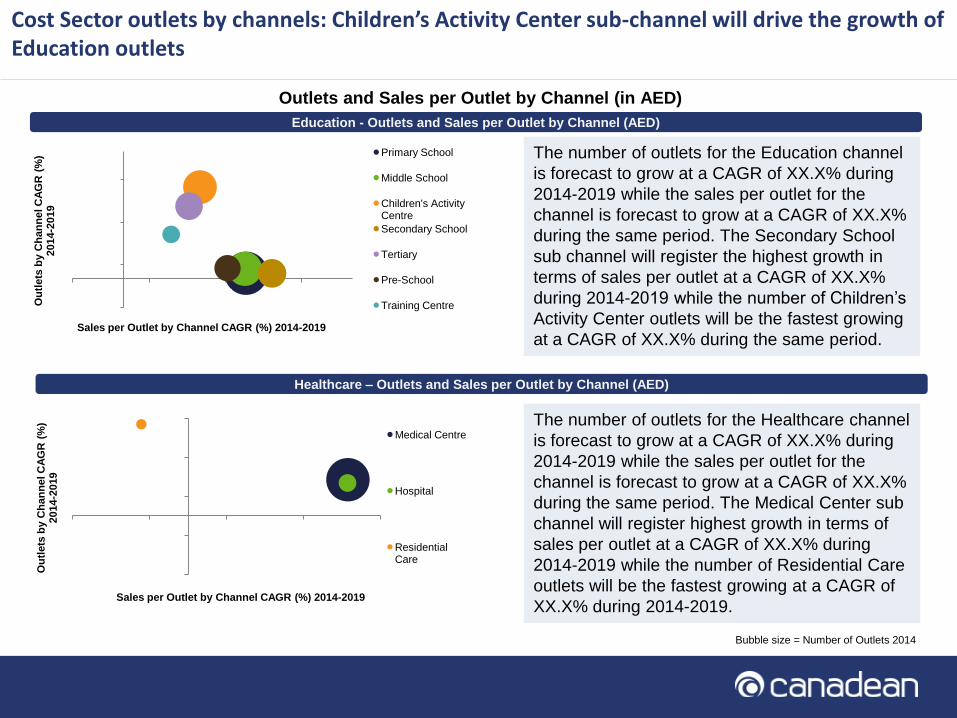

Cost Sector outlets by channels: Children’s Activity Center sub-channel will drive the growth of Education outlets

Education - Outlets and Sales per Outlet by Channel (AED)

Outlets and Sales per Outlet by Channel (in AED)

The number of outlets for the Education channel

is forecast to grow at a CAGR of XX.X% during

2014-2019 while the sales per outlet for the

channel is forecast to grow at a CAGR of XX.X%

during the same period. The Secondary School

sub channel will register the highest growth in

terms of sales per outlet at a CAGR of XX.X%

during 2014-2019 while the number of Children’s

Activity Center outlets will be the fastest growing

at a CAGR of XX.X% during the same period.

Healthcare – Outlets and Sales per Outlet by Channel (AED)

The number of outlets for the Healthcare channel

is forecast to grow at a CAGR of XX.X% during

2014-2019 while the sales per outlet for the

channel is forecast to grow at a CAGR of XX.X%

during the same period. The Medical Center sub

channel will register highest growth in terms of

sales per outlet at a CAGR of XX.X% during

2014-2019 while the number of Residential Care

outlets will be the fastest growing at a CAGR of

XX.X% during 2014-2019.

Bubble size = Number of Outlets 2014

-2%

1%

4%

7%

-2% 1% 4% 7%

Ou

tlets

by C

ha

nn

el C

AG

R (

%)

2014-2

019

Sales per Outlet by Channel CAGR (%) 2014-2019

Primary School

Middle School

Children's Activity Centre

Secondary School

Tertiary

Pre-School

Training Centre

-3%

-1%

1%

3%

5%

-3% -1% 1% 3% 5%

Ou

tlets

by C

ha

nn

el C

AG

R (

%)

2014-2

019

Sales per Outlet by Channel CAGR (%) 2014-2019

Medical Centre

Hospital

Residential Care

11/08/2015 10 8/11/2015 10 8/11/2015 10 8/11/2015 10

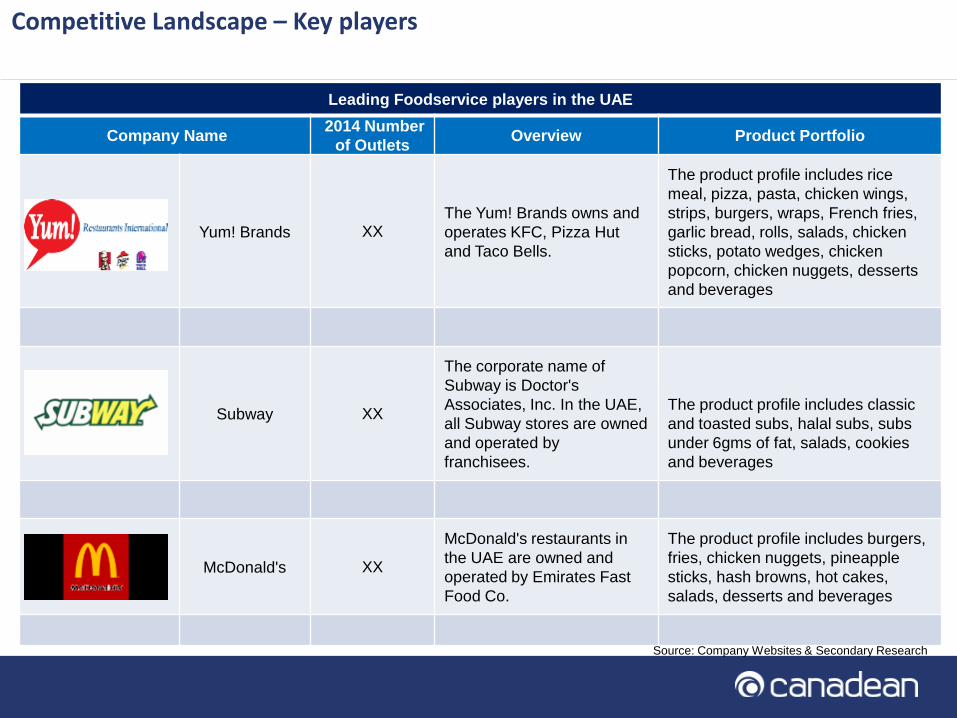

Competitive Landscape – Key players

Leading Foodservice players in the UAE

Company Name 2014 Number

of Outlets Overview Product Portfolio

Yum! Brands XX The Yum! Brands owns and

operates KFC, Pizza Hut

and Taco Bells.

The product profile includes rice

meal, pizza, pasta, chicken wings,

strips, burgers, wraps, French fries,

garlic bread, rolls, salads, chicken

sticks, potato wedges, chicken

popcorn, chicken nuggets, desserts

and beverages

Subway XX

The corporate name of

Subway is Doctor's

Associates, Inc. In the UAE,

all Subway stores are owned

and operated by

franchisees.

The product profile includes classic

and toasted subs, halal subs, subs

under 6gms of fat, salads, cookies

and beverages

McDonald's XX

McDonald's restaurants in

the UAE are owned and

operated by Emirates Fast

Food Co.

The product profile includes burgers,

fries, chicken nuggets, pineapple

sticks, hash browns, hot cakes,

salads, desserts and beverages

Source: Company Websites & Secondary Research

Appendix - Profit Sector Outlets

Channel Sub-Channel 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Accommodation

Bed and Breakfasts

(B&B)

Guest Houses

Holiday Parks

Hostels

Hotels and Motels

Leisure

Entertainment

Venue

Visitor Attractions

Pubs, Clubs and

Bars

Pubs and Bars

Private Member and

Social Clubs

Nightclubs

11/08/2015 12 8/11/2015 12 8/11/2015 12 8/11/2015 12

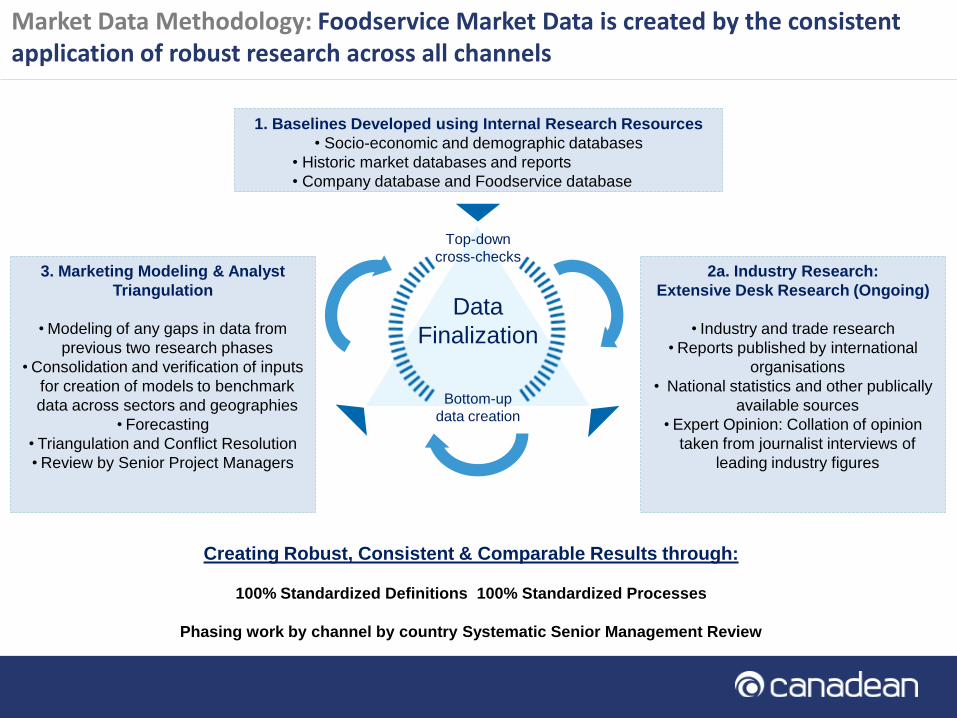

Market Data Methodology: Foodservice Market Data is created by the consistent application of robust research across all channels

Creating Robust, Consistent & Comparable Results through:

100% Standardized Definitions 100% Standardized Processes

Phasing work by channel by country Systematic Senior Management Review

1. Baselines Developed using Internal Research Resources

• Socio-economic and demographic databases

• Historic market databases and reports

• Company database and Foodservice database

2a. Industry Research:

Extensive Desk Research (Ongoing)

• Industry and trade research

• Reports published by international

organisations

• National statistics and other publically

available sources

• Expert Opinion: Collation of opinion

taken from journalist interviews of

leading industry figures

Top-down

cross-checks

Bottom-up

data creation

Data

Finalization

3. Marketing Modeling & Analyst

Triangulation

• Modeling of any gaps in data from

previous two research phases

• Consolidation and verification of inputs

for creation of models to benchmark

data across sectors and geographies

• Forecasting

• Triangulation and Conflict Resolution

• Review by Senior Project Managers

11/08/2015 13 8/11/2015 13 8/11/2015 13 8/11/2015 13

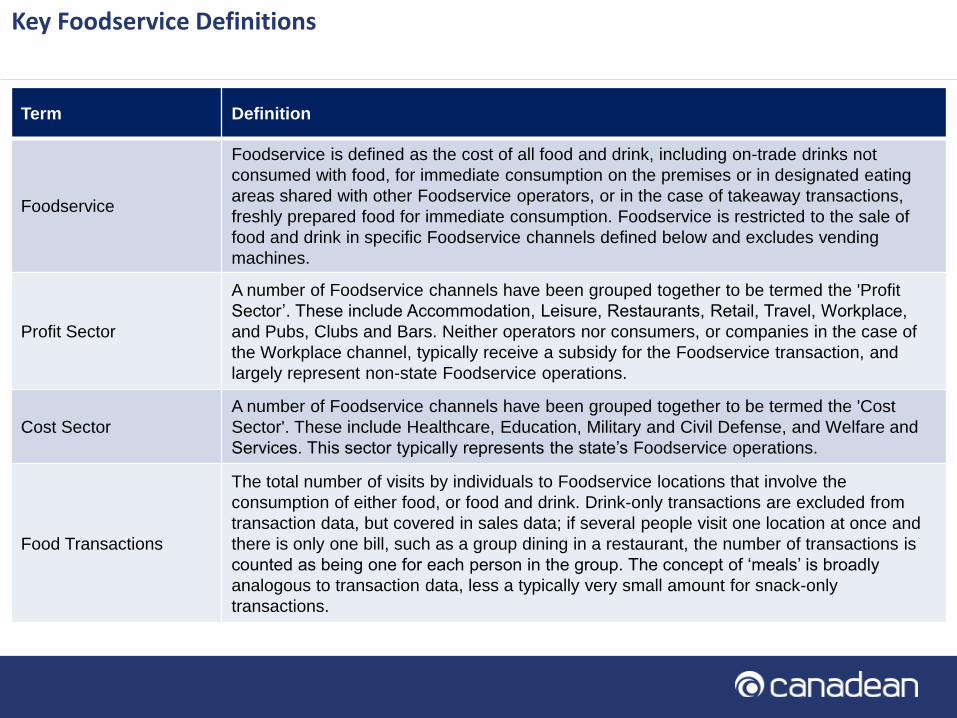

Key Foodservice Definitions

Term Definition

Foodservice

Foodservice is defined as the cost of all food and drink, including on-trade drinks not

consumed with food, for immediate consumption on the premises or in designated eating

areas shared with other Foodservice operators, or in the case of takeaway transactions,

freshly prepared food for immediate consumption. Foodservice is restricted to the sale of

food and drink in specific Foodservice channels defined below and excludes vending

machines.

Profit Sector

A number of Foodservice channels have been grouped together to be termed the 'Profit

Sector’. These include Accommodation, Leisure, Restaurants, Retail, Travel, Workplace,

and Pubs, Clubs and Bars. Neither operators nor consumers, or companies in the case of

the Workplace channel, typically receive a subsidy for the Foodservice transaction, and

largely represent non-state Foodservice operations.

Cost Sector

A number of Foodservice channels have been grouped together to be termed the 'Cost

Sector'. These include Healthcare, Education, Military and Civil Defense, and Welfare and

Services. This sector typically represents the state’s Foodservice operations.

Food Transactions

The total number of visits by individuals to Foodservice locations that involve the

consumption of either food, or food and drink. Drink-only transactions are excluded from

transaction data, but covered in sales data; if several people visit one location at once and

there is only one bill, such as a group dining in a restaurant, the number of transactions is

counted as being one for each person in the group. The concept of ‘meals’ is broadly

analogous to transaction data, less a typically very small amount for snack-only

transactions.

11/08/2015 14 8/11/2015 14 8/11/2015 14 8/11/2015 14

Related Reports

• Japanese Foodservice: The Future of Foodservice in Japan to 2019

• Spanish Foodservice: The Future of Foodservice in Spain to 2019

• French Foodservice: The Future of Foodservice in France to 2019

• German Foodservice: The Future of Foodservice in Germany to 2019

• Chinese Foodservice: The Future of Foodservice in China to 2019

• The UK Foodservice: The Future of Foodservice in the United Kingdom to 2019

• Italian Foodservice: The Future of Foodservice in Italy to 2019

• Turkish Foodservice: The Future of Foodservice in Turkey to 2019

• Austrian Foodservice: The Future of Foodservice in Austria to 2019

11/08/2015 15 8/11/2015 15 8/11/2015 15 8/11/2015 15

Executive Summary

Macro Economic Analysis and Trends Macroeconomic Analysis

Consumer Trends

Operator Trends

Technology Trends

Foodservice Market Attractiveness Market Size and Forecasts

Market Share split by Profit Sector and Cost Sector

Profit Sector Analysis Profit Sector Analysis by Channels & Sub-channels- Sales Analysis, Outlet Analysis and Transaction Analysis • Accommodation - Bed & Breakfast, Guest House, Holiday Park, Hostel, Hotel & Motel

• Leisure – Entertainment, Venue, Visitor Attraction

• Pub, Club & Bar – Pub & Bar, Private Member & Social Club, Nightclub

• Restaurants - Full Service Restaurant, Quick Service Restaurant & Fast Food, Coffee & Tea Shop, Ice Cream Vendor

• Retail – Baker, Convenience Store, Delicatessen, Department Store, Garden Centre, Other Retail, Service Station Forecourt,

Supermarket & Hypermarket

• Travel – Air, Rail, Sea

• Workplace - Government Department & Local Authority, Industrial, Retail, Financial & Office Based

Cost Sector Analysis Cost Sector Analysis by Channels & Sub-channels- Sales Analysis, Outlet Analysis and Transaction Analysis • Education - Children’s Activity Centre, Further Education, Pre-School, Primary School, Secondary School, Tertiary, Training Centre

• Healthcare – Hospital, Medical Centre, Residential Care

• Military & Civil Defence - Military Overall, Police & Emergency Service

• Welfare & Service - Other Welfare & Service, Prison, Welfare Meal

Competitive Landscape Company Overview , Product Portfolio and Number of Outlets

Regulatory Scenario

Appendix

Table of Contents

11/08/2015 16 8/11/2015 16 8/11/2015 16 8/11/2015 16

Appendix

Profit Sector Outlets

Cost Sector Outlets

Profit Sector Transactions (Million), 2009-2019

Cost Sector Transactions (Million), 2009-2019

Profit Sector Sales (AED Million), 2009-2019

Cost Sector Sales (AED Million), 2009-2019

11/08/2015 17 8/11/2015 17 8/11/2015 17 8/11/2015 17

List of Figures

Figure 1: GDP per Capita, 2009-2014 Figure 2: Consumer Price Index, 2009-2014 Figure 3: Unemployment Rate, 2009-2014 Figure 4: Age Profile, 2014 Figure 5: UAE Foodservice: Overall Sales (AED Million) & Annual Growth (%), 2009-2019 Figure 6: UAE Foodservice: Sales by Sector (%), 2014 vs. 2019 Figure 7: Comparative Growth Analysis by Channels, 2009-2014 vs 2014-2019 Figure 8: Profit Sector: Channel share (%), 2014 vs. 2019 Figure 9: Profit Sector: Average Transaction Price (AED), 2009-2019 Figure 10: Profit Sector: Comparative Growth Analysis by Channels, 2009-2014 vs 2014-2019 Figure 11: Accommodation- Sales (AED) and sales growth (%), 2009-2019 Figure 12: Leisure- Sales (AED) and sales growth (%), 2009-2019 Figure 13: Pub, Club & Bar- Sales (AED) and sales growth (%), 2009-2019 Figure 14: Restaurants - Sales (AED) and sales growth (%), 2009-2019 Figure 15: Retail - Sales (AED) and sales growth (%), 2009-2019 Figure 16: Travel - Sales (AED) and sales growth (%), 2009-2019 Figure 17: Workplace - Sales (AED) and sales growth (%), 2009-2019 Figure 18: Profit Sector: Comparative Growth Analysis by Channels, Sales per Outlet & Number of Outlets, 2009- 2014 vs 2014-2019 Figure 19: Accommodation - Outlets and Sales per Outlet by Channel (AED), 2009-2019 Figure 20: Leisure - Outlets and Sales per Outlet by Channel (AED), 2009-2019 Figure 21: Pub, Club, and Bar - Outlets and Sales per Outlet by Channel (AED), 2009-2019 Figure 22: Restaurants – Outlets and Sales per Outlet by Channel (AED), 2009-2019 Figure 23: Retail – Outlets and Sales per Outlet by Channel (AED), 2009-2019 Figure 24: Workplace - Outlets and Sales per Outlet by Channel (AED), 2009-2019 Figure 25: Profit Sector: Comparative Growth Analysis by Channels, Transactions per Outlet & Number of Transactions, 2009- 2014 vs 2014-2019

List of Figures

11/08/2015 18 8/11/2015 18 8/11/2015 18 8/11/2015 18

List of Figures

Figure 26: Accommodation - Transactions and Transactions per Outlet by Channel, 2009-2019 Figure 27: Leisure - Transactions and Transactions per Outlet by Channel, 2009-2019 Figure 28: Pub, Club, and Bar - Transactions and Transactions per Outlet by Channel, 2009-2019 Figure 29: Restaurants - Transactions and Transactions per Outlet by Channel, 2009-2019 Figure 30: Retail - Transactions and Transactions per Outlet by Channel, 2009-2019 Figure 31: Workplace - Transactions and Transactions per Outlet by Channel, 2009-2019 Figure 32: Cost Sector: Channel share (%), 2014 vs. 2019 Figure 33: Cost Sector: Average Transaction Price (AED), 2009-2019 Figure 34: Cost Sector: Comparative Growth Analysis by Channels, 2009-2014 vs 2014-2019 Figure 35: Education- Sales (AED) and sales growth (%), 2009-2019 Figure 36: Healthcare- Sales (AED) and sales growth (%), 2009-2019 Figure 37: Military & Civil Defense - Sales (AED) and sales growth (%), 2009-2019 Figure 38: Welfare & Services - Sales (AED) and sales growth (%), 2009-2019 Figure 39: Cost Sector: Comparative Growth Analysis by Channels, Sales per Outlet & Number of Outlets, 2009- 2014 vs 2014-2019 Figure 40: Education - Outlets and Sales per Outlet by Channel (AED), 2009-2019 Figure 41: Healthcare - Outlets and Sales per Outlet by Channel (AED), 2009-2019 Figure 42: Military & Civil Defense - Outlets and Sales per Outlet by Channel (AED), 2009-2019 Figure 43: Welfare & Services – Outlets and Sales per Outlet by Channel (AED), 2009-2019 Figure 44: Cost Sector: Comparative Growth Analysis by Channels, Transactions per Outlet & Number of Transactions, 2009- 2014 vs 2014-2019 Figure 45: Education- Transactions and Transactions per Outlet by Channel, 2009-2019 Figure 46: Healthcare - Transactions and Transactions per Outlet by Channel, 2009-2019 Figure 47: Welfare & Services - Transactions and Transactions per Outlet by Channel, 2009-2019

List of Figures

11/08/2015 19 8/11/2015 19 8/11/2015 19 8/11/2015 19

List of Tables

Table 1: Leading Foodservice players in UAE, 2014 Table 2: Profit Sector Outlets, 2009-2014 Table 3: Cost Sector Outlets, 2009-2014 Table 4: Profit Sector Transactions (Million), 2009-2014 Table 5: Cost Sector Transactions (Million), 2009-2014 Table 6: Profit Sector Sales (AED Million), 2009-2014 Table 7: Cost Sector Sales (AED Million), 2009-2014 Table 8: Key Foodservice Definitions Table 9: Profit Sector Definitions Table 10: Cost Sector Definitions

List of Tables