Food as Placemaking - Rail~Volution

29

0 LELAND CONSULTING GROUP | Rail~Volution 2012 Rail~Volution 2012 | Brian Vanneman Food as Placemaking

Transcript of Food as Placemaking - Rail~Volution

0LELAND CONSULTING GROUP | Rail~Volution 2012Rail~Volution 2012 | Brian Vanneman

Food as Placemaking

1LELAND CONSULTING GROUP | Rail~Volution 2012

2000

100+ Cars2012

45+ Carts

www.andrewburdickphotography.com

www.andrewburdickphotography.com

“If you want to

seed a place

with activity,

put out food.”

Source: William Whyte.

"What South Waterfront really

needs is a grocery store."

Source: Tom Heinicke in Portland Mercury .

Food as

Placemaking

Strategy

Source: Project for Public Spaces.

“Coffee, food, bikes, beer, pinot noir.” – CEO, Act On Software

Grocery Stores

10LELAND CONSULTING GROUP | Rail~Volution 2012

DOWNTOWN HOUSTON SURVEY:

• “Residents and workers

consider a grocery store to

be the missing element of

downtown.”

• Grocery shopping

listed as the second most

popular leisure activity, after

listening to live music for

residents over 40.

11LELAND CONSULTING GROUP | Rail~Volution 2012

+ 17%

Source: Urban Living Infrastructure report, Metro, 2007.

Form follows rent

12LELAND CONSULTING GROUP | Rail~Volution 2012

Models

Portland Bungalow

1910s, 10 du/acre

Belmont Dairy

1996, Grocery & residential

Rowhouses

1999, 33 du/acre

Belmont Lofts

2004, 74 du/acre with retail

Belmont Neighborhood Center, Portland, OR

Highest apartment rents

Southeast Portland submarket

1996 - 2006

13LELAND CONSULTING GROUP | Rail~Volution 2012

Models

Orenco Station, Suburban TOD/Neighborhood Center

Development concept: "The ability to walk to a quart of milk"

14LELAND CONSULTING GROUP | Rail~Volution 2012

Models

Safeway, Museum Place

“Let There be Ralphs”

South Park/Downtown LA

Brewery Blocks, Portland

15LELAND CONSULTING GROUP | Rail~Volution 2012

Development Prospects

URBAN LAND INSTITUTE, 2010

• Development: “Write off the year,

as well as 2011 and Probably

2012.”

URBAN LAND INSTITUTE, 2012

• “For 2012, well situated grocery

anchored retail will do well.

• “Food and entertainment

become even more important for

driving traffic and sales.”

16LELAND CONSULTING GROUP | Rail~Volution 2012

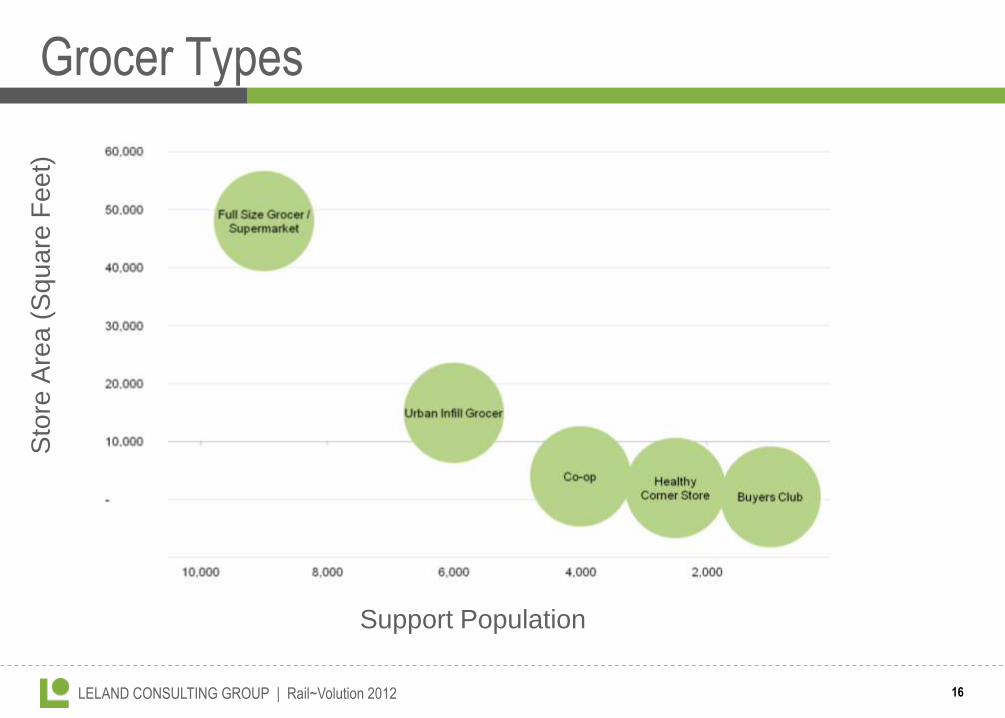

Grocer TypesS

tore

Are

a (

Sq

ua

re F

ee

t)

Support Population

17LELAND CONSULTING GROUP | Rail~Volution 2012

The Supermarket, 1950 - Present• 40,000 – 60,000 sf

• Site selection criteria vary!

• Location

• 15,000+ ADT

• Drive-home side

• Site size: 3 acres+

• Households

• 4,000+ in

primary market area,

“primary shoppers”

• Additional demand within 2

to 5 mi. radius

• Incomes

• Education

• Neighborhood revitalization

18LELAND CONSULTING GROUP | Rail~Volution 2012

Location

Source: Peter Calthorpe, 1993.

City

Center

19LELAND CONSULTING GROUP | Rail~Volution 2012

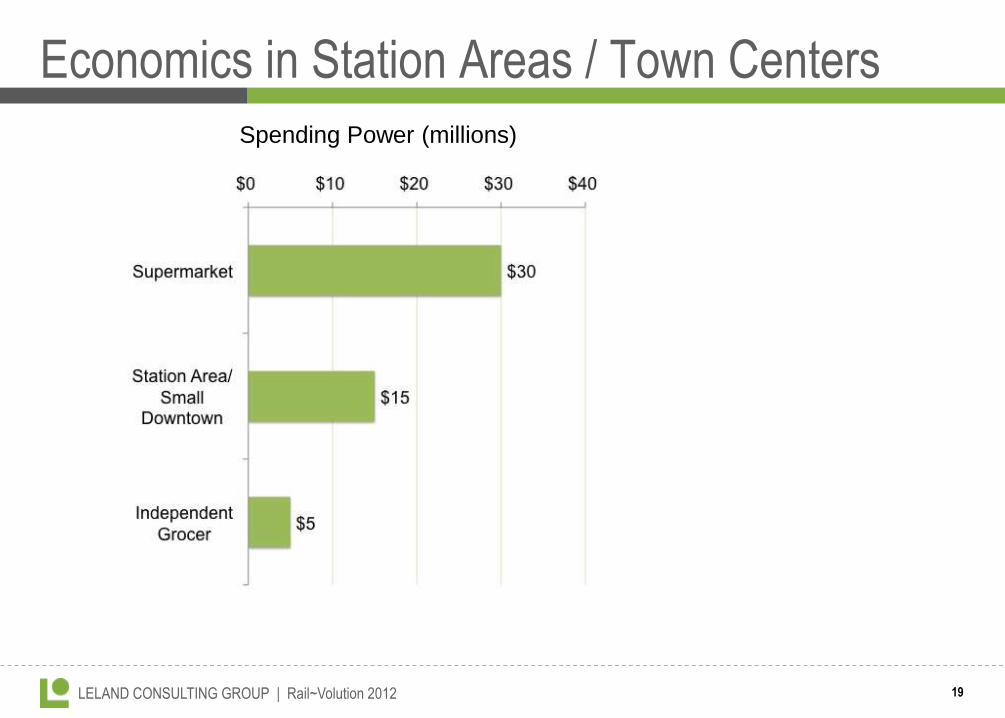

Economics in Station Areas / Town Centers

Spending Power (millions)

20LELAND CONSULTING GROUP | Rail~Volution 2012

Urban Infill Grocers

Fresh and Easy,

by Tesco, 13,000 sf

People’s Co-op,

Portland only, locally owned

The Market,

by Safeway

• Emerging, exciting format

• 3,000 – 15,000 sf

• Independents, mom and pops,

chains

21LELAND CONSULTING GROUP | Rail~Volution 2012

Parking

Caltrans,

ABAG/MTC

Parking

Standards

22LELAND CONSULTING GROUP | Rail~Volution 2012

Many Formats

• Co-ops

• Healthy Corner Stores

• Buyers Clubs

• Farmers Markets

• Public Markets

Weavers Way Co-op, Philadelphia

Public Market, San Francisco

23LELAND CONSULTING GROUP | Rail~Volution 2012

Shopping List

• Capture the opportunity as

neighborhoods revitalize,

transit arrives

• Pick the right location

• Research and explain the market

• Right size parking requirements

• Talk to grocer real estate

representatives

• Work with the right developer

• Use the public sector

development toolkit

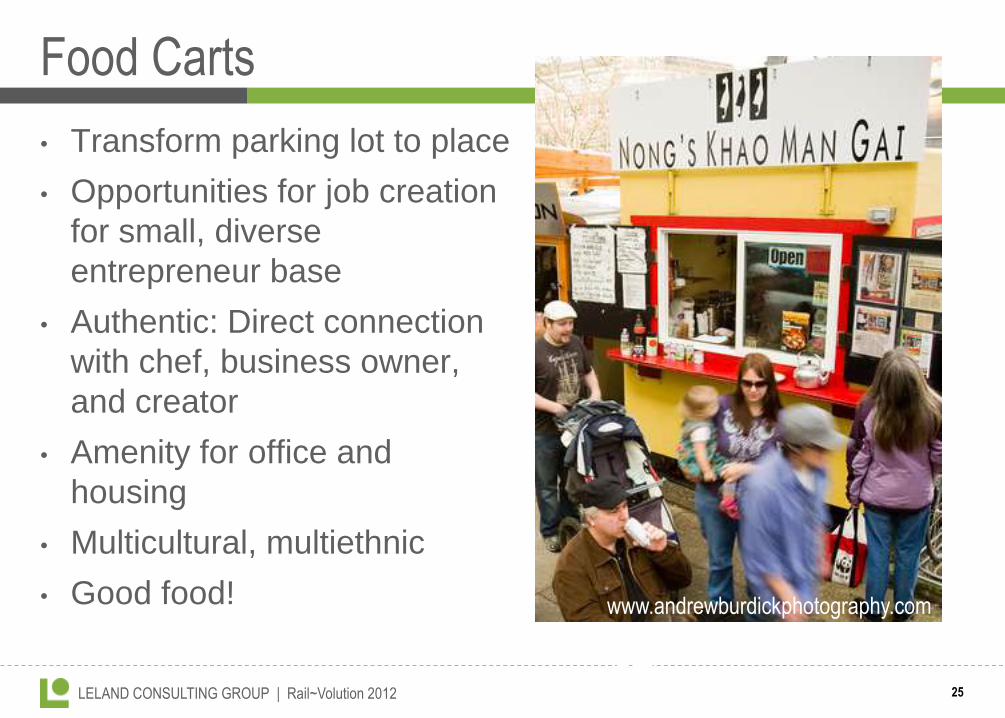

Food Carts

www.andrewburdickphotography.com

25LELAND CONSULTING GROUP | Rail~Volution 2012

Food Carts

• Transform parking lot to place

• Opportunities for job creation

for small, diverse

entrepreneur base

• Authentic: Direct connection

with chef, business owner,

and creator

• Amenity for office and

housing

• Multicultural, multiethnic

• Good food! www.andrewburdickphotography.com

26LELAND CONSULTING GROUP | Rail~Volution 2012

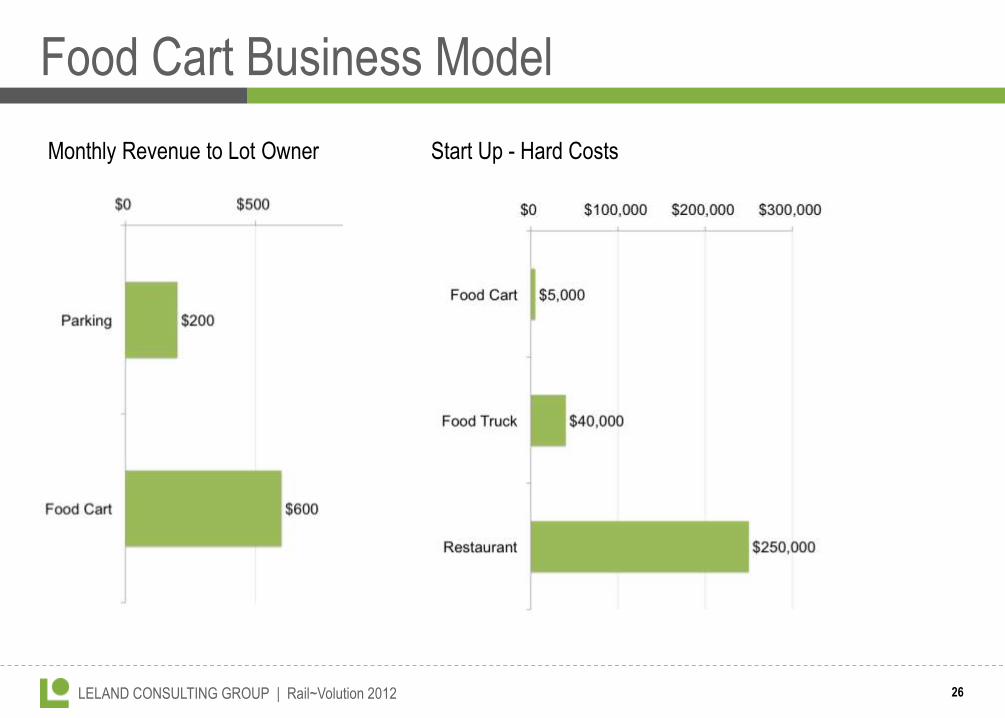

Food Cart Business Model

Monthly Revenue to Lot Owner Start Up - Hard Costs

27LELAND CONSULTING GROUP | Rail~Volution 2012

Regulation

• Portland

• 1 day, $800

• Food handlers’ license

• Business license

• Other Cities

• 1 or 2 hour time limit

• 200’ or more from

restaurant

• Permitting: Time

consuming and

expensive

LELAND CONSULTING GROUP

Real Estate Advisors / Urban Strategists

503.222.1600

www.lelandconsulting.com

![Volution, Fashion & Semiotics - Yoad.infoChapter 3: The Volution & Fashion 15 [The Volution in Fashion land] Chapter 4: The Volution & Semiotics 29 [You Can walk the (cat)walk but](https://static.fdocuments.in/doc/165x107/5f02118a7e708231d4026a99/volution-fashion-semiotics-yoad-chapter-3-the-volution-fashion.jpg)