Folio JR - Media Super Member PDS

72

Effective: 1 June 2009 print entertainment media arts MEMBER BOOKLET Product Disclosure Statement PART 1 of 2

-

Upload

jonathon-rann -

Category

Documents

-

view

219 -

download

3

description

An example of layout, tweak design, forms design and finished art

Transcript of Folio JR - Media Super Member PDS

Effective: 1 June 2009

printentertainment

mediaarts

member bookletProduct Disclosure Statement Part 1 of 2

This Product Disclosure Statement (PDS) effective June 2009 was prepared by Media Super Limited ABN 30 059 502 948, AFSL 230254 (Trustee), the trustee of Media Super. The PDS is made up of two parts. You should read all parts of the PDS before you make a decision to become a member of Media Super.

Part 1 of the Product Disclosure Statement contains important information about Media Super, including the features, costs, benefits and risks of Media Super.

Part 2 of the Product Disclosure Statement contains important information about the insurance arrangements offered to members of Media Super.

The PDS will help you decide whether or not Media Super will meet your needs and, if you have a choice, to compare Media Super with other superannuation funds.

An electronic copy of parts 1 and 2 of the Media Super PDS is available from www.mediasuper.com.au or by phoning 1800 640 886. If you make the Media Super PDS available to another person, you must give them the entire electronic file or printout, including both Part 1 and Part 2 and the application forms.

Please note: Some of the information contained in the Media Super PDS may change from time to time. If there is a materially adverse change, the Trustee will issue a new PDS or a Supplementary PDS. Where a change to the information in the PDS is not materially adverse, the Trustee will provide a written update on the website. You may request a printout of the update from the Trustee, who will provide it to you free of charge. The current version of the Media Super PDS is available at www.mediasuper.com.au or by phoning 1800 640 886.

General information warningThe information in this PDS is general information only. It does not take into account your individual objectives, financial situation or particular needs. Before making a decision to invest in Media Super, you should read the Media Super PDS in its entirety to assess whether or not Media Super is appropriate to your individual circumstances. We recommend that you also consider obtaining financial advice from a licensed financial adviser.

Investment returns are not guaranteed, as all investments carry some risk. Past performance gives no indication of future returns.

Financial product advice can only be provided by a financial services licensee or an authorised representative of a financial services licensee. Unless your employer holds a financial services licence, they are unable to provide you with any financial product advice or recommend any superannuation product to you.

All persons featured in this PDS have given their consent. This consent has not been withdrawn at the time of publication.

Note: All references to spouse and defacto relationships include same-sex couples.

Further informationUpon request to the Trustee, you are entitled to receive further information about Media Super. The Trustee will provide all information it reasonably believes a member would reasonably need to make an informed assessment of the management and financial situation of Media Super. If you require further information, contact us. The provision of further information may be subject to charge.

Visit www.mediasuper.com.au for further information.

Out of 200 super funds that SuperRatings surveys, only 15% are awarded a Platinum rating – the highest rating a super fund can achieve. We’re one of them.

Excellence gets results

Contact usGeneral enquiriesmail: Media Super Limited Locked Bag 1229, Wollongong NSW 2500

Phone: 1800 640 886

Fax: 1800 246 707

email: [email protected]

Website: www.mediasuper.com.au

3

Contents46

1622

36

Welcome to Media Super 4 Extra membership benefits 49

Your Super 6Making contributions 8Tax on super 12Accessing your super 15

Pensions 16Pension payments 18 Taxation on pensions 20

Investments 22Unitised investments explained 24Investment basics 25Your investor profile 26Your investment options 27Super investments and risk 34

General information 36Fees and other costs 38Other important information 42How to complete the forms 46

Look for Super Hero in this handbook for helpful tips and informationVisit www.mediasuper.com.au

Welcome to Media SuperThe industry super fund for print, media, entertainment and arts professionals.

4

5

Media Super was created on 1 July 2008 as a result of the merger of Print Super and JUST SUPER.

Both Print Super and JUST SUPER were established in 1987 and have long histories of low fees and strong performance.

We are run only to benefit+ you – the member. This means that Media Super rewards members with our low fees and strong long-term investment performance.

Strong PerformerAssets: more thAn $2.5 billion

Members:more thAn 115,000

low fees Strong long-term investment performance Super you can take from job to job market-leading pension products for retirement Personalised service from people who understand

your industry Flexible contribution arrangements Choice of 10 investment options regular communication insurance benefits (if you are eligible).

As a member of Media Super, you benefit from:

An Industry Super Fund that looks after you

About Industry Super FundsNot all super funds are the same. Industry Super Funds are run only to benefit members. This means that the Fund rewards members with low fees instead of paying financial planners and sales people commissions on your super. Over a 40-year working life, even small differences in fees can have a huge financial impact.

Media Super is governed by a Trustee Board of Directors. As an industry super fund, the Board is made up of an equal number of employer and employee representatives and two independent directors. The current Media Super Board of directors includes representatives from:

Printing Industries Association of Australia – three directors;

Fairfax Media Limited – one director;

Live Performance Australia or the Screen Producers Association of Australia – one director;

the Printing Division of the AMWU – three directors;

Media, Entertainment and Arts Alliance – two directors.

The role of the directors is to make sure that Media Super is run according to its Trust Deed and Rules (the document that controls Media

Super’s operation) and to act in the best interests of all members and beneficiaries. The Directors of Media Super (or the organisation they represent) are compensated for the time they spend on the management of Media Super. From time to time, the Trust Deed may need to be amended. If so, all members will be advised. A copy of the Trust Deed is available on request.

6 ‘We’re all in the same boat. It’s good to know we’re all together.’mathew barker, Web offset printer

Your super 7

Choosing Media Super means you are growing your retirement savings with a fund that understands the way you work.

Your super

We offer two types of super accounts:

EmPloyEr-SPonSorED accountIf your employer is a participating Media Super employer, you are considered an ‘Employer-sponsored member’ and should open this type of account.

to join:1. Complete the membership application form at the back of this PDS and either: A. send it to Media Super, or B. give it to your employer (who will send it to us with your next contribution).2. Complete the Standard choice form (if applicable) at the back of this PDS and return it to your employer.

1

PErSonal accountAnyone who is eligible to join a super fund can open this type of account. It is especially designed for self-employed, freelance and contract workers, as well as for people requiring spouse accounts or selecting Media Super under super choice where their employer is not a participating employer.If you open this type of account, you are considered a ‘personal account member’.For more information about super choice, see www.mediasuper.com.au/superchoice.

to join:1. Complete the membership application form at the back of this PDS and send it to Media Super

along with your first contribution.

2

Media Super offers eligible members with super accounts insurance cover for Death and Total and Permanent Disablement and Income Protection. The type of insurance we offer depends on your situation.Part 2 of the PDS outlines the applicable insurance arrangement. If you have not received Part 2 outlining your insurance arrangements, please phone 1800 640 886.

Important note

8 Your super

From 1 July 2009, non-wage remuneration will be included in income tests used to determine eligibility for a range of government financial assistance programs. Certain salary sacrifice superannuation contributions will be included as income for income testing purposes, as well as the self-employed 10% income test and the spouse contribution rebate income test. This change to income could affect your eligibility to receive the Federal Government Co-contribution and spouse rebate. If you are eligible for a co-contribution, it will continue to be automatically calculated by the Australian Taxation Office (ATO) and deposited into your super fund each year after you lodge your tax return.

concESSional contributionSConcessional contributions are pre-tax contributions paid by employers (or other eligible persons). Concessional contributions include:

Employer contributionsThe Superannuation Guarantee (SG) is the minimum amount of superannuation contributions that an employer is legally required to pay into a complying fund, such as Media Super, on behalf of an employee. Currently the minimum SG is 9% of Ordinary Time Earnings. Generally, if you are aged between 18 and 70 and earning more than $450 from an employer in a calendar month, you should be receiving SG contributions. Awards and industrial agreements may stipulate a higher employer contribution rate, or your employer may voluntarily choose to pay you additional superannuation.

Salary sacrificeSalary sacrifice involves making an agreement with your employer to sacrifice some of your pre-tax salary into your super account.Salary sacrificing into super can offer a number of advantages:

It lowers your taxable income. However, from 1 July 2009 any sacrificed salary will be included for relevant income testing.

Contributions up to certain limits will be taxed at 15% (not your marginal tax rate) – refer to page 12 for details.

You may benefit over the long term from the low-tax environment of super.

It may not substantially reduce your take-home pay.

Making contributions

Remember to clarify the terms of your salary sacrifice agreement with your employer to:

ensure that your 9% employer SG contributions are based on your pre-salary sacrifice salary;

check that entitlements such as long-service leave or loadings are not adversely affected.

If your employer offers a salary sacrifice option, make sure that your salary sacrifice agreement is in writing – Media Super has a sample agreement at www.mediasuper.com.au/forms to help you with this.

Generally, contributions fall into three categories: concessional contributions, non-concessional contributions and other contributions.

Your super 9

non-concESSional contributionSNon-concessional contributions generally come from an individual’s after-tax income. Non-concessional contributions include:

Voluntary contributionsVoluntary contributions are contributions that you choose to make out of your after-tax income (take-home pay). These contributions can be made as frequently as you like (up to the cap amount). The Voluntary contribution form is available at www.mediasuper.com.au/forms or by phoning 1800 640 886. See the ‘How to contribute’ table on page 11 for contribution methods.

Spouse contributionsSpouse contributions are designed to help build super for non-working or low-income partners.If you are married or in a defacto relationship* and make contributions on behalf of your spouse, you may be eligible for a tax rebate of up to $540.The spouse making the contribution will receive an 18% tax rebate on contributions (up to $3000 per year) where the receiving spouse earns less than $10,800 per year. If the receiving spouse earns more than $10,800 per year, a partial rebate applies before phasing out at incomes of $13,800 per year.To be eligible, you must be living together at the time; however, it doesn’t matter whether you are employed or not. Please also see the ‘Restrictions on receiving super contributions’ table on page 11 for age restrictions that apply. The rebate will be calculated by the Australian Taxation Office (ATO) when you lodge your tax return at the end of the financial year. To make a spouse contribution, simply complete the Spouse contribution form available from www.mediasuper.com.au/forms, and make a contribution into your spouse’s Media Super account.

* effective 1 July 2009 for people in defacto relationships.

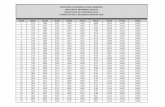

contribution caPSThere are limits on the amount of concessional and non-concessional contributions you can make each financial year, as shown in the table below.

budget ChangesThe Federal Government proposed changes to contribution limits in the May 2009 budget. If the budget changes are passed with no amendments then the ‘after budget’ contributions caps will apply for the 2009/10 year.

ContributionS CAP

2008-09 2009/10 (before budget)

2009/10 (after budget)

Concessional contributions cap

Under age 501 $50,000 $55,000 $25,000

Aged 50 or over2 (until 30/6/2012)

$100,000 $100,000 $50,000

non-concessional contributions

Annual cap3 $150,000 $165,000 $150,000

Three-year cap4 $450,000 $495,000 $450,000

1. these thresholds are indexed in line with movements in Average Weekly ordinary time earnings (AWote) in increments of $5,000.

2. this cap is not indexed.3. it is proposed that from 2009/10, this cap will be equal to six times the

concessional contributions cap.4. this cap only applies to individuals aged less than 65 in the financial

year they make the contribution. if you choose to exceed the annual cap, you will not be able to make any further contributions for the next two financial years.

note: For more information on how contributions are taxed, see the ‘Tax on super’ section on page 12.

if you are self-employed and wish to claim a tax deduction for contributions AnD make a super split, by law you must claim the tax deduction beFore lodging your super splitting application.

Hint

Self-employed contributions

If you are self-employed – or substantially self-employed (that is, you earn less than 10% of your income, including assessable income, reportable fringe benefits and employer super contributions, from an employer) – you can make contributions to super and claim a full tax deduction. These contributions will then be treated as concessional contributions.Please note that if you don’t claim your super contributions as a tax deduction, they will be regarded as after-tax, voluntary non-concessional contributions, and thus you may be eligible for the Government Co-contribution (see opposite). For full details on claiming a tax deduction, see page 14.

10 Your super

Co-contributionThe co-contribution is a payment made by the Federal Government for low and middle-income earners. The payment is designed to reward those who make an additional contribution to their super, on top of what their employer contributes.

budget ChangesThe Federal Government proposed changes to the maximum co-contribution limit in the May 2009 budget. If the budget changes are passed with no amendments then the maximum co-contribution limit will reduce from $1,500 to $1,000. For example, until 30 June 2009, if you earn less than $60,342* per annum and make a voluntary super contribution (see page 9), you may be eligible for a co-contribution of up to $1,500. The maximum co-contribution of $1,500 applies for people earning up to $30,342* who have made a voluntary super contribution of $1,000 to their super account. The amount of co-contribution reduces for incomes above $30,342*.From 1 July 2009, the maximum co-contribution will be $1000. See the table below for co-contribution matching rates.

Contribution yeAr

mAtChinG rAte mAximum Co-Contribution

2009/10 100% $1,000

2010/11 100% $1,000

2011/12 100% $1,000

2012/13 125% $1,250

2013/14 125% $1,250

2014/15 150% $1,500

If you are eligible for a co-contribution, it will be automatically calculated by the Australian Taxation Office (ATO) and deposited in your super fund each year after you lodge your tax return.For assistance on calculating the level of co-contribution that you’re eligible for, try the Co-contribution calculator at www.mediasuper.com.au/calculators.* these amounts are indexed annually. the figures shown here apply

for 2008/09. For 2009/10 figures, visit www.ato.gov.au.

Employment Termination PaymentsEmployment Termination Payments (ETP) – such as unused sick leave, amounts of time in lieu, golden handshake and employment invalidity payments – cannot be rolled into super unless the following transitional conditions are met:

The payment was specified as part of an existing employment contract, law or agreement as at 9 May 2006; and

The payment is made before 1 July 2012.

othEr contributionS

Super splittingYou may be able to split superannuation with your spouse. Super splitting is only available for concessional contributions. Members can split 85% of concessional contributions up to the annual concessional contributions cap. Media Super requires that a minimum of $1,000 be split and also that your account balance cannot be less than $5,000 after the split. Please note that the amount transferred to your spouse’s super account does not reduce the concessional contributions counted towards your cap.See the ‘Important notes’ section on page 11 for restrictions.You can make only one super splitting application per year. To split your super, request a super splitting pack from us by phoning 1800 640 886. This pack will contain a statement showing the concessional contributions we received from you in the previous financial year and the maximum amount you can split, as well as a form for you to advise us how you wish to split your super. A $30 withdrawal fee applies to super splits being sent to a non-Media Super account.

RolloverA rollover is super that you transfer from another super fund you belong to. Given the nature of their employment, many Media Super members have accumulated multiple super accounts over the years. Multiple super accounts equal multiple super fees. Consolidating your super into one account can help you build your retirement savings faster. It also reduces the hassle of managing multiple super accounts. To make Media Super the home for your super, simply roll over your other super accounts using the rollover form at the back of this PDS.

Your super 11

How to contribute

methoD SuitAble For WhAt to Do

Direct Debit – enables a specified amount to be deducted from your bank account monthly and paid into your Media Super account.

• Voluntary contributions

• Self-employed contributions

• Spouse contributions

Complete the Direct debit request form and Spouse contribution form (if applicable) and return them to Media Super.

eFt – You can transfer amounts directly from your bank account to Media Super.

• Voluntary contributions

• Self-employed contributions

• Spouse contributions

Contact us on 1800 640 886 to establish an EFT arrangement.

Cheque – for regular or one-off payments into your Media Super account.

• Voluntary contributions

• Self-employed contributions

• Spouse contributions

Send your cheque to Media Super along with any relevant paperwork (e.g. Voluntary contribution form or Spouse contribution form). At a minimum, your cheque must be accompanied by your membership number or it will be returned.

Payroll – your employer will adjust your pay (according to your instructions) and send contributions to Media Super on your behalf.

• Voluntary contributions

• Salary sacrifice

Find out if your employer offers this service. If so, sign and return to your employer the Payroll deduction authority form.

If you intend to claim a tax deduction for self-employed contributions, see page 14 for further requirements.

Restrictions on receiving super contributions

Contribution tyPeyour AGe

leSS thAn 65 65-69 70-74 75+

mandated employer contribution1

Accepted without restriction

Accepted without restriction

Accepted without restriction

Accepted without restriction

Additional employer contribution2

Accepted without restriction

Accepted provided you are gainfully employed on at least a part-time3 basis.

Accepted provided you are gainfully employed on at least a part-time3 basis.

Cannot be accepted5

Voluntary contribution Accepted without restriction

Accepted provided you are gainfully employed on at least a part-time3 basis.

Accepted provided you are gainfully employed on at least a part-time3 basis.

Cannot be accepted5

Spouse contribution Accepted without restriction

Accepted provided the receiving spouse is gainfully employed on at least a part-time3 basis.

Cannot be accepted Cannot be accepted

Government co-contribution Accepted without restriction

Accepted without restriction4

Cannot be accepted Cannot be accepted

1. includes SG (to age 70 only) and contributions stipulated by Awards and Agreements.2. includes additional employer contributions, salary sacrifice contributions and self-employed contributions where a tax deduction has been claimed.3. Part-time means you must have worked at least 40 hours in 30 consecutive days in the financial year. 4. the co-contribution will only be paid in line with a period where you were eligible to make voluntary contributions.5. if you are gainfully employed on at least a part-time basis during the financial year that contributions are made, contributions received on or before

the day that is 28 days after the end of the month in which you turn 75 can be accepted.

important notes: • Super-splitting transfers cannot be received by a spouse who is aged 65 years or more, or has reached their Preservation Age and is retired.• Further restrictions on receiving contributions may apply if you have not supplied your tax file number. See page 12 for details.• There are no restrictions on receiving a rollover.

12 Your super

tax FilE numbErS

Different rules apply if Media Super does not have your tax file number (TFN) recorded, including an additional tax of 31.5%, including Medicare levy, on top of your normal 15% contributions tax – a total of 46.5% tax.If you do not provide Media Super with your TFN, you will pay the higher tax on all employer and salary sacrifice contributions and Media Super will not be able to accept any other contributions on your behalf.As a member of Media Super, it is your responsibility to ensure that Media Super has your TFN on file. If your employer has neglected to supply your TFN, you will still be subjected to additional tax.The additional tax will be deducted directly from your Media Super account, either at the end of the financial year or when any part of your account balance is withdrawn, whichever occurs first. Provided that you supply us with a valid TFN within three years of the end of the financial year that the contributions are made, you may be entitled to a refund of the additional tax. No interest will be earned while the additional tax is held at the Australian Taxation Office (ATO). Please note that refunds are subject to processing by the ATO.To supply your TFN to Media Super, simply visit www.mediasuper.com.au/tfn or phone 1800 640 886.

tax on contributionS

Tax on concessional contributionsConcessional contributions, up to the concessional contribution cap, are taxed at 15%.If you make contributions across multiple super funds and the total exceeds the contribution cap, the excess contributions will be taxed at the highest marginal tax rate (plus Medicare levy) – currently 46.5%.If you exceed the relevant cap, the ATO will write to you advising you of the additional tax. You can choose to pay this additional tax from either your superannuation account or another source. You will be required to advise the ATO of your choice and to pay in the timeframe advised.

Tax on non-concessional contributionsnon-concessional contributions, up to the concessional contribution cap, are not taxed in the Fund.You can make up to $150,000* (for the 2008/09 and 2009/10 financial years) of non-concessional contributions to your super account each year. Media Super is not permitted to receive contributions from you in excess of the cap.If you make contributions across multiple super funds and the total exceeds the contribution caps, the excess contributions will be taxed at the highest marginal tax rate (plus Medicare levy) – currently 46.5%.If you breach the non-concessional contribution cap, the ATO will write to you and advise you of the additional tax, which will be deducted directly from your nominated superannuation account.

Tax on other contribution typesThere is no tax applicable for Government co-contributions or super-splitting transfers for the receiving spouse.Rollovers will not be taxed unless an untaxed rollover amount (previously called a ‘post June 1983 untaxed element’) is included, which will be taxed at 15%. Generally, this is only applicable if you are transferring from an untaxed superannuation fund. For Media Super members, tax has already been deducted by us, so this tax will not apply if you roll over your account to another fund.

tax on lumP Sum amountS

Tax when super is paid in cashIf you are aged 60 years or over, you can access your superannuation with Media Super entirely tax-free. If you have reached your preservation age (see page 15), but are still under 60, you can still access the taxable component of your super tax-free up to the low-rate threshold ($145,000 for 2008/09 increasing to $150,000 for 2009/10). Amounts over the low-rate threshold will be taxed according to the table opposite. People who have not yet reached their preservation age and are eligible to gain access to their super will also be taxed according to the table shown opposite.

The information in this section generally explains the different types of tax that may apply to your super.

Tax on superEnsure that Media Super has your tax file number on record. If the Fund doesn’t and you don’t supply it, you may be subject to additional tax.

Don’t forget!

Your super 13

Tax on Terminal Illness benefits If you have been diagnosed by two medical practitioners (one needs to be a specialist) that you are terminally ill and are not expected to live beyond 12 months, and your benefit is paid as a lump sum, it will be tax-free.

EliGiblE tEmPorary rESiDEntSIf you are an eligible temporary resident (not an Australian or New Zealand citizen) and permanently leave Australia, your lump sum benefits will be taxed as follows:

Tax-free component – No tax payable

Taxable component – Up to 35%There are restrictions on when you can access your super as an eligible temporary resident. For more information see page 44.

Tax on Total and Permanent Disablement (TPD ) benefitsIf you receive a super TPD benefit and are aged 60 years and over, you can access your superannuation entirely tax-free.If you are not yet 60, part of your normal taxable component will be recalculated to form part of your tax-free component. Generally, the tax-free component is increased to reflect the period where you could have expected to be gainfully employed if the disability had not occurred. This amount is calculated based on your age, length of service and the amount of your benefit. Your adjusted tax-free and taxable components will be taxed at the rates shown in the table below.

Tax on Death benefitsIf your Death benefit is paid to a dependant for tax purposes, then the benefit is tax-free. If it is paid to a non-dependant, tax is deducted from the taxable component of the benefit at a rate of 16.5% (including Medicare levy). A higher rate will apply if the Death benefit recipient does not provide their TFN to Media Super.Any untaxed element of a taxable component of a lump sum Death benefit, where the benefit included life insurance proceeds, will be taxed at 31.5% (including Medicare levy). The untaxed element is the proportion of your total lump sum Death benefit that relates to the period from the date of death to age 65 in comparison with your total service period.

Tax on Pension payments and benefitsFor information about the applicable tax when your benefit is paid as a pension, see page 17 in the ‘Pensions’ section.

Tax on lump sum super

ComPonent AGe PAymentS tAx rAteS

tax-free All All Nil

taxable Under your preservation age

All Maximum of 21.5%

Your preservation age to 59

Up to $145,000*

Nil

59 Over $145,000*

Maximum of 16.5%

60+ All Nil

important notes: • TheMedicarelevyisincluded.• Higherratesoftaxapplytoanuntaxedrolloveramount.MediaSuper

would deduct tax on receipt of a rollover containing an untaxed amount, and the remainder would then form part of the standard taxable component.

• Ifyouhaven’tadvisedMediaSuperofyourtaxfilenumber,highertaxrates may apply.

* the figure of $145,000 will increase to $150,000 for the 2009/10 year.

14 Your super

tax on inVEStmEnt EarninGSAny investment earnings (returns) on your super are taxed at 15%, less any available tax credits. This tax is deducted from Media Super’s earnings and remitted to the ATO before earning rates are declared and allocated to your account. Earnings may be positive or negative.

GooDS anD SErVicES tax (GSt)Under current GST legislation, GST does not apply to super contributions, rollovers, earnings applied to members’ accounts or benefits paid. Media Super may, however, be required to pay GST on goods and services.

incomE ProtEction bEnEFitSIncome Protection benefits are regarded as taxable income and attract PAYG tax (the same tax that applies to salary and wages). This will be deducted and remitted to the ATO before you receive the benefit. You will be required to supply your TFN when receiving an Income Protection benefit, otherwise you will be taxed at the highest marginal tax rate plus Medicare Levy.

SurcharGEThe superannuation surcharge was abolished from 1 July 2005; however, the surcharge may still be payable for periods prior to that date.If the ATO assesses that you are liable to pay a superannuation surcharge, it will advise Media Super, and payment will be deducted from your account.

DEDuctionS For thE SElF-EmPloyEDTax deductions for the self-employed are only available for contributions paid to a complying fund such as Media Super or a retirement savings account.To be eligible for a self-employed tax deduction, you must earn less than 10% of your income, including assessable income and reportable fringe benefits, from an employer. While you can claim a tax deduction for all your super contributions in your tax return, the ATO will apply additional tax if your super contributions exceed the relevant concessional and non-concessional caps.You can only use deductions for your super contributions to reduce your taxable income to nil – you cannot add to, or create a loss for, your business through contributing.

How to claim a tax deductionIf you have made super contributions into your Media Super account and wish to claim a tax deduction, you will need to notify us before the earlier of:

the date when you lodge your tax return for the year the contributions were made; or

the end of the financial year immediately following the financial year in which you made the contributions.

You will need to request an Ato Section 290-170 form to be sent to you. This form details the amount you have paid in super contributions during the year. To claim a tax deduction, you must complete the form, return it to Media Super and receive acknowledgment of the amount from Media Super.If you operate a company, it is the company that claims the full deduction, so no Section 290-170 form applies. Super contributions made by the company are treated as employer contributions.

Important information

Generally speaking, your personal super contributions should not be taxed if you do not notify Media Super that you intend to claim a deduction.

The Ato Section 290-170 form enables you to notify Media Super of the amount you will claim as a deduction. We then provide you with an acknowledgement as proof of your notification. The ATO may require this proof that you have notified us of your intention before it allows the deduction.

Super contributions tax will be calculated on the amount that you are claiming as a tax deduction. The tax will be deducted from your Media Super account and sent to the ATO.

Your super 15

Accessing your super

PaymEnt oF bEnEFitSBenefits are generally paid as a lump sum. However, some benefits may be paid as a pension. If you have reached your preservation age, you may also request that Media Super pays your benefit as a pension.For more information on pensions, go to page 17.

claiminG your SuPEr bEnEFitIf you believe that you satisfy a condition of release and would like to access your superannuation, contact Media Super on 1800 640 886. We will send you the relevant forms.Note that specific requirements apply to each condition of release, and a $30 fee may apply.

PortabilityIf you wish to roll part of your account balance out of Media Super into another fund, at least $5,000 must remain in your Media Super account and you can only make one such withdrawal each year. If there are insufficient funds to meet your insurance premiums, your insurance cover will cease.

PrESErVation oF bEnEFitSSuperannuation is designed as a long-term investment for your retirement, so there are strict rules about when you can access your super. This generally means all contributions and any investment earnings made to your account since 1 July 1999 are preserved. That is, they must stay invested in super until you satisfy a condition of release.If you accumulated benefits before 1 July 1999, some of your super does not need to be preserved. This includes restricted non-preserved benefits that can generally be paid to you on termination of employment and/or unrestricted non-preserved benefits that can be paid to you at any time.Conditions of release include your:

permanent retirement from the workforce on or after your preservation age (see table below);

termination of employment after turning age 60 (without necessarily retiring permanently);

reaching age 65 (whether you are retired or not); death (benefits are paid to your dependants or

personal legal representative); permanent incapacity; diagnosis of a terminal medical condition; severe financial hardship; eligibility for approval on compassionate grounds by the

Australian Prudential Regulatory Authority; termination of employment with an employer-sponsor

where your preserved amount is less than $200; permanent departure from Australia if you are an

eligible temporary resident (see page 44 for more information);

satisfying any other condition of release as specified in superannuation law.

Your preservation age varies between 55 and 60 years, depending on your date of birth (see table).

Benefits at retirement

DAte oF birth PreSerVAtion AGe

Before 1/7/60 55

1/7/60 to 30/6/61 56

1/7/61 to 30/6/62 57

1/7/62 to 30/6/63 58

1/7/63 to 30/6/64 59

After 30/6/64 60

If you are aged 55 years or over, you may be able to access part of your superannuation account balance through a transition to retirement Pension, even if you’re still working. See the Pensions section on page 17 for more details.

Did you know?

16

‘I am still earning money, but I am now also getting money from my Media Super Pension, which is absolutely super.’robert Suggett, Photographer

Pensions 17Pensions 17

Intro text

PensionsConvert your super savings to a flexible, tax-effective Media Super pension. You can choose your pension amount and frequency, and pay no tax on investment earnings.

Pensions

Starting a Pension with Media Super is easy

1. Make sure you have read and understood this PDS.2. Complete the Pension member application form at the

back of this PDS.3. If you need to transfer money from another super fund,

complete the rollover form at the back of this PDS before your pension commences.

4. Post your completed forms, along with Certified ID to: media Super, locked bag 1229, Wollongong nSW 2500.

Media Super offers two types of pensions:

rEtirEmEnt PEnSionSuitable for those who have at least $10,000 of super money to invest, and:

have reached their preservation age (see page 15), and are fully retired; or have retired due to Total and Permanent Disablement (TPD) or permanent incapacity; or are aged 60 or more and have left employment; or are aged 65 or over.

1

tranSition to rEtirEmEnt PEnSionSuitable for those who have at least $10,000 of super money to invest, and:

have reached their preservation age (see page 15), and are still working and would like access to super at the same time.

2

18 Pensions

A pension with Media Super gives you the flexibility to choose your payment amount and frequency.

Pension payments

how much incomE can i rEcEiVE?

Retirement PensionA minimum income payment applies each financial year, depending on your age and your account balance on 1 July of that year. There is no maximum payment.For the financial year ending 30 June 2009, the Federal Government suspended the minimum draw-down requirements for account-based pensions – a 50% reduction in the minimum payment amount.Members must draw down 50% of the minimum payment for 2008/09 (and the budget proposes to extend this to the 2009/10 financial year). If any member has already withdrawn 50% of the minimum payment, they are not required to draw down again until the end of the applicable financial year.

Transition to Retirement PensionA minimum income payment applies each financial year, depending on your age and your account balance on 1 July of that year. You can receive up to a maximum of 10% of your account balance each year.The table below details the minimum yearly payment. However, if the budget changes are passed then the figures in the right column will apply.

Your minimum yearly income

AGe

minimum yeArly PAyment (% oF ACCount bAlAnCe AS At 1 July)

buDGet ProPoSeD minimum yeArly PAyment (% oF ACCount bAlAnCe AS At 1 July) For the FinAnCiAl yeAr 2009/10

Under 65 4% 2%

65-74 5% 2.5%

75-79 6% 3%

80-84 7% 3.5%

85-89 9% 4.5%

90-94 11% 5.5%

95+ 14% 7%

Each year on 1 July, your new minimum and maximum (if applicable) limits will be recalculated using your new account balance and age. We will send you a letter advising you of your new minimum and maximum (if applicable) limits. We will also seek your instructions regarding your preferred income level and payment frequency.

can i maKE aDDitional withDrawalS?Once you have started your pension, there may be times when you need extra money to cover unexpected or unplanned expenses.Media Super Retirement Pension members are able to make lump sum withdrawals in addition to their nominated pension payment amount. Transition to Retirement Pension members can only make lump sum withdrawals in limited circumstances, including if they:

reach age 65; retire permanently on, or after, their preservation age

(see page 15); reach age 60 and leave employment; become totally and permanently disabled or

permanently incapacitated; are diagnosed with a ‘terminal medical condition’; or are required to pay a Contributions Surcharge or

superannuation-related tax liability.People under the age of 60 should be aware that there may be tax implications for making additional lump sum withdrawals – see ‘Taxation on pensions’ on page 20. You can make a partial or full withdrawal, if eligible, using the benefit request form, available at www.mediasuper.com.au/forms or by phoning 1800 640 886. Payments will be made, after tax is deducted (if applicable), by cheque or EFT to your nominated bank account. A $30 fee may apply.

how oFtEn can i rEcEiVE PaymEntS?With Media Super, you can choose the frequency of your payments.

Payments

PAyment FrequenCy 15th DAy oF*

Monthly Each month

Quarterly September, December, March, June

Six-monthly December and June

Yearly June

* If the 15th day of the month falls on a weekend or public holiday, the pension payment will be made on the last business day preceding the 15th.

Pensions 19

You can change the frequency of your pension payments at any time by completing and returning the Change of details – Pension account form at the back of this PDS.You must receive at least one pension payment each year, within your minimum and maximum (if applicable) limits.

your FirSt PEnSion PaymEntIf you commence your pension on or after 1 June in any year, then no minimum payment is required to be paid to you in that financial year.

how will i rEcEiVE PaymEntS?Your payments will be credited directly to your nominated bank account or financial institution or can be paid by cheque.

can i inVESt morE monEy in my PEnSion?Once you have opened a pension, you cannot add any additional funds to it. However, you can open another pension with other super money you may have.

how lonG will my PEnSion laSt?Your pension may not provide you with an income for the rest of your life. If your account balance reaches zero, your payments will cease and your account will close. How long your pension payments continue will depend on many factors, including whether or not you choose to receive above the minimum level of payment, the level of returns on investments, and your lump sum withdrawals.

can i Still rEcEiVE a Social SEcurity PEnSion iF i commEncE a SuPErannuation PEnSion?Generally, you may still be eligible to receive a Social Security Age Pension along with your Media Super pension depending on your individual circumstances. However, it is important to note that your Media Super pension payments are considered as income for the purposes of the Social Security Age Pension income test. Also, the balance of your Media Super pension is considered as an assessable asset for the purposes of the Social Security assets test. Before commencing a Media Super pension, the Trustee recommends that you seek advice from a licensed financial adviser.

can i nominatE a rEVErSionary bEnEFiciary?A reversionary beneficiary is the person who will receive the balance of your death benefit as an income stream. Only spouses, certain children and interdependants are eligible to become reversionary beneficiaries. A child can only be a reversionary beneficiary if they are:

under the age of 18; or aged 18-25 and financially dependent; or suffering from a disability.

If your reversionary beneficiary is a child under the age of 18 at the date of your death, they can only receive your pension as an income stream until they turn 25, at which point they must convert the remaining pension into a tax-free lump sum, unless they suffer from a disability.You can nominate ONE person as a reversionary beneficiary. If you want to change your reversionary beneficiary, you will need to cancel your existing pension and commence a new pension. A valid reversionary benefit nomination is binding on Media Super.

20 Pensions

The tax applied to your pension depends on your age. If you are aged 60 years or more, any income, additional payments and investment returns from your pension are entirely tax-free. If you are under 60, then tax applies to pension income payments and benefits (see below), but investment returns are still entirely tax-free.

tax on incomETax componentsYour pension balance is made up of two components – the taxable component, and the tax-free component. As their names suggest, the taxable component attracts tax, while the tax-free component doesn’t.The proportion of these two components is calculated when you start your pension. This fixed proportion then applies to each payment you receive.if you reach your preservation age (aged 55 to 59), your pension payments will be taxed as follows:

Tax-free component is tax-free. Taxable component is taxed with PAYG tax plus

the Medicare Levy, less 15% pension offset.if you are aged under 55, your pension payment will be taxed as follows:

Tax-free component is tax-free. Taxable component is taxed with PAYG

tax plus the Medicare Levy (no tax offset).In some circumstances, individuals under 55 may be eligible for the tax pension offset (for example, if the pension is paid because of death or permanent incapacity).For further information, visit www.ato.gov.au.

PAYG taxIf you are under 60, you will be taxed PAYG (Pay As You Go) tax on the income you receive from your pension. This is the same tax that applies to salary and wages.We will deduct the appropriate amount of tax from the payments you receive and pay it to the Australian Taxation Office (ATO).

tax on aDDitional withDrawalSIf you made additional lump sum withdrawals from your pension, these will be taxed as a lump sum (see page 12 for details). This only applies to additional withdrawals from your pension. Regular payments from a pension within the applicable minimum and maximum limits are not liable for this tax.

tax on inVEStmEnt EarninGSYour investment earnings are entirely tax-free.

tax on commEncEmEntIf any part of the superannuation you use to start your pension consists of an untaxed rollover amount (previously a post June 1983 untaxed element), this portion will be taxed at 15%. Generally, this is only applicable if you are transferring from an untaxed super fund. For most members, tax has already been deducted by their super fund, so this tax will not be applicable.

SuPErannuation SurcharGE taxThe superannuation surcharge tax was abolished from 1 July 2005; however, the surcharge may still be payable for periods prior to this date. If the ATO assesses that you are liable to pay a superannuation surcharge, you will be required to pay this directly. If you need to withdraw additional funds from your pension to pay the surcharge, that withdrawal will be tax-free.

With Media Super, you pay no tax on the investment earnings of your pension, but there may be a number of other taxes applicable.

Taxation on pensions

Pensions 21

bEnEFiciariES anD PEnSionSBeneficiaries and PensionsIf your pension commenced after 1 July 2007, the following rules apply.

How will my pension be paid in the event of my death?How your pension is paid to the recipient will depend on their circumstances and relationship to you.Your pension may continue to be paid in regular payments if the recipient is a dependant. It’s important to note that for a child to receive your pension in this way, they must satisfy one of these requirements:

be aged under 18 years; be financially dependent and aged under 25 years; or have a disability as defined under the Disability

Services Act.Alternatively, your dependant can elect to receive their benefit as a lump sum.If your beneficiary is not a dependant, or is a child who doesn’t meet one of the requirements outlined previously, your pension will be paid to them as a lump sum. They cannot receive it in regular payments.

Will my beneficiary pay tax on my pension?The taxation applied to your pension on your death depends on the circumstances of you and your beneficiary, as well as how the pension is paid.If the benefit is paid as a pension, and you OR the beneficiary is aged 60 years or over, the pension will be paid entirely tax-free. If you AND the reversionary beneficiary are under 60 at the time of death, the pension will be taxed as follows:

the tax-free component is tax free; the taxable component is assessable income (i.e. it will

be taxed at the reversionary beneficiary’s Marginal Tax Rate) but the reversionary beneficiary is entitled to a tax offset equal to 15% of the taxable component; and

when the dependant turns 60, the income stream is tax free,

at the revisionary beneficiary’s Marginal Tax Rate (less any tax-free amount and pension tax offset). Otherwise, it will be tax-free. Where the pension is taxable, it will become tax-free when the reversionary beneficiary turns 60.If the benefit is paid as a lump sum, see ‘Tax on Death benefits’ on page 13 for taxation details.

22

‘I now view super as a priority and contribute each month into my account.’Priscilla nielsen, Freelance illustrator

Investments 23

We understand that members have different investment requirements. That’s why Media Super allows you to select an investment strategy designed to assist you in achieving your retirement goals.

Investments

Are there restrictions on how much I can invest in each option?You can invest your entire account balance in one option or choose any combination of some or all of the 10 options. There is no minimum or maximum amount you can invest in any one option.

When can I make an investment choice?With Media Super, you have the flexibility to make an investment choice at any time. As your personal or financial circumstances change, you can change your investment strategy accordingly. Note: the buy and sell unit prices on the day your switch is processed will be applied.

What is the cost of making a choice?Each time you make or change your investment choice, a $30 fee is charged to your account.

Can I invest my future contributions differently to my existing account balance?Yes. You can select one investment strategy for your existing account balance, and another strategy for future contributions paid into your account.

Why make a choice?How you invest your super can have a significant impact on your final super account balance.

What are my choices?Media Super members have the choice of four pre-mixed investment options and six asset-specific investment options – including a sustainable future option. You will find full details of our options on pages 27 to 33.

What is the right choice for me?The investment choice you make will depend on your personal circumstances. It’s important that you understand the basics of investing (page 25) and the risks associated with investment (page 34) and also consider your investor profile (page 26) before making an investment choice.

What if I don’t make a choice?If you don’t make a choice, your superannuation or pension will be invested in the Balanced option.

How do I make an investment choice?You can make an investment choice at any time. Making an investment choice is easy. Once you’ve read this PDS and know how you wish to invest, simply use the membership application form or Change of details form to let us know your investment choice. Alternatively, you can log on to your account at www.mediasuper.com.au and submit your choice there.As of 1 May 2009, your investment choice will be processed on the Thursday following the week it is requested. The week is calculated from Monday to Sunday. Any investment choice made between Monday and Sunday will be processed on the Thursday of the following week (e.g. if you request a change on Sunday, 10 May, it will be processed on Thursday, 14 May).

24 Investments

Unit prices go up or down depending on the value of the investments within each of the 10 available options. Influences include rental receipts, dividends, fixed interest payments and asset values.This means that the total value of your investment in Media Super is determined by multiplying the number of units you have in each of the Media Super investment options by the price of each unit in the particular investment option. You can calculate the current value of your super investment at any time by multiplying the number of units you hold in each investment option by the latest published sell price.The investment return will depend on the investment option selected and the buy price applicable at the time of buying into that investment option, i.e. at the time each contribution is made. If you make an enquiry about your account balance, the balance quoted will be based on the sell price.Unit prices for each of the Media Super investment options are updated on a weekly basis. You can access updated prices at www.mediasuper.com.au or by phoning 1800 640 886.The Trustee reserves the right to change any unit price when it sees it is in the best interests of all members invested in that investment option. The Trustee will advise you of the performance of each of the investment options as part of its regular reporting requirements and to assist you in comparing the returns to industry benchmarks.

The Media Super investment options operate using a unitised system. You may be familiar with this kind of system if you have invested money in a personal investment product such as a managed fund.

Unitised investments explained

Example: Unitised investments

If you have 25,000 units in Media Super’s Balanced option valued at $1.04 per unit and 25,000 units in the Growth option valued at $1.02 per unit, then your total superannuation investment would be valued at:

balanced Growth total25,000 x $1.04 + 25,000 x $1.02 = $51,500

buyinG anD SEllinG unitSWhen you change or switch your investment option or mix of investment options, you are, in effect, buying and selling units. As such, your investment will be affected by the buy and sell price that applies on the date your switch is made. A separate buy and sell unit price is quoted for each investment option on a weekly basis after allowing for fees, taxes and buy-sell spreads on the Media Super underlying investments. See the Fees and other costs section on page 38 for details of the buy-sell spreads of each option. Note: Different unit prices apply to super and pensions, as pension prices do not allow for tax on investment earnings.

LABoUR STANDARDS AND ENVIRoNMENTAL, SoCIAL AND ETHICAL CoNSIDERATIoNSThe Trustee selects investments and investment managers on the basis of potential financial return for its members and does not take into account labour standards or environmental, social or ethical considerations (the Standards) for the purpose of selecting, retaining or realising investments except to the extent that it appoints investment managers in respect of its Sustainable Future Shares investment option with a mandate to consider such Standards as part of meeting the investment objectives of the Sustainable Future Shares investment option.For information on our Sustainable Future Shares option see our Sustainable Future Shares Investment Guide dated 2 February 2009. The purpose of this guide is to provide you with detailed information about the Sustainable Future Shares option, including information about:

which Standards are taken into account; the extent to which the Standards are taken

into account; and the retention and realisation policies.

You may receive a copy of this document free of charge by:

phoning or writing to us and requesting a copy of document number SFS100 05/08;

downloading a copy from our website. Visit www.mediasuper.com.au/sustainableinvest.

Investments 25

Before becoming an active super investor, it is worth familiarising yourself with the investment basics we cover in this section.

Investment basics

ASSetS investments are generally divided into two types – defensive assets and growth assets. Growth assets carry higher risk, but can deliver higher returns over the long term. Defensive assets generally carry less risk, and can therefore be used to protect your investment against loss. however, defensive assets generally deliver lower returns over the long term, and can deliver poor returns in certain environments.MediaSuper’sinvestmentoptionsprovideyouwiththechoiceyouneedtocreatethebestmixofinvestmentstobuildaportfolioyou’recomfortablewith.Themixofoptionsyouchooseshouldbedeterminedbyyourinvestmentobjectives.

SharesCompanies listed on a stock exchange issue shares (also known as equities or stocks) to raise capital. You become a shareholder and part-owner of the company when you purchase ordinary shares in a company. That means that you are entitled to dividend payments when the company decides there are earnings available for distribution to shareholders. Company performance (including debt levels), industry conditions or movements in the share market can affect the share price and make it rise and fall.

PropertyLand and buildings that can be bought, sold or leased are known as property. Investing in property through a super fund lets you and other members pool your money to enable you to part own properties that would otherwise be too expensive for you to aquire on your own, for example, office buildings and shopping centres. Property includes investments in property trusts, which may be listed on the stock exchange. Like shares, the value of property is influenced by many factors, including supply and demand and market conditions.

Fixed interestWhen an investor lends money to governments, semi-government bodies and corporations, interest is paid at an agreed rate which is fixed for the term of the loan. These investments are known as bonds on fixed interest. Fixed interest investments can be held until they mature or they can be traded at any time before maturity. If they are sold before maturity, the price will depend on the interest rate at the time. Returns from fixed interest investments occur from regular interest payments and any change in value caused by movements, either up or down, in interest rates. Fixed interest is usually a more stable investment than shares, but this depends on the investment environment.

CashInvestments in cash include money invested in term deposits or bank bills. Interest is earned on the cash invested. This is similar to having money in a bank account. Over the long term, cash is likely to produce the lowest return of all the main asset classes.

Alternative assetsAlternative assets generally comprise those investments which do not fit within traditional broad asset classes (such as shares, property, fixed interest and cash). Examples may include absolute return funds (e.g. hedge funds), private equity, infrastructure, property development, etc. Some alternative assets may be considered to have more growth than defensive characteristics, and vice-versa. Media Super reviews each asset class to determine where it best fits.

overseas investmentsFor some options, Media Super invests overseas. When investing overseas, returns can also be affected by changes in the value of the Australian dollar. These changes can enhance overseas returns (when the Australian dollar is falling and there is no currency hedging) or detract from overseas returns (when the Australian dollar is rising and there is no currency hedging). Currency hedging protects overseas investment returns from movements in the Australian dollar.

Sustainable investmentsSocially responsible or sustainable investments are made in assets which are aligned with more sustainable and socially responsible outcomes. They may be selected based on environmental, social and/or economic factors. To achieve the appropriate level of portfolio diversification, they may also include companies that are leaders within their industry sector.

26 Investment

inVEStmEnt timEFramEYou need to consider your investment timeframe when selecting investment products. Your investment timeframe is the length of time before you will want to access your investment. It is generally accepted that the longer your investment timeframe, the more risk you can afford to take.

riSK anD rEturnYour super is invested in financial markets. Therefore, you are exposed to investment risk.Investment risk is the degree to which returns go up and down in value over time. You cannot consider return without risk and, generally, the higher the potential return, the higher the risk. In order to achieve higher returns, you must be willing to take on more risk. While shares, property and fixed interest securities historically offer higher long-term returns than cash, they also expose you to higher levels of risk, particularly in the short term. The variability of returns is a risk associated with investment, and the assets that offer higher potential return generally have the highest fluctuations in returns. The assets that have a lower risk (and lower potential return) generally have less pronounced fluctuations in returns.In financial terms, there is also a risk of not having enough assets or money to provide you with the lifestyle you desire in retirement. Therefore, if you try to avoid investment risk altogether, you may have to save more for your retirement.

Read this section to help understand the things you should consider when selecting an investment strategy tailored for your situation.

Your tolerance to risk is an important factor to consider before making your investment choice. Everyone has a different tolerance to risk, and you need to be comfortable with the level of risk that is associated with the investment option or mix of investment options that you choose.The risk/return profile of each of Media Super’s options is determined by the percentage allocated to growth assets relative to defensive assets. The greater the proportion of growth assets, the riskier the investment becomes, but the greater the potential return in the longer term.See page 34 for further information on risks.

DiVErSiFicationDiversifying or spreading your investments across a range of individual assets, asset classes, countries or investment managers has the potential, over time, to smooth out any ups and downs in investment returns, as it is unlikely that all asset classes will have negative returns at the same time.

Your investor profile

that you consider investment risk, return and diversification before making an investment choice.

We recommend...

Investments 27

Media Super members can choose from four pre-mixed options and six single asset options or you can mix and match to design your own investment portfolio by simply combining our investment options in the proportions you choose.

imPortAnt noteSThe long-term strategic asset allocation for each option is outlined on the following pages. The underlying asset allocation for each option will vary according to the investment managers’ day-to-day asset allocation decisions.Returns are shown for each investment option, after fees and taxes. The return you receive will depend on when you invested in the option and market movements. The yearly returns detailed on the following pages are the actual returns earned for each applicable year. The five-year average figures are the compound average figures for each applicable investment option.The investment objectives of our options outline our aims and are not indicative of their actual returns. Over rolling five-year periods, each option will aim at a return that falls above the median in the SuperRatings survey (or equivalent) of comparable funds. All probabilities of achieving a crediting rate equivalent to inflation will be measured by the change in the Australian Consumer Price Index.Media Super was created on 1 July 2008 following the merger of Print Super and JUST SUPER. The historical investment returns detailed on the following pages are those of the previous Print Super investment options. To view historical investment returns for JUST SUPER to 30 June 2008, visit www.mediasuper.com.au/justsuper.Past performance is not an indicator of future performance. You should also expect the returns on each of your investment options to vary over time due to fluctuations in the value of investments with each investment option.

If you choose to invest 35% in balanced and 65% in Growth, you will achieve just over 80% exposure to growth assets and almost 20% to defensive assets.

bAlAnCeD GroWth totAl

Growth assets

35% of 73.5% = 25.72%

+ 65% of 85% = 55.25%

= 80.97%

Defensive assets

35% of 26.5% = 9.28%

+ 65% of 15% = 9.75%

= 19.03%

If you choose to invest 30% in Sustainable Future Shares and 70% in balanced, you will achieve just over 80% exposure to growth assets and almost 20% to defensive assets.

SuStAinAble Future ShAreS bAlAnCeD totAl

Growth assets

30% of 100% = 30%

+ 70% of 73.5% = 51.45%

= 81.45%

Defensive assets

30% of 0% = 0%

+ 70% of 26.5% = 18.55%

= 18.55%

Mix & match Mix and match to choose more than one investment option or create a diverse portfolio with your investments spread across many options. You can choose any mixture of pre-mixed and single asset investment options to match your own investment strategy.

Here are just two examples (see investment mix for profiles of these options on pages 28, 30 and 32).

or

note: calculations are based on long-term strategic allocations only, and will not affect each actual investment.

Your investment options

Rememberthe higher your exposure to growth assets, such as shares and property, the riskier your portfolio will be over any given period. but, at the same time, you are increasing the likelihood of achieving higher returns over the long term.

Pre-mixed or single asset optionsPre-mixed options allow you to diversify your investments with ease. Each of the four pre-mixed options have different asset allocations designed to certain risk profiles and with particular investment objectives in mind. Choose from Balanced, High Growth, Growth and Stable.

Single asset options allow you to choose exactly which assets you want your super invested in at any time. You may choose a single asset option if, for example, you only want to invest in sustainable shares.

28 Investments

Pre-mixed

Balanced – the Default optioninvestment mix

risk profile Medium to high risk

investment objectivesOver rolling five-year periods having a 75% probability of achieving a crediting rate equivalent to inflation, plus 3.5% per annum. The estimated chance that negative returns will occur, after tax and fees, in any financial year is less than one in nine.

investment strategyBalanced offers a significant exposure to growth assets (73.5%), including Australian and overseas shares, property and alternative assets (illiquid assets). The 26.5% allocation to defensive assets includes Australian and overseas fixed-interest securities, alternative assets, hedged funds and cash.

investment time horizonMedium to long (5–10 years)

Asset allocationThe underlying asset allocation for Balanced will vary in line with the investment managers’ day-to-day asset allocation decisions around their benchmark positions. The long-term strategic asset allocation for Balanced is illustrated in the pie chart above.

ASSET SECToR

STRATEGIC ASSET

ALLoCATIoN %

RANGES %

GroWth

Australian Shares 32.0 22-42

Australian Private Equity 2.0 0-5

Overseas Shares (Unhedged) 20.0 10-30

Overseas Shares (Hedged) 2.0 0-5

International Private Equity 3.0 0-6

Absolute Return Strategies (Growth)

3.0 0-6

Infrastructure* 6.0 3-9

Direct Property* 3.5 1-6

Real Estate Investment Trusts 2.0 0-5

DeFenSiVe

Absolute Return Strategies (Defensive)

3.0 0-6

Australian Fixed Interest 6.0 0-12

International Fixed Interest (Hedged)

4.0 0-8

Cash 4.0 0-8

Infrastructure* 6.0 3-9

Direct Property* 3.5 1-6

*Note: Growth assets and Defensive assets include 50% each of both Infrastructure and Direct Property investments.

investment returns to 30 June (% net return p.a.)

RETURNS SUPER %

PENSIoN %

INfLATIoN %

2003/04 13.9 13.9 2.5

2004/05 13.1 15.1 2.5

2005/06 14.5 16.4 4.0

2006/07 15.3 16.9 2.1

2007/08 -6.5 -8.6 4.5

5-year average (compound) 9.7 10.3 3.1

73.5% Growth

26.5% Defensive

Investments 29

High Growthinvestment mix

risk profileVery high risk

investment objectivesOver rolling five-year periods having a 65% probability of achieving a crediting rate equivalent to inflation, plus 5% per annum. The estimated chance that negative returns will occur, after tax and fees, in any financial year is less than one in six.

investment strategyHigh Growth provides a high growth-oriented investment strategy, with 98% invested in growth assets such as shares and 2% invested in defensive assets (cash).

investment time horizonVery long (15+ years)

Asset allocationThe underlying asset allocation for High Growth will vary in line with the investment managers’ day-to-day asset allocation decisions around their benchmark’s position. The long-term strategic asset allocation for High Growth is illustrated in the pie chart above.

ASSET SECToR

STRATEGIC ASSET

ALLoCATIoN %

RANGES %

GroWth

Australian Shares 43.0 33-53

Australian Private Equity 4.0 0-8

Overseas Shares (Unhedged) 32.7 23-43

Overseas Shares (Hedged) 3.3 0-6

International Private Equity 5.0 0-10

Absolute Return Strategies (Growth)

10.0 0-15

Infrastructure* 0.0 0

Direct Property* 0.0 0

Real Estate Investment Trusts 0.0 0

DeFenSiVe

Absolute Return Strategies (Defensive)

0.0 0

Australian Fixed Interest 0.0 0

International Fixed Interest (Hedged)

0.0 0

Cash 2.0 0-5

Infrastructure* 0.0 0

Direct Property* 0.0 0

*Note: Growth assets and Defensive assets include 50% each of both Infrastructure and Direct Property investments.

investment returns to 30 June (% net return p.a.)

RETURNS SUPER %

PENSIoN %

INfLATIoN %

2003/04 19.7 19.6 2.5

2004/05 17.0 19.0 2.5

2005/06 19.9 22.3 4.0

2006/07 20.0 21.6 2.1

2007/08 -11.8 -15.0 4.5

5-year average (compound) 12.2 12.5 3.1

98% Growth

2% Defensive

30 Investments

Growthinvestment mix

risk profile High risk

investment objectives Over rolling five-year periods having a 65% probability of achieving a crediting rate equivalent to inflation, plus 4.5% per annum. The estimated chance that negative returns will occur, after tax and fees, in any financial year is less than one in seven.

investment strategyGrowth provides a growth-oriented investment mix, with an 85% allocation to growth assets.

investment time horizonLong (10+ years)

Asset allocationThe underlying asset allocation for Growth will vary in line with the investment managers’ day-to-day asset allocation decisions around their benchmark positions. The long-term strategic asset allocation for Growth is illustrated in the pie chart above.

ASSET SECToR

STRATEGIC ASSET

ALLoCATIoN %

RANGES %

GroWth

Australian Shares 37.0 27-47

Australian Private Equity 3.0 0-5

Overseas Shares (Unhedged) 24.5 15-35

Overseas Shares (Hedged) 2.5 0-5

International Private Equity 4.0 0-8

Absolute Return Strategies (Growth) 8.0 0-12

Infrastructure* 3.5 0-6

Direct Property* 1.5 0-2.5

Real Estate Investment Trusts 1.0 0-3

DeFenSiVe

Absolute Return Strategies (Defensive) 0.0 0

Australian Fixed Interest 3.5 0-7

International Fixed Interest (Hedged) 2.5 0-5

Cash 4.0 0-8

Infrastructure* 3.5 0-6

Direct Property* 1.5 0-2.5

*Note: Growth assets and Defensive assets include 50% each of both Infrastructure and Direct Property investments.

investment returns to 30 June (% net return p.a.)

RETURNS SUPER %

PENSIoN %

INfLATIoN %

2003/04 16.2 16.4 2.5

2004/05 13.9 15.9 2.5

2005/06 17.0 19.1 4.0

2006/07 17.5 19.2 2.1

2007/08 -8.6 -11.2 4.5

5-year average (compound) 10.7 11.2 3.1

85% Growth

15% Defensive

Investments 31

Stableinvestment mix

risk profile Medium risk

investment objectivesOver rolling five-year periods having a 80% probability of achieving a crediting rate equivalent to inflation, plus 2.5% per annum. The estimated chance that negative returns will occur, after tax and fees, in any financial year is less than one in 20.

investment strategyStable aims to provide relatively steady overseas returns through a 69.5% allocation to defensive assets.

investment time horizonShort to medium (under 5 years)

Asset allocationThe underlying asset allocation for Stable will vary in line with the investment managers’ day-to-day asset allocation decisions around their benchmark positions. The long-term strategic asset allocation for Stable is illustrated in the pie chart above.

ASSET SECToR

STRATEGIC ASSET

ALLoCATIoN %

RANGES %

GroWth

Australian Shares 13.0 6-20

Australian Private Equity 0.0 0

Overseas Shares (Unhedged) 8.2 3-13

Overseas Shares (Hedged) 0.8 0-2

International Private Equity 0.0 0

Absolute Return Strategies (Growth) 0.0 0

Infrastructure* 4.5 2-7

Direct Property* 2.0 0-4

Real Estate Investment Trusts 2.0 0-5

DeFenSiVe

Absolute Return Strategies (Defensive) 5.0 0-10

Australian Fixed Interest 17.0 10-24

International Fixed Interest (Hedged) 11.0 6-16

Cash 30.0 20-40

Infrastructure* 4.5 2-7

Direct Property* 2.0 0-4

*Note: Growth assets and Defensive assets include 50% each of both Infrastructure and Direct Property investments.

investment returns to 30 June (% net return p.a.)

RETURNS SUPER %

PENSIoN %

INfLATIoN %

2003/04 7.7 7.5 2.5

2004/05 9.3 11.7 2.5

2005/06 8.7 8.6 4.0

2006/07 9.5 11.1 2.1

2007/08 0.0 -0.6 4.5

5-year average (compund) 7.0 7.6 3.1

69.5% Defensive

30.5% Growth

32 Investments

Australian Sharesrisk profileVery high risk

investment objectivesOver rolling five-year periods having a 60% probability of achieving a crediting rate equivalent to inflation, plus 5% per annum. The estimated chance that negative returns will occur, after tax and fees, in any financial year is less than one in four.

investment strategyThe Australian Shares sector option provides a high growth-oriented investment strategy predominantly invested in Australian shares.

investment time horizonVery long (15+ years)

Asset allocation

ASSET SECToR STRATEGIC ASSET ALLoCATIoN %

RANGES %

GroWth

Australian Shares 100.0 95-100

DeFenSiVe

Cash 0 0-5

investment returns to 30 June (% net return p.a.)

RETURNS SUPER %

PENSIoN %

INfLATIoN %

2005/06 22.0 24.0 4.0

2006/07 23.8 25.2 2.1

2007/08 -10.0 -12.5 4.5

This option commenced on 1 April 2005.

Overseas Sharesrisk profileVery high risk

investment objectivesOver rolling five-year periods having a 55% probability of achieving a crediting rate equivalent to inflation, plus 5% per annum. The estimated chance that negative returns will occur, after tax and fees, in any financial year is less than one in four.

investment strategyThe Overseas Shares sector option provides a high growth-oriented investment strategy predominantly invested in overseas shares.

investment time horizonVery long (15+ years)

Asset allocation

ASSET SECToR STRATEGIC ASSET ALLoCATIoN %

RANGES %

GroWth

Overseas Shares (Unhedged) 91.0 80-100

Overseas Shares (Hedged) 9.0 0-20

DeFenSiVe

Cash 0 0-5

investment returns to 30 June (% net return p.a.)

RETURNS SUPER %

PENSIoN %

INfLATIoN %

2005/06 17.9 21.8 4.0

2006/07 12.4 14.5 2.1

2007/08 -14.0 -17.3 4.5

This option commenced on 1 April 2005.

Sustainable Future Sharesrisk profileVery high risk

investment objectivesOver rolling five-year periods having a 60% probability of achieving a crediting rate equivalent to inflation, plus 5% per annum. The estimated chance that negative returns will occur, after tax and fees, in any financial year is less than one in four.

investment strategyThe Sustainable Future Shares sector option provides a high growth-oriented investment strategy predominantly invested in Socially Responsible Australian and overseas shares.

investment time horizonVery long (15+ years)

Asset allocation

ASSET SECToR STRATEGIC ASSET ALLoCATIoN %

RANGES %

GroWth

Australian Shares 60.0 50-70

Overseas Shares (Unhedged) 40.0 30-50

DeFenSiVe

Cash 0 0-5

investment returns to 30 June (% net return p.a.)

RETURNS SUPER %

PENSIoN %

INfLATIoN %

2005/06 21.6* 23.4* 4.0

2006/07 19.0 20.6 2.1

2007/08 -13.4 -16.4 4.5

This option commenced on 1 August 2005.* The 2005/06 figure represents the return for the period from 1 August

2005 to 30 June 2006.

Single assets

Investments 33

Propertyrisk profileMedium to high risk

investment objectivesOver rolling five-year periods having a 70% probability of achieving a crediting rate equivalent to inflation, plus 3.5% per annum. The estimated chance that negative returns will occur, after tax and fees, in any financial year is less than one in 10.

investment strategyThe Property sector option provides a growth-oriented investment strategy predominantly invested in property.

investment time horizonLong (10+ years)

Asset allocation

ASSET SECToR STRATEGIC ASSET ALLoCATIoN %

RANGES %

GroWth

Direct Property 75.0 65-85

Real Estate Investment Trusts 25.0 15-35