Flanders Language Valley; Industrial Districts and...

28

1 Contact authors at: René Wintjes MERIT, University Maastricht, Postbus 616, 6200 MD Maastricht [email protected] Tel: (31) (0) 43-3883893 Flanders Language Valley; Industrial Districts and Localized Technological Change 1 René Wintjes & Jan Cobbenhagen MERIT, Maastricht University Postbus 616, 6200 MD Maastricht December 1999 Abstract This case study questions how Flanders Language Valley developed as a cluster of localized technological change. Through licensing the attracted small, mostly foreign firms use the research lab of L&H Speech Products as a common source of codified knowledge and with their fast entrepreneurial reaction they complement it by developing a broad range of applications. Subsequently, the created favorable communication conditions induced innovative linkages between the attracted SMEs. Like the Silicon Valley role-model, a strong pilot firm, venture capital, education and most of all the informal networking were critical to the development of FLV. Companies ‘find’ each other at FLV to their mutual advantage. They learn from each other and benefit from developing and using common pools of resources in proximity, e.g., companies find employees in the ‘collective pool of labour’ created by several education and training programmes. 1 This paper is written under the EU TSER project "Industrial districts and localised technological knowledge" (INLOCO). We thank Robin Cowan and Claire Nauwelaers and those attending the Nice Seminar of the INLOCO research group for comments on a previous version of this paper.

Transcript of Flanders Language Valley; Industrial Districts and...

1

Contact authors at:René WintjesMERIT, University Maastricht,Postbus 616, 6200 MD [email protected]: (31) (0) 43-3883893

Flanders Language Valley; Industrial Districts andLocalized Technological Change 1

René Wintjes & Jan Cobbenhagen

MERIT, Maastricht University

Postbus 616, 6200 MD Maastricht

December 1999

Abstract

This case study questions how Flanders Language Valley developed as a

cluster of localized technological change. Through licensing the attracted

small, mostly foreign firms use the research lab of L&H Speech Products as

a common source of codified knowledge and with their fast entrepreneurial

reaction they complement it by developing a broad range of applications.

Subsequently, the created favorable communication conditions induced

innovative linkages between the attracted SMEs. Like the Silicon Valley

role-model, a strong pilot firm, venture capital, education and most of all

the informal networking were critical to the development of FLV.

Companies ‘find’ each other at FLV to their mutual advantage. They learn

from each other and benefit from developing and using common pools of

resources in proximity, e.g., companies find employees in the ‘collective

pool of labour’ created by several education and training programmes.

1 This paper is written under the EU TSER project "Industrial districts and localised technologicalknowledge" (INLOCO). We thank Robin Cowan and Claire Nauwelaers and those attending the Nice Seminarof the INLOCO research group for comments on a previous version of this paper.

2

1 Introduction

Based on the presence of Lernout & Hauspie Speech Products (L&H) as the core

technological firm, and the availability of multi-lingual engineers and highly educated

linguists in the Belgian province of West Flanders, the Flanders Language Valley (FLV)

initiative was launched to create a world-wide centre of competence in speech and language

technologies. Following the model of Silicon Valley, a number of local actors sought to build

an ICT-valley in the small, rural town of Ieper. In order to do so, a venture capital fund - the

FLV Fund - focusing on speech and language related technology applications was established

in 1995. After just three years of dynamic technological clustering through licensing, and

financial clustering through participations, several language and speech related technology

firms have clustered in a geographical sense. At present there are some 34 fast growing,

innovative, FLV firms which are supported by the incubation services of the FLV

Foundation2 and another fifty additional companies (foreign as well as indigenous) are

expected to join. In 1999 the first group of firms have located at a 65-acre business in Ieper,

Some firms have relocate from temporary locations elsewhere in Ieper, but most firms will be

‘green-field’ investments as subsidiaries of mostly foreign companies. Many of these firms

are pioneering firms themselves, originating from technological districts like Boston and

Silicon Valley. To use the words of Amin & Thrift (1992) it looks like Ieper has become a

neo-Marshallian node in a global network of interlinked districts. In spite of its peripheral

position, the Ieper area is now the European centre of speech and language technology that

currently attracts more than one new company per month, drawing people and capital from all

over the world.

Two things are particularly striking about FLV, however. In the first place, we ask why it is

that this clustering of innovation has taken place in such a small, relatively isolated rural

area? Secondly, why does geographical proximity remain important when many licence

arrangements reveal tradable technological interdependencies, that is, knowledge which

seems codifiable and which could be sold through licences?

Like the Silicon Valley role-model, three factors have been acknowledged as critical to the

development of FLV: a strong pilot firm at the centre of a localised network, venture capital,

and education. These factors are considered to be the three pillars of this now highly

specialised cluster. To analyse the process of technological, financial and geographical

2 As of november 1999 the FLV Foundation is renamed “S.A.I.L. Trust”. With FLV as the first “S.A.I.L.Port”, the foundation will replicate and localize the FLV concept in 9 international centers of excellence, aimingfor a worldwide network of centers for the development of Speech, Artificial Intelligence and Language (SAIL)technologies. In 2000 the next ‘ports’ will be located in Norway and Singapore. There are contacts andagreements for ‘ports’ in Israel, Hungary and US East Coast, and plans for Japan, US West Coast, SouthAmerica and South Africa (SAIL, White Paper, version november 1999, http://www.s-ai-l.com)

3

clustering of innovation, we begin with a description of the local and regional context from

which FLV arose. We then focus on L&H as the originating and principal firm, and speech

products as the technological core. A discussion of the formation of FLV and the FLV Fund

follows, including an account of the involvement of the FLV companies. Finally, we discuss

the role of the FLV Foundation and public policy. At present Flanders Language Valley itself

has become a role-model for Flanders ‘clusterpolicy’3 and especially the recent policy

innitiative which goes by the name of ‘technology-valleys’.

2 Ieper, a small town in West-Flanders, Belgium

With 35.000 inhabitants the city of Ieper is one of the smaller centres in the Belgian province

of West Flanders. Kortrijk, Brugge and Oostende are becoming the dominant cities in West-

Flanders, a NUTS level 2 region that is bordered by East Flanders, the sea and France. As a

whole West Flanders has a broad-based economic structure and it is well known for its large

number of small and medium-sized enterprises, with high export rates. Among West-

Flanders’ major assets are the entrepreneurial climate, language skills, high level of education

and work ethic of the labour force.

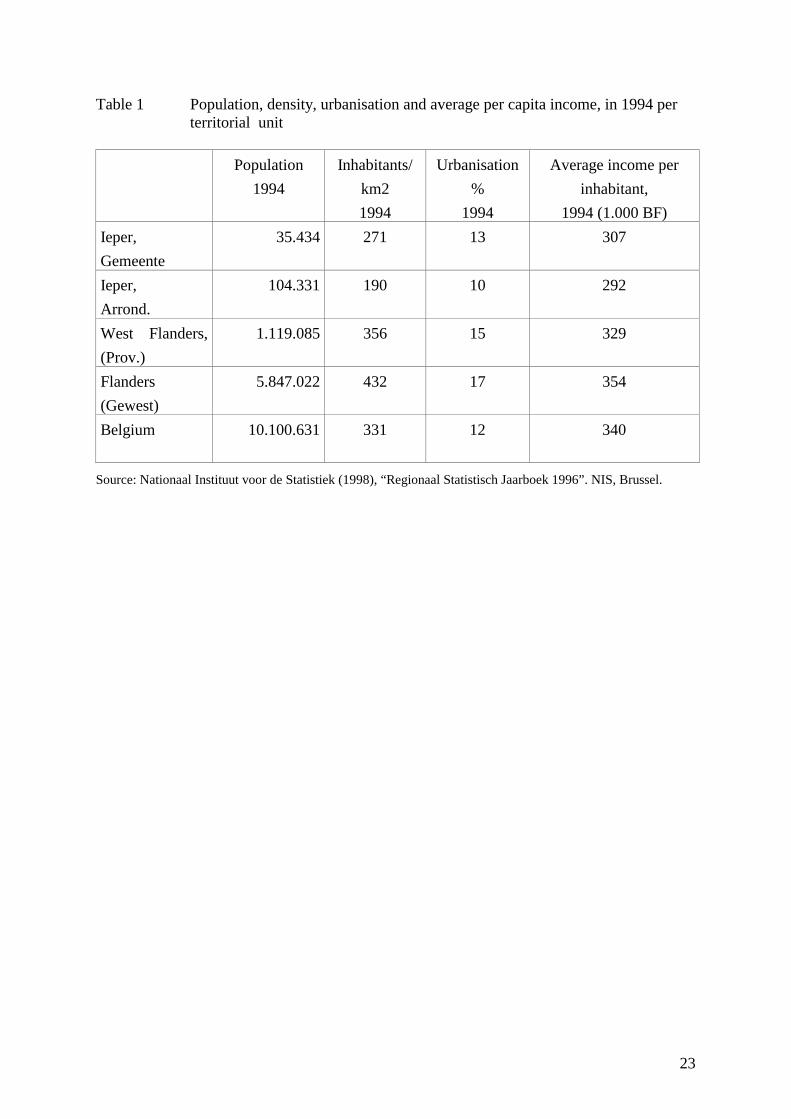

[Insert about here]

[Table 1 Population, density, urbanisation and average per capita

income, in 1994 per territorial unit]

Unlike West-Flanders as a whole, however, the Ieper area (NUTS level 3) has a more lop-

sided industrial structure. Situated in an agricultural outpost known as the Westhoek, it is

characterised by all the disadvantages of an off-centre position. Up to West Flanders’

standards the Ieper area (arrondissement) is sparsely populated with a low level of

urbanisation (table 1). Agriculture is still an important sector for the local economy of the

Ieper area, e.g. 34 percent of the firms were engaged in agriculture in 1994. The economy of

the Ieper area is restructuring, however, and the average anual growth of GDP between 1986

and 1996 has been relatively high compared to the rest of the Province, Gewest, and the

country (table 2). Located close to France the area has the characteristics of a border region,

e.g. the main road stops in Ieper. Helped by several decades of government aid and support

from the European Community, the Westhoek region has undergone a remarkable revival.

3 Vlaamse regering, Minister-President L.Van den Brande (1998), ‘Valleien aan het werk, werk in devalei; De Vlaamse regering: katalysator voor technologievalleien’. Vlaamse regering: Brussel; Vlaamseregering, Minister-President L.Van den Brande (1999), ‘Het Vlaamse Wetenschaps-, Technologie- enInnovatiebeleid; Beleidsbrief voor het jaar 1999’. Vlaamse regering: Brussel.

4

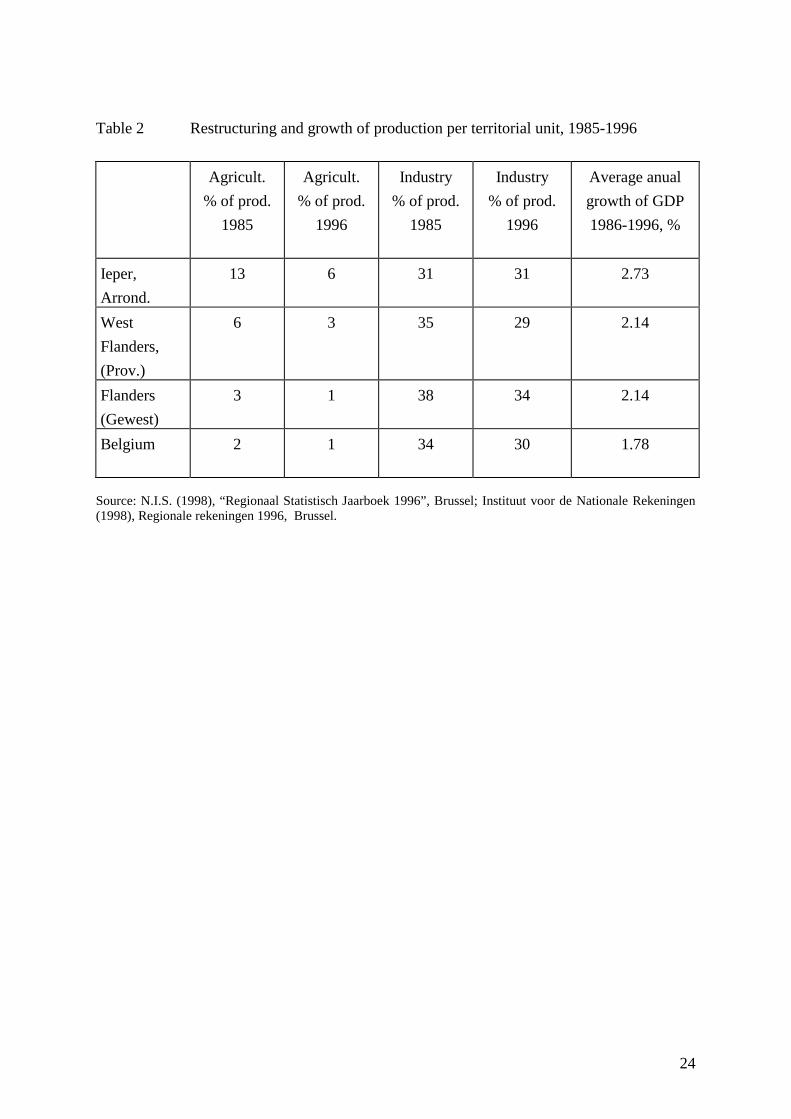

[Insert about here]

[Table 2 Restructuring and growth of production per territorial unit,

1985-1996]

Several authors have characterised the economic development in the southern part of West-

Flanders as endogenous growth or autonomous industrialisation (Musyck 1993)4, originating

from new start-ups and growth of indigenous single plant family firms. Accumulated family

capital and strong entrepreneurial spirit are the critical factors behind the success of this part

of West Flanders. Musyck (1993) identified the regional specificity and embeddedness of

capital and labour as contributing factors. Small and medium sized enterprises dominate the

economy, while the dominant expansion strategy of the firms is autonomous growth, keeping

ownership and control in the same local hands. Like the Marshallian-districts type of regime,

these SME’s are export-oriented, but compete locally. The most competitive ‘clusters’ can be

classified as traditional or skill-intensive industries like construction, textile-, wood- and

metal-industries. Industry- and firm-specific skills are said to be based on experience and

learning-by-doing. Thus tacit knowledge and skills are embodied in ‘pools’ of labour which

makes de-localisation difficult.

We note also a resemblance with the entrepreneurial mode of the so called Schumpeter Mark

I Regime. The innovation regime based on Schumpeter’s early work is one that is run by

brave, visionary entrepreneurs. The family-capital structure in this West Flanders sub-region,

with its unity of management and ownership, created the risk-taking opportunity of venture

capital. And like the creative destruction which arose from the brave, stubborn, innovators in

Schumpeter’s early work, the creativity of the risk-taking family capital is vital to the

restructuring of the regional economy of the south of West-Flanders. Besides the advantages,

Vanhaverbeke (1998)5 also mentions some disadvantages concerning the endogenous growth

he describes. First of all, because of the family capital structure and typical autonomous

growth strategies, the size of firms is limited. More importantly, the mentality to solve

4 See also: Vanhaverbeke, W. (1998), Streekcharter voor het Arrondissement Kortrijk, REBAK vzw:Maastricht/Kortrijk. And: Vanhaverbeke, W. (1995), ‘De economische uitdagingen voor de sub-regio ZuidWest-Vlaanderen’. Research Memorandum METEOR RM/95/012. Maastricht University: Maastricht.5 Vanhaverbeke, W. (1998), Streekcharter voor het Arrondissement Kortrijk, REBAK vzw:Maastricht/Kortrijk.

5

technological problems internally, “to keep it in the family” so to speak, hampers the use of

external sources of innovation, which makes it more difficult to transform the area into

networking-firms in a knowledge economy.

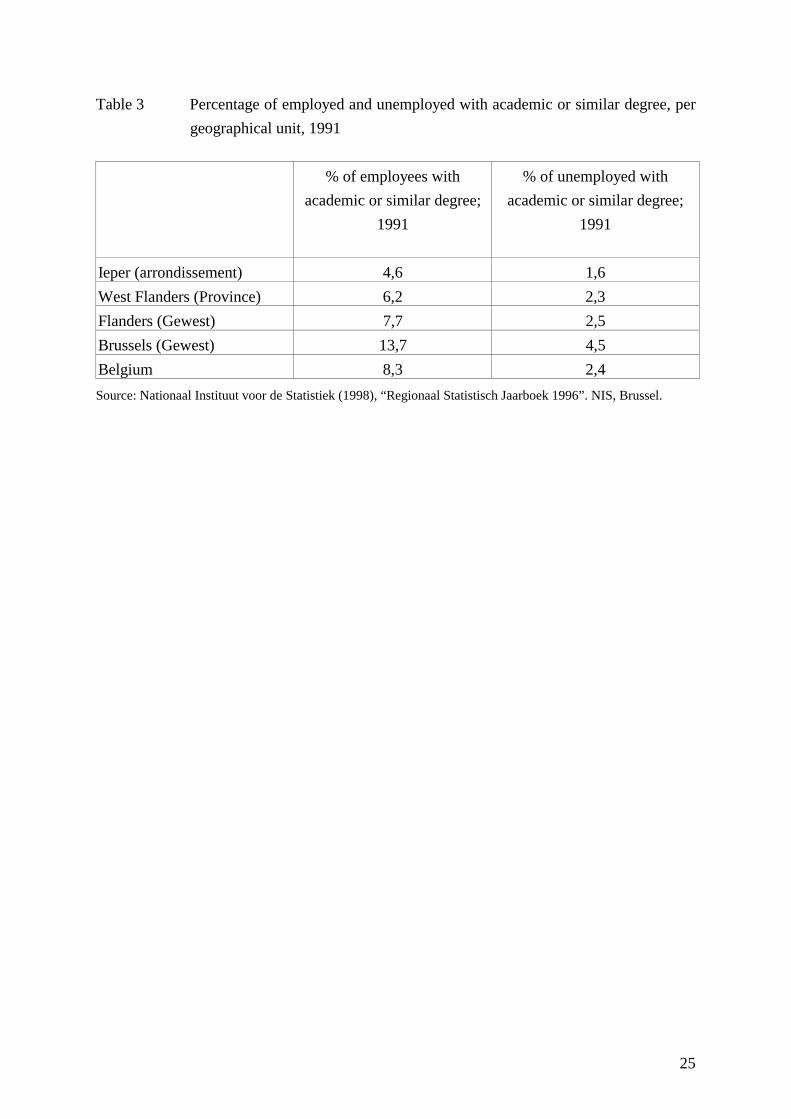

Added to an inherited business-culture, there is a relatively poor knowledge base in the region

due, at least in part, to its peripheral location, i.e. the lack of a University. Kortrijk has some

higher education facilities, but young people, who want to get an academic degree have to

leave the Ieper area. After their studies they may want to go back to their home-region, but

there are not many jobs that require an academic degree (table 3). Thus the ‘brain-drain’ from

Ieper moves toward the economic and scientific core of Flanders: ‘Vlaamse Ruit’ (Gent,

Antwerpen, Brussel, Leuven). Whether based on so-called ‘MAR-externalities’, ‘Jacobs-

externalities’ or both, one would expect a high-tech ICT cluster like FLV to be located

somewhere in this core-area and not in Ieper.

Fortunately, two men who initially left the region returned to their home, and founded the

speech and technology firm which is now at the core of the Flanders Language Valley

initiative. Clearly, this was an instrumantal move by Lernout and Hauspie.

[Insert about here]

[Table 3 Percentage of employed and unemployed with academic or

similar degree, per geographical unit, 1991]

3 Lernout and Hauspie Speech Products

In 1987 Jo Lernout and Pol Hauspie founded L&H. Jo Lernout had worked with Barco and

with Bull & Wang computers. Pol Hauspie, an accountant, worked as an entrepreneur in the

Far East. After several years of working outside Europe, they both returned to their home-

region and met in Ieper. Once they decided to do business together they asked themselves

three questions: Is there a market for language- and speech-technology?; Can it be produced

in Flanders?; Is it possible to maintain the market share when competitors follow?

Their answers were positive:

“At the time, there was no text-to-speech market, most speech recognition was being done in

English, and all of it was speaker dependent. We saw it would be possible at some future time

to have sophisticated voice input and speech synthesis and output combined in one spoken

6

dialogue between user and machine. We felt that if we could do this in many languages, we

should have a market to license this technology because most companies only make either the

input or the output and in many cases just in a few languages”6.

Wang was one of the companies that was working on a technology to codify speech, but it

focused exclusively on English. Within the multilingual context of Belgium and Europe L&H

focused on a multi-lingual-technology. The availability of many multilingual engineers and

highly educated linguists in (the rest of) Flanders made them confident that they could realize

their ideas in Flanders. Ten years after the start-up in 1987, the multi-lingual trajectory

seemed to have paid off rather well. The language-expert-system developed by L&H is more

intelligent and flexible than their competitors. As a ‘language factory’ it is able to ‘produce’

new languages up to 7 times faster than the system of IBM (one of the few remaining

competitors).

Before L&H could even start developing the technology they had in mind, they had to raise

the initial funds to launch the new business. It is not easy to raise money in order to try to

codify a tacit vision that you eventually want to sell through licensing. As mentioned in the

EU Green Paper on Innovation: “Financing is the obstacle to innovation most often quoted by

firms, whatever their size, in all Member States of the European Union and in virtually all

sectors”. Venture Capital plays a crucial role in financing innovative enterprises.

Furthermore, start-ups are not likely to obtain the long-term bank loans required to develop

the technology. To raise the initial capital Lernout & Hauspie visited many local private

sources: “Persuading local bakers, butchers and farmers to invest was part of our daily routine

for a long time in those early days, because traditional investors did not have faith in the

project”7. Fortunately, since the beginning, several private people that go by the name of

Business Angels have invested in L&H. They are people from the region who share the

entrepreneurial spirit that the Westhoek is famous for.

Besides local family capital, they approached a number of institutional investors with the help

of the European Venture Capital Association (EVCA). The most important was the Flemish

regional investment company: GIMV. Founded with government money GIMV is now

registered at the Belgium stock-exchange as a private company (have to check if and which

governments are still shareholders). The two partners persuaded the GIMV to take a

shareholding of 1,5 million USD, or 70 percent of the capital, and started their company in a

business centre that was part of a regional employment project (T-zone). They occupied one

of the twenty offices in the building that was set up by the regional development agency

6 L&H Magazine (1998), p. 10, spring 1998. Lernout & Houspie Speech Products N.V.: Ieper.7 FLV Magazine (1998b), p.4, Number 2, September. FLV: Ieper.

7

(GOM-West-Vlaanderen) to stimulate these kind of ‘high-tech’ projects. After nine months

there were 8 people working at L&H. Later, when they occupied 15 out of the 20 offices in

the start-up-building, they moved to the ‘doorgangshallen’, a growth area assigned by the

GOM-West-Vlaanderen. In 1989, L&H had approximately 80 employees in Ieper. One of the

Business Angels who continues to hold a seat on the board of directors financed the present

building. In the third year of their existence they hired an office in Wemmel that is located

near Brussels. Initially this building was just meant for giving demonstrations, but because of

the labour shortages for IT-specialists L&H soon started to expand in Wemmel too, where it

was less difficult to recrute new employees than it was in Ieper.

L&H did not have an easy start. In 1991 the GIMV decided to pull out its investment because

the company lacked an export strategy and there were no real prospects of growth. Thanks to

the confidence of the Business Angels, L&H survived this hard period. By 1992 L&H had

succeeded in developing a ‘language factory’ using a multi-lingual approach and combining

the three basic voice technologies of compression, recognition and synthesis. A new language

could be codified within less then 12 months time. L&H explored the US market and went

back to the GIMV with a strategic plan that was based on granting non-exclusive

international licences. The GIMV backed this plan with an investment of 5 million US dollars

and also helped to guide the development. With a million dollars worth of equipment they

started ‘production’. The growth of L&H drew the attention of a big US company, AT&T,

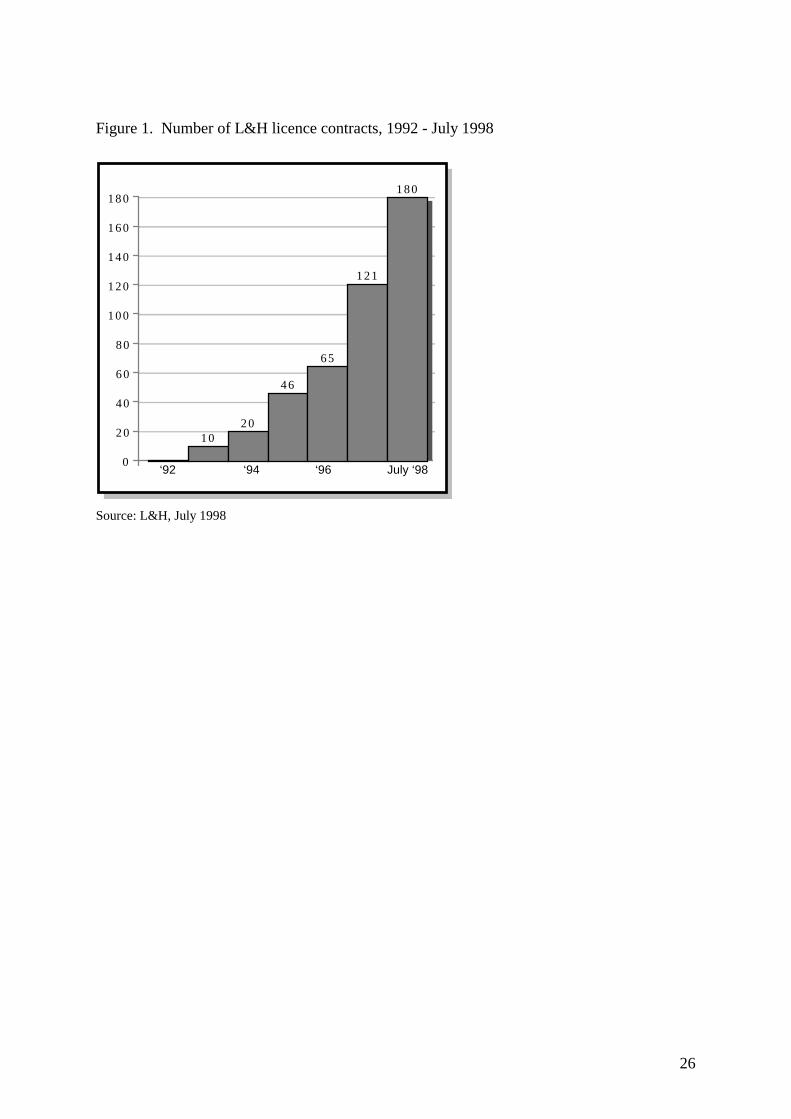

which acquired a 5 percent stake in L&H. During the growth in 1994 they sold licences

(figure 1), received the first revenues and opened two offices in the USA. As a GIMV

manager, Philip Vermeulen took a seat on the Board of Directors. GIMV’s strategic and

operational role made it possible to attract new investors and to achieve a successful launch

on the NASDAQ in 1995, and the Brussels-based EASDAQ later on. Three years later Philip

Vermeulen, by that time ex-GIMV manager, would also bring the FLV Fund to Easdaq; we

will discuss this financial novelty below.

[Insert about here]

[Figure1. Number of L&H licence contracts, 1992 - July 1998]

In 1996, for the first time in ten years, L&H made a profit by selling licences, and started to

acquire other companies. Until then, speech technology was still a fragmented, new market

8

with a lot of small pioneering firms. Through determined specialisation L&H had become a

giant in this niche-market, e.g. they employed more linguistic engineers than IBM, one of

their competitors. The years of research, specialisation, autonomous growth, and the internal

creation of a technological core, generated internal economies of scale that resulted in

technological leadership and market power. L&H started to diversify and build a global

network of technological complementary activities via international joint ventures and

acquisitions. By acquiring the speech technology activities of firms like Siemens Nixdorf and

Novell, and by taking over other technological pioneers, L&H generated both internal

economies of scale and scope. In other words, trough acquisitions MAR- as well as Jacobs-

like-externalities were internalised into the global network of an IT multinational.

First of all L&H started with a lot of small international joint ventures in order to obtain the

native speech databanks and expertise that is required to codify new languages. The

acquisition of Mendez, and other human translation companies, helped to enhance machine

translation and again to develop enormous databases of natural human speech of natives that

are needed to fuel the ‘language factory’. “From the beginning we knew language was the

basis of everything we do, whether decoding spoken words into something machines can

recognise or translating text into another human language, it’s the same technology”8.

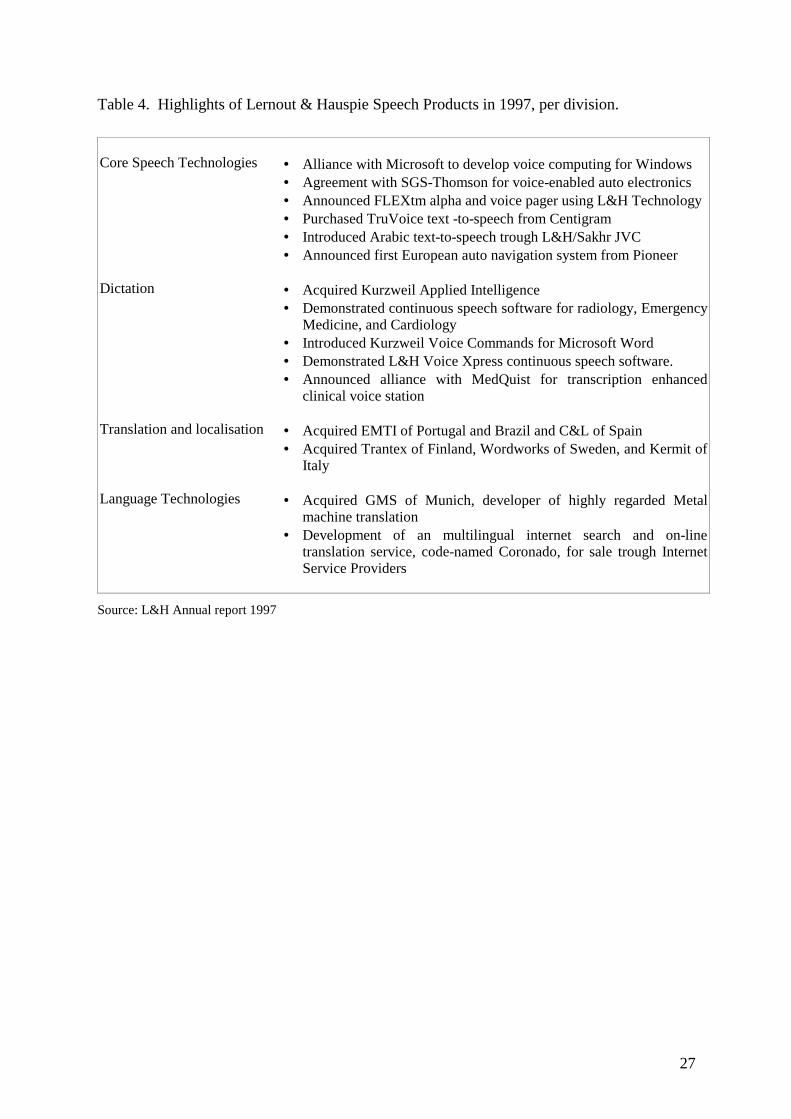

In 1997 L&H took over Kurzweil Applied Intelligence Inc. located in the USA, a well known

technological pioneer in dictation systems, which became the heart of L&H dictation

division. Despite the close technological proximity between L&H and Kurzweil, they had to

put a lot of effort into integrating the firms and their technologies. L&H managed to

internalise the externalities of combining and integrating two separate, albeit complementary,

technologies. The process of (re-)combining the codified knowledge of the two firms,

however, was not a matter of simple exchange, adding an extra set of codes to the existing

stock of codified knowledge. Intensive communication between researchers was needed in

order to integrate the two technologies. To facilitate the intensive communicative

interactions, bridging the physical distance between the two research teams was inevitable.

For this reason twenty researchers from the L&H unit in Wemmel (Brussels) went to

Kurzweil in Massachusetts USA for a month and several people came to work in Wemmel. In

part the technological combination and integration process was also a standardisation process

from which arose certain social complications. Both the L&H researchers and their former

Kurzweil colleagues backed their ‘own’ technology when they had to make choices between

technologies. For several reasons they decided to physically integrate the already existing unit

of L&H with Kurzweil. Both companies had sites near Boston (USA) so they merged into

one new establishment, where the two techniques were integrated in a new generation of

8 L&H Magazine (1998), p. 11, spring 1998. Lernout & Houspie Speech Products N.V.: Ieper.

9

dictation products that could recognise ‘continuous natural speech’ up to 140 words per

minute and instantly transform it into sentences on a computer screen. The latest version also

gave users the possibility to navigate, format, edit and command by their voice.

In just two years the market structure had changed dramatically, and L&H had been strong

contributors to the change. L&H thinks it is big enough now, but according to L&H the

worlds biggest IT firms will soon enter the market. In the beginning large IT-firms did not

show too much interest in developing speech-technology. They watched from the side-lines

as small pioneering firms took the risk of developing the technology. But as the technology

matured and the opportunities for successful applications increased, they showed more

interest. Since ‘the market’ selects which technology survives, its of vital importance to be

selected by the leaders of the market.

Therefore the strongest endorsement for L&H core speech technologies came in September

1997 as Microsoft invested 45 million dollars in L&H common stock, taking over 8 percent

of the ownership. This raised the company’s visibility across the entire computer industry and

pushed the price of L&H shares up by nearly 20 percent in a single day. Moreover, this was

the start of a closer technical and commercial alliance. L&H technologies are now integrated

in several Windows applications and will be at the centre of the recently announced Auto PC.

One of the advantages of the partnership with Microsoft was the possibility to send L&H

speech-compression technology together with the three-monthly Windows up-date to 140.000

software-developers. Microsoft pays L&H for it, and the programmers can use the L&H

technology tools for a month at no extra cost, after which they are asked to buy a

‘maintenance-contract’. It is a priceless distribution channel.

It may be clear from the above that most of the recent growth took place outside Ieper and

outside Belgium (see also table 4). The European Headquarters and the technological core,

however, are still located at Ieper. At the end of 1998 some 250 employees will move to the

new building that is located next to the FLV-campus that is currently under construction.

From the above, however, we may conclude that L&H, with 1500 employees distributed over

20 firms world-wide, had become a global technological network. By linking to global

resources (human, financial, technological) L&H became less dependent on local resources.

Without the FLV initiative the territorial embeddedness of L&H and its speech and language

technology in the Ieper area would probably not exceed the embeddedness of ‘a cathedral in

the desert’.

[Insert about here]

10

[Table 4. Highlights of Lernout & Hauspie Speech Products in 1997,

per division]

4 The Flanders Language Valley initiative

In the beginning of 1995 L&H got many requests from clients wanting access to their R&D

core, the language laboratory in Ieper. A lot of small firms had signed licence agreements in

order to integrate L&H technology with their own technology. The communication had to be

done over long distances, but despite their ICT capabilities this caused miscommunications

and delays. Therefore, clients began visiting Ieper, usually for several months. Some three

firms a year come to Ieper for this reason and they have to be accommodated within the L&H

building. At first L&H was not very enthusiastic about showing them their technological core

because in the end they all could become competitors. On second thought, L&H became

aware of the fact that the more the technology is used by companies to make applications the

better it is for L&H as this would help them in making their technology the industry standard.

Furthermore, they had learned to appreciate interaction with customers. They had leared to

learn from inter-acting with external sources of knowledge. After years of internal

orientation, the autarkic, closed mentality made room for a network mentality. By supporting

the FLV initiative, L&H would support the growth of their customers. Besides, Jo Lernout

and Pol Hauspie had not forgotten the support they got from the region during the difficulties

in the early years. With FLV they could make their dream come through: creating

employment by building a world-wide centre of competence in speech and language

technologies in Ieper.

The idea of creating a small Silicon Valley was launched in December 1995 with the start of

the FLV Fund. Several regional and local financial institutions were interested in joining this

initiative. The Regional Development Agency of West-Flanders (GOM) thought it would be

the next logical step following the original employment-zone (T-zone) that had supported

L&H with their start-up. The idea was to provide venture capital to stimulate starting and

fast-growing young firms, which would be located in a business park in Ieper where they

could make use of all kinds of services and infrastructure. The firms would learn from each

other and benefit from developing and using common pools of resources. The prime resource

would be human resources, therefore a shortage of IT-personnel would be the biggest threat

to the project. Although the IT-labour shortages in the Ieper area are not unique, the initiators

knew from the beginning that they would have to invest heavily in training and education.

This is of course an additional interest of L&H (and even Microsoft). It is estimated that

11

within ten years time about two or three thousand employees will be needed in Flanders

Language Valley.

The dynamics of FLV is based on four pillars:

• The physical and technological proximity of L&H’s expertise;

• The venture capital from the FLV Fund focused on speech and Language related

technology applications;

• The FLV Foundation offering business support, incubation services, training and

education;

• The technological dynamics among the FLVcompanies.

5 The FLV Fund

As soon as the idea of building FLV was launched in 1995 a group of institutional and private

investors were interested in what they saw as good investment opportunities. The Fund

initially started with 5,6 million USD and began to invest in dynamic high-tech companies

which focused on applications based on language and speech technology, or closely related

technological fields. The FLV Fund approached promising companies that were in search of

venture capital to start up a business or to grow after a succesful start-up period. The first

company the fund invested in was Voxtron in 1995, a Belgium start-up. Since then the FLV

fund has invested in some 34 companies and this number is growing with approximately one

firm per month.

The concept of a venture capital fund specialised in one sector was not new. In the USA as

well as Europe there were already some specialised venture capital funds, e.g. in ICT or

Bioscience, but never in just one technology. The FLV Fund had 60 million USD under

management before they got listed in July 1998 on the Eastdaq (a Brussels-based, pan-

European exchange for growth companies, in co-operation with Nasdaq in the USA). The

most important names on the list of investors are: GIMV, Artesia, Microsoft, Lessius,

Kredietbank and Mercator-Noordstar. In 1997 Microsoft Corporation invested three million

USD in the FLV Fund. This increased the visibility of the Fund enormously.

Some 50 companies from Asia, the US and Belgium contacted them. Out of these requests

six to seven concrete opportunities were selected. This is an important point, since the

screening procedure typically canvasses the opinion of L&H and the other firms in order to

validate the technological and commercial capabilities of potential candidates to see if there

could be some common interest or complementarity. In other words, it is part of the strategy

to look for possible technological spill-overs between the firms. In the beginning the

technological complementarity was reflected by the fact that almost every firm the FLV fund

12

invested in was a client of L&H. Almost all of the firms use L&H technology in their

applications.

Later on the FLV companies also started to license technology from each other. This is a

slightly different point, but again verry important. To lisence something you have to know it

exsists. These firms know about each other and what they are doing because of the FLV

canvassing procedure. These licence agreements can be conceived as traded

interdependencies. However, when the management of the FLV Fund selects new firms to

expand the network of FLV companies they certainly have the localising effect of untraded

interdependencies in mind, as do the firms themselves.

More than half of the FLVcompanies are foreign. In some cases the FLV Fund invested in

both the ‘mother company’ (located outside Ieper and in many cases outside Europe) and in

the start up of a European office in Ieper. One of the criteria to select firms to invest in is the

interest they show in a location on the FLV Campus in Ieper. Not every firm is already

present in Ieper, but some are, spread throughout the city, waiting for the campus to be built.

In 1999 the first 10 companies have located at the campus. Twenty additional units will soon

follow and eventually some 100 firms will be located around the campus. After the start of

the FLV Fund the non-profit FLV Foundation started to develop and carry out plans

concerning education, incubation services, building the campus, et cetera.

6 The FLV Foundation

In contrast to the FLV Fund,the FLV Foundation is a non profit organisation that was funded

and founded in 1997 by the following initiators:

• Jo Lernout and Pol Hauspie (Founders of L&H);

• The city of Ieper;

• The Flemish Government;

• The Regional Development Agency (GOM);

• The West-Flanders Intercommunity for Economic expansion and Reconversion (WIER).

Besides the financial contributions of the above mentioned initiators, there were other

contributors, such as Microsoft, that donated 3 million USD to the Foundation, especially for

education and the formation of a Language University. As the strategy of the FLV Fund

proved to be very successful in a very short time, they had to speed up those aspects of the

FLV concept that took more time. The two most important tasks of the foundation are to

create the infrastructure and to increase the availability of human resources for language and

speech technology in the region. The FLV Foundation itself expanded and with great

13

ambition and speed they managed to realise more and more of their goals. The Foundation is

subdivided into 6 non-profit organisations and 6 profit organisations which are supporting

companies. We will discuss the most important ones.

FLV Business Development operates promotion platforms in Flanders, Boston, Singapore and

San Francisco. These platforms offer FLV companies a spring-board for their world-wide

expansion by setting up offices, attracting management, performing market research,

providing sales and marketing support and publicity assistance. The platforms also identify,

attract and lead promising high-tech companies to FLV in Ieper.

FLV Education takes care of several training and education programmes (10 in total as of

september 1998) upon which the existence and sustenance of FLV depends. A lack of

enthusiasm for the education programmes or job-openings does not seem to be a problem,

since about 1300 people visited the FLV-Job-Day that was organised in 1998.

In co-operation with KATHO (the higher education institute in Kortrijk) a faculty of

computer-linguistics was set up. In 1997 eighty people attended the first course, a post-

graduate course in computer linguistics, and 140 people have attended the programme in

1998.

More recently the University of Leuven opened a campus in Kortrijk where, in co-opreation

with Flanders Language Valey they have set-up an Artificial Intelligence department.

A third programme started in October 1998. About 150 people attended emergency courses.

In the short term of a few months they were trained and re-educated into software

programmers.

A fourth education project concerns the formation of Flanders Language University at the

FLV campus. Experts in computational linguistics from all over the world will be asked to

participate in order to build a scientific network. The relations with MIT and Kyoto

University will play an important role. The FLUniversity focuses on highly specific training

courses for FLV personnel.

In cooperation with several other excisting training institutions, another six ICT training

projects not only serve the future of the FLV companies but the future of the Westhoek-

society in general as well9 .

FLV Human Resources works together with a Flemish employment agency (VDAB) and

several selection and recruitment agencies and serves to acquire highly educated employees

for FLV companies.

9 FLV Magazine (1998a), p.3, Number 1, April. FLV: Ieper.

14

FLV Finance manages a local start-up fund and takes care of the contacts with the FLV Fund.

It is a local investment bank that co-ordinates the activities of a number of local Business

Angels. This initiative is a shadow of the regional family venture capital tradition, since it is a

forum where young firms can show their business strategies to local private investors. The

institutionalised environment of the FLV Fund with its professional investors does not suit

the local Business Angles. They want to invest their capital privately, by scouting for local

talent themselves and sharing their vision in person.

FLV Telecom provides the necessary telecommunication infrastructure, not only for their own

needs but also for thousands of local end-users. There are plans to install thousands of

highbandwidth internal access-points at private households in the vicinity, in exchange for

active participation in testing of products of FLV companies, e.g. the computertelephony

products of Voxtron. This looks like an interesting attempt to expand the ‘network’ outside

the traditional business bounderies to include local households. As a result even more

interactive user-producer relationships will be localised within the regional tissue of the Ieper

area.

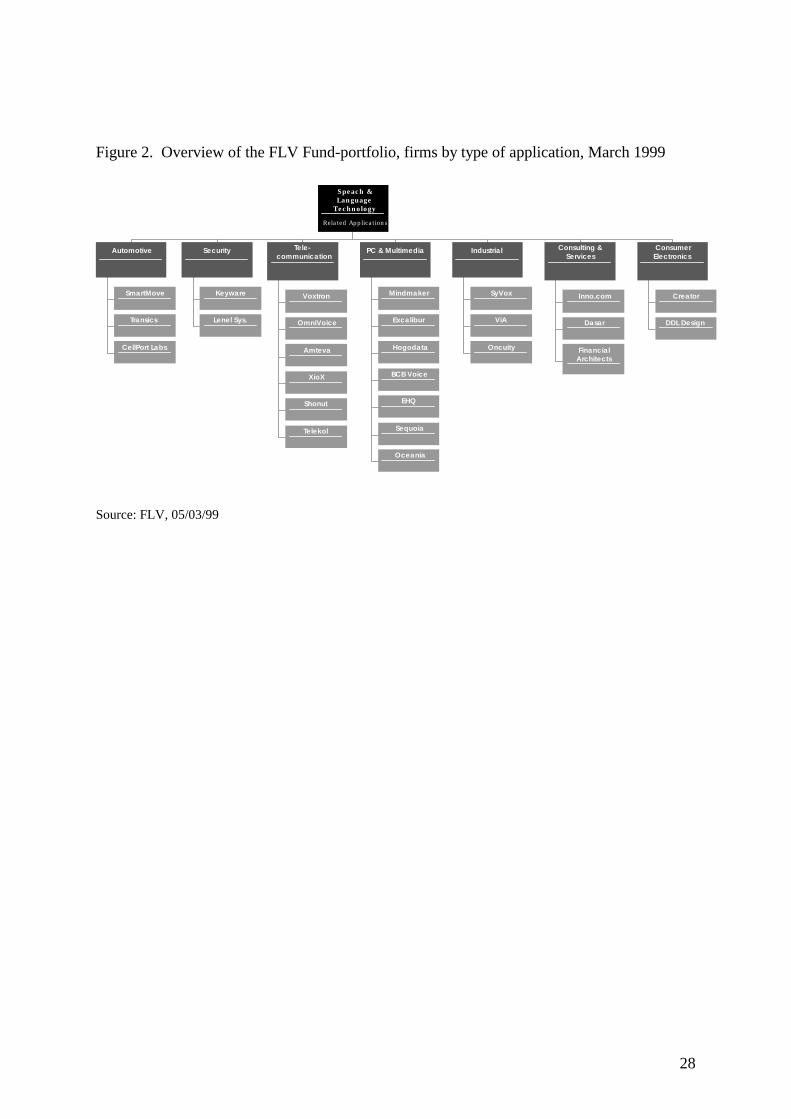

[Insert here]

[Figure 2. Overview of the FLV Fund-portfolio, firms by type of

application, 1999]

7 FLV Companies

In September 1998 the number of FLV Companies has increased up to 16 firms and eight

moths later the number was 26 (figure 1). November 1999 the number is 34. Secondary data

and the interviews indicate the major characteristics of the FLV firms. They are generally

young, small, fast growing and mostly of foreign origin. The ‘average’ FLV firm is three

years old, employs 17 people of which almost 90 percent have a higher educational degree.

Not only the Ieper subsidiaries themselves fall into the SME category, but also these

multinational companies as a whole are mostly still SMEs (no more than 250 employees). On

average the Ieper firms estimated that some 70 percent of the knowledge and ideas that make

15

up their innovative capacity stems from internal sources of knowledge (experiential learning

and R&D). Furthermore, on average, more than 40 percent of the knowledge that originates

from external sources originates from other companies within the FLV cluster; whether by

socialising or recombination, whether by perculation through the back-door or delivered at

the front-door by the market. Most FLV companies do not make profits, some of them do not

even have revenues yet. All are specialised in language or speech related technologies and the

highly educated staff spend a lot, if not all of their time, on research and development. The

commercial activities are mostly addressed to Europe where their multi-lingual asset is

assumed to pay off best.

We will discuss some of these companies to illustrate their role in the innovation process and

to see what their motives for and experience with technological and geographical clustering

are.

• Voxtron Flanders NV

The first participation from the FLV Fund was in the start-up in 1995 in Ieper of a firm that

was part of the American company called Quarterdec. Recently the firm became part of the

international Voxtron group, which is headquartered in Belgium (Voxtron Europe in Sint-

Niklaas) and also has offices in Singapore, Hong Kong, the Philippines and India. In total

around 80 people work on Computer Telephony products. At the time of the interview the

office in Ieper employed four people. In the beginning the location in Ieper was mainly

motivated by the proximity to L&H. During the development of Earmail (software that

enables one to use the phone and listen to your e-mail) it was important to be close to L&H,

the technological source. The proximity to L&H speeded up the development and launching

of the product. Like L&H, Voxtron’s strength is the multilingual approach; 9 and soon 15

languages will be integrated. New advantages of being located in Ieper, besides the proximity

to L&H, have emerged as more potential partners came to Ieper and as more FLV services are

provided, for example, searching for new employees. Since the interview in 1998 the number

of employees will probably have doubled or tripled. The labour shortages in Ieper were still

severe in 1998, but already were changing for the better, according to Stefaan Vandaele

(authors interview 1998):

“Like most FLV companies we use the knowledge of L&H in our applications. L&H does not

make the products, we do. They do the research and develop the technology. We make the

applications and combine licenses into new products. We also have licensed technology from

other FLV companies, like Xiox and Keyware Technologies”.

Because of FLV, Voxtron came into contact with firms they had had no prior dealings with.

Voxtron is also interested in co-operating with an Israeli firm that would also like to come to

16

Ieper. The FLV Fund was negotiating with this potential FLV candidate and asked the

existing FLV companies if they saw some possibilities in working together with the Israeli

firm. The firm visited Voxtron to see if their technologies were complementary and both

firms think it will be fruitful to work together, since it may be interesting to combine two of

their products: listening to your e-mail by phone and listening to your fax by using the

telephone. Voxtron, however, is only interested in making an arrangement to see if it is

fruitful to exchange and integrate technologies when they come to Ieper and become an FLV

company:

“You can sign a non-disclosure contract and show each other your technological

capabilities, but if this Israelian company does not act according to this contract, you can not

take him to court. If they are located here in Ieper and they participate in FLV they would not

even think about this kind of abuse”.

This is an important aspect in the localising strategy of FLV, since the institutional

architecture and the geographic proximity within FLV seems necessary to ‘open-up’

communication channels in order to look for possible technological complementarities and

create valuable behaviour norms.

• Keyware Technologies NV

Keyware develops and provides Layered Biometric Verification (LBV) for enhanced security.

Among others, Keyware combines two biometric technologies into one solution: image

pattern recognition technology, from Excalibur Technologies (a FLV company) and speaker

verification technology, licensed from Lernout and Hauspie. Keyware also maintains

technological relationships with FLV companies like Voxtron, Amteva and Lenel. Actually, it

was Keyware that brought Lenel in contact with FLV; Lenel already was a client of Keyware

before Lenel joined the club. The technological interaction with Voxtron and Amteva is a

result of FLV.

Keyware Technologies was founded in 1996 by opening at the same time an office in

Zaventem (Brussels) and in the USA. According to Francis Declecq from Keyware:

“The FLV concept actually came too late for Keyware, otherwise we would have started-up

in Ieper and we would have used the international FLV platforms instead of opening up a

branch-office in the US ourselves. Without any support it was easier to find employees and

all kind of facilities in Brussels”.

17

As soon as the Campus was finished Keyware opened an office in Ieper, which employed

about 20 people. At the recently organised FLV Job-day they already found several

employees they were looking for. In total Keyware has 50 employees, 15 of them work in

Brussels.

Keyware started with the knowledge of others. By integrating several technologies and

enhancing it, they developed their LBV-system. At the moment, they are searching for

alliances and acquisitions in order to expand this technological base. Clients have become the

most important external source of knowledge. Some 50 percent of the knowledge originating

from external sources originated from the FLV cluster. Until 1998 Keyware has signed 25

contracts, some with FLV companies, others with clients like BULL, Smartcard and Unisys.

• SyVox Europe NV (former Speech Systems)

The founder of Speech Systems in Bolder, Colorado, is one of the famous scientific pioneers

on speech-technology in the USA. As a university spin-off firm it started at the same time as

L&H , but unlike L&H, it did not succeed in developing a product nor in marketing their

technology. Until recently, the firm did not seem to survive the selection process between the

pioneers in speech technology. After a change in management (less scientific) they

acknowledged that their language technology lost when compared with their competitors’, but

they discovered that there was still one competitive advantage left: the technology to filter

voice from a noisy environment. Acknowledging they had lost the technology race, they

licensed L&H technology and integrated their own technology that is used for speech

recognition applications for industrial logistic purposes, like speech-enabled warehouse

‘order-picking’. To accelerate European market penetration and develop new applications in

multiple languages, they created a subsidiary in Belgium as an FLV company. Recently, they

acquired a Belgian firm and changed their name to SyVox. In 1999, SyVox will move within

Ieper and open up a subsidiary at the FLV Campus, where they will employ approximately 20

to 30 people.

• SmartMove NV

As a privately owned Belgian company, SmartMove was founded in 1996 in Leuven by a

team of engineers working in close relationship with IMEC. (IMEC is one of the world’s

largest independent research centres in micro-electronics, founded in 1984 by the Flemish

government in association with the Leuven University. IMEC employs 750 people of which

70 percent are engaged in R&D, and it announced in September, 1998 it will open a research

unit within the speech and language environment of FLV). SmartMove develops a hand-free

vehicle communications platform that combines telecommunication and information

18

technology, i.e. the technology of L&H. Since L&H is engaged with Microsoft in the autoPC

project one questions if these projects compete with each other. According to Smartmove,

however, they are complementary, since SmartMove uses Java technology, a computer-

language that is well known for its compatibility with other codifying technologies.

However, even if these technologies compete with one another, and only one survives the

selection and standardisation process, the FLV system as a whole will not be locked into the

technology that does not survive, thanks to the external economies of scope provided by the

‘the strength of weak ties’ (Granovetter 1973), or the long-term stability of ‘flexible

specialisation’.

8 FLV: creating a ‘second nature’ to the region

A lot has been changed in the last two years and FLV became visible to the people in Ieper,

the region and beyond. Many people and organisations are now eager ‘to hop on the train’.

Finally the people can believe the words of the mayor of Ieper when he said that FLV would

become as important to the region as the textile industry had been in the 12th and 13th

century. Some 100 firms are expected to locate in Ieper and they will employ about two to

three thousand people. Now an increase in image and expectations is increasing returns. The

local government has begun negotiating plans to build houses for the influx of people to the

area. Local businessmen are planning to invest as well, e.g. in extra hotel-accommodation.

As an innovation system Flanders Language Valley is highly specialised and concentrated in

a technological and geographical sense. But why in a small city in a rural area? The localised

knowledge can hardly be traced back to the original locational advantages (or disadvantages)

of the region. It seems that the technological idea and assistance for L&H was destined to

come from foreign sources so, from a technological point of view it didn’t really matter if the

company was located in a bigger center in Belgium or not (apart from the fact that an airport

might be convenient). Either way they were going to have to travel and ‘shop’ outside of the

country (USA as it turns out initially) to get the ‘brains’ they needed. However, the

entrepreneurial spirit, the availability of venture capital in the region and the multi-lingual

aspect can be conceived as a sort of ‘first nature’ (Krugman 1993) of the regional specific

advantages on which the success of L&H and its technology is partly based. Actually the

strong family-oriented business ethic seems crucial: first of all with regard to the boys’ initial

homecoming and secondly with regard to the faith of local private investors puting money

into their vision, i.e.: Would Lernoud and Hauaspie have succeeded in persuading local

butchers and bakers in a community they were not familiar with, like Brussels? Social links

19

drew and ‘tied’ them into Ieper. These innitial local links, however, could not prevent L&H

from growing out of Ieper into a global network.

As “we can know more than we can tell” (Polanyi 1966, 4), L&H knew more than it could

sell and their clients wanted more than they could buy through licences. As this case shows,

the exchange of codified knowledge in the form of licence agreements can be a highly

localised learning process. The need for face-to-face contacts in order to better interact and

exchange the tacit knowledge which is used to combine the codified knowledge started to

attract other firms with similar and complementary technologies to Ieper. This inspired Jo

Lernout & Pol Hauspie and some regional and local institutions to establish the joint public

and private policy of the Flanders Language Valley initiative. A broad set of instruments were

designed to increase ‘receptivity’ and ‘connectivity’ and localise the internal and external

codification processes into the region in order to jointly economise on the localised

knowledge spillovers. Building on the ‘first nature’ advantages and the presence of L&H, the

FLV initiative created ‘second nature’ advantages by attracting additional firms with

complementary technologies to the region and supporting them. L&H, The FLV Fund, the

FLV Foundation and the attracted FLV firms are transforming the region by creating a

localised innovation system that sets the cumulative causation of increasing returns in motion.

20

Summary

• The homecoming of Lernout and Hauspie;

• Research and development funded by ‘regional’ Venture Capital, from institutional as well as

private investors stemming from what appears to be a significant inherited business mentality in

the area;

• L&H adopts network mentality (letting others in) in spite of the fear others becoming

competitors: L&H saw learning potential and opportunities to standardise their own technology;

• Intensive communication regarding integration of technologies forced physical integration (L&H

with Kurzweil for example). Face-to-face communication seemed necessary due to the

complexity of the projects;

• L&H supported the FLV initiative. In part out of gratitude, but they also saw more opportunity

for themselves, i.e. concerning investments in education and training; influx of human resources;

support their clients; shared knowledge and integration of other technologies;

• The investors of FLV fund see good business opportunities, because the firms are all in the same

promising field of language and speech technology;

• The building of a local industrial park saying ‘come to us’;

• A big IT firm comes on board (Microsoft). This was important publicity for attracting others;

• Screening policy (looking for spillovers) through L&H and other participating firms. It keeps the

firms closely linked (almost ‘personal’) and progressively linked (each new firm must have

something to add);

• FLV companies know about each other and what each is doing. They license from each other,

which ‘forced’ face-to-face sharing;

• FLV companies must be willing to locate in Ieper and get ‘educated’ in Ieper: ‘forcing’ a

clustering process;

• Formation of the FLV foundation: more support to the young SME’s, ‘monitoring’ and ‘keeping

pace’ with very fast developments, investments in human resources and attracting public funds

for it;

• Enhancing interactive user-producer relations in the region: i.e., offering household use of

products strengthens the clustering effect by moving it beyond the business sector but keeping it

local;

• Companies ‘find’ each other at FLV to their mutual advantage, based on the convenience of

single (‘collective’) source shopping;

• Companies find employees in the ‘created collective pool of labour’, e.g., at the local job fair or

from FLV’s education services;

• More employment, more advertising by the government’s actions (i.e. plans to build more local

housing).

21

• More enthusiasm among the business-, social- and policy-community: FLV now has the

‘popularity vote’: all create and sustain the clustering effect.

22

References

Amin, A. and N. Thrift (1992), ‘Neo-Marshallian nodes in global networks’, International

Journal of Urban and Regional Research, 16/4, 571-587

Granovetter, M. (1973), ‘The Stength of Weak Ties’. In: American Journal of Sociology,

vol.78, nr. 6, pp. 1360-1380.

Krugman, P. (1993), ‘First nature, second nature and metropolitan location’, Journal of

Regional Science, vol. 33,1.

Musyck, B. (1993), ‘Autonomous Industrialisation in South-West-Flanders’, doctoral thesis.

University of Sussex, Brighton.

Polanyi, M. (1966), ‘The Tacit Dimension’. Routledge: London.

23

Table 1 Population, density, urbanisation and average per capita income, in 1994 per territorial unit

Population

1994

Inhabitants/

km2

1994

Urbanisation

%

1994

Average income per

inhabitant,

1994 (1.000 BF)

Ieper,

Gemeente

35.434 271 13 307

Ieper,

Arrond.

104.331 190 10 292

West Flanders,

(Prov.)

1.119.085 356 15 329

Flanders

(Gewest)

5.847.022 432 17 354

Belgium 10.100.631 331 12 340

Source: Nationaal Instituut voor de Statistiek (1998), “Regionaal Statistisch Jaarboek 1996”. NIS, Brussel.

24

Table 2 Restructuring and growth of production per territorial unit, 1985-1996

Agricult.

% of prod.

1985

Agricult.

% of prod.

1996

Industry

% of prod.

1985

Industry

% of prod.

1996

Average anual

growth of GDP

1986-1996, %

Ieper,

Arrond.

13 6 31 31 2.73

West

Flanders,

(Prov.)

6 3 35 29 2.14

Flanders

(Gewest)

3 1 38 34 2.14

Belgium 2 1 34 30 1.78

Source: N.I.S. (1998), “Regionaal Statistisch Jaarboek 1996”, Brussel; Instituut voor de Nationale Rekeningen(1998), Regionale rekeningen 1996, Brussel.

25

Table 3 Percentage of employed and unemployed with academic or similar degree, per

geographical unit, 1991

% of employees with

academic or similar degree;

1991

% of unemployed with

academic or similar degree;

1991

Ieper (arrondissement) 4,6 1,6

West Flanders (Province) 6,2 2,3

Flanders (Gewest) 7,7 2,5

Brussels (Gewest) 13,7 4,5

Belgium 8,3 2,4

Source: Nationaal Instituut voor de Statistiek (1998), “Regionaal Statistisch Jaarboek 1996”. NIS, Brussel.

26

Figure 1. Number of L&H licence contracts, 1992 - July 1998

180

160

140

120

100

80

60

40

20

0

1020

46

65

121

180

‘92 ‘94 ‘96 July ‘98

Source: L&H, July 1998

27

Table 4. Highlights of Lernout & Hauspie Speech Products in 1997, per division.

Core Speech Technologies • Alliance with Microsoft to develop voice computing for Windows• Agreement with SGS-Thomson for voice-enabled auto electronics• Announced FLEXtm alpha and voice pager using L&H Technology• Purchased TruVoice text -to-speech from Centigram• Introduced Arabic text-to-speech trough L&H/Sakhr JVC• Announced first European auto navigation system from Pioneer

Dictation • Acquired Kurzweil Applied Intelligence• Demonstrated continuous speech software for radiology, Emergency

Medicine, and Cardiology• Introduced Kurzweil Voice Commands for Microsoft Word• Demonstrated L&H Voice Xpress continuous speech software.• Announced alliance with MedQuist for transcription enhanced

clinical voice station

Translation and localisation • Acquired EMTI of Portugal and Brazil and C&L of Spain• Acquired Trantex of Finland, Wordworks of Sweden, and Kermit of

Italy

Language Technologies • Acquired GMS of Munich, developer of highly regarded Metalmachine translation

• Development of an multilingual internet search and on-linetranslation service, code-named Coronado, for sale trough InternetService Providers

Source: L&H Annual report 1997

28

Figure 2. Overview of the FLV Fund-portfolio, firms by type of application, March 1999

Speach &Language

Technology

Related Applications

PC & MultimediaTele-communication

Voxtron

OmniVoice

Amteva

XioX

Shonut

Telekol

IndustrialSecurityAutomotive Consulting &Services

ConsumerElectronics

SmartMove

Transics

CellPort Labs

Keyware

Lenel Sys.

Mindmaker

Excalibur

Hogodata

BCB Voice

EHQ

Sequoia

Oceania

SyVox

ViA

Oncuity

Inno.com

Dasar

FinancialArchitects

Creator

DDL Design

Source: FLV, 05/03/99