Fixed Income Investor Review - Citibank · Disciplined asset budgeting and allocation ... Citibank,...

22

Fixed Income Investor Review July 23, 2008 Gary Crittenden, CFO Zion Shohet, Treasurer

Transcript of Fixed Income Investor Review - Citibank · Disciplined asset budgeting and allocation ... Citibank,...

Fixed Income Investor ReviewJuly 23, 2008

Gary Crittenden, CFOZion Shohet, Treasurer

1

Agenda

Citi Overview

Balance Sheet Management

Capital Markets & Funding

Q & A

Citi OverviewGary Crittenden, CFO

Balance Sheet Management and Capital Markets & FundingZion Shohet, Treasurer

4

Proactive Capital Issuances

($bn)

-15.2 Net Loss

9.3 Common*

11.7 Preferred

15.7 Convertible Preferred

7.5 Equity Units

5.5 ETruPS

$49.7 Capital Issuance since

3Q’07

3Q’07- 2Q’08 Net Losses

* Includes $4.4bn issued related to Nikko transaction

5

0

20

40

60

80

100

120

140

160

1Q06 2Q06 3Q06 4Q06 1Q07 2Q07 3Q07 4Q07 1Q08 2Q08

Stable Equity Metrics$bn

Tier 1

Shareholders’ Equity

Note: Total Equity includes Common Equity and preferred stock, but excludes the impact of $7.5 billion of convertible equity units which begin mandatory conversion into common shares on March 15th, 2010.

6

Disciplined asset budgeting and allocation

Focus on returns

Dynamic transfer pricing

Active reduction through

– Divestitures

– Asset sales

– Run-off

Active Asset Program

Core Assets

Legacy Assets

7

Asset Trends

(1) Preliminary.

1.88

2.02

2.22

2.36

2.19 2.202.10

4Q'06 1Q'07 2Q'07 3Q'07 4Q'07 1Q'08 2Q'08

25%$474B

(11)%$(257)B

(1)

($Tr)

8

Citi Capital Ratios

11.6% 11.7% 11.9% 11.7% 11.5% 11.2%10.6% 10.7%

11.2%

12.2%

8.3%7.9%

7.3% 7.1%7.7%

5.2% 4.8%4.4% 4.1% 4.0%

4.4%5.0%

8.7%8.6% 8.5% 8.6% 8.6%

5.2%5.2%5.2%

0%

1%2%

3%

4%5%

6%7%

8%

9%10%

11%

12%13%

14%

1Q'06 2Q'06 3Q'06 4Q'06 1Q'07 2Q'07 3Q'07 4Q'07 1Q'08 2Q'08

Total Capital Ratio Tier 1 Capital Ratio Leverage Ratio

--- Represents minimum for “well capitalized” bank holding company

9

INTEGRATEDFUNDING AND LIQUIDITY

MANAGEMENT

INTEGRATEDFUNDING AND LIQUIDITY

MANAGEMENT

Market Access Limits

Internal andExternal Triggers

Internal andExternal Triggers

ContingencyFunding

Plan

ContingencyFunding

Plan

Liquidity RatiosLiquidity Ratios

Liquidity Risk Management Tools

10

Liquidity HighlightsDiversified and stable deposit base– $804bn sourced globally as of 6/30/08; up $32bn YoY

Structural liquidity enhanced by recent deleveraging– Assets down $120bn YoY; structural liquidity of equity, long-term debt, and

deposits up $119bn YoY

Reduced bank unsecured wholesale borrowings– As of recently, net placer of interbank funds

Extended maturity profile of liabilities– Average maturity of long-term debt extended to 7.3 years

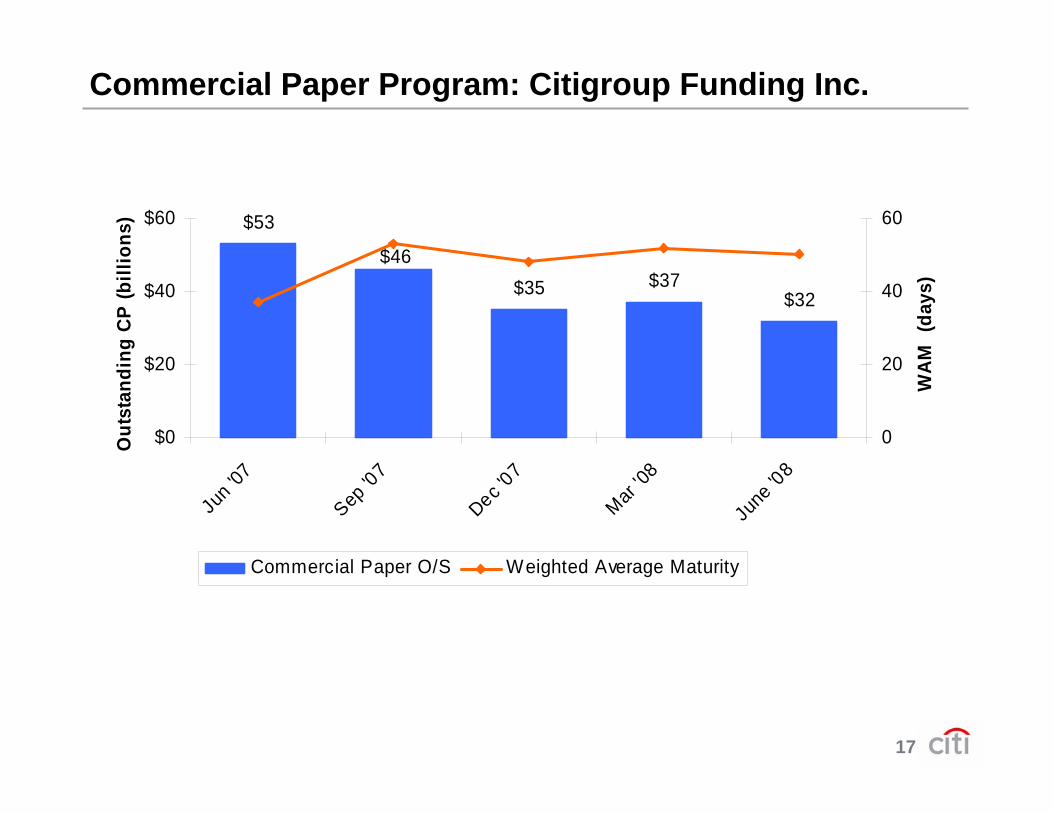

Smaller and extended CP program– Commercial paper outstanding has been reduced to $32bn, and weighted

average maturity extended to 50 days

Expanded cash and highly liquid securities – $65bn of cash and highly liquid securities (excluding unencumbered box) at the

holding company and broker dealer as of 6/30/08; up from $24bn at 12/31/07

11

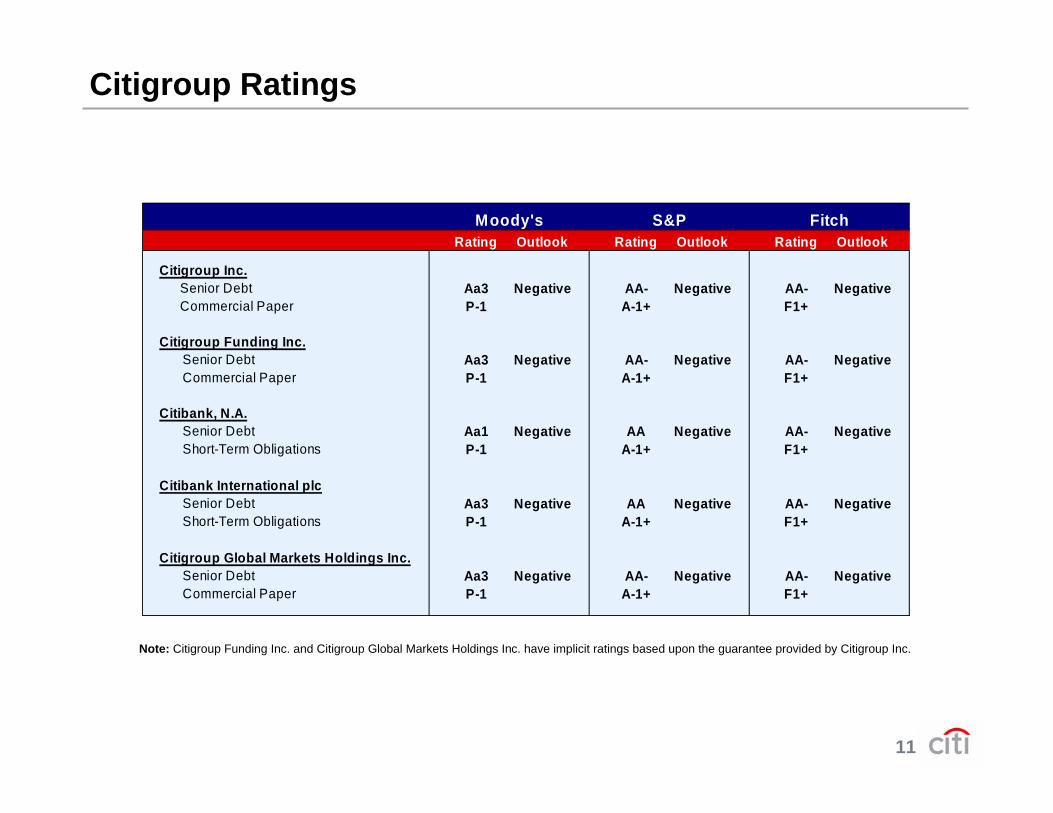

Citigroup Ratings

Rating Outlook Rating Outlook Rating Outlook

Citigroup Inc.Senior Debt Aa3 Negative AA- Negative AA- NegativeCommercial Paper P-1 A-1+ F1+

Citigroup Funding Inc.Senior Debt Aa3 Negative AA- Negative AA- NegativeCommercial Paper P-1 A-1+ F1+

Citibank, N.A.Senior Debt Aa1 Negative AA Negative AA- NegativeShort-Term Obligations P-1 A-1+ F1+

Citibank International plcSenior Debt Aa3 Negative AA Negative AA- NegativeShort-Term Obligations P-1 A-1+ F1+

Citigroup Global Markets Holdings Inc.Senior Debt Aa3 Negative AA- Negative AA- NegativeCommercial Paper P-1 A-1+ F1+

Citigroup Inc.Summary of Credit Ratings and Outlooks

Moody's S&P Fitch

Note: Citigroup Funding Inc. and Citigroup Global Markets Holdings Inc. have implicit ratings based upon the guarantee provided by Citigroup Inc.

12

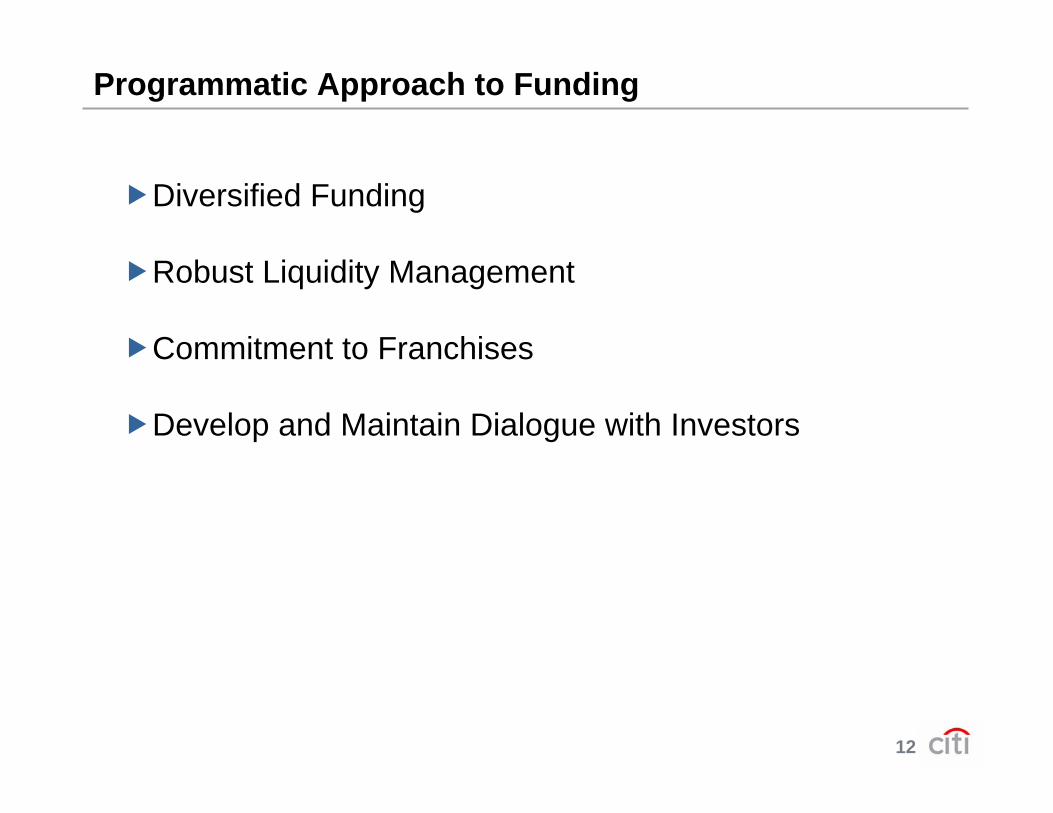

Programmatic Approach to Funding

Diversified Funding

Robust Liquidity Management

Commitment to Franchises

Develop and Maintain Dialogue with Investors

13

$0

$5

$10

$15

$20

$25

$30

$35

$40

2002 2003 2004 2005 2006 2007 2008 YTD

USD Non-USD

$13.7

$22.8$23.9 $23.9

$29.6

$37.4

13% 22% 31% 35% 44% 48%

Global Franchises – Citigroup Inc.

(Billions)

Non-USD % of Total Outstandings

$70B $82B $97B $101B $122B $155B

$20.6

$171B

50%

Historical Issuance

CHF EUR JPY

CHF EUR GBP JPY

AUD CHFEUR GBP

SGD

AUD CADCHF EURGBP JPY

SGD

AUD CADCHF EURGBP HKDJPY SEKSGD THB

AUD CADCHF DKKEUR GBPHKD JPYNZD SEKSGD THB

EUR GBPJPY SGD

THB

14

Issuance Weighted Average Maturity– 2007: 8.6-years– YTD 2008: 10.9-years

Maturity Profile – Citigroup Inc.

4%

9%10%

9%

14%

9% 8%

3%4%

7%

5%

8%9%

0%

2%

4%

6%

8%

10%

12%

14%

16%

2H'0

8

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

-202

8

2029

+

Distribution of Maturities

70 82 97 101 122 155 171

4.9

5.7

6.5 6.77.0

7.37.0

60

80

100

120

140

160

180

2002 2003 2004 2005 2006 2007 Current0

1

2

3

4

5

6

7

8

Total Outstandings ($B) and Remaining Life (yrs)

15

EUR15.9%

GBP14.9%

JPY14.3%

USD52.4%

SGD2.1%

THB0.4%

Larger transaction sizes– Feb: $2.5B 30-yr– Mar: EUR 2B 5-yr– Apr: $4.75B 5-yr– May: $3.0B 10-yr

4.83.6

2.51.2 1.8

3.5

1.5

0.2

1.6

$0.0

$2.0

$4.0

$6.0

$8.0

$10.0

1.5 Yr 3 Yr 5 Yr 10 Yr 15 Yr 20 Yr 30 Yr

non-USDUSD

2008 YTD Issuance Summary: Citigroup Inc.($B) By Tenor By Currency

16

EUR19.7%JPY

0.5%Other2.8%

SEK0.1%

GBP0.2%

USD76.8%

Raised $13.5B in 11 currencies: WAM: 3.3yrs, non-USD: 23.2%, structured: 46%

Diversification across products and markets– Distribution in 19 European countries– Product Innovation: Rate Structured, Inflation Linked, Equity Linked– Expansion of currencies (Scandinavia, Eastern Europe)

4.4

3.6

1.6

0.4 0.3 0.0

0.1

1.7

0.80.4

0.1

0.01

$0

$1

$2

$3

$4

$5

1 yr 2 yr 3-5 yr 6-10 yr 12-15 yr 18+ yr

non-USDUSD

2008 YTD Issuance Summary: Citigroup Funding Inc.($B) By Tenor By Currency

17

$53

$35 $37$32

$46

$0

$20

$40

$60

Jun '

07

Sep '0

7

Dec '07

Mar '08

June

'08

Out

stan

ding

CP

(bill

ions

)

0

20

40

60

WAM

(da

ys)

Commercial Paper O/S Weighted Average Maturity

Commercial Paper Program: Citigroup Funding Inc.

18

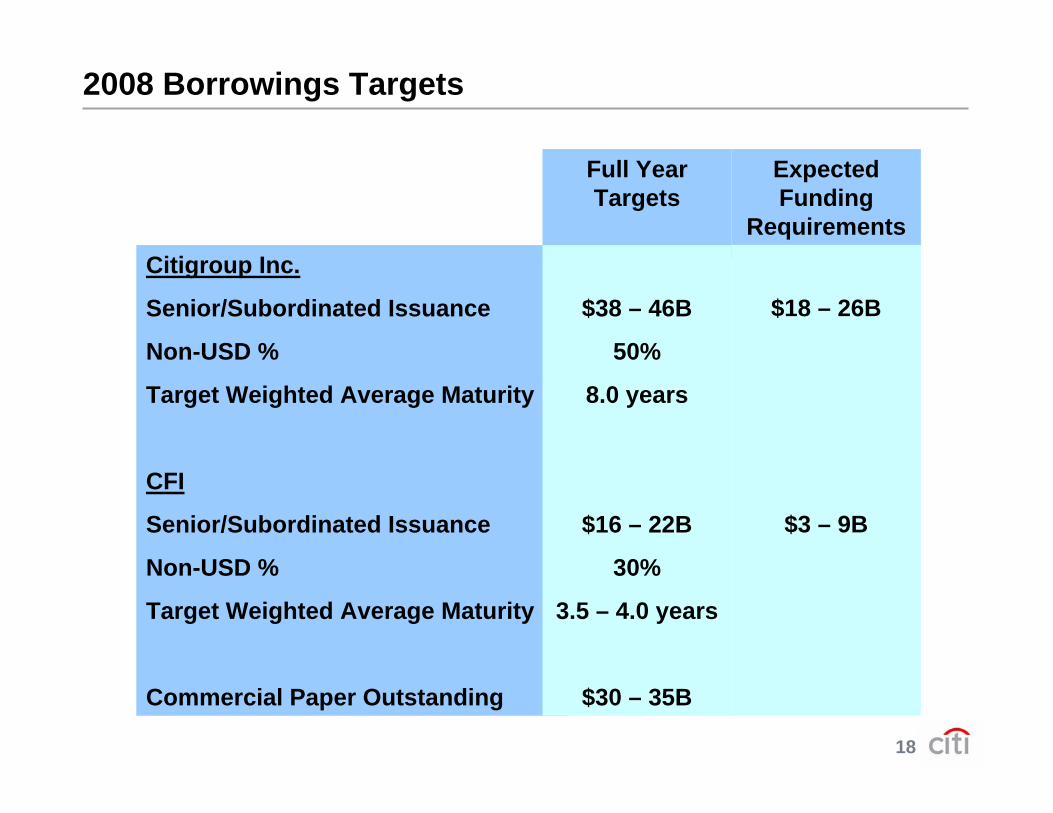

2008 Borrowings Targets

Expected Funding

Requirements

Full Year Targets

Citigroup Inc.

Senior/Subordinated Issuance

Non-USD %

Target Weighted Average Maturity

CFI

Senior/Subordinated Issuance

Non-USD %

Target Weighted Average Maturity

Commercial Paper Outstanding

$38 – 46B

50%

8.0 years

$16 – 22B

30%

3.5 – 4.0 years

$30 – 35B

$18 – 26B

$3 – 9B

19

Investor Connections

Fixed Income Investor Website– www.citigroup.com/citigroup/fixedincome

Information and Communications Resource for Fixed Income Investors

Contact us– [email protected]

20

Certain statements in this document are “forward-looking

statements” within the meaning of the Private Securities Litigation

Reform Act. These statements are based on management’s

current expectations and are subject to uncertainty and changes in

circumstances. Actual results may differ materially from those

included in these statements due to a variety of factors. More

information about these factors is contained in Citigroup’s filings

with the Securities and Exchange Commission.

Certain statements in this document are “forward-looking

statements” within the meaning of the Private Securities Litigation

Reform Act. These statements are based on management’s

current expectations and are subject to uncertainty and changes in

circumstances. Actual results may differ materially from those

included in these statements due to a variety of factors. More

information about these factors is contained in Citigroup’s filings

with the Securities and Exchange Commission.

Question and Answer SessionGary Crittenden, CFOZion Shohet, Treasurer

![[Citibank] Asset Based Finance Citibank(Bookos-z1.Org)](https://static.fdocuments.in/doc/165x107/55cf97e7550346d033945106/citibank-asset-based-finance-citibankbookos-z1org.jpg)