FIRST NINE MONTH OF 2010 - ROADSHOW - …€¦ · Financial results for first 9 months of 2010...

52

Financial results for first 9 months of 2010 Peter Straarup CEO & Chairman of the Executive Board 2 November 2010 FIRST NINE MONTH OF 2010 - ROADSHOW Lars Andreasen Acting CFO

-

Upload

duonghuong -

Category

Documents

-

view

214 -

download

0

Transcript of FIRST NINE MONTH OF 2010 - ROADSHOW - …€¦ · Financial results for first 9 months of 2010...

Financial results for first 9 months of 2010Peter StraarupCEO & Chairman of the Executive Board

2 November 2010

FIRST NINE MONTH OF 2010 - ROADSHOW

Lars AndreasenActing CFO

Agenda

Slide

• Key messages 3

• Highlights 4

• Business trends 5

• Basel III / CRD IV 18

• Macroeconomics 19

• Outlook 20

• Q&A session 21

• Appendix: Trends in focus areas & business units 22

AGENDA

2

-2,000

-1,000

0

1,000

2,000

Den

ma

rk*

No

rwa

y

Sw

eden

Ba

ltic

s

Fin

lan

d

N. I

rela

nd

Irel

an

d

Earnings recovery continues as impairments decline

• Net profit 198% Y/Y to DKK 2.6bn in 9M 2010

• Q3 result shows strong improvement in Denmark

• Cost management continues to deliver results

• Declining impairment charges

• Capital and liquidity are strong

3

DKK m

Profit before taxes(Q3 2010)

* Adjusted for Banking Package 1 (guarantee fee & loan impairment charges)

Q3 2010Q2 2010

DKK m 9M 2009 9M 2010 Index Q2 2010 Q3 2010 Index

Net interest income 20,759 17,774 86 5,927 5,840 99

Net fee income 5,601 6,185 110 2,068 2,069 100

Net trading income 16,283 7,126 44 2,817 1,930 69

Other income 2,211 2,844 129 1,091 703 64

Net income from insurance business 1,031 1,461 142 153 705 461

Total income 45,885 35,390 77 12,056 11,247 93

Expenses* 21,723 19,553 90 6,836 6,294 92

Profit bef. loan imp. charges 24,162 15,837 66 5,220 4,953 95

Loan impairment charges 20,695 10,835 52 3,479 3,083 89

Profit before tax 3,467 5,002 144 1,741 1,870 107

Tax 2,159 2,409 112 804 983 122

Net profit for the period 1,308 2,593 198 937 887 95

Cost/income ratio (%) ex integr.,GW & state guar.fee 38.8 48.5 125 50.1 48.9 98

Core tier 1 capital ratio (%) 8.5 9.8 115 9.1 9.8 107

Risk-weighted assets (DKK bn) 934 843 90 879 843 96

Total loans ex repos (DKK bn) 1,698 1,680 99 1,689 1,680 99

Deposits (ex repos) & issued RD bonds (DKK bn) 1,502 1,487 99 1,487 1,487 100

Total assets (DKK bn) 3,298 3,361 102 3,364 3,361 100

4

* Includes state guarantee fees: DKK 625 m per quarter.

Declining expenses and impairments more than offset lower income

4,500

5,500

6,500

7,500

Q1

08

Q2

08

Q3

08

Q4

08

Q1

09

Q2

09

Q3

09

Q4

09

Q1

10

Q2

10

Q3

10

Quarterly change in net interest income

Y/Y 12%Q/Q 1%

Stable quarterly net interest income not inflated by one-offs

DKK m

* White block is the net cost of government hybrid capital.

*

*

5

Quarterly net interest incomeDKK m

*

*

5,927 5,840

52 9

201

65

82 28

5,000

5,400

5,800

6,200

Q2

20

10

No.

of d

ays

Dep

osit

mar

gin

Lend

ing

mar

gin

Vol

ume

Cur

renc

y ef

fect

Oth

er *

Q3

20

10

* Includes interest on tax refund of DKK106 m in Q210 and 53m higher funding costs

*

*

Stable net fee income despite slow summer season; strong performance at Danske Capital

Activity based fees Y/Y 5% Q/Q 5%Portfolio based fees Y/Y 9% Q/Q 3%

6

Quarterly net fee incomeDKK m

0

500

1,000

1,500

2,000

2,500

Q3 09 Q4 09 Q1 10 Q2 10 Q3 10250

300

350

400

450

Q309 Q409 Q110 Q210 Q310

Quarterly fee income in Danske Capital

DKK m

Total fee income

Fee income adj. for performance fee

0

15

30

45

60

75

90

Jun-08 Mar-09 Dec-09 Sep-10

7

Net trading income at normalised level despite low activity

Breakdown of net trading income

* Q2 10 includes a capital gain of DKK 659m owing to merger of PBS Holding and Nordito AS.** 99% confidence level, 10-day horizon. Calculated as an average of daily VaR values during the period.

IndexDKK m Q2 2009 Q3 2009 Q4 2009 Q1 2010 Q2 2010 Q3 2010

Trading activities 4,410 3,194 1,791 2,013 1,665 1,420

Group Treasury 297 567 -152 119 692 99

Institutional banking (non-Nordic) 26 50 24 75 100 54

Danske Markets in total 4,733 3,811 1,663 2,207 2,457 1,573

BA Denmark 147 139 20 96 159 168

Other trading activities 38 -64 278 76 201 189

Net trading income 4,918 3,886 1,961 2,379 2,817 1,930

Value at Risk (DKK bn)** 0.2 0.2 0.2 0.2 0.3 0.3

*

VIX Volatility

Index

5.8

9.8

5.44.7

0

2

4

6

8

10

12

8

Insurance income up on strong investment return and improved unit-linked result

Net income from insurance businessDKK m 9M 2009 9M 2010 Index Q2 2010 Q3 2010 Index

Premiums (DKK bn) 14.3 17.7 124 5.7 5.5 97

Net income before postponed risk allowance 1,840 1,461 79 330 528 160

Postponed risk allowance -809 0 - -177 177 -

Net income from insurance business 1,031 1,461 142 153 705 461

Unit-linked insurance businessInvestment returns, YTDCustomers’ funds

%

Investments & liabilitiesInvestment return

9M 20109M 2009-50

0

50

100

150

200

250

-15

0

15

30

45

60

75

9M 2006 9M 2007 9M 2008 9M 2009 9M 2010

Premiums Assets under management

DKK mDKK bn

Insurance result

9

Underlying cost base continues to decline; sharp reduction Q/Q owing to seasonality

Expenses and number of employees Quarterly trend in expensesDKK m

DKKm 9M 2009 9M 2010 IndexExpenses 21,723 19,553 90Integration expenses 245 139 57Amortisation of intangibles 380 380 100Severance payments 521 109 21Goodwill impairment charges 1,417 0 -State guarantee fee (Bank Package I) 1,875 1,875 100

Underlying cost base 17,285 17,050 99

Total FTEs (end-period) 22,441 21,634 96

6,836

6,294

290

145

108 45

47

93

6,000

6,500

7,000

Q2

20

10

Hol

iday

pay

men

ts

Dep

. gua

rant

ees

Dep

r. o

f sol

d ca

rs

Pen

sion

obl

igat

ions

Sev

eran

ce p

ay

Oth

er

Q3

20

10

-50

0

50

100

150

200

-2,500

0

2,500

5,000

7,500

10,000

Q4

08

Q1

09

Q2

09

Q3

09

Q4

09

Q1

10

Q2

10

Q3

10

10

Impairment charges fell for seventh consecutive quarter, down almost 50% Y/Y

bp

Total loan imp. charges in basis points

Total impairment chargesCollective impairment charges

Quarterly loan imp. chargesDKK m

Loan impairment charges

DKK m

0

5,000

10,000

15,000

20,000

25,000

9M 2009 9M 2010

0

10

20

30

40

Q109 Q209 Q309 Q409 Q110 Q210 Q310

-1,000

1,000

3,000

5,000

7,000

9,000

Q109 Q209 Q309 Q409 Q110 Q210 Q310

11

Loan impairment charges still dominated by SMEs, but fewer customers in default

Impairments by customer segment- SMEs account for most of the Group’s impairments

PersonalFinancialsLarge corp.SMEs

Net exposures in rating categories 10 and 11*- Declining trend in rating category 11

Exposure DKK bn

Rating category 10

+9%

DKK m

Rating category 11

* Rating category 11 (customers in default)Rating category 10 (financial difficulty, not in default)

3,3192,885

2,097

2,899

2,1682,790

2,195

1,343

0

1,000

2,000

3,000

4,000

5,000

Q4 08 Q1 09 Q2 09 Q3 09 Q4 09 Q1 10 Q2 10 Q3 10

437

297

67

210

10232 3 -11

-100

0

100

200

300

400

500

600

Q4 08 Q1 09 Q2 09 Q3 09 Q4 09 Q1 10 Q2 10 Q3 10

395 385

895

554

-111

125 64 87

-250

0

250

500

750

1,000

1,250

Q4 08 Q1 09 Q2 09 Q3 09 Q4 09 Q1 10 Q2 10 Q3 10

391297

115 109

-12

103

-10 24

-200

0

200

400

600

Q4 08 Q1 09 Q2 09 Q3 09 Q4 09 Q1 10 Q2 10 Q3 10

12

Nordic impairments: Strong improvement in Denmark, stable in other Nordics

Sweden,11% of Group’s lending

Denmark, 59% of Group’s lending Finland, 9% of Group’s lending

Norway, 9% of Group’s lending

*Acc. imp. DKK 19,304 m - Individual 168 bp

- collective 24 bp

DKK m DKK m

127 bp112 bp 114 bp

137 bp

92 bp 91 bp

216 bp

25 bp

90 bp

68 bp

27 bp

55 bp

124 bp

77 bp

18 bp

* Accumulated impairments at the end of period in DKK m and as basis points of total lending. ** Exclusive of payment to Financial Stability.

82 bp 86 bp

- 28 bp

-3 bp27 bp

DKK mDKK m

111 bp

32 bp

23 bp

8 bp

*Acc. imp. DKK 2,674 m - individual 156 bp

- collective 13 bp

*Acc. imp. DKK 1,388 m - individual 69 bp

- collective 4 bp

*Acc. imp. DKK 1,503 m - Individual 92 bp

- collective 4 bp

87 bp

-2 bp

16 bp

1 bp

53 bp(33 bp **)

5 bp

22 bp

-3 bp

3,027

1,640771

75871

-124-725

229

-1,000

0

1,000

2,000

3,000

4,000

5,000

Q4 08 Q1 09 Q2 09 Q3 09 Q4 09 Q1 10 Q2 10 Q3 10

1,002

1,473 1,346 1,232 1,187 1,089

1,647

1020

0

800

1,600

2,400

Q4 08 Q1 09 Q2 09 Q3 09 Q4 09 Q1 10 Q2 10 Q3 10

213

559

839714

613

13851 -18

-400

0

400

800

1,200

Q4 08 Q1 09 Q2 09 Q3 09 Q4 09 Q1 10 Q2 10 Q3 10

415 445 419371

164120

254

409

0

250

500

750

Q4 08 Q1 09 Q2 09 Q3 09 Q4 09 Q1 10 Q2 10 Q3 10

13

Other impairments: Northern Ireland and Ireland are the most problematic

DKK m

DKK mDKK m

DKK m

Other activities

Northern Ireland, 3% of Group’s lending Ireland, 4% of Group’s lending

Baltics, 1% of Group’s lending

Incl. Danske Markets, 4% of Group’s lending

279 bp

311 bp 358 bp296 bp

633 bp

505 bp

736 bp683 bp

1,027 bp

280 bp

749 bp

1,173 bp1,039 bp

577 bp

317 bp

36 bp

127 bp

620 bp

914 bp

467 bp

96 bp

576 bp

211bp

-69 bp

* Accumulated impairments at the end of period in DKK m and as basis points of total lending.

*Acc. imp. DKK 2,839 m - individual 472 bp

- collective 53 bp

*Acc. imp. DKK 10,744 m - individual 1358 bp

- collective 119 bp

*Acc. imp. DKK 3,034 m - individual 860 bp- collective 366 bp

*Acc. imp. DKK 4,897m - individual 707 bp

- collective 57 bp

185 bp

80 bp

883 bp

-377 bp

303 bp

561 bp

143 bp-29 bp

0

20

40

60

80

Q409 Q110 Q210 Q310

Tax rate is inflated by losses in Ireland and adjustment of previous years

14

DKK m Q1 2010 Q2 2010 Q3 2010Pre-tax profit, Group 1,391 1,741 1,870Pre-tax loss, BA Ireland 992 1,553 942Gain on PBS-Nordito merger - 659 -

A Pre-tax profit, Group, adjusted 2,383 2,635 2,812

Tax according to P&L 622 804 983Portion from adj. of previous years - 47 249

B Tax , adjusted 622 757 734

B/A Tax rate, adjusted 26.1% 28.7% 26.1%

Explanation of tax rate Quarterly tax rate%

Adjusted tax rate

Actual tax rate

One-offs

0

10

20

30

40

0

50

100

150

200

2008 2009 2010 2011

Funding need for 2010 completed with duration extended; very limited need in 2011

DKK bn

Issued funding until end of Q3 2010 Estimated funding need

Funding sources- Shift towards long-term funding sources

Cen

tral

ban

ks

Cre

dit

inst

. (ex

. CB

)

Rep

o

Sho

rt-t

erm

bon

ds

Dep

osit

s

Mor

tgag

e fin

ance

(mat

ch-f

unde

d)

Cov

ered

bon

ds

long

-ter

m b

onds

Sub

ordi

nate

d de

bt

Sha

reho

lder

s' e

quit

y

Q3 2010

Q4 2008

%

New funding 2008-11- Entire funding need of DKK 30bn for 2010

already more than covered

Short-term funding Long-term funding

15

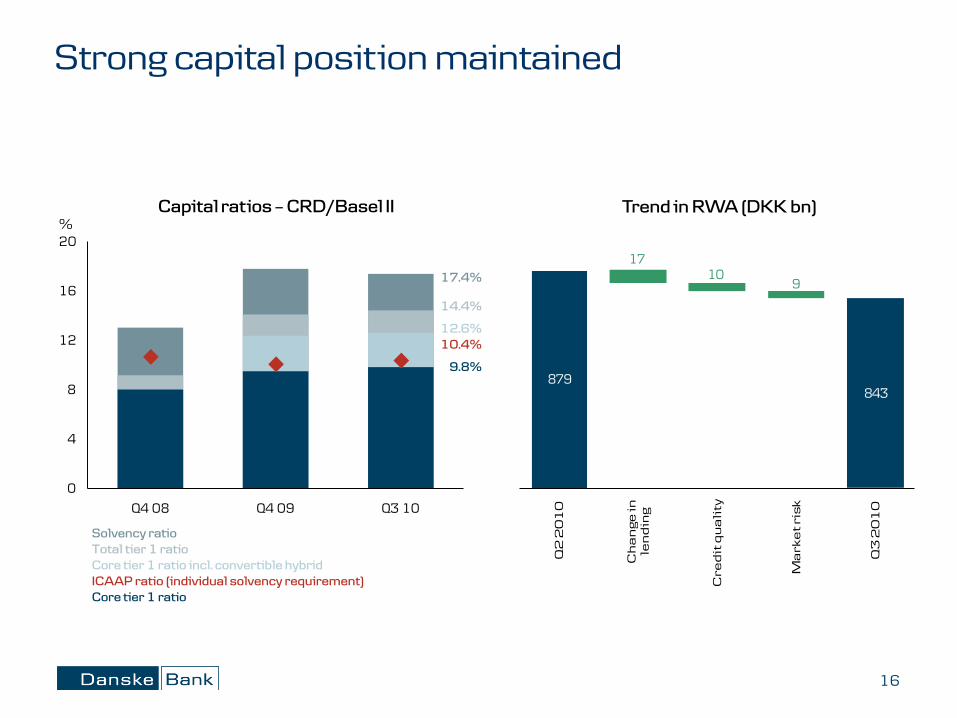

879 843

1710

9

Q2

20

10

Ch

an

ge

in

len

din

g

Cre

dit

qu

ali

ty

Ma

rke

t ri

sk

Q3

20

10

0

4

8

12

16

20

Q4 08 Q4 09 Q3 10

Strong capital position maintained

Capital ratios – CRD/Basel II Trend in RWA (DKK bn)

16

%

Solvency ratio Total tier 1 ratio Core tier 1 ratio incl. convertible hybridICAAP ratio (individual solvency requirement)Core tier 1 ratio

17.4%

14.4%

12.6%10.4%

9.8%

The new Basel III proposal is a step in the right direction, but there are still some issues

• Danske Bank is already aligned with new minimum core tier 1 ratio of 7%

• According to our preliminary assessment, Danske Bank’s core tier 1 capital will be reduced by 1 percentage point:

• RWA will increase by 5 percentage points

• Core equity will decline, mainly because of solvency requirement at Danica and minority interests

• Key concerns about the treatment of the unique Danish mortgage market have not been resolved

17

-16

-12

-8

-4

0

4

8

2009 2010E 2011E

The macroeconomic recovery is still modest

%

Source: Danske Research (October 2010).

GDP, 2009-11E(Growth Y/Y)

* Excl. one-off bank bailout costs.Source: Danske Research (October 2010).

Baltics

Ireland

Sweden

Finland

DenmarkEuroland

Norway

18

Public finances

Gross public Budget bal. Sovereign ratingdebt % of GDP % of GDP & outlook (S&P)

2010 2011Denmark 43.0 -4.4 AAA/StableSweden 43.6 -4.1 AAA/StableNorway 26.0 10.0 AAA/StableFinland 49.0 -1.5 AAA/StableIreland* 77.9 -10.0 AA/Negative

19

Outlook for the rest of 2010 remains cautious

• Macroeconomic improvement, but stable short-term rates and volumes

• Income trend in line with first nine months

• Focus on costs will continue

• Fourth-quarter specifics relative to Q3:

• Fee expenses of DKK 75 m for state guarantee on DKK 38 bn funding (80 bp)

• Expenses down DKK 625 m as fee for general state guarantee has terminated

• Expenses higher due to seasonality (holiday payments, end-of-year costs), IT investment and marketing costs

• Impairment of DKK 466 million under the state guarantee has terminated

• Solid foundation going forward

20

www.danskebank.com/ir

21

Appendix

0

250

500

750

Q1 Q2 Q3 Q4

22

Net interest income - Realkredit Danmark

DKK m

20102009

Note: ex. customer margin and interest on convertible gov’t hybrid capital.

0.75

1.25

1.75

2.25

2.75

Q1 09 Q2 09 Q3 09 Q4 09 Q1 10 Q2 10 Q3 10

23

Net interest income – NII margins by business unit

Net interest margins Q1 2009 – Q3 2010(NII /loan stock)%

Baltics

Ireland

Sweden

Norway

DenmarkGroup

Northern Ireland

Finland

0.0

0.5

1.0

1.5

2.0

2.5

Denmark Finland Sweden Norway Northern Ireland Ireland Baltics

24

Lending margins under pressure as competition grows

%

Quarterly lending margins Q1 2009 – Q3 2010(loan stock)

* Incl. Realkredit Danmark

*

-0.2

0.0

0.2

0.4

0.6

0.8

1.0

Denmark Finland Sweden Norway Northern Ireland Ireland Baltics

25

In some markets, deposit margins are benefiting from increasing short-term rates

Quarterly deposit margins Q1 2009 – Q3 2010(deposit stock)%

0

1

2

3

4

Jun-07 Dec-07 Jun-08 Dec-08 Jun-09 Dec-09 Jun-10

USD

EUR

-100

0

100

200

300

400

Jan-08 Jul-08 Jan-09 Jul-09 Jan-10 Jul-10

26

Favourable market conditions for Danske Markets, but levelling off as expected

EUR/SEK 12M volatility- High FX volatility boosts activity

%

DKK yield curve-Flattening yield curve erodes earnings%

Year

% 3 M Libor vs. overnight swap rate -spread

-Back to pre-crisis level

Covered and mortgage bond ASW spreads- Maintained low spreads on Danish covered bonds

bp, mid

Ireland

Spain

UK

Denmark

Germany

1

2

3

4

5

0 3 6 9 12 15 18 21 24 27 30

30/12/2009

30/06/2010

30/09/2010

0

5

10

15

20

Jul-08 Apr-09 Jan-10 Oct-10

0

1,000

2,000

3,000

4,000

Q1 09 Q2 09 Q3 09 Q4 09 Q1 10 Q2 10 Q3 10

Rise in trading and investment portfolio YTD driven by falling interest rates and increasing USD

Other assets +12%

Trading & inv. portfolio

Banks & repos - 21%

DKK bn

Lending - 1%

Change Y/Y

+18%

Total + 2%

Trend in total assetsend of period

27

Credit exposure decreased by 5% Y/Y

Credit exposure from lending activity, end-Q3 2010(DKK 2,330bn, including DKK 1,846bn in lending and repos)

28

Central and local governments

5% Subsidised housing companies

5%

Banks8%

Commercial property

10%

Construction, engineering and

building products2%

Diversified financials8%

Other financials3%

Energy and utilities2%

Consumer discretionary and consumer staples

9%

Transportation and shipping

3%

Other industrials8%

Personal customers37%

0

20

40

60

80

2001 2002 2003 2004 2005 2006 2007 2008 2009 9M 2010

Source: Moody’s and own data.

Upgrades/downgrades ratio is improving, but Denmark continues to lag

29

Downturn DownturnUpturn

Upgrades > downgrades

Downgrades > upgrades

Upgrades / total internal rating changes on the corporate book%

Denmark

Outside Denmark

0

100

200

300

400

500

19

79

19

80

19

81

19

82

19

83

19

84

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

09

10

30

Much larger increase in bankruptcies in Denmark than in the other Nordic countries

SwedenFinland

Denmark

Norway

Number of monthly bankruptcies in the Nordics(indexed, Jan. 1996 =100)

Index

Denmark updated until September 2010.Source: EcoWin.

Credit exposure to commercial property and construction segments

3131

DKK bnCommercial

property

Portion from

developers

Construction and building

materialsSector in

totalDenmark 109.5 1.0 12.7 122.1Finland 15.2 0.6 6.7 21.9Sweden 57.0 0.2 4.8 61.8Norway 32.7 2.4 2.4 35.1Northern Ireland 9.8 3.2 4.4 14.2Ireland 15.7 4.4 3.3 19.1Baltics 2.2 0.8 0.5 2.7Other 1.1 0.1 2.3 3.3Total 243.1 12.7 37.1 280.2

Gross exp. subject to individual imp.testing 32.3 7.4 39.7Individual impairment charges 12.2 3.4 15.6 Portion from BA Ireland 7.8

Exposure to agriculture DKK bn Realkredit Danmark 45Banking Activities Denmark 13Other business units 14Agriculture 71

Agriculture LTV, Realkredit Danmark %Q4 2008 46Q4 2009 64Q2 2010 72Q3 2010 71

Danish agriculture sector pressured by lower property and output prices

32

Agriculture26%

Cattle breeding24%Pig breeding

23%

Grocery trade14%

Mixed operations

7%

Other6%

429 511

183281

1,097

2,990

1,801

1,986

595

0

500

1,000

1,500

2,000

2,500

3,000

Denmark Finland Sweden Norway Northern Ireland

Ireland Baltics Other Act. Group

Q208 Q308 Q408 Q109 Q209 Q309 Q409 Q110 Q210 Q310

Gross exposure subject to individual imp. test in basis points of total loansbp

33

Gross exp. subject to individual imp. test; reflects difficult economic conditions in certain markets

43.2

5.7

11.4

10.4

7.36.5 0.4

8.13.44.55.9

21.7

4.411.1

60.666.3

77.8

88.195.5

102.0 102.4 102.4

0

20

40

60

80

100

120

Q1 09 Q2 09 Q3 09 Q4 09 Q1 10 Q2 10 Q3 10 Q3 10

Gross exposure subject to individual impairment testDKK bn

34

Quarterly trend in gross exposure subject to individual impairment test

In basis points of gross lending

Ireland 2,990 bp

Other 1,986 bp

Finland 511 bp

Denmark 429 bp

Norway 281 bp

Baltics 1,801 bp

Sweden 183 bp

N. Ireland 1,097 bp

140

160

180

200

4,000

8,000

12,000

16,000

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

E

20

11

E

20

12

E

Region Prices Price fall Change inpeaked since peak (%) Q310 (%)

Copenhagen Q3 2006 -24.9 1.4Zealand Q3 2007 -21.6 0.4South Denmark Q1 2008 -3.8 -0.6Central Jutland Q4 2007 -1.8 1.3North Jutland Q2 2010 -1.4 -1.4Denmark overall Q2 2007 -12.5 0.6

0

500

1,000

1,500

2,000

0

5

10

15

19

80

19

84

19

88

19

92

19

96

20

00

20

04

20

08

0

100

200

300

400

500

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

Q3

10

35

Property pricesIndex 1996 = 100

Correlation between unemploymentand foreclosures in Denmark

10-year yield

Unemployment

Foreclosures

Source: Danske Research.

No.

Ireland

UK

Norway

DenmarkFinlandSweden

Source: Danske Research.

Signs of housing market stabilising

Correlation between house prices and consumption in Denmark

Source: Danske Research.

Source: Realkredit Denmark.

Consumption

Priceper sqm. DKK bn

House prices

Danish house price development by regions

%

9M

10

0.4

0.6

0.8

1.0

1.2

Feb-

09

Mar

-09

Apr

-09

May

-09

Jun-

09

Jul-0

9

Aug

-09

Sep

-09

Oct

-09

Nov

-09

Dec

-09

Jan-

10

Feb-

10

Mar

-10

Apr

-10

May

-10

Jun-

10

Jul-1

0

Aug

-10

0

25

50

75

100

125

150

0

1,500

3,000

4,500

6,000

20

01

20

02

20

03

20

04

20

05

20

06

20

07

Q1

08

Q2

08

Q3

08

Q4

08

Q1

09

Q2

09

Q3

09

Q4

09

Q1

10

Q2

10

Q3

10

Mortgages in Denmark: low average LTV ratio, arrears picking up, but still low

Mortgage finance: number of arrears, end-period 3- & 6-month arrears and repossessed properties No. No.

Danish mortgages• 145 repossessed properties and 3908 arrears out

of 412,262 loans at end-Q3 (0.9%)• 1.1% of loans with LTV>80% and low rating• Max. 80% LTV on origination for private individuals

(legal requirement)• Max. 60% LTV on origination for commercial

mortgages (legal requirement)• Average LTV of 68% at end-Q3

Breakdown of loans by LTV and rating categoryMortgage finance (residential & commercial)

End-Q310

Arrears on retail loans with monthly payments - Improvement due to lower rates on 1 year floaters

%

36

LTV/rating 1-3 4-7 8-11 Total

0-20% 8.6% 21.8% 4.2% 34.6%

20-40% 5.9% 18.5% 3.9% 28.2%

40-60% 3.5% 13.6% 3.2% 20.4%

60-80% 1.7% 7.9% 2.1% 11.7%

>80% 1.0% 3.1% 1.1% 5.2%

Total (DKK bn) 147 462 104 712

Credit bonds 5%

Certificates 2%Quasi-

government 2%

Swedish covered bonds

15%

Other covered bonds 5%

Governments & municipals 27%

Danish mortgage bonds

44%

Liquid, highly rated bond portfolio

Bond portfolio(DKK 418bn)

37

Rating distribution

Level 1-3 assets

Level 1 89%Level 2 11%Level 3 0%

AAA 82%

AA+ 7%

AA 1%

AA- 4%

A+ 2%

A 1%

A- 0%

BBB+ 0%

BBB 1%

BBB- 0%

BB+ 0%

BB 0%

BB- 0%

Lower 0%

NA 1%

-150

0

150

300

450

1 m

onth

2 m

onth

s

2 m

onth

s

4 m

onth

s

5 m

onth

s

6 m

onth

s

9 m

onth

s

12

mon

ths

105

110

115

120

125

0

100

200

300

400

Q408 Q109 Q209 Q309 Q409 Q110 Q210 Q310

Strong loan-to-deposits ratio and liquidity position

38

Loan-to-deposit gap (DKK bn) and ratio (%)

Note: Deposits include Realkredit Denmark bonds.

DKK bn %

Loan-to-deposit gap Loan-to-deposit ratio

DKK bn

* Main assumptions: No access to capital markets; no refinancing of debt to credit institutions, issued bonds or subordinated capital; and moderate reduction of business activities.

12-month liquidity*Moody’s Financial Strength

End-Q3 2010

End-Q4 2008

End-Q4 2009

Well-diversified funding position

• 57% deposits and fully match-funded Danish mortgage bonds (net)

• Long-term bonds DKK 186bn

• Issued covered bonds DKK 117bn

• Termination of state guarantee at end-September has not changed the funding market.

• Total borrowing decreased by DKK 48 billion in Q3 due to scheduled repayment

39

Deposits, 32%

Match-funded DK mortgage bonds,

25%

Covered bonds, 4%

Subordinated debt, 3%

L-T bonds, 8%

S-T bonds, 7%

Banks, net, 6%

Repos, 6%

Central banks, 4%Equity, 4%

Frontloaded on funding in 2010; all completed with long duration and without guarantees

• YTD Danske Bank has issued bonds for DKK 40 bn, covering more than the estimated long-term funding needed for 2010 (DKK 30 bn)

• 47% of the issuance in covered bonds and 53% in senior debt

• Longest maturity: 15 years

• Weighted average maturities:

– All issues: 7 years– Covered bonds: 10 years– Senior debt: 4 years

• First 12-year covered bond benchmark from Nordic issuer

40

Issues by type and currency

Issue type Currency DKK bnCovered bonds EUR 17

NOK 2CHF 1

Senior debt EUR 11USD 4GBP 3Other 2

Total 40

0

1

2

3

4

Q309 Q409 Q110 Q210 Q310

20

25

30

35

Q309 Q409 Q110 Q210 Q310

41

Banking Activities Denmark: Improvement due to lower costs and impairments, but s-t rate hurts

Profit before loan impairment charges 21%- Declining NII reduces income, partly offset by drop in expenses

DKK bn

Trend in lending volume(average)

Corporate: Y/Y 6%Q/Q 0%

Retail: Y/Y 0%Q/Q 0%

% Market shares(ex Realkredit Danmark)

Deposits

Lending

Deposits

Lending

% Margin trends(ex Realkredit Danmark)

Note: As per 1.1. 2010 operating leasing moved from BA Denmark to Other Banking Act.Move reduces BA Denmark’s quarterly other income and expenses by approx. DKK 150m.

DKK m 9M 2009 9M 2010 IndexNet interest income 12,075 10,015 83 Net fee income 2,708 2,970 110 Other income 1,240 770 62 Total income 16,023 13,755 86 Total expenses 9,311 8,442 91 Profit bef. loan imp. charges 6,712 5,313 79 Loan impairment charges 7,881 6,328 80 Profit before tax -1,169 -1,015 -Bank pack.1 (fees & loan imp.charges) 3,078 3,268 106 Adj. profit before tax 1,909 2,253 118

ROE before loan imp. chgs 23.0 18.90

150

300

450

600

Q309 Q409 Q110 Q210 Q310

0.0

0.5

1.0

1.5

Q309 Q409 Q110 Q210 Q310

6

9

12

15

18

Q309 Q409 Q110 Q210 Q310

Banking Activities Finland: Lower costs and imp. charges, but declining NII reduces profit

Profit before loan impairment charges 53%- NII pressured by low interest rates despite strong deposit growth

Trend in lending volume(average)

%

Deposits

Lending

42

DKK bn Retail: Y/Y 3%Q/Q 2%

Corporate: Y/Y 12%Q/Q 1%

Deposits

Lending

% Market sharesMargin trends

DKK m 9M 2009 9M 2010 IndexNet interest income 2,387 1,739 73 Net fee income 818 863 106 Other income 337 313 93 Total income 3,542 2,915 82 Total integration expenses 520 491 94 Expenses ex total intgr. exp. 1,979 1,937 98 Profit bef. loan imp. charges 1,043 487 47 Loan impairment charges 1,834 276 15 Profit before tax -791 211

ROE before loan imp. chgs 18.5 9.7 50

75

100

Q309 Q409 Q110 Q210 Q310

0.0

0.5

1.0

1.5

Q309 Q409 Q110 Q210 Q310

25

50

75

100

125

Q309 Q409 Q110 Q210 Q310

0

2

4

6

8

Q309 Q409 Q110 Q210 Q310

43

Banking Activities Sweden: Benefits from increasing short-term rates and low impairments

Profit before loan impairment charges 21%- Affected by 11% appreciation of SEK against DKK

Trend in lending volume(average, %-change in local currency)

% Market shares

LendingLending

Deposits

Deposits

DKK bn Retail: Y/Y 17%Q/Q 5%

Corporate: Y/Y 2%Q/Q 1%

% Margin trends

DKK m 9M 2009 9M 2010 IndexNet interest income 1,508 1,710 113 Net fee income 467 515 110 Other income 101 125 124 Total income 2,076 2,350 113 Expenses 1,095 1,161 106 Profit bef. loan imp. charges 981 1,189 121 Loan impairment charges 521 117 22 Profit before tax 460 1,072 233

ROE before loan imp. chgs 15.8 19.3

0

2

4

6

8

10

Q309 Q409 Q110 Q210 Q310

0.0

0.5

1.0

1.5

Q309 Q409 Q110 Q210 Q310

44

Banking Activities Norway: Lower loan imp. charges lead to improved profit before taxes

Profit before loan impairment charges 14%- Costs 4% in local currency. 10% appreciation of NOK against DKK

Trend in lending volume(average %-change in local currency)

%

DepositsDeposits

Lending

Lending

Retail: Y/Y 16%Q/Q 2%

Corporate: Y/Y 1%Q/Q 1%

DKK bn

% Market sharesMargin trends

DKK m 9M 2009 9M 2010 IndexNet interest income 1,988 1,764 89 Net fee income 254 279 110 Other income 436 519 119 Total income 2,678 2,562 96 Expenses 1,349 1,417 105 Profit bef. loan imp. charges 1,329 1,145 86 Loan impairment charges 574 24 4 Profit before tax 755 1,121 148

ROE before loan imp. chgs 23.0 19.725

50

75

100

125

Q309 Q409 Q110 Q210 Q310

0

10

20

30

40

Q309 Q409 Q110 Q210 Q310 0.0

0.5

1.0

1.5

2.0

2.5

Q309 Q409 Q110 Q210 Q310

DKK m 9M 2009 9M 2010 IndexNet interest income 978 899 92 Net fee income 221 232 105 Other income 54 79 146 Total income 1,253 1,210 97 Total integration expenses 53 0 -Expenses ex total intgr. exp. 812 867 107 Profit bef. loan imp. charges 388 343 88 Loan impairment charges 1,235 783 63 Profit before tax -847 -440 -

ROE before loan imp. chgs 26.1 24.1

45

Banking Activities Northern Ireland: Resilient top line, but loan impairments still high

Profit before loan impairment charges 12%- Slightly declining NII despite higher deposits (in local currency)

Market shares%Margin trends%

Trend in lending volume(average, %-change in local currency)

Corporate

Retail

Lending

Deposits

* Corporate lending growth is adjusted for lending to public authorities.

DKK bn

* *

0

25

50

Q309 Q409 Q110 Q210 Q310 * Incl. a levy of DKK 49m in 9M09 and DKK 45m in 9M10

by the UK financial services compensation scheme.

Corporate: Y/Y 7%*Q/Q 1%*

Retail: Y/Y 3%Q/Q 0%

0

2

4

6

8

Q309 Q409 Q110 Q210 Q310

46

Banking Activities Ireland: Still high impairment charges for commercial property segment

%

Profit before loan impairment charges 24%- Income under pressure, cost reduction not fully visible until 2011

Margin trends% Market shares

Trend in lending volume(average)

Lending

Deposits

Lending

Deposits

DKK bnRetail: Y/Y 7%

Q/Q 2%Corporate: Y/Y 5%

Q/Q 3%

DKK m 9M 2009 9M 2010 IndexNet interest income 897 809 90 Net fee income 98 80 82 Other income 42 35 83 Total income 1,037 924 89 Total integration expenses 24 0 -Expenses ex total intgr. exp. 658 655 100 Profit bef. loan imp. charges 355 269 76 Loan impairment charges 4,051 3,756 93 Profit before tax -3,696 -3,487 -

ROE before loan imp. chgs 14.6 12.6 0

25

50

Q309 Q409 Q110 Q210 Q310

0.0

0.5

1.0

1.5

2.0

Q309 Q409 Q110 Q210 Q310

-0.5

0.0

0.5

1.0

1.5

2.0

Q309 Q409 Q110 Q210 Q310 0

5

10

15

Q309 Q409 Q110 Q210 Q310

0

10

20

Q309 Q409 Q110 Q210 Q310

47

Banking Activities Baltics: Profit turns positive as loan impairment charges normalises

Profit before loan impairment charges turns positive- Increased efficiency and profitability due to tight cost control Trend in lending volume

(average)

%Market shares – lending

Retail: Y/Y 6%Q/Q 2%

Corporate: Y/Y 16%Q/Q 3%

Estonia

Latvia

Lithuania

DKK bn

Margin trends

Deposits

Lending%

DKK m 9M 2009 9M 2010 IndexNet interest income 378 376 99 Net fee income 100 115 115 Other income 98 83 85 Total income 576 574 100 Goodwill impairment charges 1,417 0 -Expenses ex. gw imp. charges 287 259 90 Profit bef. loan imp. charges -1,128 315 -Loan impairment charges 2,112 171 8 Profit before tax -3,240 144 -

ROE before loan imp.chgs & gw 27.5 36.0

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

48

Danske Markets: Income down to more normal level

Profit before tax down to more normal level- Decline reflects exceptionally high income in 9M09

Quarterly breakdown of income

Trading activities – accumulated incomeFixed income and forex

2010 2008

Q1 Q2 Q3 Q4

Market position in the Nordics- Strong position in all main product areas

Source: Prospera.

2009

DKK m 9M 2009 9M 2010 IndexTotal income 15,575 6,237 40 Expenses 2,231 2,077 93

Profit bef.loan imp.charges 13,344 4,160 31

Loan impairment charges 2,343 -683 -

Profit before tax 11,001 4,843 44

ROE before loan imp. chgs 381.6 115.0

DKK m Q4 2009 Q1 2010 Q2 2010 Q3 2010Trading activities 1,791 2,013 1,665 1,420Group Treasury -152 119 692 99

Institutional banking (non-Nordic) 24 75 100 54

Danske Markets in total 1,663 2,207 2,457 1,573

*Q2 10 includes a capital gain of DKK 659m owing to merger of PBS Holding and Nordito AS.

*

Product area / # NordicFixed income 2 1 3 2 2Forex 1 2 3 2 2Derivatives 2 1 1 1 1Equities 1 6 11 2 5

49

Danske Capital: Net fees up 23% due to higher volume in assets under management

AuM – Customer breakdownDKK bn

AuM – Asset breakdown

%

Bonds

Equities

Cash

Margin for asset management(adjusted income incl. performance fee/business volume end of period)

Life insurance

Retail cust.

Institutional

Private equity

Profit before loan impairment charges 4%- Lower total income reflects change of business Luxembourg

%

0

25

50

75

100

Q309 Q409 Q110 Q210 Q310

0.10

0.15

0.20

0.25

0.30

0.35

Q309 Q409 Q110 Q210 Q310

0

200

400

600

Q309 Q409 Q110 Q210 Q310

DKK m 9M 2009 9M 2010 IndexNet fee income 873 1,074 123 Total income 1,236 1,199 97 Expenses 718 702 98 Profit bef. loan imp. chrg ex.GL&off-offs 518 497 96 Loan impairment charges 54 4 7 Profit before tax 464 493 106

-60%

-40%

-20%

0%

20%

40%

60%

-2% -1% 0% 1% 2%

Cha

nge

in e

quit

y pr

ices

Change in interest rate

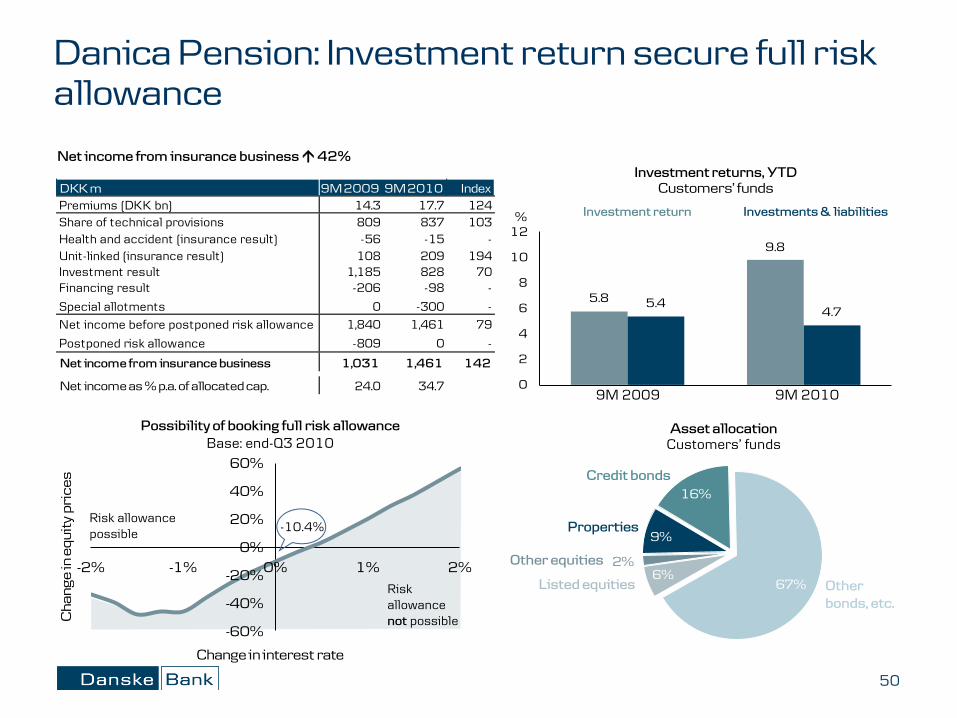

6%2%

9%

16%

67%

5.8

9.8

5.44.7

0

2

4

6

8

10

12

Risk allowance possible

Risk allowance not possible

Danica Pension: Investment return secure full risk allowance

Investment returns, YTDCustomers’ funds

Net income from insurance business 42%

%

Possibility of booking full risk allowance Base: end-Q3 2010

Investments & liabilitiesInvestment return

Other bonds, etc.

Listed equities

Other equities

Asset allocationCustomers’ funds

Properties-10.4%

50

9M 20109M 2009

DKK m 9M 2009 9M 2010 IndexPremiums (DKK bn) 14.3 17.7 124Share of technical provisions 809 837 103Health and accident (insurance result) -56 -15 -Unit-linked (insurance result) 108 209 194Investment result 1,185 828 70Financing result -206 -98 -

Special allotments 0 -300 -Net income before postponed risk allowance 1,840 1,461 79

Postponed risk allowance -809 0 -

Net income from insurance business 1,031 1,461 142

Net income as % p.a. of allocated cap. 24.0 34.7

Credit bonds

837

Profit model DKK m

• Risk allowance 64 bp of technical prov. (DKK 174 bn)

• Return on investment portfolio at shareholders’ risk 828

• Financing result-98

• Insurance result, Unit linked long-term: 0.4-0.5% of AuM

209

Total 1461

Condition / sensitivity

• No usage of bonus potential of paid-up policies and sufficient investment income

• Equity markets, interest rates

• ST interest rate (equity –alloc. cap. + subord. bonds)

• High new sales will lower result and vice versa

9M 2010

• Positive technical basis of DKK 3.6 bn

• Annualised investment return: 3.5%

• Low short-term interest rate

+

+

+

=

∑

1

2

3

4

51

Danica’s profit model

• Special allotments, depending on profit and business volume -300

• Expected to be –DKK 0.5 bn p.a. in next 2-4 years, then declining5

• DKK 300 m in Q1-Q3 2010

• Shadow account

• Health & accident 0

-15

• DKK 583 m remains

• Combined ratio6

• Possibility of booking evaluated at the end of the year

• High competition

+

+

• Result of unit-linked business is now positive

Disclaimer

This presentation does not constitute or form part of and should not be construed as, an offer to sell or issue or the solicitation of an offer to buy or acquire securities of Danske Bank A/S in any jurisdiction or an inducement to enter into investment activity. No part of this presentation, nor the fact of its distribution, should form the basis of, or be relied on in connection with, any contract or commitment or investment decision whatsoever.

This presentation contains forward-looking statements that reflect management’s current views with respect to certain future events and potential financial performance. Although Danske Bank believes that the expectations reflected in such forward looking statements are reasonable, no assurance can be given that such expectations will prove to have been correct. Accordingly, results could differ materially from those set out in the forward-looking statements as a result of various factors many of which are beyond Danske Bank’s control.

This presentation does not imply that Danske Bank has undertaken to revise these forward-looking statements, beyond what is required by applicable law or applicable stock exchange regulations if and when circumstances arise that will lead to changes compared to the date when these statements were provided.

52

![First Nine Weeks - lcboe.net grade[1].docx · Web viewLaurens County Pacing Guide. First Nine Weeks. Units 1-3. Second Nine Weeks](https://static.fdocuments.in/doc/165x107/5a9d95527f8b9a21688ca075/first-nine-weeks-lcboe-grade1docxweb-viewlaurens-county-pacing-guide-first.jpg)