Financial results Q1 2017 - SHW · 2017-12-04 · Q1 2016 Q1 2017. 3 > Sales development as...

17

Outlook for fiscal year 2017 confirmed Financial results Q1 2017 Analyst and Investor Conference Call, 3 May 2017

Transcript of Financial results Q1 2017 - SHW · 2017-12-04 · Q1 2016 Q1 2017. 3 > Sales development as...

Outlook for fiscal year 2017 confirmed

Financial results Q1 2017

Analyst and Investor Conference Call, 3 May 2017

1

Agenda

> Financial results January to March 2017

> Outlook for fiscal year 2017

Drive international growth and leverage

innovation leadership

2

Stable market environment in Q1 2017

SHW well positioned to benefit from structural market changes and strong demand

for mobility solutions

> Light vehicle production: +

4.2 per cent to 24.0 million

units with marked growth

rate differences

> Gasoline engines gain

further market share; diesel

engines stable

> Above-average growth rates

for automatic transmissions

– global production

increased by 8.0 per cent to

14.0 million units

Light Vehicle Production(< 6 t) (m units)

Source: IHS, April 2017

Global Engine Production(m units)

Global Transmission Production(m units)

104.3106.6

SHW Group Sales (€m)

4.94.8

Gasoline

18.918.1

Diesel

13,0

10,0

14,0

9,8

AutomaticManual

5.95.5

China

6.76.5

South

America

0.70.6

North

America

4.54.5

Europe

Q1 2016

Q1 2017

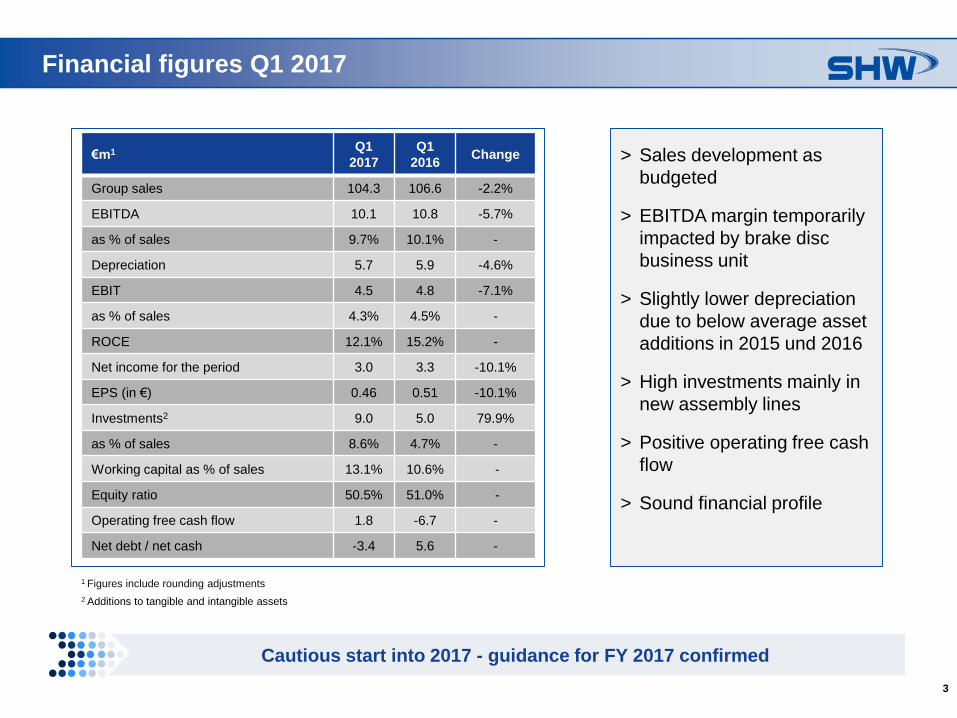

3

> Sales development as

budgeted

> EBITDA margin temporarily

impacted by brake disc

business unit

> Slightly lower depreciation

due to below average asset

additions in 2015 und 2016

> High investments mainly in

new assembly lines

> Positive operating free cash

flow

> Sound financial profile

Financial figures Q1 2017

Cautious start into 2017 - guidance for FY 2017 confirmed

€m1 Q1

2017

Q1

2016Change

Group sales 104.3 106.6 -2.2%

EBITDA 10.1 10.8 -5.7%

as % of sales 9.7% 10.1% -

Depreciation 5.7 5.9 -4.6%

EBIT 4.5 4.8 -7.1%

as % of sales 4.3% 4.5% -

ROCE 12.1% 15.2% -

Net income for the period 3.0 3.3 -10.1%

EPS (in €) 0.46 0.51 -10.1%

Investments2 9.0 5.0 79.9%

as % of sales 8.6% 4.7% -

Working capital as % of sales 13.1% 10.6% -

Equity ratio 50.5% 51.0% -

Operating free cash flow 1.8 -6.7 -

Net debt / net cash -3.4 5.6 -

2 Additions to tangible and intangible assets

1 Figures include rounding adjustments

4

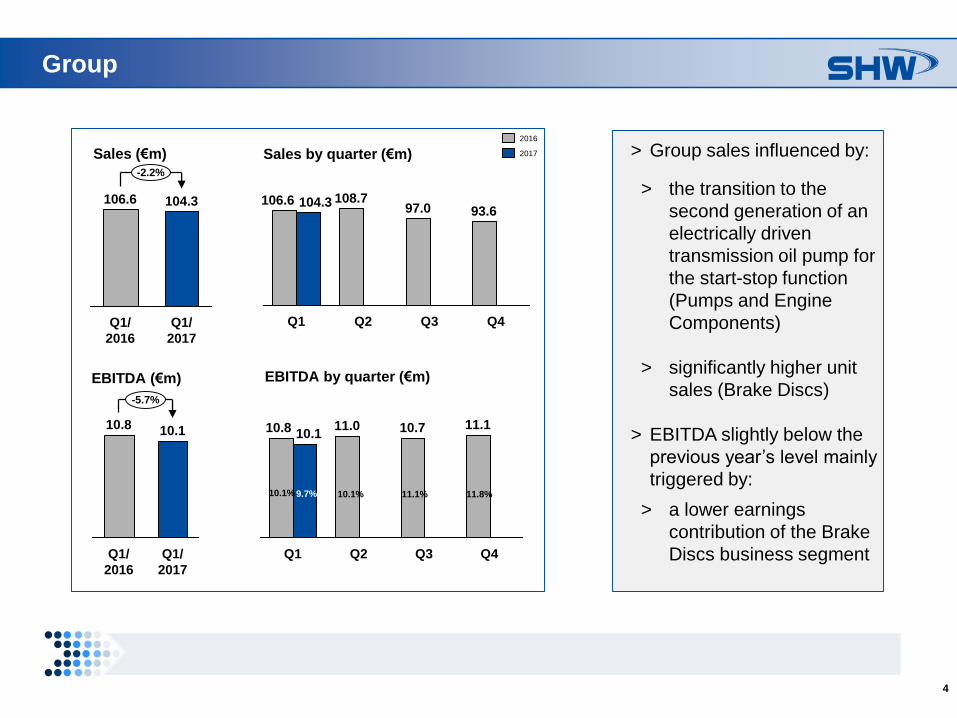

Group

Sales by quarter (€m)

EBITDA (€m)

Sales (€m)

Q1/

2017

104.3

Q1/

2016

106.6

-2.2%

Q4

93.6

Q3

97.0

Q2

108.7

Q1

104.3106.6

10.8

-5.7%

Q1/

2017

10.1

Q1/

2016

> Group sales influenced by:

> the transition to the

second generation of an

electrically driven

transmission oil pump for

the start-stop function

(Pumps and Engine

Components)

> significantly higher unit

sales (Brake Discs)

> EBITDA slightly below the

previous year’s level mainly

triggered by:

> a lower earnings

contribution of the Brake

Discs business segment

EBITDA by quarter (€m)

Q4

11.1

Q3

10.7

Q2

11.0

Q1

10.110.8

10.1%

2016

2017

9.7% 10.1% 11.1% 11.8%

5

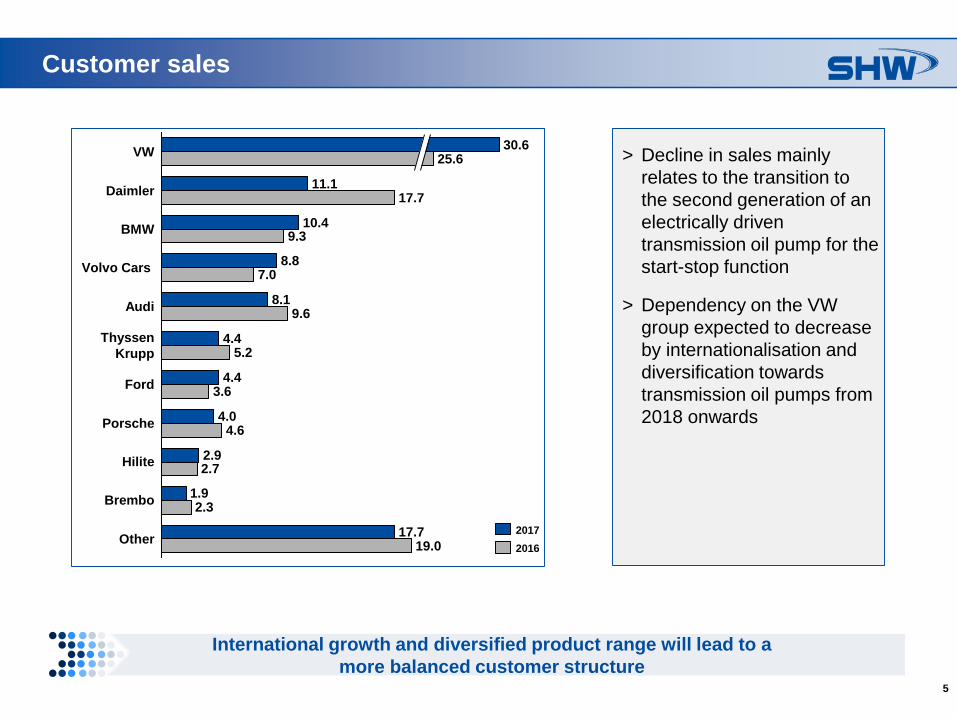

Customer sales

International growth and diversified product range will lead to a

more balanced customer structure

> Decline in sales mainly

relates to the transition to

the second generation of an

electrically driven

transmission oil pump for the

start-stop function

> Dependency on the VW

group expected to decrease

by internationalisation and

diversification towards

transmission oil pumps from

2018 onwards

VW

Other

3.6

4.6

Ford

4.0

2.7

Porsche

2.9

2.3

Hilite

1.9

19.0

Brembo

17.7

4.4

9.6

Volvo Cars

8.1

5.2

Audi

4.4

7.08.8

Daimler11.1

17.7

BMW10.4

9.3

30.625.6

Thyssen

Krupp

2016

2017

6

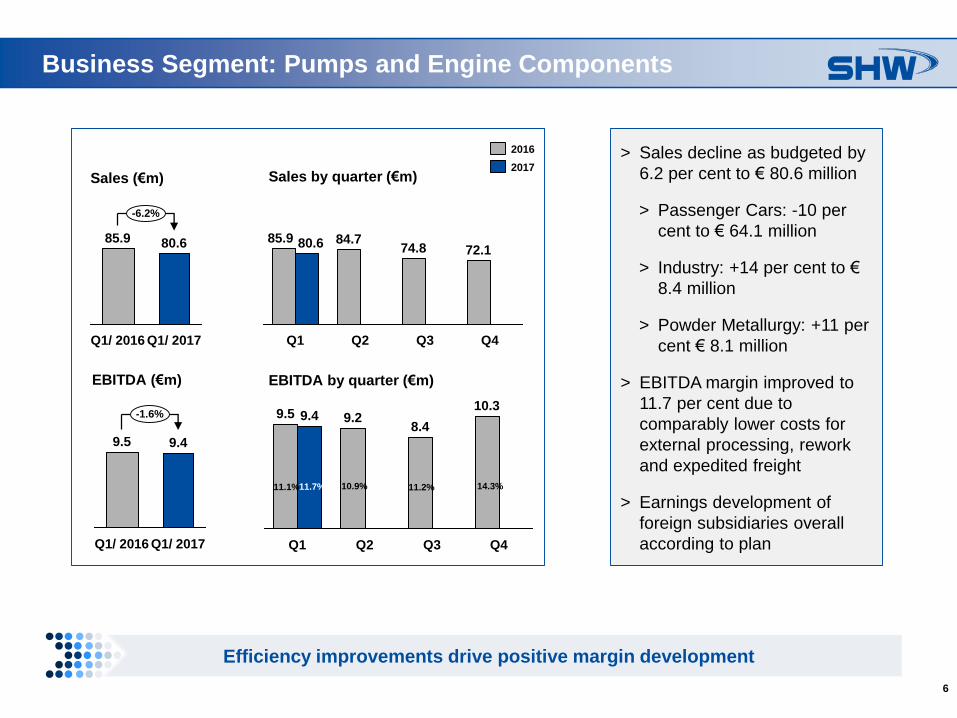

Business Segment: Pumps and Engine Components

Efficiency improvements drive positive margin development

> Sales decline as budgeted by

6.2 per cent to € 80.6 million

> Passenger Cars: -10 per

cent to € 64.1 million

> Industry: +14 per cent to €

8.4 million

> Powder Metallurgy: +11 per

cent € 8.1 million

> EBITDA margin improved to

11.7 per cent due to

comparably lower costs for

external processing, rework

and expedited freight

> Earnings development of

foreign subsidiaries overall

according to plan

Sales by quarter (€m)

EBITDA (€m)

Sales (€m)

Q4

74.8 72.185.9 80.6 84.7

Q2Q1 Q3Q1/ 2016

80.685.9

Q1/ 2017

-6.2%

EBITDA by quarter (€m)

10.3

8.4

Q3

9.2

Q2 Q4Q1

9.49.5

11.1%11.7% 10.9% 11.2% 14.3%

2017

2016

Q1/ 2016

9.49.5

Q1/ 2017

-1.6%

7

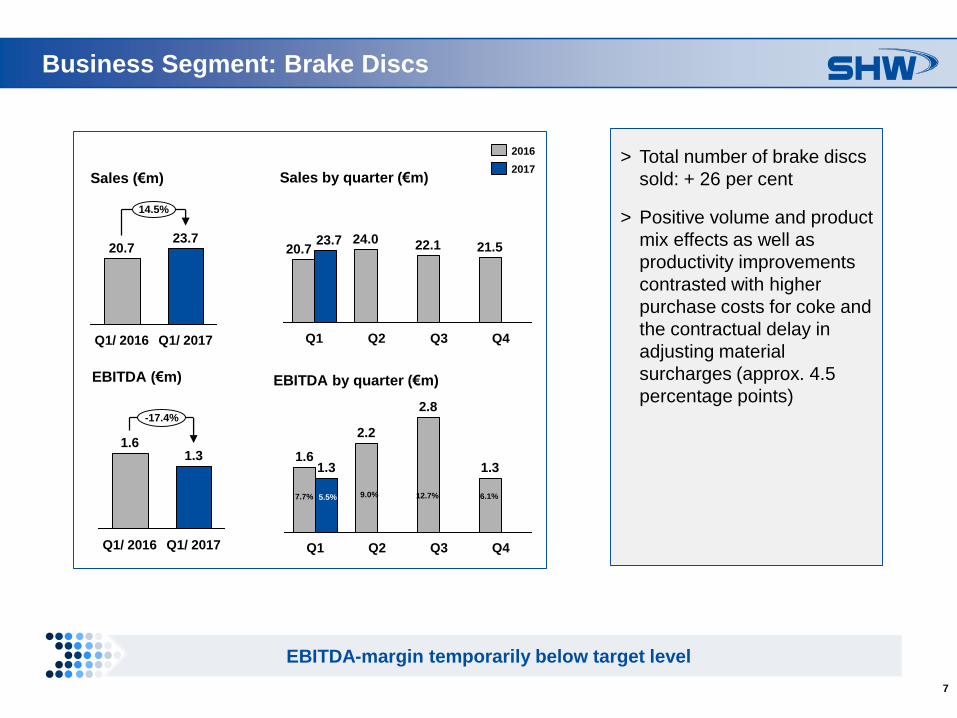

Business Segment: Brake Discs

EBITDA-margin temporarily below target level

> Total number of brake discs

sold: + 26 per cent

> Positive volume and product

mix effects as well as

productivity improvements

contrasted with higher

purchase costs for coke and

the contractual delay in

adjusting material

surcharges (approx. 4.5

percentage points)

Q4

21.5

Q3

22.1

Q2

24.0

Q1

23.720.7

Q1/ 2016

20.7

14.5%

Q1/ 2017

23.7

Q4

1.3

Q3

2.8

Q2

2.2

Q1

1.31.6

7.7% 5.5% 9.0% 12.7%

2017

2016

Sales by quarter (€m)Sales (€m)

EBITDA (€m) EBITDA by quarter (€m)

6.1%

-17.4%

Q1/ 2017

1.3

Q1/ 2016

1.6

8

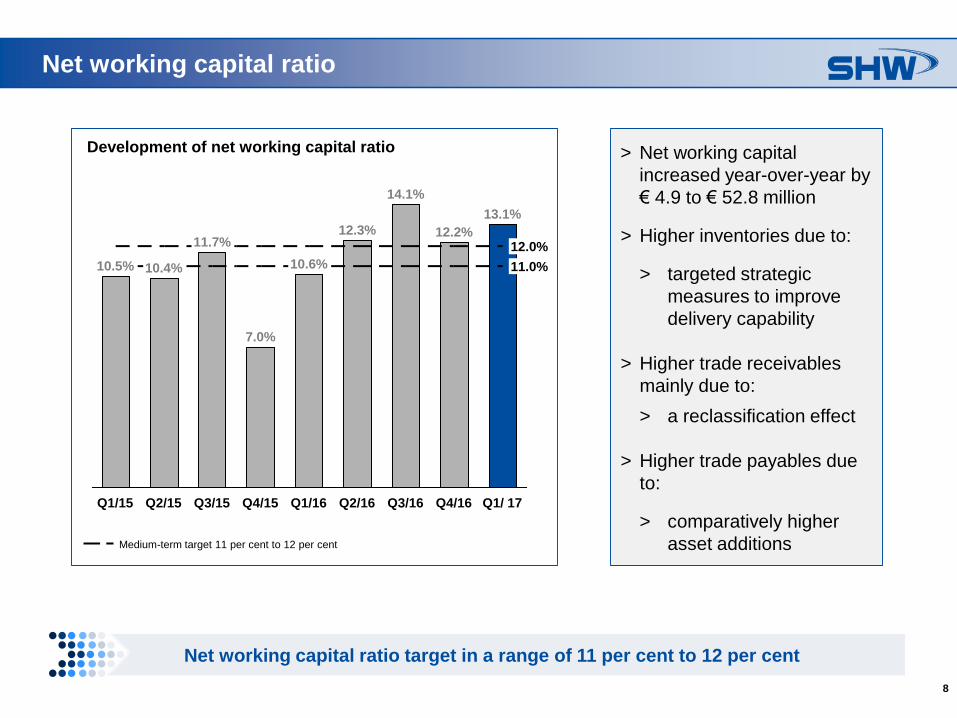

Net working capital ratio

Net working capital ratio target in a range of 11 per cent to 12 per cent

> Net working capital

increased year-over-year by

€ 4.9 to € 52.8 million

> Higher inventories due to:

> targeted strategic

measures to improve

delivery capability

> Higher trade receivables

mainly due to:

> a reclassification effect

> Higher trade payables due

to:

> comparatively higher

asset additions

13.1%

Q1/15

10.5%

12.3%

Q1/16

10.6%

Q4/15

7.0%

Q3/15

11.7%

Q2/15

10.4%

Q1/ 17

12.0%

11.0%

Q4/16

12.2%

Q3/16

14.1%

Q2/16

Development of net working capital ratio

Medium-term target 11 per cent to 12 per cent

9

Investments and depreciation

> Investments in property,

plant and equipment and

intangible assets at a total of

€ 9.0 million

> Pumps & Engine

Components: mainly for new

assembly lines in Germany

and China (total: € 7.5m)

> Brake Discs: mainly for

second automated

aluminium casting line (total:

€ 1.4m)

> Slightly lower depreciation

due to below average asset

additions in 2015 und 2016

Investments by quarter (€m)

Depreciation (€m) Depreciation by quarter (€m)

Investments (€m)

9.0

5.0

Q4

8.0

Q3

6.8

Q2

4.9

Q1

5.9

Q1

2017

5.7

Q1

2016

5.75.9

Q4

6.3

Q3

6.1

Q2

6.2

Q1

Q1

2017

9.0

Q1

2016

5.0

5.6%

4.7%

2017

2016

5.4% 5.8% 6.3%

4.5% 7.0%8.4% 8.6%

6.3%

10

> Operating cash flow

improved mainly due to a

significant increase in trade

payables

> Total free cash flow

influenced by payment of

second purchase price

instalment for joint venture

SHW Longji Brake Discs

Cash Flow

Strong focus on operating free cash flow

(€m)1 Q1 2017 Q1/2016

Cash flow from operating activities 10.6 -1.7

Cash flow from investing activities

- tangible and intangible assets

-8.8 -5.0

Operating free cash flow 1.8 -6.7

Cash flow from investing activities

- financial assets-6.8 -0.0

Total free cash flow -5.0 -6.7

Other (esp. capital increase / dividend

payment) 0.0 -0.1

Change in net cash -5.0 -6.8

1 Figures include rounding adjustments

11

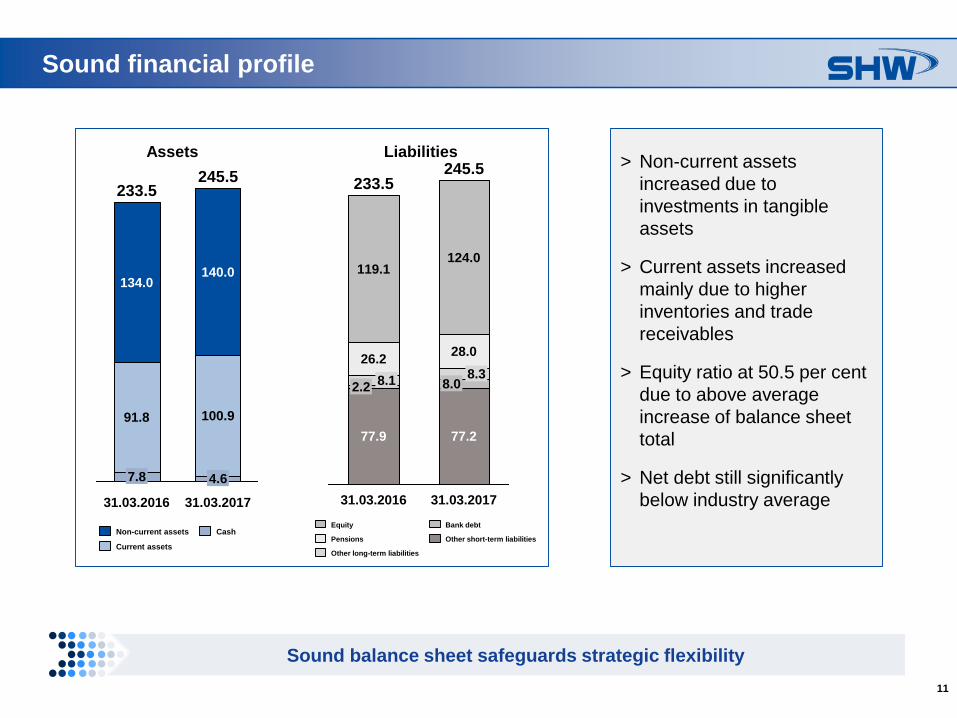

> Non-current assets

increased due to

investments in tangible

assets

> Current assets increased

mainly due to higher

inventories and trade

receivables

> Equity ratio at 50.5 per cent

due to above average

increase of balance sheet

total

> Net debt still significantly

below industry average

Sound financial profile

Sound balance sheet safeguards strategic flexibility

31.03.2017

8.08.3

28.0

245.5

77.2

233.5

31.03.2016

124.0

77.9

2.2

119.1

8.1

26.2

LiabilitiesAssets

31.03.2017

91.8

134.0

233.5

7.8

100.9

140.0

31.03.2016

245.5

4.6

Current assets

CashNon-current assetsOther short-term liabilities

Other long-term liabilities

Bank debtEquity

Pensions

12

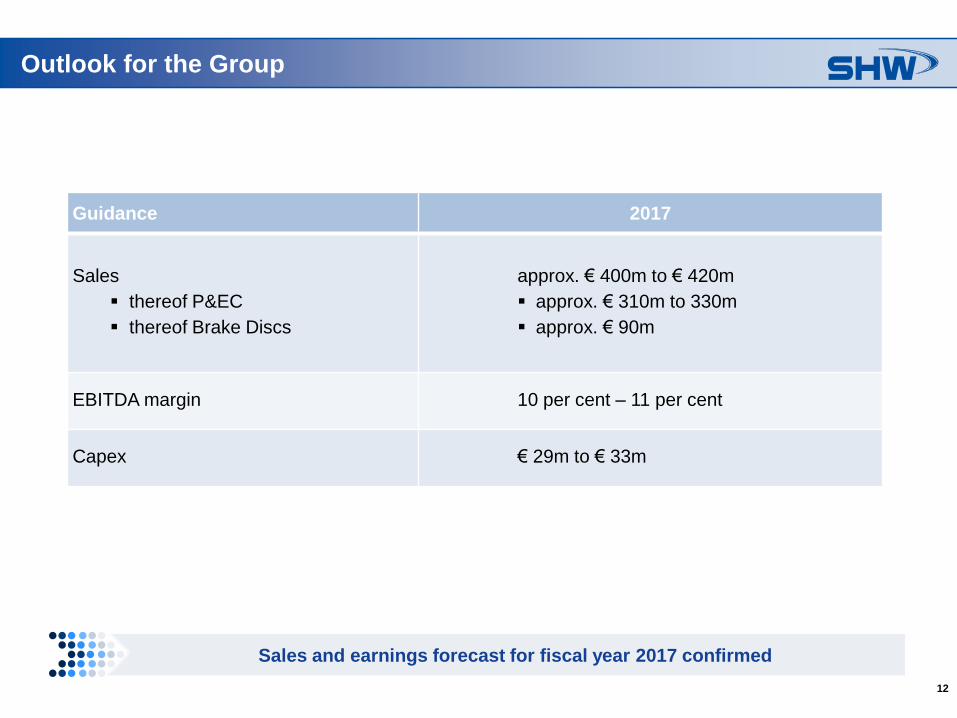

Outlook for the Group

Guidance 2017

Sales

thereof P&EC

thereof Brake Discs

approx. € 400m to € 420m

approx. € 310m to 330m

approx. € 90m

EBITDA margin 10 per cent – 11 per cent

Capex € 29m to € 33m

Sales and earnings forecast for fiscal year 2017 confirmed

13

Your key takeaways

Pumps & Engine business segment well on track

Brake Discs business segment temporarily below target level

We reiterate our full year guidance of Group sales of € 400m to € 420m and an

EBITDA-margin of 10 per cent to 11 per cent

Sound balance sheet safeguards strategic flexibility

14

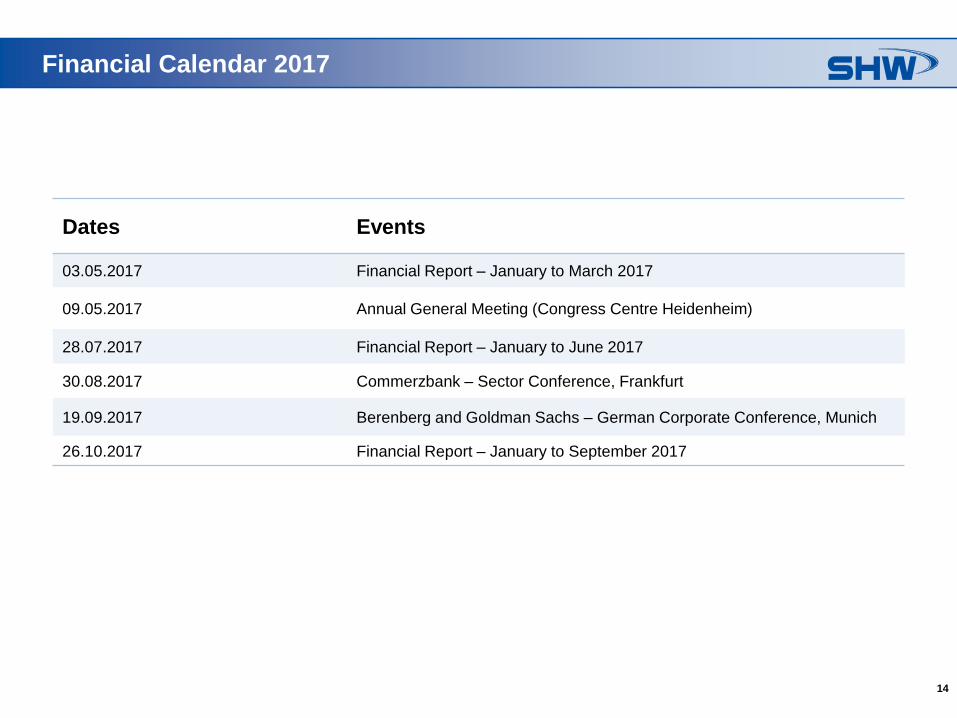

Financial Calendar 2017

Dates Events

03.05.2017 Financial Report – January to March 2017

09.05.2017 Annual General Meeting (Congress Centre Heidenheim)

28.07.2017 Financial Report – January to June 2017

30.08.2017 Commerzbank – Sector Conference, Frankfurt

19.09.2017 Berenberg and Goldman Sachs – German Corporate Conference, Munich

26.10.2017 Financial Report – January to September 2017

15

Michael SchicklingHead of Investor Relations & Corporate Communications

Telephone: +49 (0) 7361 502-462

E-Mail: [email protected]

Sandra SchererJunior Manager Investor Relations & Corporate Communications

Telephone: +49 (0) 7361 502-469

E-Mail: [email protected]

Contact Investor Relations

16

Disclaimer

No offer or investment recommendation

This document, which has been issued by SHW AG (the “Company” or “SHW”), does not constitute an offer to sell, or the solicitation of an offer to subscribe for or

buy, any shares in the Company, nor shall it or any part of it nor the fact of its distribution form the basis of, or be relied on in connection with, any contract or

investment decision in relation thereto.

The contents of this presentation are may not be reproduced, redistributed or passed on, directly or indirectly, to any other person or published, in whole or in part,

for any purpose. Neither the Company nor any other party is under any duty to update or inform you of any changes to such information. In particular, it should be

noted that financial information relating to the Company contained in this document has not been audited and in some cases is based on management information

and estimates.

This material is given in conjunction with an oral presentation and should not be taken out of context.

Certain market data and financial and other figures (including percentages) in this document were rounded in accordance with commercial principles. Figures

rounded may not in all cases add up to the stated totals or the statements made in the underlying sources. For the calculation of percentages used in the text, the

actual figures, rather than the commercially rounded figures, were used. Accordingly, in some cases, the percentages provided in the text may deviate from

percentages based on rounded figures.

Future Oriented Statements

Certain statements in this presentation are forward-looking statements. By their nature, forward-looking statements involve a number of risks, uncertainties and

assumptions that could cause actual results or events to differ materially from those expressed or implied by the forward‐looking statements. These risks,

uncertainties and assumptions could adversely affect the outcome and financial consequences of the plans and events described herein.

No obligation to update the information

The Company does not undertake any obligation to update or revise any forward-looking statements, whether as a result of new information, future events or

otherwise, except as otherwise required by applicable laws and regulations. You should not place undue reliance on forward-looking statements, which speak as

only of the date of this presentation. Statements contained in this presentation regarding past trends or events should not be taken as a representation that such

trends or events will continue in the future.

![Welcome [] · 15/12/2017 · 2012 q1 2013 q1 2014 q1 2015 q1 2016 q1 2017 q1 unemployment rate, lhs (% labour force, seasonally adjusted) Job vacancies rate, rhs (%labour force,](https://static.fdocuments.in/doc/165x107/5f9663c45f9e000e8c444eed/welcome-15122017-2012-q1-2013-q1-2014-q1-2015-q1-2016-q1-2017-q1-unemployment.jpg)