Financial Reporting: What is Your Responsibility? · Financial Reporting: What is Your...

30

Financial Reporting: What is Your Responsibility? Tina Kettle, United Technologies Corporation Doug Stewart, AircraftLogs Monday, Jan 16, 3:30 – 5:00

-

Upload

nguyenthien -

Category

Documents

-

view

216 -

download

0

Transcript of Financial Reporting: What is Your Responsibility? · Financial Reporting: What is Your...

Financial Reporting:What is Your Responsibility?Tina Kettle, United Technologies Corporation

Doug Stewart, AircraftLogs

Monday, Jan 16, 3:30 – 5:00

Agenda

• Session Objective

– Understanding the impact of data

– Getting the most out of your system

– Help to plan improvements

• Operational Reporting

– Impact of Data

– Types of Operational Reports

– Understanding Reporting Needs/Requirements

• Financial Reporting

– SEC Reporting

– IRS SIFL Income

– IRS Expense Disallowance

• Internal Accounting/Reporting

– ISBAO

– Time Share / Dry Lease / Wet Lease

– Establish a relationship with your Finance Dept.

– Explore your software

• Questions

Session Objectives

• Understand the impact of data on Operational Reporting

– Budgeting

– Cost Reporting

– Performance Metrics

• Identify critical data elements which support Financial Reporting

– IRS reporting for the company and the passengers

– SEC reporting for investors

• Be aware of specialized Internal Accounting your company may need totrack:

– Time Share & Dry Leases

– IS-BAO

• Summary: Be prepared to help others in your company with reporting tosupport your flight department.

Operational ReportingImpact of Data

Types of Operational Reports

Understanding Needs & Requirements

Operational Reporting

Impact of Data

• Aids Flight Department with budgeting and forecasting.

• Monitor monthly/yearly goals (metrics).

• Generated directly from data entered by Dispatch Office after acompleted trip.

• Accuracy of data input is critical to producing error free reports.

• Reports reviewed by Senior Executives, Tax Department,Compensation Department and Flight Department personnel.

• When Flight Departments have a Financial Manager within theirorganization, that individual is generally the liaison between theCorporate Office and the Flight Department for all Financial andOperational Reports.

Types of Operational Reports - Monthly

Flight Hour Reports

Hour Plan by Aircraft

Hours Flown by Authorizer

International Hours Flown

Budget Tracking

Hour/Budget Comparison

Monthly Budget Status (by cost center and by aircraft)

Fuel Reports (dollars & gallons)

Maintenance

Dispatch Reliability

Aircraft Availability

Corporate Executives

Flight Justifications

Aircraft Chargebacks

SIFL Calculations

SEC Valuation

Operational Reporting -Tracking Flight Time

Operations Reporting - Trip Types

Operational Reporting - Passenger Coding

Operational Reporting - Chargebacks

Operational Reporting

Understand Reporting Needs & Requirements

• Knowing what type of data to track for reporting is essential.

• Talk to your Finance/Tax departments to get a better understanding ofwhat the company needs and requirements are.

• Work with your software provider to make capturing data easier for yourdepartment. There are usually ways to customize fields for inputting datarequired for specific reports.

Aviation Reporting Generates Significant Workload

Financial ReportingIRS – SIFL Reporting for Passengers

IRS – Corporate Expense Disallowance

SEC – Annual Reporting to Investors

New Challenges Facing Corporate Flight Departments

• Greater Demand, More Corporate “Users” of Aviation Data

– Corporate Jet “crackdown” creates compliance challenges

– IRS & SEC Compliance More Challenging than FAA Compliance

– Corporate executives expect greater visibility and performance metrics

• Internal Processes have not evolved as Aviation Reporting requirements haveincreased

– New compliance requirements create complex business processes

– Incomplete data captured and stored

– Lack of accounting, reconciliation and “close the books” capabilities

• Scheduling systems are being stretched

– Scheduling systems and process designed for airplanes and pilots; not to manage processesabove

– System architecture restricts information sharing outside the flight department

Flight Request &Approval

SchedulingFlight

PostingManagement

Reporting

Board of Directors

FlightPlanning

Internal Accounting

Tax Accounting

Compliance Reporting

External Reporting

Executives

Exec. Assistants

Maintenance

IRS & SEC - Becoming Harder than the FAA?

Primary Reporting Elements:

1. Aircraft Expense Disallowances (IRS)

2. SIFL / Fringe Benefits (IRS)

3. Proxy Reporting / Executive Compensation (SEC)

4. Related-Party Transactions (SEC)

5. Federal Excise Tax (IRS)

6. Internal Chargebacks

7. FAS109/FIN48 (GAAP)

Compliance Requirements

1. ISBAO (IBAC)

2. Pilot & Crew Training & Experience (FAA)

3. Aircraft Maintenance Status (FAA)

4. Corporate Quality Processes

U.S. Securitiesand ExchangeCommission

SIFL Overview = SIFL is a GREAT DEAL

• “Standard Industry Fare Level” -- mileage rates & terminal charges

• Company-provided use of an aircraft is viewed as Compensation by theIRS

• Imputed Income = The IRS requires the value of this compensation be“imputed” to the employee’s income. Generally, you can use one of twomethods

– SIFL rates set by the IRS each year

– Charter Rate Method (market prices)

– Included in Your W-2 or 1099

• Control Employees Imputed 10X Higher than Non-ControlEmployees!

A round trip in a Gulfstream between Los Angeles and New Yorkgenerates only $3,600 per pax in SIFL income to the executive; but if

improperly calculated, the IRS could impose the charter rate method,skyrocketing taxable income to roughly $50,000 per trip.

Aircraft Expense Disallowance

• American Jobs Creation Act of 2004 (“AJCA”) requires companies todisallow the cost of personal entertainment flights provided to “specifiedindividuals”.

– This calculation becomes a percentage of your aircraft use

– IRS Notice 2005-45 explained “how” to disallow – and severelyimpacted the deductibility of corporate aircraft.

• Many companies still unaware and fail to disallow.

– Often its caused by a process breakdown

– Critical data never gets from the flight department to the reportingteam or tax staff.

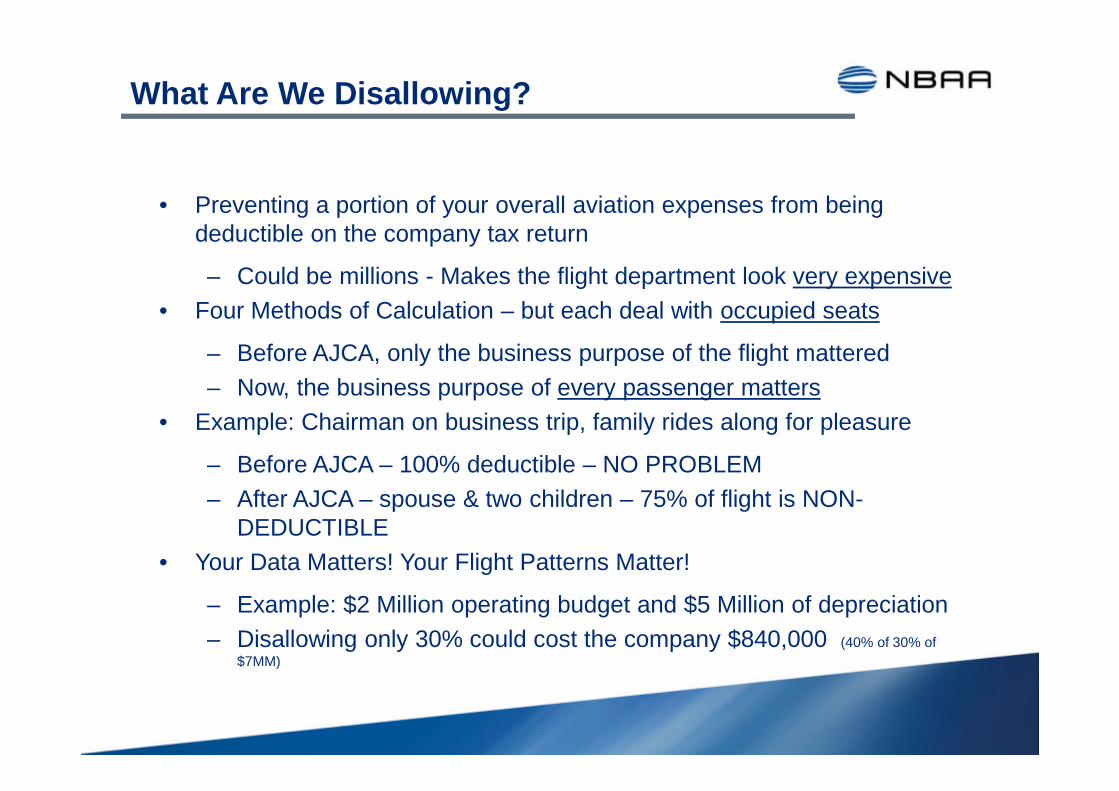

What Are We Disallowing?

• Preventing a portion of your overall aviation expenses from beingdeductible on the company tax return

– Could be millions - Makes the flight department look very expensive

• Four Methods of Calculation – but each deal with occupied seats

– Before AJCA, only the business purpose of the flight mattered

– Now, the business purpose of every passenger matters

• Example: Chairman on business trip, family rides along for pleasure

– Before AJCA – 100% deductible – NO PROBLEM

– After AJCA – spouse & two children – 75% of flight is NON-DEDUCTIBLE

• Your Data Matters! Your Flight Patterns Matter!

– Example: $2 Million operating budget and $5 Million of depreciation

– Disallowing only 30% could cost the company $840,000 (40% of 30% of

$7MM)

SEC – Annual Reporting to Shareholders

• What’s a Proxy Statement?

– Published annually for shareholder votes (same timing as annual reports)

– Many disclosures required about “NEO’s” (Named Executive Officers)

• Must Disclose the “Value” of Aircraft Personal Use for each NEO

– If the value of personal use exceeds $10,000 it must be disclosed in thecompany’s proxy statement

– If it exceeds $25,000, it gets its own footnote

• Value = “Incremental Cost” (there are no guidelines)

• Other Considerations

– SIFL is often disclosed for informational purposes, but cannot beused in lieu of incremental cost

– Time-sharing agreements, if in place, must be settled to avoid “loans toofficers”

corporate can jet trigger SEC reporting requirements.”

“Just one round-trip between Los Angeles and New York in a

corporate can jet trigger SEC reporting requirements.”

Sample SEC Disclosure: General Electric

Internal AccountingDepartmental Chargebacks

Time Share Agreements

Executive-Owned Aircraft

Departmental Chargebacks

• General Description: Allocation of costs back to internal departments of acompany, often designed to manage the use of the aircraft by thosedepartments (or cost centers, divisions, etc.)

• More common in larger companies with widespread use of their aircraft

• Typically charged via an hourly rate; occasionally flight miles or othermethods are used

• Common methods used for allocation, depending upon companyaccounting goals:

– Charge individual flights to department of the “lead passenger”

– Charge flights “pro rata” to the “home departments” of each passenger

– Charge flight department costs across all departments (whether theyfly or not) as company overhead

• Benefit: May generate a more accurate view of which departments utilizebusiness aviation, while also ensuring those departments recognize thecost.

Time Share Arrangements

• Under Part 91.501(c)(1), a time-sharing agreement allows an aircraftoperator to be reimbursed for a limited set of costs for a flight.

• Corporate flight departments often provide time-sharing arrangements,allowing an executive to reimburse the company for personal use of theaircraft. These arrangements require specific tracking of ten eligible costson each flight:

1. Fuel, oil, lubricants, and other additives.

2. Travel expenses of the crew

3. Hangar and tie-down costs away from home base)

4. Insurance for a specific flight

5. Landing fees, airport taxes, and similar assessments.

6. Flight-specific customs, foreign permits, and similar fees

7. In-flight food and beverages.

8. Passenger ground transportation.

9. Flight planning and weather contract services.

10. An additional charge equal to 100 percent of the expenses listed in item 1 (fuel)

• Time-sharing arrangement typically also trigger excise tax

Executive-Owned Aircraft

• Often, an executive may own an aircraft, and lease it back to his/heremployer.

• This will create further internal accounting needs, depending on the natureof the arrangement:

– Dry leases

– Time shares

– Etc.

• For both Executive-Owned Aircraft and Time-Sharing Arrangements, theexecutives involved and the company will need to “settle up” periodically(who owes who). The data provided by the flight department will directlyaffect these calculations.

• Settlements will often occur quarterly, in order to be finalized for SECreporting purposes (see next page for example)

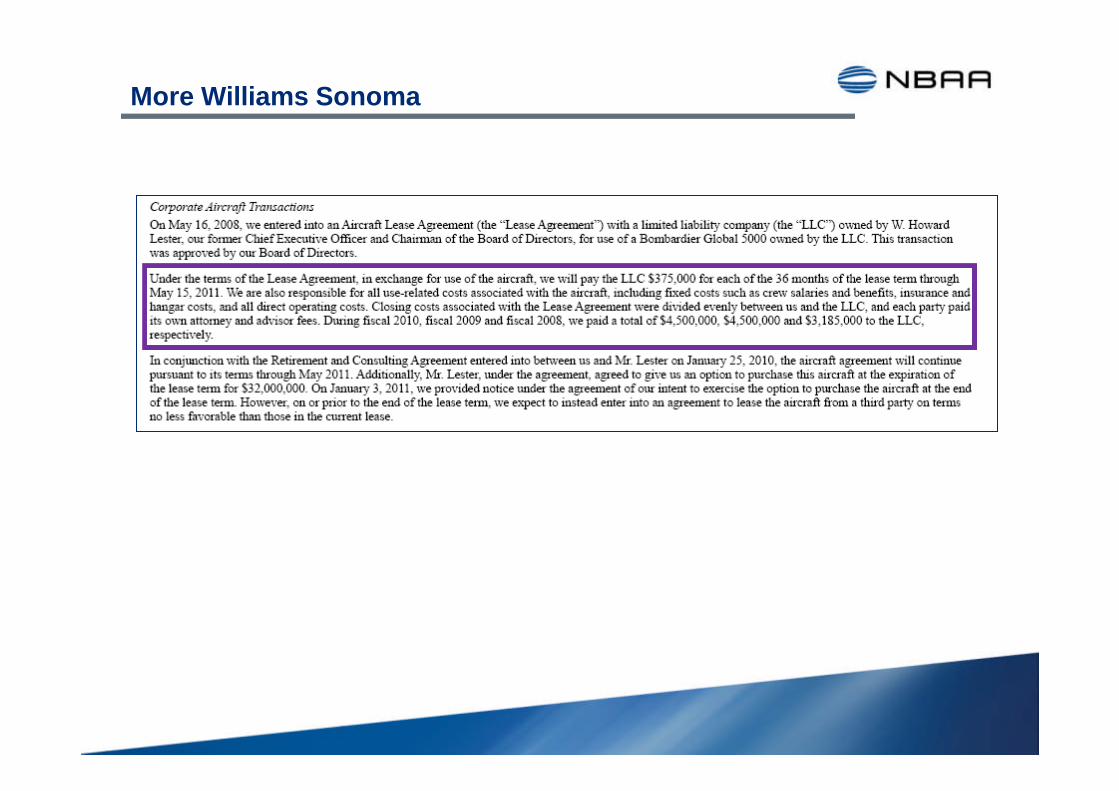

More Williams Sonoma

Wrap Up & Q&A

Closing Comments

• Most companies have reporting needs which aredirectly impacted by the flight department

• The data you need is passing through yourhands…Capture it!

• Most companies use 30% of their software capabilities

• Tip: The NBAA Tax Class is Two Days Long

Don’t know who your tax people are? You mayhave trouble!

Use This Map to Find the People Who Need You!!

[email protected]@UTC.com