Tv Designed for Entertainment & Designed for Entertainment &

01/09/14

Copyright 2014 Wolcott Aviation Seminars, LLC 1

© 2014 Wolcott Aviation Seminars, LLC

SIFL and ENTERTAINMENT COST DISALLOWANCE:

REPORTING PERSONAL USE of a BUSINESS AIRCRAFT

January 09, 2014

2© 2014 Wolcott Aviation Seminars, LLC

Sue Folkringa, CPA, MBACommercial Pilot, AS/MEL, Glider, Instrument

Airplane

Jed Wolcott, CPA, MBAPresident

3© 2014 Wolcott Aviation Seminars, LLC

Today’s Webinar Topics Using SIFL to calculate the employee fringe

benefit for non-business use of company aircraft Calculating the cost disallowance to the

company for entertainment flights Methods to document and track the flight

data for preparation of tax returns

01/09/14

Copyright 2014 Wolcott Aviation Seminars, LLC 2

4© 2014 Wolcott Aviation Seminars, LLC

Why Are These Rules Important? Aircraft, as listed property, are IRS audit targets Failure to follow the reporting requirements can

lead to: Taxes and penalties to the employees using the

aircraft Reduction or even disallowance of aircraft costs

and deductions to the company As of August 01, 2012 the aircraft flight records

have become part of the tax return

5© 2014 Wolcott Aviation Seminars, LLC

Wolcott & Associates, P.A. - What We Do We are an aviation-dedicated firm of CPAs and

accounting professionals Our clients are aircraft owners, operators, and

accounting firms that have aircraft owner-clients We specialize in the preparation of aircraft income tax

returns, state tax matters, IRS audits, structuring aircraft ownership, and related aviation tax and financial matters.

We identify, protect and preserve tax deductions for your aircraft and those of your clients!

6© 2014 Wolcott Aviation Seminars, LLC

Resource Lookup

01/09/14

Copyright 2014 Wolcott Aviation Seminars, LLC 3

7© 2014 Wolcott Aviation Seminars, LLC

Resource Materials

Copies of today’s materials are available at our website at www.aviation-cpa.com.

Look for the green lookup bar on the Wolcott and Associates, PA homepage

This PowerPoint presentation – You will find other Resource Material links

throughout today’s presentation

50119

50119

8© 2014 Wolcott Aviation Seminars, LLC

Webinars Later this Year

Aircraft Audit Strategies Section 1: Ordinary & Necessary Use, Hobby Loss, Excise Tax & Flight

Department Companies Section 2: Personal Use, Passive Activity, Depreciation, Owner-Basis

Preparation of Tax Returns for Company-Owned Aircraft Preparation of Owner-Pilot Tax Returns Ownership Structures, Avoiding Passive Loss Limitations and

Hobby Loss Rules State Sales and Use Taxes

9© 2014 Wolcott Aviation Seminars, LLC

Definition of FAA-Related Terms

Part 91: Section of the Code of Federal Regulations covering the general operating rules for aircraft. Aircraft operating under Part 91 rules may not engage in flights for hire

Part 135: Section of the Code of Federal Regulations governing aircraft “for hire” operations. Requires an FAA Operating Certificate. These operations are typically called charter flights, and often utilize company aircraft. Flight rules are generally more restrictive under Part 135 than Part 91

Dry Lease: Lease of aircraft only, with no pilot services or direct operating costs

01/09/14

Copyright 2014 Wolcott Aviation Seminars, LLC 4

10© 2014 Wolcott Aviation Seminars, LLC

Using SIFL to Calculate the

Taxable Fringe Benefit to the

Employee for Personal Flights in a Company Aircraft

11© 2014 Wolcott Aviation Seminars, LLC

IRS Regulations for Non-Business Use

Company

Imputed income for employees & guests

Treas. Reg. 1.61‐21

Entertainment Flight Cost Disallowance

IRC 274(e)

10400

10290

12© 2014 Wolcott Aviation Seminars, LLC

IRS has Specific Rules for Reporting Employee Use of Company Aircraft

Personal use is considered a “Taxable Fringe Benefit” Aircraft rules found at Reg. § 1.61-21 Personal use rules are not limited to aircraft; includes

automobiles, real estate and boats See IRS Publication 15-B Employer’s Guide to Fringe

Benefits

Aviation Tax Guides at www.aviation-cpa.com/guides

10400

10411

01/09/14

Copyright 2014 Wolcott Aviation Seminars, LLC 5

13© 2014 Wolcott Aviation Seminars, LLC

IRS Rules Require “Recognition” of Taxable Fringe Benefits from Personal Use

FAA limits the reimbursement to the employer for the use of a Part 91 company aircraft

IRS has no objection to direct reimbursement Both IRS and FAA permit imputation of the

value of flight to the passengers If the aircraft is operated under Part 135, the

company can charge as it wishes

40000

14© 2014 Wolcott Aviation Seminars, LLC

The employee is taxed for the guests, not the guests themselves

Guests are taxed to the employee authorizing the travel, at that employee’s SIFL rate

The employee does not have to be on the aircraft to be taxed for the flight

Children under age 2 years are never taxed

Employee Is Taxed For The Non-Business Transportation

15© 2014 Wolcott Aviation Seminars, LLC

Employee Is Taxed For The Non-Business Transportation

01/09/14

Copyright 2014 Wolcott Aviation Seminars, LLC 6

16© 2014 Wolcott Aviation Seminars, LLC

Types of Personal Use Calculations

Standard Industry Fare Level (SIFL) Uses a DOT-published rate per mile to calculate the

value of the flight to the employee

Calculated on point-to-point, not leg-by-leg basis

Fair Market Value Method (also called statutory or charter-rate method) Values the flight at a commercial charter rate

Requires the company to have and keep evidence of commercial charter rate quotes in a similar aircraft

Generally more expensive for the employee

17© 2014 Wolcott Aviation Seminars, LLC

Bob’s Trip to/from LA

KDPA [Dupage]

KHOU [Houston Hobby]

KVNY [Van Nuys]

941 sm

933 sm

KBFI [Aircraft based at Boeing Field]

Airplane’s miles traveled = 6,534

Bob’s miles for SIFL = 3,436 (1,718 x 2)

SIFL miles are point‐to‐pointDeadhead Leg

SIFL is Calculated on a Point‐to‐Point Basis

18© 2014 Wolcott Aviation Seminars, LLC

Overlooking Bob’s point-to-point routing and calculating his SIFL leg-by-leg results in Bob paying unnecessary taxes! Taxable income from SIFL point-to-point routing

= $ 2,058 Taxable income from SIFL leg-by-leg routing

= $2,676 Results in additional taxable income of $618 to Bob

SIFL Calculation Caution:

01/09/14

Copyright 2014 Wolcott Aviation Seminars, LLC 7

19© 2014 Wolcott Aviation Seminars, LLC

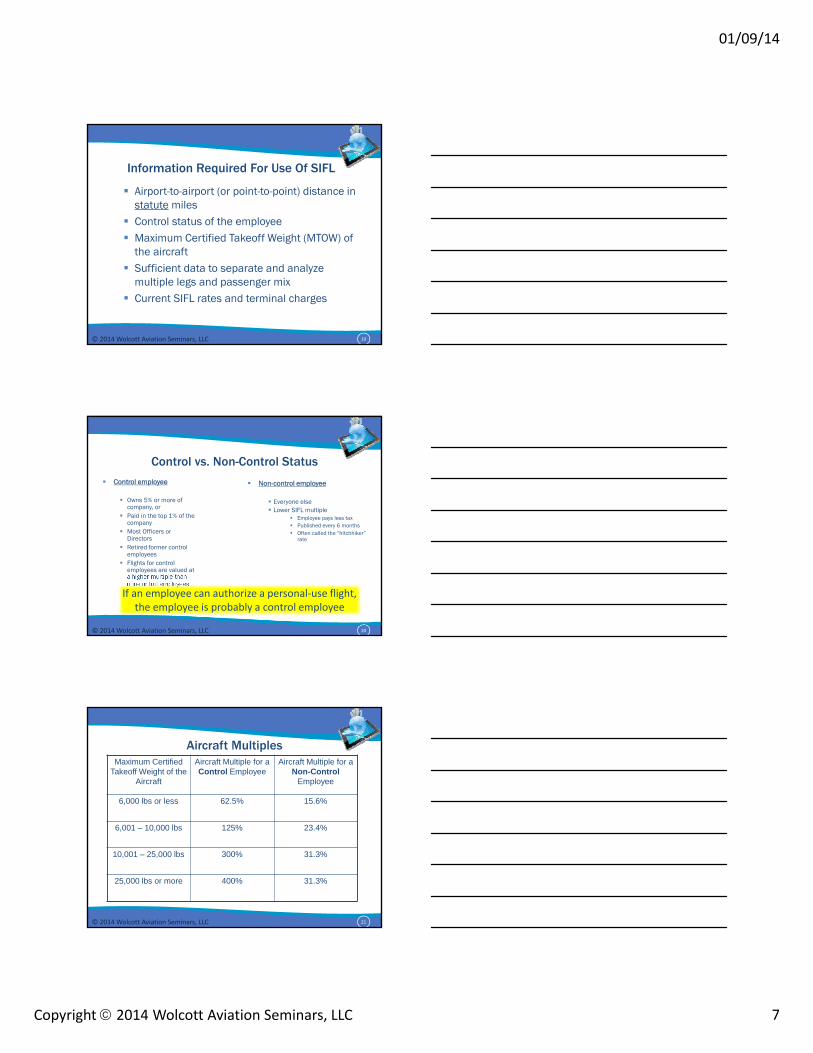

Information Required For Use Of SIFL

Airport-to-airport (or point-to-point) distance in statute miles

Control status of the employee Maximum Certified Takeoff Weight (MTOW) of

the aircraft Sufficient data to separate and analyze

multiple legs and passenger mix Current SIFL rates and terminal charges

20© 2014 Wolcott Aviation Seminars, LLC

Control vs. Non-Control Status Control employee

Owns 5% or more of company, or

Paid in the top 1% of the company

Most Officers or Directors

Retired former control employees

Flights for control employees are valued at a higher multiple than non-control employees

Non-control employee

Everyone else Lower SIFL multiple

Employee pays less tax Published every 6 months Often called the “hitchhiker”

rate

If an employee can authorize a personal‐use flight, the employee is probably a control employee

21© 2014 Wolcott Aviation Seminars, LLC

Aircraft MultiplesMaximum Certified

Takeoff Weight of the Aircraft

Aircraft Multiple for a Control Employee

Aircraft Multiple for a Non-Control

Employee

6,000 lbs or less 62.5% 15.6%

6,001 – 10,000 lbs 125% 23.4%

10,001 – 25,000 lbs 300% 31.3%

25,000 lbs or more 400% 31.3%

01/09/14

Copyright 2014 Wolcott Aviation Seminars, LLC 8

22© 2014 Wolcott Aviation Seminars, LLC

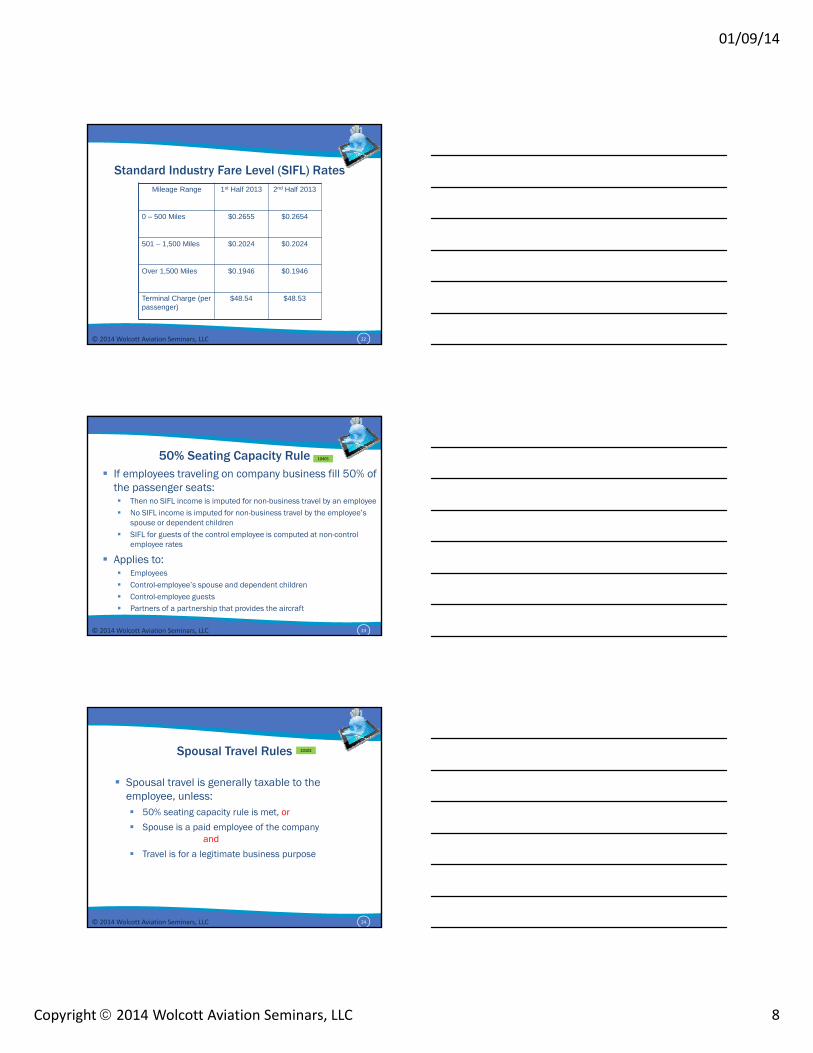

Standard Industry Fare Level (SIFL) RatesMileage Range 1st Half 2013 2nd Half 2013

0 – 500 Miles $0.2655 $0.2654

501 – 1,500 Miles $0.2024 $0.2024

Over 1,500 Miles $0.1946 $0.1946

Terminal Charge (per passenger)

$48.54 $48.53

23© 2014 Wolcott Aviation Seminars, LLC

50% Seating Capacity Rule If employees traveling on company business fill 50% of

the passenger seats: Then no SIFL income is imputed for non-business travel by an employee No SIFL income is imputed for non-business travel by the employee’s

spouse or dependent children SIFL for guests of the control employee is computed at non-control

employee rates

Applies to: Employees Control-employee’s spouse and dependent children Control-employee guests Partners of a partnership that provides the aircraft

10405

24© 2014 Wolcott Aviation Seminars, LLC

Spousal Travel Rules

Spousal travel is generally taxable to the employee, unless: 50% seating capacity rule is met, or

Spouse is a paid employee of the company and

Travel is for a legitimate business purpose

10102

01/09/14

Copyright 2014 Wolcott Aviation Seminars, LLC 9

25© 2014 Wolcott Aviation Seminars, LLC

Foreign Travel in Excess of 7 Days

Foreign travel SIFL reduction rules apply if the following 2 conditions are met: Business trip outside the United States lasts for more than 7

days At least 25% of the individual’s time on the trip is devoted to

non-business activities

If both conditions are met, SIFL may be reduced to the ratio of non-business days divided by total days

Travel days and weekend days count as business days Does not apply to employees or guests traveling

entirely for non-business purposes

10303

26© 2014 Wolcott Aviation Seminars, LLC

“Bona Fide” Security Programs

Permits executive to fly on company plane for non-business flights at reduced SIFL rates

Requires that a security study be performed. A separate study is required for family members if they travel alone. The study must conclude that a security risk to the executive exists

The security plan must be part of a complete security program (24 hours)

Provides “Safe Harbor;” use 200% multiple regardless of weight of aircraft Can result in significant savings to the employee for use of large

aircraft

10410

27© 2014 Wolcott Aviation Seminars, LLC

SIFL Calculation874 Statute Miles300% aircraft4 Passengers

0‐500 miles @0.2654 $ 132.70

501‐1500 miles @0.2024 75.70

1501 + @ 0.1964 0

Subtotal 208.40

Multiple by Aircraft Multiple X 300%

625.20

Terminal Charge 48.53

Subtotal 673.73

Multiply by # of Passengers X 4

SIFL Charge to Employee $2,694.92

01/09/14

Copyright 2014 Wolcott Aviation Seminars, LLC 10

28© 2014 Wolcott Aviation Seminars, LLC

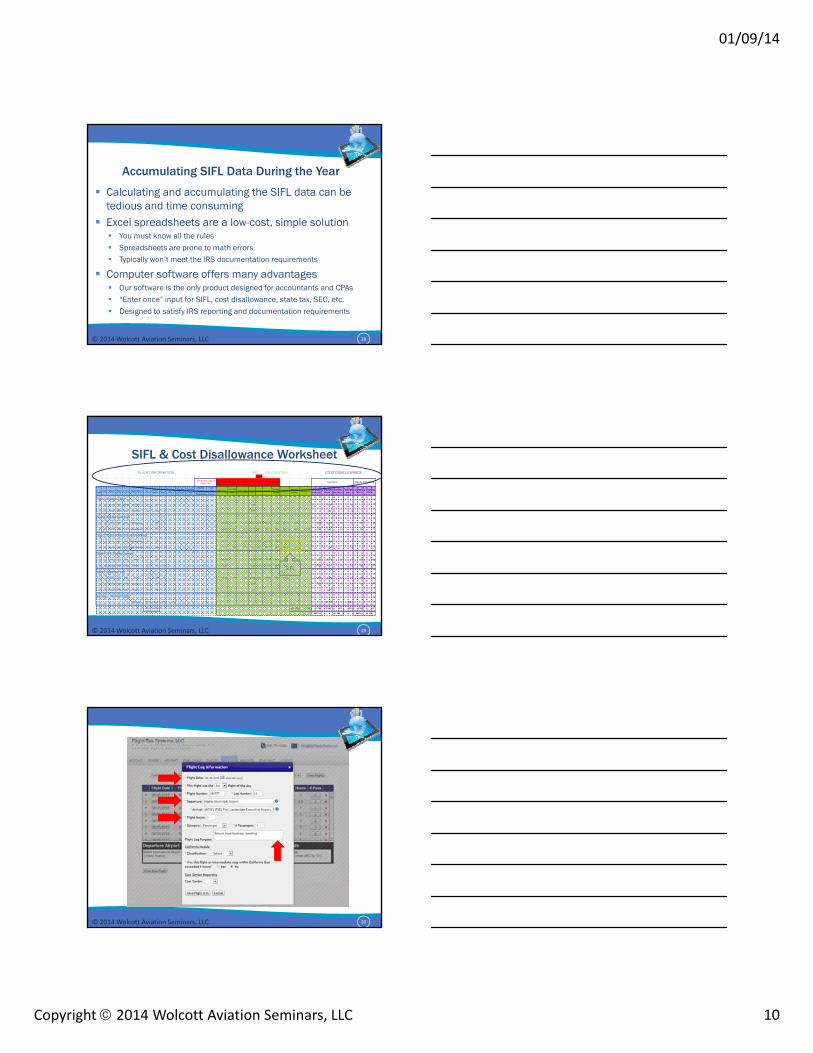

Accumulating SIFL Data During the Year

Calculating and accumulating the SIFL data can be tedious and time consuming

Excel spreadsheets are a low-cost, simple solution You must know all the rules Spreadsheets are prone to math errors Typically won’t meet the IRS documentation requirements

Computer software offers many advantages Our software is the only product designed for accountants and CPAs “Enter once” input for SIFL, cost disallowance, state tax, SEC, etc. Designed to satisfy IRS reporting and documentation requirements

29© 2014 Wolcott Aviation Seminars, LLC

31.3%

0.2569$ 0.1959$ 0.1884$ 300% 46.97$

Flight

Leg Date From To Flight Type Hrs. Statute

Miles Total Pax

Business Pax

Pers Non-Ent Pax

Entertain Pax

Exempt Spouse &

Dependents

Non-Control Guests

0-500 Miles501-1500

Miles1500+ Miles Subtotal Factor Subtotal

Terminal Charge

Subtotal Imputed Income

Reimbursed Entertain Seat Miles

Total Seat Miles

Entertain Seat Hours

Total Seat Hours

Entertain Miles

Entertain Hours

Flight 1: Business Flight

1 1 7/1/12 STL MDW Business 0.7 251 6 6 0.00 - - 1,506 4.2 - -

1 2 7/2/12 MDW STL Business 0.7 251 6 6 0.00 - 1,506 4.2 - -

Flight 2: Entertainment Flight

2 1 7/10/12 STL ORL Entertainment 2.1 874 4 4 128.45 73.27 0.00 201.72 300% 605.15 46.97 652.12 2,608 - 3,496 3,496 8.4 8.4 874 2.10

2 2 7/20/12 ORL STL Entertainment 2.1 874 4 4 128.45 73.27 0.00 201.72 300% 605.15 46.97 652.12 2,608 2,520 3,496 3,496 8.4 8.4 874 2.10

Flight 3: Personal Non-Entertainment Flight

3 1 8/1/12 STL AAO Other Business 0.9 378 2 2 97.11 0.00 0.00 97.11 300% 291.32 46.97 338.29 677 - - 756 1.8 - -

3 2 8/5/12 AAO STL Other Business 0.9 378 2 2 97.11 0.00 0.00 97.11 300% 291.32 46.97 338.29 677 - - 756 1.8 - -

Flight 4: 50% Seating Capacity

4 1 10/18/12 STL PDK Mixed 1.0 476 10 5 5 4 1 122.28 122.28 31.3% 38.28 46.97 85.25 85 - 2,380 4,760 5.0 10.0 238 0.50

4 2 10/20/12 PDK STL Mixed 1.0 476 10 5 5 4 1 122.28 122.28 31.3% 38.28 46.97 85.25 85 - 2,380 4,760 5.0 10.0 238 0.50

Flight 5: Deadhead Leg

5 1 11/18/12 STL PDK Mixed 1.0 476 8 4 4 122.28 0.00 0.00 122.28 300% 366.85 46.97 413.82 - - 1,904 3,808 4.0 8.0 238 0.50

5 2 11/19/12 PDK HPN Deadhead 1.8 763 7 5 2 0.00 - - 1,526 5,341 3.6 12.6 218 0.51

5 3 11/20/12 HPN STL Business 2.0 895 5 5 0.00 - - 4,475 10.0 - -

Summary: All Other Flights

Business 77.5 39,062 215 215 122,762 286.4

91.7 45,154 6,741 2,520 15,182 157,422 34.4 365.8 2,680 6.21

9.64% 9.40% 5.94% 6.78%

SIFL CALCULATION COST DISALLOWANCE

Seat Method Flight-By-Flight Method 50% Seating Capacity

Flights Only

FLIGHT INFORMATION

20,406

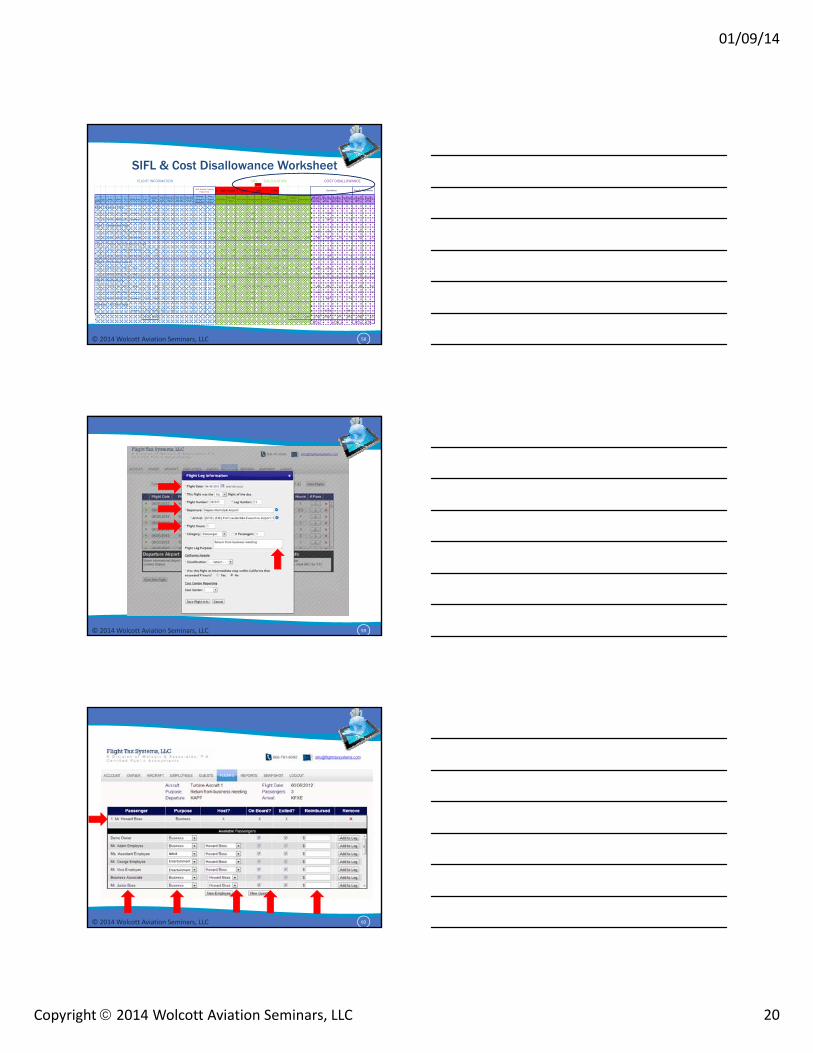

SIFL & Cost Disallowance Worksheet

SIFL

20,406

30© 2014 Wolcott Aviation Seminars, LLC

01/09/14

Copyright 2014 Wolcott Aviation Seminars, LLC 11

31© 2014 Wolcott Aviation Seminars, LLC

SIFL Year‐to‐Date Summary

SIFL Report

Footnotes explain SIFL reporting rules

32© 2014 Wolcott Aviation Seminars, LLC

Imputed Income (SIFL) Is Not A Deductible Company Expense

Imputed income is a non-cash fringe benefit Company reports SIFL on employee’s W-2 Employee reports on 1040, pays personal income tax SIFL imputed income is not deductible to the

company

33© 2014 Wolcott Aviation Seminars, LLC

Report Imputed Income To Social Security Administration & IRS

Earnings may be reported monthly, quarterly, or annually

Company reports on Form 941 and annual 940 Earnings are subject to Social Security and Medicare Employee should consider withholding or making

estimated tax payments 1099 may be substituted for SIFL to a non-employee

01/09/14

Copyright 2014 Wolcott Aviation Seminars, LLC 12

© 2014 Wolcott Aviation Seminars, LLC 34

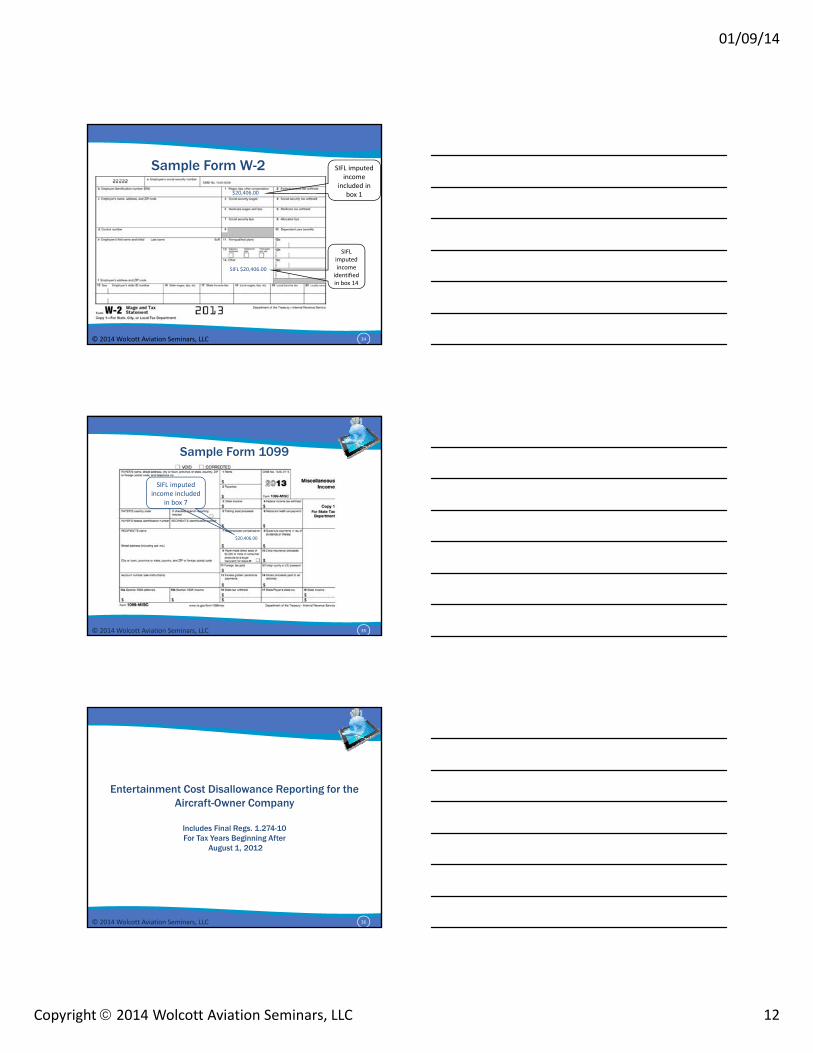

Sample Form W-2 SIFL imputed income

included in box 1

SIFL imputed income identified in box 14

$20,406.00

SIFL $20,406.00

35© 2014 Wolcott Aviation Seminars, LLC

Sample Form 1099

$20,406.00

SIFL imputed income included

in box 7

36© 2014 Wolcott Aviation Seminars, LLC

Entertainment Cost Disallowance Reporting for the Aircraft-Owner Company

Includes Final Regs. 1.274-10 For Tax Years Beginning After

August 1, 2012

01/09/14

Copyright 2014 Wolcott Aviation Seminars, LLC 13

37© 2014 Wolcott Aviation Seminars, LLC

Entertainment Flight Cost Disallowance

IRC 274(e) 10290

There are Two Sets of IRS Regulations for Non-business Use of Company Aircraft

Company

Imputed income for employees & guests

10400 Treas. Reg. 1.61‐21

38© 2014 Wolcott Aviation Seminars, LLC

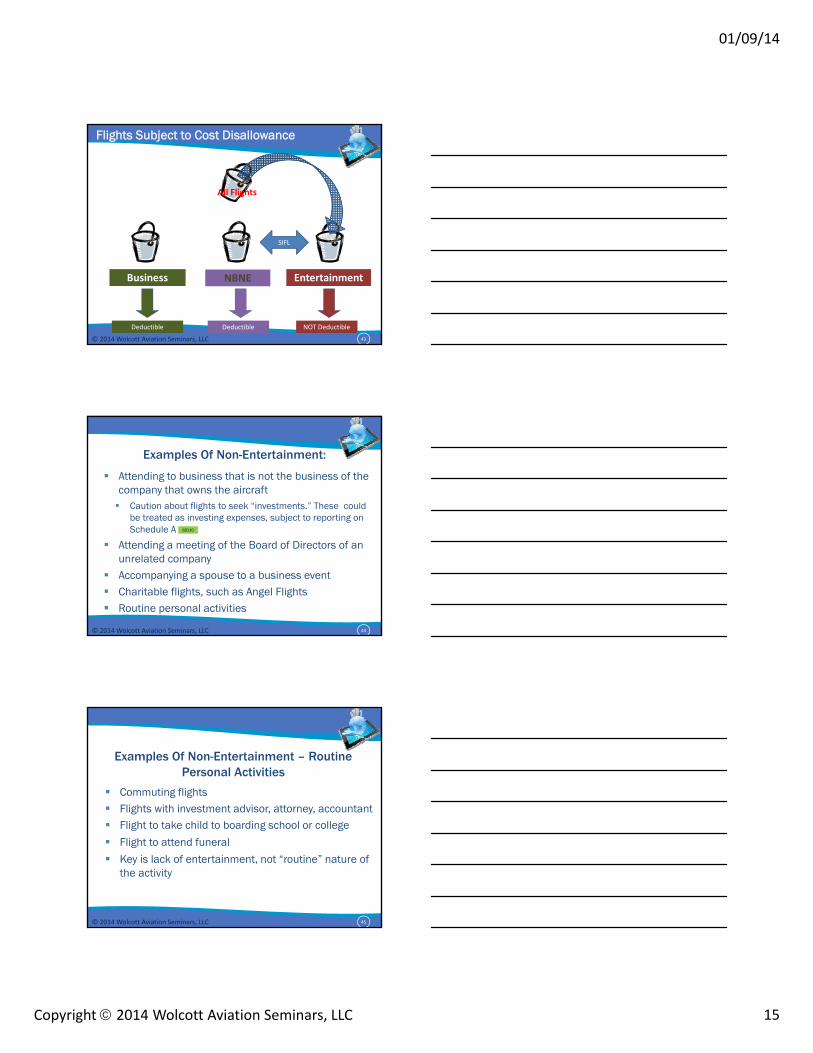

Types of Company Flights

Business Flights – Flights that are incidental to the companies’ business No SIFL, fully deductible

Non-Business Non-Entertainment Flights (NBNE) –Flights that are for business, but not the business of the company owning or operating the aircraft SIFL, no cost disallowance

Entertainment Flights – Flights that are for transportation to activities that provide entertainment to the passengers SIFL and cost disallowance both apply

39© 2014 Wolcott Aviation Seminars, LLC

What Is Entertainment? “Entertainment” means any activity which is

generally considered to constitute entertainment, amusement or recreation: Treas. Reg. 1.274-2(b)(1)

“Entertainment use is an amusement or recreational activity, such as traveling to a sporting event or a vacation destination” Notice 2005-45

An activity not “directly related to” or “associated with” the active conduct of a trade or business

Entertainment is often described as a frame of mind…passenger expects enjoyment after flight

10304

10307

01/09/14

Copyright 2014 Wolcott Aviation Seminars, LLC 14

40© 2014 Wolcott Aviation Seminars, LLC

Business NBNE

All Flights

Entertainment

Flights Subject to Cost Disallowance

41© 2014 Wolcott Aviation Seminars, LLC

Business NBNE

All Flights

Entertainment

Deductible

Flights Subject to Cost Disallowance

42© 2014 Wolcott Aviation Seminars, LLC

Business NBNE Entertainment

All Flights

Deductible Deductible

Flights Subject to Cost Disallowance

01/09/14

Copyright 2014 Wolcott Aviation Seminars, LLC 15

43© 2014 Wolcott Aviation Seminars, LLC

Business NBNE

All Flights

Entertainment

Deductible NOT DeductibleDeductible

SIFL

Flights Subject to Cost Disallowance

44© 2014 Wolcott Aviation Seminars, LLC

Examples Of Non-Entertainment:

Attending to business that is not the business of the company that owns the aircraft Caution about flights to seek “investments.” These could

be treated as investing expenses, subject to reporting on Schedule A

Attending a meeting of the Board of Directors of an unrelated company

Accompanying a spouse to a business event Charitable flights, such as Angel Flights Routine personal activities

60110

45© 2014 Wolcott Aviation Seminars, LLC

Examples Of Non-Entertainment – Routine Personal Activities

Commuting flights Flights with investment advisor, attorney, accountant Flight to take child to boarding school or college

Flight to attend funeral

Key is lack of entertainment, not “routine” nature of the activity

01/09/14

Copyright 2014 Wolcott Aviation Seminars, LLC 16

46© 2014 Wolcott Aviation Seminars, LLC

Specified Individual Entertainment reporting requires the presence of a

Specified Individual; if no Specified Individual is on the flight, then no entertainment disallowance

A Specified Individual is anyone in the company who is subject to section 16(a) of the Securities Exchange Act, or any individual who would be subject to it if the company were an issuer of equity securities subject to the Securities Act.

Specified individuals generally include officers, directors, 10% owners, principal financial officers, vice presidents in charge of a principal business unit division or function

47© 2014 Wolcott Aviation Seminars, LLC

COSTS SUBJECT TO DISALLOWANCE

In determining the amount of expenses subject to disallowance under this section, a taxpayer must include all of the expenses of operating the aircraft, including all fixed and variable expenses the taxpayer deducts in the taxable year. These expenses include, but are not limited to:Salaries for pilots, maintenance personnel, and other personnel assigned to the aircraft; meal and lodging expenses of flight personnel; take-off and landing fees; costs for maintenance flights; costs of on-board refreshments, amenities and gifts; hangar fees (at home or away); management fees; costs of fuel, tires, maintenance, insurance, registration, certificate of title, inspection, and depreciation; interest on debt secured by or properly allocated (within the meaning of §1.163-8T) to an aircraft; and all costs paid or incurred for aircraft leased or chartered to the taxpayer. 1.274-10(d)(1)

48© 2014 Wolcott Aviation Seminars, LLC

Disallowance Calculation Methods

1. Occupied Seat Miles: Annual entertainment passenger seat miles divided by total passenger flight seat miles

2. Occupied Seat Hours: Annual entertainment passenger seat hours divided by total passenger flight seat hours

3. Flight-By-Flight Miles: Annual entertainment flight miles divided by total flight miles

4. Flight-By-Flight Hours: Annual entertainment flight hours divided by total flight hours

01/09/14

Copyright 2014 Wolcott Aviation Seminars, LLC 17

49© 2014 Wolcott Aviation Seminars, LLC

Disallowance Calculation Example 2,000 mile flight with 3 business passengers and 2 entertainment

passengers; example using Occupied Seat Miles method

The objective is to calculate an entertainment disallowance percentage. The taxpayer may use the lowest of the four (4) methods allowed for calculating the percentage

Total Miles Business Entertainment

Flight miles 2,000 2,000 2,000

Passengers X 5 X 3 X 2

Occupied Seat Miles 10,000 6,000 4,000

Use Percentage 100% 60% 40%

50© 2014 Wolcott Aviation Seminars, LLC

Deadhead flights are flights with no passengersDeadhead flights must be treated as passenger

flights for calculating OSH, OSM, or flight-by-flight hours or miles “Passengers” are “ghosted” and classified

according to the previous or subsequent passengers for the flights with which they are associated If the deadhead is related to one occupied flight,

the deadhead passenger count is easy to determine

Deadhead Flight Rules

51© 2014 Wolcott Aviation Seminars, LLC

Deadhead Flight Rules

A

BLeg 1 = Occupied Leg

4 Business Passengers

Deadhead return leg:Calculate using 4

business passengers

01/09/14

Copyright 2014 Wolcott Aviation Seminars, LLC 18

52© 2014 Wolcott Aviation Seminars, LLC

Deadhead Flight Rules When the deadhead flight is related to two or more

flights, it may be determined two different ways: The weighted average method calculates the passenger by

OSM or OSH methods

Flight-by-flight method uses the percentage of each type of passengers on occupied flights before and after the deadhead

The IRS gives examples of each method, and neither method accurately calculates the deadhead passengers

Any realistic approach is probably acceptable providing it is applied in a consistent manner

53© 2014 Wolcott Aviation Seminars, LLC

Three legged flight Leg 1: 6 hours, A-B, 12 pax, 8 business, 4 entertainment Leg 2: 4 hours, B-C, deadhead (requires “ghosted” passengers) Leg 3: 2 hours, C-A, 12 pax, 6 business, 6 entertainment Total 12 flight hours and 24 pax, 14 business, 10 entertainment

Deadhead flights – IRS Example Flight-By-Flight Method

A

C

54© 2014 Wolcott Aviation Seminars, LLC

Leg Total Business Entertainment

1 12 8 4

2 (DH) 12 7 5

3 12 6 6

Totals 36 21 15

100% 58.33% 41.67%

Deadhead Flights – Flight-by-Flight Method

Leg Total Business Entertainment

1 12 8 4

2 (DH) 12 7 5

3 12 6 6

Totals 36 21 15

100% 58.33% 41.67%

Leg Total Business Entertainment

1 12 8 4

2 (DH) 12 7 5

3 12 6 6

Totals 36 21 15

100% 58.33% 41.67%

Leg Total Business Entertainment

1 12 8 4

2 (DH) 12 7 5

3 12 6 6

Totals 36 21 15

100% 58.33% 41.67%

Leg Total Business Entertainment

1 12 8 4

2 (DH) 12 7 5

3 12 6 6

Totals 36 21 15

100% 58.33% 41.67%

Leg Total Business Entertainment

1 12 8 4

2 (DH) 12 7 5

3 12 6 6

Totals 36 21 15

100% 58.33% 41.67%

Leg Total Business Entertainment

1 12 8 4

2 (DH) 12 7 5

3 12 6 6

Totals 36 21 15

100% 58.33% 41.67%

Leg Total Business Entertainment

1 12 8 4

2 (DH) 12 7 5

3 12 6 6

Totals 36 21 15

100% 58.33% 41.67%

01/09/14

Copyright 2014 Wolcott Aviation Seminars, LLC 19

55© 2014 Wolcott Aviation Seminars, LLC

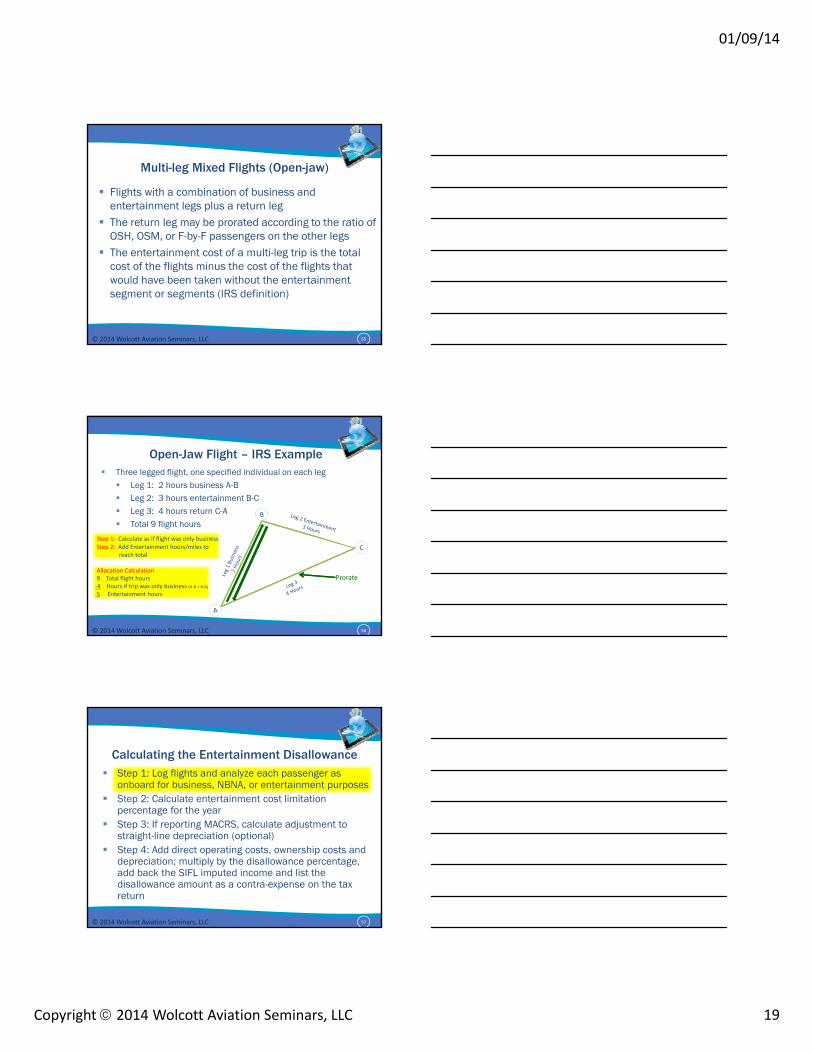

Multi-leg Mixed Flights (Open-jaw)

Flights with a combination of business and entertainment legs plus a return leg

The return leg may be prorated according to the ratio of OSH, OSM, or F-by-F passengers on the other legs

The entertainment cost of a multi-leg trip is the total cost of the flights minus the cost of the flights that would have been taken without the entertainment segment or segments (IRS definition)

56© 2014 Wolcott Aviation Seminars, LLC

Open-Jaw Flight – IRS Example Three legged flight, one specified individual on each leg Leg 1: 2 hours business A-B Leg 2: 3 hours entertainment B-C Leg 3: 4 hours return C-A Total 9 flight hours

Prorate

Step 1: Calculate as if flight was only businessStep 2: Add Entertainment hours/miles to

reach total

Allocation Calculation9 Total flight hours‐4 Hours if trip was only business (A‐B + B‐A)5 Entertainment hours

57© 2014 Wolcott Aviation Seminars, LLC

Step 1: Log flights and analyze each passenger as onboard for business, NBNA, or entertainment purposes

Step 2: Calculate entertainment cost limitation percentage for the year

Step 3: If reporting MACRS, calculate adjustment to straight-line depreciation (optional)

Step 4: Add direct operating costs, ownership costs and depreciation; multiply by the disallowance percentage, add back the SIFL imputed income and list the disallowance amount as a contra-expense on the tax return

Calculating the Entertainment Disallowance

01/09/14

Copyright 2014 Wolcott Aviation Seminars, LLC 20

58© 2014 Wolcott Aviation Seminars, LLC

31.3%

0.2569$ 0.1959$ 0.1884$ 300% 46.97$

Flight

Leg Date From To Flight Type Hrs. Statute

Miles Total Pax

Business Pax

Pers Non-Ent Pax

Entertain Pax

Exempt Spouse &

Dependents

Non-Control Guests

0-500 Miles501-1500

Miles1500+ Miles Subtotal Factor Subtotal

Terminal Charge

Subtotal Imputed Income

Reimbursed Entertain Seat Miles

Total Seat Miles

Entertain Seat Hours

Total Seat Hours

Entertain Miles

Entertain Hours

Flight 1: Business Flight

1 1 7/1/12 STL MDW Business 0.7 251 6 6 0.00 - - 1,506 4.2 - -

1 2 7/2/12 MDW STL Business 0.7 251 6 6 0.00 - 1,506 4.2 - -

Flight 2: Entertainment Flight

2 1 7/10/12 STL ORL Entertainment 2.1 874 4 4 128.45 73.27 0.00 201.72 300% 605.15 46.97 652.12 2,608 - 3,496 3,496 8.4 8.4 874 2.10

2 2 7/20/12 ORL STL Entertainment 2.1 874 4 4 128.45 73.27 0.00 201.72 300% 605.15 46.97 652.12 2,608 2,520 3,496 3,496 8.4 8.4 874 2.10

Flight 3: Personal Non-Entertainment Flight

3 1 8/1/12 STL AAO Other Business 0.9 378 2 2 97.11 0.00 0.00 97.11 300% 291.32 46.97 338.29 677 - - 756 1.8 - -

3 2 8/5/12 AAO STL Other Business 0.9 378 2 2 97.11 0.00 0.00 97.11 300% 291.32 46.97 338.29 677 - - 756 1.8 - -

Flight 4: 50% Seating Capacity

4 1 10/18/12 STL PDK Mixed 1.0 476 10 5 5 4 1 122.28 122.28 31.3% 38.28 46.97 85.25 85 - 2,380 4,760 5.0 10.0 238 0.50

4 2 10/20/12 PDK STL Mixed 1.0 476 10 5 5 4 1 122.28 122.28 31.3% 38.28 46.97 85.25 85 - 2,380 4,760 5.0 10.0 238 0.50

Flight 5: Deadhead Leg

5 1 11/18/12 STL PDK Mixed 1.0 476 8 4 4 122.28 0.00 0.00 122.28 300% 366.85 46.97 413.82 - - 1,904 3,808 4.0 8.0 238 0.50

5 2 11/19/12 PDK HPN Deadhead 1.8 763 7 5 2 0.00 - - 1,526 5,341 3.6 12.6 218 0.51

5 3 11/20/12 HPN STL Business 2.0 895 5 5 0.00 - - 4,475 10.0 - -

Summary: All Other Flights

Business 77.5 39,062 215 215 122,762 286.4

91.7 45,154 6,741 2,520 15,182 157,422 34.4 365.8 2,680 6.21

9.64% 9.40% 5.94% 6.78%

SIFL CALCULATION COST DISALLOWANCE

Seat Method Flight-By-Flight Method 50% Seating Capacity

Flights Only

FLIGHT INFORMATION

SIFL & Cost Disallowance Worksheet

59© 2014 Wolcott Aviation Seminars, LLC

60© 2014 Wolcott Aviation Seminars, LLC

NBNE

Entertainment

Entertainment

01/09/14

Copyright 2014 Wolcott Aviation Seminars, LLC 21

61© 2014 Wolcott Aviation Seminars, LLC

Step 1: Log flights and analyze each passenger as onboard for business, NBNA, or entertainment purposes

Step 2: Calculate entertainment cost limitation percentage for the year

Step 3: If reporting MACRS, calculate adjustment to straight-line depreciation (optional)

Step 4: Add direct operating costs, ownership costs and depreciation; multiply by the disallowance percentage, add back the SIFL imputed income and list the disallowance amount as a contra-expense on the tax return

Calculating the Entertainment Disallowance

62© 2014 Wolcott Aviation Seminars, LLC

Summary

Flight Leg Date From To Flight Type Hrs.

Statute Miles

Total Pax

Business Pax

Pers Non-Ent Pax

Entertain Pax

Entertain Seat Miles

Total Seat Miles

Entertain Seat Hours

Total Seat Hours

Entertain Miles

Entertain Hours

Summary: All Other Flights

Business 77.5 39,062 215 215 122,762 286.4

91.7 45,154 15,182 157,422 34.4 365.8 2,680 6.21

21.8% 24.9% 20.5% 23.9%

COST DISALLOWANCE

Seat Method Flight-By-Flight Method

FLIGHT INFORMATION

63© 2014 Wolcott Aviation Seminars, LLC

Calculates entertainment cost disallowance under all four methods. Permits taxpayer to select the method that has the best results.

20.5%

Cost Disallowance Report

01/09/14

Copyright 2014 Wolcott Aviation Seminars, LLC 22

64© 2014 Wolcott Aviation Seminars, LLC

Step 1: Log flights and analyze each passenger as onboard for business, NBNA, or entertainment purposes

Step 2: Calculate entertainment cost limitation percentage for the year

Step 3: If reporting MACRS, calculate adjustment to straight-line depreciation (optional)

Step 4: Add direct operating costs, ownership costs and depreciation; multiply by the disallowance percentage, add back the SIFL imputed income and list the disallowance amount as a contra-expense on the tax return

Calculating the Entertainment Disallowance

65© 2014 Wolcott Aviation Seminars, LLC

Use of Straight-Line Depreciation for Disallowed Depreciation

“Solely for purposes of paragraph (d)(1) of this section, a taxpayer may elect to treat as its depreciation deduction the amount that would result from using the straight-line method of depreciation over the class life (as defined by section 168(i)(1)…”

Means taxpayer has the option to substitute straight-line depreciation for the disallowed portion of depreciation

Disallowed depreciation is added back to the basis of the aircraft

§1.274‐10 (d)(3)(i) Special rules for aircraft used for entertainment 10302

66© 2014 Wolcott Aviation Seminars, LLC

If Part 91 is the predominant use, use MACRS 5-year If Part 135 is the predominant use, use MACRS 7-year Reduce depreciation by the disallowance percentage Taxpayer has the option to convert the disallowed

depreciation to straight line Report depreciation at gross amount on the Form 4562 Adjust for percentage of disallowance and optional

conversion to SL in workpapers Include depreciation adjustment in the Sec. 274

adjustment line item

Calculating the MACRS Depreciation Disallowance

01/09/14

Copyright 2014 Wolcott Aviation Seminars, LLC 23

67© 2014 Wolcott Aviation Seminars, LLC

Summary: Use of Straight-Line for Disallowed Depreciation

Converting the disallowed depreciation to straight-line works best if the aircraft is at the beginning of the depreciation cycle

Disallowed depreciation is added back to the basis of the aircraft at disposition

Even fully depreciated aircraft will have basis remaining to offset gain at sale if there was entertainment use

§1.274‐10 (d)(3)(i) Special rules for aircraft used for entertainment

10302

68© 2014 Wolcott Aviation Seminars, LLC

Step 1: Log flights and analyze each passenger as onboard for business, NBNA, or entertainment purposes

Step 2: Calculate entertainment cost limitation percentage for the year

Step 3: If reporting MACRS, calculate adjustment to straight-line depreciation (optional)

Step 4: Add direct operating costs, ownership costs and depreciation; multiply by the disallowance percentage, add back the SIFL imputed income and list the disallowance amount as a contra-expense on the tax return

Calculating the Entertainment Disallowance

69© 2014 Wolcott Aviation Seminars, LLC

Calculating the Disallowance

Category Amount

Direct Operating Costs $225,000

Ownership Costs 330,356

Depreciation 1,000,000

Subtotal 1,555,356

Entertainment Disallowance Percentage X 20.5%

Gross Disallowance 318,848

Add Back SIFL 20,406

Net Entertainment Cost Disallowance $ 298,442

01/09/14

Copyright 2014 Wolcott Aviation Seminars, LLC 24

© 2014 Wolcott Aviation Seminars, LLC 70

2013

71© 2014 Wolcott Aviation Seminars, LLC

Expense Amount

Fuel $225,000

Crew Costs 195,000

Maintenance 135,000

Hangar 45,000

1.274‐10(e) Adjustment ‐298,442

Line 26 ‐ Total Other Deductions $166,202

Reporting the Entertainment Cost Disallowance on the Tax Return Supporting Schedule

Expense Amount

Fuel $225,000

Crew Costs 195,000

Maintenance 135,000

Hangar 45,000

1.274‐10(e) Adjustment ‐298,442

Line 26 ‐ Total Other Deductions $166,202

72© 2014 Wolcott Aviation Seminars, LLC

Disallowance Must Include All Costs -

Individual 1040

Operating Company

Apply entertainment cost limitations to both

entities

Depreciation, Interest Expense

Direct Operating Costs, Pilot/Crew Costs, Insurance

Dry LeaseAircraft Owning

Entity

Even If In Separate Entities

01/09/14

Copyright 2014 Wolcott Aviation Seminars, LLC 25

73© 2014 Wolcott Aviation Seminars, LLC

CHECKLIST FOR SIFL, COST DISALLOWANCE & FETTopic SIFL Employee

IncomeApply 274 Cost Disallowance

Company Business Flights (Bucket #1) No No

Other Business Flights (Bucket #2) Yes No

Entertainment Flights (Bucket #3) Yes Yes

Deadhead Flight No Yes

Timeshare Flight – Employee Yes Yes

Timeshare Flight – Non‐Employee No No

Schwab Flights Yes Yes

Open Jaw Flights Yes Yes

Fiscal Year Reporting (October 31) Yes No

Calculate using all 4 methods, and compare No Yes

Control & Non‐Control Employees Yes No

Specified Individuals No Yes

Bona Fide Security Plan Yes No

Chartered or Leased Aircraft Yes Yes

Commuting Flights Yes No

74© 2014 Wolcott Aviation Seminars, LLC

Upcoming Webinars February 6, 2014: SIFL Income Calculations for Employee Use

of Company Aircraft (Advanced Level Course). An in-depth study of the rules and techniques for calculating SIFL imputed income. Many example flights. 1 hr. CPE and CLE

February 13, 2014: Reporting Entertainment Cost Disallowance Adjustments (Advanced Level Course). What’s new in the Final Regulations, analyze calculation methods, special flight types, such as deadhead and open jaw, and 11 strategies for minimizing the disallowance. 1 hr. CPE and CLE

National Association of State Boards of Accountancy (NASBA) Group Internet Based Programs sponsor ID 108984

Florida Bar Association Continuing Legal Education Accreditation Provider # 283052

75© 2014 Wolcott Aviation Seminars, LLC

Flight Tax Systems, LLC

Software for Aircraft Owners, Operators, and Tax Professionals

01/09/14

Copyright 2014 Wolcott Aviation Seminars, LLC 26

76© 2014 Wolcott Aviation Seminars, LLC

General Features

Prepares SIFL reports ready for use by payroll department

Cost disallowance reports ready for accounting department

Federal Excise Tax reporting SEC incremental cost reporting State tax reporting Cost center reporting No date restrictions; input last year’s flights as well

as this year’s flights

Flight Tax Systems

77© 2014 Wolcott Aviation Seminars, LLC

Internet-based; access anywhere there is web-access Multiple owners/one aircraft and multiple aircraft/one

owner Fleet can include owned, fractional, and jet card

aircraft Fully annotated with links to the IRS tax code and

regulations Import flight data electronically from: Excel spreadsheets CSV files Most commercial scheduling software programs

General Features

Flight Tax Systems

© 2014 Wolcott Aviation Seminars, LLC 78

The Aviation Tax Reporting Process

Flight Reports Tax

Reports

Flight TrackingFlight Tax Systems

BookkeepingPost Receipts

Pay Bills

Prepare Tax

Returns

Personal1040

Pt‐ship1065

S‐Corp1120‐S

Corporate1120

State Sales & Use

Contract Labor 1099

PayrollW‐2

SpecialPurpose

Maint.

Training

PAX

Flight Types

MainFrame

Quicken

QuickBooks

Excel

Accounting

TrialBalance

BalanceSheet

IncomeStatement

CashFlows

Reports

SIFL

CostDisallow.

PrimaryPurpose

Leasing

Sales & Use Tax

Reports

SEC

01/09/14

Copyright 2014 Wolcott Aviation Seminars, LLC 27

79© 2014 Wolcott Aviation Seminars, LLC

SIFL Reporting

Point-to-point reporting, control and non-control employees

Recognizes 50% seating capacity rules Follows international SIFL rules for flights lasting in

excess of 7 days Recognizes children under age 2, Bona Fide Security

Plans, spousal travel reporting Fiscal and calendar year reporting

Flight Tax Systems

80© 2014 Wolcott Aviation Seminars, LLC

SIFL Year‐to‐Date Summary

SIFL Report

Footnotes explain SIFL reporting rules

Flight Tax Systems

81© 2014 Wolcott Aviation Seminars, LLC

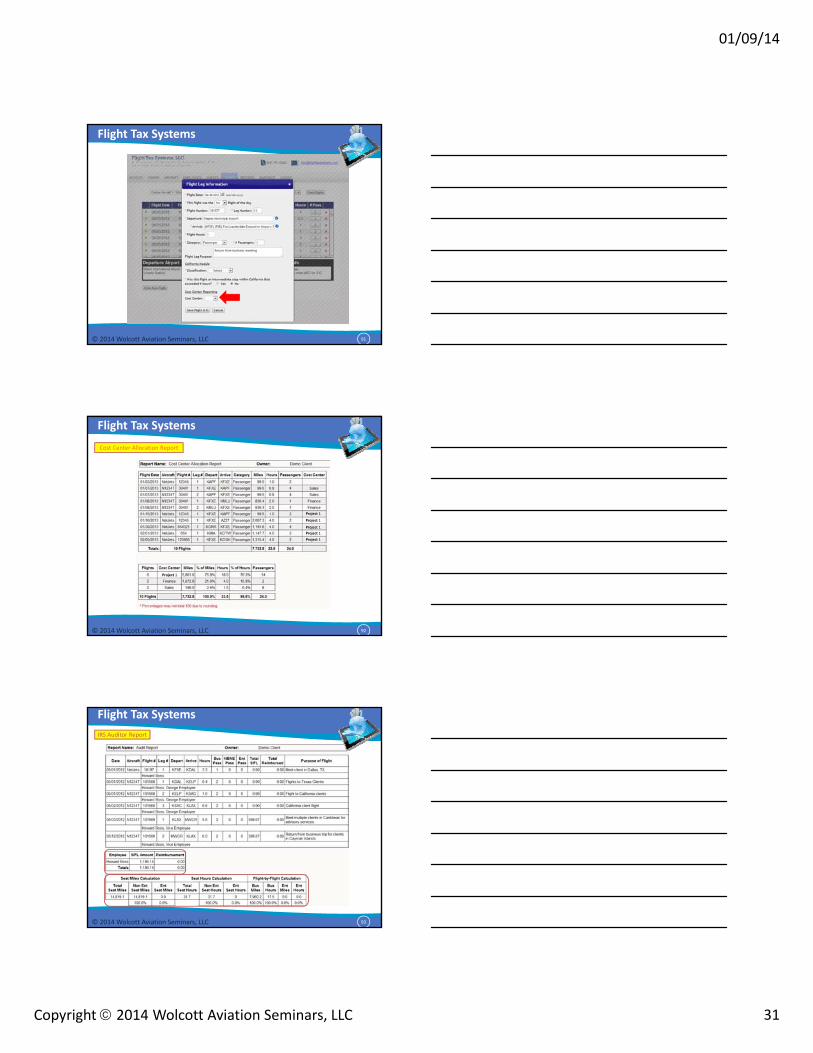

Cost Disallowance Reporting

Conforms to final Regs. issued August 1, 2012 Tracks each individual on each flight, as

required by IRS rules Reports deadhead flights as IRS requires Calculates cost disallowance using all four

methods allowed by IRS “Open Jaw” flight reporting Timeshare flights Schwab reimbursement flights

Flight Tax Systems

01/09/14

Copyright 2014 Wolcott Aviation Seminars, LLC 28

82© 2014 Wolcott Aviation Seminars, LLC

Calculates entertainment cost disallowance under all four methods. Permits taxpayer to select the method that has the best results.

Entertainment Cost Disallowance Report

Flight Tax Systems

83© 2014 Wolcott Aviation Seminars, LLC

Special Reports for CPAs and Accountants

Treas. Reg. 280F Depreciation Report Calculates the eligibility for MACRS &

bonus depreciation Includes analysis of 5% owner leasing use

Treas. Reg. 1.469 Active vs. Passive Analysis Calculates % of active use vs. passive use Prorates maintenance and training use

between active and passive

Flight Tax Systems

84© 2014 Wolcott Aviation Seminars, LLC

SEC Reporting Names and tracks all seven principal and highly

compensated executives according to SEC reporting rules Tracks dates of applicability for each reportable executive Assigns incremental hourly cost amount to each aircraft in

the company’s fleet Prints individual and combined reports for each

reportable executive Wolcott & Associates, P.A. can provide a compilation

report explaining the methods for computing the incremental cost and executive compensation listed in the SEC reports and proxy statement

Flight Tax Systems

01/09/14

Copyright 2014 Wolcott Aviation Seminars, LLC 29

© 2014 Wolcott Aviation Seminars, LLC 85

SEC reporting for executive fringe benefits for proxy reporting.

Flight Tax Systems

SEC Report

86© 2014 Wolcott Aviation Seminars, LLC

Reports for calculating sales and use taxes Reports for limiting ad valorem taxes States included in Enterprise Version:

Florida

California

Texas

Louisiana

Georgia

Mississippi

STATE TAX MODULES

Flight Tax Systems

87© 2014 Wolcott Aviation Seminars, LLC

California Module Use Tax Exemptions - Tracks aircraft use and rules

for use tax exemptions: Not Purchased for Use in California Interstate and Foreign Commerce Exemption Common Carrier Exemption

Aircraft Leasing Company: Tracks use of the aircraft for aircraft leasing company sales or use tax deferral provision

Personal Property Taxes: Days-in-state report Ground time by county report

Flight Tax Systems

01/09/14

Copyright 2014 Wolcott Aviation Seminars, LLC 30

88© 2014 Wolcott Aviation Seminars, LLC

Flight Tax Systems

© 2014 Wolcott Aviation Seminars, LLC 89

California Landing Report

Flight Tax Systems

90© 2014 Wolcott Aviation Seminars, LLC

Cost Center Reporting Assigns a cost per hour to each aircraft in the fleet Allows an unlimited number of user definable cost centers User assigns flight legs to specific departments or cost

centers Allows companies to bill aircraft use to divisions,

departments, or cost centers

Flight Tax Systems

01/09/14

Copyright 2014 Wolcott Aviation Seminars, LLC 31

91© 2014 Wolcott Aviation Seminars, LLC

Flight Tax Systems

92© 2014 Wolcott Aviation Seminars, LLC

Cost Center Allocation Report

Flight Tax Systems

Project 1

Project 1

Project 1

Project 1

Project 1

Project 1

93© 2014 Wolcott Aviation Seminars, LLC

IRS Auditor Report

Flight Tax Systems

01/09/14

Copyright 2014 Wolcott Aviation Seminars, LLC 32

94© 2014 Wolcott Aviation Seminars, LLC

General Flight Report

Flight Tax Systems

95© 2014 Wolcott Aviation Seminars, LLC

COST, BILLING AND SUPPORT

Annual subscription is $3,995 (Enterprise version) Provides 12 months of program access Unlimited use; no date or aircraft restrictions Custom programming and reports available Aviation CPAs from our parent company provide 2

hours of free support. We take you through setup and flight recording. Additional support available

Call 866-791-6092 www.flighttaxsystems.com to sign up!

Flight Tax Systems

96© 2014 Wolcott Aviation Seminars, LLC

Thank You Very Much!

Jed R. Wolcott, MBA Sue Folkringa, MBACertified Public Accountant Certified Public Accountantjedw@aviation‐cpa.com Suef@aviation‐cpa.com

Wolcott & Associates, P.A.Flight Tax Systems, LLC

5525 NW 15th Avenue, Suite 203Fort Lauderdale, Florida 33309

866‐791‐6092www.aviation‐cpa.com

Flight Tax Systems