Financial Planning

31

F inancial P lanning PND MENTOR CONSULTANTS From: PND Mentor Consultants (A Trusted Advisor)

-

Upload

nimesh-dedhia -

Category

Services

-

view

152 -

download

0

Transcript of Financial Planning

Financial Planning

From:PND Mentor Consultants

(A Trusted Advisor)PND MENTOR CONSULTANTS

Financial Planning

From:PND Mentor Consultants

(A Trusted Advisor)

What is Financial Planning?

• Financial planning is the process of creating,managing & enhancing wealth during the lifetime orwe can say it is the process of meeting your life goalsthrough the proper management of your finances.

• Life goals can include buying a home, saving for yourchild's education or planning for retirement.

• It includes insurance planning, investment planning,tax planning, retirement planning and estate planning.

PND MENTOR CONSULTANTS

• Financial planning is the process of creating,managing & enhancing wealth during the lifetime orwe can say it is the process of meeting your life goalsthrough the proper management of your finances.

• Life goals can include buying a home, saving for yourchild's education or planning for retirement.

• It includes insurance planning, investment planning,tax planning, retirement planning and estate planning.

Why Financial Planning?• Inflation

Cost of Education / Medical increasing exponentially

• Rising Life expectancyestimated to increase from 75 to 85 in next decade

• Protection against the uncertaintyProtect lifestyle of family in your absence

• Balanced Assets AllocationAllocate your investment in Short Term & Long Termperspective to achieve maximum gain at minimumrisk.

PND MENTOR CONSULTANTS

• InflationCost of Education / Medical increasing exponentially

• Rising Life expectancyestimated to increase from 75 to 85 in next decade

• Protection against the uncertaintyProtect lifestyle of family in your absence

• Balanced Assets AllocationAllocate your investment in Short Term & Long Termperspective to achieve maximum gain at minimumrisk.

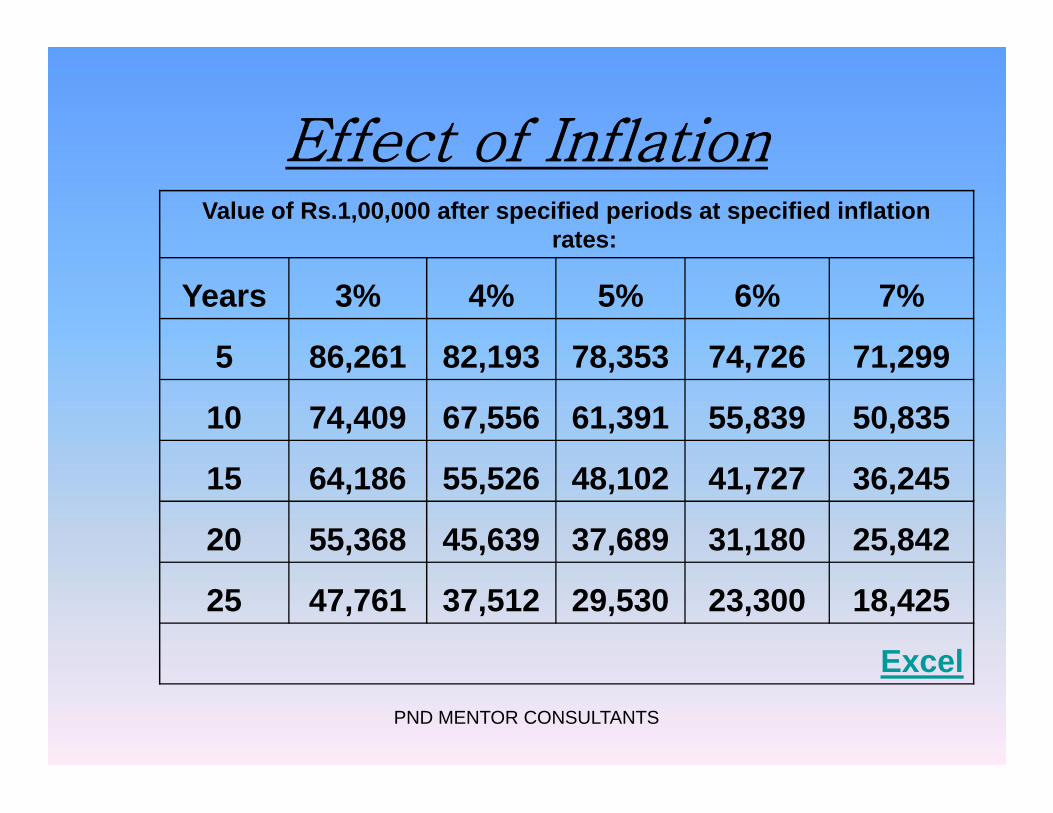

Effect of InflationValue of Rs.1,00,000 after specified periods at specified inflation

rates:

Years 3% 4% 5% 6% 7%

5 86,261 82,193 78,353 74,726 71,299

10 74,409 67,556 61,391 55,839 50,835

PND MENTOR CONSULTANTS

10 74,409 67,556 61,391 55,839 50,835

15 64,186 55,526 48,102 41,727 36,245

20 55,368 45,639 37,689 31,180 25,842

25 47,761 37,512 29,530 23,300 18,425

Excel

What is Insurance Planning?

• Insurance planning is a tool to minimiseor to avoid risks.

• What type of Risk?1. Risk of Early Death2. Risk of Disability3. Risk of Assets

PND MENTOR CONSULTANTS

• Insurance planning is a tool to minimiseor to avoid risks.

• What type of Risk?1. Risk of Early Death2. Risk of Disability3. Risk of Assets

How to Avoid Risk?

• Identify your needs

• How much insurance do you need?

• Which product should you consider?

PND MENTOR CONSULTANTS

• Identify your needs

• How much insurance do you need?

• Which product should you consider?

How to Identify your needs?

• An individual is single & a marriedindividual who has family membersdependent on him both has a differentneed.

• Dependency of your family on your incomewill help to calculate your need.

PND MENTOR CONSULTANTS

• An individual is single & a marriedindividual who has family membersdependent on him both has a differentneed.

• Dependency of your family on your incomewill help to calculate your need.

How much insurance do you need?

• The concept of human life value (HLV) can help indeciding how much life cover an individual should optfor.

• Human Life Value (HLV) is a methodology to determinethe appropriate amount of sum assured you need tohave at present in case of future loss of income.

• In simple words, it is that amount, which can ensure thatthe standard of living of the family is not affected even ifthe earning member is not there.

PND MENTOR CONSULTANTS

• The concept of human life value (HLV) can help indeciding how much life cover an individual should optfor.

• Human Life Value (HLV) is a methodology to determinethe appropriate amount of sum assured you need tohave at present in case of future loss of income.

• In simple words, it is that amount, which can ensure thatthe standard of living of the family is not affected even ifthe earning member is not there.

How to Calculate HLVMonthly income of a person Rs.10,000

His personal expenses per month Rs.2,000

Monthly income provided to family Rs.8,000

Therefore, annual income provided Rs.96,000

PND MENTOR CONSULTANTS

Amount of money to be put in the bankto earn Rs.96,000 pa at 8% interest rate

Rs.12,00,000

Hence, HLV is Rs.12 lakhs

Please note that however we have not taken into account the future income growth of theperson. This is, therefore, not an exact way of calculating the Human Life Value. This is only arepresentation to give the participants a fair idea of how this works.

Excel

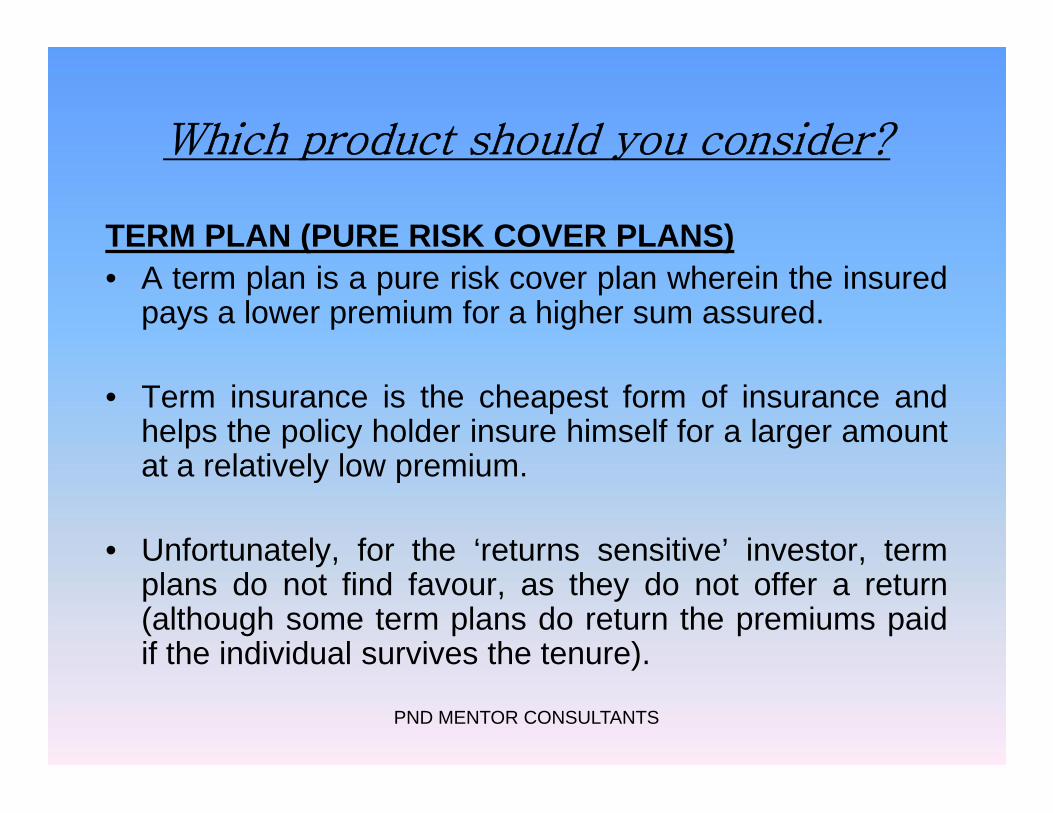

Which product should you consider?

TERM PLAN (PURE RISK COVER PLANS)• A term plan is a pure risk cover plan wherein the insured

pays a lower premium for a higher sum assured.

• Term insurance is the cheapest form of insurance andhelps the policy holder insure himself for a larger amountat a relatively low premium.

• Unfortunately, for the ‘returns sensitive’ investor, termplans do not find favour, as they do not offer a return(although some term plans do return the premiums paidif the individual survives the tenure).

PND MENTOR CONSULTANTS

TERM PLAN (PURE RISK COVER PLANS)• A term plan is a pure risk cover plan wherein the insured

pays a lower premium for a higher sum assured.

• Term insurance is the cheapest form of insurance andhelps the policy holder insure himself for a larger amountat a relatively low premium.

• Unfortunately, for the ‘returns sensitive’ investor, termplans do not find favour, as they do not offer a return(although some term plans do return the premiums paidif the individual survives the tenure).

Comparison B/W Term Plan &Endowment Plan of LIC

Details of Term Plan from LICAge

(Yrs)Sum

Assured (Rs)AnnualPremium

(Rs)Tenure

(Yrs)Total

Premium*(Rs)

Maturityamount onsurvival (Rs)

30 10,00,000 3,820 25 95,500 Nil

PND MENTOR CONSULTANTS

30 10,00,000 3,820 25 95,500 Nil

Details of Endowment Plan from LICAge

(Yrs)Sum

Assured (Rs)AnnualPremium

(Rs)Tenure

(Yrs)Total

Premium*(Rs)

Maturityamount onsurvival (Rs)

30 10,00,000 38,820 25 9,70,500 22,57,600(Approx 6%)

What should be the plan?Case Particulars Age

(Yrs)Avenues Tenure

(Yrs)Amount

(Rs)Return

(%)Maturity

Amount(Rs)

1 Term plan (10 Lacs+

Secured mutualfund

(100% Debt)

30 Term plan 25 3,820 * Nil

Mutual fund 25 35,000 8 27,63,406

2 Term plan (10Lacs) +

Balanced mutualfund

(40% in Equities)

30 Term plan 25 3,820 * Nil

PND MENTOR CONSULTANTS

Term plan (10Lacs) +

Balanced mutualfund

(40% in Equities)

30 25 3,820 *

Mutual fund 25 35,000 10 37,86,367

3 Term plan (10Lacs)+

Diversified equityfund

(100% in Equity)

30 Term plan 25 3,820 * Nil

Diversifiedequityfund

25 35,000 15 85,64,937

Investment in mutual funds are subject to market risk. Excel

Investment Planning

• What is Investing?Investment refers to a commitment of funds to one ormore assets that will be held over some future timeperiod.

• What is Investment Planning?Investment Planning means to manage our wealtheffectively, obtaining the most from it.

• Why Investment Planning?Creating wealth over the long termAcquiring assets like a dream house or a dream carFulfilling your need for financial security

PND MENTOR CONSULTANTS

• What is Investing?Investment refers to a commitment of funds to one ormore assets that will be held over some future timeperiod.

• What is Investment Planning?Investment Planning means to manage our wealtheffectively, obtaining the most from it.

• Why Investment Planning?Creating wealth over the long termAcquiring assets like a dream house or a dream carFulfilling your need for financial security

What Investment Planning Includes?

• Evaluating Risk

• Asset Allocation

• Creation and Accumulation of Wealth throughSystematic Investment Plans (SIP)

• Regular review of progress and PortfolioRebalancing

PND MENTOR CONSULTANTS

• Evaluating Risk

• Asset Allocation

• Creation and Accumulation of Wealth throughSystematic Investment Plans (SIP)

• Regular review of progress and PortfolioRebalancing

Evaluating Risk

• Thumb rule says you should invest in Equityinverse to your age (means 30 year age personcan take risk of investing in equity up to 70%)

• Age, personal circumstances & general marketconditions is crucial factor while deciding risk.

• Right investment is a balance of three things:Liquidity, Safety and Return.

PND MENTOR CONSULTANTS

• Thumb rule says you should invest in Equityinverse to your age (means 30 year age personcan take risk of investing in equity up to 70%)

• Age, personal circumstances & general marketconditions is crucial factor while deciding risk.

• Right investment is a balance of three things:Liquidity, Safety and Return.

Asset Allocation

• Assets allocation is the main aspects ofthe investment planning.

• Allocate your investment looking to yourfuture plans.

• You should have Cash/Liquid Assts, Shortterm Assets, Medium Term Assets & LongTerm Assts as per your Future Goal.

PND MENTOR CONSULTANTS

• Assets allocation is the main aspects ofthe investment planning.

• Allocate your investment looking to yourfuture plans.

• You should have Cash/Liquid Assts, Shortterm Assets, Medium Term Assets & LongTerm Assts as per your Future Goal.

NO. YEAR END SENSEX ROLLING 1YEAR

GROWTH

ROLLING 3YEAR

GROWTH

ROLLING 5YEAR

GROWTH

ROLLING 7YEAR

GROWTH

ROLLING 10YEAR GROWTH

ROLLING 15YEAR GROWTH

0 Mar-79 1001 Mar-80 129 28.57%2 Mar-81 173 34.90%3 Mar-82 218 25.52% 29.58%4 Mar-83 212 -2.85% 18.05%5 Mar-84 245 15.99% 12.24% 19.64%6 Mar-85 354 44.24% 17.56% 22.43%7 Mar-86 574 62.24% 39.45% 27.03% 28.33%8 Mar-87 510 -11.10% 27.66% 18.57% 21.76%9 Mar-88 398 -21.94% 4.02% 13.48% 12.60%14 Mar-93 2281 -46.78% 42.88% 41.73% 21.76% 26.82%15 Mar-94 3779 65.71% 47.85% 39.54% 33.08% 31.43% 27.37%16 Mar-95 3261 -13.71% -8.70% 33.07% 35.02% 24.85% 24.04%17 Mar-96 3367 3.24% 13.85% 23.55% 24.79% 19.33% 21.84%18 Mar-97 3361 -0.17% -3.83% -4.74% 23.16% 20.72% 20.00%19 Mar-98 3893 15.82% 6.08% 11.28% 18.75% 25.59% 21.41%20 Mar-99 3740 -3.92% 3.57% -0.21% -1.92% 18.01% 19.90%21 Mar-00 5001 33.73% 14.15% 8.92% 11.86% 20.39% 19.30%22 Mar-01 3604 -27.93% -2.53% 1.37% -0.67% 11.92% 13.02%23 Mar-02 3469 -3.75% -2.47% 0.64% 0.89% -2.09% 13.62%24 Mar-03 3049 -12.12% -15.21% -4.77% -1.41% 2.94% 14.52%25 Mar-04 5591 83.38% 15.74% 8.36% 7.53% 3.99% 14.70%26 Mar-05 6493 16.14% 23.21% 5.36% 7.58% 7.12% 15.15%27 Mar-06 11280 73.73% 54.61% 25.61% 17.07% 12.85% 16.31%28 Mar-07 13072 15.89% 32.73% 30.36% 14.71% 14.54% 7.71%29 Mar-08 15644 19.68% 34.03% 38.64% 23.31% 14.91% 13.69%30 Mar-09 9709 -37.94% -4.87% 11.66% 15.82% 10.00% 6.49%31 Mar-10 17528 80.54% 10.26% 21.96% 28.36% 13.35% 11.86%32 Mar-11 19445 10.94% 7.52% 11.50% 19.48% 18.35% 12.39%33 Mar-12 17404 -10.50% 21.46% 5.89% 15.11% 17.49% 11.58%34 Mar-13 18836 8.23% 2.43% 3.78% 7.59% 19.96% 11.07%35 Mar-14 22386 18.85% 4.80% 18.18% 7.98% 14.87% 12.66%36 Mar-15 27957 24.89% 17.12% 9.78% 8.64% 15.71% 12.15%

12/36 6/34 3/32 3/30 1/27 0/22

PERFORMANCE OF BSE SENSEX

Probability of LossPND MENTOR CONSULTANTS

NO. YEAR END SENSEX ROLLING 1YEAR

GROWTH

ROLLING 3YEAR

GROWTH

ROLLING 5YEAR

GROWTH

ROLLING 7YEAR

GROWTH

ROLLING 10YEAR GROWTH

ROLLING 15YEAR GROWTH

0 Mar-79 1001 Mar-80 129 28.57%2 Mar-81 173 34.90%3 Mar-82 218 25.52% 29.58%4 Mar-83 212 -2.85% 18.05%5 Mar-84 245 15.99% 12.24% 19.64%6 Mar-85 354 44.24% 17.56% 22.43%7 Mar-86 574 62.24% 39.45% 27.03% 28.33%8 Mar-87 510 -11.10% 27.66% 18.57% 21.76%9 Mar-88 398 -21.94% 4.02% 13.48% 12.60%14 Mar-93 2281 -46.78% 42.88% 41.73% 21.76% 26.82%15 Mar-94 3779 65.71% 47.85% 39.54% 33.08% 31.43% 27.37%16 Mar-95 3261 -13.71% -8.70% 33.07% 35.02% 24.85% 24.04%17 Mar-96 3367 3.24% 13.85% 23.55% 24.79% 19.33% 21.84%18 Mar-97 3361 -0.17% -3.83% -4.74% 23.16% 20.72% 20.00%19 Mar-98 3893 15.82% 6.08% 11.28% 18.75% 25.59% 21.41%20 Mar-99 3740 -3.92% 3.57% -0.21% -1.92% 18.01% 19.90%21 Mar-00 5001 33.73% 14.15% 8.92% 11.86% 20.39% 19.30%22 Mar-01 3604 -27.93% -2.53% 1.37% -0.67% 11.92% 13.02%23 Mar-02 3469 -3.75% -2.47% 0.64% 0.89% -2.09% 13.62%24 Mar-03 3049 -12.12% -15.21% -4.77% -1.41% 2.94% 14.52%25 Mar-04 5591 83.38% 15.74% 8.36% 7.53% 3.99% 14.70%26 Mar-05 6493 16.14% 23.21% 5.36% 7.58% 7.12% 15.15%27 Mar-06 11280 73.73% 54.61% 25.61% 17.07% 12.85% 16.31%28 Mar-07 13072 15.89% 32.73% 30.36% 14.71% 14.54% 7.71%29 Mar-08 15644 19.68% 34.03% 38.64% 23.31% 14.91% 13.69%30 Mar-09 9709 -37.94% -4.87% 11.66% 15.82% 10.00% 6.49%31 Mar-10 17528 80.54% 10.26% 21.96% 28.36% 13.35% 11.86%32 Mar-11 19445 10.94% 7.52% 11.50% 19.48% 18.35% 12.39%33 Mar-12 17404 -10.50% 21.46% 5.89% 15.11% 17.49% 11.58%34 Mar-13 18836 8.23% 2.43% 3.78% 7.59% 19.96% 11.07%35 Mar-14 22386 18.85% 4.80% 18.18% 7.98% 14.87% 12.66%36 Mar-15 27957 24.89% 17.12% 9.78% 8.64% 15.71% 12.15%

12/36 6/34 3/32 3/30 1/27 0/22

PERFORMANCE OF BSE SENSEX

Probability of Loss

PND MENTOR CONSULTANTS

Power of Compounding

• The following table shows how much your money would grow whenyou invest a fixed amount per month over a period of 5,10, 15, 20, 25,and 30 years at following interest rates:

Rs.1,000 Invested Monthly Amount (Rs)

Years 8% 10% 15% 20% 25%

5 73,967 78,082 89,682 103,454 119,844

PND MENTOR CONSULTANTS

5 73,967 78,082 89,682 103,454 119,844

10 184,166 206,552 278,657 382,364 532,805

15 348,345 417,924 676,863 1,134,295 1,955,785

20 592,947 765,697 1,515,955 3,161,479 6,859,095

25 957,367 1,337,890 3,284,074 8,626,708 23,754,942

30 1,500,295 2,279,325 7,009,821 23,360,802 81,974,715

Excel

Retirement Planning

Why Retirement Planning?• The average life expectancy has expected to

risen to 75-85 years.

• Inflation is hovering around the 5-7 per centmark increasing the cost of living.

• Children settle abroad or away from home andeven the elderly do not want to be dependent ontheir children anymore.

PND MENTOR CONSULTANTS

Why Retirement Planning?• The average life expectancy has expected to

risen to 75-85 years.

• Inflation is hovering around the 5-7 per centmark increasing the cost of living.

• Children settle abroad or away from home andeven the elderly do not want to be dependent ontheir children anymore.

Retirement Planning ExampleCase I Case II Case III

Aggressive Balanced Secured

Current Age 30 30 30

Retirement Age 60 60 60

Time to retirement 30 30 30

Inflation 6% 6% 6%

PND MENTOR CONSULTANTS

Inflation 6% 6% 6%

Rate of return assumed pre-retirement: 15% 10% 8%

Rate of return assumed post-retirement: 8% 8% 8%Current Expenditure required at

retirement 20,000 20,000 20,000Monthly Expenditure required at

retirement 114,870 114,870 114,870

Table continued………………..

Retirement Planning Exampleconti………….

Case I Case II Case III

Aggressive Balanced Secured

Annual Exp. Required at retirement 1,378,438 1,378,438 1,378,438

Other Expenses Required 500,000 500,000 500,000

PND MENTOR CONSULTANTS

Total Expenses required at retirement 1,878,438 1,878,438 1,878,438

Money required to meet the aboveExpenses 23,480,474 23,480,474 23,480,474

Current Investments 100,000 100,000 100,000

Current Investments grown to tillretirement 6,621,177 1,744,940 1,006,266

Net Fund required or to beaccumulated 16,859,296 21,735,533 22,474,208

Retirement Planning Example

Solution:Net Fund required or to be

accumulated 16,859,296 21,735,533 22,474,208

Rate of return assumed pre-retirement: 15% 10% 8%

Available time for Investment (in years) 30 30 30

PND MENTOR CONSULTANTS

Available time for Investment (in years) 30 30 30

Savings required

One Time Savings 254,627 1,245,632 2,233,427

Annual Savings 33,721 120,123 183,694

Monthly Savings 2,405 9,536 14,980

Excel

The Importance of StartingInvestment Early

Case I• Mr. A & Mr. B both aged 30 years wish to make an

investment to build a Retirement Fund.

• Mr. A starts immediately with annual investment ofRs.10,000/- @ 10% p.a.

• While Mr. B starts investing after 10 years but withRs.25,000/- @ 10% p.a.

• Both the Mr. A & Mr. B would like to Retire at Age 60year

PND MENTOR CONSULTANTS

Case I• Mr. A & Mr. B both aged 30 years wish to make an

investment to build a Retirement Fund.

• Mr. A starts immediately with annual investment ofRs.10,000/- @ 10% p.a.

• While Mr. B starts investing after 10 years but withRs.25,000/- @ 10% p.a.

• Both the Mr. A & Mr. B would like to Retire at Age 60year

The Importance of Starting Early

Particulars Mr. A Mr. B

Amount Invested Per Annum 10000 25000

Tenure of Investment 30 20

PND MENTOR CONSULTANTS

Tenure of Investment 30 20

Total Investments 300000 500000

Returns @10% 10% 10%

Maturity Amount 1,809,434 1,575,062

The Importance of Starting Early

Case IIParticulars Mr. A Mr. B Mr. C

Age 30 40 50

Retirement Age 60 60 60

Years available for Investment 30 20 10

PND MENTOR CONSULTANTS

Years available for Investment 30 20 10

Corpus required at retirement age 2,500,000 2,500,000 2,500,000

Rate of Returns 10% 10% 10%

Annual Investment required 13,816 39,681 142,603

Monthly Investment required 1,097 3,265 12,103

Excel

Simple Steps to be a WealthCreator!!!!!

• There is no better time than today to start yourinvestment.

• Waiting for the golden moment will not help in any manner.

• We all know that tax-planning investments can be doneright from the start of the financial year in April, but howmany people actually do it?

• Transfer all risks such as death, disability, critical illness,accident, health and property to the insurance company.

• Understand the consequences of risks more than anythingelse and do not think of insurance as an expense.

PND MENTOR CONSULTANTS

• There is no better time than today to start yourinvestment.

• Waiting for the golden moment will not help in any manner.

• We all know that tax-planning investments can be doneright from the start of the financial year in April, but howmany people actually do it?

• Transfer all risks such as death, disability, critical illness,accident, health and property to the insurance company.

• Understand the consequences of risks more than anythingelse and do not think of insurance as an expense.

Refrain from these 6 mistakesFinally refrain from these 6 mistakes that most equity and

mutual fund investors make:

• Having irrational expectations.• Selling out in bad markets.• Investing short-term money in equity and long-term

money in debt.• Being affected by news, interest rates, oil prices and

losing confidence too soon.• Trying to time the market and waiting for the best time to

buy or sell.• Getting greedy and opting for spicy derivatives,

commodities, trading without understanding the risksassociated.

PND MENTOR CONSULTANTS

Finally refrain from these 6 mistakes that most equity andmutual fund investors make:

• Having irrational expectations.• Selling out in bad markets.• Investing short-term money in equity and long-term

money in debt.• Being affected by news, interest rates, oil prices and

losing confidence too soon.• Trying to time the market and waiting for the best time to

buy or sell.• Getting greedy and opting for spicy derivatives,

commodities, trading without understanding the risksassociated.

Last Thought !!!!!!!!!!!

Even if your financial decision isnot perfect, it may still leave youin a better position than if you haddone nothing.

PND MENTOR CONSULTANTS

Even if your financial decision isnot perfect, it may still leave youin a better position than if you haddone nothing.

PROFILE OF ADVISOR

CA Nimesh Dedhia is a qualified CharteredAccountant since 1999. He has also clearedexamination of Certified Financial Planner. He isalso holding degree of DISA (ICAI).

He has more than 15 years experience in the fieldof Tax Planning & Financial Planning.

Our ARN is 48678 & advising in the field of MutualFund since 2007 and served more than 300 clients.

CA Nimesh Dedhia is a qualified CharteredAccountant since 1999. He has also clearedexamination of Certified Financial Planner. He isalso holding degree of DISA (ICAI).

He has more than 15 years experience in the fieldof Tax Planning & Financial Planning.

Our ARN is 48678 & advising in the field of MutualFund since 2007 and served more than 300 clients.