Financial Crisis and Global Recession: At a Turning...

32

Financial Crisis and Global Recession: At a Turning Point? Richard Newfarmer Special Representative to UN and WTO World Bank Cairo June 15, 2009

Transcript of Financial Crisis and Global Recession: At a Turning...

Financial Crisis and Global Recession:

At a Turning Point?

Richard Newfarmer

Special Representative to UN and WTO

World Bank

Cairo

June 15, 2009

Main messages

Recession in the US now appears to be bottoming out,

but speed and strength of recovery is uncertain

Even though recession will eventually end, several

daunting challenges remain, particularly for the

poorest countries and vulnerable social groups

Domestic policy is critical, but generating a sustained

recovery requires new forms of multilateral

collaboration

Excessively easy money after 2001

Fiscal stimulus as US budget swung from surplus to large deficit

Expansion of opaque financial innovation

– Subprime mortgages

– Home equity lending

– Consolidated Debt Obligations

– Credit Default Swaps

Emergence of unregulated borrowing in the shadow banking system

– Mortgage companies

– Investment banks

– Hedge funds

…leading to excessive leverage of consumers, corporates, and public sectors

…financed by China and other countries accumulating large reserves

Causes: Macroeconomic policy and changes in the

financial system create conditions for the perfect financial

storm

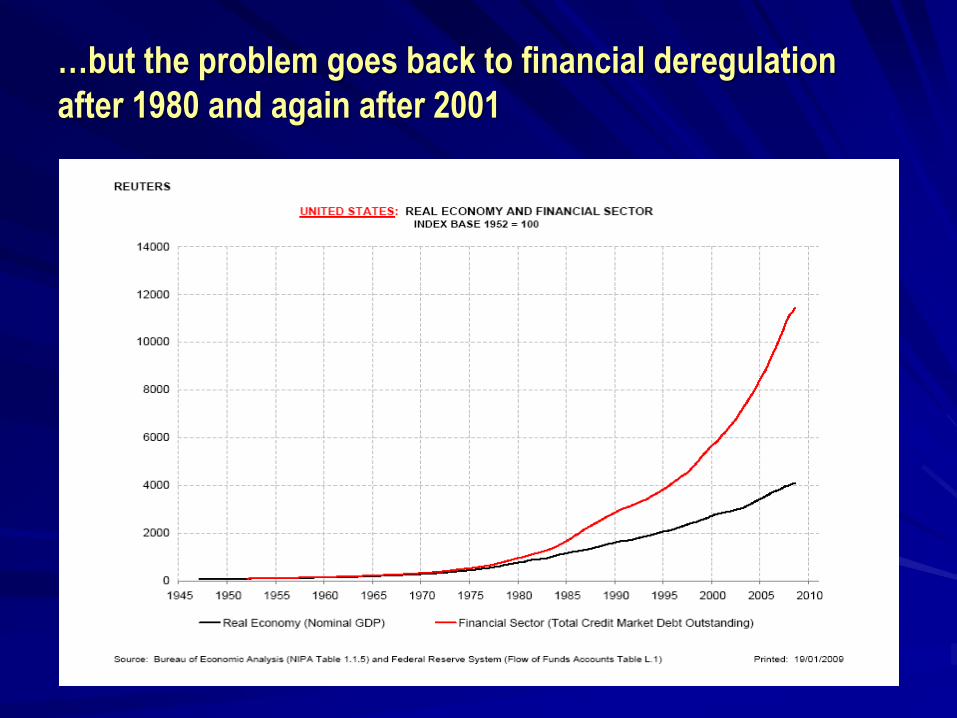

…but the problem goes back to financial deregulation

after 1980 and again after 2001

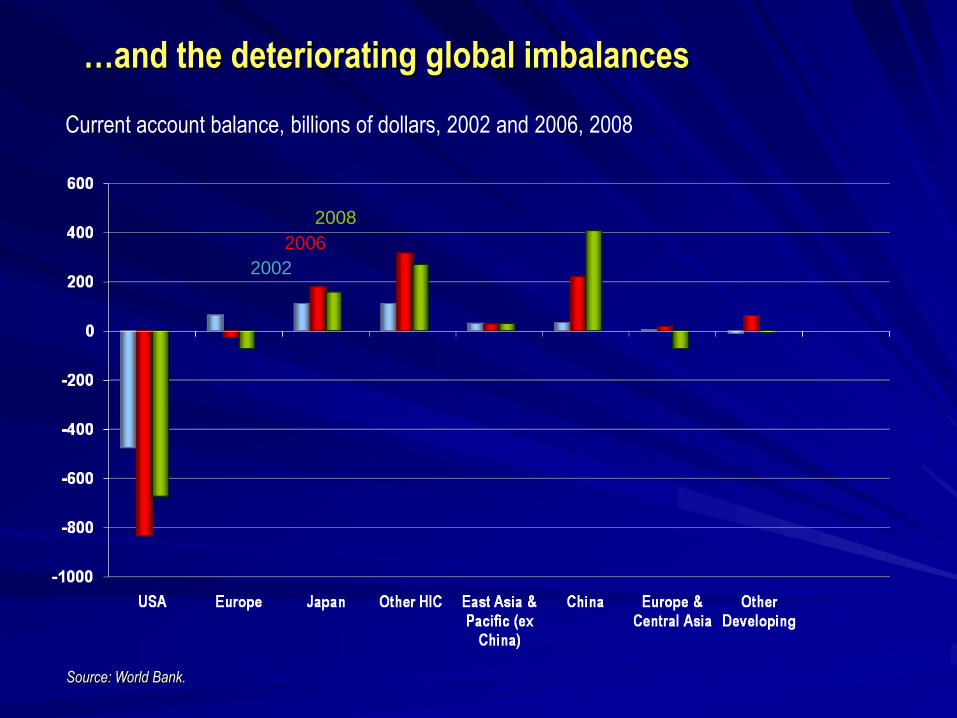

…and the deteriorating global imbalances

Current account balance, billions of dollars, 2002 and 2006, 2008

Source: World Bank.

2002

2006

2008

Emerging markets

USA

Euro Area

Sept-2008

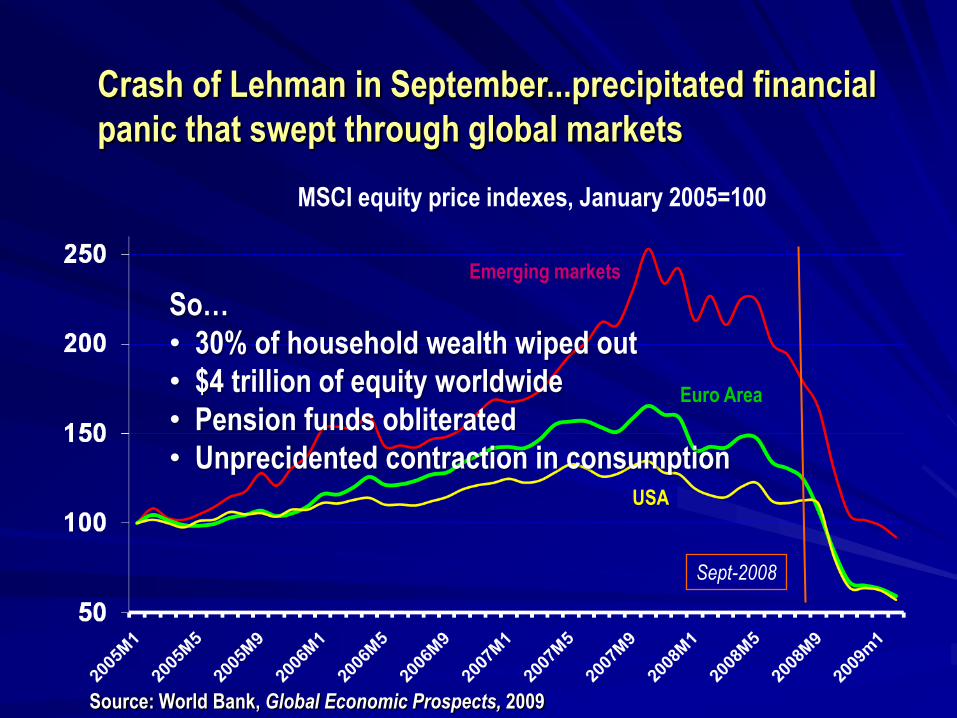

MSCI equity price indexes, January 2005=100

Crash of Lehman in September...precipitated financial

panic that swept through global markets

Source: World Bank, Global Economic Prospects, 2009

So…

• 30% of household wealth wiped out

• $4 trillion of equity worldwide

• Pension funds obliterated

• Unprecidented contraction in consumption

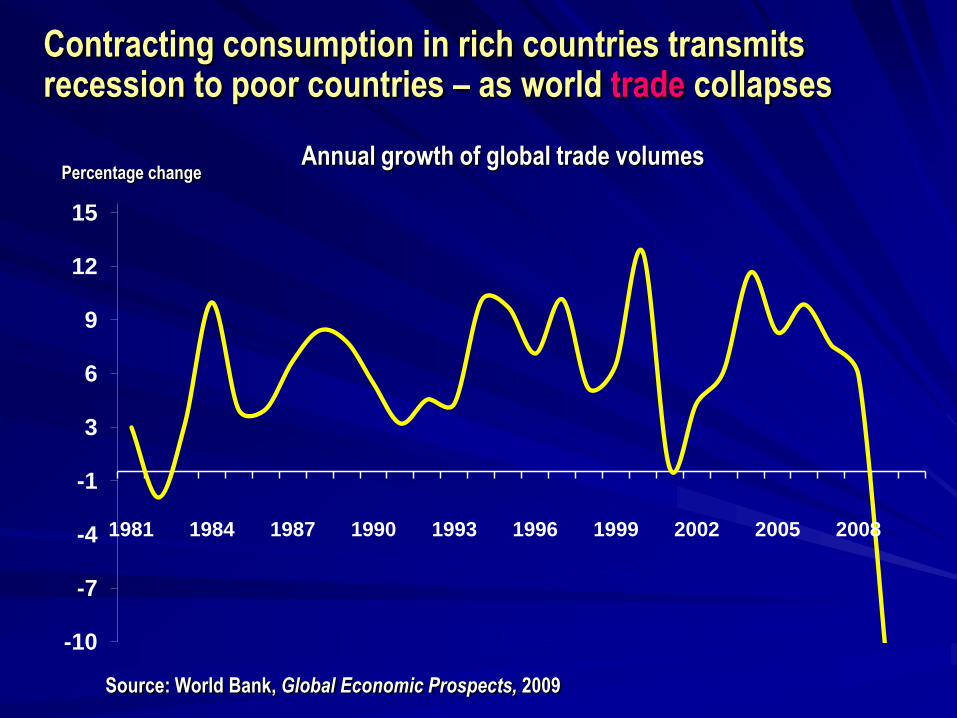

Contracting consumption in rich countries transmits recession to poor countries – as world trade collapses

-10

-7

-4

-1

3

6

9

12

15

1981 1984 1987 1990 1993 1996 1999 2002 2005 2008

Percentage changeAnnual growth of global trade volumes

Source: World Bank, Global Economic Prospects, 2009

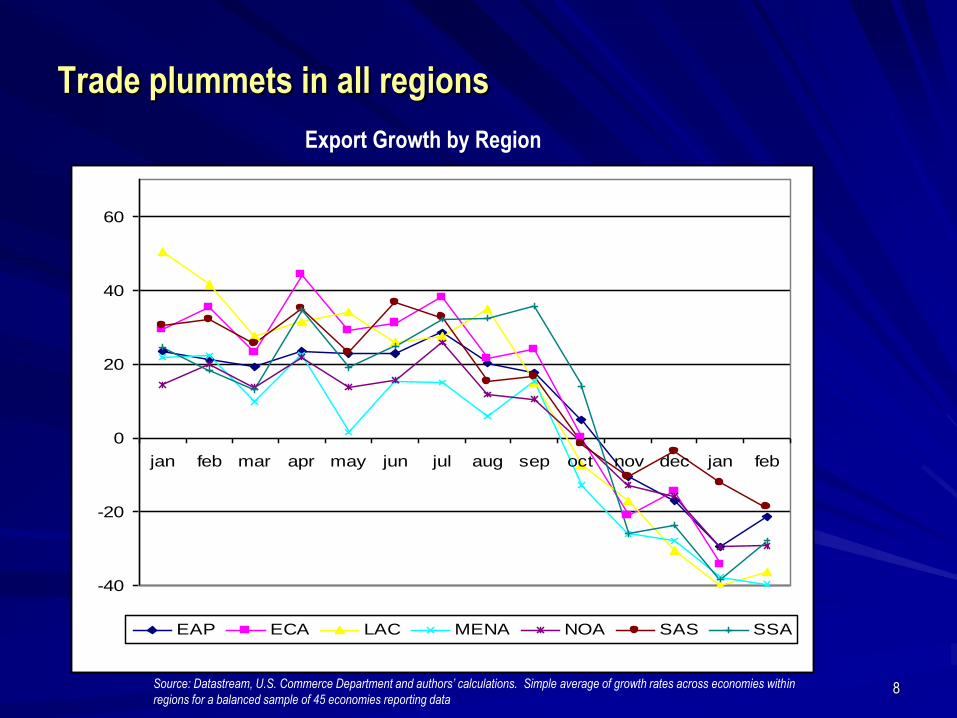

8

Trade plummets in all regions

Source: Datastream, U.S. Commerce Department and authors’ calculations. Simple average of growth rates across economies within

regions for a balanced sample of 45 economies reporting data

-40

-20

0

20

40

60

jan feb mar apr may jun jul aug sep oct nov dec jan feb

EAP ECA LAC MENA NOA SAS SSA

Export Growth by Region

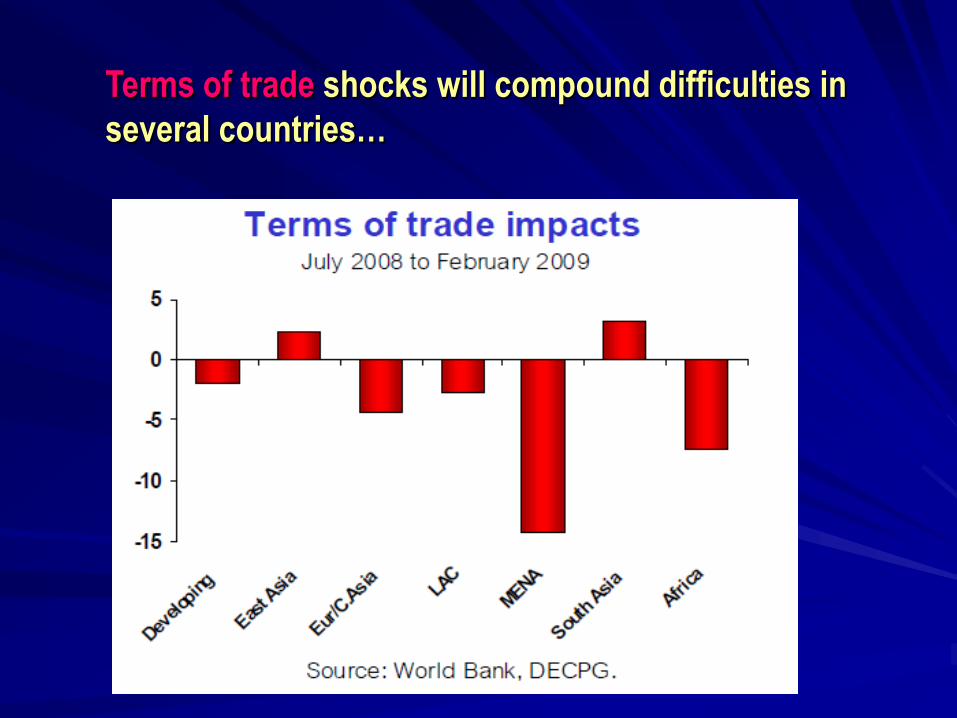

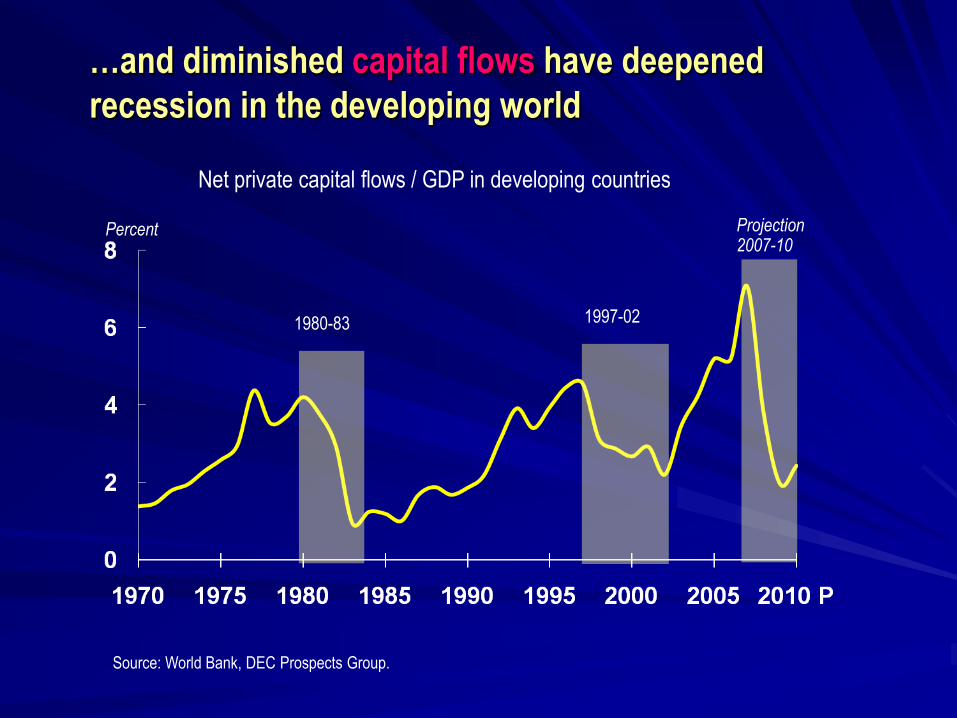

Terms of trade shocks will compound difficulties in

several countries…

Percent

1980-83 1997-02

Projection2007-10

Net private capital flows / GDP in developing countries

Source: World Bank, DEC Prospects Group.

…and diminished capital flows have deepened

recession in the developing world

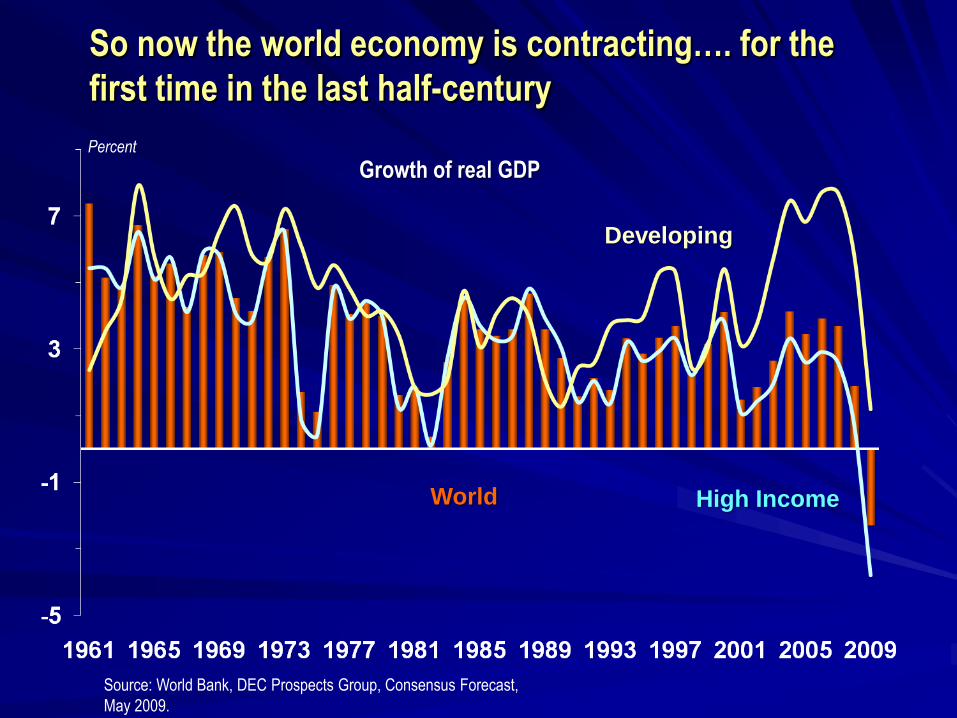

So now the world economy is contracting…. for the

first time in the last half-century

World High Income

Developing

Growth of real GDPPercent

Source: World Bank, DEC Prospects Group, Consensus Forecast,

May 2009.

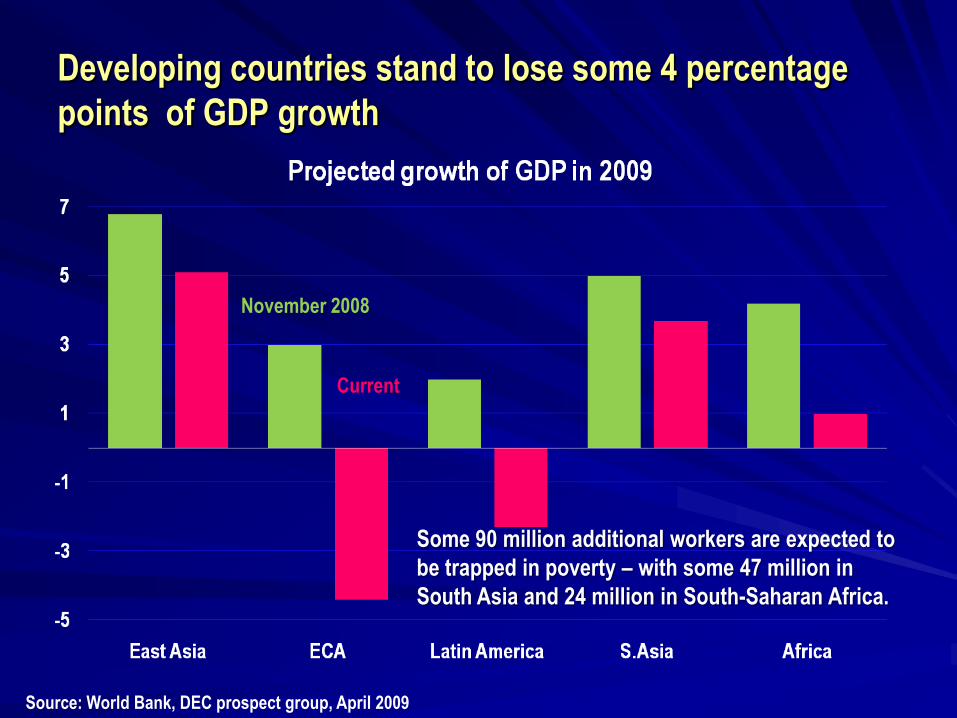

Developing countries stand to lose some 4 percentage

points of GDP growth

November 2008

Current

Source: World Bank, DEC prospect group, April 2009

Some 90 million additional workers are expected to

be trapped in poverty – with some 47 million in

South Asia and 24 million in South-Saharan Africa.

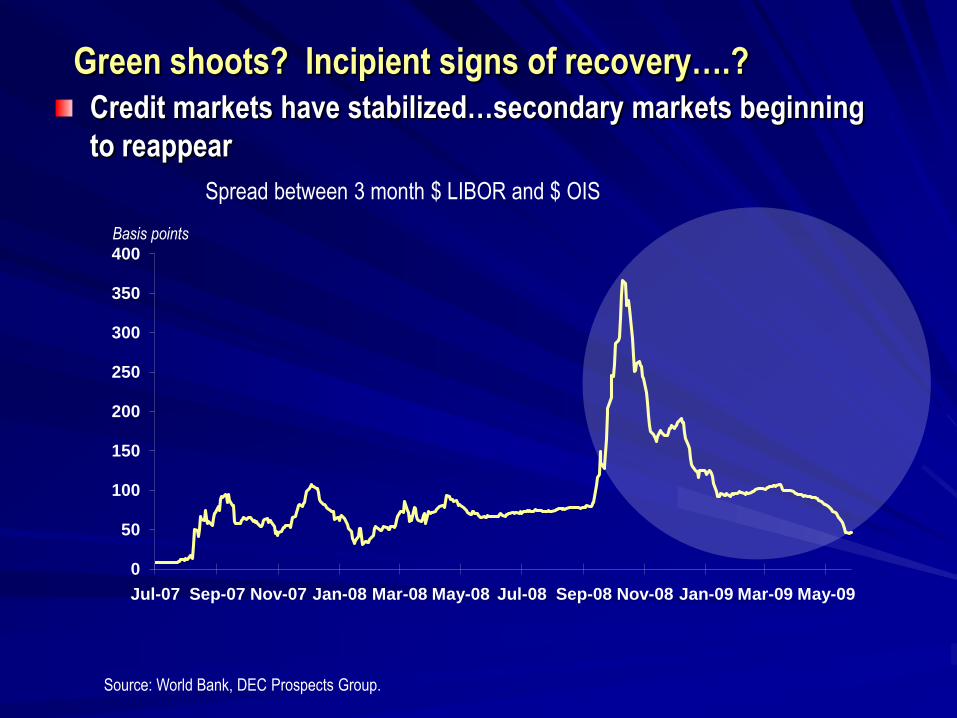

Credit markets have stabilized…secondary markets beginning

to reappear

Green shoots? Incipient signs of recovery….?

0

50

100

150

200

250

300

350

400

Jul-07 Sep-07 Nov-07 Jan-08 Mar-08 May-08 Jul-08 Sep-08 Nov-08 Jan-09 Mar-09 May-09

Spread between 3 month $ LIBOR and $ OIS

Source: World Bank, DEC Prospects Group.

Basis points

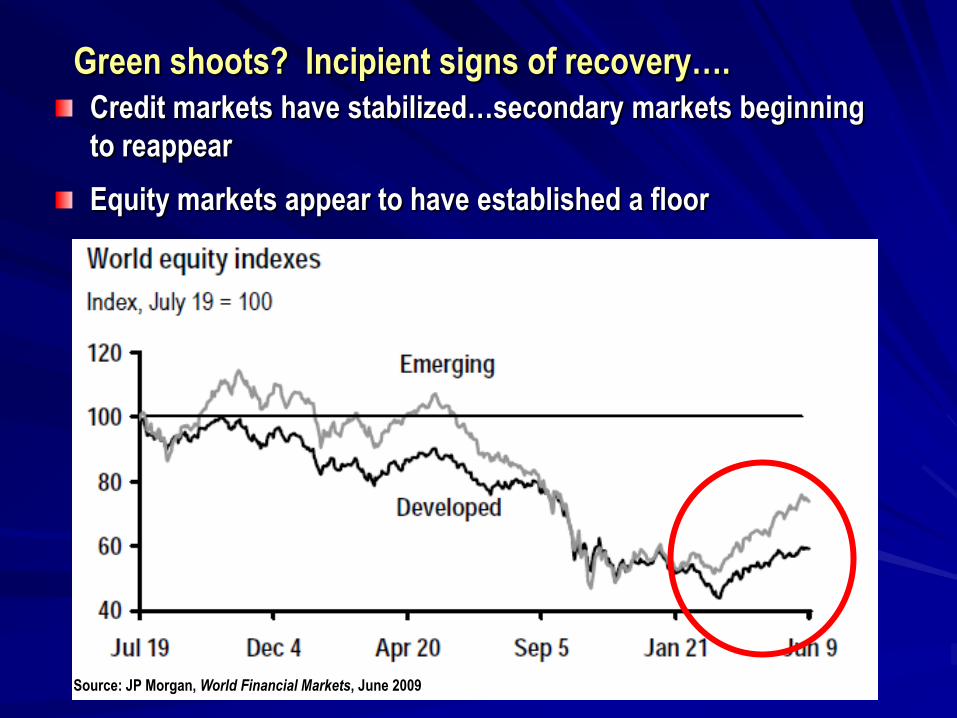

Credit markets have stabilized…secondary markets beginning

to reappear

Equity markets appear to have established a floor

Green shoots? Incipient signs of recovery….

Source: JP Morgan, World Financial Markets, June 2009

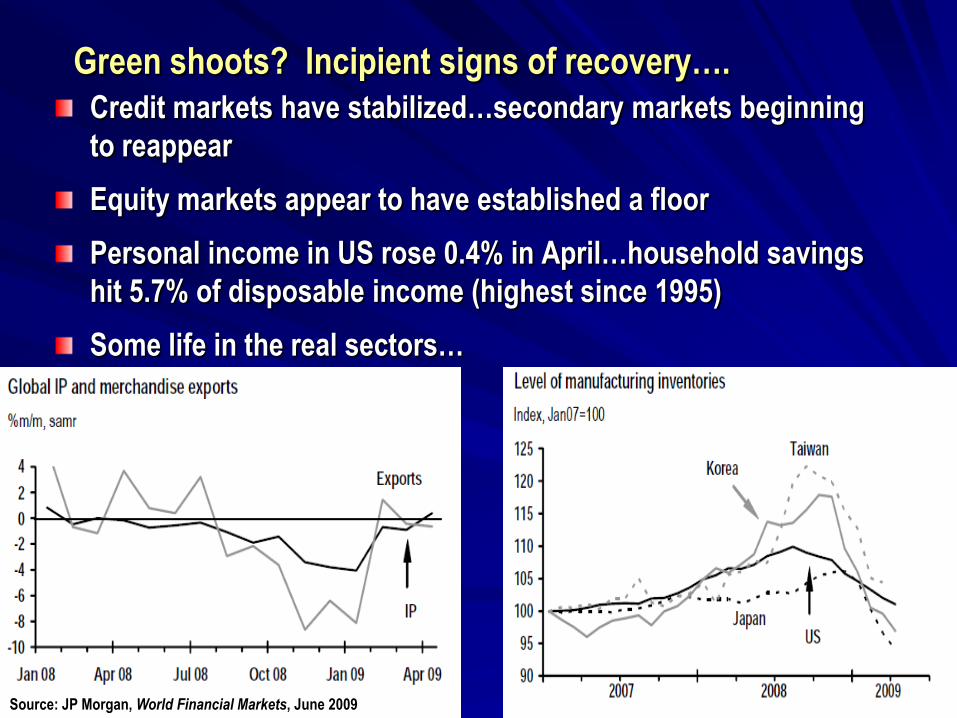

Credit markets have stabilized…secondary markets beginning

to reappear

Equity markets appear to have established a floor

Personal income in US rose 0.4% in April…household savings

hit 5.7% of disposable income (highest since 1995)

Some life in the real sectors…

Green shoots? Incipient signs of recovery….

Source: JP Morgan, World Financial Markets, June 2009

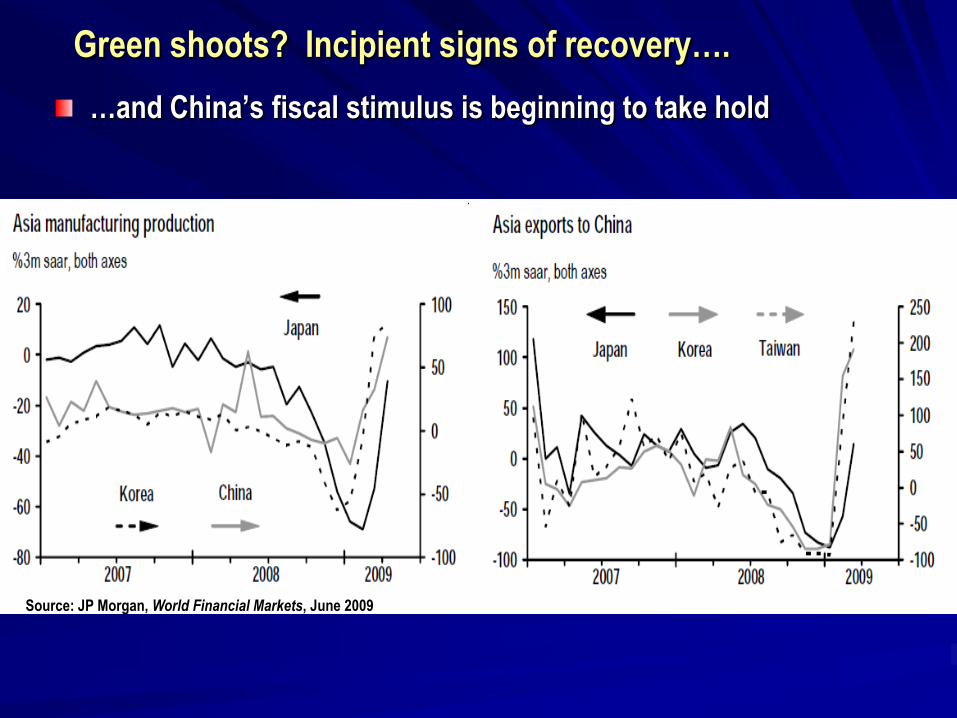

Green shoots? Incipient signs of recovery….

…and China’s fiscal stimulus is beginning to take hold

Source: JP Morgan, World Financial Markets, June 2009

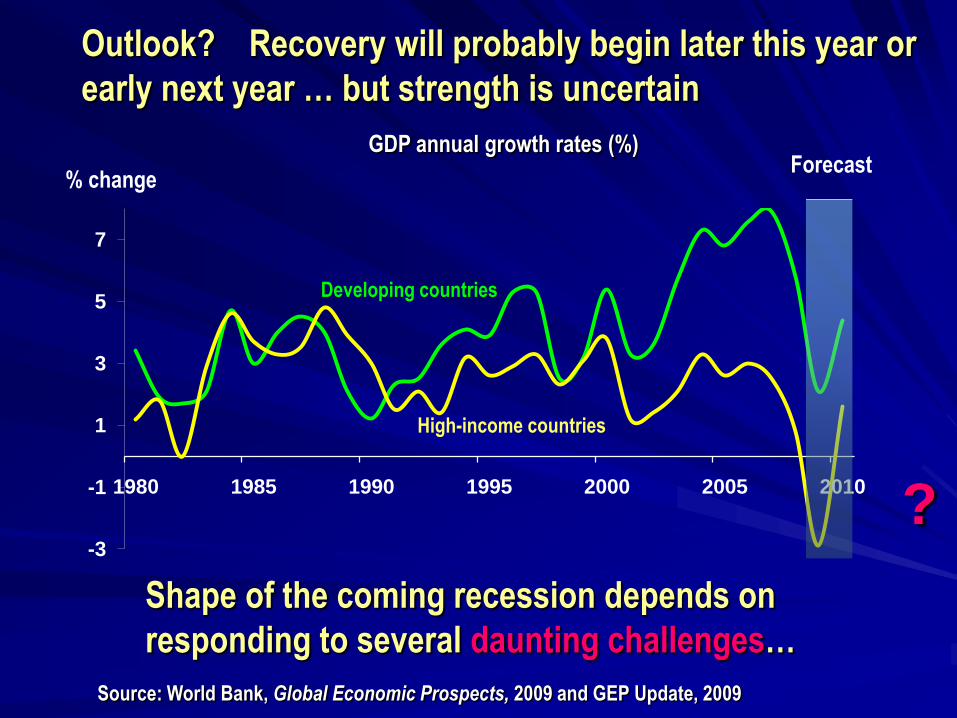

-3

-1

1

3

5

7

1980 1985 1990 1995 2000 2005 2010

Developing countries

High-income countries

GDP annual growth rates (%)Forecast

Shape of the coming recession depends on

responding to several daunting challenges…

Outlook? Recovery will probably begin later this year or

early next year … but strength is uncertain

% change

?

Source: World Bank, Global Economic Prospects, 2009 and GEP Update, 2009

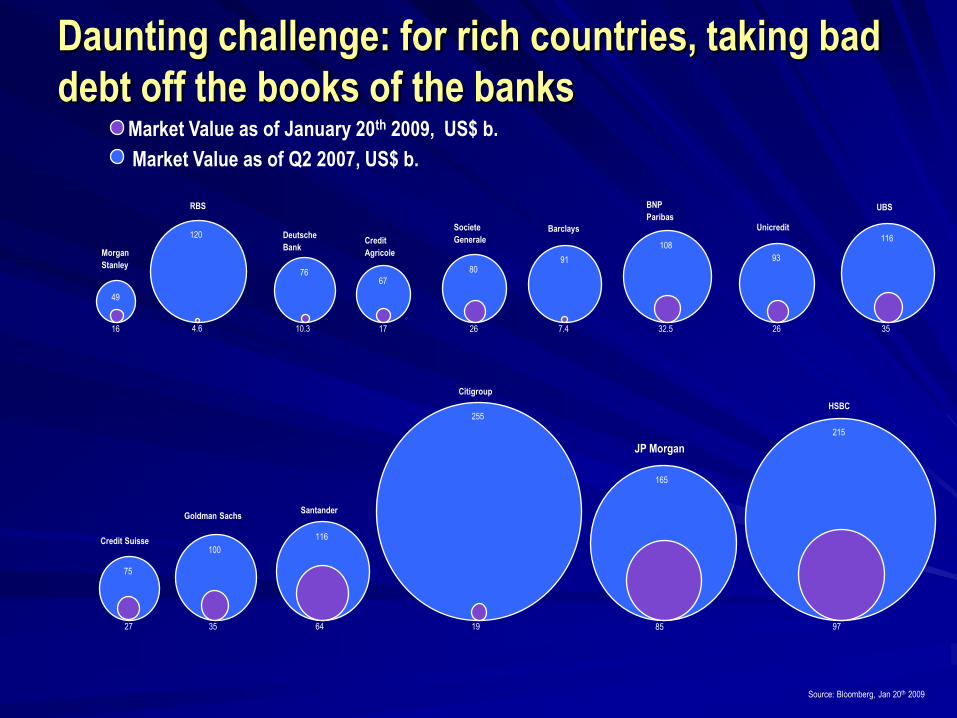

Daunting challenge: for rich countries, taking bad

debt off the books of the banks

Morgan

Stanley

RBS

Deutsche

BankCredit

Agricole

Societe

Generale

Barclays

BNP

ParibasUnicredit

UBS

Goldman SachsSantander

Citigroup

JP Morgan

HSBC

Market Value as of Q2 2007, US$ b.

Market Value as of January 20th 2009, US$ b.

Source: Bloomberg, Jan 20th 2009

Credit Suisse

49

120

7667

8091

108

93

116

75

100

116

255

165

215

16 4.6 10.3 17 26 7.4 32.5 26 35

27 35 64 19 85 97

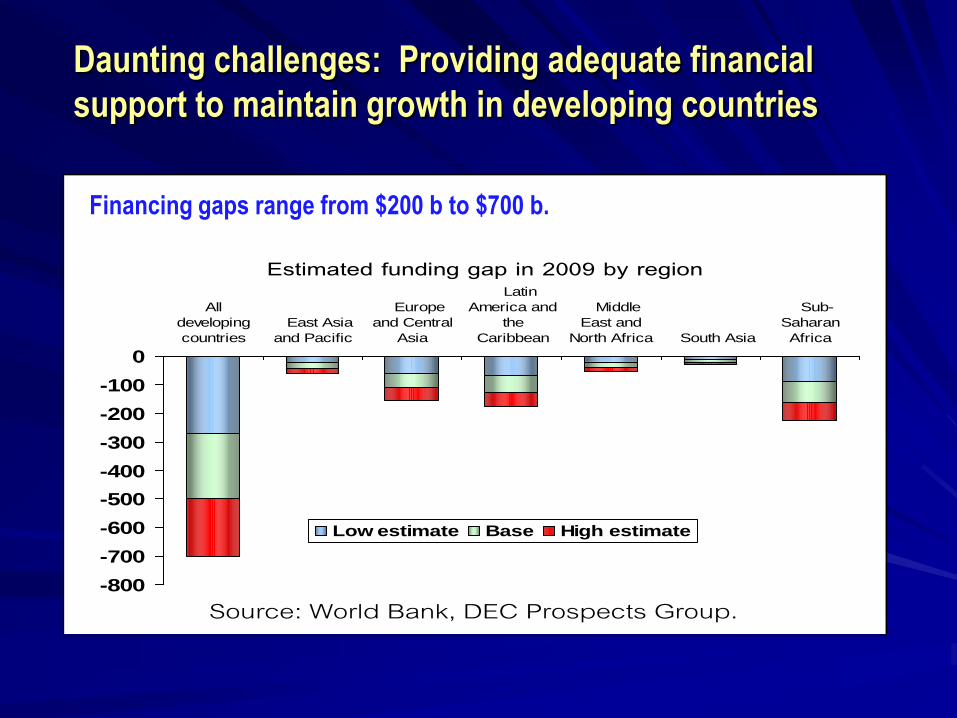

Daunting challenges: Providing adequate financial

support to maintain growth in developing countries

Figure 1.e: Credit crunch means developing

countries face significant funding gapsEstimated funding gap in 2009 by region

-800

-700

-600

-500

-400

-300

-200

-100

0

All

developing

countries

East Asia

and Pacific

Europe

and Central

Asia

Latin

America and

the

Caribbean

Middle

East and

North Africa South Asia

Sub-

Saharan

Africa

Low estimate Base High estimate

Source: World Bank, DEC Prospects Group.

Financing gaps range from $200 b to $700 b.

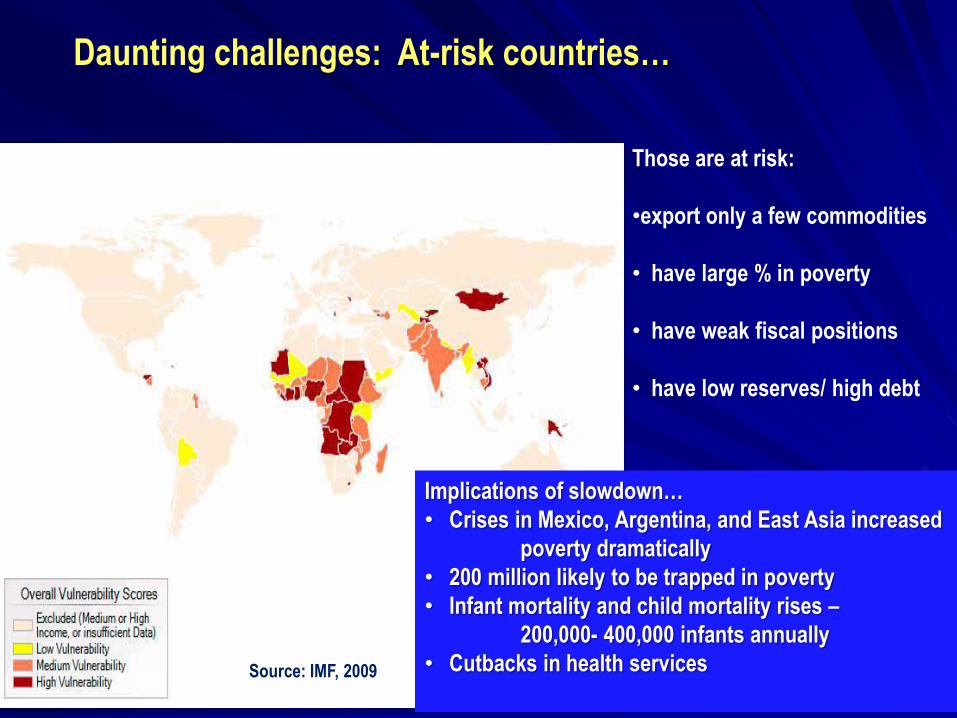

Daunting challenges: At-risk countries…

Those are at risk:

•export only a few commodities

• have large % in poverty

• have weak fiscal positions

• have low reserves/ high debt

Source: IMF, 2009

Implications of slowdown…

• Crises in Mexico, Argentina, and East Asia increased

poverty dramatically

• 200 million likely to be trapped in poverty

• Infant mortality and child mortality rises –

200,000- 400,000 infants annually

• Cutbacks in health services

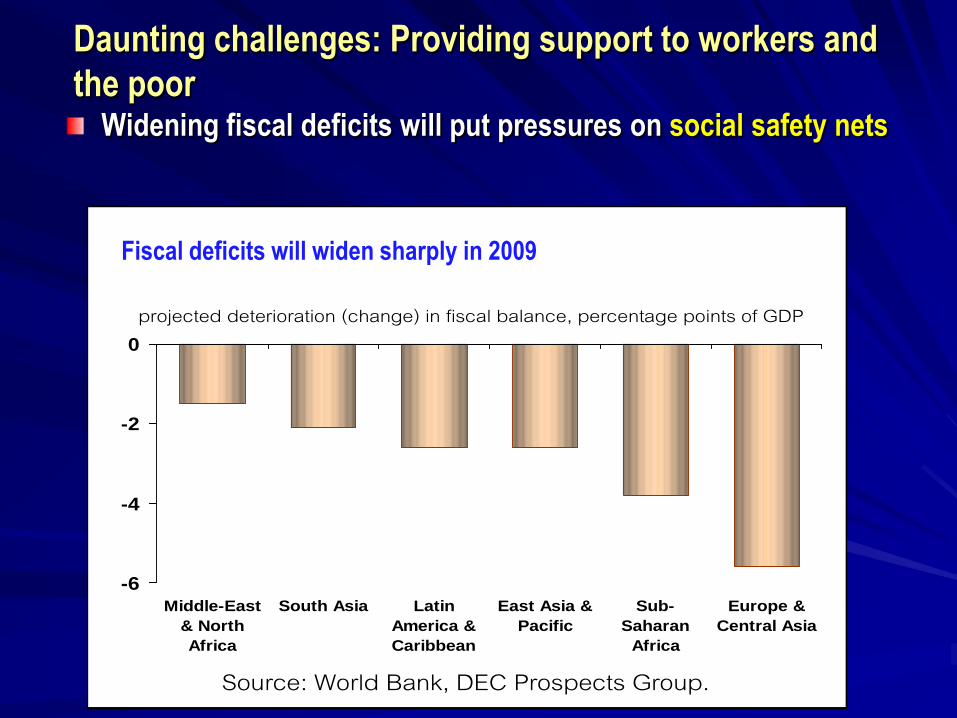

Daunting challenges: Providing support to workers and

the poorWidening fiscal deficits will put pressures on social safety nets

Figure 1.d: Weaker revenues will lead

fiscal deficits to widen sharply in 2009

-6

-4

-2

0

Middle-East

& North

Africa

South Asia Latin

America &

Caribbean

East Asia &

Pacific

Sub-

Saharan

Africa

Europe &

Central Asia

Source: World Bank, DEC Prospects Group.

projected deterioration (change) in fiscal balance, percentage points of GDP

Fiscal deficits will widen sharply in 2009

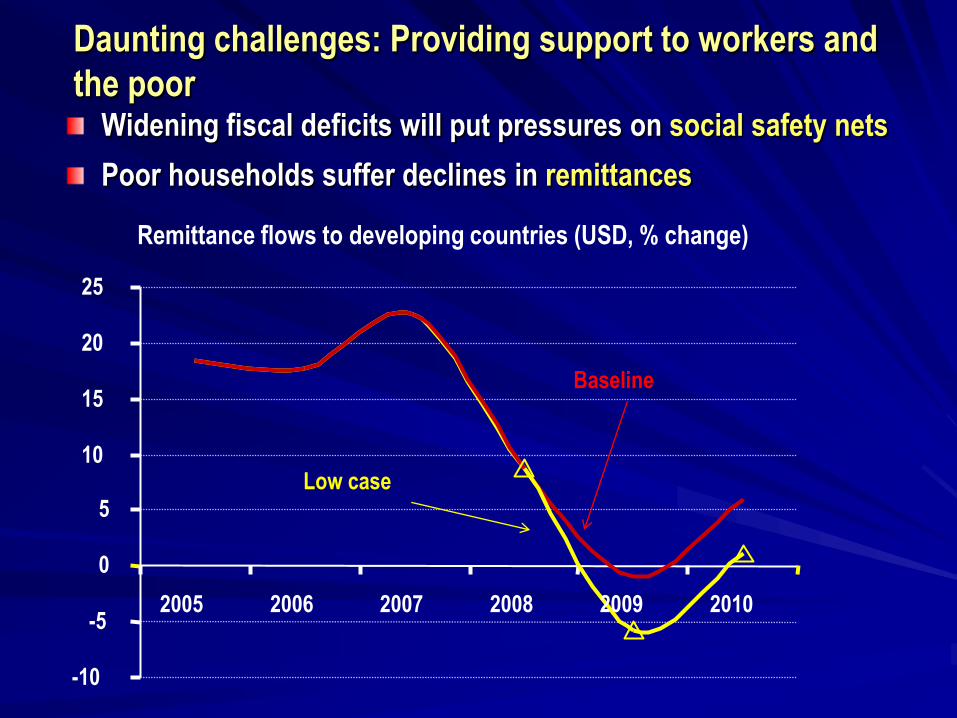

Daunting challenges: Providing support to workers and

the poorWidening fiscal deficits will put pressures on social safety nets

Poor households suffer declines in remittances

-10

-5

0

5

10

15

20

25

2005 2006 2007 2008 2009 2010

Baseline

Low case

Remittance flows to developing countries (USD, % change)

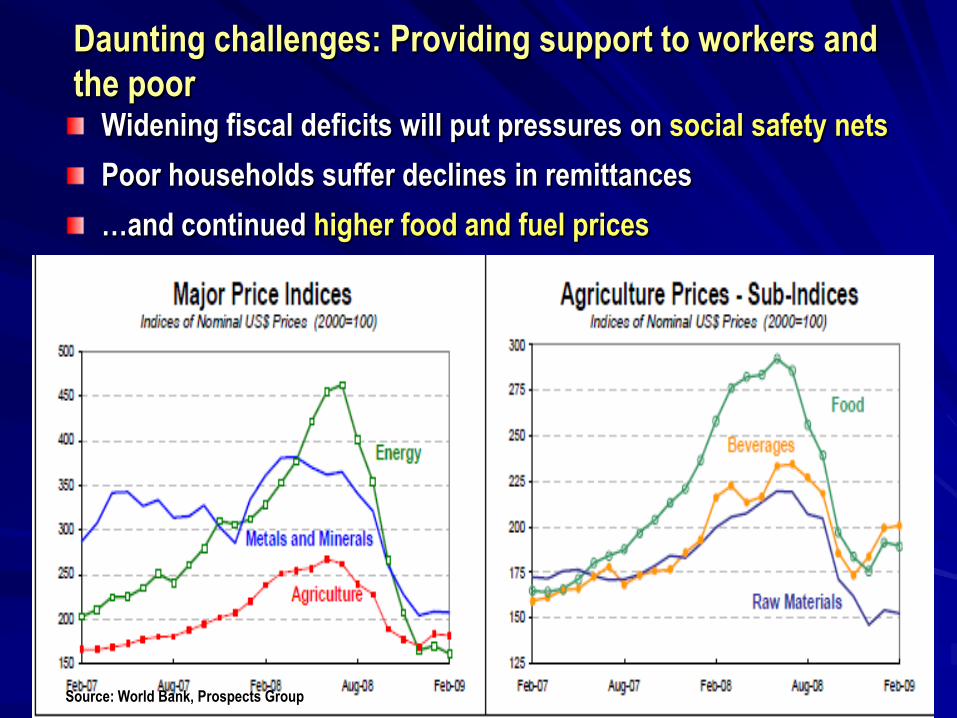

Daunting challenges: Providing support to workers and

the poorWidening fiscal deficits will put pressures on social safety nets

Poor households suffer declines in remittances

…and continued higher food and fuel prices

Source: World Bank, Prospects Group

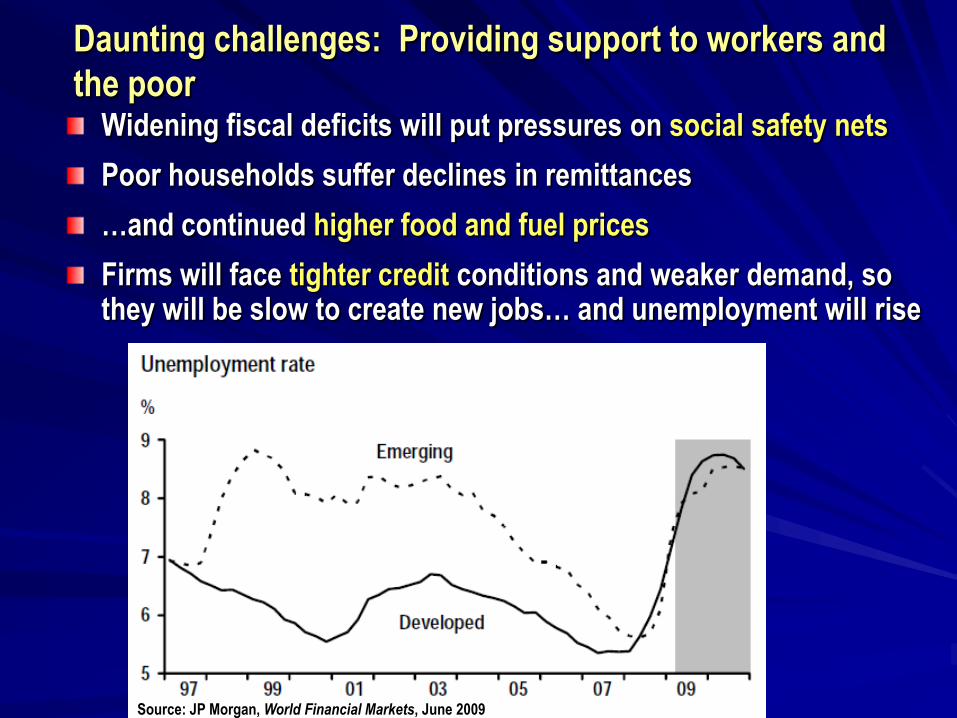

Daunting challenges: Providing support to workers and

the poorWidening fiscal deficits will put pressures on social safety nets

Poor households suffer declines in remittances

…and continued higher food and fuel prices

Firms will face tighter credit conditions and weaker demand, so they will be slow to create new jobs… and unemployment will rise

Source: JP Morgan, World Financial Markets, June 2009

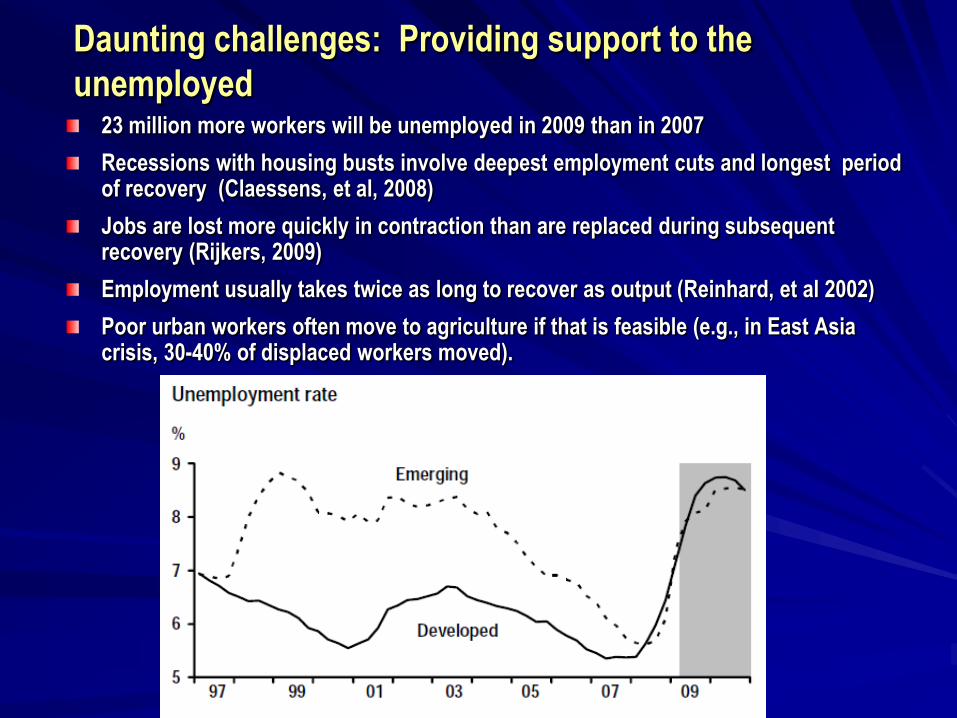

Daunting challenges: Providing support to the

unemployed 23 million more workers will be unemployed in 2009 than in 2007

Recessions with housing busts involve deepest employment cuts and longest period of recovery (Claessens, et al, 2008)

Jobs are lost more quickly in contraction than are replaced during subsequent recovery (Rijkers, 2009)

Employment usually takes twice as long to recover as output (Reinhard, et al 2002)

Poor urban workers often move to agriculture if that is feasible (e.g., in East Asia crisis, 30-40% of displaced workers moved).

Policy options? For developing countries…

Counter-cyclical policies: But only open to countries with access to noninflationary sources of finance and a sound investment climate

Since trade is a main channel of recession, policies to reduce trade costs can position countries to take advantage of recovery

– border and customs reforms

– port reforms

– improving logistics management

– Investment in labor-intensive and trade-related infrastructure, such as rural roads

Policy options? For developing countries…

Counter-cyclical policies: But only open to countries with access to noninflationary sources of finance and a sound investment climate

Since trade is a main channel of recession, policies to reduce trade costs can position countries to take advantage of recovery

Policies to support workers and the poor

– Increase in unemployment benefits

– Wage subsidies and lowering wage taxes

– Tariff reductions on food imports

– Public employment programs

– Conditional cash transfers programs (stay in school programs)

– Public investments in labor-intensive and trade-related infrastructure, such as rural roads

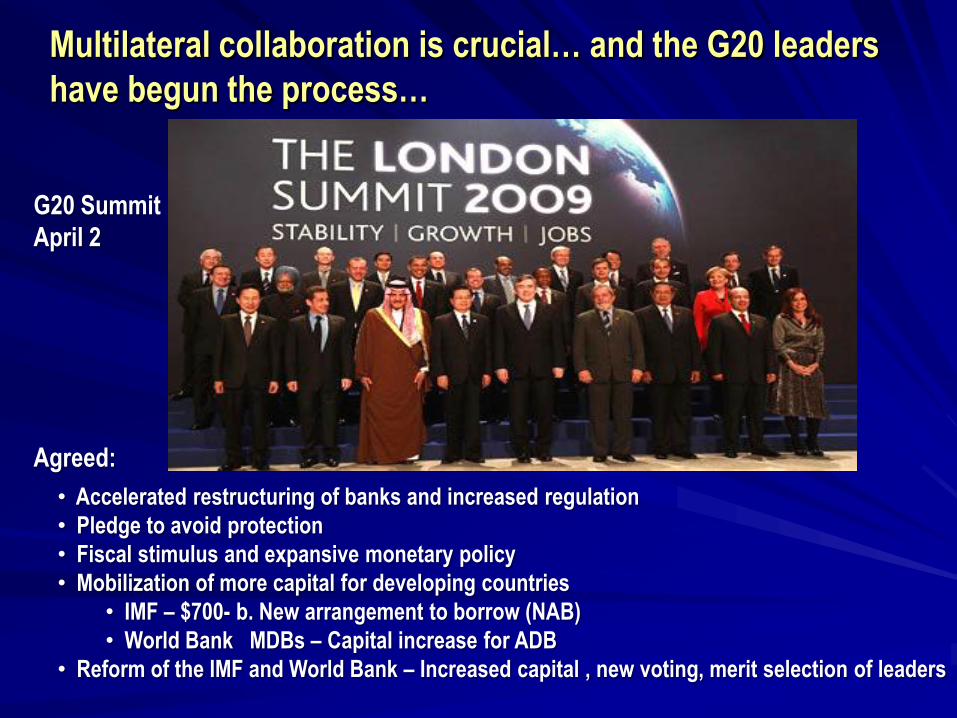

• Accelerated restructuring of banks and increased regulation

• Pledge to avoid protection

• Fiscal stimulus and expansive monetary policy

• Mobilization of more capital for developing countries

• IMF – $700- b. New arrangement to borrow (NAB)

• World Bank MDBs – Capital increase for ADB

• Reform of the IMF and World Bank – Increased capital , new voting, merit selection of leaders

Multilateral collaboration is crucial… and the G20 leaders

have begun the process…

G20 Summit

April 2

Agreed:

… but improving the multilateral response requires…

Fulfilling pledges for development assistance

Keeping global markets open and resisting pressures

for trade protection – and renewing a commitment to

the Doha Development agenda

Improving regulation of financial markets will require

careful balancing of national regulatory authorities

with international cooperation

Developing multilateral governance mechanisms to be

more inclusive

Conclusion…

Recovery is near, but its strength is in doubt and it will

take many quarters to have full effect on incomes

Meantime, assertive policy interventions are needed to

protect core social spending and support households

– and invest in reforms that will revive growth

The G20 process has helped but much remains to be

done – in keeping markets open, financial regulation,

and providing adequate development assistance

This presentation was prepared with inputs from Mansoor Dailami of DECPG , Pierella Paci of

PREM, and Margaret Grosh of HDN

Claessens, S. M. Kose, and M. Terrones (2008) “What Happens During Recessions,

Crunches and Busts” IMF Working Paper WP/08/274 December

Consensus Forecast, June 2009

International Monetary Fund (2009) “The Implications of the Global Financial Crisis

for Low-Income Countries” March

JP Morgan, various reports in October, 2008 – June 2009.

Lin, Justin “The Impact of the Financial Crisis on Developing Countries” Paper

presented at the Korean Development Institute, October 31.

OECD, Economic Outlook Interim Report March, 2009

World Bank, 2008 “Coping with New Strains in the Global Trading System: Doha Round,

Food Prices, and Aid for Trade” IMF - World Bank Staff Paper, September.

World Bank 2008, Global Economic Prospects, 2009, and Up-date March 2009 and

Global Development Finance, 2009 June 2009

Acknowledgements and Selected References

Financial Crisis and Global Recession:

At a Turning Point?

Richard Newfarmer

Special Representative to UN and WTO

World Bank

Cairo

June 15, 2009