FINAlternatives Hedge Fund

33

® Hedge Fund Technology & Trading 2009 sponsored by

description

Transcript of FINAlternatives Hedge Fund

®

Hedge Fund Technology & Trading

2009

sponsored by

Work Faster and Smarter

GENEVA®

Read a Case Study or Watch the Geneva Demo at www.advent.com/agilityRead a Case Study or Watch the Geneva® Demo at www.advent.com/agility

call us at 800 833.3626call us at 800 833.3626

Read a Case Study or Watch the GenevayRead a Case Study or Watch the GenevaRead a Case Study or Watch the Geneva® call us atcall us at call us at call us at

Power and Agility

Geneva® is the most powerful, full financial accounting and real time investment platform offering a unified data model that supports all instruments, all departments, and all offices across a firm.

Now, Geneva® delivers another advantage—an entirely new user interface and reporting platform for easier, faster access to critical information across the firm. Retrieving and acting on accurate, real time data has never been easier.

Traders can view up-to-the-minute positions; operations can drill down and correct trade breaks; accounting can work from a closed set of books; and management can analyze profit and loss at any level, from feeder fund to strategy to trader. Designed to handle ever-evolving strategies and instruments, Geneva® gives your firm the power and agility to never miss another opportunity.

FINalternatives 1 Hedge Fund Technology & Trading 2009

Inside This IssueOverview: The Changing Hedge Fund Landscape Shapes Demand For Technology 2

From CRM To Compliance: The Madoff Effect Drives Demand For A Data Trail 7

Risk Management: The Pros And Cons Of Building Your Own System 10

FINalternatives Survey: High-Frequency Trading Has a Bright Future 15

Need For Speed Drives Technology 15

Q&A: PerTrac Execs Say Hedge Funds Need to Step Up Transparency, Risk Management To Lure Investors 19

Hedge Funds Slash Overhead, Vendors Reap The Rewards 23

Hedge Fund Software & Technology Providers 27

Copyright 2009 by Stone Street Media, LLC. Copying or distributing without permission is prohibited. Please call +1.212.966.0047 to inquire about reprints and permissions.

FINalternatives 2 Hedge Fund Technology & Trading 2009

Last year’s major shakeout in the hedge fund industry—with roughly 20% of all funds clos-ing up shop—has radically altered its technol-ogy and risk management landscape. Those funds that did survive and the new ones just entering the market are scrambling to equip their operations with the best platforms to ap-pease both their investors and the regulators tightening the screws on them.

But after the recent market bloodbath, and the attendant disastrous returns and huge redemptions, building operations in-house, or even supporting existing technol-ogy, is sometimes no longer financially feasi-ble. Outsourcing, once taboo in hedge fund circles, has become a viable option for funds looking to scale down their in-house opera-tions, while at the same time improving risk management and transparency—the new buzz words in the hedge fund industry.

But the question of whether or not to outsource certain middle- and back-office functions is a big one, and there is no blanket answer. Matt Simon, an analyst at independent research firm Tabb Group, explains that a fund’s size, strategy and philosophy all contribute to whether or not a firm decides to utilize third-party vendors.

“One thing that hedge funds have learned over the years is that building technology can be time-consuming and is not their core business. They are there to manage mon-ey, not to build technology,” he says. “But, for some of these high-frequency/stat-arb-type players, the building of technology is

their core bread and butter. So, for those guys, the building of technology is some-thing that they are going to continue to do.”

Hedgies Split On StrategyIn fact, Simon, who has been studying the industry in preparation for a report due out in September, says that the hedge fund universe is increasingly breaking into two camps—the “Warren Buffet-style, buy-and-hold” camp, where managers study balance sheets and read sell-side reports, and the “trading” camp, where sophisticat-ed proprietary traders try to capture small profits from large volumes of trading.

“The traders don’t really care what the underlying names are; they are more inter-ested in being able to capture spreads and be able to profit from short-term blips in the market trading patters,” Simon says.

Addison Tsai, managing director at Old Greenwich, Conn.-based hedge fund shop SDS Capital Group, is seeing tremendous growth in this area first-hand.

“A lot of trading strategies are converg-ing to higher frequencies,” says Tsai.

And while the number of money man-agement firms utilizing so-called high-frequency trading strategies is miniscule compared to the overall universe of asset managers, according to Simon, those trad-ers are responsible for 73% of the equities trading volume on U.S. exchanges, and he expects them to consume an even bigger piece of the pie in the future. ►

The Changing Hedge Fund Landscape Shapes Demand For TechnologyBy Deirdre Brennan

FINalternatives 3 Hedge Fund Technology & Trading 2009

In Shift, Investors Hold The CardsOnce upon a time, an investor counted himself lucky to be able to gain access to a top-tier hedge fund. Managers such as SAC Capital Advisors’ Steve Cohen and Renaissance Technologies’ Jim Simmons could write the rules, imposing hefty mini-mum investment requirements, long lock-up periods and high performance fees, with smaller, less pedigreed managers following suit. Investors smiled and handed over their money, satisfied that they were getting the best possible returns on their investments.

Then, in 2008, the sky fell. Lehman Brothers collapsed, Bear Stearns went the way of the dodo, liquidity and credit dried up, arch-fraudsters Bernard Madoff and Marc Dreier revealed that supposedly sophisticated hedge funds and funds-of-hedge-funds were some of their biggest patsies, and hedge fund managers lost the biggest bargaining chip they had over their investors—solid returns.

“This fall was a key pivot point in the industry, where for a long time investors didn’t have a lot of power—hedge funds did things their way,” says Chris Momsen, senior vice president and general manager of global accounts at Advent, a financial software firm that specializes in portfolio management and accounting platforms for asset managers. “I think hedge funds had inappropriately structured their fees in re-gards to their investment strategy.” He ex-plains that managers who were investing in illiquid securities that became even more il-liquid were facing off against investors who wanted to redeem.

“Managers had to give them their mon-ey within 30 days or put up gates, which caused problems,” he says. “So what I

think you are going to see going forward is a better alignment between the time hori-zon of investors and the management style of the hedge fund.”

And how will this be achieved? Trans-parency.

“Some of that will be solved by look-through reporting, so the fund investors will see their underlying investments in the fund,” he says.

Transparency rules the roost in 2009. According to Tabb’s Simon, “transparency of positions, transparency of balances, transparency of pricing—anything to do with transparency,” is foremost on both in-vestors’ and managers’ minds.

One firm that has always insisted on full transparency is New York-based hedge fund incubator SkyBridge Capital. Co-founder and managing partner Anthony Scaramucci explains that all of the funds that his firm seeds must be completely transparent.

“We want to have an interface with a fund manager’s prime broker. It’s like a Reagan ‘trust but verify’ relationship,” he says. “What we do is have a feed from one of the software providers where everything gets uploaded into that system, and we have a global macro portfolio report that gets generated by that software.”

The data feed not only provides Sky-Bridge with piece of mind that everything is on the up and up and the trades are being cleared and reconciled correctly, but it also serves as a risk management tool. The system SkyBridge utilizes, GlobeOp Risk Services’ GoRisk, can be used for back testing and stress testing strategies, and also to independently confirm to investors that agreed investment style, risk profiles and limits are being adhered to. ►

FINalternatives 4 Hedge Fund Technology & Trading 2009

“It has proven to be a good way to sell these managers because when we go out to market them to institutions and high net-worth individuals, us being able to say that we have transparency and that we have a great, solid risk management team working alongside the manager adds credibility to the manager,” he says.

Transparency Is Key, But Accuracy Is KingWhile transparency is important, accuracy is critical. If managers don’t have proper data, all the analysis and transparency in the world won’t help them make good in-vestment decisions.

“The Advent view of the world is that everything is based on accurate account-ing information,” Momsen says. “If people have data in spreadsheets, and the infor-mation in someone’s hand is not accurate, then the firm can make erroneous deci-sions, and that can allow them to be un-dermargined or overmargined; it can cause trading errors.”

Rachel Minard, president of San Fran-cisco-based hedge fund Cogo Wolf Asset Management, agrees that the most impor-tant thing for her is to get accurate data so that her fund managers can make informed decisions.

“New technologies and the costs asso-ciated [with them] are not the biggest chal-lenge, but rather procuring the relevant in-formation to inform the investment team’s top-down views,” says Minard, whose firm employs a combination of both in-house and outsourced technology and software. “Almost all hedge fund data is historical. Constructing the appropriate optimiza-tion model and programming the relevant

stress tests to properly inform the portfo-lio manager’s macroeconomic views takes time and must be customized. It’s not the complexity of the technological screens that will impact an investor portfolio. It’s the hedge fund manager’s proper interpreta-tion of the information that far surmounts the aesthetics. All said, consistency and content outweigh all else.”

The Prime FocusIn the past year, the wisdom of the prov-erb warning not to keep one’s eggs in just one basket proved true once again. When Lehman’s basket had the table knocked out from under it, the hedge funds that used its prime brokerage services were left with egg on their face. The result? Hedge funds are now using more than one prime broker. This, of course, comes with its own set of operational issues.

“Most systems out there were either built by broker-dealers or bought by bro-ker-dealers. As a result, there was a lack of willingness to work with other broker-dealers,” says Bo Vastine, director of sales at Advanced Financial Applications, a tech-nology company that provides a platform to help traders manage their workflow in a multi-prime environment. “When you be-gan to see not just the large hedge funds, but the medium and small hedge funds moving toward a multi-prime scenario, the system that they may have been using for their single prime could no longer facilitate the workflow for their second prime. That meant a lot of manual processing, even cutting and pasting.”

Vastine says that what hedge funds are looking for is a system to tie these multiple primes together, with some important ►

FINalternatives 5 Hedge Fund Technology & Trading 2009

considerations to take into account, such as ease of use, ease of integration and connectivity.

“A system like ours that is agnostic al-lows them to generate those end-of-day files to multiple prime brokers and custodi-ans,” he says.

Advanced Financial Applications cur-rently works with 23 different prime bro-kers, and its open architecture allows it to be fully customized to the users’ needs.

Picking Your ProvidersWhile there are a multitude of factors for hedge funds to consider when selecting service providers, one long-time industry expert says that hedge funds aren’t, in fact, actively selecting their service providers, which can be a costly mistake.

“The due diligence that hedge funds do when picking their service providers is hor-rible,” says Jeffrey Rathgeber, co-founder of hedge fund consultancy Pelorus Advi-sors. “If you go to those meetings where hedge funds are picking a fund administra-tor or a prime broker, the [fund managers] let the prime broker run the show.”

He also says that hedge fund firms of-ten let pre-existing relationships influence which providers they use, even if that provider is not the best one for the given task. He points to a case where one of his former hedge fund clients traded bonds through Goldman Sachs and traded equi-ties through Lehman Brothers.

“The managing partners had their minds set on it because those were their existing relationships,” adding that at the time, “Goldman was the king of equities and Lehman was the king of fixed-income. They had it backwards.”

Rathgeber says that no matter what the software or type of technology a fund is thinking of using, the managers should make a list of exactly what they want or need from a system, and then give that list to the service provider well in advance of the presentation. That way, the service provider will have time to put together a presentation to show the manager exactly how the system or software can perform those stated tasks.

“If you look at a hedge fund, the amount of operational effort that is spent recreat-ing the world that they wanted all along but never really communicated effectively is staggering,” he says.

The Road Ahead Could Be RosyWhile some hedge fund investors may use the tough economic environment as an excuse to sit on the sidelines, some see a reason for optimism. In fact, according to one investor and manager, there may nev-er be a better time to make money.

“In an environment like this there has never been greater opportunity,” says Scaramucci, who will be rolling out the third SkyBridge fund of hedge funds later this summer. “First, there is a tremendous amount of talent still looking for homes in the musical chairs of Wall Street and hedge funds. Second, there is a shortage of capital. People are fearful to put money out. And third, you add to that distressed prices, and that sets up pretty well for good investment opportunities.”

But to profit from those opportunities, hedge fund managers need to adapt to the changing needs and requirements of in-vestors and regulators, as well as those of a changing marketplace.

© 2009 PerTrac Financial Solutions. All rights reserved.

Are you a professional investor looking to grow your portfolio? A fund manager look-ing to grow your asset base? An industry service provider looking to grow your bottom line?

We’ve grown.

We can help your business grow too.

Wherever your firm fits into the investment industry, the software and services available from PerTrac Financial Solutions can help you reach your goals. Since launching in 1996, we’ve grown from a small business with one product to an industry leader with a full suite of applications and thousands of clients around the world. Let us help your firm grow too.

PerTrac’s integrated suite of products gives our clients the tools to organize, analyze, under-stand, and act upon the information central to their businesses. The end results: maximized op-portunities, better decisions, and accelerated growth.

For an introduction to our major software ap-plications, keep reading. And to learn more about how PerTrac products can help your firm reach its growth potential, visit us online at pertrac.com.

• PerTrac Analytical Platform: the world’s leading in-vestment analysis and asset allocation software, with access to a wide range of investment databases, plus over 900 statistics and professional-quality reports

• PerTrac P-Card: a revolutionary new tool for distribut-ing and collecting performance numbers, portfolio infor-mation and other fund data

• PerTrac CMS: the alternative investment industry’s pre-miere workflow solution for investment management, capital raising, investor relations, and regulatory compli-ance

• PerTrac Portfolio Manager: the command center for your fund of funds or other multi-manager portfolio, cov-ering processes from due diligence to trade entry and cash management to risk assessment

FINalternatives 7 Hedge Fund Technology & Trading 2009

Bernard Madoff has gone up the river, un-likely to ever return. But the specter of his $65 billion Ponzi scheme continues to hang over the alternative investments industry.

For many investors, especially those of the all-important institutional variety, the only way to combat Madoff’s dark cloud is to shine a bright light on what have long been the more secretive corners of the industry. One-page monthly statements from hedge fund managers are no longer enough; their clients are demanding transparency, due diligence and risk management previously anathema to many in the industry. They want detailed reports on everything from how managers are selected and who their prime brokers are to how those managers reconcile their trades and balance their books.

“Since the Madoff scandal, we’ve been dealing with multi-billion dollar endowments and pension funds that are looking to auto-mate and create an [audit trail] around their research and diligence process,” says Jer-emy Bacon, a Goldman Sachs veteran and founder of Backstop Solutions, which offers customer relationship management, sales, marketing and accounting services. Chicago-based Backstop has a total of 185 custom-ers on its platform, 105 of them being hedge funds. Bacon says the firm has continued to grow, despite the recent trials and travails of the alternative investment industry.

“We’ve obviously had clients fold, but we’ve continued to add more clients than we’ve lost,” he says.

Erol Dusi of Imagineer Technology, which provides software and tools to help hedge funds and other investors run their businesses more efficiently, has also seen his firm benefit from growing demand for transparency. He says hedge funds that previously did not report their numbers to databases are now rushing to get their in-formation out.

“We’re seeing a tremendous [move-ment] in that direction, and it’s all a result of what has happened within the last six months,” he says.

Baseball fans spend countless hours debating a player’s “intangibles,” the things that don’t show up in box scores or statis-tics but that can be the difference between winning and losing. There is a similar focus today from investors—spooked, no doubt, by the shadiness of Madoff’s operations—on the things that don’t have a metric rep-resented by a letter of the Greek alphabet.

“The fact is, you’re investing in the man-agers’ ability to manage during tough mar-kets, and you’re investing in his integrity and personality,” Dusi says. “Those things are not going to be captured in returns. Rather, they are going to be calculated from your meetings with them and data from background checks.”

In fact, it is those intangible details that are often the deciding factor in whether a fund manager wins a mandate, according to one consultant from Cambridge Associ-ates, who asked not to be named. ►

From CRM To Compliance: The Madoff Effect Drives Demand For A Data TrailBy Hung Tran & Jonathan Shazar

FINalternatives 8 Hedge Fund Technology & Trading 2009

“I take detailed notes on every manager I meet, from whether they seem fidgety to what they order at lunch,” said the consul-tant. “If the guy I’m meeting with has whisky on his breath and bags under his eyes, you can bet that I’m not going to recommend him to my client, even if his numbers are out of the park.”

Specter Of Regulation Looms Large Fear of being taken in by the next Bernard Madoff is not the only factor driving the de-mand for a paper trail. New regulation of the alternative investment industry looming both in the U.S. and in Europe has man-agers rushing to anticipate what will be re-quired of them by authorities.

While it’s still unclear what form new regulations will take—that there will be new regulations is a certainty. It seems equally clear that new regulations will, at a mini-mum, force hedge fund and private equity managers to offer greater transparency and impose stricter compliance requirements.

Research and advisory firm Celent ex-pects that global information technology spending associated with governance, op-erational risk and compliance activities will increase from $1.4 billion in 2008 to $1.7 billion in 2011.

“There is now a ‘get big or get out’ theme at play,” says Cubillas Ding, a se-nior analyst at Celent. “Firms and vendors need to position themselves accordingly in terms of purchasing or developing solu-tions. Significant investments are required in an end-user market which is increasingly sophisticated in its demands.”

Ding’s colleague, Isabel Schauerte, concurs.

“Regulation is sure to place greater bur-dens on the middle- and back-office func-tions of hedge funds,” says Schauerte, a capital markets analyst at Celent. “Here, the last years have seen great progress in terms of technological sophistication. In many cases, funds have grown to a size and scope that forces managers to run their business more formally. This has spurred technology adoption rates.”

Schauerte also credits the increase in institutional investors’ allocations to hedge funds for the push to adopt better technology.

“The growth in assets from this breed of investors comes with requirements on operations and risk management that have forced hedge funds to embrace IT to a greater extent,” says Schauerte.

“Going forward, regulatory compliance is also going to be a greater issue for hedge fund administrators.”

But despite the inevitability of stricter regulation, many firms have not accorded improved compliance systems the priority they deserve, according to Bill Mulligan of New York-based HedgeOp Compliance, which provides compliance, operational and due diligence reporting to the alterna-tive investment industry.

“When we get involved, we make sure that there are not other priorities that are going to push compliance issues to the back of the line,” he says.

And according to Backstop Solutions’ Bacon, the time to prepare for the looming regulations is now.

“Each vendor out there has had to make sure that their systems can help to buoy the compliance and regulatory requirements as related to the products that they’re offer-ing,” he says.

FINalternatives 10 Hedge Fund Technology & Trading 2009

Necessary ToolsSince risk management is a quantitative discipline, the first step in developing risk management infrastructure is the develop-ment of a repository to house four types of data:

1. Holding and trade level data 2. Historical pricing data for securities trad-

ed by the fund3. Historical data for risk factors used in

various analyses 4. Results of risk management analyses

It’s been a long term practice in the financial services to use Microsoft Excel as a tool for both storing data and performing analysis. The growing complexity of financial products and the need to have robust systems make Excel spreadsheets a less than ideal envi-ronment to store data. To be truly reliable, the data used in risk management analysis should be housed in a relational database such as a MS SQL Server or Oracle.

Once the data repository is built, tools to analyze the data need to be put in place.

Risk Management: The Pros And Cons Of Building Your Own SystemBy Aleksey Matiychenko, Risk-AI, and Alexander Makeyenkov, DataArt

Risk Management is in vogue these days. The crisis of 2007-2008 has in many ways been blamed on the failure of risk managers to predict the stress that we have all now lived through. With global markets rebounding and hedge funds posting positive results, the discussions about improving risk management policies and systems are taking place at many hedge funds.

Effective risk management requires that the firms establish culture, policies and pro-cedures that are specific to their operating model. However, at its core risk manage-ment is a quantitative discipline that requires significant investment in data, systems and people. In this article we discuss what it takes to develop internal risk management architecture.

The exact set of tools depends on a hedge fund’s strategy, range of securities traded, liquidity and other factors. There are, how-ever, some tools that are likely to be used across all hedge funds.

● Value at Risk (VaR) – Perhaps no other tool received as much criticism and blame for the current crisis as VaR. While VaR has many well documented shortcom-ings, it’s likely to remain an important part of a risk manager’s toolbox. VaR provides risk managers (and their bosses) with a quick read of the hedge fund’s risks.

● Stress Tests – Scenario analysis based on either historical stress events or theo-retical scenarios can be used to comple-ment VaR analysis.

● Greeks – Various sensitivity measures such as Option Delta, Gamma and others provide important information about the fund’s exposure to different market factors.

● Factor Analysis – Factor analysis can be used to uncover potential hidden tilts in the fund’s portfolio. ►

FINalternatives 11 Hedge Fund Technology & Trading 2009

Risk management systems should be able to perform the above analysis and provide clear and consistent reporting mecha-nisms so the output of the analysis can be used by risk managers, traders and a fund’s investors. Build vs. BuyWhenever new systems need to be put in place, the usual question of build versus buy arises. There may be many factors that affect the ultimate decision to build or buy a system. Though price is often an important criterion, it should not be the deciding factor. There are many in-stances when a hedge fund should opt for a buy decision and avoid spending time and resources on internal development. The buy decision is usually justified when implementing systems that aren’t specific or critical to the hedge fund’s core strate-gy. Such systems usually include: contact management, accounting, trade capture and others.

The decision to buy or build a risk man-agement system depends on the complex-ity of the hedge fund’s strategy and the variety of products traded. Most commer-cially available systems may be sufficient to analyze a certain range of products. Few systems are able to produce meaningful analysis of a diversified and complex port-folio. Even fewer do it well.

If anything can be learned from the current crisis it is that risk management needs to be part of a core strategy of any investment firm. What this means is that risk management systems need to be part of the core strength of any hedge fund that wants to stand out. For such hedge funds, buying an off-the-shelf product may be a first step in

developing risk management architecture, but it shouldn’t be the only step.

Ultimately, all commercial packages are made to be able to satisfy the largest num-ber of customers. Some packages can be customized to each client’s needs, but the customization effort may be complex, limit-ed in scope and expensive. We have seen such implementation at a number of hedge funds. The usual architecture involves a vendor risk management package such as Risk Metrics, MeasureRisk or others. Any risk management system (vendor or in-house) needs to be integrated with trade capture, portfolio management, and back office systems.

Depending on the complexity of the fund’s portfolio, the vendor system may not be capable of handling certain instruments. In such situations, the solution may involve either building an internal system to handle these instruments or purchasing an addi-tional vendor system(s). We, in fact, have seen multi-strategy hedge funds purchase one system to handle equity products, a second system to handle fixed income, and a third system to handle exotic prod-ucts. Ultimately, all these systems need to work together.

While ensuring seamless dataflow and building custom reporting that integrates all the systems is a big task in itself, there is an even a bigger issue. At the end of the day, a risk manager needs to have a complete picture of portfolio exposures. Such a picture needs to incorporate cor-relations among various products that ex-ist in disparate systems. Building a tool to bring all these exposures together is akin to developing a complete risk system from scratch. ►

FINalternatives 12 Hedge Fund Technology & Trading 2009

For a fund that has decided to dedicate time and resources to develop its own risk man-agement system, the decision of whether to hire full-time personnel or to outsource the development needs to be made.

Developing a risk management sys-tem is not a trivial process and is likely to take significant time and money. Human resources required to implement such a project typically require at least two, and likely more, highly-skilled professionals with graduate or post-graduate degrees and extensive software skills. Even in the stressed employment markets that we are experiencing right now, such individuals carry an expensive price tag. Hiring sev-eral such individuals may not justify the value added by the development. Addi-

tionally, a proper enterprise-level devel-opment effort will require investment into project management, quality assurance and maintenance practices, all of which will call for extra hires. The solution to this may lie in outsourcing a significant part of such development to a firm specializing in such projects.

The in-house vs. outsource decision does not need to (and perhaps shouldn’t) be mutually exclusive. In order to extract the full benefit from the custom developed system, the fund should employ at least one of those highly-skilled risk profession-als capable of modifying and maintaining the system. Having an outside vendor per-form most of the development would en-sure faster implementation. ►

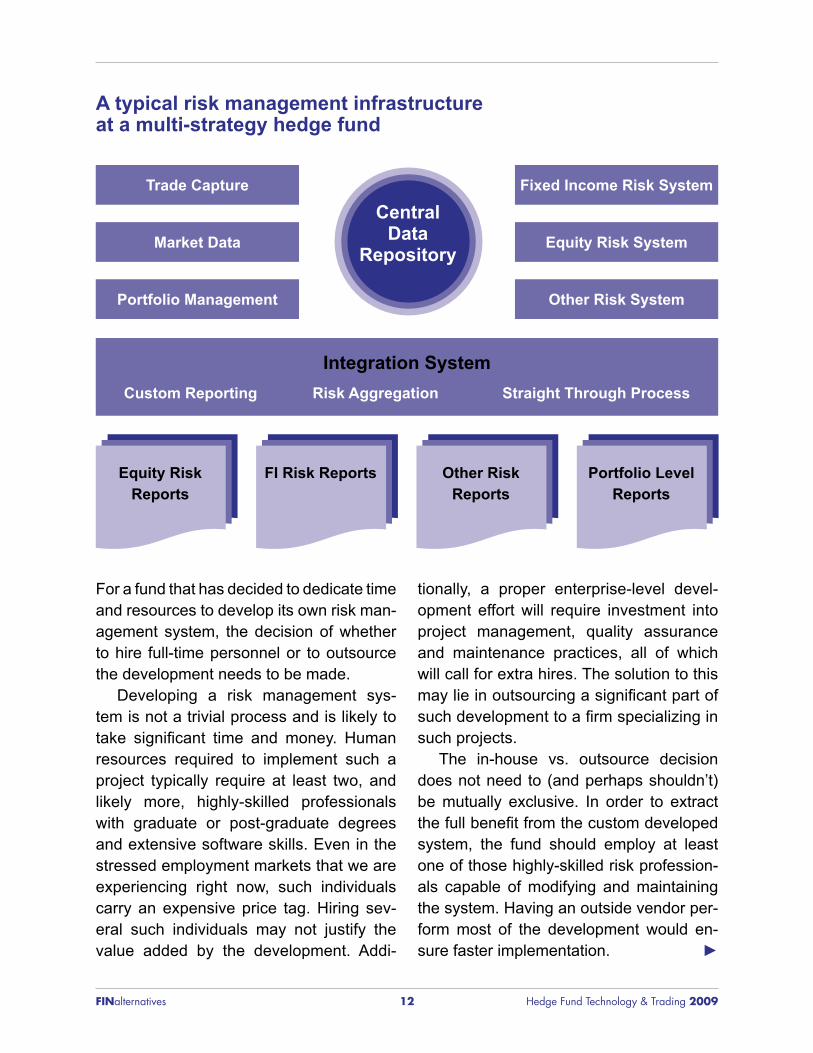

Central Data

Repository

Trade Capture

Integration SystemCustom Reporting Risk Aggregation Straight Through Process

Fixed Income Risk System

Market Data Equity Risk System

Portfolio Management Other Risk System

Equity Risk Reports

FI Risk Reports Other Risk Reports

Portfolio Level Reports

A typical risk management infrastructure at a multi-strategy hedge fund

FINalternatives 13 Hedge Fund Technology & Trading 2009

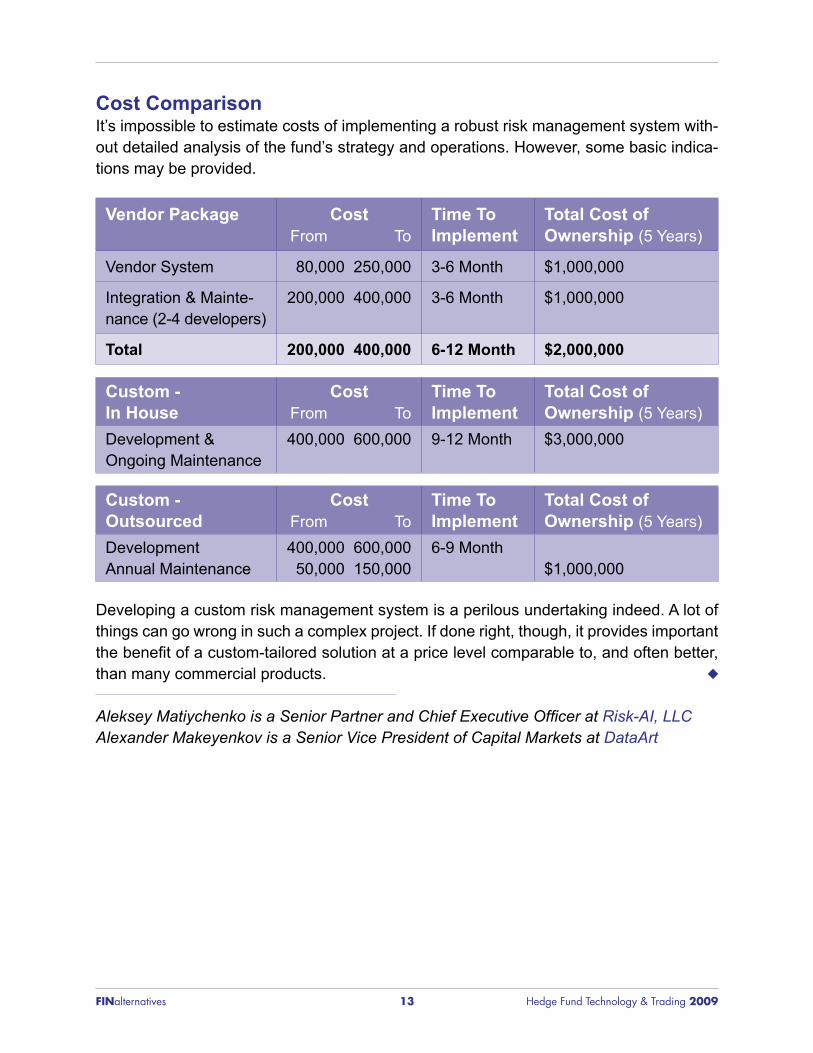

Cost ComparisonIt’s impossible to estimate costs of implementing a robust risk management system with-out detailed analysis of the fund’s strategy and operations. However, some basic indica-tions may be provided.

Vendor Package Cost From To

Time To Implement

Total Cost of Ownership (5 Years)

Vendor System 80,000 250,000 3-6 Month $1,000,000

Integration & Mainte-nance (2-4 developers)

200,000 400,000 3-6 Month $1,000,000

Total 200,000 400,000 6-12 Month $2,000,000

Custom - In House

Cost From To

Time To Implement

Total Cost of Ownership (5 Years)

Development & Ongoing Maintenance

400,000 600,000 9-12 Month $3,000,000

Custom - Outsourced

Cost From To

Time To Implement

Total Cost of Ownership (5 Years)

DevelopmentAnnual Maintenance

400,000 600,000 50,000 150,000

6-9 Month$1,000,000

Developing a custom risk management system is a perilous undertaking indeed. A lot of things can go wrong in such a complex project. If done right, though, it provides important the benefit of a custom-tailored solution at a price level comparable to, and often better, than many commercial products.

Aleksey Matiychenko is a Senior Partner and Chief Executive Officer at Risk-AI, LLCAlexander Makeyenkov is a Senior Vice President of Capital Markets at DataArt

IneffIcIent posItIon sIzIng Is the bIggest

rIsk funds take today.

Alpha Theory fixes the problem and provides

true risk management for fundamental investors.

ALPHA THEORY (212) 461-4757 | [email protected] | www.AlphaTheory.com

1. a blackjack player has 19, takes a hit and gets a 2 for 21. Was the decsion to take a hit a: a. Good decision b. Bad decision

2. a $20 stock has $15 in net cash and a volatility of 50%. the risk of this stock should be measured by:a. Downside potential - $15 net cash b. Volatility - $10 (based on 50% volatility

on $20 stock price)

3. Letting “winners run” should enhance portfolio returns: a. True b. False

4. you buy a house for $1 million that subsequently declines in value to $500,000. someone offers you $800,000 for the house. do you:a. Take the deal b. Pass

5. human instincts are well-designed for portfolio management:a. True b. False

6. risk-adjusted return should be the highest weighted factor in determining position size:a. True b. False

7. the best time to buy is when:a. Fear in the market is low b. Fear in the market is high

8. economic forecasts are an easy way to improve an investment thesis:a. True b. False

9. two stocks trading at $20 have the same potential upside to $40 and downside to $10. you have greater confidence in the upside being achieved for stock one. assuming all else equal you would:a. Have a greater exposure to Stock 1 b. Have equal exposure to both assets

10. Modern portfolio theory is the optimal method to manage a portfolio: a. True b. False

To find these answers visit Alpha Theory’s website at: www.AlphaTheory.com/quiz.

The Great Investor’s Mentality Quiz

do you have it?Take the quiz and remember that great investing is a mindset, not a skill-set. Unfortunately, mindsets are harder to change than skill-sets. But just like other great investors, you can put systems and discipline in place to help foster a culture with the “great investor” mentality.

FINalternatives 15 Hedge Fund Technology & Trading 2009

FINalternatives Survey: High-Frequency Trading Has a Bright Future By Irene Aldridge

High-frequency trading has grown expo-nentially in the past several years, and, according to the FINalternatives 2009 Technology and High-Frequency Trading Survey, that growth is here to stay.

A whopping 90% of respondents think that HFT has a bright future. In compari-son, only half believe that the investment management industry has favorable pros-pects, and only 42% have a positive out-look when it comes to the U.S. economy. Given that dose of pessimism, it should be noted that HFT tends to work particularly well in volatile range-bound markets like the current economic environment.

The optimism for HFT—which research firm Tabb Group estimates accounts for 73% of equities trading volume on U.S. exchanges—is bound to bring additional skill and capital to the high-frequency

arena. At present, many financial indus-try participants understand the business of HFT, yet few understand the details and implementation involved. Some 39% of hedge fund managers, investment ad-visers, executing brokers and proprietary traders have just “a little” understanding of the high-frequency business, accord-ing to the FINalternatives survey, with 52% reporting a solid understanding. By contrast, only 40% of the respondents report that they had a solid grip on the implementation of HFT, with 19% report-ing no understanding of implementation tactics whatsoever.

The outlook for HFT is largely driven by the high profitability potential of well imple-mented HFT systems. While traditional buy-side trading strategies hold positions for weeks or even months, HFT is

Need For Speed Drives Interest In TechnologyThere’s a major technology shift happening in the financial markets, one that isn’t go-ing unnoticed by the alternative investment industry.

New exchanges and electronic communication networks have come online, frag-menting the market and increasing the potential number of trades. All of these innova-tions require efficient data transmission: messaging involved in order transmission, confirmation of order placement and the like. Technology has enabled these changes, especially the efficiency and speed of execution, most notably, increasing the number of daily trades while simultaneously decreasing the average trade size.

Given the changes, it’s no surprise that over 60% of the respondents to the FINal-ternatives 2009 Technology and High-Frequency Trading Survey said their ability to execute electronic trades is “extremely important.” ►

►

FINalternatives 16 Hedge Fund Technology & Trading 2009

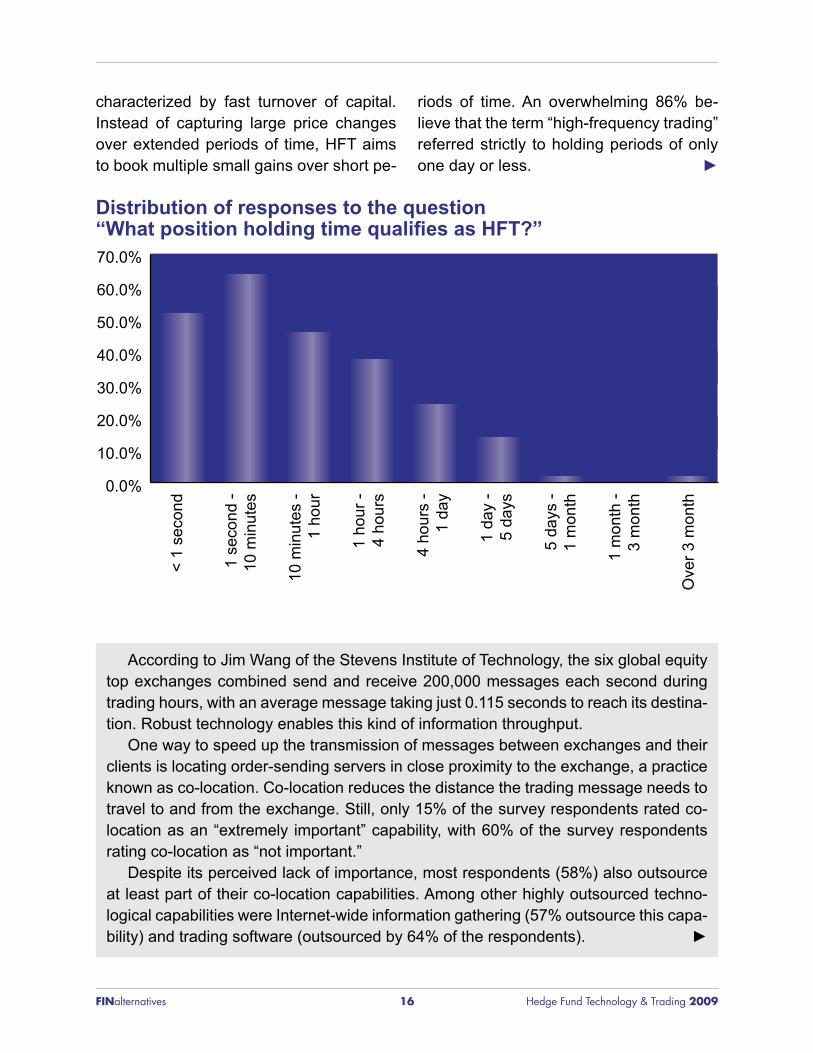

Distribution of responses to the question “What position holding time qualifies as HFT?”

Source: July 2009 FINalternatives Hedge Fund Technology & Trading Survey

characterized by fast turnover of capital. Instead of capturing large price changes over extended periods of time, HFT aims to book multiple small gains over short pe-

riods of time. An overwhelming 86% be-lieve that the term “high-frequency trading” referred strictly to holding periods of only one day or less. ►

< 1

seco

nd

1 se

cond

- 1

0 m

inut

es

10 m

inut

es -

1 h

our

1 ho

ur -

4 h

ours

4 ho

urs

- 1

day

1 da

y -

5 d

ays

5 da

ys -

1 m

onth

1 m

onth

- 3

mon

th

Ove

r 3 m

onth

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

According to Jim Wang of the Stevens Institute of Technology, the six global equity top exchanges combined send and receive 200,000 messages each second during trading hours, with an average message taking just 0.115 seconds to reach its destina-tion. Robust technology enables this kind of information throughput.

One way to speed up the transmission of messages between exchanges and their clients is locating order-sending servers in close proximity to the exchange, a practice known as co-location. Co-location reduces the distance the trading message needs to travel to and from the exchange. Still, only 15% of the survey respondents rated co-location as an “extremely important” capability, with 60% of the survey respondents rating co-location as “not important.”

Despite its perceived lack of importance, most respondents (58%) also outsource at least part of their co-location capabilities. Among other highly outsourced techno-logical capabilities were Internet-wide information gathering (57% outsource this capa-bility) and trading software (outsourced by 64% of the respondents). ►

FINalternatives 17 Hedge Fund Technology & Trading 2009

The two least-outsourced areas proved to be computer-aided number-crunching and computerized generation of trading signals: 62% and 58% of the survey participants, re-spectively, indicated that they prefer to perform these functions internally in their entirety. Other functions for which the participants showed strong preference to develop and run in-house were backtest engines and investment allocation modeling software.

Still, survey participants reported interest in buying selected off-the-shelf software. In particular, 55% of the respondents reported having bought electronic execution soft-ware and trading software; 50% noted buying Internet-wide information gathering soft-ware and real-time third-party research.

It seems that trading technology still has long ways to go to meet the rising interest and demand.

Intra-day position management is impor-tant for two reasons: savings from the over-night position carry costs and elimination of the overnight risk. The carry is the cost of holding a margined position through the night; it is usually computed on the margin portion of account holdings after the close of the North American trading sessions. Overnight carry charges can substantially cut into the trading bottom line in periods of tight lending or high interest rates.

Second, closing down positions at the end of each trading day also reduces the risk exposure from the passive overnight positions. Smaller risk exposure again re-sults in considerable risk-adjusted savings.

In addition to high capital turnover and intraday entry and exit of positions, the FINalternatives survey respondents further identified the following key distinctions of HFT: Trading decisions made upon tick-by-tick data analyses and Algorithmic trading.

Tick-by-tick data processing and high capital turnover do indeed define much of HFT. Identifying small changes in the quote stream sends rapid fire signals to open and close positions. The term “high-frequency”

itself refers to fast entry and exit of trad-ing positions, the process best executed by algorithms and dedicated computer pro-grams employing artificial intelligence.

Only 51% of the respondents report us-ing HFT at present, but 60% of the respon-dents indicate that they intend to use HFT in the future.

The FINalternatives survey garnered 202 responses, of which half worked for a hedge fund, 26% for an investment ad-visory or consulting firm, 12% for a fund of hedge funds, and smaller numbers for executing brokers, proprietary traders, mu-tual funds, research providers, technology firms and family offices. Some 59% said that portfolio management is their primary responsibility.

Irene Aldridge is an expert in algorithmic and high-frequency trading. Ms. Aldridge’s new book “High-Frequency Trading: A Practical Guide to Algorithmic Strategies and Trad-ing Systems” (Wiley Trading, ISBN: 978-0470563762) is available for pre-order on Amazon.com. Ms. Aldridge can be reached at [email protected].

MERIDIAN EQUITY PARTNERS is an independently owned Wall Street broker dealer with a global reach and a local feel. We provide customized, best-of-breed strategic solutions to the investment management community. Products include: equities, options, futures, fixed income and forex.

We make you feel like a BIG

fish in a small pond.

Our goals are simple:• Allow clients to operate on a variable cost basis, without sacrificing performance• Provide customized solutions that are creative, flexible and cost-effective• Develop client trust through consistent performance

5 Hanover Square, 21st Fl.New York, NY 10004

T: 212.500.6650 F: 212.742.2737 Member NYSE, FINRA, NFA & SIPC

Prime Brokerage Services• Start-Up Services• Administrative & Operational Support• Technology & Infrastructure Support• e-Trading Solutions & Outsourced Trading

Institutional Brokerage• Meridian ProTrade – Electronic Trading• NYSE Floor Operations• Sales & Trading

Analytics, Research & Corporate Access• Risk Management Advisory• Option Analytics• Technical Analysis• C-Level Corporate Access

Capital Placement & Advisory Services• Asset Gathering • Marketing & Consulting Services • Manager Due Diligence

FINalternatives 19 Hedge Fund Technology & Trading 2009

Q&A: PerTrac Execs Say Hedge Funds Need To Step Up Transparency, Risk Management To Lure Investors

When it comes to analytic and workflow solutions for investment profession-

als, PerTrac is the undisputed 800-pound gorilla of the asset management

industry. The firm boasts more than 2,000 clients in 50 countries, including

institutional investors, family offices, private banks, service providers and

money managers.

While the firm is best known in the hedge fund industry for its PerTrac

Analytical software, which tackles the quantitative side of investment man-

agement by helping money managers track and analyze investments, that is

only one spoke in the wheel. Two other software systems complete the firm’s

PerTrac suite: PerTrac CMS—which helps managers keep track of commu-

nications with their investors and service providers—and PerTrac Portfolio

Manager, which helps funds of funds and institutional investors manage in-

formation relevant to their portfolios.

And while growth in the money management industry has slowed, PerTrac

has continued to roll out innovate new products, such the snappy sounding

P-Card, which promises to help smooth communications between managers

and investors.

FINalternatives recently sat down with PerTrac’s president and CEO, Ger-

ald Mintz, and his colleague, managing director Meredith Jones, to discuss

how the hedge fund industry is changing, and more specifically, how new

pressures on the industry are forcing managers to increase transparency,

strengthen due diligence and invest in technology. ►

FINalternatives 20 Hedge Fund Technology & Trading 2009

How did last year’s tough market condi-tions and high-profile scandals affect the alternative investment industry?

Mintz: The industry has really gone through a severe shock—some people have fallen out and other people will likely still fall out. I would say that all of the trends in the indus-try argue toward people having more au-tomated, third-party systems. There’s less confidence in a marketing report that is produced by a manager’s own Excel tem-plate and own calculations than one pro-duced by something like PerTrac that has a known name. There is a strong desire for people to have tools to track and document due diligence.

Also, traditionally managers were reluc-tant to share informa-tion with investors, but investors are now de-manding that they get more information about the underlying risk. In-vestors want things like sector exposure or strategy exposure or re-gional exposure, and they want to be able to aggregate that information and make decisions.

Liquidity mismatches are also a big deal for people—making sure that the promised liquidity of, say, a fund-of-funds product actually matches the liquidity of the underlying investments. For example, if an institutional investor is co-mingled in a fund with high net-worth investors, that may not be such a great thing. Some of the high net-worth investors may want to cash out and that would force redemp-tions, while the institutions might say,

‘Don’t redeem; hold on.’ So, I think all of those shifts are going to cause people to want to track each of those things more carefully going forward.

What changes are happening in the indus-try now, and how are they driving demand for technology?

Jones: I’ve been in the industry since be-fore Long-Term Capital Management blew up, and I’ve watched the progression of how the industry has matured following each cri-sis. After LTCM, after the tech wreck, and now, clearly, after the market meltdown and Bernie Madoff, there’s been a period of

rapid maturation in the markets and in the alternatives space. What we’re beginning to see right now is an accelerated process focusing on transparency. You can’t see a survey these days where they don’t rank transparency and risk-management right behind performance, whereas before, per-formance was far and away the most im-portant thing that investors were looking for.

How is the looming potential for increased regulation affecting funds?

Jones: In terms of internal systems, cer-tainly regulation could have a large ►

“You can’t see a survey these days where they don’t rank transparency andrisk-management right behind performance.”

FINalternatives 21 Hedge Fund Technology & Trading 2009

impact on that as well. What’s required by various governments will drive to a large extent how the industry has to evolve with respect to technology. The way they do business, who they talk to, who they don’t talk to; all of those kinds of things. A lot of things are up in the air right now. Clearly, with the whole regulation issue, there have been some proposals on the table, but nothing concrete. I think all of those things are going to push toward transparency as well. We’re moving further down the trans-parency line and we’re also moving toward daily and weekly estimates so that people have a better view as to what’s going on in their portfolio.

Are you seeing any new hedge fund launches?

Jones: I did a prime broker event and, of the 25 groups that were there, four of them were new funds that were just start-ing out. But they’re taking a more cau-tious approach, and they’re also taking the time to get some systems in place. It’s not just two guys in a townhouse running a fund anymore. We’re probably looking toward the late third or fourth quarter for the number of new funds to starting ramp-ing up again.

Mintz: I think what Meredith said that is a really important point to emphasize is that barriers to entry are higher because inves-

tors are looking for proper risk systems and transparency, at least in terms of where the assets are, and making sure you’re not de-pendent on one prime broker.

The Lehman situation certainly scared a lot of people with the assets kind of held in limbo. And then on the fund of funds side, people are looking to see what’s your val-ue-add. If it’s due diligence, prove to me that you have a really rigorous due dili-gence process and systems around that. If it’s portfolio construction, show me that you’ve got a good handle on risk and you can give me a portfolio that’s going to per-form well and not give me as much kind of a dispersion that I might get if I just picked a set of funds.

So, in each case, managers are going to have to put in systems and procedures to show investors that it’s worth invest-ing in them. That, of course, will raise the cost of a launch. So, it argues that funds have to be a little bit larger to be able to afford those kinds of systems. I think the bar has been raised for what you need to run a fund.

What is the future of the industry?

Mintz: I think you’ll see more outside ad-ministration, and I think more focus on custody of the assets. We may see more in managed accounts, which is one way to address some of the custody and li-quidity issues.

When every millisecond counts, you can count

on this book.

Written by industry expert Irene Aldridge, High-Frequency Trading offers innovative insights into this dynamic discipline. Covering all aspects of high-frequency trading—from the formulation of ideas and the development of trading systems to application of capital and subsequent performance evaluation—this reliable resource will put you in a better position to excel in today’s turbulent markets.

Pre order your copy TODAY!Available January 2010.

FINalternatives 23 Hedge Fund Technology & Trading 2009

Hedge Funds Slash Overhead, Vendors Reap The Rewards By Hung Tran

As assets under management dwindle and performance fees fall, hedge funds are in-creasingly looking for ways to cut costs. But choosing whether or not to outsource certain operations—especially those that have traditionally been done in-house, such as risk management—is a big deci-sion. Managers must not only look at the potential cost savings, but must also con-sider the quality, reliability and security of their vendors. Despite the caveats, hedge funds are increasingly taking the leap.

“It used to be a black mark to have out-side risk managers,” says Kenneth Grant, who has served as head of risk manage-ment for some of the world’s most promi-nent hedge funds, including SAC Capi-tal Advisors, Tudor Investment Corp. and Cheyne Capital. In 2005, Grant set up his own shop, but he didn’t go the hedge fund route. Instead, he opted to focus on what he knows best—creating customized risk management reports for hedge funds.

His firm, Risk Resources, employs 20 people and works 24 hours a day analyzing everything from volatility and portfolio expo-sures to value at risk and scenario analysis. While Grant says there are many firms that provide some sort of risk management ser-vices software, it is the qualitative side of the analysis that is often lacking.

“Managers need someone to interpret all the data that they are given and tell them what it means,” he says. “It isn’t enough to just crunch the numbers.”

Jayesh Punater, founder of New York-based Gravitas Technology, which special-izes in providing technology and software integration services to the alternative in-vestment community, says he is seeing a surge in hedge fund firms choosing to out-source in order to save money and stream-line operations.

“This is the era of hedge fund 3.0,” Pu-nater says. “These hedge funds are smart-er, rather than larger. They’re reducing overhead by using outsourced data cen-ters and their focus has shifted from invest-ing to running a real business.”

Punater says that pressure from inves-tors and regulators is forcing hedge funds to expand their definition of risk, and hence, to find ways to manage it.

“No longer are firms just focused on P&L and trading risks; now they’re focus-ing on regulatory risks and the needs of investors,” he says. “What we’re seeing is increased demand for customized risk dashboards.”

Outsourcing the IT GuyAnother way hedge funds are reducing costs is by cutting personnel. Whereas funds once flush with cash could afford a full-time information technology staff, tough times call for tougher decisions.

“We recently saw a fund that was $6 bil-lion before 2008,” says Alexander Kouper-man, president of InfoHedge, a four-year-old technology firm. “We met with ►

FINalternatives 24 Hedge Fund Technology & Trading 2009

the CFO and the chief technology officer, and the CFO pointed a finger at the CTO and said, ‘This guy is my old friend and our wives are friends, but I have to fire him now because we don’t have the money to pay his salary.’”

Kouperman says his InfoHedge, which counts more than 90 hedge funds among its clients, is seeing a boom in demand, es-pecially from firms that are being forced to downsize their operations due to decreas-ing assets under management.

“The outsourcing space is definitely in good shape, given what is currently hap-pening in the market,” he says.

Warren Finkel, president of Network Doctor, which special-izes in providing IT ser-vices to the financial community, says he, too, is seeing an in-crease in business from the hedge fund sector.

“We are seeing a strong move towards complete managed ser-vice offerings where IT consultants are being hired to handle all technology and not just relying on break/fix work,” Finkel says. “This allows the hedge fund owners to plan their spending and also allows them to focus their efforts on managing funds rather than worrying about day-to-day IT problems.”

He adds that another advantage of us-ing an outside IT provider is that “a man-aged service provider can offer 24/7 sup-port, monitoring and maintenance and provide technicians who are certified and proficient in each technology includ-ing networking, phones and computers.

A managed service provider also has the knowledge of the technology options and possibilities since they provide support to multiple businesses and are able to bring this value to the fund.”

Protecting The Secret SauceBut not all hedge fund executives are sold on the prospects of outsourcing every-thing but the trading to vendors. Brian Kim, founder of New York-based hedge fund Liquid Capital Management, says outside technology is a double-edged sword.

“If everybody was buying the same risk management platform, frankly, I don’t feel like it could be any good,” he says.

“If [third-party vendors] were so good at managing risk, then they should be doing my job.”

Dmitri Sogoloff, founder of New York-based Horton Point, a quantitative hedge fund, echoes Kim’s sentiments. Sogoloff, whose firm uses InfoHedge’s technology, says while he’s satisfied with the vendor’s capabilities, there are just some functions that hedge funds should not outsource.

“We’re a technology-heavy shop and we have a lot of stuff that we develop in-house,” he said. ►

“These hedge funds are smarter, rather than larger. They’re reducing overhead by using outsourced data centers and their focus has shifted from investing to running a real business.”

FINalternatives 25 Hedge Fund Technology & Trading 2009

Indeed, despite the growing clamor for outsourcing solutions, Kim says ven-dors have more work to do. He has been searching for a way to ease the burden of labor-intensive back-office functions, but has found the solutions available wanting.

“Back-office and mid-office support is something I feel is a little lacking in the indus-try,” he said. “Everybody wants to sell you the latest trade management and execution platforms, but if I could get some more help in the back office, that would alleviate my burden from an administrative standpoint.”

The Nuts & Bolts: Servers, Hardware, Telephones & IT ExpertsWhile some hedge funds—especially those dealing in high-frequency trading strategies like Horton Point—may be loath to use outside risk management systems, many of those same hedge funds prefer to employ third-party hardware vendors to manage servers, telephones, data recov-ery systems and the like.

In fact, Horton’s Point’s Sogoloff says he is comfortable with outsourcing the

generic infrastructure that every hedge fund firm must have, such as computer hardware and backup services that pro-vide business continuity in case of a di-saster.

“We don’t need to spend the time or the money internally to do this,” he says.

New York-based technology provider Richard Fleischman Associates is benefit-ing from clients like Sogoloff—who in es-sence use a combination of in-house and outsourced technology. The firm boasts more than 400 hedge funds, private equity firms and broker/dealers as clients and is growing at a rapid clip.

“We probably do about 100 startups a year, and one of the things we’ve seen, post-Madoff, is a spread of outsource and in-source solutions, whether it’s with equip-ment offsite or with in-house facilities,” firm founder and namesake Richard Fleis-chman said. “For folks starting new busi-nesses, there is a lot of trepidation about building new offices, and they come to us for hosted solutions where they can get off the ground pretty quickly with minimum out-of-pocket expense.”

Fast access to real-time accurate research is crucial to making timely and informed investment decisions. Tamale RMS® brings together all of your research on a central platform configured to support your unique investment process. Tamale pioneered the field of Research Management Solutions with a simple-to-use software application that helps investment professionals manage and process the firehose of research information, more effectively. Tamale RMS makes it easy to capture, store, find and share your research. Nearly 2,000 front office professionals rely on Tamale RMS® to manage their research workflow. Now you can manage more ideas and make better investment decisions.

TAMALE

RMS®

See what a little pepper can do for your research process.

Read a Case Study or Watch a Product Demo at www.advent.com/tamaleRead a Case Study or Watch a Product Demo at www.advent.com/tamale

call us at 800 833.3626call us at 800 833.3626

Read a Case Study or Watch a Productd / l

Read a Case Study or Watch a Product Read a Case Study or Watch a Product Read a Case Study or Watch a Product call us at call us at call us at call us at

FINalternatives 27 Hedge Fund Technology & Trading 2009

Hedge Fund Software & Technology Providers

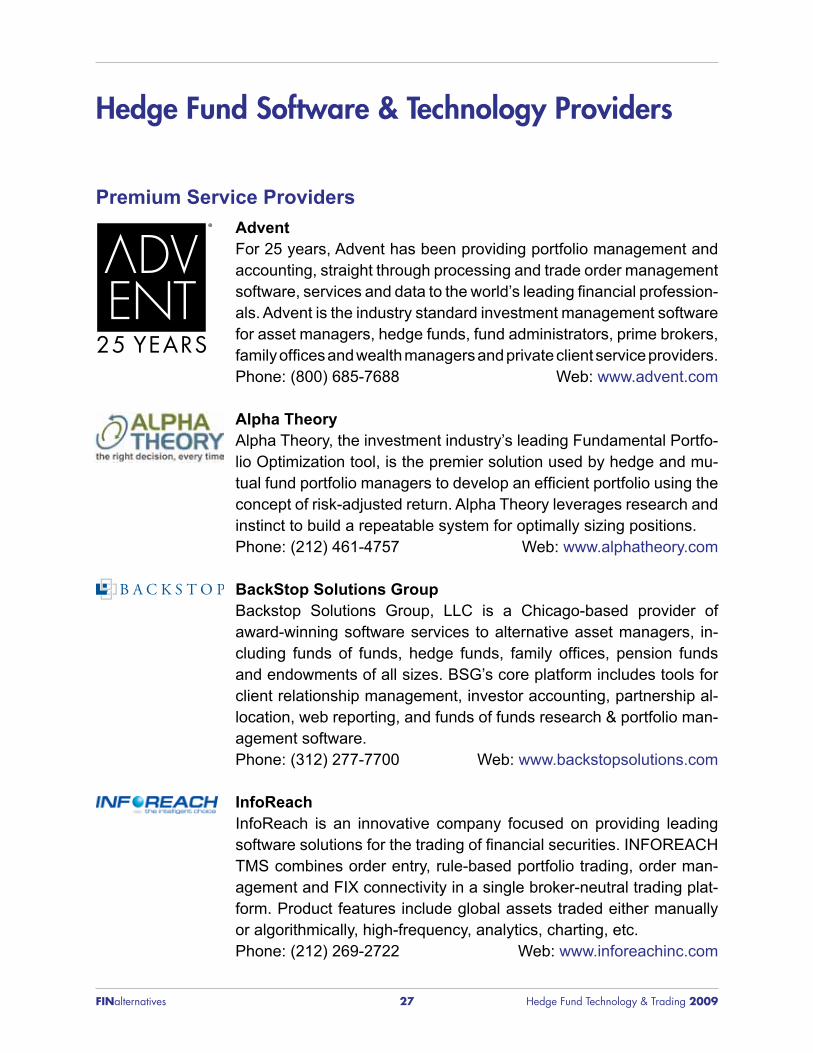

Premium Service ProvidersAdventFor 25 years, Advent has been providing portfolio management and accounting, straight through processing and trade order management software, services and data to the world’s leading financial profession-als. Advent is the industry standard investment management software for asset managers, hedge funds, fund administrators, prime brokers, family offices and wealth managers and private client service providers. Phone: (800) 685-7688 Web: www.advent.com

Alpha TheoryAlpha Theory, the investment industry’s leading Fundamental Portfo-lio Optimization tool, is the premier solution used by hedge and mu-tual fund portfolio managers to develop an efficient portfolio using the concept of risk-adjusted return. Alpha Theory leverages research and instinct to build a repeatable system for optimally sizing positions.Phone: (212) 461-4757 Web: www.alphatheory.com

BackStop Solutions GroupBackstop Solutions Group, LLC is a Chicago-based provider of award-winning software services to alternative asset managers, in-cluding funds of funds, hedge funds, family offices, pension funds and endowments of all sizes. BSG’s core platform includes tools for client relationship management, investor accounting, partnership al-location, web reporting, and funds of funds research & portfolio man-agement software. Phone: (312) 277-7700 Web: www.backstopsolutions.com

InfoReachInfoReach is an innovative company focused on providing leading software solutions for the trading of financial securities. INFOREACH TMS combines order entry, rule-based portfolio trading, order man-agement and FIX connectivity in a single broker-neutral trading plat-form. Product features include global assets traded either manually or algorithmically, high-frequency, analytics, charting, etc.Phone: (212) 269-2722 Web: www.inforeachinc.com

®

FINalternatives 28 Hedge Fund Technology & Trading 2009

Meridian Equity PartnersMeridian Equity Partners is an independently owned Wall Street bro-ker dealer with a global reach and a local feel. We provide custom-ized, best-of-breed strategic solutions to the investment management community. Products include: equities, options, futures, fixed income and forex. Member NYSE, FINRA, NFA & SIPC. Phone: (212) 500-6650 Web: www.meptraders.com

PerTrac Financial Solutions PerTrac Financial Solutions was founded in 1996 with the goal of creating a comprehensive suite of software solutions for investment professionals. Now an industry standard, PerTrac software is used by more than 2,000 clients in 50 countries, including banks, brokerage firms, consultants, plan sponsors, family offices, investment manag-ers and funds of funds. The company’s foundation product, the Per-Trac Analytical Platform, is now the world’s leading asset allocation and investment analysis software. Phone: (212) 661-6050 Web: www.pertrac.com

Client Relationship Management

Actuate www.actuate.com

Advent Software www.advent.com

Backstop Solutions www.backstopsolutions.com

Code Red www.coderedinc.com

Digiterre www.digiterre.com

EZ Data www.ezdata.com

Fidelity National Info. Services www.fidelityinfoservices.com

FundCount www.fundcount.com

Imagineer Technology Group www.itgny.com

Netage Solutions www.netagesolutions.com

PerTrac www.pertrac.com

ProTrak International www.protrak.com

RiskMetrics Group www.riskmetrics.com

Satuit Technologies www.satuit.com

UNAPEN www.unapen.com

Viveo www.viveo.com

FINalternatives 29 Hedge Fund Technology & Trading 2009

Compliance Software

Global Relay Communications www.globalrelay.com

HedgeOp Compliance www.hedgeop.com

MyComplianceOffice www.mycomplianceoffice.com

Smarsh www.smarsh.com

Electronic Trading / Trade Execution

Aegisoft www.aegisoft.com

Baxter Financial www.baxter-fx.com

Chi-Tech www.chi-tech.com

Fidessa www.fidessa.com

First Advantage www.fadv.com

First Derivatives www.firstderivatives.com

Flextrade www.flextrade.com

Inforeach www.in4reach.com

Investment Technology Group www.itg.com

Lightspeed Trading www.lightspeed.com

Market Technologies www.tradertech.com

Marketcetera www.marketcetera.com

Meridian Equity Partners www.meptraders.com

Omego www.omgeo.com

OptionsHouse www.optionshouse.com

Orc Trading www.orcsoftware.com

smartTrade www.smart-trade.net

Streambase www.streambase.com

Thesys Technologies www.thesystechnologies.com

thinkorswim www.thinkorswim.com

Traderserve www.traderserve.com

Trading Metrics www.tradingmetrics.com

XELink www.xelink.net

FINalternatives 30 Hedge Fund Technology & Trading 2009

Hardware & IT

Alden Technology Partners www.aldentech.comEze Castle Integration www.eci.comGeneric Network Systems www.gnetsys.netGravitas Technology www.gravitastechnology.comIndus Valley Partners www.indusvalleypartners.comInvestment Technology Partners www.investtechpartners.comMTM Technologies www.mtm.comNetwork Doctor www.networkdr.netVichara Technologies www.vichara.com

Portfolio Analytics, Accounting & Risk Management

Advent www.advent.comAlgorithmics www.algorithmics.comAlpha Theory www.alphatheory.comAlternativeSoft www.alternativesoft.comAppian Analytics www.appiananalytics.comAPT www.apt.comArchway Technology www.archwaytechnology.netAxioma www.axiomainc.comBravura Solutions www.bravurasolutions.com.auCalypso www.calypso.comCharles River Development www.crd.comCogency Software www.cogencysoft.comCognizant www.cognizant.comDataArt www.dataart.comDST Global Solutions www.dstglobalsolutions.comEagle Investment Systems www.eagleinvsys.comFermat www.fermat.frFidessa www.fidessa.comFinAnalytica www.finanalytica.comFinLab www.finlab.comFiserv www.fiserv.com

FINalternatives 31 Hedge Fund Technology & Trading 2009

Fi-Tek www.fi-tek.comFundCount www.fundcount.comGlobeOp Financial Services www.globeop.comHorizon Software www.hsoftware.comImagine Software www.derivatives.comImagineer Technology Group www.itgny.comIsis Financial Systems www.isisfs.comLinedata Services www.ldsam.comMurex www.murex.comNirvana Solutions www.nirvanasolutions.comNorthfield Information Services www.northinfo.comOdyssey Financial Technologies www.odyssey-group.comOmego www.omgeo.comOpenLink www.olf.comPaladyne www.paladynesys.comPartnersAdmin www.partnersadmin.comPatni www.patni.comPenny IT Works www.pennyitworks.comPerTrac www.pertrac.comPNC Global Investment Servicing www.pncgis.comRichard Fleischman & Associates www.rfa.comRisk-AI www.risk-ai.comRiskdata www.riskdata.comRiskMetrics www.riskmetrics.comSimCorp www.simcorp.comSmartStream www.smartstream-stp.comSophis www.sophis.netSS&C Technologies www.ssctech.comSungard www.sungard.comSybase RAP www.sybase.comTKS Solutions www.pennyitworks.comTwenty-First Century www.21stcenturycompany.comViteos www.viteos.comXenomorph www.xenomorph.com

Note: This list is not all inclusive. Large banks, hedge fund adminis-trators and prime brokers also offer many of these services.