Final Report NCCRP Baseline Study TEF/JBDC

67

BASELINE REPORT: STUDY OF THE CRAFT SECTOR ON THE NORTH COAST CORRIDOR NORTH COAST CRAFT REVITALIZATION PROJECT Prepared and Submitted by: Jamaica Business Development Corporation 14 Camp Road, Kingston 4 Jamaica Tele: 928-5161-5 Email: [email protected] Website: www.jbdc.net 2013

-

Upload

jamaica-business-development-corporation -

Category

Documents

-

view

222 -

download

2

description

Â

Transcript of Final Report NCCRP Baseline Study TEF/JBDC

BASELINE REPORT:

STUDY OF THE CRAFT SECTOR ON THE NORTH COAST CORRIDOR

NORTH COAST CRAFT REVITALIZATION PROJECT

Prepared and Submitted by:

Jamaica Business Development Corporation 14 Camp Road, Kingston 4

Jamaica Tele: 928-5161-5

Email: [email protected] Website: www.jbdc.net

2013

1

List of Plates Plate I Craft Producers at their workshop in Cambridge St James

Plate II Craft Producers displaying their wares in Coopers Pen Trelawny

Plate III Typical Tools shared by craftsmen in Mt Zion St Ann

List of Charts Chart 1 Organizations Recognized as Assisting Craft Producers

Chart 2 Additional Products Desired by Craft Producers in St Ann

Chart 3 Additional Products Desired by Craft Producers in Trelawny

Chart 4 Additional Products Desired by Craft Producers in St James

Chart 5 Diversity of Customer Base – All Producers

Chart 6 Methods Used for Keeping Records of Earnings

Chart 7 Methods Used for Keeping Records of Expenses

Chart 8 Methods Used for Keeping Track of Expenses

List of Figures Figure 1 Core Business Processes for Aboriginal Art (Simplified)

Figure 2 Core Business Processes for Leather Craft (Simplified)

Figure 3 Core Business Processes for Needle-craft- Dressmaking (Simplified)

List of Tables Table 1 Average Age of Proprietor by Sex and by Parish

Table 2 Average Number of Employees per Producer Organization

Table 3 Knowledge of Organizations or Groups that Support Craft Producers

Table 4 Assistance from Organizations that Support Craft Producers

Table 5 Nature of Assistance Received From Support Organizations by Parish

Table 6 Requirement for Additional Support by Parish

Table 7 Expected Impact of Additional Support – St Ann Producers

2

Table 8 Expected Impact of Additional Support – Trelawny Producers

Table 9 Expected Impact of Additional Support – St James Producers

Table 10 Producer/Employee Skills for Craft Producing Organizations (that employ workers)

Table 11 Producer/Employee Skills for Craft Producing Organizations (that do not employ

workers)

Table 12 Frequency Table for Skills Required in the Parish of St Ann

Table 13 Frequency Table for Skills Required in the Parish of Trelawny

Table 14 Frequency Table for Skills Required in the Parish of St James

Table 15 Craft Items by Product Group

Table 16 Product Profile of Craft in the Parish of St Ann

Table 17 Product Profile of Craft in the Parish of Trelawny

Table 18 Product Profile of Craft in the Parish of St James

Table 19 Years in Operation for the Typical Craft Producing Organization

Table 20 Future Products Desired by Parish

Table 21 Major Challenges Foreseen to Launch Future Products (St Ann Producers)

Table 22 Major Challenges Foreseen to Launch Future Products (Trelawny Producers)

Table 23 Major Challenges Foreseen to Launch Future Products (St James Producers)

Table 24 Tools and Technologies Used to Make Products

Table 25 Adequacy of Current Tools for the Undertaking of Production

Table 26 Tools and Technologies of Craft Producers by Product Group

Table 27 Market Segmentation for Craft Producers by Parish

Table 28 Distribution Channels – St Ann

Table 29 Distribution Channels – Trelawny

Table 30 Distribution Channels – St James

Table 31 Marketing Methods Used by Parish

Table 32 Level of Export of Craft Items by Parish

Table 33 Price Determination Methods by Parish

Table 34 Average Revenue and Expenditure Reported by Craft Producers by Parish

Table 35 Craft Producers who have a Designated Bank Account for their Business

3

Table 36 Where Money is kept when there is no Bank Account for Business

Table 37 Number of Businesses and Registration by Parish

Table 38 Overall Level of Education of Craft Producers

Table 39 Education Level of Staff Members

Table 40 Ability of Craft Producers to Use a Computer

Table 41 Number of Craft Producers who desire Computer Training

List of Acronyms JAMPRO Jamaica Promotion

JBDC Jamaica Business Development Corporation

TEF Tourism Enhancement Fund

UK United Kingdom

USA United States of America

List of Appendices Appendix I – Instruments

Attachment I – Producer Questionnaire

Attachment II – Focus Group Guide

4

Table of Contents

EXECUTIVE SUMMARY .......................................................................................................................... 6

1.0 INTRODUCTION ............................................................................................................................ 8

1.1 Background to the North Coast Craft Sector ................................................................................ 8

1.2 Objectives of the Baseline Study .................................................................................................. 8

1.3 Scope of Work and Deliverables .................................................................................................. 9

1.4 Technical Approach and Methodology ......................................................................................... 9

1.4.1 Work plan and Timelines .................................................................................................... 10

1.4.2 Geographical Areas Covered .............................................................................................. 10

1.4.3 Nature and Overall Behaviour of Respondents ................................................................... 10

1.5 Limitations .................................................................................................................................. 10

2.0 NORTH COAST CORRIDOR CRAFT SECTOR REPORT ........................................................ 11

2.1 Environmental Setting................................................................................................................. 11

2.1.1 Situational Analysis ............................................................................................................ 15

2.1.2 Screening Question A1 ............................................................................................................ 17

2.1.3 Demographic Description of Producers ........................................................................... 18

2.2 Membership Structure ................................................................................................................ 18

2.2.1 Leadership and Management .............................................................................................. 18

2.2.2 Employee Profile................................................................................................................. 19

2.2.3 Current Ventures ................................................................................................................. 20

2.3 Existing Skills ............................................................................................................................. 24

2.3.1 Craft Related Skills ............................................................................................................. 24

2.3.2 Other Skills ......................................................................................................................... 28

2.4 Products and Production Processes ............................................................................................. 29

2.4.1 Types of Products................................................................................................................ 29

2.4.2 Details of Operations .......................................................................................................... 34

2.4.3 Future Products ................................................................................................................... 37

2.4.4 Tools and Technologies ...................................................................................................... 39

2.5 Markets ....................................................................................................................................... 41

2.5.1 Current Markets and Targeted Customers .......................................................................... 42

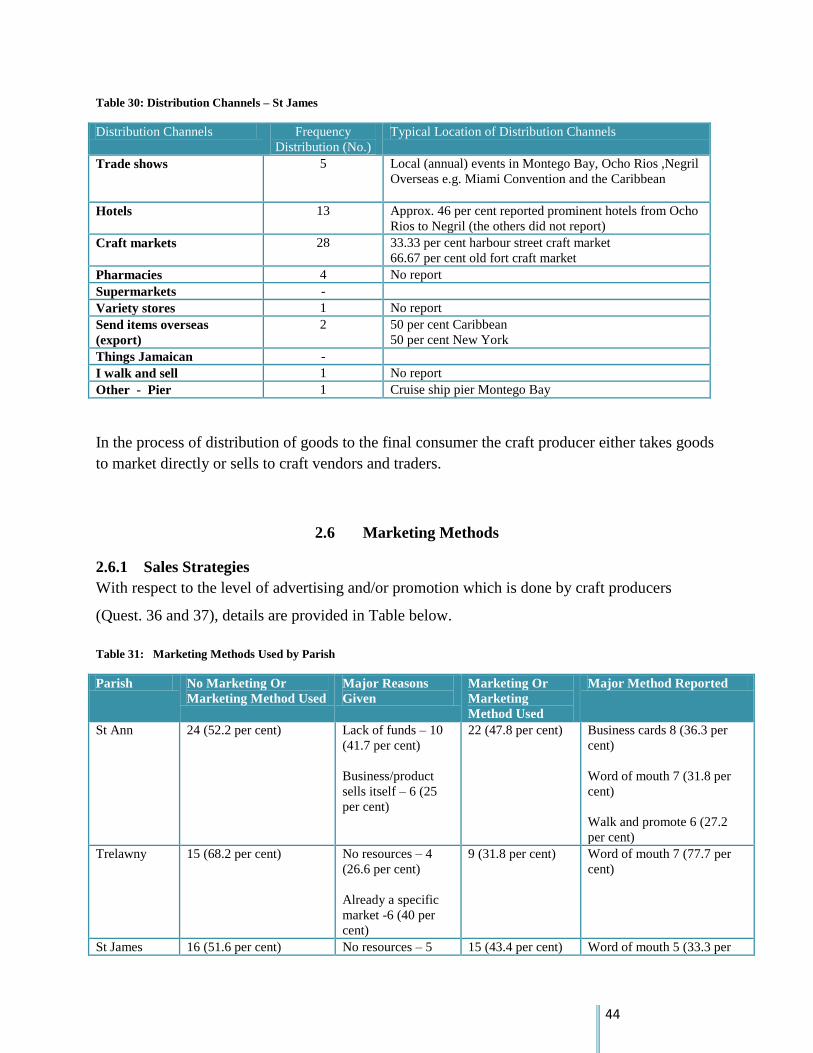

2.5.2 Distribution Channels ......................................................................................................... 43

2.6 Marketing Methods ..................................................................................................................... 44

5

2.6.1 Sales Strategies ................................................................................................................... 44

2.6.2 Exports ................................................................................................................................ 45

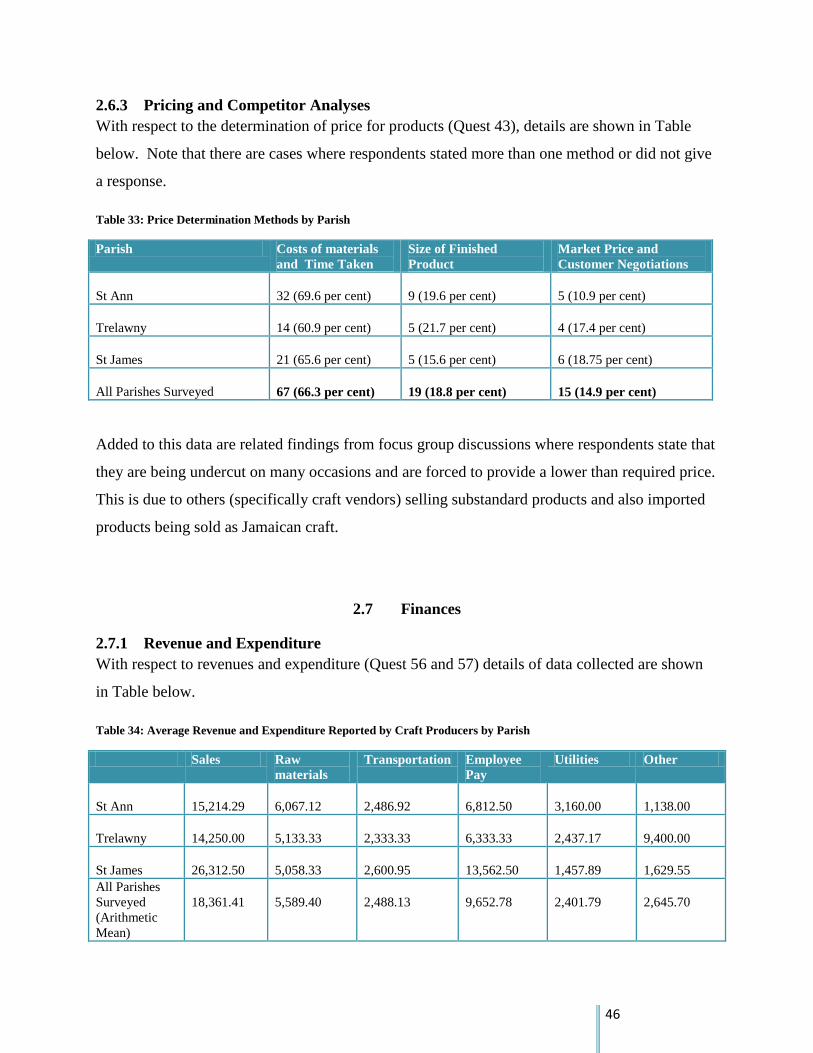

2.6.3 Pricing and Competitor Analyses ....................................................................................... 46

2.7 Finances ...................................................................................................................................... 46

2.7.1 Revenue and Expenditure ................................................................................................... 46

2.7.2 Financial Management ........................................................................................................ 47

2.8 Support Services ......................................................................................................................... 50

2.8.1 Permits and Licenses ........................................................................................................... 50

2.9 Legal Status of Business ............................................................................................................. 50

2.9.1 Registration ......................................................................................................................... 50

2.10 Business Development ................................................................................................................ 51

2.10.1 Extent of Business Formulation .......................................................................................... 51

2.10.2 Literacy and Numeracy ....................................................................................................... 51

2.10.3 Previous Exposure to Business ........................................................................................... 52

2.10.4 Computer Literacy .............................................................................................................. 52

3.0 CONCLUSION ............................................................................................................................... 54

PLATES ...................................................................................................................................................... 55

6

EXECUTIVE SUMMARY

The current situation with respect to craft producer organizations on the North Coast Corridor is

one which sees the following:

1. They are predominantly micro-producers who operate on a small scale having,

businesses which are predominantly unregistered (with the Companies office of

Jamaica).

2. The craft producers represent strong personal and business ties which have endured

sometimes for more than a generation within communities. However these relations

have not yet been formalized into advocacy groups in order to minimize the current

common challenges faced in the sector.

3. Training is in many cases informal (and strongly linked to personal talent) and there are

no industry-wide standards within which craft producers (in their various trades)

operate.

4. Products made are done under highly labour intensive conditions.

5. There are high transaction costs in some cases especially that of transportation of goods

and raw materials.

6. The industry has a plethora of small firms which struggle to expand based on financial

constraints, lack of required training, machinery and tools. This poses a risk to the

sector especially in current times of economic austerity.

7. The sector offers a significant opportunity to improve employment specifically youth

employment.

Based on the field survey, the average craft producing organization, along the North Coast

Corridor has been in operation for an average of approximately 20 years. This is almost half the

life of the owner/proprietor who is on average 48.63 years. Information from the study shows

that almost 70 per cent of such enterprises do not employ people. The average workforce size

(mean) of these organizations is 3.1 persons (1.8 part time and 1.4 full time).

Employees are in many cases family members (e.g. spouses and children) who assist in the

business or who are undergoing apprenticeship training. Additional staff is sometimes hired

seasonally to do part time work in most organizations. The majority of respondents can be

7

deemed both literate and numerate with the average proprietor having acquired secondary level

education (40 per cent). In addition 39 per cent have completed primary school and 9 per cent

tertiary education. Assessment of workers in craft producing organizations shows that the

average employee has 12.47 years of schooling (those who reported).

With respect to tools and technologies used these vary significantly by individual craft

producer and also by type of craft being produced. Only 28 per cent of respondents stated that

they used their hands only as 69 per cent of respondents stated that they used a combination of

hand, machinery and other tools. Discussions with craft producers show that they would like

more electrical tools to improve production.

The typical customer targeted by craft producers is a tourist as stated by 41 per cent of

respondents. However more detailed analysis shows that producers cater to more than one niche

market as evidenced by the fact that 24 per cent of respondents stated that they catered to more

than three major markets.

The craft market is the dominant distribution channel followed by the use of contacts in

hotels. The majority of respondents (54.5 per cent) stated in the questionnaire that they did not

do any form of marketing advertisement marketing and/promotion. More than half of same

stated that the major reason that they participate in no form of advertising, marketing

and/promotion is due to the fact that they have a ready market and also their products (and in

some cases their customers) are well known.

There is low exporting as less than 8 per cent of craft producers in the target area reported

that they directly exported products. With respect to the pricing of goods, the dominant rationale

for a final price is that of the cost of raw materials and the time taken to make the product (66.3

per cent of respondents). The size of the finished product (18.8 per cent) and prevailing market

conditions (14.9 per cent) are also significant considerations.

Based on revenue and expenditure data given by craft producers the average organization

shows that no profit is earned. In addition financial management data shows that there is also a

lack of fiscal discipline existing in day to day management of these organizations. This is

evidenced by high incidences of no records being kept and also the lack of a designated bank

account for the business.

8

1.0 INTRODUCTION

1.1 Background to the North Coast Craft Sector

The Jamaican Craft Sector is not only a significant aspect of the Tourism Industry but also a

major aspect of economic activity across Jamaica. In many communities (especially those in and

around the North Coast), this sector is a stalwart contributor to employment and creates

backward and forward linkages. These linkages are not just to communities where there are craft

producers but also those that provide raw materials and distribute finished products.

Notwithstanding this, the sector is far from maximizing its returns. There are now

poignant issues related to quality of finish, distribution channels, access to markets, pricing, the

influence of middlemen and traders and training. These are needed especially for the North

Coast Corridor; including the parishes of St Ann, Trelawny and St James which are areas with

internationally famous attractions.

It is within this context that the Jamaica Business Development Corporation (JBDC) and

the Tourism Enhancement Fund (TEF) has commissioned a study of Craft Producers from the

parishes of St Ann, Trelawny and St James. The project will seek to address the current

shortfalls in areas such as product development and design; business and professional skills;

marketing and market development

1.2 Objectives of the Baseline Study

This assignment provided baseline information of the target group to guide the development of

the work plan for the North Coast Craft Revitalization Project. It provided current, accurate and

relevant information regarding the size, location and areas of specialization of the craft

producing sector in the target area. The study also examined the challenges faced by the

producers and their needs.

9

1.3 Scope of Work and Deliverables

The major requirements of the study included:

1. A comprehensive report on Craft Producers/Businesses within the target area. Report should

provide adequate information as outlined in the Scope.1

2. A comprehensive database of craft producers and craft association in the target areas (St.

James, Trelawny and St. Ann) including information such as:

Contact Person

Telephone / Email

Address / Location

Major Products / Services

Major Business Constraints

Skill Level

Types of Assistance being received (if any)

1.4 Technical Approach and Methodology

The baseline database and comprehensive report was compiled from both primary and secondary

data sources. With respect to secondary sources, past reports of a similar nature were collected

and sourced and also community profiles from organizations such as the Social Development

Commission (SDC).

With respect to primary data collection, the sampling technique used was purposive

sampling. Primary data was collected mainly through direct discussions, interviews and field

observations in the parishes of St Ann, Trelawny and St James. The major instruments and

collection methods used were:

1. A direct six (6) page questionnaire was filled out by 101 craft producers from the

parishes of St Ann (46), St James (31) and Trelawny (24). The majority of these

questionnaires were executed through in-depth face to face interviews with five (5)

done through telephone conversations.

1 Based on the Term of Reference [Section 3.2] the major areas required for research are: [a] environmental setting, [b] membership structure, [c]

existing skills, [d] products, [e] products, [f] markets, [g] marketing methods, [h] finances, [i] legal status, [j] support services and [k] business development.

10

2. Three (3) focus groups (each comprising five respondents) were kept for each parish

being studied i.e. St Ann, Trelawny and St James on August 14, 2013.

3. Field trips to three (3) communities with craft producers ; Mt Zion in St Ann, Coopers

Pen in Trelawny and Cambridge in St James.

4. A (non-coded) database in MS Excel was developed for the results of the 101

questionnaires

Data analysis included both quantitative and qualitative methods. Typical quantitative methods

included the employment of basic descriptive statistical methods while quantitative methods

included the use of case studies, SWOT analyses and flow charting.

1.4.1 Work plan and Timelines

The stipulated time for the assignment was four (4) weeks.

1.4.2 Geographical Areas Covered

Field trips took place over the period August 12 to 15, 2013. These were in the subject parishes

of St James, Trelawny and St Ann inclusive of direct visits to communities with craft producers

in all three parishes. These included Mt Zion district (St Ann), Coopers Pen (Trelawny) and

Cambridge (St James).

1.4.3 Nature and Overall Behaviour of Respondents

Respondents showed willingness to being interviewed and contributed to frank discussions about

the challenges they faced being craft producers. There were also cases of scepticism and lack of

trust (where some respondents thought that this was another attempt to get taxes).

Notwithstanding this all producers approached in the respective parishes agreed to do the

interview.

1.5 Limitations

The major limitation in undertaking this task was time due to the fact that this is the first project

of its nature being undertaken on such a large scale for craft producers. The lack of a pilot study

or a pre-testing exercise created limitations in the design of instruments; being largely

exploratory and open-ended. With respect to the results, some respondents may have

underreported in some cases, especially with respect to raw materials (for example for knitting

some may not have stated needles as a raw material).

11

2.0 NORTH COAST CORRIDOR CRAFT SECTOR REPORT

2.1 Environmental Setting

Mount Zion-St Ann

The Community of Mount Zion is located on a very hilly terrain, 1500-1800 feet above sea

levels, in the parish of St Ann. It is bordered to the east by the district of Chester, to the west

Runaway Bay and to the south Lime Hall. Mount Zion district has a population of approximately

2000 residents, 20% of whom are children below 12 years old.

According to the Social Development Commission (SDC) Community Profile (2007) 91.1%

of households have electricity, but the entire community is poorly lit at nights due to the absence

of street light. The community is plagued with low or no water pressures; 39.6% of the residents

access water from public water standpipes, 17% have private piped water, the other 44.4% get

their water from harvesting of rain water in tanks, and from springs and or rivers. 95.6% of

households have telephone service, of which 100% is cellular phones. However only 6.7 % have

access to internet, a contributory factor could be the slow speed of internet through cellular

phones. Road condition leading to the community from the north coast highway is in a

deplorable condition and this poses a major challenge to the residents and the taxi operators who

traverse the roads daily. Licensed taxis are the mode of transportation used by residents in this

community.

Mount Zion has no health centre located in the community therefore residents travel to

Runaway Bay or St Ann’s Bay for basic health services. The housing stock in the community is

in fairly good condition. 73.3% of residents own their houses. 25% of the houses are made of

block and steel and 20% of wood and brick. There are 2 schools in the community a basic, and

an all age school.

Economic activity in the district is dependent on tourism, farming, trade, and self-

employment. The SDC Community Profile (2007) indicates that 52% of the employable

population is employed, 81% full time,5% self-employed, 10% part time, 3% seasonally and 2%

on contract. Of this population 30% is involved in craft and related trade workers, 30% are

12

service workers, shop and market sales workers, 15% are professionals, senior officials and

technicians and 25 are engaged in agriculture and plant and machine operators.

Environmental challenges being faced by the community are blocked drains caused by the

illegal dumping of garbage. This is a catalyst for environmental damage caused from flooding,

landslides, and rock falls. There is also the possibility of poor water quality. This is so as 38.4%

of residents utilize water closets not linked to sewer, 24% uses pit latrines and so there is a strong

possibility of raw sewage seeping into water resources in and around the community.

Cambridge , St James

The Community of Cambridge, the first rural town in St James, is located in a partially hilly

and undulating terrain, in the south easterly section of the parish of St James, 18 miles from

Montego Bay.

Cambridge district has a population of approximately 4811 residents of which there are 55%

females and 45% males. 36.62% of the population are children below 14 years old. There is 1162

household. This community is deemed to have low levels of volunteerism, civic pride and

community spirit.

According to the Social Development Commission (SDC) Community Profile (2009) 92.9%

of households have electricity, 6.2% uses oil lamps and .9% uses candles. In the community

24.8% of the residents access water from public water standpipes, 20.4 % have private piped

water, 39.9% have public piped water. 94% of households have telephone service, of which 74.5

% have cellular phones and 24.6% uses both land lines and cellular phones. However only 17.3

% have access to internet, a contributory factor could be the slow speed of internet through

cellular phones. Main road leading to the community from Montego Bay is in good condition,

however, the secondary and arterial roads are in a deplorable condition and this poses a major

challenge to the residents and vehicular traffic which traverse the roads daily. For transportation

to and from the community 81.4% of the residents use buses, 8.8% private cars and .9% donkey.

Cambridge has a type 11 health centre located in the community which is utilized by

approximately 30.93% of the residents. The housing stock in the community is in fairly good

13

condition. 77.6% of the houses are made of block and steel and 48% of board. There are 4

schools in the community a basic, infant, all age and high school.

Economic activity in the district is mainly focused on the provision of services and is

dependent on construction, cabinet making, farming, beauty care, and secretarial. The SDC

Community Profile (2009) indicates that 66% of the heads of households who are trained in

specific areas are employed using the training received. Highest areas of skill for female are

hospitality (31%) and professional and technical services (29%); for male construction and

cabinet making (30.5%) and machine and appliance (22%). There is 52% unemployment among

the youth between the ages of 14-29.

Main challenges affecting businesses in the community, are high transportation and

labour costs, high unemployment and low levels of disposable income.

Environmental challenges being faced by the community are blocked drains due to illegal

dumping of garbage. This is a catalyst for environmental damage caused from flooding and land

slides. There is also the possibility of poor water quality. This is so as 16.1% of residents utilize

water closets not linked to sewer, 15.4% uses pit latrines and so there is a strong possibility of

raw sewage seeping into water resources in and around the community.

Coopers Pen , Falmouth, Trelawny

The Community of Coopers Pen a district of Falmouth, is located mainly on 11 acres of

beach land, in the north easterly section of the parish of Trelawny, 2 miles from Falmouth.

Coopers Pen community has a population of approximately 2785 residents occupying 202

households.

According to the Social Development Commission (SDC) Community Profile on the

wider community of Falmouth (2009) 97% of households have electricity, 3% uses oil lamps. In

the community 7.7 % access water from private catchments, 48.5 % have private piped water,

39.3% have public piped water. 99% of households have telephone service, of which 66 % have

cellular phones and 33 % uses both land lines and cellular phones and 1% landlines only.

However 28 % have access to internet. The main roads leading to the community from the North

14

Coast Highway is in good condition. For transportation to and from the community 79% of the

residents use licensed taxis, 15.1% robots, 25 % private cars and 11.8 % the bus system .

Falmouth has 2 type 1V health centre and one type C hospital located in the community

which is utilized by approximately 27 % and 86% of the residents respectively. The housing

stock in the community is in fairly good condition. 67.4 % of the houses are made of block and

steel and 24.3 % of board. All houses in the Coopers Pen district are of block and steel. There

are 10 schools in the Falmouth community.

Economic activity in the district is mainly focussed on the provision of services and is

dependent on construction, cabinet making, farming, beauty care, secretarial. The SDC

Community Profile (2009) indicates that 72 % of the heads of households are employed; of the

male headed households 83.6% are employed and 57.1% of the female headed households. Of

the employed groups 24.6% are service workers and shop and market sales workers, 14.3% are

professionals, 13.6% are craft producers and workers, 7.4% are elementary occupation and 3.3%

are involved in agriculture. Unemployment is highest among the seniors aged 60 and over. 29%

of this unemployment is due to retirement.

Challenges affecting businesses in the community are high transportation and labour

costs, high unemployment and low levels of disposable income. Environmental challenges being

faced by the community are blocked drains due to illegal dumping of garbage. This is a catalyst

for environmental damage caused from flooding and landslides. There is also the possibility of

poor water quality. This is so as 50.7 % of residents utilize water closets not linked to sewer and

35.7 % use ones that are linked to sewer , 14.7 % uses pit latrines and so there is a strong

possibility of raw sewage seeping into water resources in and around the community. There is

also dumping of the mangroves (a breeding ground for lobster and fish) for housing

developments. Waste water is also being channelled into the sea which affects the foreshore and

the marine environment

15

2.1.1 Situational Analysis

Assessments of the three craft producing communities showed the following strengths:

A sense of unity and mutual support among craftsmen – this is more so in sites visited

in Mt Zion and Cambridge where tools are shared by workers

Organizations at the community level are quite resilient, built upon long forged

informal networks of family, friends and acquaintances

There are scale benefits as raw material, transportation and distribution costs are shared

among craftsmen

A market exists nearby – this is the case only for Coopers Pen where producers are near

the pier and also near a major local hotel where they have access to sell to the tourist

directly 7 days per week. They also sell in bulk to craft traders, this helps to increase

the average price for products overall.

Wood carvers in Coopers Pen are known for their high quality finished products

Wood carvers in Mount Zion, Coopers Pen and Cambridge have been carving in these

communities for over 20 years.

Highly intelligent, high school graduates are among the woodcarvers in the 3 areas

There is real time information and skills exchange where in some areas (Cambridge and

Mt Zion) carving is done at one physical site and actual production and learning takes

place almost simultaneously

The following weaknesses were identified:

In many cases craftsmen produce the same type of products.

For the most part, craft producers seem to be price takers (low market power in the

setting of a market price). Producers also lack knowledge on how to price their

products, as they have very , poor record-keeping skills.

There are no major industry standards with respect to work quality.

Transportation and distribution costs can be high as many producers do not have their

own transportation especially those in deep rural areas. Areas such as Mt Zion had

almost impassable roads.

16

Numerous distances sometimes have to be travelled to get raw materials for example

trees/wood for carving.

Some areas are highly gender biased which limits the talent pool e.g. wood carving is

male dominated.

More modern tools are required to improve product quality and productivity. In some

cases almost 20 individuals shared the same set of tools (Mt Zion).

There is not much value added in properly ‘finishing work’ from the stand point of the

craft producer. This excludes them from a major aspect of the value chain.

Critical markets are not accessible to them and this limits their production levels. For

example producers in Cambridge state that the fact that they do not have direct access

to hotels and tourists have been a critical obstacle to doing business.

Not many community and advocacy groups represent craft producers at the local level.

More formal training may be required to harness and improve existing talent.

Low levels of formal business training and acumen. This has seen low levels of record

keeping, business strategy planning and other critical steps required to be not just a

subsistence activity but one which is profitable.

Wood craft producers use cedar trees as their main source of raw material, but they do

not replant trees in the community.

They are not organized into formal groups although they have been working as groups

for years.

The woodcraft producers do not have proper shelter/workshop for example producers in

Mount Zion workshop is under a tree from which they have been working for many

years, those in Cambridge have limited covering and would also be affected by the bad

weather. This lack of proper workshops, does hamper production during rainy seasons.

The major opportunities open to craft producers are:

Major markets still remain untapped e.g. discussions show that Kingston and other

local urban areas have not been fully exposed to Jamaican craft producers.

The access of social media to promote products.

The sector has survived numerous downfalls e.g. natural disasters but has still been

resilient.

17

To formalize training and apprenticeship schemes that will involve youth. This

demographic currently has the highest unemployment rate nationally.

Grant funding available to groups for product development

The major threats that exist in the sector are:

Existing regime of devaluation and related austerity measures. This has been quite

impactful with respect to raw materials and utility bills.

Cheap imported goods which are said to be of lesser quality which is gradually

marginalizing the local industry.

The ageing demographic which is now participating in the craft producing trades will

threaten a loss of skills over time which will not be passed on to present and future

generations.

2.1.2 Screening Question Results A1

All respondents who were approached and fulfilled the criteria (i.e. being a craft producer

and working or residing in the parishes of St Ann, Trelawny and St James) agreed to participate

in the interview process.

Efforts were therefore made at the start of the interview process to ensure that all

respondents were craft producers who made craft items themselves. With respect to question 1A

all producers gave their names and there was no producer group (1B) stated. With regard to

availability of a contact number (Ques. 4) only seven (7) respondents in all parishes surveyed

could not provide a cell phone contact at all. On the other hand only two (2) respondents

provided a separate work phone and only two (2) respondents provided a separate home phone.

All respondents in all parishes (Ques. 5) surveyed provided an address (inclusive of the parish).2

With respect to an email address (Ques. 6) only thirteen (13) respondents (12.9 per cent) could

furnish the interviewer with this when asked.

2 Note that this address was either their workplace or home (or some cases this was one and the same place)

18

2.1.3 Demographic Description of Producers

The craft sector in the three parishes (St Ann, Trelawny and St James) shows a higher level of

males participating than females overall (Producer Questionnaire – Quest 2). However based on

the survey data, St James sees a dominance of women. There are also marginal differences in

their respective ages by parish (Quest. 3). Further details are shown in Table 1 below.

Table 1: Average Age of Proprietor by Sex and by Parish

Parish Male Female Total Avg. Age

(Years)

Modal

Age

Median

Age

Min

Value

Max

Value

St Ann 24 22 46 48.31 55 50 23 69

Trelawny 19 5 24 49.09 52 51 26 68

St James 14 17 31 48.76 48 48 31 66

All Parishes

Surveyed 57 44 101 48.63

52 49.5 23 69

Source: North Coast Corridor Craft Baseline Study 2013

2.2 Membership Structure

2.2.1 Leadership and Management

Leadership and management is to some extent automatic in these entities; in many cases

respondents are sole traders who are using craft production to support themselves and their

dependents. Their daily activities include the ability to co-ordinate resources to achieve a

common goal (whether this is for survival or profit). Discussions with most craft producers

show many elements of leadership such as resilience, initiative, and decision-making. Focus

groups, interviews and community discussions show that to operate a craft organization

successfully requires these and related traits such as fortitude, initiative and a high tolerance for

risk.

19

However to become more competitive and to have more sustainable organizations,

respondents agree that there is the need for improvement in areas such as advocacy,

professionalism, goal setting and adherence to production standards. This is not just lacking at

the firm level but sector wide. In addition, at the community level although craft producers have

taken initiatives to work together including sharing of tools and other resources, they have not

formed themselves into formally registered groups. For instance field interactions and

discussions in focus groups show that craft producers are just starting to form themselves into

advocacy groups e.g. Jamaica Independent Artisan Cooperative Society (JAMIA).

2.2.2 Employee Profile

Overall 29.7 per cent of respondents in all three parishes stated that their organization

employed someone other than the owner proprietor (Quest 13). When broken down by parish,

nine (9) respondents from St Ann (19.6 per cent) stated that they employed people in their

organizations. For Trelawny there were ten (10) respondents (41 per cent) who stated that they

had hired staff. Responses in St James saw eleven (11) respondents (35.5 per cent of

respondents) stating that they hired staff.

Average employment by organization varied marginally by parish with St James

organizations having the highest levels. Further details are shown in table 2 below.

Table 2: Average Number of Employees per Producer Organization

Parish Avg. Number

Employed

Avg. Number Full

Time

Avg. number Part-Time

St Ann

2.7

2

1

Trelawny

2.7

1.4

1.4

St James

3.8

2.0

1.8

All Parishes Surveyed - Mean

3.1

1.8

1.4

Mode of All Parishes

2.0

1.0

1.0

Median of All Parishes

2.0

1.0

1.0

Max Value – All Parishes

12

10

5

Min Value – All Parishes3

1

1

1

3 It is assumed that the owner is also provided with employment.

20

Observations and discussions show that in many cases, micro-enterprises predominantly hire a

family member or close associate and the payment is that of a stipend [Section 2.7]. In many

cases this is also an apprenticeship arrangement with not many workers being formally trained in

their respective skills [Section 2.3.1].

2.2.3 Current Ventures

With respect to knowledge of organizations that support craft producers (Quest 44) 30.7 per cent

of all respondents (in all three parishes) stated that they knew of such organizations. Further

details by parish are shown in table below.

Table 3: Knowledge of Organizations or Groups that Support Craft Producers

Parish Knowledge of Support

Organizations that Assist Craft

Producers

No Knowledge of Support

Organizations that Assist Craft

Producers

St Ann

16(34.8 per cent)

30 (65.2 per cent)

Trelawny

5 (20.9 per cent)

19 (79.1 per cent)

St James

10 (47.6 per cent)

21 (42.4 per cent)

All Parishes Surveyed

31 (30.7 per cent)

60 (69.3 per cent)

The organizations recognized by craft producers as supportive to their ventures (Quest 45) are

shown in Chart 1 below.

Jamaica National, 3, 10%

JAMAIA, 4, 13%

Things Jamaican, 3, 10%

TPDCo, 10, 32%

JAMPRO, 6, 19%

Other, 5, 16%

0 5 10 15

Jamaica National

JAMAIA

Things Jamaica

TPDCo

JAMPRO

Other

Chart 1: Organizations recognized as Assisting Craft Producers

21

With respect to organizations benefiting from assistance in the past (Quest 46) details are shown

by parish in table 4 below

Table 4: Assistance from Organizations that Support Craft Producers

Parish Benefited from Assistance in the

Past

Did not Benefit From Assistance

in the Past

St Ann

8 (17.4 per cent)

38 (82.6 per cent)

Trelawny

2 (8.3 per cent)

22 (91.6 per cent)

St James

10 (32.3 per cent)

21 (67.7 per cent)

All Parishes Surveyed

20 (19.8 per cent )

81 (80.2 per cent)

With respect to the nature of assistance received from support organizations (Quest 47) this is

shown in the Table below.

Table 5: Nature of Assistance Received From Support Organizations by Parish

Parish Organization Types Nature of Assistance Service Improvements

Reported as a Result of

Assistance

St Ann

(note that only 7 people

responded in this parish

to this section)

Tourism Development

and Attractions – 57.14

per cent

Technical (Craft Related)

– 14.29 per cent

Financial – 28.57 per cent

Trade licence

Visits to shows

overseas

Visa to import goods

Selling spaces

Appraisal of items

Loans

Reponses here were not very

clear only two respondents

stated categorically that they

were able to access raw

materials as a result of the

assistance.

Trelawny

(note that only 3 people

responded in this parish

to this section)

Tourist Development –

33.33 per cent

Small Business

Development – 33.33 per

cent

Financial – 33.33 per cent

Seminar

Loan

Training

Learn about Jamaica

Better pricing and presentation

of items

St James

(note that only five

respondents were tallied

in this section

Investment – 60 per cent

Tourism Development –

40 per cent

Certification

Only two respondents

contributed here and they both

stated that the assistance was

instrumental in them knowing

more about other customs and

the customs of Jamaica

22

With respect to additional support required (Quest 48) these are shown in detail in table below.

Table 6: Requirement for Additional Support by Parish

Parish Needs Additional Support at this

Time

Do Not Need Additional Support at

this Time

St Ann

45 ( 97.8 per cent)

1 (2.2 per cent)

Trelawny

24 (100 per cent)

0

St James

31 (100 per cent)

0

All Parishes Surveyed

100 (99 per cent)

1 (1 per cent)

With respect to the expected impact of additional support (Quest. 49) the major responses are

shown in Tables 7-9 below. It is important to note that responses here are not mutually exclusive

as some respondents stated multiple support needs.

Table 7: Expected Impact of Additional Support – St Ann Producers

Assistance Needed

Frequency (Percentage)

Forecasted Impact

Equipment and Raw

Materials

54.4 per cent

Increased production – 76 per cent

Reduces strenuous work 8 per cent

Better storage and inventory management – 8 per cent

Increase sales overall – 8 per cent

Financial Assistance

43.5 per cent

Increase employment and training – 35 per cent

Expand business and diversify product line – (50 per

cent)

Produce more and improve product quality – 15 per

cent

Market Access and

Sales Promotion

19.6 per cent

Improved sales revenue – 44.44 per cent

Improved innovation and quality – 22.22 per cent

Other (e.g. increased customer service, ability to get

better prices for product, etc) – 33.34 per cent

Additional Employees

and Training

Programmes

4.3 per cent

Increased employment – 50 per cent

Improve exports – 50 per cent

23

Table 8: Expected Impact of Additional Support – Trelawny Producers

Assistance Needed Frequency (Percentage) Forecasted Impact

Equipment and Space

58.3 per cent

Increased production – 78.6 per cent

Other (inclusive of purchase of more stock, expanded

markets, increased revenues) – 21.4 per cent

Financial Assistance

33.3 per cent

More tools and materials – 37.5 per cent

Produce more goods – 37.5 per cent

Other( improve product quality, pass on knowledge to

others, upgrade business facilities etc) – 25 per cent

Market Access,

Promotion and

Distribution

33.3 per cent

Increased sales revenue – 62.5 per cent

Other (passing on of knowledge, improved product

quality, employment, etc) – 37.5 per cent

Training and Materials

12.5 per cent

Improved products and revenue (all respondents)

Table 9: Expected Impact of Additional Support – St James Producers

Assistance Needed Frequency (Percentage) Forecasted Impact

Equipment and Space

38.7 per cent

Increased employment – 25 per cent

Increased production – 50 per cent

Other (producing genuine Jamaican goods, increased

sales, export development, etc) – 25 per cent

Finance and Raw

Materials

48.4 per cent

Increased production – 26.7 per cent

Employ more people – 26.7 per cent

Improved distribution systems and inventory – 13.3

Increased sales revenue – 13.3 per cent

Other (ability to export, work faster, etc) – 20 per cent

Marketing and Training

41.9 per cent

Expanded market – 30.8 per cent

Increased sales – 38.5 per cent

Other (improved business skills, expanded export

operations, no response) 30.7 per cent

There are presently not many ventures which support craft producers along the North

Coast Corridor. Based on information from one on one discussions, community visits and focus

groups only a few communities currently have mechanisms in place that fully support craft

production. For example discussions in focus groups show that communities such as Catadupa

have made skills training a major aspect of early education as shown through activities in local 4-

H clubs and annual displays. This although talked about, is quite rare in other communities.

24

Focus groups with Trelawny craft producers had discussions centred on the new trend for carvers

which is the use of the dolomite stone and shell jewellery.

Visits to other communities (Mt Zion – St Ann, Coopers Pen-Trelawny and Cambridge –

St James) show that all out community support to craft production is still in fledgling stages.

More is still required with respect to training, raw material provisions, work environment and

related business support services for such activities. They are recognized and respected in their

respective localities but the multiplier effects of craft production are still low. These arguments

are also supported by the fact that in the survey there was a relatively low level of positive

responses with respect to those craft producers who knew of organizations and or agencies that

assisted craft producers. [Table 3]

2.3 Existing Skills

2.3.1 Craft Related Skills

With respect to the profile of people employed in organizations, the Table below shows skills,

sources and training reported for employees (Quest 15). Note that in many cases employees

have more than one skill.

Table 10: Producer/Employee Skills for Craft Producing Organizations (that employ workers)

Parish Typical Skills Reported Average

Tenure (Yrs)4

Source of Skill/Training Reported

for Employees

St Ann

Carving – 4 organizations (44.44 per

cent of those reporting)

Not yet trained/apprentice – 2 (22.22 per

cent of those reporting)

Leather craft and jewelry - 1

organization (11.1 per cent of those

reporting)

Doll making 1 organization (11.11 per

cent of those reporting)

Painting – 1 organization (11.11 per cent

of those reporting)

10.63

High School/Heart Academy – 2

organizations (28.6 [per cent of

those reporting)

Self-taught/Talent – 3

organizations (42.8 per cent of

those reporting)

Apprenticeship – 2 organizations

(28.6 per cent of those reporting)

Trelawny

Carvers - 63.6 per cent of organizations

Dressmaking and needlecraft – 36.4 per

cent of organizations

8.13

Self-taught/talent – 30 per cent of

organizations reporting

Apprenticeship – 70 per cent of

those reporting

Carving and furniture making – 41.2 per Self-taught/talent – 16.67 per cent

4 It is important to note that these were crude estimates as advised by respondents as many did not recall precisely how long their workers were at their establishment.

25

St James cent of organizations

Dressmaking and needlecraft skills -

Leather craft – 16.6 percent of

organizations

Jewellery – 25 per cent of organizations

Decorative art (e.g. aboriginal art) – 8.3

per cent of organizations

Other (including basket weaving, etc) –

8.3 per cent of organizations

6.75 of those reporting

Apprenticeship/on the job training

– 75.03 per cent

Formal institution – 8.3 per cent

All Parishes

Surveyed

8.42

In addition to existing skills there are situations from the survey where employees

(including the proprietor) required more skills. For those that employ people (Quest. 16) St Ann

craft producers had five (5) respondents (41.3 per cent) who stated that they required more

training at their organization. It is important to note that nine (9) respondents (19.6 per cent) did

not answer this question and 39.1 per cent represented those who stated categorically that they

did not require any further training. The specific skills required (Quest. 17) were; time

management, painting, machinery and symmetric skills and one respondent saying that he

needed nothing specific just anything that provides all round improvement. With respect to any

attempt made to acquire theses skills (Quest 18) only two (2) respondents from St Ann stated that

they took any initiative on this. The challenges that they faced were [a] language barriers and [b]

not finding the right instructors (Quest 19-20).

For Trelawny craft producers (who employ people) fifteen (15) respondents did not

answer this question (62.5 per cent), four (4) respondents (12.5 per cent) stated that their

organizations required more training while five (5) respondents (20.8 per cent) stated

categorically that they did not require any training. The required training was centred on: [1]

design training, [2] carving techniques, [3] leather craft, [4] marketing and [5] jewellery making.

One respondent stated that training was sought but the availability of machinery and/or

equipment to train with was a problem.

For St James twenty (20) respondents (64.5 per cent) did not give a response to this

question while nine (9) respondents (25.8 per cent) stated categorically that their organization

required additional training. One (1) respondent categorically stated that no training was

required. For the nine (9) who stated that they needed training in their organizations this

26

included: [1] detailed operations on operating respective machinery (2 responses), [2] systems

operations, [3] ice carving, [4] management marketing and customer relations (3 responses), [5]

internet sales. Two (2) respondents stated that they made attempts to acquire these skills and

both stated that they experienced challenges. These challenges were: [1] skills were not readily

available and [2] being nervous at the last opportunity to train.

With respect to the skills profile of organizations that do not employ people (Quest. 21)

details are shown in Table below. Note that some owner/proprietors have more than one craft

skill.

Table 11: Producer/Employee Skills for Craft Producing Organizations (that do not employ workers)

Parish Craft Skills Reported Source of Craft

Skill/Training

Reported for

Employees

Non Craft Training

Skills Reported

Method of Access

for Skills

St. Ann

Carving – 42.5 per

cent

Needlecraft and

sewing – 17.5 per cent

Bracelet and jewellery

making – 30 per cent

Other (e.g. painting

and doll making) – 10

per cent

Self-taught/talent

– 42.1 per cent

Formal training at

an institution –

32.68 per cent

Apprenticeship/on

the job training –

22.25 per cent

Construction

related trades –

33.33 percent

Secretarial and

sales – 22.22 per

cent

Housekeeping –

11.11 per cent

Other (e.g. spear

fishing, cake

decorating,

gardening etc) –

33.33 per cent

Enlisted in a

course – 31.25

per cent

Observation/Self

Visualization –

34.85. per cent

At the workplace

– 34.85 per cent

Trelawny

Carving – 61.5 per

cent

Needlecraft and

sewing – 23.1 per cent

Bracelet and

Jewellery making –

15.4 per cent

Self-taught/talent

– 58.33 per cent

Formal training at

an institution –

8.34

Apprenticeship –

33. 33 per cent

1 person –

domestic helper

Enlisted in a

course – 20 per

cent

Observation/Self

Visualization –

20 per cent

At the workplace

– 60 per cent

St. James

Carving – 30 per cent

Weaving and basket

making – 20 per cent

Needlecraft – 20 per

cent

Painting and

decorative art – 15 per

cent

Other – 15 per cent

Apprenticeship –

47.3 per cent

Self-taught/talent

– 31.57 per cent

Formal training –

21.13 percent

1 person

bartending

1 person

business classes

Carpentry

Enrolled in an

institution –

15.80 per cent

Observation/self-

visualization –

68.40

At the workplace

– 15.80 per cent

27

When organizations who hired no employees (other than owner/proprietor) were

questioned with respect to current skill and training requirements (Quest. 22) the results varied

by parish. For St Ann organizations twenty (20) respondents stated that they required training

(43.5 per cent) while seventeen (17) respondents (37 per cent) stated that they required no

training. Altogether nine (9) respondents (19.5 per cent) did not give a reply. With respect to

the type of training required (Quest. 23) these are shown in Table below.

Table 12: Frequency Table for Skills Required in the Parish of St Ann

Training

Required

Needlecraft

/Sewing

Art/Painting Wood

Carving/Finishing

Jewellery

Making/Basket

Weaving

Business

Training/Computing

Other

Training

Frequency

(No.)

9

2

2

3

3

1

Five (5) respondents from this parish stated that they sought to acquire the skills/training that

they needed while fifteen (15) said that they did not seek to acquire such skills (Quest 24).

There were seven (7) respondents (29.2 per cent) who stated that they required training

for their organization in Trelawny. Four (4) respondents stated that they did not require any

training (16.67 per cent) while one organization stated that it did not know/was not sure (4.2 per

cent). There were eleven (11) respondents who did not provide an answer to this question from

this parish (45.8 per cent).

Table 13: Frequency Table for Skills Required in the Parish of Trelawny

Training Required Art/Painting Leather and Mat making Jewellery Making/Basket

Weaving

Frequency (No.)

2

1

2

For Trelawny only one (1) respondent sought the training required. The major challenge faced

was that of unavailability of machinery to train workers (Quest 24).

For St James respondents ten (10) stated that they required more skills training (32.3 per

cent), ten (10) also stated that they did not require any training or skill requirement. Note also

that ten (10) did not provide an answer to this question. Five respondents (5) stated that they had

28

made attempts to acquire these skills and of these one (1) stated the challenges experienced was

that of improper tutoring. The frequency of skills required is shown in Table below.

Table 14: Frequency Table for Skills Required in the Parish of St James

Training

Required

Management and

Marketing

Weaving

and

Furniture

Making

Knitting

Machine

Potter/Wire

Art

Better

Finishing

Training

Music

Frequency

(No.)

5

1

1

1

1

1

There are numerous craft production skills which were picked up via the field survey

questionnaire. The dominant reported skills were wood carvings, knitting and related

needlecraft, doll making jewellery, leather specialists and miscellaneous items ( e.g. making of

key chains, refrigerator magnets etc)

2.3.2 Other Skills

Site visits and focus group discussions show that some craft producers have other support

jobs which are typically low paying in the sectors such as agriculture and fisheries, construction

trades and the hospitality industry. For St Ann 39.1 per cent of respondents stated that they had a

non-craft skill or training, for Trelawny respondents this figure was 4.1 per cent and St James

16.5 per cent.

It is also important to note that as reported from focus groups there are other non-craft

skills required especially to operate the organization. These are inclusive of being high risk

takers, an acumen for business, having mental toughness, discipline and the ability to negotiate

plan and organize.

29

2.4 Products and Production Processes

2.4.1 Types of Products

Examination of products (Quest. 27) show that there are at least five or six major product areas

with many craft producers doing more than one type of product. This is shown in Table below.

Table 15: Craft Items by Product Group

PRODUCT GROUP TYPICAL SUB PRODUCTS FREQUENCY (from

Questionnaire Interview)

Carvings Wood carvings

Stonework

38

Dolls Pencil dolls

Reggae dolls

Animated dolls

10

Needle Craft t-shirts

swimwear,

dresses

crochet

knitted headwear

bags

34

Jewellery Bracelets

Organic jewellery

Earrings

Anklets

23

Leather Items Leather and leatherette products 7

Miscellaneous Items Key chains

Coins

Basket weaving

Paintings

6

For craft producers in the parish of St Ann the typical product profiles (Quest 27) are shown in

Table below.

Table 16: Product Profile of Craft in the Parish of St Ann

Product Typical Raw Materials

Used

Location of Raw

Material

Supplier/Source of

Raw Material

Average/Typical

Prices Per Unit

(J$)

Carvings –

40 per cent

of St Ann

Craft

Producers

Wood/Lumber - 79 per

cent of respondents who

do carving)

Bamboo – 21 per cent of

respondents who do

carving)

Additives and Finishing’s

(Sandpaper lacquer,

Wood/Lumber/bamboo

Not easy to access

– 15.7 per cent.

easy to access –

84.3 per cent

Additives and Finishing

100 per cent easy

to access locally

Deep rural

farmers

Lumberyards in

and around Ocho

Rios

Local hardware

stores (e.g. Ocho

Rios)

Trees – $12,200.00

ea

Cut Lumber –

$125/ft

Bamboo – no cost

Sandpaper –

$120/ft

30

thinner, sealer) – 10 per

cent of respondents

reported this overall

Lacquer – $200

per bottle

Dolls –

21.7 per

cent of St

Ann Craft

Producers

Wool – 71.4 per cent of

respondents (who do

dolls)

Thread5 – (28.5 per cent )

Pencil – 57.1 per cent of

all respondents who do

dolls

Sponge – 14.3 per cent of

respondents who do dolls

Cloth/material – 85.71

per cent of respondents6

Beads – 71.4 per cent of

respondents who do dolls

All respondents stated

that materials are easy

to access (in and around

Ocho Rios). Only one

respondent (14.3 per

cent) imports (material

only).

Local hardwares and

haberdasheries (Ocho

Rios) and imported.

Wool – $ 675/yd

Thread - $686.67

per roll7

Pencil - $100 per

dozen

Sponge/Stuffing -

$200/lb

Material -

$232.85/yd

Beads - $550 per

bag

Needle

Craft –

21.7 per

cent of

craft

producers

in St Ann

Material/Fabric – (44.44

per cent of respondents

who do needlecraft)

Needles – 33.33 per cent 8

Thread – 88.88 per cent9

Wool – 55.55 per cent of

respondents who do

needlecraft

Zippers – 11.11 per cent

of respondents who do

needlecraft

All located and easy to

access in Ocho Rios.

Only 22.22 per cent of

respondents imported

fabric

Ocho Rios shops and

haberdasheries

Imported from

overseas suppliers

Needles - $400 per

pack or 50 each

Thread - $725.00

per roll

Wool – $537.50 per

yard

Zippers – $150 per

dozen

Jewellery –

34.8 per

cent of

craft

producers

in St Ann

Wire/fish line- 42.8 per

cent of those who do

jewellery

Earring sticks – 7.1 per

cent

Shells and cow horn –

21.4 per cent

33.33 per cent of

respondents stated that

they had to import

goods from overseas

(e.g. beads wire fittings

and stones)

All other respondents

state that raw materials

are easy to access

Ocho Rios

Overseas (e.g.

Panama)

Wire/Fish Line -

$140 per roll10

Shells - $300 per

bag

Cow Horn - $500

per bag

5 May be underreported based on the fact that all dolls seen were sewn. 6 May be underreported as all dolls need materials 7 Thread has high variations ranging from $160 per roll to $1500 per roll. It is assumed that this is dependent on type and quality. 8 May be underreported and must be assumed to be 100 per cent 9 Must be assumed under reported 10 Ranges from $50-$310.00

31

Beads - 85.7 per cent

Stones – 16.67 per cent

locally

Beads - $100/ string

or $600 per bag

(US5.00 for bagel

beads)

Stones – $250 per

string or $50 per bag

Leather

Items – 4.3

per cent of

all St Ann

producers

Leather and Leatherette –

all respondents

Not easy to access (2

respondents)

Sometimes imported

(2 respondents)

No price given

Paintings –

6.5 per

cent of

producers

in St Ann

Paint /Brushes/Canvas –

used by all respondents

Easy to access locally

Haberdasheries in

Ocho Rios

Canvas - $350 per

yard

Brushes – $450/pk

Paint - $600 per

Tube/$2000 per

gallon

For craft producers in the parish of Trelawny the product profiles are shown in Table below.

Table 17: Product Profile of Craft in the Parish of Trelawny

Product Typical Raw

Materials Used

Location of Raw

Material

Supplier/Source of

Raw Material

Average/Typical

Prices Per Unit

(J$)

Carvings – 66.66 per

cent of all craft

producers in

Trelawny

Wood - 77.8 per cent

of all respondents

doing carvings

Stone – 5.6 per cent

of all respondents

doing carvings

Marine Artefacts –

5.6 per cent of all

respondents doing

carvings

Bamboo/Calabash,etc

– 5.6 per cent of all

respondents doing

carvings11

Additives and

Finishes – 61.11 per

cent of all carvers

62.3 per cent of

wood carvers say

wood is hard to

access (outside of

parish or deep rural

Trelawny)

Stone – seas and

mountains (not hard

to access)

Bamboo/Calabash –

easy to access

Wood – hills of

Trelawny and other

parishes,

lumberyards

Wood – $8,593.75

per tree

Calabash – $1500

ea

Bamboo – $500 ea

Sandpaper -

$120/ft

Lacquer –

$135/quart

Polish – $50 ea

1111 One person here also does basket weaving in addition to carving.

32

Needlecraft/Clothing

– 25 per cent of

producers in

Trelawny

Thread – all

respondents doing

needlecraft

Wool – 40 per cent of

all respondents doing

needlecraft

Material – 20 per cent

of needle craft

workers

Needles – mentioned

by one person

(underreported)

Only 20 per cent of

respondents stated

that some items were

not always easy to

locate (belt buckle

and wool

sometimes)

Local stores

(Montego Bay)

Kingston Stores

Material – $380/yd

Wool - $328.33

per roll

Thread – $400/roll

Jewellery – 20.8 per

cent of craft

producers

Beads – 50 per cent

of respondents doing

jewellery products

Stones - 16.67 per

cent of jewellery

producers

Lines and latches –

16.67 per cent of

jewellery producers

(may be

underreported)

All raw materials

easy to access most

of the time

Local stores in and

around the parish

and Montego Bay

Beads – $200/pk

Stones - no cost

Hooks and Latches

– $120 ea

Misc. e.g. Leather

Products - 4.2 per

cent of respondents

Leatherette – all

respondents (only one

respondent)

Easy to access in and

around the areas

Fabric stores

Leatherette -

$375/yd

For craft producers in the parish of St James the typical product profiles are shown in Table

below

Table 18: Product Profile of Craft in the Parish of St James

Product Typical Raw

Materials Used

Location of Raw

Material

Supplier/Source of

Raw Material

Average/Typical

Prices Per Unit (J$)

Carvings and

Woodwork – 25.8

per cent of

respondents from St

James

Wood – all

respondents doing

carvings

Additives and

Finishes – 8.3 per

cent of all carvers

(may be

underreported)

41.7 per cent of

respondents state

that wood is not

easily accessible.

Carpentry and

hardware stores in

Montego Bay and

environs.

Tree - $11,500 ea

Wood – $130/ft

Varnish - $700/qt

Sandpaper – $130/ft

Glue – $130/qt

33

Needlecraft/Clothing

/Dolls – 35.5 per

cent of respondents

from St James

Wool – 66.66 per

cent of those in

needlecraft

Material (cloth,

burlap, raffia)- 50

per cent of those in

needlecraft

Thread – 75 per cent

of those in

needlecraft (may be

underreported)

Needles – 16.67 per

cent of respondents

in needlecraft (may

be underreported)

Raw materials in and

around the parish

easy to access for all

respondents (only

acrylic sometimes

not easy)

Local shops and

haberdasheries

Burlap – 100/yd

Wool - $687.50/roll

Thread - $283.33

Material - $275/yd

Needles – $50/pk

Raffia - $90/bundle

Paint – $500/tube

Jewellery – 12.5 per

cent of respondents

Organic materials

(e.g. goat skin, cow

hides, horns etc) –

20 per cent of all

jewellers

Stones – 20 per cent

of all jewellers

Beads – 60 per cent

of all jewellers

80 per cent of

respondents state

that materials easy to

access in and around

the parish. Polish

has to be imported

for organic jewellery

Butchers,

haberdasheries,

other local shops.

Goat skin - $600/lb

Cow hide - $700/lb

Cow horn - $1000

per bag

Seashells - $1500

per bag

Beads -100 per bag

Souvenir Items (e.g.

magnets, key rings

etc) – 12.5 per cent

of respondents

Coconut Shells – all

respondents in

souvenir items

Rings – 66 per cent

of all respondents

use ring

Magnets – 33 per

cent use magnets

Additive and

Finishes – 66 per

cent use additives

and finishes (may be

underreported)

33 per cent report

that magnets are

hard to get locally

otherwise other

materials are easy to

access

Hardware stores and

related shops in

Montego bay

Coconut shells -

$200/bag

Paint – $500/tube

Rings – $1000/100

Labels - $1/ea

Leather craft – 12.5

per cent of

respondents

Animal hides – all

respondents

Additives and

Finishes – all

respondents

50 per cent of

respondents state

that leather and

polish is not easy to

access.

Local farmers

Overseas

Animal hide –$

650/lb

34

Decorative Baskets

and Art – 25 percent

of respondents.

Straw – 60 per cent

of respondents

Zip and lining – 20

per cent of

respondents

Additives and

finishes – 40 per

cent of respondents

Canvas – 20 per cent

of respondents

All easy to access

and available in

parish

Carpentry stores,

local hardwares and

haberdasheries

Canvas - $500/yd

Acrylic – $500/tube

Straw –

$2000/bundle

Zips – $150/doz

Focus group discussions with respect to products raised the issue of quality and the

dominant responses were centred on the fact that producers do not think that local craft is being

produced to an international standard. They actually require that some basic standards be set in

the sector with more prominent roles for organizations such as Things Jamaican and also the

Edna Manley School for the Arts especially in appraisal and quality control. They also suggest

the need for exchange programmes (including alliances with overseas partners) and more

research and development in the craft producing sector

It was also stated that there is the need for more prominent use of indigenous materials

and assistance in patents and property rights to protect local art and craft. Training must also be

directed at craft producers with respect to areas project and product management and the proper

use of machinery.

2.4.2 Details of Operations

Based on data gathered from the field interviewer survey, the typical craft producing

organization has on average been in operation for approximately 20 years – which is roughly half

the life of the owner; who in many cases started the firm on his/her own. With respect to years

in operations (Quest. 9) there were some producers who did not respond to this as in some cases

they could not remember precisely. For St Ann ten (10) respondents (22 per cent) could not

precisely state for how long they were in operation. For Trelawny there were two (8 per cent)

such respondents and for St James one respondent (3 per cent) could not recall the length of time

of operations.

35

Table 19: Years in Operation for the Typical Craft Producing Organization

Parish Avg. (Mean) Years in

Operation

Mode Median Min Max

St Ann

20.2

10

22.5

0.3

38

Trelawny

21.2

30

19.5

2

43

St James

19.7

20

20

3

37

All Parishes Surveyed

20.2

25

20.5

0.3

43

Discussions (i.e. direct interviews, focus groups and community discussions) also show that the

typical operations are strongly related to those of micro-enterprises i.e.

Working Hours - Craft producers state in discussions that their typical working hours vary.

For those who do unfinished products and sell to craft vendors their working hours are

dependent on orders and also seasonality (i.e. high and low tourist seasons). For those who

make craft and sell in the craft markets (and other retail outlets) the working hours are more

regular as (evidenced by visits) some arrive even before 7:00 am to prepare for a typical

working day.

Small tools and low levels of mechanization and automation – operations are highly labour

intensive where in most cases more than half the work is done by hand

Sharing of equipment – there are cases where equipment has to be shared

Distribution Chain – the distribution chain in most cases seem to be dependent on public

transport as numerous producers state that do not have personal transport.

It is important to note that technical operations vary according to the type of craft being

produced. Each product has various steps but generally speaking there are universal steps in the

process that can be identified. These include the formulation of a concept, the acquisition of the

necessary materials, initial creations, finishing work, packaging and sales. Simplified steps for

three (3) various craft/skills are shown below in Figures 1-3:

36

CONCEPT/

VISUALIZATION

ACCESS RAW

MATERIAL (e.g.

Wood)

CARVE WOOD

TO REQUIRED

SPECIFICATIONS

SAND

PRIME

SEAL

COLOUR AND

DECORATE

PACKAGE AND

DISPLAY