Final project dabur

43

Session 2012-13 CONTENTS Sl. No. Topics Pg. No. 1. Introduction 2 2. Objectives of the Study 3 3. Research Design of the Study 4 4. Methodology 4 5. Tools used for Analysis of Financial Statements 4 6. Limitation of the Study 5 7. Company Profile 6 8. Financial Statements Analysis 9-20 9. Ratio Analysis 21 10. Findings (Interpretation) 23 11. Suggestions 24 12. Conclusion 25 13. References 1 | Page Roll No.: 68203U09038

-

Upload

ashis-mohapatra -

Category

Education

-

view

238 -

download

5

Transcript of Final project dabur

Session 2012-13

CONTENTS

Sl. No. Topics Pg. No.

1. Introduction 2

2. Objectives of the Study 3

3. Research Design of the Study 4

4. Methodology 4

5. Tools used for Analysis of Financial Statements 4

6. Limitation of the Study 5

7. Company Profile 6

8. Financial Statements Analysis 9-20

9. Ratio Analysis 21

10.Findings (Interpretation) 23

11.Suggestions 24

12.Conclusion 25

13.References

1 | P a g e Roll No.: 68203U09038

Session 2012-13

INTRODUCTION

Financial analysis is the starting point for making plans, before using any

sophisticated forecasting and planning procedures. Understanding the past is a

prerequisite for anticipating the future. Financial analysis is the process of

identifying the financial strength and weakness of the firm by properly

establishing relationship between the items of the balance sheet and the profit

and loss account. Financial analysis can be undertaken by management of the

firm, or by parties outside the firm, viz. owners, creditors, investors and others.

The nature of analysis will differ depending on the purpose of the analyst.

The story of Dabur began with a small, but visionary endeavour by Dr. S. K.

Burman, a physician tucked away in Bengal. His mission was to provide effective

and affordable cure for ordinary people in far-flung villages. With missionary

zeal and fervour, Dr. Burman undertook the task of preparing natural cures for

the killer diseases of those days, like cholera, malaria and plague.

Soon the news of his medicines traveled, and he came to be known as the trusted

'Daktar' or Doctor who came up with effective cures. And that is how his venture

Dabur got its name - derived from the Devanagri rendition of Daktar Burman.

Dr. Burman set up Dabur in 1884 to produce and dispense Ayurvedic medicines.

Reaching out to a wide mass of people who had no access to proper treatment.

Dr. S. K. Burman's commitment and ceaseless efforts resulted in the company

growing from a fledgling medicine manufacturer in a small Calcutta house, to a

household name that at once evokes trust and reliability.

2 | P a g e Roll No.: 68203U09038

Session 2012-13

OBJECTIVES TO THE STUDY

The objectives of the study are to evaluate the financial position and

performance of the “TATA Consultancy Services” The purpose of the study

aims at a critical analysis of the financial statements of the Company. And makes

attempt to get better insight about the financial strength and weakness of the

organisation by analyzing and interpreting the data for a period of 2 years i.e.

2010 and 2011.

To study the financial performance of “TATA Consultancy Services”.

To determine the profitability or earning capacity of the concern

To analyze the strength and weakness of the organisation on the basis of its

financial position.

To suggest solution, if any, to the unfavorable financial conditions and

financial performance.

To act of analysis may also reveal areas where control is deficit and

desirable for the efficient operating of the organisation which in turn

help to achieve organizational goals.

To know the solvency of the company.

To make comparative study with other year performance.

To know the capability of payment of dividend and interest.

To know the profitability of the company in the form of ratios

3 | P a g e Roll No.: 68203U09038

Session 2012-13

RESEARCH DESIGN OF THE STUDY

Research design means a search of facts, answers to question and solution

to the problems. It is a prospective investigation. Research is a systematical

logical study of an issue or problem through scientific method. It is a

systematic and objective analysis and recording of controlled observation that

may lead to the development of generalization, principles, resulting in

prediction ultimate control of events.

Research design is the arrangement of conditions for the collection and

analysis of data in manner that aims to combine relevance to the research

purpose with relevance to economy. There are various designs, which are

descriptive and helpful for analytical research.

METHODOLOGY

Sources of data can be classified into two groups they are:

Primary data and

Secondary data

In this project all the data are analyzed on the basis of secondary data.

Secondary Sources:

The investigation relied on books, documents, annual report, financial

assessments, literature, files and personal observation to have an idea about

the organizational set up, functions of financial department and other groups.

4 | P a g e Roll No.: 68203U09038

Session 2012-13

TOOLS USED FOR ANALYSIS OF FINANCIAL STATEMENTS:

The numbers given in the financial statement are not of much use to the

decision maker. These numbers are to be analysed over a period of time or

relation to other numbers so that significant conclusions could be drawn

regarding the strengths and weakness of a business enterprise. The tools of

financial analysis help in this regard. These tools include:

Comparative Statements;Common-size Statements;Comparative Balance Sheet;Common Size Balance Sheet;Ratio Analysis;Cash flow Statements;Changes in Financial Position.

In this project we show or discuss:

1. Profit & Loss Account

2. Balance Sheet

3. Comparative Statements.

4. Common-Size Statements &

5. Comparative Balance Sheet;

6. Common Size Balance Sheet;

7. Ratio Analysis of financial statement of “TATA Consultancy Services”

Limitation of the Study:

Every work has its own limitation. During the process of conducting the

research study the following limitations may be faced:-

Due to insufficient time I have analyzed only two years financial

analysis of this company.

Statistical tools used limits the testing and findings

Findings are general.

Due to non-availability of sufficient time and money a detailed study

could not be made.

5 | P a g e Roll No.: 68203U09038

Session 2012-13

COMPANY PROFILE

Tata Consultancy Services started in 1968. Mr.F.C Kohli who is presently the

Deputy Chairman was entrusted with the job of steering TCS. The early days

marked TCS resonsibility in managing the punch card operations of Tisco. The

company, which was into management consultancy from day one, soon felt the

need to provide solutions to its clients as well.TCS was the first Indian company

to make forays into the US market with clients ranging from IBM, American

Express, Sega etc. TCS is presently the top software services firm in Asia.

During the Y2K buildup, TCS had setup a Y2Kfactory in Chennai as a short-term

strategy. Now, with E-business being the buzzword, the factory is developing

solutions for the dotcom industries. Today, about 90 percent of TCS' revenue

comes from consulting, while the rest from products. TCS has great training

facilities. In addition to training around 5 percent of the revenue is spent upon its

R&D centres like the Tata Research Design and Development Centre at Pune,

along with a host of other centres at Mumbai and Hyderabad.

It benchmarked its quality standing, invested heavily in software engineering

practices and built intellectual property-in terms of patents,code and branded

products. At the same time, it expanded its relationships with technology

partners and organisations, increased linkages with academic institutions and

incubated technologies and ideas of people within TCS and outside. TCS has

already patented 12 E-Commerce solution product packages and has filed six

more applications for patent licences.

Over $25 million were spent on enhancing hardware and software infrastructure.

The company now has 72 offices worldwide. As many as seven centres were

assessed at SEI CMM Level 5 last year(3.4 mistakes in a million

oppurtunities).These include Chennai, Mumbai, Bangalore, Calcutta, Hyderabad

and Lucknow.Several business and R&D relationship with global firms like IBM,

General Electric, Unigraphics Solutions have been made.

6 | P a g e Roll No.: 68203U09038

Session 2012-13

The present CEO of the company is Mr.S.Ramadorai. The companies strength is

about 14,000.

Tata Consultancy Services Limited (TCS) is engaged in providing information

technology (IT) services, business solutions and outsourcing. The Company’s

services portfolio consists of application development and maintenance, business

intelligence, enterprise solutions, assurance, engineering and industrial services,

IT infrastructure services, business process outsourcing, consulting and asset

leveraged solutions. TCS also services several other industries, such as life

sciences and healthcare, hi-tech, energy, resources and utilities, media and

entertainment and travel, transportation and hospitality. On August 31, 2010,

Diligenta Limited acquired Unisys Insurance Services Limited (UISL). On October

4, 2010, Tata America International Corporation acquired MS CJV Investments

Corporation. On October 8, 2010, the Company acquired SUPERVALU Services

India Private Limited.

History

1968 to 2000

Tata Consultancy Services (TCS) was founded in 1968. Its early contracts

included providing punched card services to sister company TISCO

(now Tata Steel), working on an Inter-Branch Reconciliation System for

the Central Bank of India, and providing bureau services to Unit Trust of

India.

In 1975, TCS conducted its first campus interviews, held at IISc, Bangalore.

The recruits comprised 12 Indian Institutes of Technology graduates and

three IISc graduates, who became the first TCS employees to enter a

formal graduate trainee programme.

In 1979, TCS delivered an electronic depository and trading system called

SECOM for the Swiss company SIS SegaInterSettle. TCS followed this up

with System X for the Canadian Depository System and automating

7 | P a g e Roll No.: 68203U09038

Session 2012-13

the Johannesburg Stock Exchange. TCS associated with a Swiss partner,

TKS Teknosoft, which it later acquired.

In 1981, TCS established India's first dedicated software research and

development center, the Tata Research Development and Design Center

(TRDDC) in Pune. In 1985 TCS established India's first client-dedicated

offshore development center, set up for client Tandem.

In the early 1990s the Indian IT outsourcing industry grew rapidly due to

the Y2K bug and the launch of a unified European currency, Euro. TCS

created the factory model for Y2K conversion and developed software

tools which automated the conversion process and enabled third-party

developer and client implementation.

2000 to present

By 2004, TCS's e-business activities were generating over US$500 million

in annual revenues.

On 25 August 2004 TCS became a publicly listed company.

In 2005 TCS became the first India-based IT services company to enter

the bioinformatics market.

In 2006 TCS designed an ERP system for the Indian Railway Catering and

Tourism Corporation.

In 2008 TCS undertook an internal restructuring exercise which aimed to

increase the company's agility.

TCS entered the small and medium enterprises market for the first time in

2011, with cloud-based offerings. On the last trading day of 2011, TCS

overtook RIL to achieve the highest market capitalisation of any India-

based company.

In the 2011/12 fiscal year TCS achieved annual revenues of over U$10

billion for the first time.

8 | P a g e Roll No.: 68203U09038

Session 2012-13

Full Services Portfolio

Our full services portfolio enables us to provide integrated solutions that help

you recognize value quickly by reducing costs and improving business agility.

Our full services portfolio combines traditional IT and Remote Infrastructure

services with knowledge-based services such as Consulting and Business Process

Outsourcing. The efficiency and seamlessness of our engagements makes TCS an

excellent partner to companies looking for an integrated approach to managing

all IT and operational programs.

Our intellectual property—from software products, to technology and business

components, to service and process frameworks—is the culmination of our

business knowledge, technology excellence and process innovation and helps

transform businesses around the world.

Industry specific software products in Banking and Financial

Services, Insurance, Retail,Healthcare, Telecom, Government and High

Tech sectors provide our customers with a competitive edge. Our library of

Technology and Domain components enable us to build high quality solutions

and bring them to market faster. Our service and process frameworks improve

operational efficiencies and business agility.

Corporate Facts

Who We Are: Tata Consultancy Services is an IT services, business solutions and

outsourcing organization that delivers real results to global businesses, ensuring

a level of certainty that no other firm can match.

What We Offer: TCS offers a consulting-led integrated portfolio of IT and IT-

enabled services delivered through its unique Global Network Delivery Model™

(GNDM™), recognized as the benchmark of excellence in software development.

Lineage: TCS is part of the Tata group, one of India’s largest industrial

conglomerates and most respected brands.

9 | P a g e Roll No.: 68203U09038

Session 2012-13

History: TCS was established in 1968 as a division of Tata Sons Limited. TCS Ltd.

got incorporated as a separate entity on January 19, 1995.

Mission: To help customers achieve their business objectives by providing

innovative, best-in-class consulting, IT solutions and services. To make it a joy for

all stakeholders to work with us.

Values: Leading change, Integrity, Respect for the individual, Excellence,

Learning and sharing.

Workforce: TCS has over 254,000 of the world’s best-trained IT consultants

in 44 countries.

Full Services Portfolio: Application Development and Maintenance, Business

Intelligence,Enterprise Solutions, Assurance Services, Engineering and Industrial

Services, IT Infrastructure Services, Business Process

Outsourcing, Consulting and Asset Leveraged Solutions. Newer services

include Mobility, Connected Marketing, Social Computing, Big Data and Cloud.

Industries Serviced: Banking, Financial Services and Insurance, Retail and

Consumer Packaged Goods, Telecom, Media and Information Services, High

Tech, Manufacturing, Life Sciences and Healthcare, Energy, Resources and

Utilities, and Travel, Transportation and Hospitality.

Financial Information: Revenue of $10.17 billion, up 24.2% over prior year;

operating margin of 27.6% and net income margin of 21.8% (fiscal year ending

March 31, 2012). For detailed financial information quarterly statements, annual

reports and operating metrics, visit the Financial Information page.

Stock Symbols

NSE (National Stock Exchange of India): TCS

BSE (Bombay Stock Exchange of India): 532540

Quality Framework: We are the world’s first organization to achieve an

enterprise-wide Maturity Level 5 on CMMI® and P-CMM® based on SCAMPISM,

the most rigorous assessment methodology.

10 | P a g e Roll No.: 68203U09038

Session 2012-13

TCS Integrated Quality Management System (iQMS) integrates processes,

people and technology maturity through various established frameworks and

practices, including IEEE, ISO 9001: 2000, CMMi, SW-CMM, P-CMM and Six-

Sigma.

Board of Directors: TCS has 11 non-executive and two executive board

members.

Leadership Team:

N Chandrasekaran, Chief Executive Officer and Managing Director

S Mahalingam, Chief Financial Officer and Executive Director

The TCS Advantage: Features like TCS’ GNDM™, Customer-centric Engagement

Model, Full Services Portfolio, and Innovation Labs and Co-innovation Network

(COIN™) set us apart. Read more about the TCS advantage here.

Alliances: TCS has a strong network of strategic and solution partners with a

joint objective of helping its customers become high-performance businesses by

maximizing the value of their technology investments. Visit TCS’ Global Alliances.

Subsidiaries: TCS has 58 subsidiaries.

11 | P a g e Roll No.: 68203U09038

Session 2012-13

12 | P a g e Roll No.: 68203U09038

Session 2012-13

COMPARATIVE STATEMENT:

It refers to the comparison of financial statements of an enterprise for two

consecutive periods. It measures the efforts of the farm by giving a clear sight of the

performance.

Comparative statements are of two types.

Comparative Income Statement

Comparative Balance Sheet.

The comparative income statements.

The comparative income statements reflect the operating activities of the

business where as the comparative. Balance Sheet reflects the finance & investing

activities of the enterprise. In such statement the figures are shown as.

1) In terms of absolute monetary value.

2) Increase/Decrease in absolute value.

3) Proportionate changes by way of Percentage.

13 | P a g e Roll No.: 68203U09038

Session 2012-13

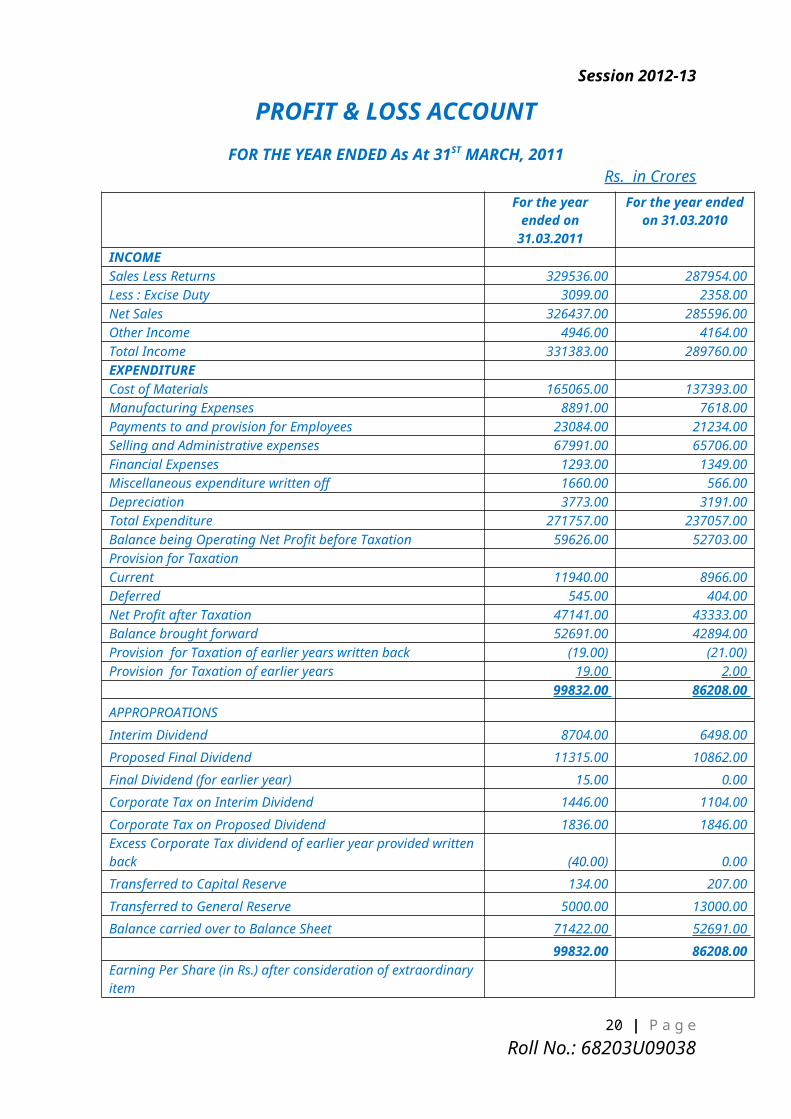

PROFIT & LOSS ACCOUNTFOR THE YEAR ENDED As At 31ST MARCH, 2011

Rs. in CroresFor the year ended

on 31.03.2011For the year ended

on 31.03.2010INCOMESales Less Returns 329536.00 287954.00 Less : Excise Duty 3099.00 2358.00 Net Sales 326437.00 285596.00 Other Income 4946.00 4164.00 Total Income 331383.00 289760.00 EXPENDITURECost of Materials 165065.00 137393.00 Manufacturing Expenses 8891.00 7618.00 Payments to and provision for Employees 23084.00 21234.00 Selling and Administrative expenses 67991.00 65706.00 Financial Expenses 1293.00 1349.00 Miscellaneous expenditure written off 1660.00 566.00 Depreciation 3773.00 3191.00 Total Expenditure 271757.00 237057.00 Balance being Operating Net Profit before Taxation 59626.00 52703.00 Provision for TaxationCurrent 11940.00 8966.00 Deferred 545.00 404.00 Net Profit after Taxation 47141.00 43333.00 Balance brought forward 52691.00 42894.00 Provision for Taxation of earlier years written back (19.00) (21.00)Provision for Taxation of earlier years 19.00 2.00

99832.00 86208.00

APPROPROATIONS

Interim Dividend 8704.00 6498.00

Proposed Final Dividend 11315.00 10862.00

Final Dividend (for earlier year) 15.00 0.00

Corporate Tax on Interim Dividend 1446.00 1104.00

Corporate Tax on Proposed Dividend 1836.00 1846.00 Excess Corporate Tax dividend of earlier year provided written back (40.00) 0.00

Transferred to Capital Reserve 134.00 207.00

Transferred to General Reserve 5000.00 13000.00

Balance carried over to Balance Sheet 71422.00 52691.00

99832.00 86208.00 Earning Per Share (in Rs.) after consideration of extraordinary item

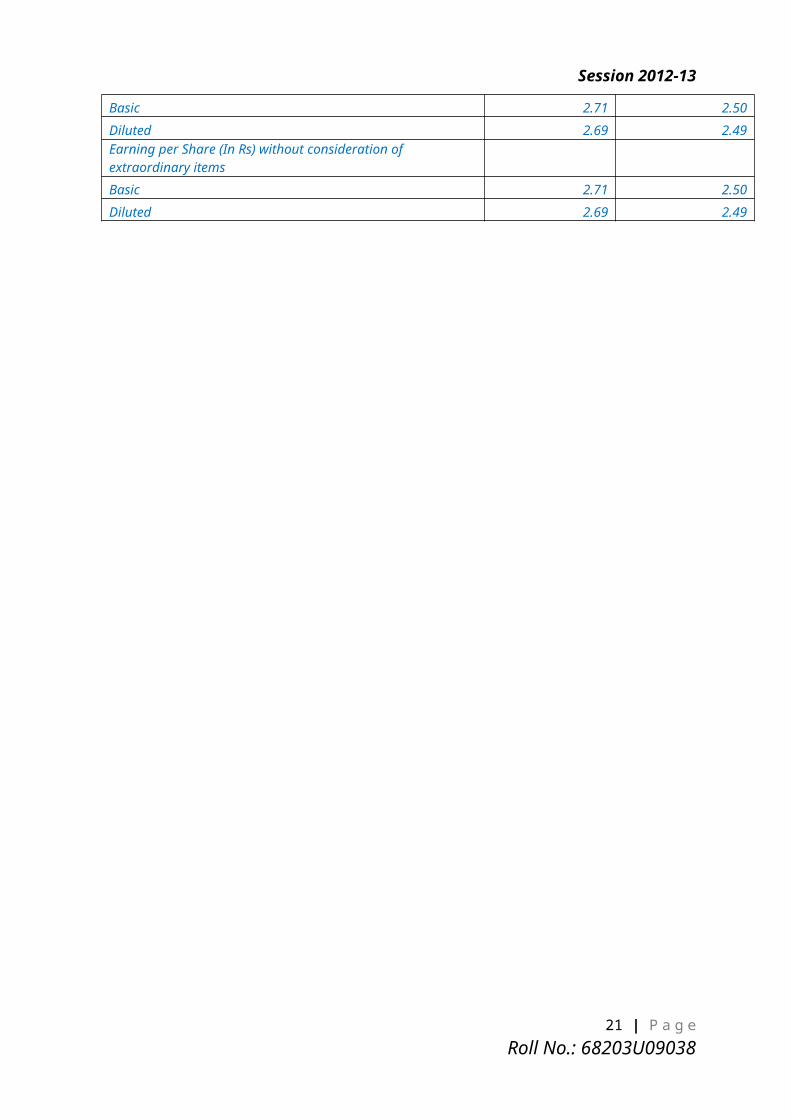

Basic 2.71 2.50

Diluted 2.69 2.49 Earning per Share (In Rs) without consideration of extraordinary items

Basic 2.71 2.50

Diluted 2.69 2.49

14 | P a g e Roll No.: 68203U09038

Session 2012-13

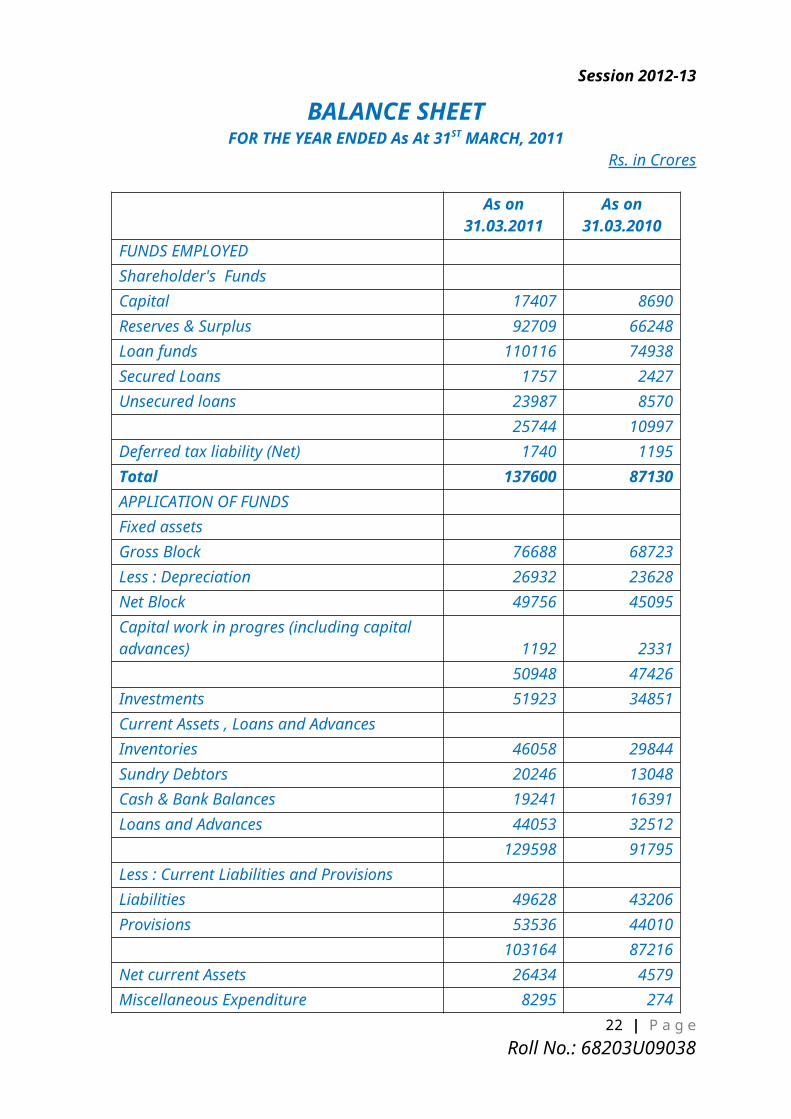

BALANCE SHEETFOR THE YEAR ENDED As At 31ST MARCH, 2011

Rs. in Crores

As on 31.03.2011

As on 31.03.2010

FUNDS EMPLOYEDShareholder's FundsCapital 17407 8690Reserves & Surplus 92709 66248Loan funds 110116 74938Secured Loans 1757 2427Unsecured loans 23987 8570

25744 10997Deferred tax liability (Net) 1740 1195Total 137600 87130APPLICATION OF FUNDSFixed assetsGross Block 76688 68723Less : Depreciation 26932 23628Net Block 49756 45095Capital work in progres (including capital advances) 1192 2331

50948 47426Investments 51923 34851Current Assets , Loans and AdvancesInventories 46058 29844Sundry Debtors 20246 13048Cash & Bank Balances 19241 16391Loans and Advances 44053 32512

129598 91795Less : Current Liabilities and ProvisionsLiabilities 49628 43206Provisions 53536 44010

103164 87216Net current Assets 26434 4579Miscellaneous Expenditure 8295 274Total 137600 87130

15 | P a g e Roll No.: 68203U09038

Session 2012-13

COMPARATIVE INCOME STATEMENT

A Comparative Income Statement gives the reader a frame of

reference for comparing the current year amounts. Comparative income

statement presents both the current period (typically current month or

current year to date) compared to normally a prior year same period.

comparative income statement consist of two columns of amounts (one is

of current year and another is of prior year) appearing to the right of the

account titles or descriptions. The amounts are shown side by side to make it

easy to compare the two periods presented. Comparative income statement

may also refer to this same type of comparison for current period to

budget for the same period.

16 | P a g e Roll No.: 68203U09038

Session 2012-13

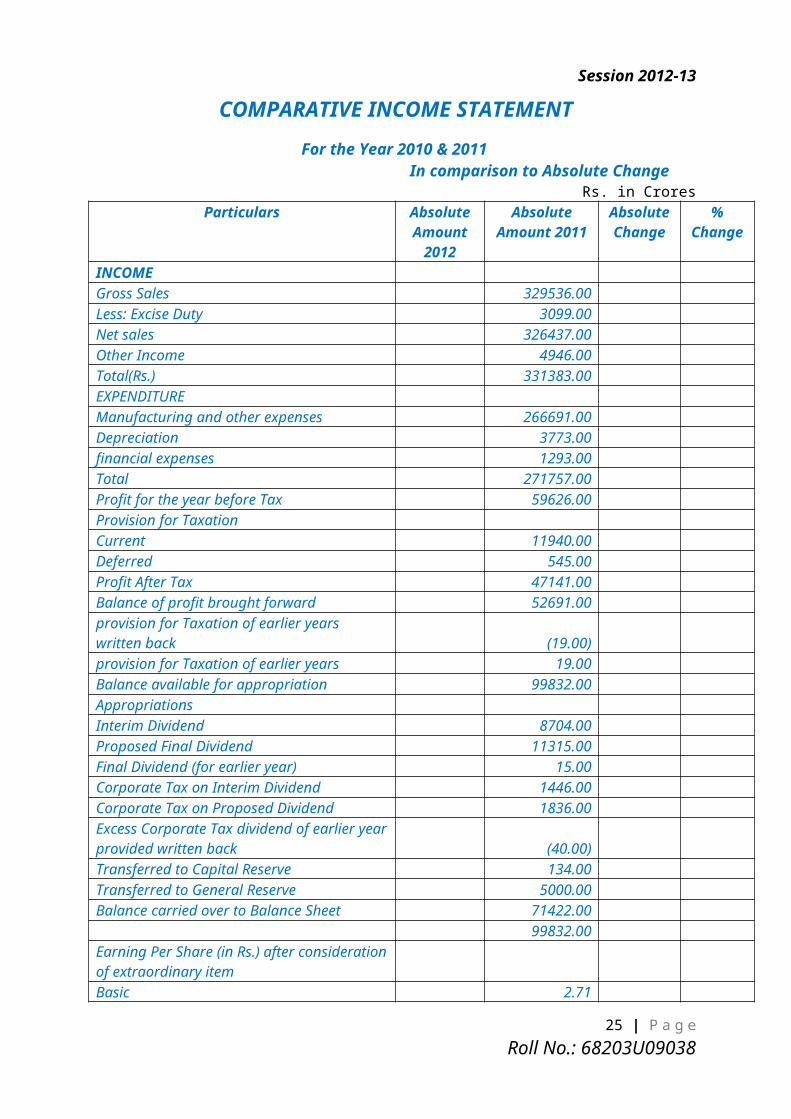

COMPARATIVE INCOME STATEMENT

For the Year 2010 & 2011In comparison to Absolute Change

Rs. in CroresParticulars Absolute

Amount 2012

Absolute Amount 2011

Absolute Change

% Change

INCOMEGross Sales 329536.00 Less: Excise Duty 3099.00 Net sales 326437.00 Other Income 4946.00 Total(Rs.) 331383.00 EXPENDITURE Manufacturing and other expenses 266691.00 Depreciation 3773.00 financial expenses 1293.00 Total 271757.00 Profit for the year before Tax 59626.00 Provision for TaxationCurrent 11940.00 Deferred 545.00 Profit After Tax 47141.00 Balance of profit brought forward 52691.00 provision for Taxation of earlier years written back (19.00)provision for Taxation of earlier years 19.00 Balance available for appropriation 99832.00 Appropriations Interim Dividend 8704.00 Proposed Final Dividend 11315.00 Final Dividend (for earlier year) 15.00 Corporate Tax on Interim Dividend 1446.00 Corporate Tax on Proposed Dividend 1836.00 Excess Corporate Tax dividend of earlier year provided written back (40.00)Transferred to Capital Reserve 134.00 Transferred to General Reserve 5000.00 Balance carried over to Balance Sheet 71422.00

99832.00 Earning Per Share (in Rs.) after consideration of extraordinary itemBasic 2.71 Diluted 2.69 Earning per Share (In Rs) without consideration of extraordinary itemsBasic 2.71 2.50 Diluted 2.69 2.49

17 | P a g e Roll No.: 68203U09038

Session 2012-13

COMPARATIVE BALANCE SHEET

A comparative balance sheet presents side-by-side information about an

entity's assets, liabilities, and shareholders' equity as of multiple points in time. For

example, a comparative balance sheet could present the balance sheet as of the end

of each year for the past three years. Another variation is to present the balance

sheet as of the end of each month for the past 12 months on a rolling basis. In both

cases, the intent is to provide the reader with a series of snapshots of a company's

financial condition over a period of time, which is useful for developing trend line

analyses (though this works better when the reader has the entire set of financial

statements to work with and not just the balance sheet).

18 | P a g e Roll No.: 68203U09038

Session 2012-13

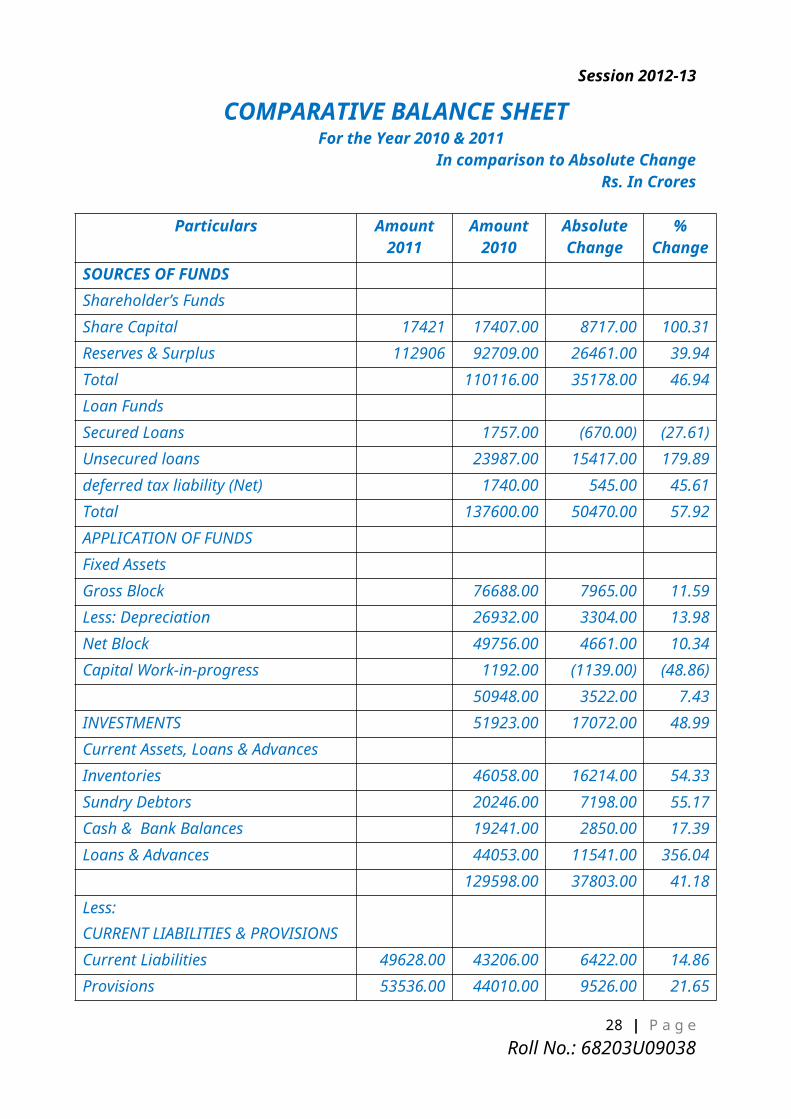

COMPARATIVE BALANCE SHEETFor the Year 2010 & 2011

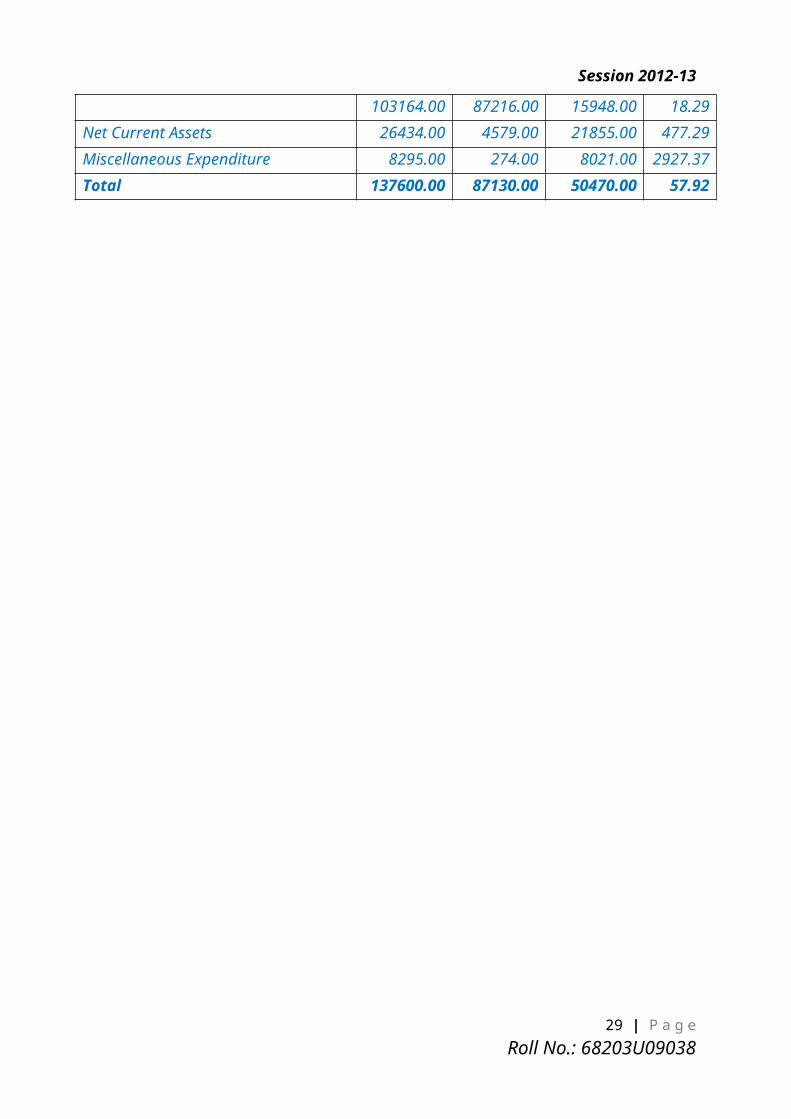

In comparison to Absolute Change Rs. In Crores

Particulars Amount 2011

Amount 2010

Absolute Change

% Change

SOURCES OF FUNDS

Shareholder’s Funds

Share Capital 17421 17407.00 8717.00 100.31

Reserves & Surplus 112906 92709.00 26461.00 39.94

Total 110116.00 35178.00 46.94

Loan Funds

Secured Loans 1757.00 (670.00) (27.61)

Unsecured loans 23987.00 15417.00 179.89

deferred tax liability (Net) 1740.00 545.00 45.61

Total 137600.00 50470.00 57.92

APPLICATION OF FUNDS

Fixed Assets

Gross Block 76688.00 7965.00 11.59

Less: Depreciation 26932.00 3304.00 13.98

Net Block 49756.00 4661.00 10.34

Capital Work-in-progress 1192.00 (1139.00) (48.86)

50948.00 3522.00 7.43

INVESTMENTS 51923.00 17072.00 48.99

Current Assets, Loans & Advances

Inventories 46058.00 16214.00 54.33

Sundry Debtors 20246.00 7198.00 55.17

Cash & Bank Balances 19241.00 2850.00 17.39

Loans & Advances 44053.00 11541.00 356.04

129598.00 37803.00 41.18

Less: CURRENT LIABILITIES & PROVISIONS

Current Liabilities 49628.00 43206.00 6422.00 14.86

Provisions 53536.00 44010.00 9526.00 21.65

103164.00 87216.00 15948.00 18.29

Net Current Assets 26434.00 4579.00 21855.00 477.29

Miscellaneous Expenditure 8295.00 274.00 8021.00 2927.37

Total 137600.00 87130.00 50470.00 57.92

19 | P a g e Roll No.: 68203U09038

Session 2012-13

COMMON SIZE INCOME STATEMENT

Common size income statements are basically used for analysis purposes

where each item on the face of income statement is expressed in relation to revenue

so that users can easily understand that how different expenses and other incomes

and gains adds up to gross profit and net profit. This is widely used in ratio analysis

and serve as a vital tool start up a financial analysis of the key areas of

performance and then detailed ratios are applied on each item afterwards.

Although common size income statements do not provide a detailed financial

analysis of income statement and its items but it does help in comparing the

financial performance of the company with the preceding accounting periods

known as trend-analysis or time-series analysis. We can also compare financial

information of one company with other companies in the industry which is known

as cross-sectional analysis. The good thing about common-size analysis is that it is

really easily to do and also interpreting the results is not so difficult. Even the users

who are not proficient in analysis techniques can gain insight of company’s

financial performance to some extent from common size financial statements i.e.

income statement and statement of financial position.

20 | P a g e Roll No.: 68203U09038

Session 2012-13

COMMON SIZE INCOME STATEMENT

FOR YEAR 2010 & 2011Rs. in Crores.

Amount2011

Amount2010

% of Sales 2011

% of Sales 2010

% Change

Net Sales 326437.00 285596.00 100.00 100.00 0.00

(-) Operating Expenses 197040.00 166245.00 60.36 58.21 2.15

Operating Profit 129397.00 119351.00 39.64 41.79 (2.15)

(-) Non Operating Expenses 70944.00 67621.00 21.73 23.68 (1.94)

(+) Non Operating Income 4946.00 4164.00 1.52 1.46 0.06

Net Profit Before Tax & Depreciation 63399.00 55894.00 19.42 19.57 (0.15)

(-) Depreciation 3773.00 3191.00 1.16 1.12 0.04

Net Profit Before Tax 59626.00 52703.00 18.27 18.45 (0.19)

Tax (Net of Deferred Tax) 12485.00 9370.00 3.82 3.28 0.54

Net Profit 47141.00 43333.00 14.44 15.17 (0.73)

21 | P a g e Roll No.: 68203U09038

Session 2012-13

COMMON SIZE BALANCE SHEET

A common size balance sheet presents not only the standard information

contained in a balance sheet, but also a column that notes the same information as

a percentage of the total assets (for asset line items) or as a percentage of total

liabilities and shareholders' equity (for liability or shareholders' equity line items).

It is extremely useful to construct a common size balance sheet that itemizes

the results as of the end of multiple time periods, so that you can construct trend

lines to ascertain changes over longer time periods. The common size balance sheet

is also useful for comparing the proportions of assets, liabilities, and equity between

different companies, particularly as part of an industry analysis or an acquisition

analysis.

22 | P a g e Roll No.: 68203U09038

Session 2012-13

COMMON SIZE BALANCE SHEET

For the Year 2010 & 2011 In comparison to Capital Employed

Rs. in Crores

Particulars Amount 2011

Amount 2010

% of capital Employed

2011

% of capital Employed

2010

% Change

Fixed Asset 50948.00 47426.00 37.73 54.43 (16.70)

Investment 51923.00 34851.00 37.73 40.00 (2.26)

Working Capital

i. Current Asset 129598.00 91795.00 94.18 105.35 (11.17)

ii. Current Liability 103164.00 87216.00 74.97 100.10 74.97

Working Capital (i-ii) 26434.00 4579.00 19.21 5.26 13.96

Miscellaneous Expenditure 8295.00 274.00 6.03 0.31 5.71

Capital Employed (A+B+C) 137600.00 87130.00 100.00 100.00 0.00

(-)Deferred Tax Net 1740.00 1195.00 1.26 1.37 (0.11)

(-) Long Term Loan 25744.00 10997.00 18.71 12.62 6.09

110116.00 74938.00 80.03 86.01 (5.98)

Shares Holders Fund

Share Capital 17407.00 8690.00 12.65 9.97 2.68

Reserve & Surplus 92709.00 66248.00 67.38 76.03 (8.66)

Total Share Holders Fund 110116.00 74938.00 80.03 86.01 (5.98)

23 | P a g e Roll No.: 68203U09038

Session 2012-13

RATIO ANALYSIS:

Ratio analysis is a powerful tool of financial analysis. A ratio is defined as ‘the indicated quotient of two mathematical expressions’ and “The relationship between two or more things.”

In financial analysis, a ratio is used as a benchmark for evaluating the financial position and performance of a firm. The absolute accounting figures reported in the financial statements do not provide a meaningful understanding of the performance and financial position of firm.

A. Short term Solvency:-

Current Ratio:

It is an indicator used to measure the Short term Solvency of a company. The ideal

ratio is 2:1

Current ratio = Current Asset/ Current Liability =

129598/103164= 1.25:1

It indicates that the current ratio of the company is above the norm & hence the short term

solvency of the company is sound enough to meet the short term obligations of the

company.

B. Long Term Solvency:

Debt equity Ratio:

It is a measure to ascertain the long term financial policies of Company. The ideal

ratio is 1:1

Debt equity ratio= Long Term Debt/Share Holders Funds

= 25744/ 110116=0.23:1

The company does have a debt equity ratio higher than the standard for the company. Or

in other words the company has enough share holders funds to repay the debts.

C. Capital Turnover Ratio:

It shows whether the capital utilization leads to higher profit or not.

Capital Turnover Ratio= Sales / Capital Employed

= 326437/ 137600=2.37:1

The capital has been utilized properly as indicated from the above ratio.

24 | P a g e Roll No.: 68203U09038

Session 2012-13

D. Fixed asset Turnover ratio:

It shows the extent to which the investment of the fixed assets contributes to words sales:

Fixed asset turnover ratio: Net Sales/Net Fixed Assets

= 326437/ 50948 = 6.41:1

It indicates that fixed assets contribute a much to the sales in the current year.

E. Net Working Capital Turnover Ratio:

It shows the unit utilized in the working capital to which extent it generates sales.

Net working capital turnover ratio= Sales / Net Working Capital

= 326437/ 26434= 12.25:1

It shows the working capital was properly utilized.

F. Net profit Ratio:

It measures the relationship between Net Profit & Net Sales. It determines the overall

probability due to various factors such as operational efficiency, trading on equity etc.

Higher the ratio greater is the capacity of the firm to withstand adverse economic

condition.

Net Profit Ratio = Net Profit x 100/ Net Sales

= 47141/ 326437X 100= 14.44%

The company does maintain a healthy net profit ratio, however there has been an decrease

in net profit ratio as the company had a net profit ratio of 14.44% in the previous year.

Therefore it can be said that the company has not been able to hold on to the previous year

results during the current year.

25 | P a g e Roll No.: 68203U09038

Session 2012-13

FINDINGS: (INTERPRETATION)

Analysis of Comparative Income Statement

On comparison of the above two years figures it is observed that the sales of the company has increased by 14.30% over previous year and other incomes have increased by 18.78%. Direct costs have increased by 14.70% and interest (net) has decreased by 4.15% over previous year. Profit before tax has increased by 13.14% and profit after tax has increased by 8.79% over previous year. The company performed better during the current year. Dividend proposed is Rs.11315 crores in the current year against Rs.10862 Crores in the previous year. The earnings per share have also increased by 8.40% over previous year. It can therefore be said that the company has been able to satisfy both the customers and the share holders during the current fiscal.

Analysis of Comparative Balance Sheet

On comparison of balance sheet of above two years it is observed that the fixed assets have increased by 10.34% over previous year. The capital work in progress has decreased by Rs.1139 Crores which shows that few of the capital works in progress has been completed during the current year. The loan funds have increased by 134.10% which implies that the company has raised a further long term loan. Sundry debtors have increased by 55.17% which means that the company has not been able to decrease the credit sales. Cash & bank balance have increased by a whooping Rs. 2850 crores which implies that the company is having surplus funds unutilized. The total current assets have increased by 41.18% over previous year where current liabilities has been increased by a 18.29% over previous year.

Analysis of Common Size Income Statement

On comparison of the income statement figures in relation to sales it is observed that the operating expenses have increased by 2.15% which is reflected in the decrease in operating profit by the equal amount. There has also been an increase in non operating income by 0.06% over previous year. The profit before tax has also decreased by 0.19% over previous year and the profit after tax has decreased by 0.73 over previous year. It can therefore be said that the company has not performed better than the level operation of previous year during the current year.

Analysis of Common Size Balance Sheet

On comparison of the balance sheet figures in relation to the total capital employed it is observed that fixed assets have increased by 10.34% and investments have increased by 48.99% over previous year. Current assets have increased by 41.18% and current liabilities have increased by 18.29% over previous year in relation to the total capital employed. The total capital has increased by 50470 crores over previous year. It can be said that the short term solvency of the company is in dire straits.

26 | P a g e Roll No.: 68203U09038

Session 2012-13

SUGGESTIONS:

In my opinion and to the best of my knowledge , It can be said that

although the company has fared up well on basis of operations in the current

but the financial status of the company is not well. So in order to increase the

performance of the company there should be an adequate internal control

system commensurate with the size of the Company and the nature of its

business with regard to purchases of inventory and fixed assets and the sale

of goods and services. However the working capital of the company is in a

positive which is a good sign and the only weak link of the company as a

result of increase in short term loans. Sundry debtors have increased

significantly as compared to its previous year figure .So there should be an

adequate internal control over it’s credit sales.

27 | P a g e Roll No.: 68203U09038

Session 2012-13

CONCLUSION:

The company has been able to increase its sales but there was a decrease in

profit during the year as there was a significant increase in operating expenses

during the year. The operations of the company has not therefore improved as

compared to the previous year. The net profits ratio has not increased which

proves that the company has not been able to control the costs effectively. The

depreciation has been increased significantly as a result of huge addition in fixed

asset. Cash & bank balance have increased by a whooping which implies that the

company is having surplus funds unutilized. The current assets of the company

are enough to meet the current liabilities. The loan funds have been increased

which implies that the company has been raised further loan. Dabur holding the

highest share market and does enjoy a good credibility which is evident in the

amount of current liabilities held at the balance sheet date but the current ratio

should be at least 1:1 keeping in view the size of the company and its activities.

From the share holder’s point of view the company has been a profitable venture

as the proposed dividend has increased. The earning per share has increased in

comparison to previous year as a result of decrease in profit after tax.

28 | P a g e Roll No.: 68203U09038

Session 2012-13

References:

1. General Accountancy

by Gupta and Agarwal

2. Fundamental of Accounting

By S PAUL

3. Advanced Accounting

by Paul M. Fischer, William J. Taylor, Rita H. Cheng,

4. Accounting Information Systems

by Marshall B. Romney, Paul John Steinbart

5. Management Accounting

by Tata McGraw Hill – Khan & Jain

Newspapers & Magazines:

1. Economics Times

2. India Today

3. Business Times

Websites:

1. www.dabur.com

2. www.equitymaster.com

3. www.moneycontrol.com

4. www.google.com

29 | P a g e Roll No.: 68203U09038