Final presentation galp energia_brazil_internationalization

61

✧Agnieszka Machala - 1841 ✧André Alves - 1554 ✧Daniela Zerpa - 1834 ✧Nicola Loffredo - 1569 ✧Pietro Barindelli - 1530 ✧Stefany Agredo Martin - 1649 Team D ❖ Agnieszka Machała - 1841 ❖ André Alves - 1554 ❖ Daniela Gonzalez - 1834 ❖ Pietro Barindelli - 1530 ❖ Nicola Loffredo - 1569 ❖ Stefany Agredo - 1649 TEAM D

-

Upload

nicola-loffredo -

Category

Economy & Finance

-

view

151 -

download

4

Transcript of Final presentation galp energia_brazil_internationalization

✧Agnieszka Machala - 1841 ✧André Alves - 1554 ✧Daniela Zerpa - 1834 ✧Nicola Loffredo - 1569 ✧Pietro Barindelli - 1530 ✧Stefany Agredo Martin - 1649

Team D

❖ Agnieszka Machała - 1841

❖ André Alves - 1554

❖ Daniela Gonzalez - 1834

❖ Pietro Barindelli - 1530

❖ Nicola Loffredo - 1569

❖ Stefany Agredo - 1649

TEAM D

Galp Energia is an energy company specialized in finding and extracting oil and natural gas from sites across four continents to deliver energy to

millions of customers every day.

1

Source: www.galp.com

Com

pany´s

Pro

file

Market capitalisation: €9.752 million

Turnover: €18.507 million

Net profit RCA: €360 million

Number of employees: 7,241

Reserves 3P: 783 mboe

Refineries: 2

Service stations: 1,486

Sales of natural gas: 6.253 mm³

Presence in four continents:

Europe: Portugal and Spain.

South America Brazil, Uruguay Venezuela.

Africa:

Asia:

Angola, Mozambique, Cape Verde, Guinea-

Bissau, Swaziland, Gambia, Equatorial

Guinea, Morocco and Namibia.

East-Timor

*Data from the end of 2012

2

Source: www.galp.com

His

torical B

ackgro

und

in B

razil

1999

Galp starts extraction

operations as Petrogal

2000

The first important extraction block was

awarded to the consortium for oil exploratory rights in

Santos

2005

With 20% participation the block ES-M-592 was awarded to the

consortium in Espirito Santo and 10% participation in blocks: POT-17, M-665, POT-M-853 and POT-M-855

in Portiguar

2007

Exploration right was awarded for blocks C-M-593, and BM-C-44 with 15.5% participation in

Campos

2006 Exploration in three

ultradeep water blocks in Pernanbuco

Revenues were about 7.6 million

Brazilian reais The Declaration of

Commerciality is issued to the Dó-Ré-Mi field in

Serguipe

2008

With 40% participation, 27,5 million Brazilian Reais were collected

from Amazonas

2012 With 10%

participation Lula Camp is awarded

2013

Currently Galp Energia participates in more than

20 projects in Brazil, where it is in partnership with oil

operator Petrobras Attempt to approach the midstream and downstream

markets. Analysis did not go as expected.

3

Source: www.galp.com

Pro

ducts

As PetroGal is only on the upstream

business PURE OIL is the core and unique product

4

Source: www.galp.com

Busin

ess

Oppo

rtunity

BRAZIL

Indicators:

- 190 million inhabitants

- Strong growth rates

- Vast natural resources (biggest oil discovery in decade)

Opportunity:

- Cultural & Political Affiliations

- Increasing Liberalization of Markets

- Petrogal has past experience

- Portfolio diversification

- Learning opportunity

- Gateway to other markets

5

Mis

sio

n

Creation of value for its shareholders taking into

account the economic, social, environmental backgrounds

6

Source: www.galp.com

Vis

ion

Participation in future rounds of bids to

increase Galp‘s presence in Brazil

7

Source: www.galp.com

Quantified S

trate

gic

Obje

ctives

8

Source: internal source

Increase production in Brasil to 100000 barrels per day by

2020

With 25% higher cash flow the company will

increase its participation in future

contracts

With more participation Petrogal plans to strengthen its relationship with local

partners

With higher financial power, specilized

operations and good recognition for the last

decades on the market, Galp wants to become an integrated operator, recognised

for its exploration successes

Targ

et M

ark

et

LULA Field Project, BRAZIL 9

Source: www.galp.com

Exploration and Production (upstream)

• The largest oil and natural gas reservoirs discovered in the last 30 years located in the Santos basin, off the Brazilan Coast.

• Exploration, appraisal and developlment of ultra deep-water field

Valu

e c

ha

in a

naly

sis

As the value chain is a process where raws materials are transformed

in diferent steps that add value, in the oil industry this transition is

divided into three parts:

•UPSTREAM → process of finding and extracting crude oil from the

ground.

•MIDSTREAM → process of refining crude oil into its various sub-

products that can be used for many functions.

•DOWNSTREAM → process of marketing and distributing refined

products to consumers.

→ GAS → OIL

10

Source: www.galp.com

Valu

e c

ha

in a

naly

sis

Operation Cost Gross margin Net Margin Percent

Exploration 2.97 16.33 13.36 36%

Production 17.78 32.67 14.89 41%

Transportation 1.00 2.96 1.96 5%

Refining 3.70 8.50 4.80 13%

Distribution 1.90 3.23 1.33 4%

Marketing 0.80 1.16 0.36 1%

Pump taxes 19.15 0.00 0.00 0%

36.70 100%

Oil and Gas Economics

(data are expressed in $cents/gallon)

• Over 75% of an integrated oil company’s net margins are in the upstream • 2013-2020: 80% of Galp’s projects will focus on Exploration and Production • Return rate: Upstream (risky) 10%, Downstream (less risky) 5% • Brazil → Lula → Joint Venture with Petrobras

11

Source: www.worldoil.com

12

Source: internal source

Cultural

and

political

afilliation

BUSINESS MODEL

Value proposition

1. File for data 2. Bid/Accept proposal 3. Geological field

Surveys 4. Apply for licenses (ANP) 5. Installation of facilities

6. Drilling tests 7. Beginning of production

Political &

legislations

(Ibama)

Accomplish

Env. rules

Start the

extraction

process

Low Cost: 15% R&D, Field search, profitability analysis, labor

Medium Cost: 15% Storage, transportation,

external logistics High Cost: 70% Production (drilling, extraction)

Petrobras: 65% GB Group : 25% Petrogalp: 10%

Technology force & Local Experience

Accomplish Quantitve Strategies

Exploration

in Brasil

(Lula field)

Oil Raw

materials

sales

Operational model

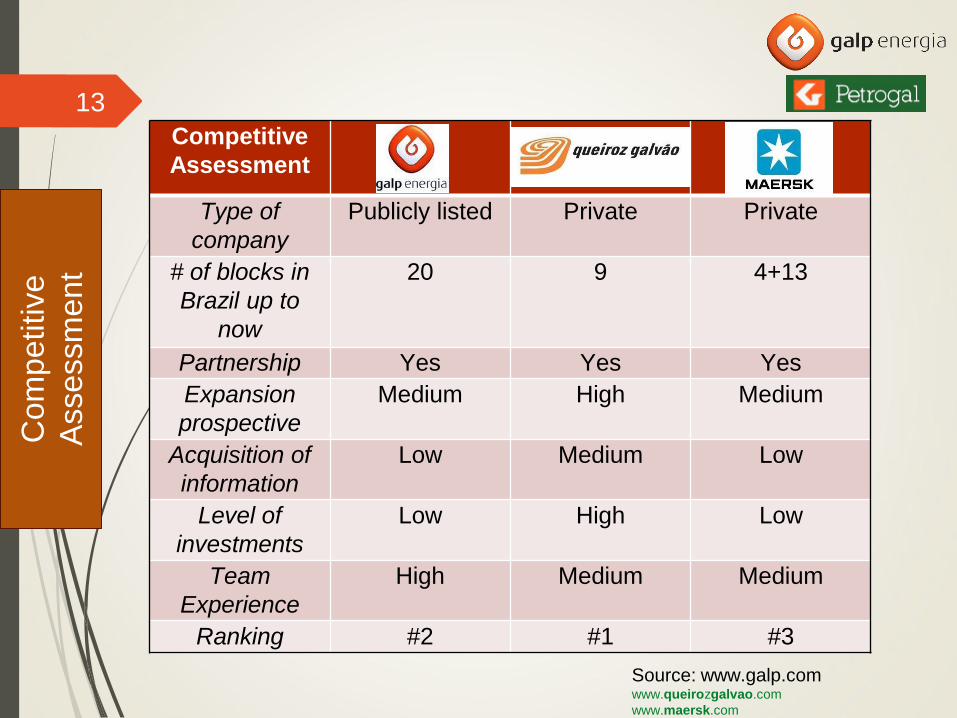

Com

petitive

Assessm

ent

Competitive

Assessment

Type of

company

Publicly listed Private Private

# of blocks in

Brazil up to

now

20 9 4+13

Partnership Yes Yes Yes

Expansion

prospective

Medium High Medium

Acquisition of

information

Low Medium Low

Level of

investments

Low High Low

Team

Experience

High Medium Medium

Ranking #2 #1 #3

13

Source: www.galp.com

www.queirozgalvao.com

www.maersk.com

Port

er

Analy

sis

Porter’s Five Forces 14

Threat of entry

Port

er’s F

ive F

orc

es

Ana

lysis

• Huge capital requirements; • Enormous fixed up-front investments for the development of oil fields; • Economies of scale to reach a decrease in unit costs in the exploration and production of oil; • The need to secure access to distribution channels; • Government policies that favour national companies.

Source: internal source

15

Threat of substitutes

Port

er’s F

ive F

orc

es

Ana

lysis

• Different substitutes that will become a threat

once the crude oil price will increase

significantly;

• Governments around the world are changing

their attitude towards fossil fuels.

16

Source: internal source

Bargaining power of

suppliers

Port

er’s F

ive F

orc

es

Ana

lysis

• Main suppliers of oil fields have significant

bargaining power;

• Many conventional suppliers from supporting

industries have low bargaining power.

Source: internal source

17

Bargaining power

of buyers

Port

er’s F

ive F

orc

es

Ana

lysis

•Different degree of bargaining power, through different volumes of demand; •Given world oil price buyers have low bargaining power; •Big-country consumers may affect global demand with an increase in bargaining power.

18

Competitive Rivalry

Port

er’s F

ive F

orc

es

Ana

lysis

•The oil industry can be described as having few major and strong players and several smaller players with less power; •The rivalry is getting increasingly fierce among big producers; •The slow industry growth also intensifies rivalry among competitors; •High exit barriers and fixed costs keep the firms in a highly competitive industry.

19

Industr

y M

appin

g

Galp Community

Competitors

Partners Clients

Suppliers

Regulator

Employees

20 Industry mapping

Employees

•Galp in Brazil- around 70 employees

•Business sectors:

–exploration and development of raw materials;

•Galp continues to run training and research programmes:

–the GeoEr programmes - Geo-Engineering of carbonate reservoirs,

–the EngIQ- a PhD programme in refining engineering in cooperation

with the prestigious Heriot-Watt university

–Petroleum and Gas institute (isPG) in partnership with seven of the

most prestigious portuguese Universities

Industr

y M

appin

g

Sources: www.galpenergia.com/EN/Investidor/Relatorios-e-resultados/relatorios-anuais/Documents/Sustainability_report_2012.pdf

21

Regulators ●Brazilian federal constitution

●Petroleum investment law:

○Legal and regulatory framework

○Liberalization of oil production

○Creation of ANP- sector regulator

The resuming of ANP bidding rounds:

Industr

y M

appin

g

Source: www.brazil.org.uk/commercial/anproadshow_files/anproadshow2013.pdf

22

Partners Galp Energia invests in onshore,

shallow water and deepwater blocks in cooperation with:

Petrobras.

BG Group,

BP

Oil block locations in Brasil:

Parnaíba, Barreirinhas Potiguar and Santos Basin

Oil field Lula in Santos Basin:

65% Petrobras ,25% BG Group, 10% Galp Energia

Reasons for cooperation:

1.Increasing capital by cofinancing the investments

2.Political impositions

3.Large-scaling oil projects Industr

y M

appin

g

Sources: www.galpenergia.com/EN/Investidor/Relatorios-e-resultados/relatorios-anuais/Documents/Sustainability_report_2012.pdf

23

Community

Galp has strong community links

Palm oil production (with Petrobras) in State of Pará

o One of the poorest regions in Brazil

o Palm oil is sustainable (plants can last for more than 40 years)

o Objective: make families self sustainable

o Petrogal & Petrobras buy oil from the families

o Decrease in the usage of fossel fuel

o Creation of 9.000 jobs (directly and indirectly)

Industr

y M

appin

g

24

Clients & suppliers

Costumers

Undisclosed customers

Can have bargaining power

Suppliers

Upstream business is different

Galp works in joint ventures

Bulk of technology is provided by the partners

Undifferentiated commodities

Industr

y M

appin

g

25

SW

OT

Analy

sis

SWOT Analysis

STRENGTHS

•Reliability, good negotiation

partner

•Language and cultural

affiliation

•Previous experience;

technological know-how

WEAKNESSES

•Small size

•Lack of financial power

•Share of total control with

Sinopec

•Lack of R&D in Brazilian

subsidiary

OPPORTUNITIES

•Enhance relationship with

Petrobras

•Learning opportunities for

GALP and its employees

•Achieving the target market

SO Strategy

•Participation in future bids for

drilling projects

•Use of technical experience

in deepwater exploration in

other projects

WO-Strategies

•Creation of R&D division with

Petrobras

THREATS

•Risky environment

•Corruption

•Accidents •Licenses restrictions

ST-Strategies

•Intensification of exploration

with seismic testing and test

wells

WT-Strategies

•Prevention of some accidents

by forecasting the risks in

close cooperation with the

partners

26

VRIO Analysis V

RIO

Analy

sis

27

MODE OF ENTRY

Joint Venture with Local & International partners

Depends on type of license

There are two ways Petrogal can enter Brazil:

o Operator

o Regular Partner

Mode o

f E

ntr

y

28

Entry barriers

High strategic entry barriers due to:

Collusion by incumbent firms

High structural entry barriers due to:

Cost structure (fixed costs)

Initial investment (high)

Strict regulations (legal and environmental)

Knowledge

Entr

y B

arr

iers

29

Types of Licenses

Type A

→ Allows for deep-water exploration

Type B (Galp)

→ Allows for off-shore exploration

Type C

→ Allows for on-shore exploration only

Types o

f Lic

enses

30

Joint Venture

Risk minimization/Cost sharing

Preferred mode of entry in Brazil

How does it work?

o One operator, multiple partners

o Established previously in contract (standard)

o Equity share

o Transparent process

Join

t V

entu

re

31

Operator

In charge of operations/processes

Only legitimate communicator in the venture

Must handle everything:

Personnel

Exploration

Explotation

Communication with regulator and partners

Communication with suppliers and clients

Opera

tor

32

Regular Partner

Direct communication with operator

Takes decisions together with operator

Other responsabilities in the venture:

o Financial backing

o Monitoring (KPIs, daily reports)

o Advising

Regula

r P

art

ner

33

Issues in the venture

OPERATOR CAN BE A MINORITY

Partners can move alone in some occasions

Contracts specify resolution of conflicts

Everything is contractualized

KPIs set by the venture

Disclosed information to partners

Financing needs

Issues in t

he V

entu

re

34

Corp

ora

tive R

ela

tion

Com

mu

nic

ations

Organizational Communication

Facilitate stakeholders‘ decision making + fulfillment of legal duties + Inform about current activities + Assistance with issues regarding Galp´s status + Mantain a good public image

35

Corp

ora

tive R

ela

tion

Com

mu

nic

ations

Dividends for the 3rd

Quarter 2013

Shareholders Actively Participate in Corporate

Decisions.

National Meeting in Brazil

Investors Communications 36

Sale

s S

trate

gy &

Tactics

SALES STRATEGY IN IBERIAN

PENINSULA AND AFRICA:

B2C & B2B Business2Consumer:

•around 1,500 service stations in Portugal, Spain and Africa. Retail is

responsible for 30% of sales to direct customers.

•market share: portuguese retail market → 30% and spanish retail market →

6% In Africa, Galp Energia owns around 100 service stations.

Business2Business:

•oil products to the transportation, aviation, industry subsegments, contractors

and marine.

•Spain is a strong growht market. Galp enjoys a leading position in spanish

market.

37

Sale

s S

trate

gy &

Tactics

OIL PRODUCTS’ SALES APPROACH IN BRAZIL:

B2B & B2C Business2Business: • Who are Galp’s clients in Brazil? Clients are fixed in contracts

and the operator signs all the contracts.

• If Galp is not the operator, Galp knows their clients only if the operator wishes (unless Galp Energia is a client itself).

• However, the biggest client of Galp in Brazil is Petrobras. Galp’s expertise, cultural and political aspects foster the relationship between the companies.

How do things work in Brazil? 38

CS

F/C

ore

pro

cesses

39

Source: internal source

Critical

Success

Factors

Implications

Strategies

KPI’s

Oil price

• Profit

• Contract

fullfillment

N/A • Fluctuations

Drilling time

Development of new

technologies

• Number of oil barrels

produced per day

Highly qualified

Employees

• Maintain

reliability and

recognition for

future deals

• Advanced training

• Distance learning

• Master and executive

programs

• Investment in Education

• Balanced Score Card

Contract

Management

• Profit

• Efficiency

Establishment of closer

links with partners and

regulatory agency

• Equity share of contract

CS

F/C

ore

pro

cesses

OIL PRICE 40

Source: internal source

CS

F/C

ore

pro

cesses

DRILLING TIME 41

Source: internal source

KPI’s Objectives

Drilling time reduced by 5%

KPI’s

Number of oil barrels produced per day

Core Processes

Operations

Strategic Objectives

Decrease of the drilling time

Critical Success Factor

Drilling Time

CS

F/C

ore

pro

cesses

HIGH QUALIFIED EMPLOYEES 42

Source: internal source

KPI’s Objectives

Efficiency increase

KPI’s

Balanced Score Card Investment in education

Core Processes

Human Resources Management

Strategic Objectives

Train and maintain the best junior and senior engineers

Clear definition of roles and responsibilities

Critical Success Factor

Highly qualified employees

CS

F/C

ore

pro

cesses

CONTRACT MANAGEMENT 43

Source: internal source

KPI’s Objectives

Increase of number and share in the contract

KPI’s

Equity share of contract

Core Processes

Procurement

Strategic Objectives

Improvement of flow of information

Critical Sucess Factor

Contract Management

4 M

‘s -

Men

The 4 M’s - MEN

Local Human Resources Task

Geologists

Study seismic tests, blocks’ measurement

and consulting to operators. Report to both

the operator and project management team

Technicians

Handle geological machinery and field work

(survey). Report to both the operator and

project management team

Project Management Team (liaison)

Monitors the operation (representative of the

partner). Consults with technical team to

provide advice to operator. Reports to head

of E&E - Petrogal

Head of exploitation & exploration

Coordinates operations in Brazil.

Decision maker

• Head of E&E reports directly to Galp Energia’s HQ in Lisbon • No need for a single project manager per project when Petrogal is not the operator (waste of

resources) • Better to have a team to oversee all projects • Team is permanently in Brazil • Reporting to operator & team is simultaneous • Terms of reporting are pre-contractualized

44

4 M

‘s -

Money

Position Monthly Salary

Geologists 4.000€ - 9.500€

Technicians 4.000€ - 8.500€

Project Management Team 5.000€ - 9.000€

Head of Exploitation & Exploration 10.000€ - 15.000€

The 4 M’s - MONEY

Salaries have great variations depending on:

✓National vs. Expatriate

✓Junior vs. Senior

✓Differences in compensation schemes Source: Hays Global Report 2012

45

4 M

‘s -

Money

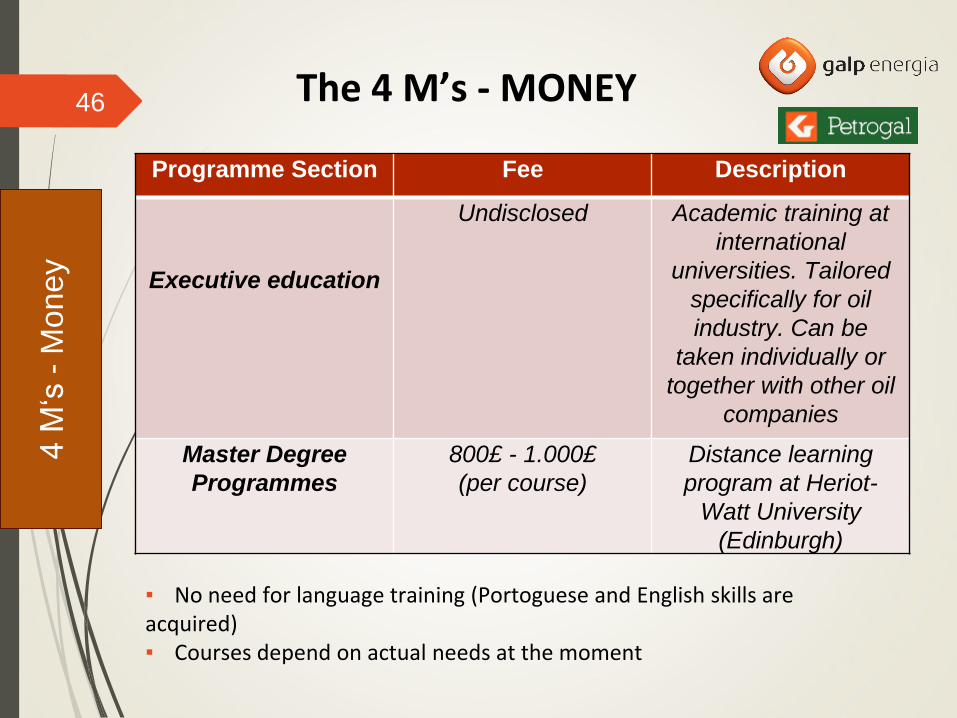

The 4 M’s - MONEY

Programme Section Fee Description

Executive education

Undisclosed Academic training at

international

universities. Tailored

specifically for oil

industry. Can be

taken individually or

together with other oil

companies

Master Degree

Programmes

800£ - 1.000£

(per course)

Distance learning

program at Heriot-

Watt University

(Edinburgh)

▪ No need for language training (Portoguese and English skills are acquired) ▪ Courses depend on actual needs at the moment

46

4 M

‘s -

Money

The 4 M’s - MONEY

Type of Expenditure Value

Geologists 4.000€ - 9.500€*

Technicians 4.000€ - 8.500€*

Project Management Team 5.000€ - 9.000€*

Head of E&E 10.000€ - 15.000€*

Training > 1.000£**

Housing 10.000€ - 20.000€*

Travel Expenses 300€ - 700€***

Oil Rig 1.000.000€****

•* Indicates monthly expenses •** Indicates punctual expenses (pre-established fees) •*** Indicates punctual expenses (determined by variable market prices) •**** Indicates daily expense

47

4 M

‘s -

Min

ute

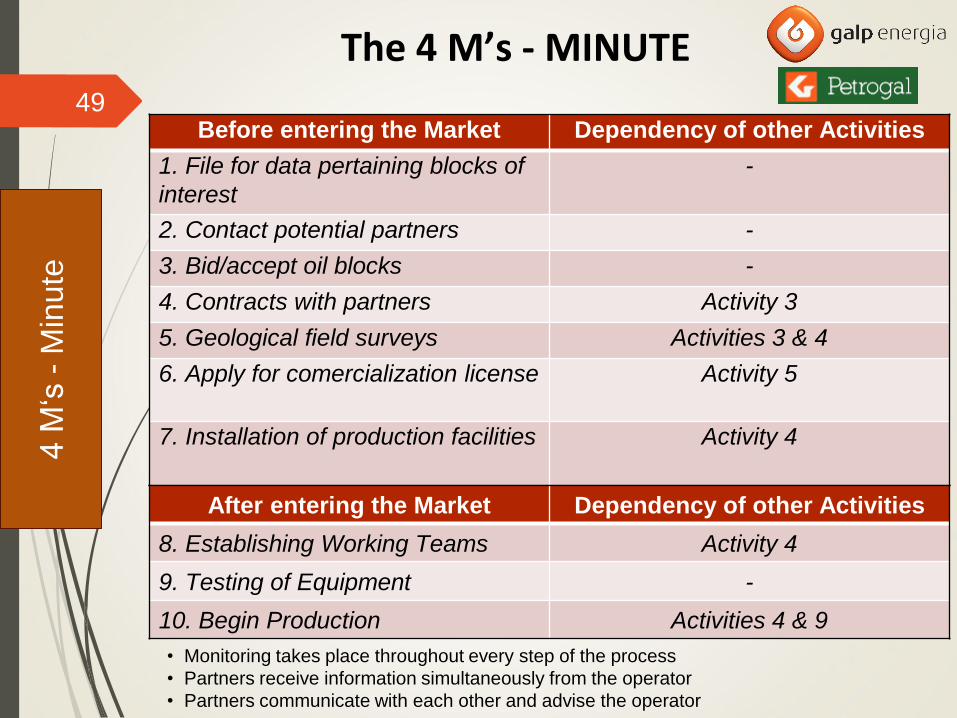

The 4 M’s - MINUTE

Before entering the Market Dependency of other Activities

1. File for data pertaining blocks of

interest

-

2. Contact potential partners -

3. Bid/accept oil blocks -

4. Contracts with partners Activity 3

5. Geological field surveys Activities 3 & 4

6. Apply for comercialization license Activity 5

7. Installation of production facilities Activity 4

48

4 M

‘s -

Min

ute

The 4 M’s - MINUTE

Before entering the Market Dependency of other Activities

1. File for data pertaining blocks of

interest

-

2. Contact potential partners -

3. Bid/accept oil blocks -

4. Contracts with partners Activity 3

5. Geological field surveys Activities 3 & 4

6. Apply for comercialization license Activity 5

7. Installation of production facilities Activity 4

After entering the Market Dependency of other Activities

8. Establishing Working Teams Activity 4

9. Testing of Equipment -

10. Begin Production Activities 4 & 9

• Monitoring takes place throughout every step of the process

• Partners receive information simultaneously from the operator

• Partners communicate with each other and advise the operator

49

4 M

‘s -

Mem

o

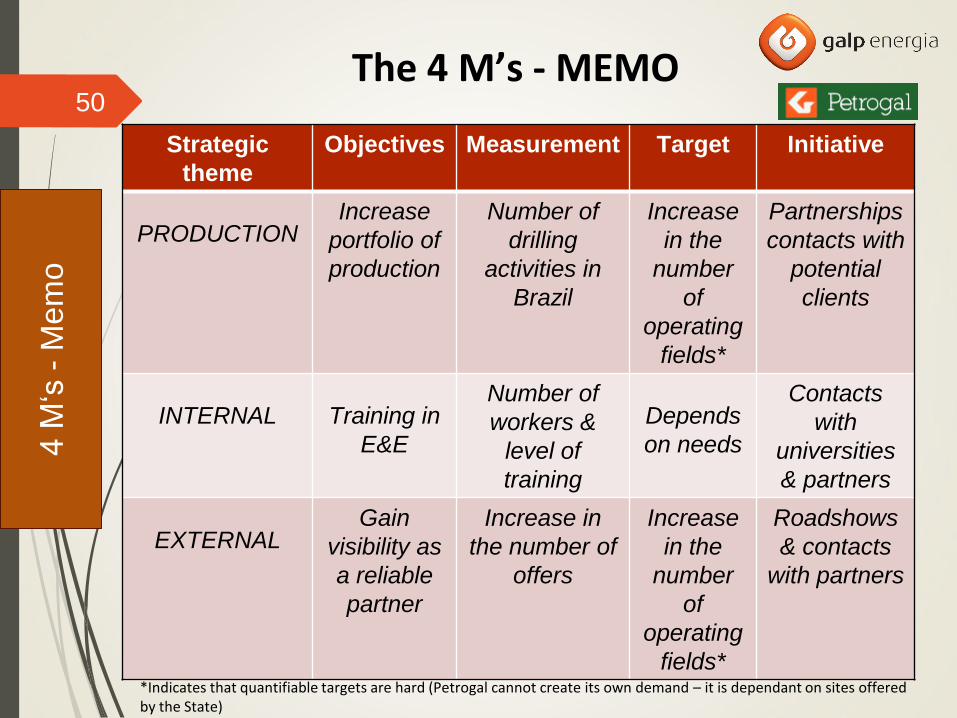

The 4 M’s - MEMO

Strategic

theme

Objectives Measurement Target Initiative

PRODUCTION Increase

portfolio of

production

Number of

drilling

activities in

Brazil

Increase

in the

number

of

operating

fields*

Partnerships

contacts with

potential

clients

INTERNAL

Training in

E&E

Number of

workers &

level of

training

Depends

on needs

Contacts

with

universities

& partners

EXTERNAL Gain

visibility as

a reliable

partner

Increase in

the number of

offers

Increase

in the

number

of

operating

fields*

Roadshows

& contacts

with partners

*Indicates that quantifiable targets are hard (Petrogal cannot create its own demand – it is dependant on sites offered by the State)

50

Chro

nogra

m

51

Chro

nogra

m

52

Chro

nogra

m

53

Chro

nogra

m

54 CONTINGENCY PLAN IN CASE OF OIL SPILL

Petrobras (the operator) will take care of this event when it happens; GALP does not have neither the responsability nor the structure to do it

Source: http://www.ipieca.org/publication/guide-contingency-planning-oil-spills-water

Ris

k a

ssessm

ent

RISK ASSESSMENT 55

Risk type Prob.ty (Scale 1-5)

Implication Impact (Scale 1-5)

Total

Risk

Price risk 3 Loss of Revenues 4 High

Supply and

demand

2 Shocks in the market 4 Medium

Operational

costs

3 Failure of machinery 5 High

Political

instability

2 Loss of Production 5 High

New

technologies

1 More Competition 4 Medium

Geological risk 1 Difficulty to extract and

find crude oil

4 Medium

Human capital

deficit

1 Unable to seize

opportunities

2 Low

Accidents 3 Loss of Production 5 High

1. Approach the downstream market

2. R&D to sustain Camp Lula (and

others)

3. Diversify portfolio (long-term)

Reccom

endations

56 RECCOMENDATIONS

1) Downstream market

Galp Energia should re-evaluate Brazil

Conditions have changed since last try

o Large investment in infrastructure

o More openness towards international firms

o Great relationship with Petrobras

There are variables to be considered

KEY DECISION VARIABLES: 1) financial power 2) partners 3) market

size 4) previous experience

ANALYSIS:

Joint venture as preferred mode of entry (Brazil is a vast market,

enormous investment is needed, Galp does not have the financial power,cost

sharing is key)

Key partner: Petrobras (key player in the downstream, it has financial power

and local knowledge)

Reccom

endations

57

2) Focus on R&D

a) Main challenge in Camp Lula

Unsure about lifetime of the machinery

Source of great potential costs

Need to mitigate risks

b) Joint efforts between partners

Petrogal can lead

Bring in Universities

Reccom

endations

58

c) Galp has worked with universities before

Contact network in researchers’ community

Petrogal can bring that advantage

d) Petrogal should be coordinating R&D

Increase importance in the venture

Knowledge spillovers

3) Diversify portfolio

Galp is mainly in the Oil&Gas business

Fossil fuels have a finite lifetime

i. Resources are getting scarce

ii. Short-run: good as prices increase

iii. Long-run: bad if there is no diversification

Galp Energia must prepare new solutions

Reccom

endations

59

BIOFUELS

already in Brazil: palm oil production in Pará state,

community work & sustainability

should intensify investment: upstream in Brazil can finance

this project, partnership with Petrobras is a possibility

![Mosonyi presentation 2007 04 21 ENG final [ r sv dett] · MOL Neste Oil PKN Orlen SA PdVSA Saras Grupa LOTOS Repsol YPF CRC LUKOIL Cepsa Eni Shell OMV Galp Energia BP Total Hellenic](https://static.fdocuments.in/doc/165x107/5f14096653ee90305d1afa23/mosonyi-presentation-2007-04-21-eng-final-r-sv-dett-mol-neste-oil-pkn-orlen-sa.jpg)