Capital Markets Day 2011 - Galp Energia33 | Capital Markets Day - March 6th 2012 Galp Energia’s...

111

Capital Markets Day 2012 Solid foundations to deliver sustainable value

Transcript of Capital Markets Day 2011 - Galp Energia33 | Capital Markets Day - March 6th 2012 Galp Energia’s...

Capital Markets Day - March 6th 2012

Capital Markets Day 2012

Solid foundations to deliver sustainable value

Page 1

Capital Markets Day - March 6th 2012

2 |

Strategy overview Manuel Ferreira De Oliveira Chief Executive Officer

Delivering on our strategy

Solid foundations in place

Ensuring sustainable and responsible growth

Final remarks

3 | Capital Markets Day - March 6th 2012

17%

11%

7% 6%

3%

-1% -2%

-5%

-8%

1%

Galp Energia

SXEP

1 Annualized shareholder return, expressed in euros, from 2006/10/23 to 2011/12/31, including dividends payment 2 Includes BG Group, BP, Eni, OMV, Petrobras, Repsol, Royal Dutch Shell and Total

Long-term performance delivering unique returns

4 | Capital Markets Day - March 6th 2012

Total annualized shareholder return since the IPO1

Peers2

2011: a year of delivery unlocking further growth

5 | Capital Markets Day - March 6th 2012

Commitment Delivery Status

Creating value through increased focus in upstream

Drilling in Rovuma basin far exceeding pre-drill estimates, turning Mozambique into a new core area

Lula development on track, well ahead of expectations

Downstream transformational optimization

Upgrade project at its final stage

Reaching a sound capital structure Capital increase at Brazilian subsidiary allowing for cash-in of c.$5.2 Bln

Solid financial structure to enable future expansion

Positioned for profitable growth

6 | Capital Markets Day - March 6th 2012

Reaping the rewards on a well-defined strategic path

Focus on three high prolific

regions: Brazil, Mozambique and Angola

Still the most leveraged player

to the outstanding

Santos basin in Brazil

Continuous downstream

optimization to maintain

contribution to earnings

Enhanced financial flexibility

allowing for expansion

opportunities

Delivering on our strategy

Solid foundations in place

Ensuring sustainable and responsible growth

Final remarks

7 | Capital Markets Day - March 6th 2012

Intensive exploration activities led to the identification of new drilling targets

World-class gas discovery in Rovuma basin, Mozambique

First development steps taken in Lula field, Brazil, exceeding expectations

Increasing our upstream portfolio potential in 2011

8 | Capital Markets Day - March 6th 2012

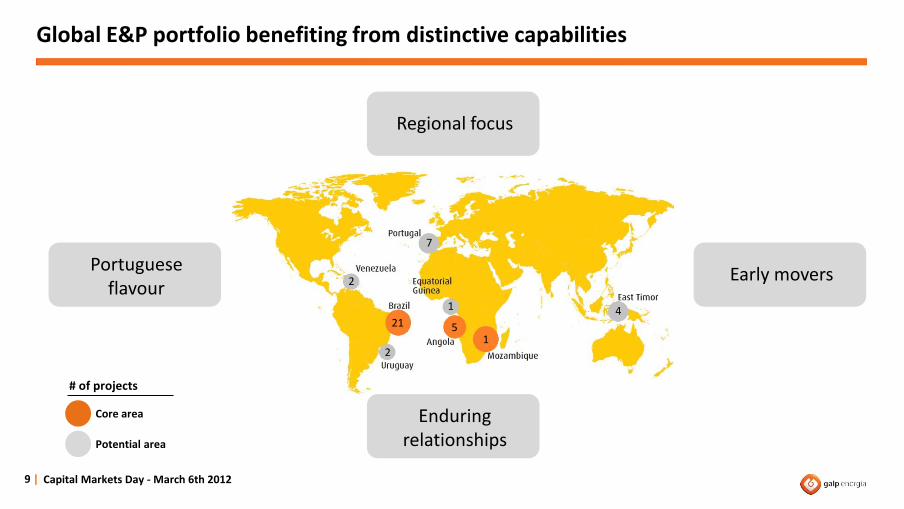

Global E&P portfolio benefiting from distinctive capabilities

9 | Capital Markets Day - March 6th 2012

Regional focus

Early movers Portuguese flavour 2

21

2

5

7

1

1

4

Core area

Potential area

# of projects

Enduring relationships

2,550

2,821

2010 2011

Exploration focus to enhance and enlarge current portfolio

Still a lot to take from current high potential exploration portfolio

Looking to enlarge portfolio

Focus on high risk/high reward exploration areas

Galp Energia to leverage on key distinctive capabilities

Exploration team allocating c.30% of its time to analyse new opportunities

10 | Capital Markets Day - March 6th 2012

Exploration resources1 (Mln Boe)

1 Mean unrisked estimate

Source: DeGolyer and MacNaughton @ 31/12/2011

+ 11%

574

709

2010 2011

2,356

2,672

2010 2011

Continuously adding resources and reserves to portfolio

11 | Capital Markets Day - March 6th 2012

3C contingent resources1 (Mln Boe) 3P reserves2 (Mln Boe)

1 Working interest 3C resources

2 Net entitlement 3P reserves Source: DeGolyer and MacNaughton @ 31.12.2011

+ 13%

+ 24%

Building certainty on high-reward projects

12 | Capital Markets Day - March 6th 2012

Faster Lula development on better reservoir data

Clear path outlined Ambition confirmed

20

11

ac

hie

vem

en

ts

WI production (kboepd)

21

2011

300

2020 target

+

+

70

2015E

Delivering profitable growth on current E&P portfolio

13 | Capital Markets Day - March 6th 2012

Strategic partnerships delivering outstanding value

Exploration in core areas being intensified

Enlarging exploration portfolio through new ventures

Still a lot to know and to take from current Brazilian portfolio

Resource base increased to 6.2 Bln boe

Upstream growth supported by downstream sound foundations

14 | Capital Markets Day - March 6th 2012

Refining & Marketing Gas & Power

245 MW of total

capacity installed by

2012

1,200 GWh of annual

electrical power

generation

Sourcing agreement of

6 bcm of natural gas

2nd natural gas player

in Iberia with over 1.3

Mln clients

11,655 km of NG

distribution network

3rd player in Iberia

1,502 service stations

and 595 non fuel

stores in Iberia and in

Africa

Annual sales of c.16

Mln tons of refined

products

Total refining capacity

of 330 kbpd

Nelson complexity of

7.71 in Sines refinery

and 10.7 in

Matosinhos refinery

1 Post-upgrade complexity index. Nelson complexity before the upgrade of 6.3 in Sines

1.310.62 0.85

-0.04

1Q11 2Q11 3Q11 4Q11

Refining margin pre-upgrade Refining margin post-upgrade

Upgrade to increase refining profitability

Refining business fundamental to our integrated player strategy

€1.4 Bln project to start generating returns from mid-2012

Upgrade crucial considering the current refining environment

Incremental refining margin throughout 2011 would have ranged between $2.5-$3.5/bbl

15 | Capital Markets Day - March 6th 2012

Galp Energia refining margin1 ($/bbl)

Range ≈ $2.5-$3.5/bbl

1 Assuming 2011 market conditions

Downstream businesses will face important challenges

16 | Capital Markets Day - March 6th 2012

Refining & Marketing Gas & Power

Guarantee successful integration of refining system

Deliver Sines post-upgrade steady production

Improve the marketing business performance

Strengthen the business in Africa

Maintain key competitive advantages in Iberia

Strengthen natural gas leading position by raising focus on trading and supply businesses

Start-up of Matosinhos cogeneration

Current European and Iberian adverse environment

Progressive increase of competition

Endogenous

Exogenous

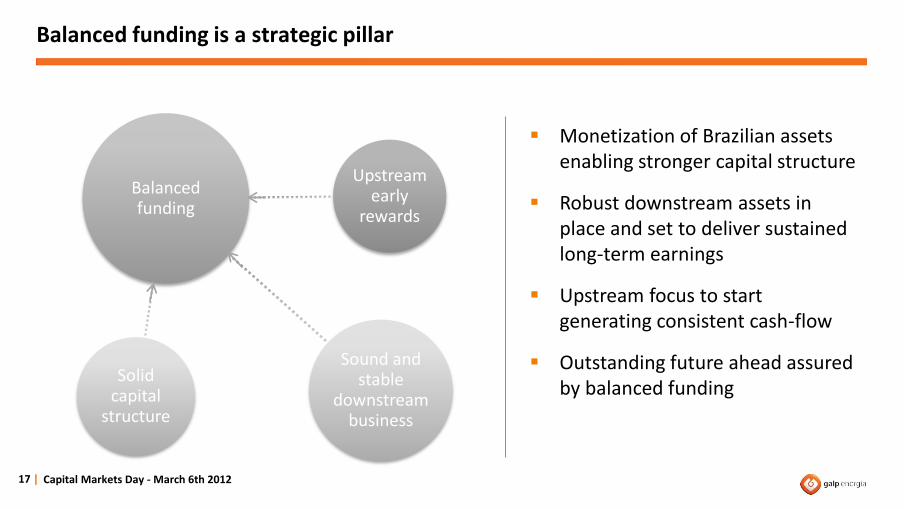

Monetization of Brazilian assets enabling stronger capital structure

Robust downstream assets in place and set to deliver sustained long-term earnings

Upstream focus to start generating consistent cash-flow

Outstanding future ahead assured by balanced funding

Balanced funding is a strategic pillar

17 | Capital Markets Day - March 6th 2012

Balanced funding

Upstream early

rewards

Solid capital

structure

Sound and stable

downstream business

Exciting future ahead supported by robust fundamentals

18 | Capital Markets Day - March 6th 2012

Outstanding exploration

potential

Delivering high

potential projects

Sound downstream

business

Solid capital

structure

Upstream profitable growth Balanced funding

Delivering on our strategy

Solid foundations in place

Ensuring sustainable and responsible growth

Final remarks

19 | Capital Markets Day - March 6th 2012

Sustainability fully integrated into our strategic decision making process

20 | Capital Markets Day - March 6th 2012

Getting the best from our people

Placing safety at the heart of our operations

Giving back to society

Responsible approach allows for

higher competitiveness,

corporate risk reduction and

enables social development

Growing with better energy

Getting the best from our people

21 |

Reservoir geoengineering advanced programme

Capital Markets Day - March 6th 2012

Leading highly skilled teams to deliver competitive performance

Partnering with renowned Portuguese and Brazilian universities to implement innovative training programmes

Promoting and developing expertise, namely in E&P and in refining businesses, through advanced training courses

Safety performance

Placing safety at the heart of our operations

Safety management showing continuous improvement, with industry-leading LTIFR

Integrated HSE management system implemented in 2006

Safety oriented training averaging more than 24,000 hours per year since 2006

HSE performance measured across all business segments

22 | Capital Markets Day - March 6th 2012

R&M 64%

4037

312.6

1.21.0

2009 2010 2011

Accidents resulting in work absence

Lost time injury frequency rate (LTIFR)

1 LTIFR is measured as the number of lost time accidents during the year per million hours worked (includes employees and contractors)

1

Actively managing our environmental footprint

23 | Capital Markets Day - March 6th 2012

R&M 64%

CO2 emissions (kton)

Leaving a smaller environmental footprint, actively managing CO2

emissions

Losses of containment index

Ecological preservation guides our activities, with good results within

API-754 performance indicator1

1 Recommended practice API 754 – Process Safety Performance Indicators identifies process safety indicators, particularly regarding the refining and petrochemical industry, where losses of containment has the potential to cause harm. Tier 1 and tier 2 represent those events which potential consequences are the most harmful. 2010 figures

0.350.87

2.24

2.71

Galp Energia CONCAWE

Tier 1 Tier 2

3,1402,941

2010 2011

Downstream Upstream

Growing with better energy

24 | Capital Markets Day - March 6th 2012

More than operating energy efficiently, we educate towards a

more sustainable world

Energy efficiency Biofuels

Over 13,000 hectares planted with Palma in Brazil and around 1,000

hectares with Jatropha in Mozambique

Giving back to society

25 |

End Hunger, Walk the World - Swaziland

Capital Markets Day - March 6th 2012

Sponsoring health initiatives that are vital to local communities

Eradicating social exclusion

Intensifying educative initiatives in Africa, namely through scholarships

Taking action towards sustainable mobility in Portugal

Actively promoting corporate volunteering

Galp Energia guided by sustainability

26 | Capital Markets Day - March 6th 2012

Sustainability incorporated into strategy and our daily routines

Galp Energia is a sustainable company, with related practices within the industry top 15%

Highly sustainable practices are already a reality, but there’s still progress to be made

Continuous improvement recognized by SAM Group, having achieved the qualification of Sector Mover 2012

Delivering on our strategy

Solid foundations in place

Ensuring sustainable and responsible growth

Final remarks

27 | Capital Markets Day - March 6th 2012

Solid foundations to deliver sustainable value

28 | Capital Markets Day - March 6th 2012

Continuously delivering on our strategy

Clearing the ground on a well defined strategic path

Incorporating high responsible practices and leading our people further

Creating shareholder value through key strategic pillars

Financial outlook Claudio De Marco Chief Financial Officer

Capital Markets Day - March 6th 2012

Page 29

Financial slack successfully achieved

Capital allocation towards upstream

Project delivery enhancing cash generation

Committed to a sound capital structure

New sustainable dividend policy

Final remarks

Appendix

30 | Capital Markets Day - March 6th 2012

Solid foundations built over years of demanding capex

Downstream transformational projects responsible for financial effort

High potential upstream projects being developed

Gearing level increased rapidly

2011 net debt to equity of 119%

31 | Capital Markets Day - March 6th 2012

Gearing evolution

0%

150%

0

600

1,200

1,800

2008 2009 2010 2011

Capex (€Mln) (lhs) Net debt/equity (rhs)

A cash in of $5.2 bln

Sinopec to hold 30% of Petrogal Brasil1, after the subscription of the capital increase

Partnership with one of the largest energy groups worldwide

Development of Brazilian projects fully funded

32 | Capital Markets Day - March 6th 2012

Galp Energia’s Brazilian portfolio

1 Petrogal Brasil and other related subsidiaries

Transaction executed in a challenging market environment

Financial environment deteriorated

Several interested parties in the deal, but few committed bidders

Implicit valuation of $12.5 bln based on a minority stake of 30%

Control and full consolidation of Petrogal Brasil1 maintained

33 | Capital Markets Day - March 6th 2012

Galp Energia’s Brazilian assets

Basin # projects % Galp Energia Operator

Potiguar 5 20% Petrobras

Santos

6 10-20% Petrobras

Espírito Santo 1 20% Petrobras

Pernambuco 3 20% Petrobras

Campos 1 15% Petrobras

Potiguar

Sergipe-Alagoas

Amazonas

5 40-50% Petrobras/Galp

Offshore

Onshore

1 Petrogal Brasil and other related subsidiaries

Flexibility to manage extra-cash at the holding level

Brazilian transaction ending a period of stretched balance sheet

10% to 20% of $4.8 bln to be retained to fund short-term capex needs

The remaining to be lent to shareholders on a pro-rata basis with reimbursements according to capex execution

34 | Capital Markets Day - March 6th 2012

Sinopec

Petrogal Brasil1

Galp Energia (70%)

Sinopec (30%)

$0.4 bln Intragroup loan reimbursement

1 Petrogal Brasil and other related subsidiaries

$4.8 bln

As a loan

Control and full consolidation maintained

Petrogal Brasil’s Board of Directors to be appointed proportionally by Galp Energia and Sinopec

Full consolidation of operations by Galp Energia

Net profit at the holding level impacted by Sinopec’s 30% share accounted in minority interests

Capex to be fully accounted at Galp Energia’s level

35 | Capital Markets Day - March 6th 2012

Financial slack successfully achieved

Capital allocation towards upstream

Project delivery enhancing cash generation

Committed to a sound capital structure

New sustainable dividend policy

Final remarks

Appendix

36 | Capital Markets Day - March 6th 2012

Capital allocation reflects the Company’s strategic path

Absorbing only maintenance capex

Investing towards higher operational safety and energy efficiency

37 | Capital Markets Day - March 6th 2012

Upstream Downstream

Reinforcing exploration budget to address new opportunities

Developing world class projects

2012: a year of capital allocation shift towards upstream

38 | Capital Markets Day - March 6th 2012

Capex by segment

€1 - €1.2bln

2011 2012

€1bln

E&P R&M G&P

2013 - 2016

c.€1.2bln/year

Brazil Mozambique

Angola Other and new ventures

Strengthening and diversifying our exploration portfolio

39 | Capital Markets Day - March 6th 2012

E&P capex 2012 exploration capex

2011 2012

Exploration Development

Financial slack successfully achieved

Capital allocation towards upstream

Project delivery enhancing cash generation

Committed to a sound capital structure

New sustainable dividend policy

Final remarks

Appendix

40 | Capital Markets Day - March 6th 2012

Strong cash generation from projects already implemented

Stable contribution from R&M business uplifted by upgrade project

G&P business to maintain solid contribution to earnings

41 | Capital Markets Day - March 6th 2012

Earnings growth by developing upstream projects

Oil price exposure increasing on cash generation

Upstream Downstream

Ebitda growth supported by upstream production ramp up

Strategy path to be materialized in earnings from 2012 onwards

42 | Capital Markets Day - March 6th 2012

Ebitda by segment

2012 2016

€0.9 – 1.1Bln

E&P R&M G&P

2011

CAGR1 ≈25% €0.8 Bln

1 CAGR 2011-2016

2011 2016

Iberia Other areas

Exposure to Iberian economic environment will decrease going forward

43 | Capital Markets Day - March 6th 2012

Ebitda 2011 vs 2016

>60%

<35%

Financial slack successfully achieved

Capital allocation towards upstream

Project delivery enhancing cash generation

Committed to a sound capital structure

New sustainable dividend policy

Final remarks

Appendix

44 | Capital Markets Day - March 6th 2012

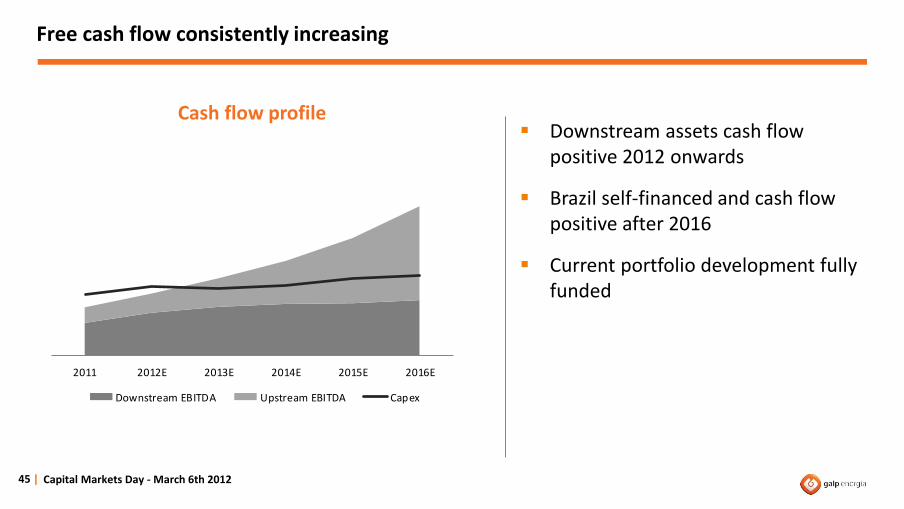

2011 2012E 2013E 2014E 2015E 2016E

Downstream EBITDA Upstream EBITDA Capex

Free cash flow consistently increasing

Downstream assets cash flow positive 2012 onwards

Brazil self-financed and cash flow positive after 2016

Current portfolio development fully funded

45 | Capital Markets Day - March 6th 2012

Cash flow profile

Sustainable and balanced capital structure going ahead

46 | Capital Markets Day - March 6th 2012

Net debt to equity

Source: Bloomberg 1 Assumes loan to Sinopec 2 Peers average includes Eni, BG Group, Repsol, OMV, Total, BP, Royal Dutch Shell and Petrobras

2 1

One of the most robust capital structures amongst peers

119%

<10%

37%<30%

2011 2011pro-forma

2011Peer average

Galp Energia target

Financial management to ensure a sound and flexible capital structure

47 | Capital Markets Day - March 6th 2012

Building up company’s flexibility

Mitigating execution risk

Enabling new venture

opportunities

Rewarding shareholders

Start of a new growth era with a sound capital structure

Financial slack successfully achieved

Capital allocation towards upstream

Project delivery enhancing cash generation

Committed to a sound capital structure

New sustainable dividend policy

Final remarks

Appendix

48 | Capital Markets Day - March 6th 2012

2007-2008 2009-2011 2012E 2013E 2014E 2015E 2016E

Rewarding shareholders through a consistent growing dividend

49 | Capital Markets Day - March 6th 2012 Dividend relates to net income of the corresponding financial year and not to the payment year 1 CAGR 2011-2016

€0.32/ share

€0.20/ share

Dividend policy to be driven by an era of progressive earnings growth

Financial slack successfully achieved

Capital allocation towards upstream

Project delivery enhancing cash generation

Committed to a sound capital structure

New sustainable dividend policy

Final remarks

Appendix

50 | Capital Markets Day - March 6th 2012

Commitment to maintain a sound financial position is a key strategic foundation

The start of a new growth era with a solid balance sheet

Execution risk mitigated and enhanced flexibility in project development

Cash flow from world class projects coming on-stream

Well balanced cash flow mix

Consistent dividend policy in line with further growth

51 | Capital Markets Day - March 6th 2012

Financial slack successfully achieved

Capital allocation towards upstream

Project delivery enhancing cash generation

Committed to a sound capital structure

New sustainable dividend policy

Final remarks

Appendix

52 | Capital Markets Day - March 6th 2012

2010 2011 Average 2012-2016

Oil price $/bbl 79.5 111 95

Benchmark refining margin $/bbl1 2.66 1.33 2.41

EUR:USD 1.33 1.39 1.40

Mid-cycle assumptions

2012-2016 Business plan assumptions

53 | Capital Markets Day - March 6th 2012

1 New post-upgrade benchmark refining margin = 42.5% cracking margin + 45.0% hydrocracking margin + 5.5% aromatics margin+ 7.0% base oils margin

Capital Markets Day - March 6th 2012

Upstream growth Fernando Gomes Executive Director

Page 54

A focused E&P strategy

Resources and targets

High potential exploration assets

Delivering world class development projects

55 | Capital Markets Day - March 6th 2012

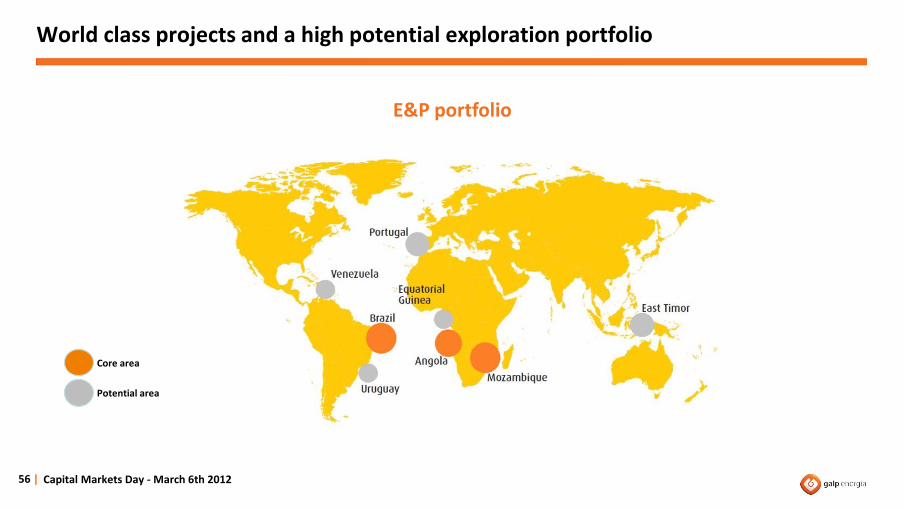

World class projects and a high potential exploration portfolio

56 | Capital Markets Day - March 6th 2012

Core area

Potential area

E&P portfolio

Capturing value from early exploration to production

57 | Capital Markets Day - March 6th 2012

Exp

lora

tio

n

Ap

pra

isal

Dev

elo

pm

ent

Pro

du

ctio

n

E&P projects lifecycle

cumulative value creation

Galp Energia is present in the entire upstream value chain

Focus on de-risking exploration assets

58 |

Project screening process R

isk

Potential

Capital Markets Day - March 6th 2012

Focus on high-risk / high-reward projects

Screening the most relevant projects to be developed first

Continuous de-risking process

Adding value to consortium decision making process

Ensuring financial discipline and funding flexibility

-

+ + -

Galp Energia is well positioned for future delivery

59 | Capital Markets Day - March 6th 2012

First mover advantage

Low entry costs

Leverage Portuguese flavour

Strategic partnerships with knowledgeable operators

Commitment to safe operations and best HSE practices

Highly qualified E&P team

Solid track record in identifying, accessing and delivering high potential and unexplored basins

Knowledge on deepwater projects

Strong resource base

Delivering value in high risk/high reward areas

Exploration footprint Exploration status

Enlarging our presence in key geographies with competitive advantages

Focus on well-known geologies and geographies

Access to new acreage in specific areas based on geological, regulatory, fiscal and political contexts

Aim to access areas with more material stakes while preserving a diversified portfolio

5

1 21

Brazil

Angola

Mozambique

Key geographies of the E&P portfolio

60 | Capital Markets Day - March 6th 2012

A focused E&P strategy

Resources and targets

High potential exploration assets

Delivering world class development projects

61 | Capital Markets Day - March 6th 2012

494 478

2,5502,821

2010 2011

Drilling activity throughout 2012 expected to unlock more than 100 Mln boe

62 | Capital Markets Day - March 6th 2012

Exploration resources1 (Mln boe)

Several high impact prospects identified within Galp Energia’s portfolio

Other areas

Other Brazil

Santos basin

1 Mean estimate Source: DeGolyer and MacNaughton @ 31/12/2011

+ 11%

Unrisked

Risked

172 202

754 870

2,356

2,672

2010 2011 2010 2011 2010 2011

Outstanding exploration delivery translated into contingent resources upgrade

63 | Capital Markets Day - March 6th 2012 1 Working interest resources Source: DeGolyer and MacNaughton @ 31/12/2011

1C 2C 3C

Contingent resources1 (Mln boe)

+ 17%

+ 15%

+ 13%

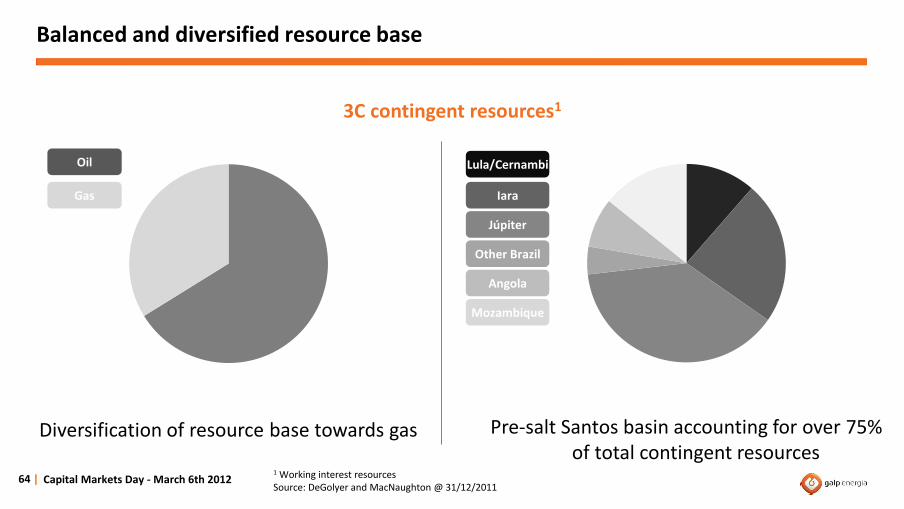

Balanced and diversified resource base

64 | Capital Markets Day - March 6th 2012

Gas

Oil

3C contingent resources1

1 Working interest resources Source: DeGolyer and MacNaughton @ 31/12/2011

Iara

Lula/Cernambi

Júpiter

Other Brazil

Angola

Mozambique

Diversification of resource base towards gas Pre-salt Santos basin accounting for over 75% of total contingent resources

128 145

397 399

574

709

2010 2011 2010 2011 2010 2011

Continuously de-risking contingent resource base

65 | Capital Markets Day - March 6th 2012

Reserves1 (Mln boe)

1Net entitlement reserves Source: DeGolyer and MacNaughton @ 31/12/2011

+ 14%

+ 0%

+ 24%

1P 2P 3P

Lula and Cernambi fields are the main contributors to reserve base

66 | Capital Markets Day - March 6th 2012

3P reserves1

1 Net entitlement reserves Source: DeGolyer and MacNaughton @ 31/12/2011

Gas

Oil

Angola

Brazil

Gas reserves accounts for c.15% of total Lula and Cernambi development projects continuously gaining relevance

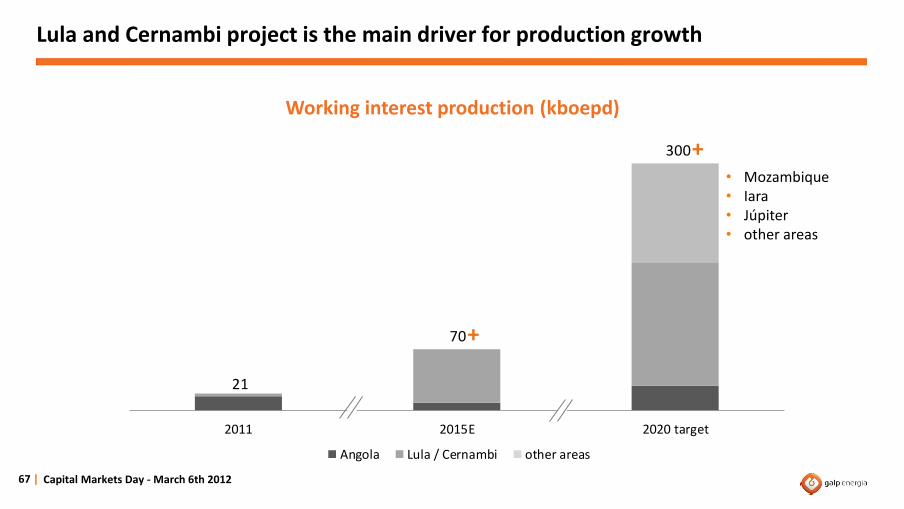

Lula and Cernambi project is the main driver for production growth

67 | Capital Markets Day - March 6th 2012

Working interest production (kboepd)

21

70

300

2011 2015E 2020 target

Angola Lula / Cernambi other areas

• Mozambique • Iara • Júpiter • other areas

+

+

Capital Markets Day - March 6th 2012

High potential exploration assets Roland Muggli Head of Exploration

Page 68

A focused E&P strategy

Resources and targets

High potential exploration assets

Delivering world class development projects

69 | Capital Markets Day - March 6th 2012

Over 100 prospects and leads currently in exploration funnel

70 | Capital Markets Day - March 6th 2012

Screen Evaluate Drilling Appraisal

Amazonas

New ventures

Pernambuco

Alentejo

Peniche Campos

Carcará

Bracuhy

Caramba

East Timor

Iara Júpiter

Block 141

Block 331

Block 14K1

Mozambique Angola LNG II

Potiguar

Espírito Santo

Uruguay

Block 321

1 projects at pre-development phase

Still a lot of upside potential from current exploration portfolio

71 | Capital Markets Day - March 6th 2012

Exploration portfolio – potential/risk profile

Lower resource potential

Hig

her

ris

k

Low

er r

isk

Higher resource potential

Blocks 32/33

Peniche basin Uruguay

Blocks 14/ 14K Campos basin

Espírito Santo basin

Amazonas basin

Mozambique

Alentejo basin

East Timor

Pernambuco basin Potiguar basin

BM-S-8

Júpiter

Caramba

112 prospects and leads identified within Galp Energia portfolio

Mozambique embraces a world class province

Mamba South-1 and North-1 wells discovered gas in place resources of up to 30 Tcf

Excellent reservoir characteristics in terms of porosity and permeability

Mamba North-1 test flowed 1 mln m3/d (35 mmscf/d) constrained by test equipment

Test also produced condensate in minor quantities

Rovuma basin discoveries

72 | Capital Markets Day - March 6th 2012

Intense exploration and appraisal campaign in place

Back-to-back drilling of 5 exploration/appraisal wells in 2012 with testing operations

Plan to also test a separate Eocene/Paleocene prospect not connected to Mamba structure

Block holds additional prospectivity warranting continued exploration during 2013

73 |

Area 4 discoveries

Capital Markets Day - March 6th 2012

Key Júpiter NE appraisal well in 2012

Júpiter discovery well found a reservoir of significant oil, condensate and gas with CO2 content

Júpiter NE appraisal well expected to be drilled in 2H2012 testing a thicker pre-salt reservoir section

Primary aim is to assess CO2 distribution and thickness of oil rim

Potential for large upside if field-wide OWC deeper than estimated in Júpiter well, not included in exploration resources

74 |

BM-S-24

Capital Markets Day - March 6th 2012

Testing Caramba resource upside in 2013

Caramba well in 2007 found a reservoir of light oil

Caramba pre-salt discovery with significant updip potential

Plan to drill Caramba Sul appraisal well in 2013

Expected DoC by April 2015

75 | Capital Markets Day - March 6th 2012

BM-S-21

3rd exploration well outcome is key to support a development plan

Evaluation plan for 2,432 km2

Two exploration wells to date encountered high API pre-salt oil in Bem-Te-Vi and Biguá accumulations

3rd exploration well, Carcará currently being drilled

Results will be an important contributor towards DoC in December 2012

76 | Capital Markets Day - March 6th 2012

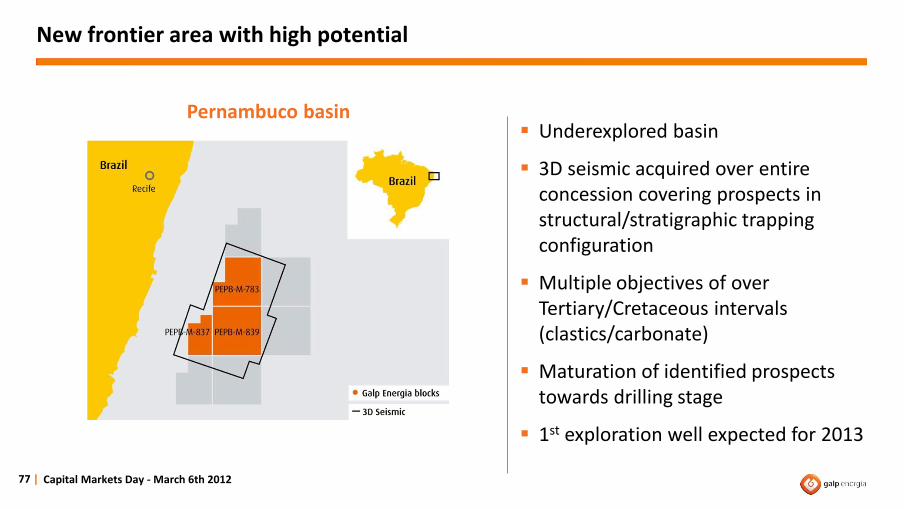

BM-S-8

New frontier area with high potential

Underexplored basin

3D seismic acquired over entire concession covering prospects in structural/stratigraphic trapping configuration

Multiple objectives of over Tertiary/Cretaceous intervals (clastics/carbonate)

Maturation of identified prospects towards drilling stage

1st exploration well expected for 2013

77 | Capital Markets Day - March 6th 2012

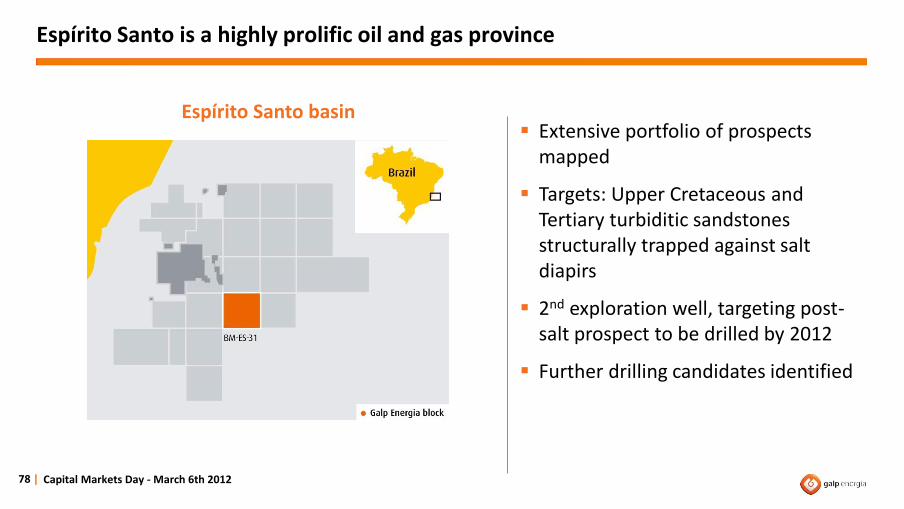

Pernambuco basin

Espírito Santo is a highly prolific oil and gas province

Extensive portfolio of prospects mapped

Targets: Upper Cretaceous and Tertiary turbiditic sandstones structurally trapped against salt diapirs

2nd exploration well, targeting post-salt prospect to be drilled by 2012

Further drilling candidates identified

78 | Capital Markets Day - March 6th 2012

Espírito Santo basin

New frontier province with significant resource potential

Two contracts including stakes in five blocks, covering an acreage of 3,736 km2

Prolific shallow waters area located near Brazilian equatorial margin

9 prospects identified in water depths of 1,500m in a predominantly stratigraphic setting (Cretaceous clastics)

1st exploration well, Ararauna, to be drilled in 2012

79 | Capital Markets Day - March 6th 2012

Potiguar basin

Exploration phase extended in East Timor

Timor island accretionary wedge and foreland basin (Northern Bonaparte)

First frontier exploration well Cova-1 in 2011 was considered to be non-commercial

Well data allowed to re-evaluate entire concession including deeper plays (Permian, Triassic)

Extension of current exploration phase until November 2012 allows to mature identified prospects towards drill or drop decision

80 | Capital Markets Day - March 6th 2012

East Timor

Alentejo basin exploration drilling to start as early as 2013

Mesozoic rift basin with large structures identified

1,800 km2 of 3D seismic with excellent quality acquired in 2011

Several prospects identified with significant resource potential

Drilling decision for the 1st exploration well to be taken in 2012

81 | Capital Markets Day - March 6th 2012

Alentejo basin

Exploration activities still in early stages

82 | Capital Markets Day - March 6th 2012

Uruguay 6,290 km of 2D seismic over Blocks 3

and 4 in Punta del Este basin

2D seismic evaluation ongoing with focus on Tertiary stratigraphic and Paleozoic syn-rift plays

Several leads identified with significant upside potential

Basin modelling to assess charge uncertainty

Next milestone: decision on 3D seismic acquisition

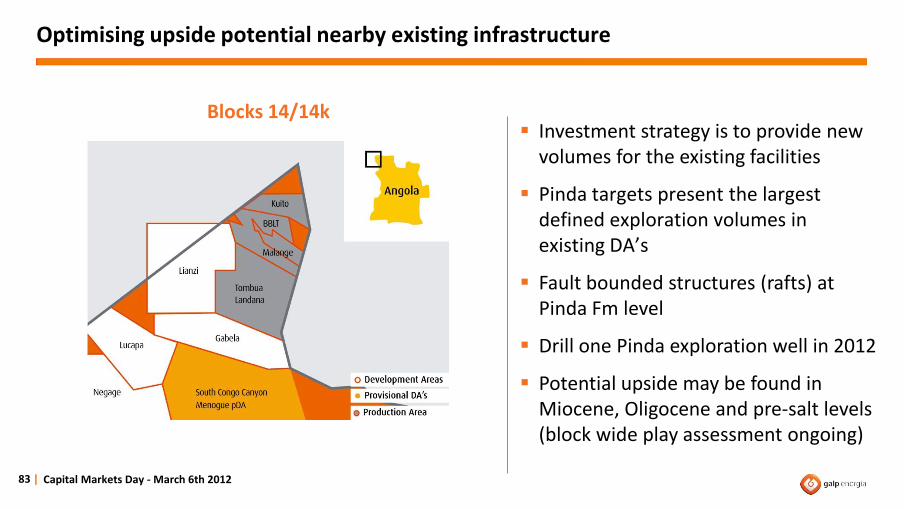

Optimising upside potential nearby existing infrastructure

Investment strategy is to provide new volumes for the existing facilities

Pinda targets present the largest defined exploration volumes in existing DA’s

Fault bounded structures (rafts) at Pinda Fm level

Drill one Pinda exploration well in 2012

Potential upside may be found in Miocene, Oligocene and pre-salt levels (block wide play assessment ongoing)

83 | Capital Markets Day - March 6th 2012

Blocks 14/14k

Evaluation program on track in blocks 32 and 33

Block 32

Five year exploration program to develop 2nd hub in block 32

Two exploration/appraisal wells in 2H12 (Gengibre-3 / Caril -2)

Oligocene/Miocene channels in mixed trapping configuration

84 | Capital Markets Day - March 6th 2012

Blocks 32/33

Block 33

One exploration well Sumate-1 to be drilled in March 2012 in block 33

1Q 2Q 3Q 4Q

Lula

Cernambi

Iara

BM-S-8

BM-S-24

Potiguar offshore

BM-ES-31

Block 14

Block 32

Block 33

LNG II

Mozambique Rovuma

Brazil

Angola

2012TotalCountry Area

More than 20 exploration and appraisal wells to drill in 2012

85 | Capital Markets Day - March 6th 2012

A A A

A

A

E

E

A

E

E

E A

E

A A A

E A A E E/A E/A

3

1

1

1

1

1

1

1

2

1

3

6

22

1 1 1

1

1

1 1

1Development de-risking wells

Delivering world class development projects Carlos Alves Head of Exploration & Production

A focused E&P strategy

Resources and targets

High potential exploration assets

Delivering world class development projects

87 | Capital Markets Day - March 6th 2012

Development options being analysed according to SEE approach

Distance to onshore just 40 km

Multi-train LNG train development scenarios are being developed

Unitisation discussions with area 1 shall take place in near future

Flow rates expected to be up to 4 Mln m3/d (150 mmscf/d) during production phase

High quality reservoir enhances flow and recovery rates, with impact on capex needs

88 | Capital Markets Day - March 6th 2012

Area 4 location

SEE: Social, Environmental, Economic impact

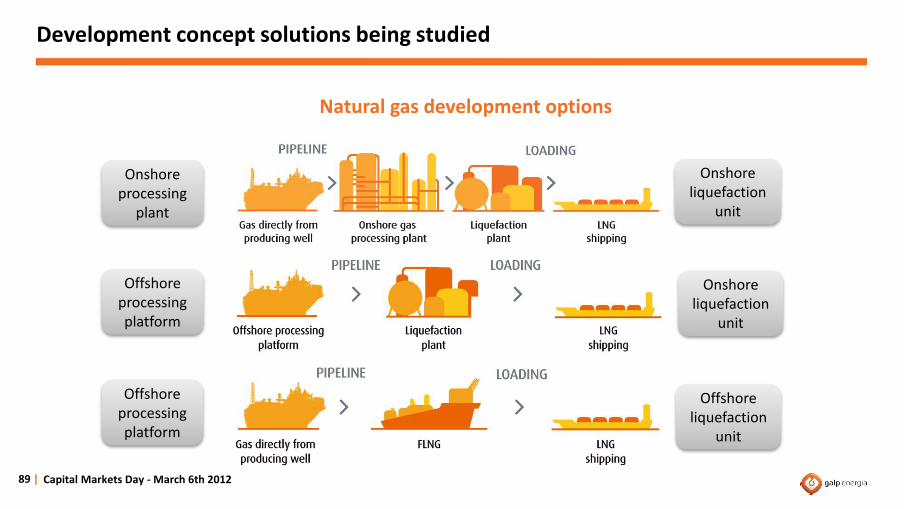

Development concept solutions being studied

Offshore processing platform

Onshore processing

plant

Offshore processing platform

Onshore liquefaction

unit

Onshore liquefaction

unit

Offshore liquefaction

unit

Natural gas development options

Capital Markets Day - March 6th 2012 89 |

Location near interesting LNG consumption markets

Global LNG market expected to double to c.400 Mtpa in 2020

Interesting geographical location to target the growing demand from Asian market

Leverage on partners and in-house Angolan and Brazilian experience to develop and market natural gas

Gas commercial production expected to start by 2018

90 | Capital Markets Day - March 6th 2012

LNG markets

Primary market targets

Pre-salt province revealed key success characteristics

Galp Energia benefited from being within the first movers into the pre-salt area

Seven discoveries within pre-salt layer in four blocks

Presence since 2000 starting to materialize

Significant upside potential from forthcoming appraisal and development activities

91 | Capital Markets Day - March 6th 2012

Pre-salt Santos basin

Potentially material appraisal activity underway in Júpiter

Gross 3C contingent resources above 5 bln boe1, of which 1/3 oil, 1/3 condensates and 1/3 natural gas

High CO2 content and to be studied by Jupiter NE appraisal well

EWT in Júpiter area expected for 2015

Expected DoC until February 2016

92 | Capital Markets Day - March 6th 2012

BM-S-24

1 Source: DeGolyer and MacNaughton @ 31/12/2011

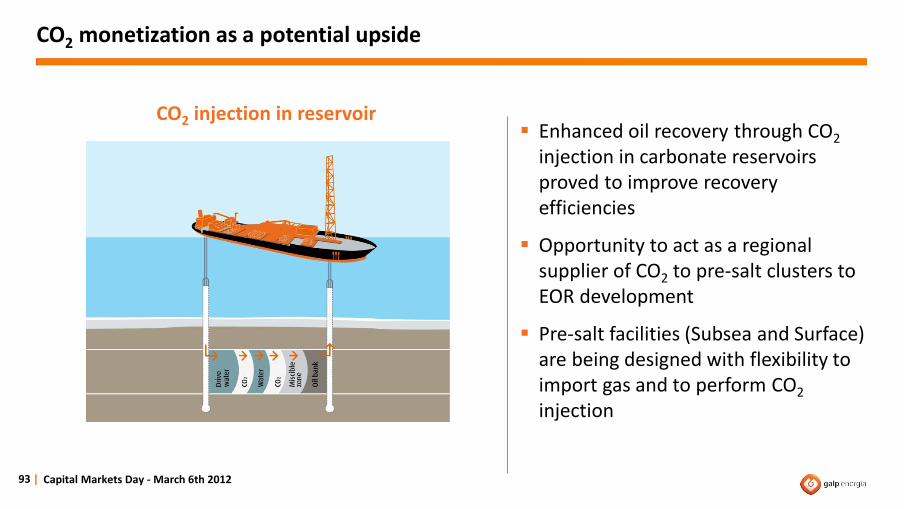

CO2 monetization as a potential upside

Enhanced oil recovery through CO2 injection in carbonate reservoirs proved to improve recovery efficiencies

Opportunity to act as a regional supplier of CO2 to pre-salt clusters to EOR development

Pre-salt facilities (Subsea and Surface) are being designed with flexibility to import gas and to perform CO2 injection

93 |

CO2 injection in reservoir

Capital Markets Day - March 6th 2012

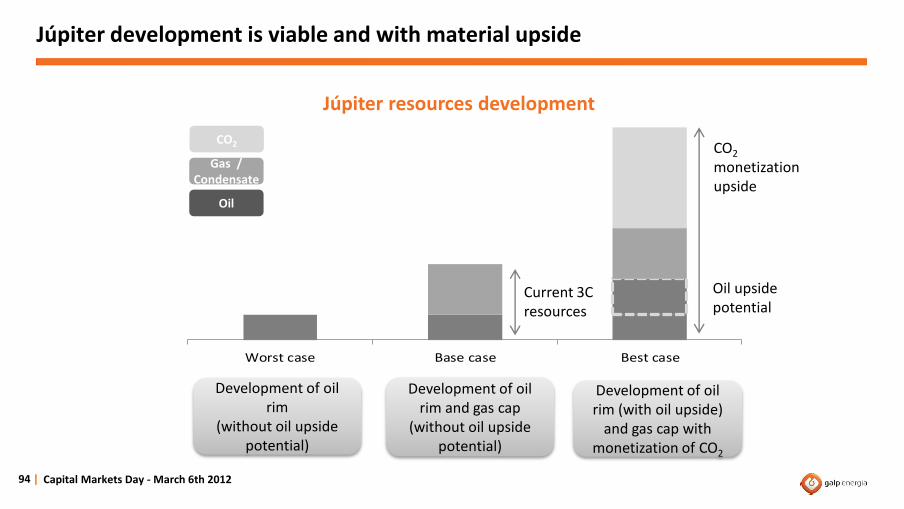

Worst case Base case Best case

Júpiter development is viable and with material upside

94 | Capital Markets Day - March 6th 2012

CO2 monetization upside

Development of oil rim (with oil upside)

and gas cap with monetization of CO2

Development of oil rim

(without oil upside potential)

Development of oil rim and gas cap

(without oil upside potential)

CO2

Gas / Condensate

Oil

Oil upside potential

Current 3C resources

Júpiter resources development

Appraisal activities confirmed Iara’s potential

Two wells drilled so far found a reservoir of oil with high quality

Reservoir rocks composed of microbial carbonates from sag and rift sections

Formation tests on Iara Horst registered good quality data

3-4 bln boe with upside potential

95 |

Iara field

Capital Markets Day - March 6th 2012

Drilling performance with high angle wells encourages application in Iara

Potential upside through multi-lateral and horizontal drilling on development phase in a cost effective manner

Technology being tested currently in Lula field

Potential for upward revision of recoverable resources

96 |

Drilling optimization

Capital Markets Day - March 6th 2012

Development of Iara being studied

Iara West currently being drilled with results expected during 2Q12 targeting a structure with potentially better reservoir characteristics

Intensive activity gathering information to prepare the development plan

EWT planned in the sequence of Iara West results

Expected DoC by December 2013

97 | Capital Markets Day - March 6th 2012

Iara field

Lula/Cernambi project has been a successful journey

98 | Capital Markets Day - March 6th 2012

• BM-S-11 awarded

• Tupi discovery

• First EWT

• Iracema discovery

• First oil from 1st pilot FPSO

• Lula/Cernambi DoC

2000

2006

2009

2010 2011

2012 and beyond

• First international oil sale

• First gas commercialization

Significant progress achieved in 2011

Appraisal activity during 2011 revealed better reservoir characteristics than initially expected

Initial flow capacity above expectations

EWT in Lula NE confirmed the productivity achieved in previous tests

Currently performing the 1st EWT in Cernambi South area

FPSO BW Cidade de São Vicente

99 | Capital Markets Day - March 6th 2012

Fast development of a world-class project

Lula – 1 project to reach full capacity in March

Four producing wells and one gas injection well to be in place at the end of March

Two WAG injection wells to be connected to FPSO Cidade de Angra dos Reis in 2012

Ready to connect highly deviated well (P8H) in 2013

100 |

Lula-1 project

Capital Markets Day - March 6th 2012

FPSO deployment in Lula/Cernambi

Infrastructure secured to support project development

2nd and 3rd production units being converted and expected to be on stream by 2Q13 and 2014 respectively

Works for the deployment of the six hulls already started at Rio Grande shipyard

FPSO deliveries on time to support the fast development of Lula/Cernambi project

Six rigs permanently allocated to BM-S-11 by YE2011

101 | Capital Markets Day - March 6th 2012

Lula/Cernambi production of c.1,500 kboepd in 2020

Production profile based on current technological achievements

Better reservoir characteristics allowed the upwards revision of production target

Knowledge acquired with Lula-1 will be key in accelerating the development of subsequent producing units

102 | Capital Markets Day - March 6th 2012

0

1,000

2,000

2012E 2013E 2014E 2015E 2016E 2017E 2018E 2019E 2020E

Lula/Cernambi production profile (kboepd)

Significant and reachable upside potential on Lula/Cernambi project

WAG alternative ready to be tested in Lula-1 from 2012 onwards

Each 1 p.p. increase in recovery factor results in an incremental c.300 Mboe of recoverable volumes

Potential for further capacity de-bottlenecking through sub-sea equipments

Potential for further economies of scale

103 |

Subsea equipment

Capital Markets Day - March 6th 2012

Angola is currently a development story

Presence in Angola rewarded with 26 discoveries

Three fields already under production: Kuito, BBLT and Tômbua-Lândana

Current projects already reached peak production

Further production increase will be driven by new projects already identified

Angola blocks

104 | Capital Markets Day - March 6th 2012

Five areas still to be developed

Kuito, BBLT and Tômbua-Lândana reaching mature phase

Lianzi, Malange and Lucapa first oil expected to occur between 2014 and 2017

Development scenarios based on both tie-backs and new FPSO production unit

World-class technical breakthroughs: Congo river crossing gas export project and Lianzi DEH flowlines application

105 | Capital Markets Day - March 6th 2012

Blocks 14/14K

From exploration success into development stage

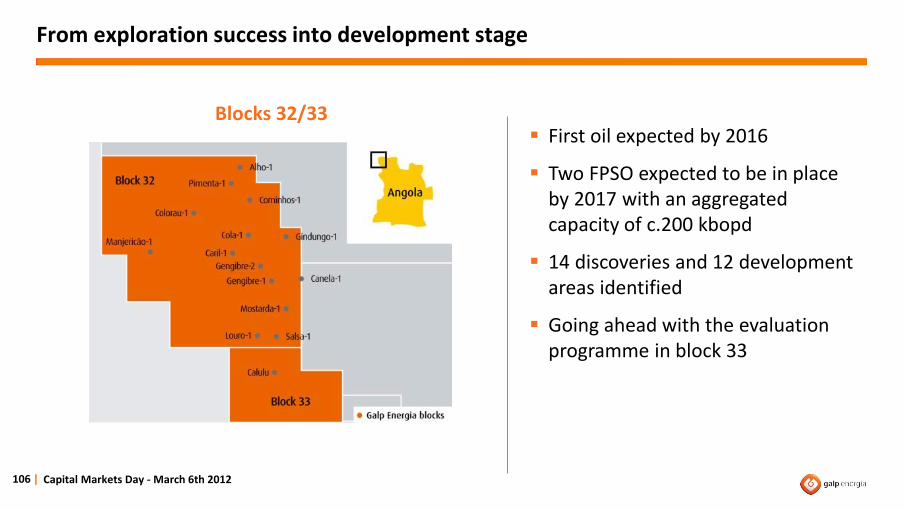

106 | Capital Markets Day - March 6th 2012

Blocks 32/33

First oil expected by 2016

Two FPSO expected to be in place by 2017 with an aggregated capacity of c.200 kbopd

14 discoveries and 12 development areas identified

Going ahead with the evaluation programme in block 33

Development of world class projects on track to achieve 300 kboepd by 2020

107 | Capital Markets Day - March 6th 2012

Mozambique development project being studied with first gas expected by 2018

Brazil gaining momentum and driving production growth

Significant upside through testing different techniques in pre-salt Santos basin

Angola development projects being prepared to support production increase

108 |

Capital Markets Day - March 6th 2012

Closing remarks Manuel Ferreira De Oliveira Chief Executive Officer

Solid foundations to deliver sustainable value

109 | Capital Markets Day - March 6th 2012

Solid financial structure

Outstanding exploration

potential

Delivering high potential projects

Sound downstream

business

Highly responsible

practices

Acronyms

110 | Capital Markets Day - March 6th 2012

# Number GWh GigaWatt hour

$ United States dol lar HSE Health, Safety and Environment

% Percentage IPO Ini tia l Publ ic Offering

2D Two dimens ional seismic Kboepd Thousand barrels of oi l equiva lent per day

3D Three dimens ional seismic Kbpd Thousand barrels per day

API gravity American Petroleum Insti tute gravi ty Km2

Square ki lometre

BBLT Benguela , Bel ize, Lobito, and Tomboco LNG Liqui fied Natura l Gas

Bbl Barrel LTIFR Lost time injury frequency rate

Bcm Bi l l ion cubic metres Mln Mil l ion

Bln Bi l l ion MW MegaWatt

Boe Barrel of oi l equiva lent Mmscf/d Mil l ion s tandard cubic feet per day

c. Circa NG Natura l Gas

CAGR Compound Annual Growth Rate OWC Oi l -water contact

Capex Capita l expenditure POS Probabi l i ty of success

CO2 Carbon Dioxide p.p. Percentage point

DA Development area R&M Refining & Marketing

DEH Direct electrica l heating RCA Replacement Cost adjusted

DoC Declaration of commercia l i ty SAM Sustainable Asset Management

E/A Exploration wel l /Appraisa l wel l SEE Socia l , Environmental and Economic impact

E&P Exploration & Production SXEP STOXX Europe 600 Oi l & Gas

EBITDA Earnings before interest, taxes , depreciation and amortization Tcf Tri l l ion cubic feet

EOR Enhanced oi l recovery Ton Tonne

EWT Extended Wel l Test WAG Water Al ternating Gas

FLNG Floating l iquefied natura l gas WI Working interest

FPSO Floating Production Storage Offloading YE Year End

Disclaimer

111 | Capital Markets Day - March 6th 2012

Financial outlook figures are RCA figures except otherwise noted.

Matters discussed in this presentation may constitute forward-looking statements. Forward-looking statements are statements other than in respect of

historical facts. The words “believe,” “expect,” “anticipate,” “intends,” “estimate,” “will,” “may,” "continue," “should” and similar expressions identify

forward-looking statements. Forward-looking statements may include statements regarding: objectives, goals, strategies, outlook and growth

prospects; future plans, events or performance and potential for future growth; liquidity, capital resources and capital expenditures; economic outlook

and industry trends; developments of Galp Energia’s markets; the impact of regulatory initiatives; and the strength of Galp Energia’s competitors. The

forward-looking statements in this presentation are based upon various assumptions, many of which are based, in turn, upon further assumptions,

including without limitation, management’s examination of historical operating trends, data contained in Galp Energia’s records and other data

available from third parties. Although Galp Energia believes that these assumptions were reasonable when made, these assumptions are inherently

subject to significant known and unknown risks, uncertainties, contingencies and other important factors which are difficult or impossible to predict and

are beyond its control. Such risks, uncertainties, contingencies and other important factors could cause the actual results of Galp Energia or the industry

to differ materially from those results expressed or implied in this presentation by such forward-looking statements.

The information, opinions and forward-looking statements contained in this presentation speak only as at the date of this presentation, and are subject

to change without notice. Galp Energia does not intend to, and expressly disclaim any duty, undertaking or obligation to, make or disseminate any

supplement, amendment, update or revision to any of the information, opinions or forward-looking statements contained in this presentation to reflect

any change in events, conditions or circumstances.