FERROVIAL, S.A. SEPARATE DIRECTORS' REPORT AND FINANCIAL ...

Upload

ferrovialCategory

view

34download

0

1

Ferrovial Investing for Growth

2

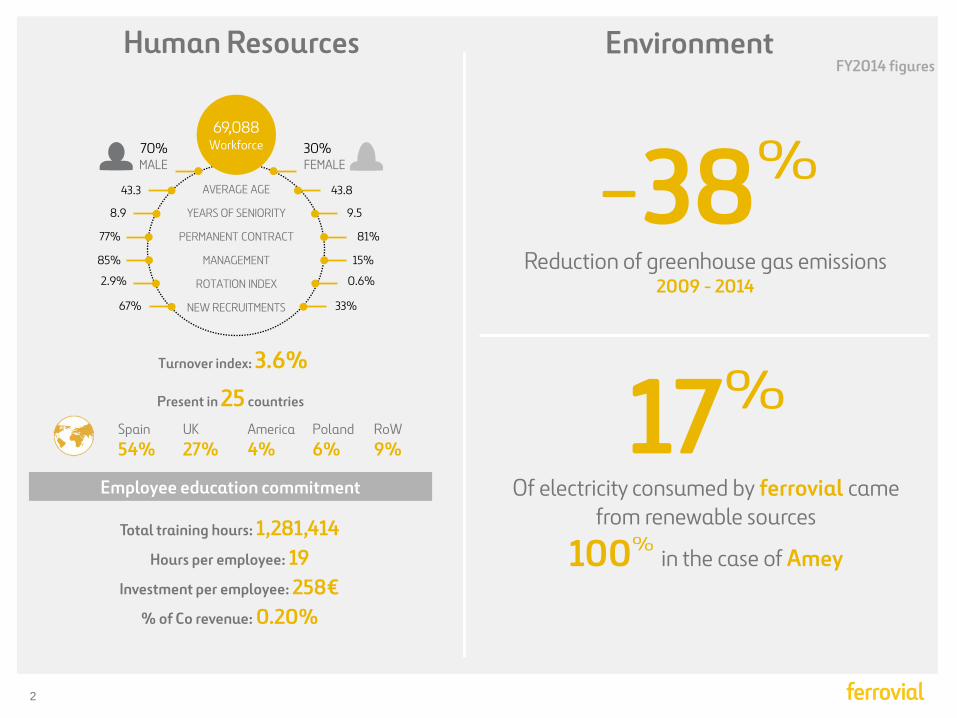

Human Resources

Total training hours: 1,281,414 Hours per employee: 19

Investment per employee: 258€ % of Co revenue: 0.20%

-38Reduction of greenhouse gas emissions

2009 - 2014

Employee education commitment

Environment

17Of electricity consumed by ferrovial came

from renewable sources

100 in the case of Amey

FY2014 figures

Spain 54%

America 4%

UK 27%

Poland 6%

RoW 9%

70% MALE

30% FEMALE

43.3 43.8 AVERAGE AGE

8.9 9.5 YEARS OF SENIORITY

77% 81% PERMANENT CONTRACT

85% 15% MANAGEMENT

2.9% 0.6% ROTATION INDEX

67% 33% NEW RECRUITMENTS

Present in 25 countries

69,088 Workforce

Turnover index: 3.6%

3

Ferrovial Overview & Strategy

4

What is Ferrovial? DESIGN & CONSTRUCTION MAINTENANCE

OPERATION

Construction Services

Toll roads Airports

Design, Financing, Construction, Operation & Maintenance of infrastructure assets & Provider of services to cities

1. CF Generation

2. Profitable Growth

3. Shareholder Remuneration

STRATEGY

INFRASTRUCTURE PROJECTS

EX-INFRASTRUCTURE PROJECTS

…

5

INFRASTRUCTURE

PROJECTS

EX-INFRASTRUCTURE

PROJECTS

Capital intensive / Inflation protected / LT duration & financing

Controlling Shareholder 43% Free float 57%

Non capital intensive / Backlog visibility / EPS accretive

Ring fenced debt

Net cash position

1. Cash Flow Generation

€255mn Dividends from Toll roads

€341mn Dividends from Airports

€387mn

€349mn EBITDA from Construction

EBITDA from Services

PARENT COMPANY

€ million 2014 figures

6

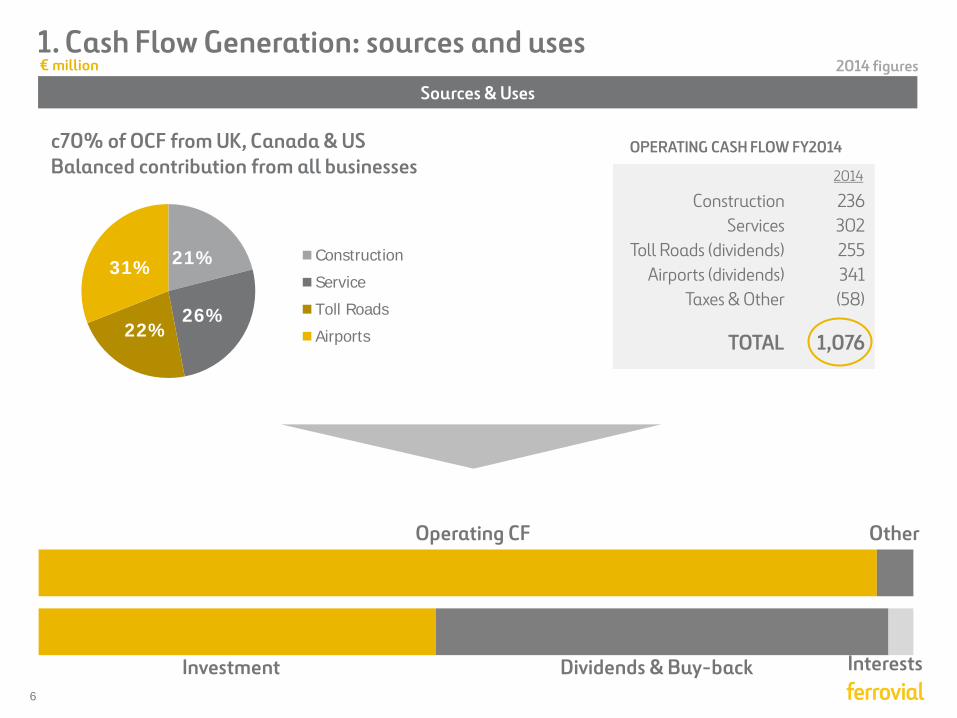

1. Cash Flow Generation: sources and uses

21%

26% 22%

31% Construction

Service

Toll Roads

Airports

€ million

OPERATING CASH FLOW FY2014

236 302 255 341 (58)

1,076

Construction Services

Toll Roads (dividends) Airports (dividends)

Taxes & Other

TOTAL

2014

Operating CF Other

Dividends & Buy-back Interests

Sources & Uses

Investment

c70% of OCF from UK, Canada & US Balanced contribution from all businesses

2014 figures

7

PARENT COMPANY

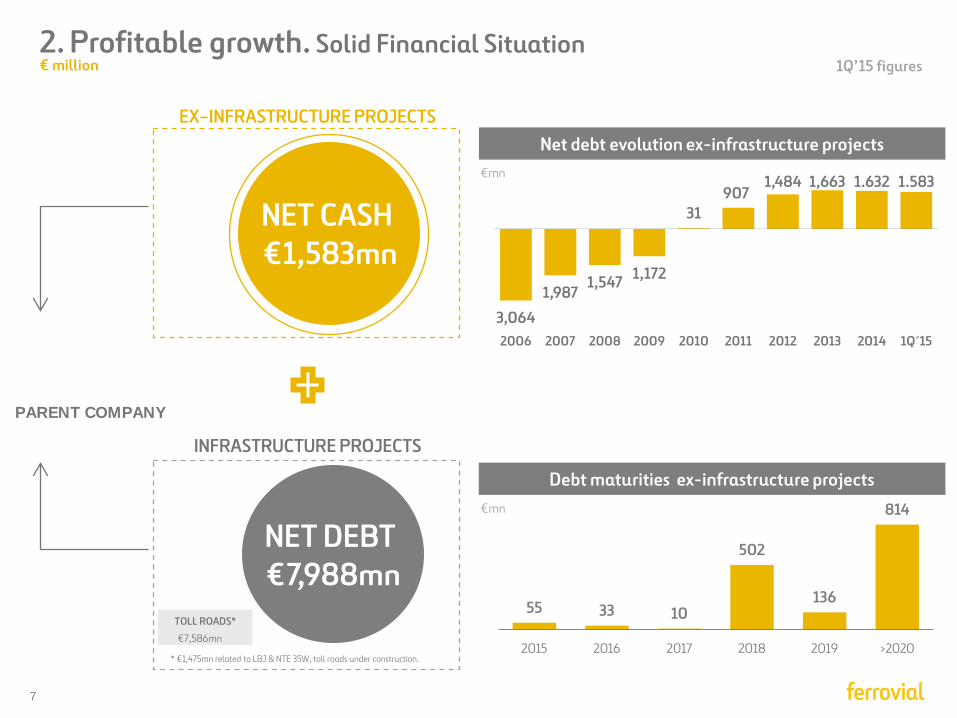

2. Profitable growth. Solid Financial Situation

Net debt evolution ex-infrastructure projects

3,064

1,987 1,547 1,172

31 907

1,484 1,663 1.632 1.583

2006 2007 2008 2009 2010 2011 2012 2013 2014 1Q´15

EX–INFRASTRUCTURE PROJECTS

TOLL ROADS* €7,586mn

* €1,475mn related to LBJ & NTE 35W, toll roads under construction.

INFRASTRUCTURE PROJECTS

Debt maturities ex-infrastructure projects

NET CASH €1,583mn

€mn

€mn

NET DEBT €7,988mn

55 33 10

502

136

814

2015 2016 2017 2018 2019 >2020

€ million 1Q’15 figures

8

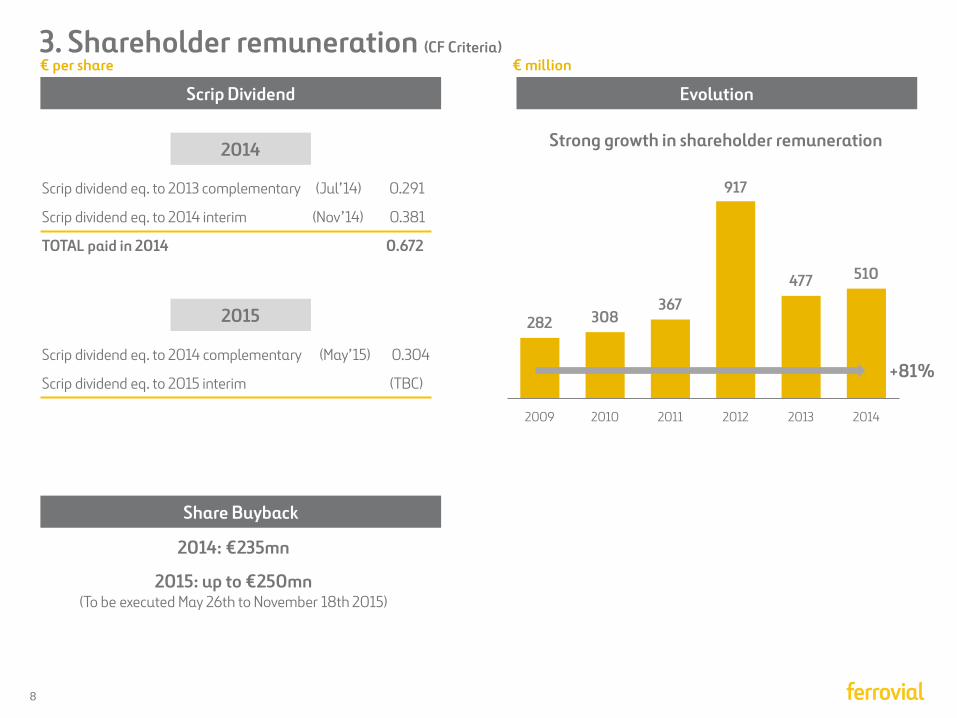

3. Shareholder remuneration (CF Criteria)

Scrip Dividend

Scrip dividend eq. to 2013 complementary (Jul’14) 0.291

Scrip dividend eq. to 2014 interim (Nov’14) 0.381

TOTAL paid in 2014 0.672

2014: €235mn

Evolution

Share Buyback

Scrip dividend eq. to 2014 complementary (May’15) 0.304

Scrip dividend eq. to 2015 interim (TBC)

2015: up to €250mn (To be executed May 26th to November 18th 2015)

282 308 367

917

477 510

2009 2010 2011 2012 2013 2014

€ per share

+81%

Strong growth in shareholder remuneration

€ million

2014

2015

9

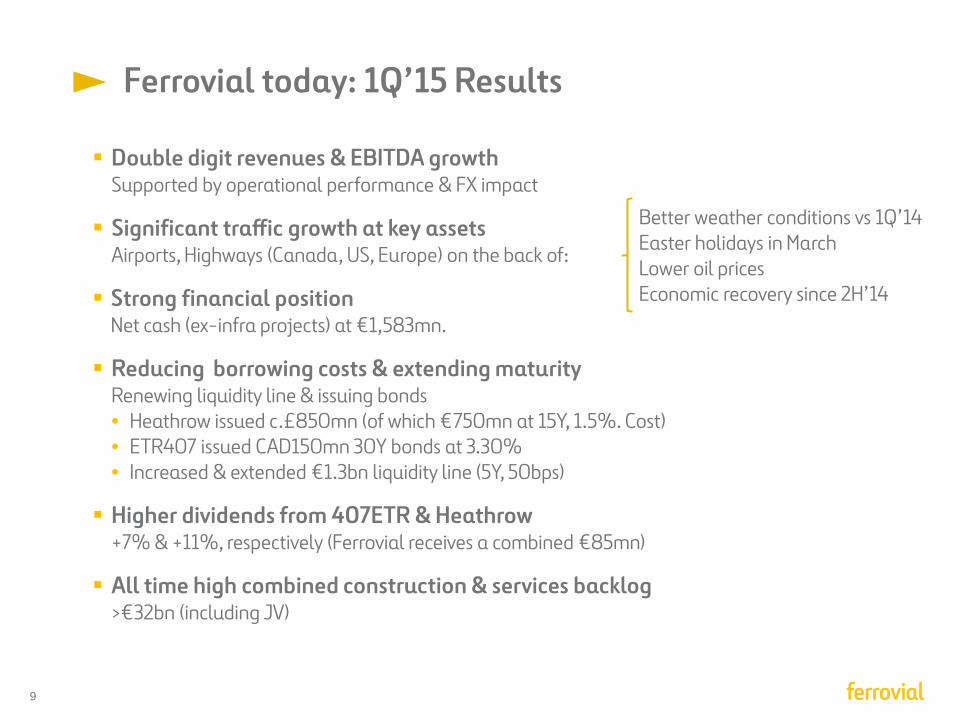

Ferrovial today: 1Q’15 Results

Double digit revenues & EBITDA growth Supported by operational performance & FX impact

Significant traffic growth at key assets Airports, Highways (Canada, US, Europe) on the back of:

Strong financial position Net cash (ex-infra projects) at €1,583mn.

Reducing borrowing costs & extending maturity Renewing liquidity line &^issuing bonds • Heathrow issued c.£850mn (of which €750mn at 15Y, 1.5%. Cost) • ETR407 issued CAD150mn 30Y bonds at 3.30% • Increased & extended €1.3bn liquidity line (5Y, 50bps)

Higher dividends from 407ETR & Heathrow +7% & +11%, respectively (Ferrovial receives a combined €85mn)

All time high combined construction & services backlog >€32bn (including JV)

Better weather conditions vs 1Q’14 Easter holidays in March Lower oil prices Economic recovery since 2H’14

10

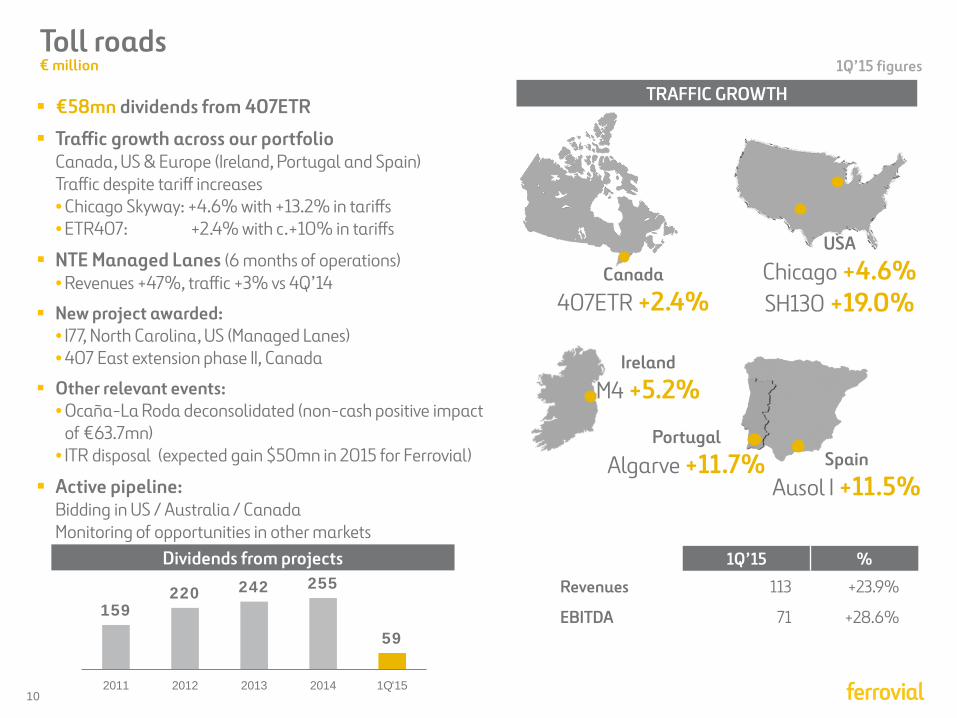

Toll roads € million

TRAFFIC GROWTH

1Q’15 figures

1Q’15 %

Revenues 113 +23.9%

EBITDA 71 +28.6%

€58mn dividends from 407ETR

Traffic growth across our portfolio Canada, US & Europe (Ireland, Portugal and Spain) Traffic despite tariff increases • Chicago Skyway: +4.6% with +13.2% in tariffs • ETR407: +2.4% with c.+10% in tariffs

NTE Managed Lanes (6 months of operations) • Revenues +47%, traffic +3% vs 4Q’14

New project awarded: • I77, North Carolina, US (Managed Lanes) • 407 East extension phase II, Canada

Other relevant events: • Ocaña-La Roda deconsolidated (non-cash positive impact

of €63.7mn) • ITR disposal (expected gain $50mn in 2015 for Ferrovial)

Active pipeline: Bidding in US / Australia / Canada Monitoring of opportunities in other markets

159 220 242 255

59

2011 2012 2013 2014 1Q'15

Dividends from projects

Canada

407ETR +2.4%

USA

Chicago +4.6% SH130 +19.0%

Ireland

M4 +5.2%

Portugal

Algarve +11.7% Spain

Ausol I +11.5%

11

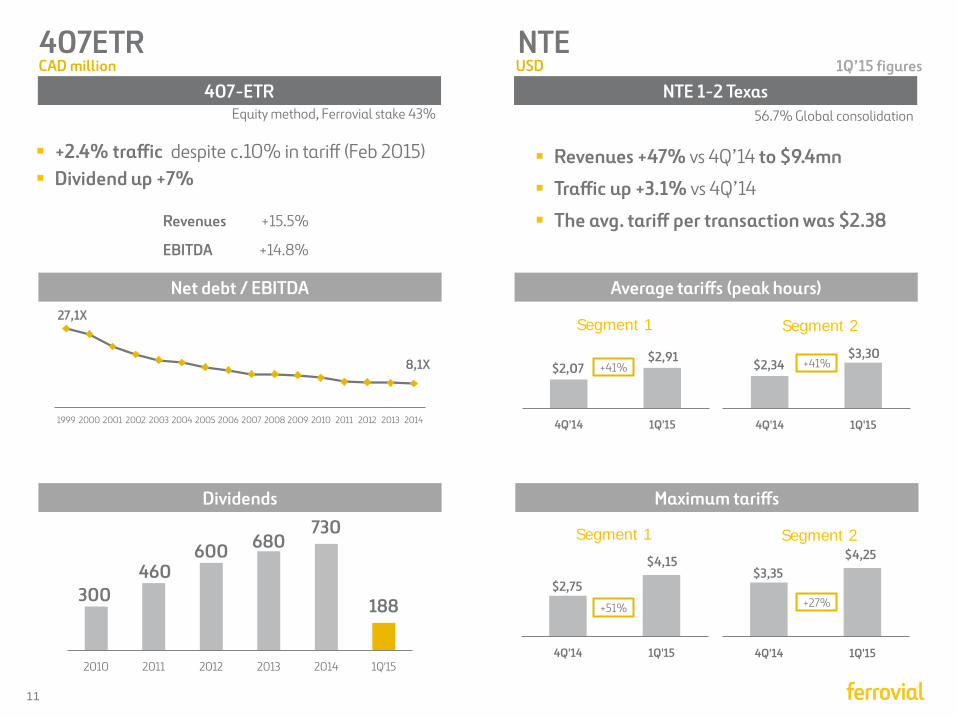

407ETR NTE CAD million USD

Revenues +15.5%

EBITDA +14.8%

+2.4% traffic despite c.10% in tariff (Feb 2015)

Dividend up +7%

300 460

600 680 730

188

2010 2011 2012 2013 2014 1Q'15

Revenues +47% vs 4Q’14 to $9.4mn

Traffic up +3.1% vs 4Q’14

The avg. tariff per transaction was $2.38

27,1X

8,1X

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Equity method, Ferrovial stake 43% NTE 1-2 Texas 407-ETR

56.7% Global consolidation

Net debt / EBITDA

Dividends

Average tariffs (peak hours)

1Q’15 figures

$2,07

$2,91

4Q'14 1Q'15

Segment 1

Maximum tariffs

$2,34

$3,30

4Q'14 1Q'15

Segment 2

$2,75

$4,15

4Q'14 1Q'15

Segment 1

$3,35

$4,25

4Q'14 1Q'15

Segment 2

+41%

+51%

+41%

+27%

12

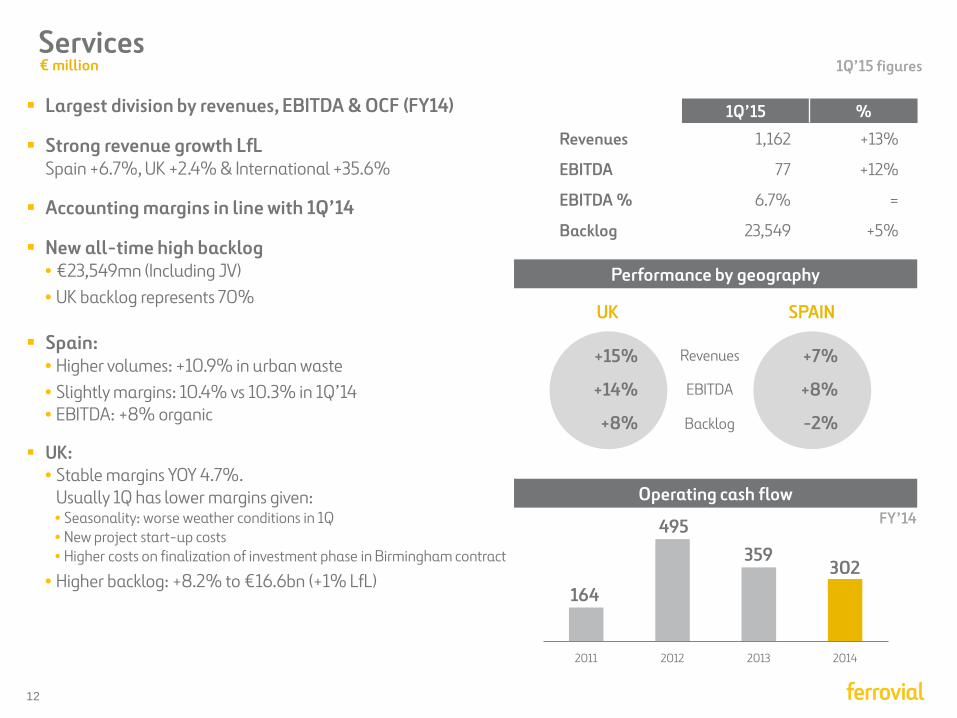

Services

Largest division by revenues, EBITDA & OCF (FY14)

Strong revenue growth LfL Spain +6.7%, UK +2.4% & International +35.6%

Accounting margins in line with 1Q’14

New all-time high backlog • €23,549mn (Including JV) • UK backlog represents 70%

Spain:

• Higher volumes: +10.9% in urban waste • Slightly margins: 10.4% vs 10.3% in 1Q’14 • EBITDA: +8% organic

UK: • Stable margins YOY 4.7%.

Usually 1Q has lower margins given: • Seasonality: worse weather conditions in 1Q • New project start-up costs • Higher costs on finalization of investment phase in Birmingham contract

• Higher backlog: +8.2% to €16.6bn (+1% LfL)

SPAIN UK

+15%

+14%

+8%

+7%

+8%

-2%

Revenues

EBITDA

Backlog

164

495 359

302

2011 2012 2013 2014

1Q’15 %

Revenues 1,162 +13%

EBITDA 77 +12%

EBITDA % 6.7% =

Backlog 23,549 +5%

Performance by geography

Operating cash flow

€ million 1Q’15 figures

FY’14

13

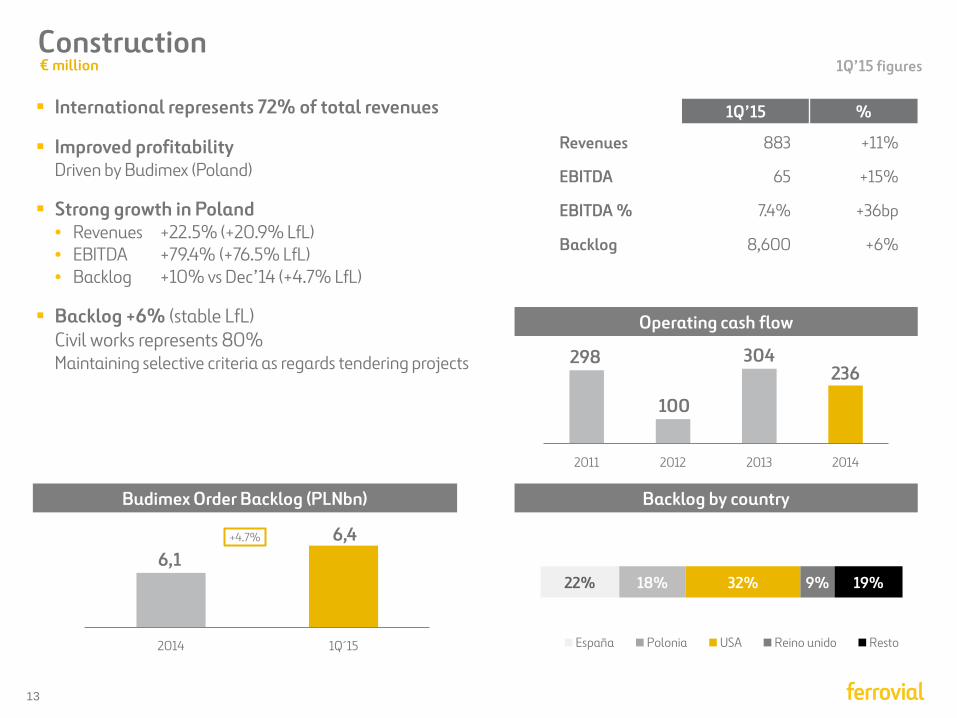

Construction

International represents 72% of total revenues

Improved profitability Driven by Budimex (Poland)

Strong growth in Poland • Revenues +22.5% (+20.9% LfL) • EBITDA +79.4% (+76.5% LfL) • Backlog +10% vs Dec’14 (+4.7% LfL)

Backlog +6% (stable LfL) Civil works represents 80% Maintaining selective criteria as regards tendering projects

1Q’15 %

Revenues 883 +11%

EBITDA 65 +15%

EBITDA % 7.4% +36bp

Backlog 8,600 +6%

298

100

304 236

2011 2012 2013 2014

Operating cash flow

Backlog by country Budimex Order Backlog (PLNbn)

6,1 6,4

2014 1Q´15

+4.7%

22% 18% 32% 9% 19%

España Polonia USA Reino unido Resto

€ million 1Q’15 figures

14

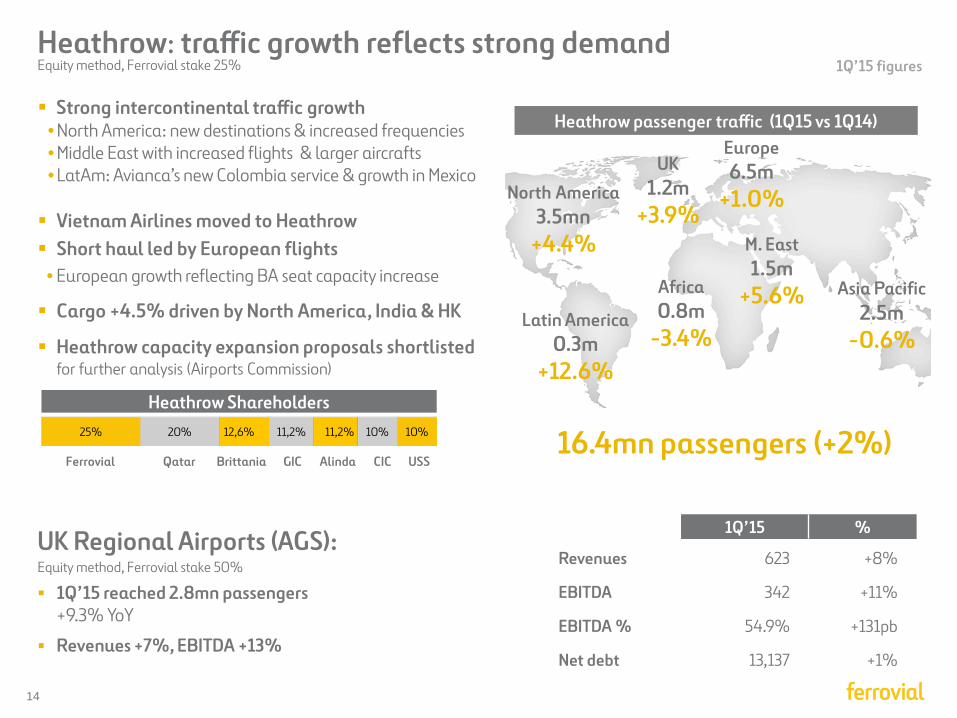

Heathrow: traffic growth reflects strong demand

Strong intercontinental traffic growth • North America: new destinations & increased frequencies • Middle East with increased flights & larger aircrafts • LatAm: Avianca’s new Colombia service & growth in Mexico

Vietnam Airlines moved to Heathrow Short haul led by European flights • European growth reflecting BA seat capacity increase

Cargo +4.5% driven by North America, India & HK

Heathrow capacity expansion proposals shortlisted for further analysis (Airports Commission)

Heathrow passenger traffic (1Q15 vs 1Q14)

1Q’15 figures

Africa 0.8m

-3.4%

M. East 1.5m

+5.6% Asia Pacific 2.5m

-0.6%

UK 1.2m

+3.9%

Europe 6.5m

+1.0%

Latin America 0.3m

+12.6%

North America 3.5mn

+4.4%

1Q’15 %

Revenues 623 +8%

EBITDA 342 +11%

EBITDA % 54.9% +131pb

Net debt 13,137 +1%

16.4mn passengers (+2%)

Equity method, Ferrovial stake 25%

Equity method, Ferrovial stake 50%

25% 20% 12,6% 11,2% 11,2% 10% 10%

Ferrovial Qatar Brittania GIC CIC Alinda USS

Heathrow Shareholders

UK Regional Airports (AGS):

1Q’15 reached 2.8mn passengers +9.3% YoY

Revenues +7%, EBITDA +13%

15

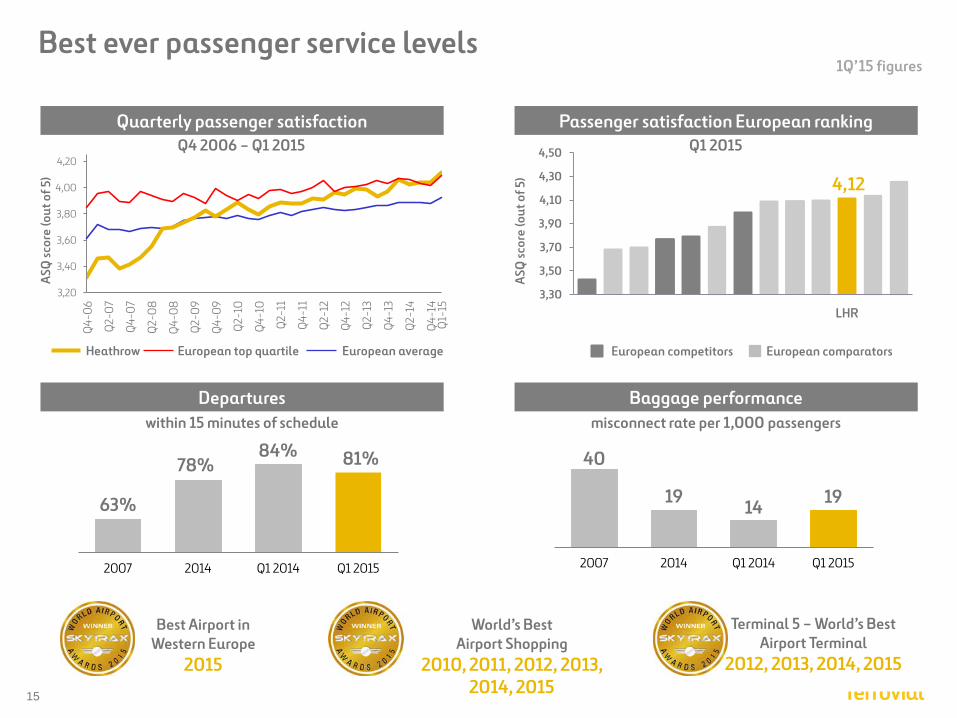

Best ever passenger service levels

Passenger satisfaction European ranking

1Q’15 figures

Best Airport in Western Europe

2015

World’s Best Airport Shopping

2010, 2011, 2012, 2013, 2014, 2015

Terminal 5 – World’s Best Airport Terminal

2012, 2013, 2014, 2015

Quarterly passenger satisfaction Q1 2015 Q4 2006 – Q1 2015

4,12

3,30

3,50

3,70

3,90

4,10

4,30

4,50

LHR

ASQ

scor

e (o

ut o

f 5)

3,20

3,40

3,60

3,80

4,00

4,20

Q4-

06

Q2-

07

Q4-

07

Q2-

08

Q4-

08

Q2-

09

Q4-

09

Q2-

10

Q4-

10

Q2-

11

Q4-

11

Q2-

12

Q4-

12

Q2-

13

Q4-

13

Q2-

14

Q4-

14Q

1-15

ASQ

scor

e (o

ut o

f 5)

European competitors European comparators Heathrow European average European top quartile

Baggage performance Departures misconnect rate per 1,000 passengers within 15 minutes of schedule

63%

78% 84% 81%

2007 2014 Q1 2014 Q1 2015

40

19 14 19

2007 2014 Q1 2014 Q1 2015

17

Appendix

Introduction to 407ETR Toll road

Managed Lanes Toll roads

18

High density population area

Ring road of Toronto 108 km

407

407

East extension

Area of expansion

407 ETR

Location

19

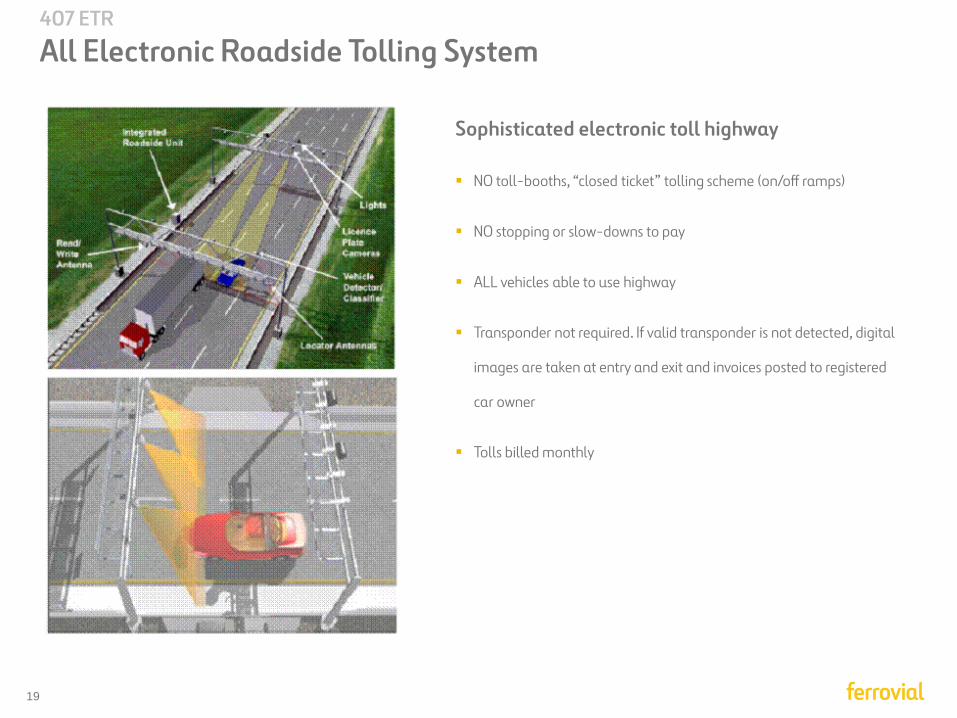

407 ETR

All Electronic Roadside Tolling System

Sophisticated electronic toll highway

NO toll-booths, “closed ticket” tolling scheme (on/off ramps)

NO stopping or slow-downs to pay

ALL vehicles able to use highway

Transponder not required. If valid transponder is not detected, digital

images are taken at entry and exit and invoices posted to registered

car owner

Tolls billed monthly

20

407 ETR

LOCATION

Greater Toronto Area 23% of Canada population

TRAFFIC

Alternatives routes are highly congested

HIGH HOUSEHOLD INCOME

46% higher than Canada average

NO REGULATORY REVIEWS

During concession life (99 years)

SPEED

Alternatives routes 40kph

vs 100kph at 407

NON-STOP TOLL FACILITY

Fully electronic with interchanges

every 3km

TOLL RATE HIGH FLEXIBILITY

Including segment, direction, time of

the day

FAST

Reliable travel times

Fast Safe

Reliable

21

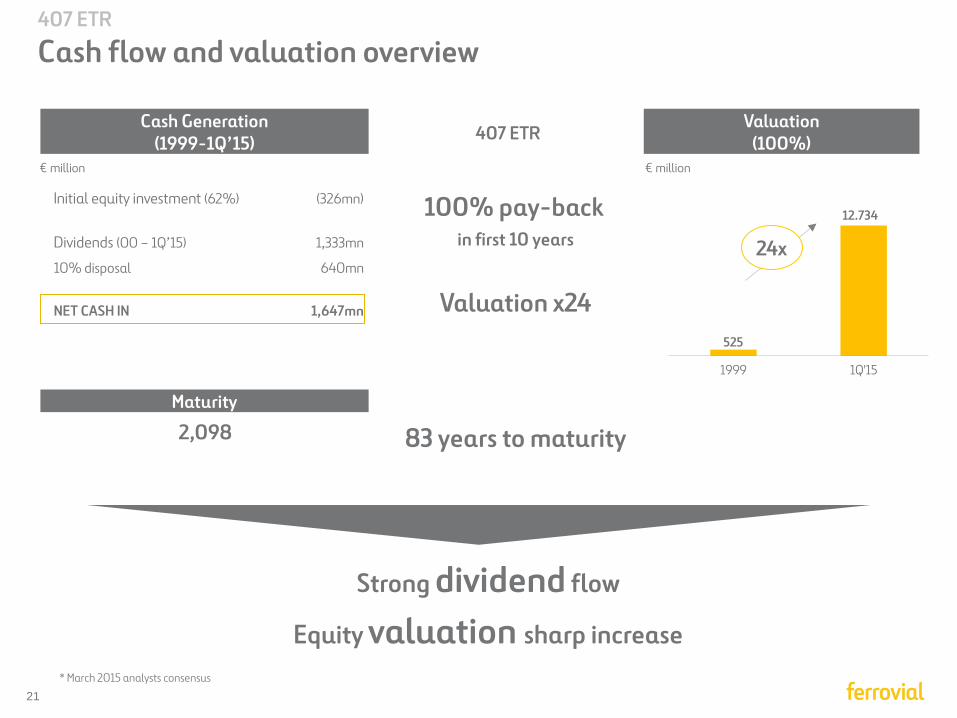

Strong dividend flow

Equity valuation sharp increase

Initial equity investment (62%) (326mn)

Dividends (00 – 1Q’15) 1,333mn

10% disposal 640mn

NET CASH IN 1,647mn

2,098

100% pay-back

in first 10 years

Valuation x24

* March 2015 analysts consensus

525

12.734

1999 1Q'15

24x

407 ETR

83 years to maturity

407 ETR

Cash flow and valuation overview

€ million

Cash Generation (1999-1Q’15)

Valuation (100%)

€ million

Maturity

22

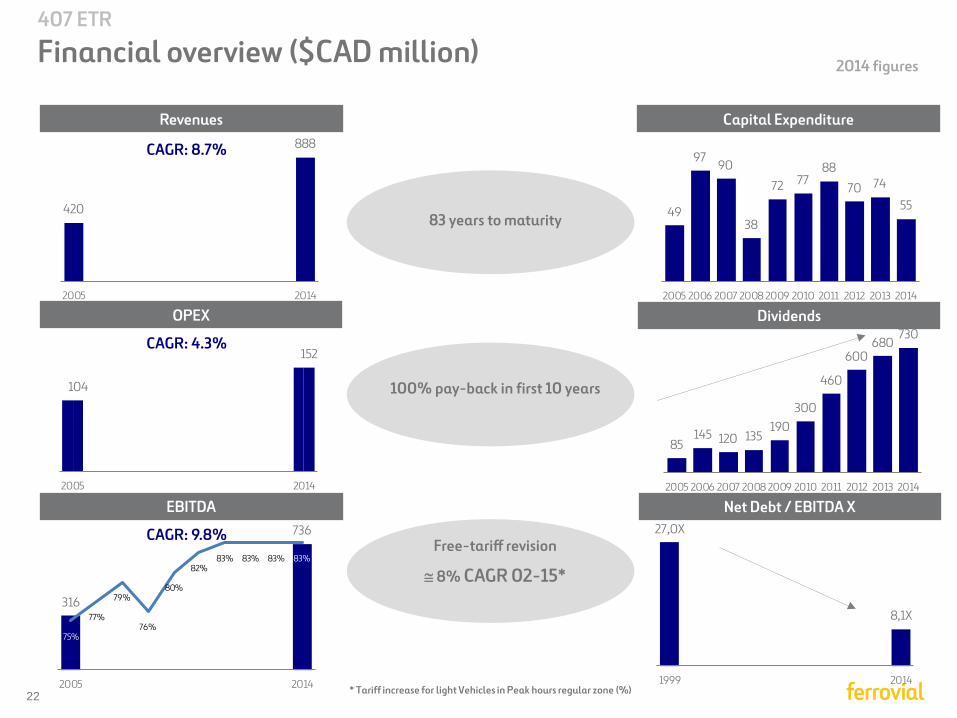

83 years to maturity

100% pay-back in first 10 years

Free-tariff revision

≅ 8% CAGR 02-15*

* Tariff increase for light Vehicles in Peak hours regular zone (%)

407 ETR

Financial overview ($CAD million)

Revenues

EBITDA

OPEX

Capital Expenditure

Dividends

Net Debt / EBITDA X

420

888

2005 2014

104

152

2005 2014

316

736

75%

77%

79%

76%

80%

82%83% 83% 83% 83%

2005 2014

CAGR: 8.7%

CAGR: 9.8%

CAGR: 4.3%

49

9790

38

72 7788

70 74

55

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

85145 120 135

190300

460

600680

730

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

27,0X

8,1X

1999 2014

2014 figures

23

Appendix

Introduction to 407ETR Toll road

Managed Lanes Toll roads

24

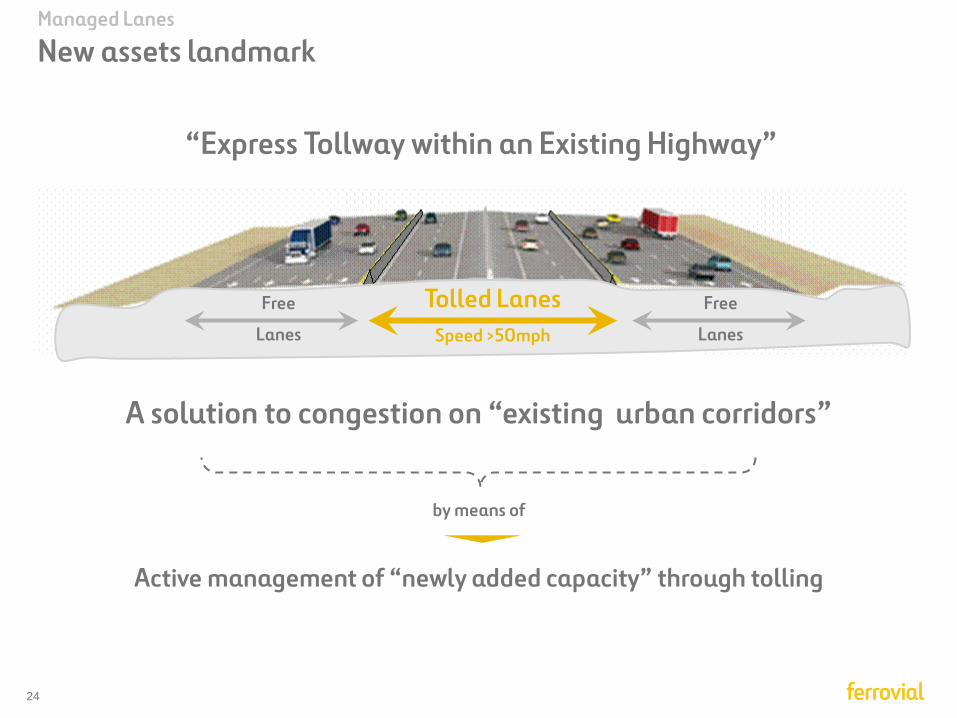

A solution to congestion on “existing urban corridors”

Active management of “newly added capacity” through tolling

by means of

Free

Lanes

Free

Lanes

Tolled Lanes Speed >50mph

“Express Tollway within an Existing Highway”

Managed Lanes

New assets landmark

25

Time of the day

Eastbound Westbound

00.00 2.00 4.00 6.00 8.00 10.00 12.00 14.00 16.00 18.00 20.00 22.00 24.00 12.00 2.00 4.00 6.00 8.00 10.00 12.00 2.00 4.00 6.00 8.00 10.00 12.00

Time of the day

Peak period

Managed Lanes

Level of demand

NTE (untolled) 407ETR (tolled)

26

Tim

e (m

in)

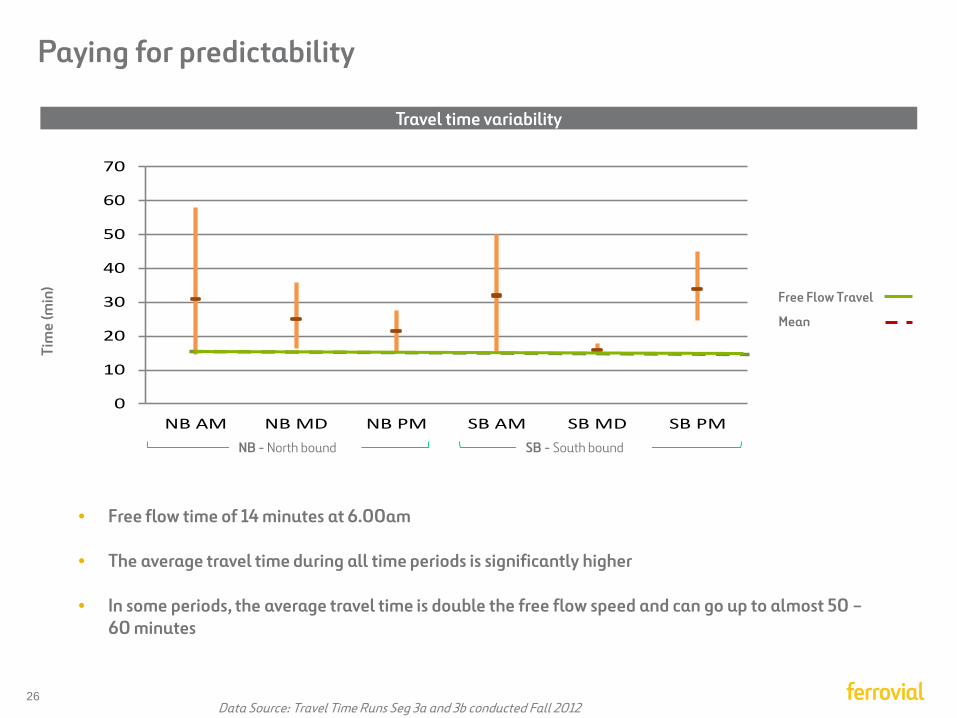

• Free flow time of 14 minutes at 6.00am

• The average travel time during all time periods is significantly higher

• In some periods, the average travel time is double the free flow speed and can go up to almost 50 – 60 minutes

0

10

20

30

40

50

60

70

NB AM NB MD NB PM SB AM SB MD SB PM

Tim

e (m

in)

Data Source: Travel Time Runs Seg 3a and 3b conducted Fall 2012

Paying for predictability

Free Flow Travel

Mean

NB - North bound SB - South bound

Travel time variability

27

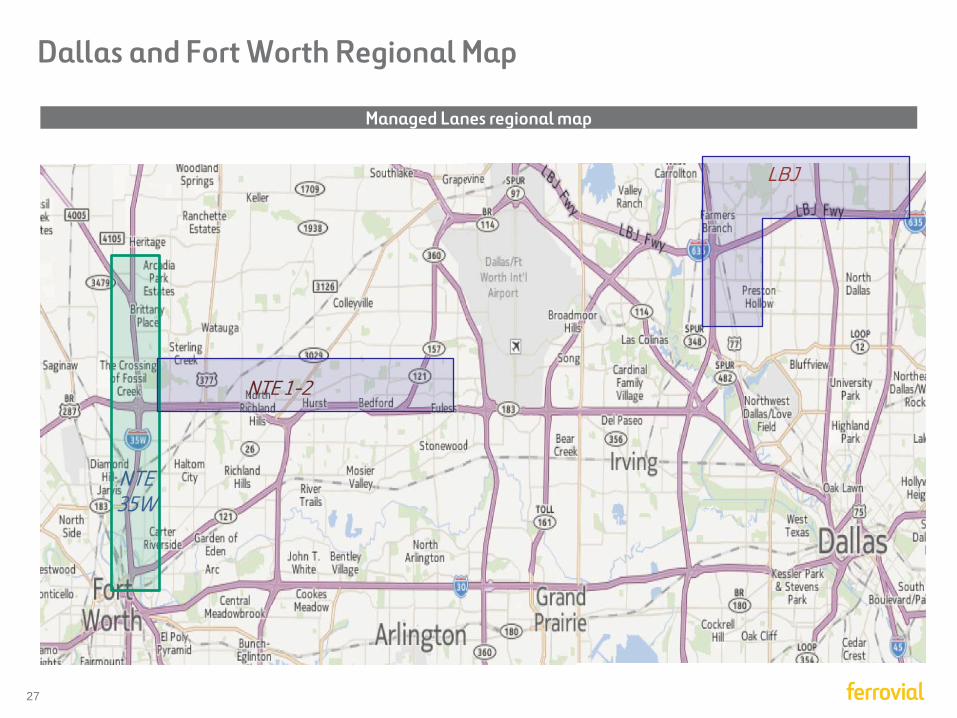

LBJ

Dallas and Fort Worth Regional Map

Managed Lanes regional map

NTE 1-2

NTE 35W

28

CINTRA MERIDIAM DALLAS

FIRE&POLICE PENSION SCHEME

DESCRIPTION:

LENGTH:

CONCESSION PERIOD:

TARIFF POLICY:

Dallas-Fort Worth Metroplex, Major thoroughfares

between Fort Worth and DFW Airport

13 mile section (IH 820 & SH 183 in Tarrant County)

52 years

Open Road Tolling System (no toll booths) with a dynamic tolling

regime (every 5 minutes) to maintain at all times a minimum speed of

50 mph

● No toll-booths, fully electronic free flow tolling system

● Tollway within a freeway: Motorists will be provided with a choice of

driving in non-tolled GP lanes or paying a toll to bypass such GP

lanes

● Tolls setting to ensure minimum speed on new lanes

● As demand grows and capacity becomes scarce, pricing power

increases

● Physically separated from the GP lanes with controlled access

EQUITY DEBT PUBLIC FUNDS

Managed Lanes

North Tarrant Express Opened on October 4th, 9 months ahead of schedule

57% 33% 10%

21% 52% 27%

Key characteristics

Shareholder structure

Financial structure

29

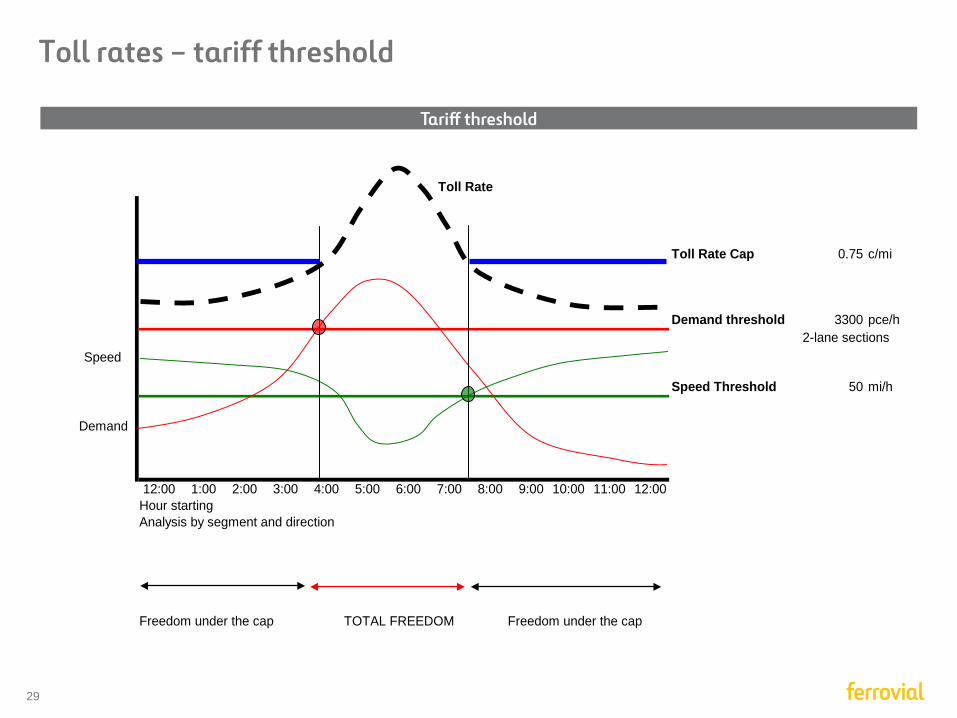

Toll rates – tariff threshold

Toll Rate Cap 0.75 c/mi

Demand threshold 3300 pce/h2-lane sections

Speed Threshold 50 mi/h

12:00 1:00 2:00 3:00 4:00 5:00 6:00 7:00 8:00 9:00 10:00 11:00 12:00Hour startingAnalysis by segment and direction

Freedom under the cap TOTAL FREEDOM Freedom under the cap

Speed

Demand

Toll Rate

Tariff threshold

30

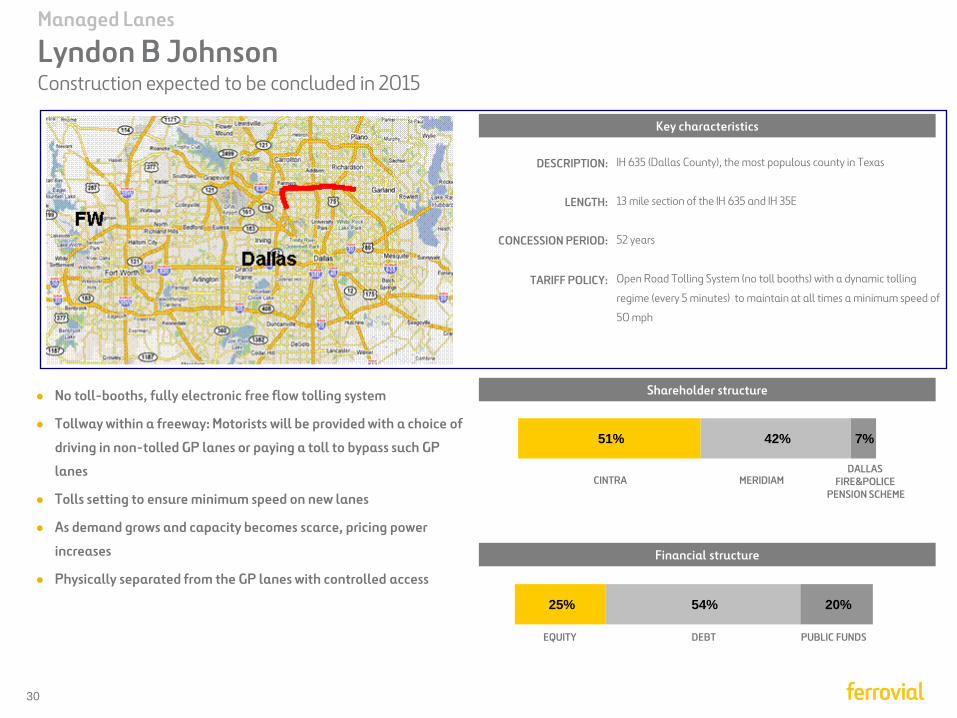

CINTRA MERIDIAM DALLAS

FIRE&POLICE PENSION SCHEME

Key characteristics

108Km Electronic toll

DESCRIPTION:

LENGTH:

CONCESSION PERIOD:

TARIFF POLICY:

IH 635 (Dallas County), the most populous county in Texas

13 mile section of the IH 635 and IH 35E

52 years

Open Road Tolling System (no toll booths) with a dynamic tolling

regime (every 5 minutes) to maintain at all times a minimum speed of

50 mph

● No toll-booths, fully electronic free flow tolling system

● Tollway within a freeway: Motorists will be provided with a choice of

driving in non-tolled GP lanes or paying a toll to bypass such GP

lanes

● Tolls setting to ensure minimum speed on new lanes

● As demand grows and capacity becomes scarce, pricing power

increases

● Physically separated from the GP lanes with controlled access

EQUITY DEBT PUBLIC FUNDS

Managed Lanes

Lyndon B Johnson Construction expected to be concluded in 2015

51% 42% 7%

25% 54% 20%

Shareholder structure

Financial structure

31

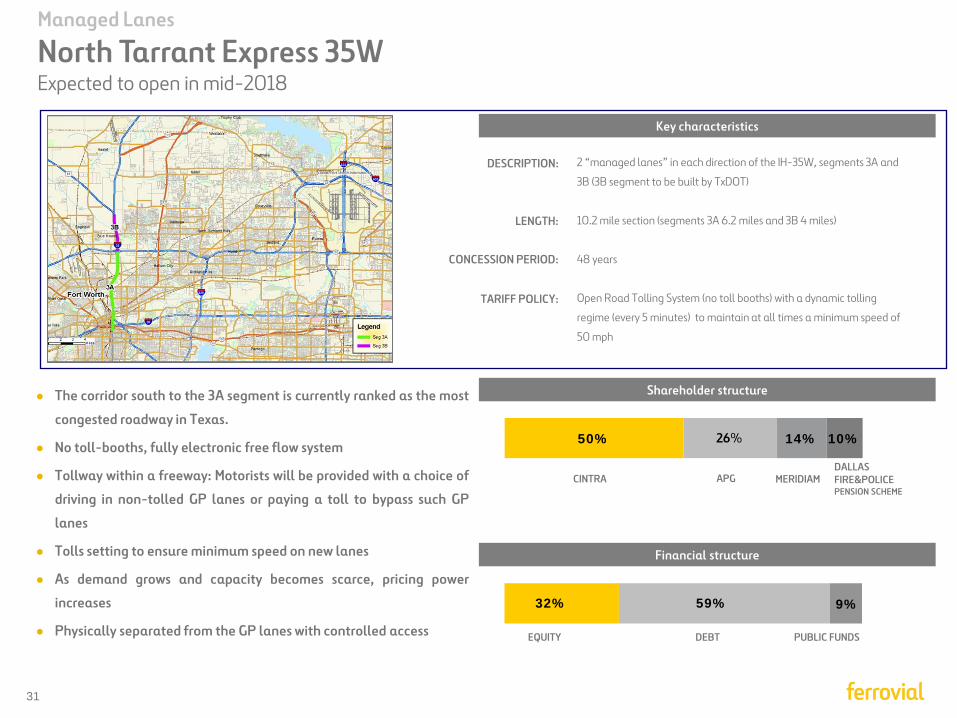

50% 14% 10%

CINTRA MERIDIAM DALLAS FIRE&POLICE PENSION SCHEME

DESCRIPTION:

LENGTH:

CONCESSION PERIOD:

TARIFF POLICY:

2 “managed lanes” in each direction of the IH-35W, segments 3A and

3B (3B segment to be built by TxDOT)

10.2 mile section (segments 3A 6.2 miles and 3B 4 miles)

48 years

Open Road Tolling System (no toll booths) with a dynamic tolling

regime (every 5 minutes) to maintain at all times a minimum speed of

50 mph

● The corridor south to the 3A segment is currently ranked as the most

congested roadway in Texas.

● No toll-booths, fully electronic free flow system

● Tollway within a freeway: Motorists will be provided with a choice of

driving in non-tolled GP lanes or paying a toll to bypass such GP

lanes

● Tolls setting to ensure minimum speed on new lanes

● As demand grows and capacity becomes scarce, pricing power

increases

● Physically separated from the GP lanes with controlled access

32% 59% 9%

EQUITY DEBT PUBLIC FUNDS

APG

Managed Lanes

North Tarrant Express 35W Expected to open in mid-2018

26%

Key characteristics

Shareholder structure

Financial structure

32

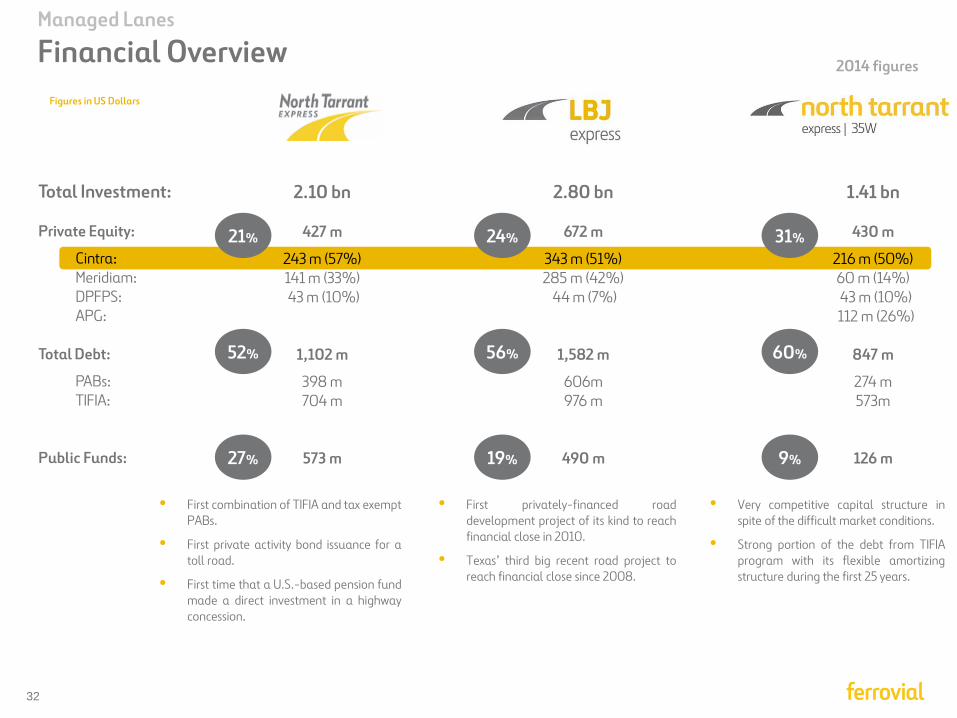

• First privately-financed road development project of its kind to reach financial close in 2010.

• Texas’ third big recent road project to reach financial close since 2008.

• First combination of TIFIA and tax exempt PABs.

• First private activity bond issuance for a toll road.

• First time that a U.S.-based pension fund made a direct investment in a highway concession.

21%

52%

27%

24%

56%

19%

Figures in US Dollars

Managed Lanes

Financial Overview

31%

60%

9%

• Very competitive capital structure in spite of the difficult market conditions.

• Strong portion of the debt from TIFIA program with its flexible amortizing structure during the first 25 years.

2.10 bn

427 m

243 m (57%) 141 m (33%) 43 m (10%)

1,102 m

398 m 704 m

573 m

2.80 bn

672 m

343 m (51%) 285 m (42%)

44 m (7%)

1,582 m

606m 976 m

490 m

1.41 bn

430 m

216 m (50%) 60 m (14%) 43 m (10%) 112 m (26%)

847 m

274 m 573m

126 m

Total Investment: Private Equity:

Cintra: Meridiam: DPFPS: APG:

Total Debt:

PABs: TIFIA:

Public Funds:

2014 figures

33

Ferrovial today:

1Q’15 Results

34

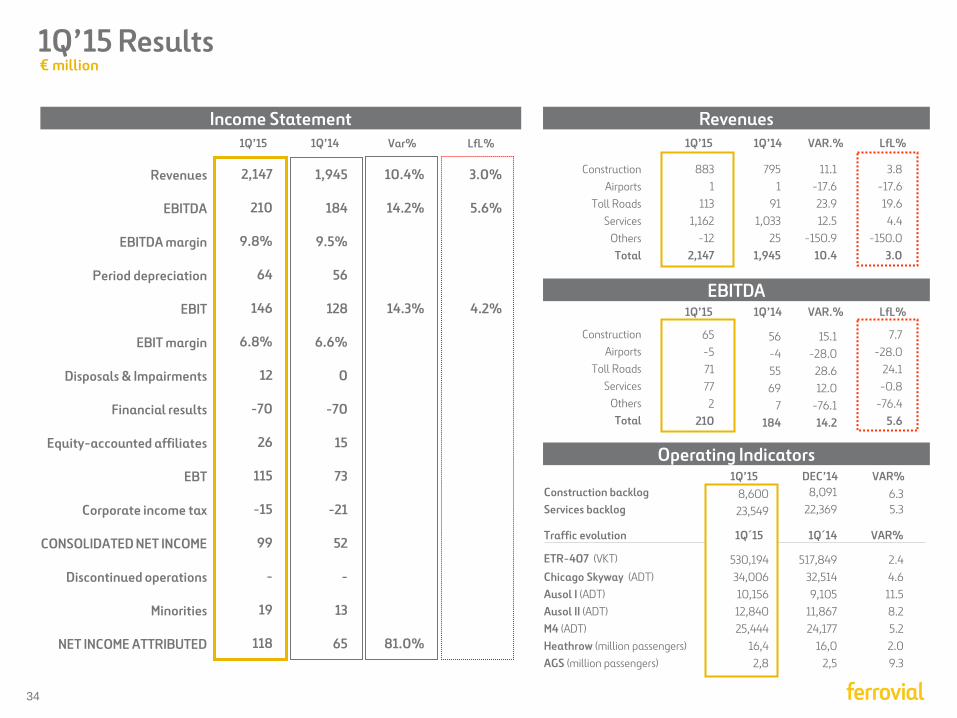

JUN’14 Var%

2,147

210

9.8%

64

146

6.8%

12

-70

26

115

-15

99

-

19

118

10.4%

14.2%

14.3%

81.0%

Construction Airports

Toll Roads Services

Others Total

883 1

113 1,162

-12 2,147

795 1

91 1,033

25 1,945

11.1 -17.6 23.9 12.5

-150.9 10.4

3.8 -17.6 19.6

4.4 -150.0

3.0

Construction Airports

Toll Roads Services

Others Total

65 -5 71 77

2 210

56 -4 55 69

7 184

15.1 -28.0

28.6 12.0

-76.1 14.2

7.7 -28.0

24.1 -0.8

-76.4 5.6

1Q’15 1Q’14 VAR.% LfL%

1,945

184

9.5%

56

128

6.6%

0

-70

15

73

-21

52

-

13

65

1Q’14

Construction backlog Services backlog

Traffic evolution

ETR-407 (VKT) Chicago Skyway (ADT) Ausol I (ADT) Ausol II (ADT) M4 (ADT) Heathrow (million passengers) AGS (million passengers)

VAR% 8,600 23,549

1Q´15

530,194 34,006 10,156 12,840 25,444

16,4 2,8

8,091 22,369

1Q´14

517,849 32,514 9,105

11,867 24,177

16,0 2,5

6.3 5.3

VAR%

2.4 4.6

11.5 8.2 5.2 2.0 9.3

1Q’15 DEC’14

LfL%

3.0%

5.6%

4.2%

1Q’15 Results

Revenues

EBITDA

EBITDA margin

Period depreciation

EBIT

EBIT margin

Disposals & Impairments

Financial results

Equity-accounted affiliates

EBT

Corporate income tax

CONSOLIDATED NET INCOME

Discontinued operations

Minorities

NET INCOME ATTRIBUTED

Income Statement Revenues

EBITDA

Operating Indicators

1Q’15 1Q’14 VAR.% LfL%

1Q’15

€ million

35

(1) Proportional: All EBITDA figures are aggregated in a proportional basis to the Ferrovial equity stake in each company or project (mainly ETR 407 toll road in Canada and UK airports).

Diversified portfolio

Services Construction Toll Roads Airports

Non Capital Intensive PROFIT GENERATION CASH GENERATION

Fully consolidated Method

€210Mn Proportional (1)

€389Mn

Capital Intensive LONG DURATION

LONG TERM VALUE

EBITDA

Services

Toll Roads

Construction

Airports

50% Spain

14% UK

17% US & Canada

18% RoW

25% Spain

41% UK

25% US & Canada

9% RoW

€ million 1Q’15 figures

Ex – Infrastructure Projects Infrastructure Projects

31%

37%

34%-2% 15%

22%

32%

31%

36

Disclaimer

This document may contain statements that constitute forward looking statements about the Company. These statements are

based on financial projections and estimates and their underlying assumptions, statements regarding plans, objectives and

expectations, which refer to estimates regarding, among others, future growth in the different business lines and the global

business, market share, financial results and other aspects of the activity and situation relating to the Company.

Such forward looking statements, by its nature, are not guarantees of future performance and involve risks and uncertainties, and

other important factors that could cause actual developments or results to differ from those expressed in these forward looking

statements.

Analysts and investors, and any other person or entity that may need to take decisions, or prepare or release opinions about the

securities issued by the Company, are cautioned not to place undue reliance on those forward looking statements which speak only

as of the date of this communication. They are all encouraged to consult the Company’s communications and periodic filings made

with the relevant securities markets regulators and, in particular, with the Spanish Securities Markets Regulator.