ferrovial Ferrovial App · UNITED NATIONS PARTNER IN SUSTAINABLE DEV’T & MEMBER OF PRIVATE SECTOR...

62

ferrovial Ferrovial App

-

Upload

phamnguyet -

Category

Documents

-

view

213 -

download

0

Transcript of ferrovial Ferrovial App · UNITED NATIONS PARTNER IN SUSTAINABLE DEV’T & MEMBER OF PRIVATE SECTOR...

1

ferrovial Ferrovial App

2

FY2016 figures

TALENT MANAGEMENT: engaged on optimize workforce & develop mobility of talent.

ENGAGEMENT: focus on being an employer of choice in the sector and markets in which it works & promote a flexible work environment.

CULTURE: attend to develop company’s leaders for an innovative culture. Ferrovial UNIVERSITY

ACKNOWLEDGEMENTS Ferrovial has been included in the DJSI (Dow Jones Sustainability Index) for the last 15 consec years, at a global level; in the FTSE 4Good index for the past 11, in the Carbon Disclosure Project for the past 5, and is also a member of Stoxx and MSCI Global Sustainability Index.

Ferrovial assumes a firm commitment on emissions reduction and environmental impact of their activities. In addition, It also drives generation of new ideas and models of business, to offer its clients & users of its assets, innovative solutions with lower environmental impact.

People Environment TALENT MANAGEMENT, ENGAGEMENT & CULTURE Operating excellence & innovation are possible given Ferrovial employees’ talent, high engagement & corporate culture. Over 96.000 people work in the Group to offer the best solutions in the markets where it operates.

WORKFORCE

Ferrovial has been recognized as Top Employer in Spain for 7 consecutive years

SERVICES 81,0%

AIRPORTS 0,03% TOLL ROADS 0,9%

CONSTRUCTION 17,0%

New competences model for 360º performance appraisal.

Implementation of 70/20/10 development model to impulse professionals' improvement.

Meeting point to catalyze learning and knowledge

School that creates a unique leadership model of company to prepare leaders and innovative teams capable of anticipating new times by acting as internal references

Forum for exchange that facilitates synergies & global business opportunities

-31,6% REDUCTION OF CO2 EMISSIONS RECYCLED WASTE (t)

-18,1% 2.083.333 -35,4% IN RELATIVE TERMS

(tCO2 eq/€mn) (2009-2016)

IN ABSOLUTE TERMS (2009-2016)

NEW REDUCTION TARGET (2009-2016)

WATER FOOT PRINT • Business Water Index (BWI): 4,146,441. Water

footprint related to water consumption and discharge carried out in Ferrovial activities.

• Water Treatment Index (WTI): -322,183,025.

The impact of the water treatment process of Cadagua and the treatment of leachate in landfills of Ferrovial Servicios and Amey on the footprint of Ferrovial.

• Water Access Index (WAI): -413.738; related to water supply projects in Social Action program.

POLAND

3

FY2016 figures

INNOVATION PROCESS

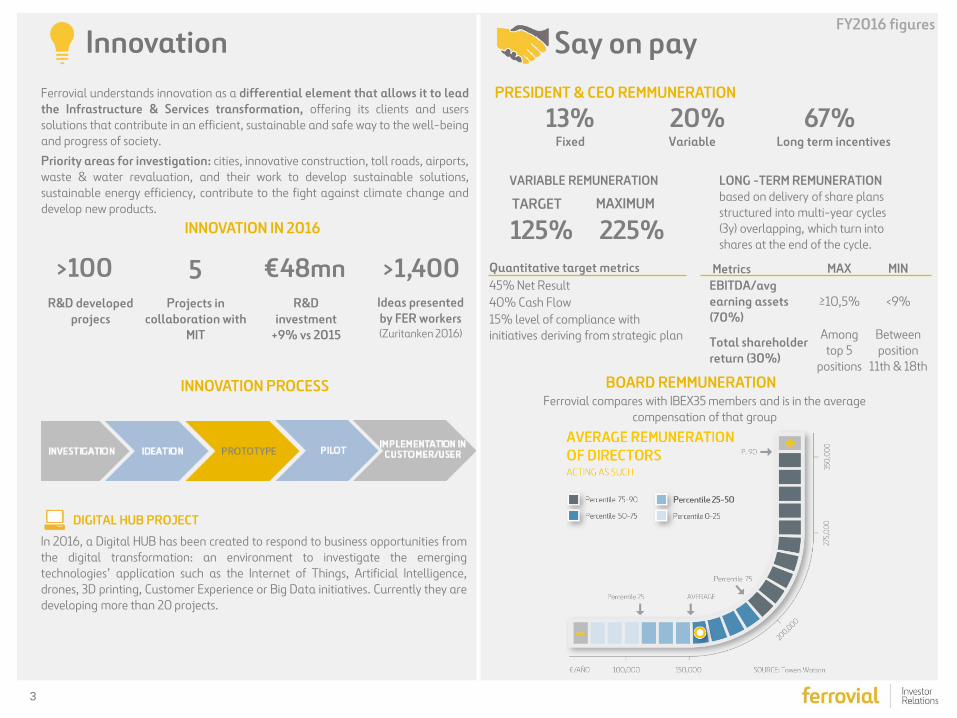

Ferrovial understands innovation as a differential element that allows it to lead the Infrastructure & Services transformation, offering its clients and users solutions that contribute in an efficient, sustainable and safe way to the well-being and progress of society. Priority areas for investigation: cities, innovative construction, toll roads, airports, waste & water revaluation, and their work to develop sustainable solutions, sustainable energy efficiency, contribute to the fight against climate change and develop new products.

INNOVATION IN 2016

>100 €48mn 5 R&D

investment +9% vs 2015

R&D developed projecs

Projects in collaboration with

MIT

DIGITAL HUB PROJECT

Say on pay Innovation PRESIDENT & CEO REMMUNERATION

13% 20% 67% Variable Fixed Long term incentives

BOARD REMMUNERATION

125% 225% MAXIMUM TARGET

VARIABLE REMUNERATION LONG -TERM REMUNERATION based on delivery of share plans structured into multi-year cycles (3y) overlapping, which turn into shares at the end of the cycle.

Metrics MAX MIN EBITDA/avg earning assets (70%)

≥10,5% <9%

Total shareholder return (30%)

Among top 5

positions

Between position

11th & 18th

Quantitative target metrics 45% Net Result 40% Cash Flow 15% level of compliance with initiatives deriving from strategic plan

Ferrovial compares with IBEX35 members and is in the average compensation of that group

In 2016, a Digital HUB has been created to respond to business opportunities from the digital transformation: an environment to investigate the emerging technologies’ application such as the Internet of Things, Artificial Intelligence, drones, 3D printing, Customer Experience or Big Data initiatives. Currently they are developing more than 20 projects.

>1,400 Ideas presented by FER workers (Zuritanken 2016)

4

FY2016 figures Community

UNITED NATIONS PARTNER IN SUSTAINABLE DEV’T & MEMBER OF PRIVATE SECTOR ADVISORY GROUP

In its commitment to the scope of Sustainable Development Goals (SDG), Ferrovial actively participates in the community through the development and execution of social programs to significantly improve people's lives. The company has a key role in the social and economic development of the countries where it carries out activities.

COMMUNITY INVESTMENT PROGRAMS Social Infrastructures Since 2011, Ferrovial has been working on this development cooperation program, which extends access to water for human consumption and basic sanitation among socially vulnerable risk groups in Africa and Latin America.

Stronger Together This program has been running since 2005 & lets employees choose social project to contribute a monthly amount that Ferrovial matches, thus doubling initial donation. In 2016, three projects were chosen by donating employees.

Community engagement in Spain Ferrovial supports refurbishment & reconditioning of offices set up for distributing food & delivering social aid packages to underprivileged groups. In 2016, Ferrovial provided support with World Vision España to improve conditions in 6 food distribution centers (Madrid, Seville, Mieres, Valencia & Barcelona).

332 COMMUNITY SUPPORT PROJECTS

191,769 BENEFICIARIES IN WATER AND SANITATION

Social Infrastructures Program: Figures & Impact

142,815 BENEFICIARIES

€1,498,126 INVESTED

€497,894 INVESTED

31,417 BENEFICIARIES

€4,565,595 INVESTED

191,769 BENEFICIARIES

18 PROJECTS

Policy Changes:

10% OF ANNUAL BUDGET for

extension of project

Community Commitment

933,152 m3

RECYCLED WATER

Out of which

875,104 m3

TREATED WATER

5

Ferrovial overview & strategy

Ferrovial main assets

Ferrovial FY16 results

Ferrovial 1Q17 results

Appendix: 407ETR toll road Managed Lanes toll roads 407ETR vs Managed Lanes Diversified porftolio Historic consolidated & business units figures

Table of Contents

6

Who we are… A transport infrastructure provider/operator with a strong focus on CF generation, based in Spain, but with c.88% international SOTP.

Pricing power, dynamic tolling & very long duration are our main differential factors vs other toll road operators. 407ETR (downtown Toronto, 43% stake) represents 43% of our value. Open, fully electronic, with +9% 2002-15 tariff CAGR, +9.5% 2016. Our managed lanes in Dallas (US) have an even more flexible tariff structure; prices can change every 5 minutes. We own & operate Heathrow (25%) & 3 regional airports (50%) in UK. Annual dividends received from 407ETR & Airports are above €400mn.

Our Construction unit is a tool to compete for complex infrastructure projects (80% of sales are civil works) present mostly in US, Poland & expanding in Australia. It generates on average c€250mn Operating CF, with c.€30mn capex. Services provides a full range of services to cities (asset management, energy efficiency...). 48% of sales from UK.

Strong financial position: €697mn net cash at parent Co, with infrastructure debt ring-fenced at individual projects. Shareholder remuneration up from €282mn to €544mn (2009-16, +93%) through scrip dividends & share buybacks. c.55% of analysts’ SOTP is consolidated by equity method, distorting any EBITDA multiple comparison versus peers.

How we create value… With our industrial approach in the global infrastructure cycle, and our three differential capabilities:

1. Managing and minimizing risks at the different stages of the project life 2. Offering innovative solutions to our clients 3. Generating operational efficiencies in projects

Objective: to increase CF generation & profitability in Construction & Services, and increase value of Infrastructure projects, to then crystallize it through greater flow of dividends or asset rotation.

Four pillars: profitable growth, selective internationalization, operational excellence and innovation; and financial discipline.

All our activities must be sustainable, from an economic, social and environmental standpoint.

Ferrovial Overview & Strategy In

fras

truc

ture

Co

ntra

ctin

g

7

World leading private infrastructure provider present in toll roads, airports and cities

AIRPORTS CONSTRUCTION TOLL ROADS SERVICES

Design Financing Operating Building Maintaining

CANADA

UK IRELAND

SPAIN

POLAND

USA

Construction Airports

Toll Roads Services

AUSTRALIA

GROUP REVENUES

Note: Airports & 407ETR are Equity Consolidated

COLOMBIA CHILE

FERROVIAL IN THE WORLD MAIN FIGURES

€10.8bn Revenues €0.9bn EBITDA 8.8% EBITDA Margin €33.5bn Backlog* €1bn OCF

2016 RESULTS

* Combined Construction & Services, incl. JVs

• Civil engineering • Industrial construction • Water treatment

• Largest airport private investor • Owns & operates key UK airports (incl.

Heathrow) with a combined 89mn passengers a year

• Leading sponsor of toll roads development worldwide

• 407ETR in Canada & 26 other concessions in 8 different countries

• Leading provider of infrast. Services, such as mgmt & maintenance

• Urban services, waste management, • Focus on intelligent cities • Broadspectrum acquisition opens new

markets in North America & Australia

What is ?

EX-INFRASTRUCTURE PROJECTS

INFRASTRUCTURE PROJECTS

Listed since 1999 Market Cap €14.3bn * 30 April 2017

24%

30%12%12%

15%7%

Spain UKUS & Canada PolandAustralia Others

56%5%

39%

Services Toll Roads

Construction Airports

8

PARENT COMPANY

INFRASTRUCTURE

PROJECTS

EX-INFRASTRUCTURE

PROJECTS

Capital intensive / Inflation protected / LT duration & financing

Non capital intensive / Backlog visibility / EPS accretive

Ring fenced debt

Net cash position

1. Cash Flow generation

€290mn Dividends from Toll roads

€134mn Dividends from Airports

€325mn

€342mn EBITDA from Construction

EBITDA from Services

€ million 2016 figures

64% Institutional & Retail Investors 36% Founder’s family members

(Chairman controls 20%)

…

9

OPERATING CASH FLOW (pre-tax) 2016Construction 245

Services 395Toll Roads (dividends) 290

Airports (dividends) 134Others (69)

TOTAL 995

SOURCES & USES

Ex- Infrastructure Projects

40% DIVIDENDS FROM INFRA PROJECTS CONSTRUCTION SERVICES

* Includes Divestments & Financing

1. Cash Flow generation – Balanced Contribution € million

37%23%27%13%

Dividends

Operating CF

Investments

Other*

Interest Taxes & others

2016 figures

OPERATING CASH FLOW

639

995

(356)

(544)

Operating Cash Flow Organic Investments Activity Cash Flow (pre-tax)

Shareholder remuneration

(pre-tax) Before M&A investment

CF GENERATION vs DIVIDENDS

10

15

526352 256

1,343

2017 2018 2019 2020 >2021

-3,064

-1,987-1,547

-1,172

31

9071,484 1,663 1,632 1,514

697

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

PARENT COMPANY

2. Profitable growth. Solid Financial Situation

Net debt evolution ex-infrastructure projects EX–INFRASTRUCTURE PROJECTS

TOLL ROADS* €4,426mn

* €641mn related to NTE 35W & I77, toll roads under construction.

INFRASTRUCTURE PROJECTS Debt maturities ex-infrastructure projects

NET CASH €697mn

€mn

€mn

NET DEBT €4,963mn

€ million FY16 figures

11

3. Shareholder remuneration (CF Criteria)

308367

917

477 510 532 544

2010 2011 2012 2013 2014 2015 2016

+2.3%

+77%

SHAREHOLDER REMUNERATION PROPOSAL 2017

Scrip dividend (€/share)

First scrip dividend (equivalent to 2016 complementary dividend) 0.32 0.311

Second scrip dividend (equivalent to 2017 interim dividend) 0.42 0.408 TOTAL 0.74 0.719

Share buyback of up to €275mn or up to 19m shares

2016

of up to €275mn or up to 19m shares

12

Valuation split by currency & asset Analyst consensus valuation

12% 5%

Toll Roads Airports Construction Services UK Rest of Services Cash

Over 70% in CAD, USD & EUR, 17% in GBP

5% from UK Services, 12% from UK airports

Source: Analyst consensus, December 2016

17%

RoW EUR CAD & USD Australia GBP

13

Ferrovial main assets

14

Valuation per asset type

ETR40745%

Man. Lanes7%

Heathrow9%

Rest of Infra7%

Construction12%

Services UK5%

Rest of Services

12%

Net cash at parent

3%

c.50% from 407ETR toll road & Managed Lanes (Canada, US)

68% from Infrastructure assets

Source: Analyst consensus, December 2016

68% INFRASTRUCTURE

15

145 120 135 190300

460600

680 730 750 790

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

27.0X

6.8x

1999 2016

525

16,110

1999 FY16

407ETR

• 108kms in Greater Toronto • Tariff freedom • Tariff flexibility by segment, direction, time, day… • 81 years to maturity (to 2098) • Alternative routes are strongly congested • Fast & reliable travel times • Free flow, fully electronic system • Strong collection security

Extraordinary operating performance in the past 10 years

Tariffs +9% CAGR (2006-16) EBITDA +10.8% CAGR (2006-16) 100% payback first 10 years

DIVIDEND GROWTH (CADmn)

31x

LOWER LEVERAGE (X EBITDA) EQUITY VALUATION 100% (€mn)

LONG DURATION & PRICING FLEXIBILITY Canada, Ferrovial stake 43%, Equity method

16

Strong EBITDA growth … even with negative traffic and GDP

EBITDA growth 6.8x GDP growth (avg 2010-16)

2016 EBITDA, the highest growth of the past 13 years. annual % growth

18.9

15.4 15.4

14.1

11.7

15.6

1.5

7.2

12.6

10.89.7 9.7

10.3

14.2

17.3

13.2

1.0

7.5

5.4

2.9

6.1

0

-1.7

5.5

-0.5

0.6 0.7

3.4 3.34.1

2.81.9

3.1 3.22.6

2.01.2

-2.7

3.4 3.01.9 2.0

2.5

1.2 1.2

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

EBITDA growth Traffic growth GDP growth (annual)

407ETR

17

Managed Lanes

• 3 Managed Lanes in Dallas - Fortworth (2 open: NTE & LBJ) • Dynamic tolling: can change tolls every 5 mins • 44 years to maturity (to 2061) • Higher speed allowed (70mph vs 60 on free lanes) • Free flow, fully electronic system • Tariff freedom up to cap (lifted if speed <50mph) • Tariff flexibility by segment, direction, time, day • No collection risk

Strong growth in both Managed Lanes since their opening TRANSACTIONS (mn) EBITDA (USDmn)

2

11

15

Q4

2014

Q4

2015

Q4

2016

7

16

Q4

2015

Q4

2016

3.9

5.76.0

Q4

2014

Q4

2015

Q4

2016

7.0

10.0

Q4

2015

Q4

2016

LONG DURATION & PRICING FLEXIBILITY

+5.1% (4Q’16)

Texas, USA, Global Consolidation. NTE 57%, LBJ 51%

NTE +45.4%

(4Q’16)

LBJ +39.4%

(4Q’16)

NTE +129%

(4Q’16)

LBJ

18

Heathrow Airport

• Best Airport in Western Europe (2nd time) • T5 ‘Best Airport Terminal (5th consecutive Yr) • Best Airport for Shopping (7th consecutive Yr) (Skytrax World Airport Awards) • Best Airport Award Europe, (3nd time) & Best European Airport over 40mn (ACI Awards) • “Operator” & “ Marketing Campaign” of the year (Frontier Awards)

• Traffic growth: +1% vs 2015 • Record passengers: 75,7mn 2016 • Heathrow operates at over 98% capacity • Annual flights 472,067 (1,293 per day) • Connected 183 destinations in 82 countries • Cargo 25% UK exports (1.5mn metric tonnes) • 3rd Runway Government’s green light announced Oct 25th

THE BUSIEST AIRPORT IN THE WORLD

63%79%

2007 2016

Punctuality

48%

84%

2007 2016

% Passengers rating Heathrow as Excellent or Very Good

SERVICE STANDARDS STRONG EBITDA GROWTH (£mn)

756885 967

1,132 1,1541,421

1,559 1,605 1,682

2008 2009 2010 2011 2012 2013 2014 2015 2016

… WITH HIGH SERVICE STANDARDS

2008-2016 CAGR : +10,5%

London, UK, Ferrovial stake 25%, Equity method

19

Source: Company information, December 2016 * Dividends paid in 2016 ** GBP Hedge, December 31st, 2016

325

113UK airports dividends*

GBP Hedge**

Over 3y expected GBP dividends hedged

INFLATION

Ferrovial positively exposed to higher inflation in UK

Macro impact FX

USD, CAD & AUD appreciated vs EUR

Additional GBP155mn 0.85 – 0.9 put spread

INTEREST RATES

15,237

-7,332

Heathrow RAB Heathrow debt linked to RPI

90% FIXED DEBT

+100bps on interest rates

+€8mn financial expenses

GBP million

GBP million

20

Looking ahead

UK turnaround Addressing pipeline in Australia

Services Construction

Additional order book from infra projects

Attractive shareholder remuneration

Scrip dividend Share Buyback

Active pipeline Infra projects

US /Australia /Canada/Poland Monitoring other

markets

High quality assets

Strong traffic trends Higher dividends

21

Ferrovial FY16 Results

22

Traffic growth across the board New awards in core markets (I-66) Total order book increase (+6.3%)

Strong operating growth

Solid cash generation €995mn Operating Cash Flow (pre-tax)

• 40% from infra projects dividends

2016 Highlights

Shareholder remuneration €544mn (€532mn in 2015)

Corporate transactions Broadspectrum acquisition Transchile acquisition Mature toll road asset rotation

• Chicago Skyway (US) • M3 & M4 stakes (Ireland) • Portuguese toll roads stakes (to be completed)

Solid financial position Ex-infra projects

€697mn net cash position €356mn ordinary CAPEX €1bn M&A investment

Environment UK & US

23

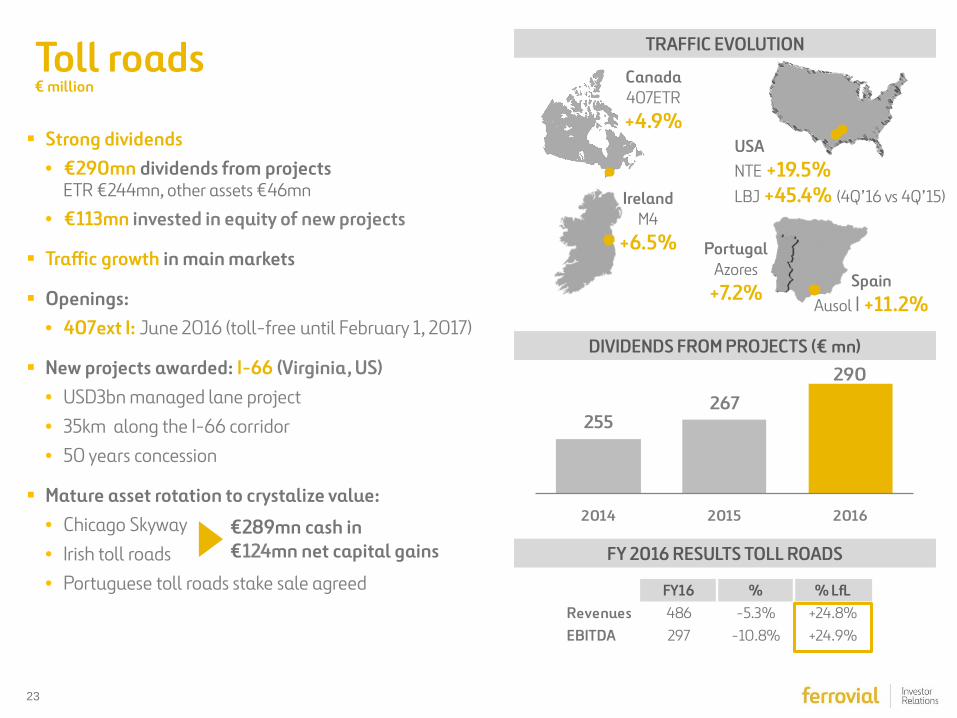

Toll roads

Strong dividends • €290mn dividends from projects

ETR €244mn, other assets €46mn

• €113mn invested in equity of new projects

Traffic growth in main markets

Openings: • 407ext I: June 2016 (toll-free until February 1, 2017)

New projects awarded: I-66 (Virginia, US) • USD3bn managed lane project • 35km along the I-66 corridor • 50 years concession

Mature asset rotation to crystalize value: • Chicago Skyway • Irish toll roads • Portuguese toll roads stake sale agreed

€ million

TRAFFIC EVOLUTION

DIVIDENDS FROM PROJECTS (€ mn)

FY 2016 RESULTS TOLL ROADS

Canada 407ETR +4.9%

USA NTE +19.5% LBJ +45.4% (4Q’16 vs 4Q’15) Ireland

M4 +6.5% Portugal

Azores +7.2%

Spain Ausol I +11.2%

FY16 % % LfLRevenues 486 -5.3% +24.8%EBITDA 297 -10.8% +24.9%

255267

290

2014 2015 2016€289mn cash in €124mn net capital gains

24

407ETR Equity method, Ferrovial stake 43%

407ETR FY 2016 RESULTS (CAD mn)

407ETR Regions includes: Toronto, Durham, Peel, Halton & York Source: Government of Ontario Places to Grow

POPULATION GROWTH (2021 – 2041) EMPLOYMENT GROWTH (2021 – 2041)

407 EAST PHASE I OPENING IMPACT

407 East I opened to traffic on June 20, 2016 407 East I was toll-free until February 1, 2017 Overall traffic impact above +2%

(CADmn) FY16 %Revenues 1,135 +13.2%EBITDA 985 +17.3%

Traffic (VKTs'000) 2,640,770 +4.9%Dividends 790 +5.3%

Highest EBITDA growth over the last 10 years

Growth in population & employment to support traffic

25

Managed Lanes (NTE & LBJ)

SPEEDS AT NTE

GROWTH SINCE OPENING (NTE)

TOLL RATES EVOLUTION (NTE)

GROWTH SINCE OPENING (LBJ)

Eastbound workday on segment 2

CAP linked to inflation

Average toll rate per

transaction (2016):

~USD3.05 +18.2%

Index 100

12am 3am 6am 9am 12pm 3pm 6pm 9pm

2014 2015 2016 Cap

100

120

140

160

180

200

4Q'15 1Q'16 2Q'16 3Q'16 4Q'16Transactions Revenue Rev/Txn

100

150

200

250

300

350

4Q'14 1Q'15 2Q'15 3Q'15 4Q'15 1Q'16 2Q'16 3Q'16 4Q'16

Revenue Txns Rev/Txn

0

10

20

30

40

50

60

70

80

12am 3am 6am 9am 12pm 3pm 6pm 9pm

2011 2016 Non-Tolled Lanes2016 TEXpress Lanes

26

Services

€ 395mn operating cash flow (OCF)

UK Services: Challenging environment

• Budget constrains • Fewer project works (higher margins) • Birmingham contract (legal expenses)

Positive evolution in Spain Profitability remains stable with EBITDA margin at 10.7%

7 months contribution from Broadspectrum

SPAIN UK

Revenues

EBITDA

Order book

€ million

PERFORMANCE BY GEOGRAPHY (LfL)

OPERATING CASH FLOW

FY16 % % LfLRevenues 6,078 +24.1% +2.8%EBITDA 325 +4.2% -12.9%EBITDA % 5.4%Order book 24,431 +7.2% -11.0%

302 289

395

2014 2015 2016

+1%-45%-16%

+5%+5%-6%

Restructuring plan focused on profitability >900 layoffs

-€21mn impact

2017E Sales slightly below 2016 figures

2017E EBITDA margin: 3% - 4%

27

Acquisition rationale:

• Platform for medium and long term growth

• Bought at low point sector cycle

• Leading position in public and infrastructure services in Australia & New Zealand

• Exposure to US

• AUD8bn order book provides revenue visibility

Ongoing strategic review

• No renewal of immigration centres contracts (contracts end October 2017)

Broadspectrum contribution: 7 months in 2016 • Revenues: €1,446mn • EBITDA: €91mn • EBITDA margin: 6.3%

100% acquisition

Broadspectrum delisted

Consolidation from May 31st

Broadspectrum TRANSACTION DETAILS TOTAL PIPELINE

Transaction terms:

• EV €934mn

• Equity €499mn

• Debt €435mn

46%

22%

13%

19%

Government TransportUrban Infrastructure Resources

TOTAL

AUD30.3bn

AUD million

28

Construction

€245mn operation cash flow (OCF)

Profitability remains at high level (EBITDA margin 8.1%) Driven by Budimex (Poland)

Strong growth in Budimex

• Revenues +8.1% (LfL)

• EBITDA +70.8% (LfL)

• Order book +6.0% (LfL)

€ million

OPERATING CASH FLOW

ORDER BOOK BY COUNTRY BUDIMEX ORDER BOOK (PLNbn)

+107%

FY16 % % LfLRevenues 4,194 -2.2% -2.7%EBITDA 342 -13.1% -12.8%EBITDA % 8.1%Order book 9,088 +4.1% +2.6%

4.36.1

8.4 8.9

2013 2014 2015 2016

236

272

245

2014 2015 2016

17% 22% 27% 8% 25%

Spain Poland US UK RotW

29

HAH 100% GBP million

+8.3% dividend increase (GBP325mn vs GBP300mn in 2015 )

All-time high in passenger number for 2016 (75.7mn of passenger; +1% vs. 2015)

RAB: positive impact from higher inflation

Heathrow expansion: Government support confirmed in Oct 2016 & draft NPS released in Feb 2017

AGS (Equity method, FERROVIAL stake 50%):

+6.7% dividend increase (GBP64mn vs GBP60mn in 2015)

Traffic +2.8% (14.4mn pax.) EBITDA +10.8% thanks to cost controls

(PAX million)

AIRPORTS TRAFFIC

OPERATING IMPROVEMENT AT HEATHROW

(Equity method, FERROVIAL stake 25%)

82 Countries

30% Transfer

Share

1% Growth

94% International

471k Flights 75.7m

Passengers

194 Destinations

HAH P&L FY16 % LfL

Revenues 2,809 +1.5%

EBITDA 1,683 +4.7%

EBITDA % 59.9%

Net debt 14,307 +6.5%

63%79%

2007 2016

Punctuality

48%

84%

2007 2016

% Passengers rating Heathrow as Excellent or Very Good

FY16 % LfL

Heathrow 75.7 +1.0%

Glasgow 9.4 +7.4%

Aberdeen 3.1 -12.2%

Southampton 2.0 +9.8%

Record service standards

30

4.19

3.00

3.50

4.00

4.50

LHR

3.20

3.40

3.60

3.80

4.00

4.20

4Q'0

62Q

'07

4Q'0

72Q

'08

4Q'0

82Q

'09

4Q'0

92Q

'104Q

'102Q

'114Q

'112Q

'124Q

'122Q

'134Q

'132Q

'144Q

'142Q

'154Q

'152Q

'164Q

'16

ASQ

scor

e (o

ut o

f 5)

European Average Heathrow European top quartile

Heathrow: Best ever passenger service levels

Passenger satisfaction European ranking

FY16 figures

Quarterly passenger satisfaction

4Q 2006 – 4Q 2016

European competitors European comparators

Baggage performance Departures misconnect rate per 1,000 passengers within 15 minutes of schedule

4Q16

Best Airport in Western Europe

World’s Best Airport Shopping

Terminal 5 – World’s Best Airport Terminal

•2016 Europe’s Best Airport

•(over 40 million passengers)

63%78% 78% 79%

2007 2014 2015 2016

40

19 17 14

2007 2014 2015 2016

31

FY16 Results

Income Statement Revenues

EBITDA

Operating Indicators

€ million

FY16 FY15 Var % LfLConstruction 4,194 4,287 -2.2% -2.7%

Airports 4 8 -49.9% -68.6%

Toll Roads 486 513 -5.3% 24.8%

Services 6,078 4,897 24.1% 2.8%

Other -4 -6 n.a. n.a.

Total 10,759 9,701 10.9% 1.2%

FY16 FY15 Var % LfLConstruction 342 393 -13.1% -12.8%

Airports -18 -13 -45.7% -54.7%

Toll Roads 297 333 -10.8% 24.9%

Services 325 312 4.2% -12.9%

Other -2 1 n.a. n.a.

Total 944 1,027 -8.1% -4.0%

FY16 2015 Var %Construction Backlog 9,088 8,731 4.1%

Services Backlog inc.JVs 24,431 22,800 7.2%

Traffic evolution FY16 FY15 Var % ETR 407 (Kms 000) 2,640,770 2,517,214 4.9%

NTE (IMD) 30,485 25,553 19.3%

LBJ (IMD) 31,582 12,861 145.6%

Ausol I (IMD) 14,637 13,165 11.2%

Heathrow (Mn pax) 75.7 75.0 1.0%

AGS (Mn pax) 14.4 14.0 2.8%

FY16 FY15 Var % LfL

Revenues 10,759 9,701 10.9% 1.2%

EBITDA 944 1,027 -8.1% -4.0%

EBITDA margin 8.8% 10.6%

Period depreciation 342 256

EBIT 602 770 -21.9% -9.7%

EBIT margin 5.6% 7.9%

Disposals & Impairments 324 131

Financial results -391 -637

Equity-accounted affiliates 82 312

EBT 617 577

Corporate income tax -233 54

CONSOLIDATED NET INCOME 383 631

Discontinued operations 0 0

Minorities -7 89

NET INCOME ATTRIBUTED 376 720 -47.7%

32

Ferrovial 1Q17 Results

33

1Q17 Results HIGHLIGHTS

Revenues & EBITDA

€ million

1Q17 Var %REVENUES 2,885 38.5%

Construction 965 19.7%

Airports 2 89.2%

Toll Roads 105 -11.3%

Services 1,807 56.1%

Others 6 n.a.

1Q17 Var.EBITDA 227 16.7%

Construction 56 -4.9%

Airports -4 -4.0%

Toll Roads 77 1.7%

Services 95 56.5%

Others 2 n.a.

P&L 1Q17

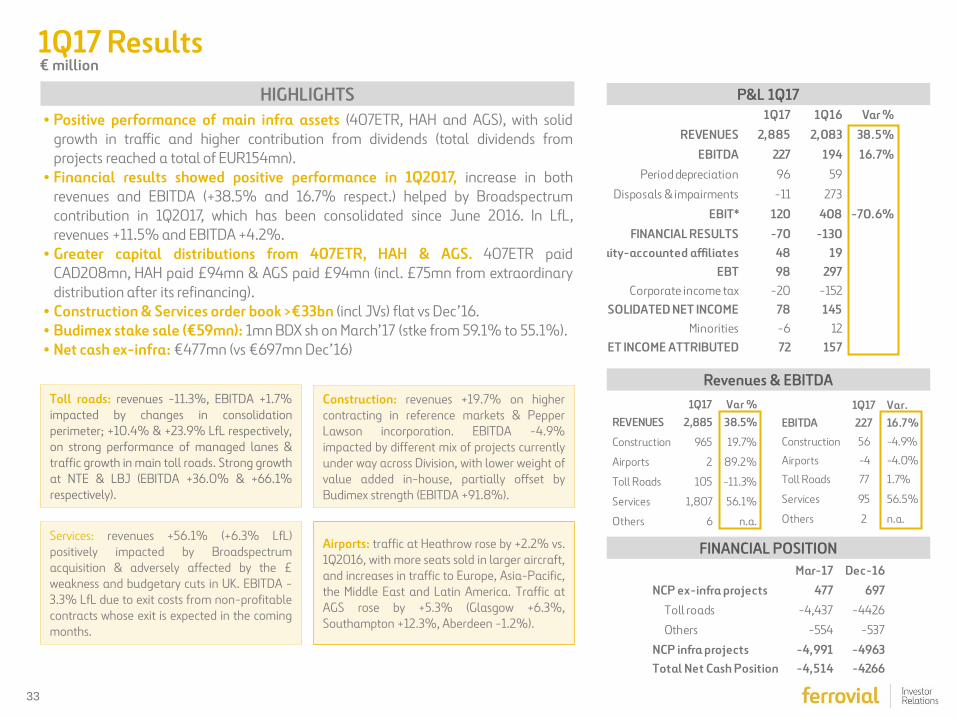

• Positive performance of main infra assets (407ETR, HAH and AGS), with solid growth in traffic and higher contribution from dividends (total dividends from projects reached a total of EUR154mn).

• Financial results showed positive performance in 1Q2017, increase in both revenues and EBITDA (+38.5% and 16.7% respect.) helped by Broadspectrum contribution in 1Q2017, which has been consolidated since June 2016. In LfL, revenues +11.5% and EBITDA +4.2%.

• Greater capital distributions from 407ETR, HAH & AGS. 407ETR paid CAD208mn, HAH paid £94mn & AGS paid £94mn (incl. £75mn from extraordinary distribution after its refinancing).

• Construction & Services order book >€33bn (incl JVs) flat vs Dec’16. • Budimex stake sale (€59mn): 1mn BDX sh on March’17 (stke from 59.1% to 55.1%). • Net cash ex-infra: €477mn (vs €697mn Dec’16)

1Q17 1Q16 Var %REVENUES 2,885 2,083 38.5%

EBITDA 227 194 16.7%Period depreciation 96 59

Disposals & impairments -11 273

EBIT* 120 408 -70.6%FINANCIAL RESULTS -70 -130

uity-accounted affiliates 48 19EBT 98 297

Corporate income tax -20 -152NSOLIDATED NET INCOME 78 145

Minorities -6 12NET INCOME ATTRIBUTED 72 157

Mar-17 Dec-16NCP ex-infra projects 477 697

Toll roads -4,437 -4426

Others -554 -537

NCP infra projects -4,991 -4963Total Net Cash Position -4,514 -4266

FINANCIAL POSITION

Toll roads: revenues -11.3%, EBITDA +1.7% impacted by changes in consolidation perimeter; +10.4% & +23.9% LfL respectively, on strong performance of managed lanes & traffic growth in main toll roads. Strong growth at NTE & LBJ (EBITDA +36.0% & +66.1% respectively).

Construction: revenues +19.7% on higher contracting in reference markets & Pepper Lawson incorporation. EBITDA -4.9% impacted by different mix of projects currently under way across Division, with lower weight of value added in-house, partially offset by Budimex strength (EBITDA +91.8%).

Airports: traffic at Heathrow rose by +2.2% vs. 1Q2016, with more seats sold in larger aircraft, and increases in traffic to Europe, Asia-Pacific, the Middle East and Latin America. Traffic at AGS rose by +5.3% (Glasgow +6.3%, Southampton +12.3%, Aberdeen -1.2%).

Services: revenues +56.1% (+6.3% LfL) positively impacted by Broadspectrum acquisition & adversely affected by the £ weakness and budgetary cuts in UK. EBITDA -3.3% LfL due to exit costs from non-profitable contracts whose exit is expected in the coming months.

35

Appendix

Introduction to 407ETR Toll road

Managed Lanes Toll roads

407ETR vs Managed Lanes

Diversified porftolio

Historic consolidated & business units figures

36

High density population area

Ring road of Toronto 108 km

407

407

East extension

Area of expansion

407 ETR

Location

37

407 ETR

All Electronic Roadside Tolling System

Sophisticated electronic toll highway

NO toll-booths, “closed ticket” tolling scheme (on/off ramps)

NO stopping or slow-downs to pay

ALL vehicles able to use highway

Transponder not required. If valid transponder is not detected, digital

images are taken at entry and exit and invoices posted to registered

car owner

Tolls billed monthly

38

407 ETR

LOCATION

Greater Toronto Area 23% of Canada population

TRAFFIC

Alternatives routes are highly congested

HIGH HOUSEHOLD INCOME

46% higher than Canada average

NO REGULATORY REVIEWS

During concession life (99 years)

SPEED

Alternatives routes 40kph

vs 100kph at 407

NON-STOP TOLL FACILITY

Fully electronic with interchanges

every 3km

TOLL RATE HIGH FLEXIBILITY

Including segment, direction, time of

the day

FAST

Reliable travel times

Fast Safe

Reliable

39

525

16,110

1999 FY16

Strong dividend flow

Equity valuation sharp increase

2098

100% pay-back

in first 10 years

Valuation x31

* December 2016 analysts consensus

407 ETR

81 years to maturity

407 ETR

Cash flow and valuation overview

€ million CASH GENERATION (1999 - FY2016) EQUITY VALUATION 100% (€mn)

€ million

MATURITY

31x

Cash GenerationInitial equity invest.(62%) -326 mnDividends 1,761 mn10%Disposal 640 mn

NET CASH IN 2,075 mn

40

353

985

77%79%

76%

80%82%

83% 83% 83% 83% 84%

87%

2006 2016

456

1,135

2006 2016

81 years to maturity

100% pay-back in first 10 years

Free-tariff revision

≅ 9% CAGR 02-15*

* Tariff increase for light Vehicles in Peak hours regular zone (%)

407 ETR

Financial overview ($CAD million)

REVENUES

EBITDA

OPEX

CAPITAL EXPENDITURE

DIVIDENDS

Net Debt / EBITDA X

2016 figures

CAGR: 9.5%

CAGR: 3.8%

103

150

2006 2016

CAGR: 10.8%

97 90

38

72 77 8870 74

5570 72

145 120 135 190300

460600

680 730 750 790

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

27.0X

6.8x

1999 2016

41

407 ETR

Value creation: EBITDA-GDP-Traffic

Strong EBITDA growth even with negative traffic and GDP

annual % growth

18.9

15.4 15.4

14.1

11.7

15.6

1.5

7.2

12.6

10.89.7 9.7

10.3

14.2

17.3

13.2

1.0

7.5

5.4

2.9

6.1

0

-1.7

5.5

-0.5

0.6 0.7

3.4 3.34.1

2.81.9

3.1 3.22.6

2.01.2

-2.7

3.4 3.01.9 2.0

2.5

1.2 1.2

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

EBITDA growth Traffic growth GDP growth (annual)

42

Appendix

Introduction to 407ETR Toll road

Managed Lanes Toll roads

407ETR vs Managed Lanes

Diversified porftolio

Historic consolidated & business units figures

43

A solution to congestion on “existing urban corridors”

Active management of “newly added capacity” through tolling

by means of

Free

Lanes

Free

Lanes

Tolled Lanes Speed >50mph

“Express Tollway within an Existing Highway”

Managed Lanes

New assets landmark

44

Time of the day

Eastbound Westbound

00.00 2.00 4.00 6.00 8.00 10.00 12.00 14.00 16.00 18.00 20.00 22.00 24.00 12.00 2.00 4.00 6.00 8.00 10.00 12.00 2.00 4.00 6.00 8.00 10.00 12.00

Time of the day

Peak period

Managed Lanes

Level of demand

NTE (untolled) 407ETR (tolled)

45

LBJ

Dallas and Fort Worth Regional Map Managed Lanes regional map

NTE 1-2

NTE 35W

46

Toll rates – tariff threshold

Toll Rate Cap 0.75 c/mi

Demand threshold 3300 pce/h2-lane sections

Speed Threshold 50 mi/h

12:00 1:00 2:00 3:00 4:00 5:00 6:00 7:00 8:00 9:00 10:00 11:00 12:00Hour startingAnalysis by segment and direction

Freedom under the cap TOTAL FREEDOM Freedom under the cap

Speed

Demand

Toll Rate

Tariff threshold

0.84 $/mi

47

CINTRA MERIDIAM DALLAS

FIRE&POLICE PENSION SCHEME

DESCRIPTION:

LENGTH:

CONCESSION PERIOD:

TARIFF POLICY:

Dallas-Fort Worth Metroplex, Major thoroughfares

between Fort Worth and DFW Airport

13 mile section (IH 820 & SH 183 in Tarrant County)

52 years (since 2009)

Open Road Tolling System (no toll booths) with a dynamic tolling

regime (every 5 minutes) to maintain at all times a minimum speed of

50 mph

● No toll-booths, fully electronic free flow tolling system

● Tollway within a freeway: Motorists will be provided with a choice of

driving in non-tolled GP lanes or paying a toll to bypass such GP

lanes

● Tolls setting to ensure minimum speed on new lanes

● As demand grows and capacity becomes scarce, pricing power

increases

● Physically separated from the GP lanes with controlled access

EQUITY DEBT PUBLIC FUNDS

Managed Lanes

North Tarrant Express Opened on October 2014, 9 months ahead of schedule

KEY CHARACTERISTICS

SHAREHOLDER STRUCTURE

FINANCIAL STRUCTURE

57% 33% 10%

21% 52% 27%

48

CINTRA MERIDIAM DALLAS FIRE&POLICE

PENSION SCHEME

108Km Electronic toll

DESCRIPTION:

LENGTH:

CONCESSION PERIOD:

TARIFF POLICY:

IH 635 (Dallas County), the most populous county in Texas

13 mile section of the IH 635 and IH 35E

52 years (since 2009)

Open Road Tolling System (no toll booths) with a dynamic tolling

regime (every 5 minutes) to maintain at all times a minimum speed of

50 mph

● No toll-booths, fully electronic free flow tolling system

● Tollway within a freeway: Motorists will be provided with a choice of

driving in non-tolled GP lanes or paying a toll to bypass such GP

lanes

● Tolls setting to ensure minimum speed on new lanes

● As demand grows and capacity becomes scarce, pricing power

increases

● Physically separated from the GP lanes with controlled access

For further information on the concession, check the following links: https://youtu.be/9GMj3H5OovA https://youtu.be/pnNFZ8qJY-c

EQUITY DEBT PUBLIC FUNDS

Managed Lanes

Lyndon B Johnson Opened on September 10th 2015, 3 months ahead of schedule

APG

51% 26% 16% 7%

24% 56% 19%

SHAREHOLDER STRUCTURE

FINANCIAL STRUCTURE

KEY CHARACTERISTICS

49

32% 59% 9%

50% 26% 14% 10%

CINTRA MERIDIAM DALLAS FIRE&POLICE PENSION SCHEME

DESCRIPTION:

LENGTH:

CONCESSION PERIOD:

TARIFF POLICY:

2 “managed lanes” in each direction of the IH-35W, segments 3A and

3B (3B segment to be built by TxDOT)

10.2 mile section (segments 3A 6.2 miles and 3B 4 miles)

48 years (since 2013)

Open Road Tolling System (no toll booths) with a dynamic tolling

regime (every 5 minutes) to maintain at all times a minimum speed of

50 mph

● The corridor south to the 3A segment is currently ranked as the most

congested roadway in Texas.

● No toll-booths, fully electronic free flow system

● Tollway within a freeway: Motorists will be provided with a choice of

driving in non-tolled GP lanes or paying a toll to bypass such GP

lanes

● Tolls setting to ensure minimum speed on new lanes

● As demand grows and capacity becomes scarce, pricing power

increases

● Physically separated from the GP lanes with controlled access EQUITY DEBT PUBLIC FUNDS

APG

Managed Lanes

North Tarrant Express 35W Expected to open in mid-2018

SHAREHOLDER STRUCTURE

FINANCIAL STRUCTURE

KEY CHARACTERISTICS

50

• First privately-financed road development project of its kind to reach financial close in 2010.

• Texas’ third big recent road project to reach financial close since 2008.

• First combination of TIFIA and tax exempt PABs.

• First private activity bond issuance for a toll road.

• First time that a U.S.-based pension fund made a direct investment in a highway concession.

21%

51%

28%

26%

56%

18%

Figures in US Dollars

Managed Lanes

Financial Overview

32%

59%

9%

• Very competitive capital structure in spite of the difficult market conditions.

• Strong portion of the debt from TIFIA program with its flexible amortizing structure during the first 25 years.

2.05 bn

426 mn

242 mn (57%) 141 mn (33%) 43 mn (10%)

1,048 mn

398 mn 650 mn

573 mn

2.62 bn

672 mn

343 mn (51%) 107 mn (16%)

44 mn (7%) 178 mn (26%)

1,456 mn

606mn 850 mn

490 mn

1.36 bn

430 mn

215 mn (50%) 60 mn (14%) 43 mn (10%) 112 mn (26%)

805 mn

274 mn 531mn

126 mn

Total Investment: Private Equity:

Cintra: Meridiam: DPFPS: APG:

Total Debt:

PABs: TIFIA:

Public Funds:

Financial structure

51

Appendix

Introduction to 407ETR Toll road

Managed Lanes Toll roads

407ETR vs Managed Lanes

Diversified porftolio

Historic consolidated & business units figures

52

How does the 407ETR compare to the new Managed Lanes? 407ETR Managed Lanes (NTE1-2)

• 56.7%. Global consolidation • Meridiam (33%), Dallas fire & police pension scheme (10%) • 52 years

Opened October 2014 (44 years remaining)

• Dallas-Fort Worth Metroplex, between Fort Worth & DFW Airport • 13 miles. 2 segments.

2 lanes per direction Tollway within a freeway

• Predictability & reliable travel times (minimum speed 50m/hr) Higher speed allowed on NTE (60mph in free lanes, 70mph NTE) Safety & comfort

• Yes. No toll booths, fully electronic, free flow system • Freedom to set tariffs up to cap ($0.84, updated with inflation)

Cap is lifted if av. speed <50m/hr of cars >3,300pce/h (2 lanes) Dynamic tolling (tariffs can be changed every 5 minutes) Different tariffs depending on segment, direction, time, day..

• Not a regulated activity, but a contractual agreement • From TxDOT (who charges the drivers). No collection risk

• 5 initial years lock-up

• 43%. Equity consolidated • SNC Lavalin (17%), CPPIB (40%) • 99 years

Opened 1999 (81 years remaining)

• Greater Toronto Area (Ontario province) • 108kms. 24 segments

From 2+2 lanes up to 5+5 lanes per direction (dep on segment) Separate toll road

• Predictability & reliable travel times Alternative routes are highly congested Average speed: 100km/h vs 40km/h on the alternative Safety & comfort

• Yes. No toll booths, fully electronic, free flow system • Freedom to set tariffs

Penalty paid if traffic falls below threshold Tariffs can be changed every 30 days Different tariffs depending on segment, direction, time, day..

• Not a regulated activity, but a contractual agreement • From drivers. Licence plate not renewed if tolls not paid.

• Strong growth (from CAD85mn 2005 to 750mn 2015)

Participation: Partners: Concession period: Location: Length: Benefits: Open tolling? Tariff Policy: Regulatory risk? Collection: Dividends:

53

Appendix

Introduction to 407ETR Toll road

Managed Lanes Toll roads

407ETR vs Managed Lanes

Diversified porftolio

Historic consolidated & business units figures

54

17%

20%

31%

32%

(1) Proportional: All EBITDA figures are aggregated in a proportional basis to the Ferrovial equity stake in each company or project (mainly ETR 407 toll road in Canada and UK airports).

Diversified portfolio

Services Construction Toll Roads Airports

Non Capital Intensive PROFIT GENERATION CASH GENERATION

Fully consolidated Method

€944Mn Proportional (1)

€1,721Mn

Capital Intensive LONG DURATION

LONG TERM VALUE

EBITDA

Services

Toll Roads

Construction

Airports

Spain UK US & Canada Poland Spain UK US & Canada

€ million 2016 figures

EX – INFRASTRUCTURE PROJECTS INFRASTRUCTURE PROJECTS

36%

34%

31%

-2%

43% 4% 19% 13% 22% 37% 25% 4%

Australia RoW

9% 11%

Poland Australia RoW

5%7%

55

Appendix

Introduction to 407ETR Toll road

Managed Lanes Toll roads

407ETR vs Managed Lanes

Diversified porftolio

Historic consolidated & business units figures

56

2015 2014 Var %

Construction Backlog 8,731 8,091 7.9%

Services Backlog inc.JVs 22,800 22,369 1.9%

Traffic evolution 2015 2014 Var %

ETR 407 (Kms 000) 2,517,214 2,436,888 3.3%

Chicago Skyway (IMD) 25,553 19,845 28.8%

Ausol I (IMD) 13,165 11,711 12.4%

Ausol II (IMD) 15,402 13,989 10.1%

M4 (IMD) 28,512 26,606 7.2%

Heathrow (Mn pax) 75.0 73.4 2.2%

AGS (Mn pax) 14.0 13.3 5.1%

2015 2014 Var % LfLConstruction 393 349 12.8% 2.3%

Airports -13 -12 -1.3% -1.3%

Toll Roads 333 257 29.6% 25.6%

Services 312 387 -19.4% -26.4%

Other 1 2 -59.8% n.s.

Total 1,027 983 4.5% -4.2%

2015 2014 Var % LfLConstruction 4,287 3,942 8.8% 1.2%

Airports 8 9 -9.7% -9.7%

Toll Roads 513 432 18.9% 17.2%

Services 4,897 4,401 11.3% 4.2%

Other -6 18 -133.9% -133.5%

Total 9,701 8,802 10.2% 3.2%

2015 Results

Income Statement Revenues

EBITDA

Operating Indicators

€ million

2015 2014 Var % LfL

Revenues 9,701 8,802 10.2% 3.2%

EBITDA 1,027 983 4.5% -4.2%

EBITDA margin 10.6% 11.2%

Period depreciation 256 244

EBIT 770 738 4.3% -7.0%

EBIT margin 7.9% 8.4%

Disposals & Impairments 131 5

Financial results -637 -377

Equity-accounted affiliates 312 138

EBT 577 504

Corporate income tax 54 -152

CONSOLIDATED NET INCOME 631 352

Discontinued operations 0 0

Minorities 89 50

NET INCOME ATTRIBUTED 720 402 79.1%

57

Historic consolidated figures: 2012-2016 Operating CF ex-infra projects (before tax.)

EBITDA & Margins

mn €

• Net cash at parent company

• Net debt at infra projects level (non recourse to parent company)

Revenues

Net debt

OCF ex-infra ND

-6,595 -7,015 -7,862 -6,057-4,963

1,489 1,663 1,632 1,514 697

2012 2013 2014 2015 2016

N. CASH EX-INFRA

INFRA PROJ.

7,446 7,686 8,1668,802 9,701

45% 38% 32% 31% 28%

55% 62% 68% 69% 72%

2012 2013 2014 2015 2016

Dom estic International

927 934 983 1,027 944

12.1%11.4%

11.2%10.6%

8.8%

7 .0 %

8 .0 %

9 .0 %

1 0. 0%

1 1. 0%

1 2. 0%

0

2 00

4 00

6 00

8 00

1 ,0 00

1 ,2 00

2012 2013 2014 2015 2016

EBITDA Margin

-16 -27 -58 -70 -69

365 461 596399 424

591663 538

560 640

2012 2013 2014 2015 2016

Op. CF (Construction& Services)

Dividens from infra(Toll roads & Airports)

Holding & Others

Op. CF:Construction 100 304 236 272 245Services 491 359 302 289 395

Dividends:Toll Roads 220 242 255 267 290Airports 145 219 341 132 134

Holding & Others -16 -27 -58 -70 -69

939 1,097 1,076 889 995 -5,106 -5,352 -6,230 -4,542 -4,266

mn €

58

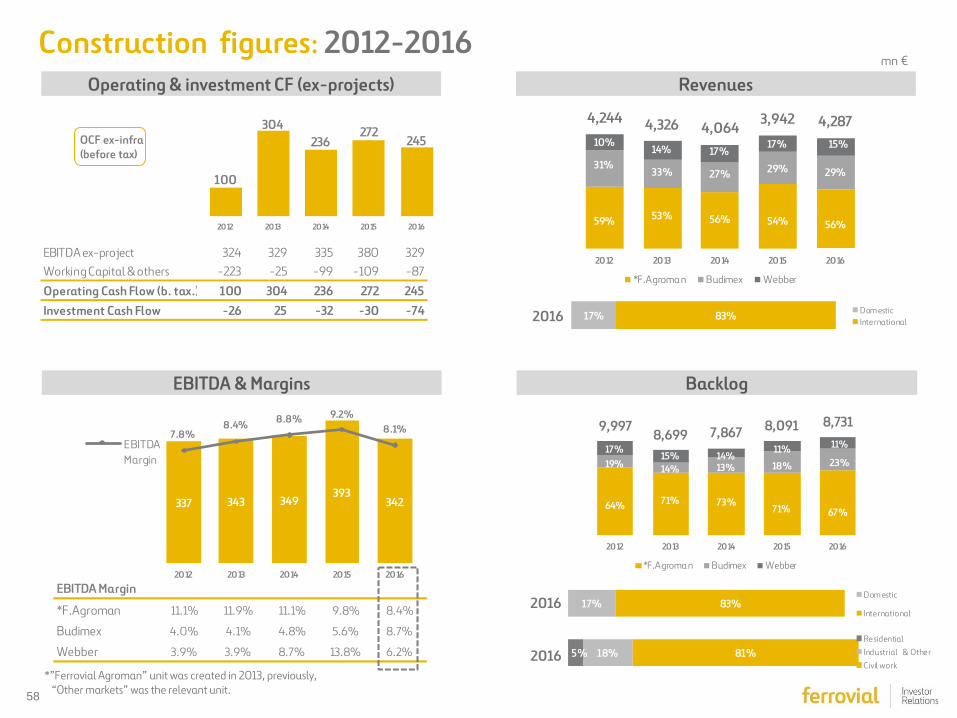

Construction figures: 2012-2016 mn €

2016

2016

Operating & investment CF (ex-projects)

Backlog

Revenues

EBITDA & Margins

100

304236

272245

2012 2013 2014 2015 2016

4,244 4,326 4,064 3,942 4,287

59% 53% 56% 54% 56%

31%33% 27% 29% 29%

10%14% 17%

17% 15%

2012 2013 2014 2015 2016

*F.Agroma n Budimex Webber

337 343 349393

342

7.8%8.4% 8.8% 9.2%

8.1%

0 .0 %

1 .0 %

2 .0 %

3 .0 %

4 .0 %

5 .0 %

6 .0 %

7 .0 %

8 .0 %

9 .0 %

1 0. 0%

0

5 0

1 00

1 50

2 00

2 50

3 00

3 50

4 00

2012 2013 2014 2015 2016

EBITDAMargin

17% 83%Dom estic

International

OCF ex-infra (before tax)

EBITDA Margin

*F.Agroman 11.1% 11.9% 11.1% 9.8% 8.4%

Budimex 4.0% 4.1% 4.8% 5.6% 8.7%

Webber 3.9% 3.9% 8.7% 13.8% 6.2% 2016

9,9978,699 7,867 8,091 8,731

64% 71% 73%71% 67%

19% 14% 13% 18% 23%17%

15% 14%11% 11%

2012 2013 2014 2015 2016

*F.Agroma n Budimex Webber

*”Ferrovial Agroman” unit was created in 2013, previously, “Other markets” was the relevant unit.

EBITDA ex-project 324 329 335 380 329Working Capital & others -223 -25 -99 -109 -87

Operating Cash Flow (b. tax.) 100 304 236 272 245Investment Cash Flow -26 25 -32 -30 -74

5% 18% 81%ResidentialIndustrial ~ & OtherCivil work

17% 83% Dom esticInternational

59

Operating & investment CF (ex-projects)

Backlog with JV’s

Revenues

EBITDA & Margins

2016

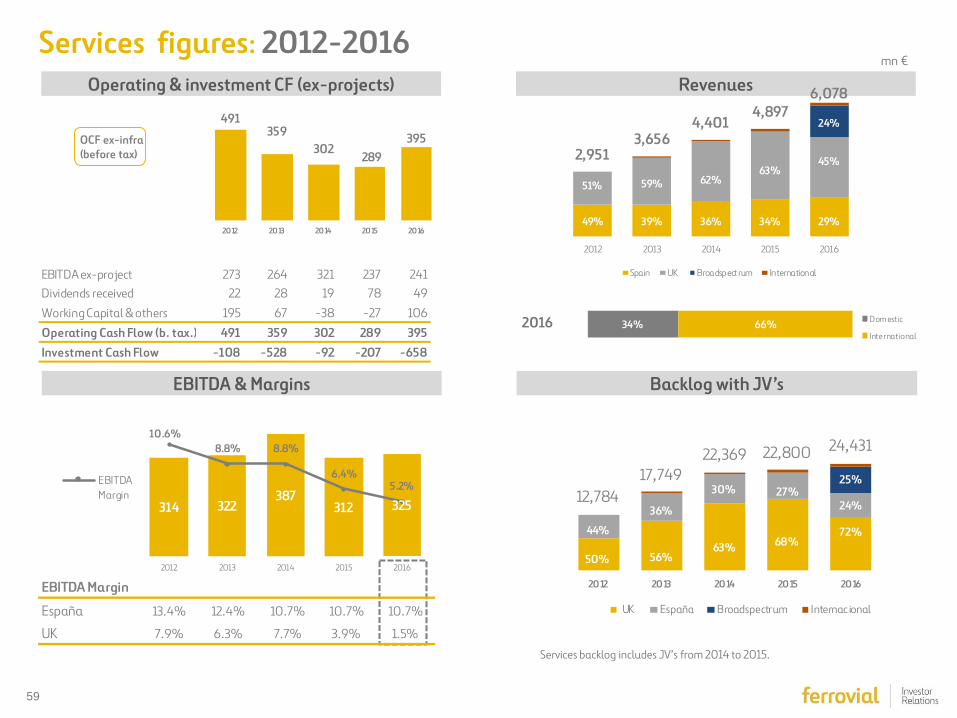

491359

302289

395

2012 2013 2014 2015 2016

2,9513,656

4,4014,897

6,078

49% 39% 36% 34% 29%

51% 59% 62%63%

45%

24%

2012 2013 2014 2015 2016

Spain UK Broadspect rum International

314 322387

312 325

10.6%8.8% 8.8%

6.4%5.2%

0 .0 %

1 .0 %

2 .0 %

3 .0 %

4 .0 %

5 .0 %

6 .0 %

7 .0 %

8 .0 %

9 .0 %

1 0. 0%

1 1. 0%

1 2. 0%

0

5 0

1 00

1 50

2 00

2 50

3 00

3 50

4 00

2012 2013 2014 2015 2016

EBITDAMargin 12,784

17,74922,369 22,800 24,431

50% 56%63% 68%

72%44%

36%

30% 27%24%

25%

2012 2013 2014 2015 2016

UK España Broadspectrum Internac ional

Services backlog includes JV’s from 2014 to 2015.

34% 66% Dom estic

International

OCF ex-infra (before tax)

Services figures: 2012-2016 mn €

EBITDA ex-project 273 264 321 237 241Dividends received 22 28 19 78 49

Working Capital & others 195 67 -38 -27 106

Operating Cash Flow (b. tax.) 491 359 302 289 395Investment Cash Flow -108 -528 -92 -207 -658

EBITDA Margin

España 13.4% 12.4% 10.7% 10.7% 10.7%

UK 7.9% 6.3% 7.7% 3.9% 1.5%

60

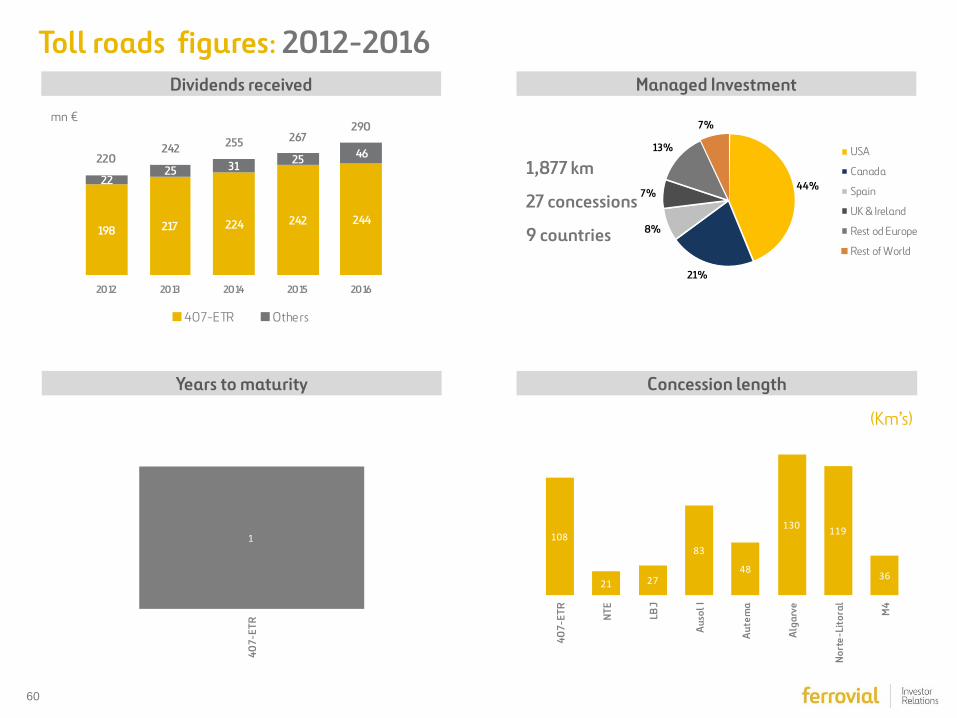

Toll roads figures: 2012-2016

mn €

1,877 km

27 concessions

9 countries

(Km’s)

Dividends received Managed Investment

Concession length Years to maturity

198 217 224 242 244

2225 31 25 46220

242 255 267290

2012 2013 2014 2015 2016

407-ETR Others

44%

21%

8%

7%

13%

7%

USA

Canada

Spain

UK & Ireland

Rest od Europe

Rest of World

1

407-

ETR

108

21 27

83

48

130 119

3640

7-ET

R

NTE

LBJ

Auso

l I

Aute

ma

Alga

rve

Nort

e-Li

tora

l

M4

61

Airports figures: 2012-2016

mn € Dividends received from airports

Heathrow (25% stake)

2 runways 183 destinations 82 Countries 80 Airlines

*AGS (50% stake) Aberdeen Glasgow Southampton

Traffic mn passengers HAH EBITDA (mn £)

Heathrow shareholders Portfolio Heathrow

*Ferrovial increased its stake in AGS from 25% (held through HAH) to 50% in 2014.

Capital expenditure (mn £)

Ferrovial Qatar Brittania GIC CIC Alinda USS

95

38

145

219

341

132

2012 2013 2014 2015

AGS

HA H

844

1,1411,283

853

627

2011 2012 2013 2014 2015

1,2871,355 1,441

1,5411,608

2011 2012 2013 2014 2015

2011 2012 2013 2014 2015

Heathrow 69.4 70.0 72.3 73.4 75.0AGS 11.8 12.3 12.6 13.3 14.0

Glasgow 6.9 7.2 7.4 7.7 8.7

Aberdeen 3.1 3.4 3.5 3.8 3.5

Southampton 1.8 1.7 1.7 1.8 1.8

25% 20% 12.6% 11.2% 11.2% 10% 10%

62

Disclaimer

This document may contain statements that constitute forward looking statements about the Company. These statements are

based on financial projections and estimates and their underlying assumptions, statements regarding plans, objectives and

expectations, which refer to estimates regarding, among others, future growth in the different business lines and the global

business, market share, financial results and other aspects of the activity and situation relating to the Company.

Such forward looking statements, by its nature, are not guarantees of future performance and involve risks and uncertainties, and

other important factors that could cause actual developments or results to differ from those expressed in these forward looking

statements.

Analysts and investors, and any other person or entity that may need to take decisions, or prepare or release opinions about the

securities issued by the Company, are cautioned not to place undue reliance on those forward looking statements which speak only

as of the date of this communication. They are all encouraged to consult the Company’s communications and periodic filings made

with the relevant securities markets regulators and, in particular, with the Spanish Securities Markets Regulator.