Federal Income Tax Update: 2014 and Then What? Tony Curatola Joseph F. Ford Professor Of Accounting...

57

Federal Income Tax Update: 2014 and Then What? Tony Curatola Joseph F. Ford Professor Of Accounting and Tax Drexel University http://home.comcast.net/~acuratola © 2015 A.P.Curatola MACE 1

-

Upload

mitchell-briggs -

Category

Documents

-

view

217 -

download

1

Transcript of Federal Income Tax Update: 2014 and Then What? Tony Curatola Joseph F. Ford Professor Of Accounting...

Federal Income Tax Update: 2014 and Then What?

Tony CuratolaJoseph F. Ford Professor

Of Accounting and Tax

Drexel University

http://home.comcast.net/~acuratola

© 2015 A.P.Curatola MACE 1

Part 1

Basic Individual TaxpayersIssues

© 2015 A.P.Curatola MACE 2

Individual Tax Provisions2014 & 2015 Tax Rates

Increase income tax rates for individuals from 10, 15, 25, 28, 33 & 35% for 2012 to 10, 15, 25, 28, 33, 35, and 39.6% for excess taxable income in 2014 & 2015

$457,600 for MJ, $432,200 for HofH & $406,750 for S $464,850 for MJ, $439,000 for HofH & $413,200 for S

The tax rate bracket are doubled for only MJ filing at 10% & 15% Marriage penalty returns What is the impact of the DOMA ruling?

MACE 3© 2015 A.P.Curatola

Individual Tax Deductions in 2014 (2015)

Standard Deduction $6,200 ($6,300) for single and $12,400 ($12,600) for MJ filing

No marriage penalty (theoretically)

MACE 4© 2015 A.P.Curatola

Individual Tax Deductions in 2014 (2015)

Standard Deduction $6,200 ($6,300) for single & $12,400 ($12,600) for MJ filing

Itemized Deductions 3% phase-out provision returns to those with excess AGI

MJ - $305,050 ($309,900), HofH - $279,650 ($284,050), & S - $254,200 ($258,250)

MACE 5© 2015 A.P.Curatola

Individual Tax Deductions in 2014 (2015)

Personal & Dependent Exemption – $3,950 ($4,000)

Phased-out ratably for AGI in excess of MJ - $305,050 ($309,900), HofH - $279,650 ($284,050), & S - $254,200 ($258,250)

Note: Phase-outs are the same for itemized deductions and personal & dependent exemptions.

MACE 6© 2015 A.P.Curatola

Tax Extender Bill Status Pre Election

Senate Bill: Expiring Provisions Improvement Reform and Efficiency

(EXPIRE) Act

Tabled until November

House Bill: Passed Without Revenue Offsets

Bills withdrawn after November elections

MACE 7© 2015 A.P.Curatola

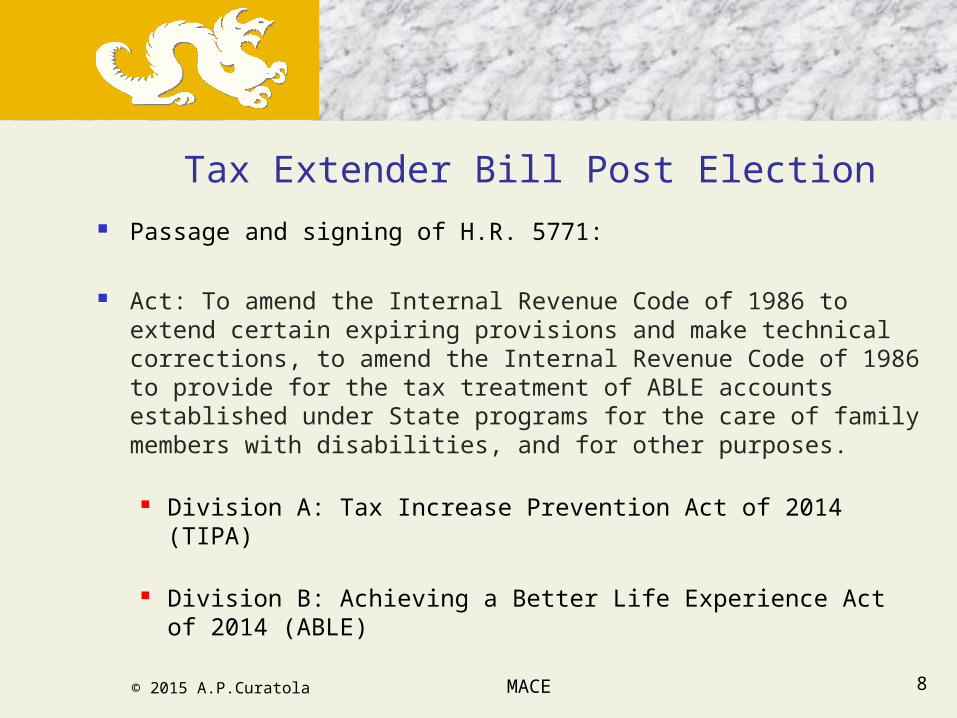

Tax Extender Bill Post Election

Passage and signing of H.R. 5771:

Act: To amend the Internal Revenue Code of 1986 to extend certain expiring provisions and make technical corrections, to amend the Internal Revenue Code of 1986 to provide for the tax treatment of ABLE accounts established under State programs for the care of family members with disabilities, and for other purposes.

Division A: Tax Increase Prevention Act of 2014 (TIPA)

Division B: Achieving a Better Life Experience Act of 2014 (ABLE)

MACE 8© 2015 A.P.Curatola

TIPA Provisions

State & Local General Taxes Deduct in lieu of State income taxes

Teacher’s Classroom Deductions Above the line deduction of up to $250 extended through 2013

Mortgage Insurance Premiums Deductible as mortgage interest extended through 2013

Discharged of indebtedness General (includible) Principal residence (excludable through 2013)

MACE 9© 2015 A.P.Curatola

TIPA Provisions

The new Act contains approximately:

8 extensions for individuals,

31 extensions for business,

11 extensions for energy,

2 extenders for multiemployer DB plans, and of course

Some technical corrections

MACE 10© 2015 A.P.Curatola

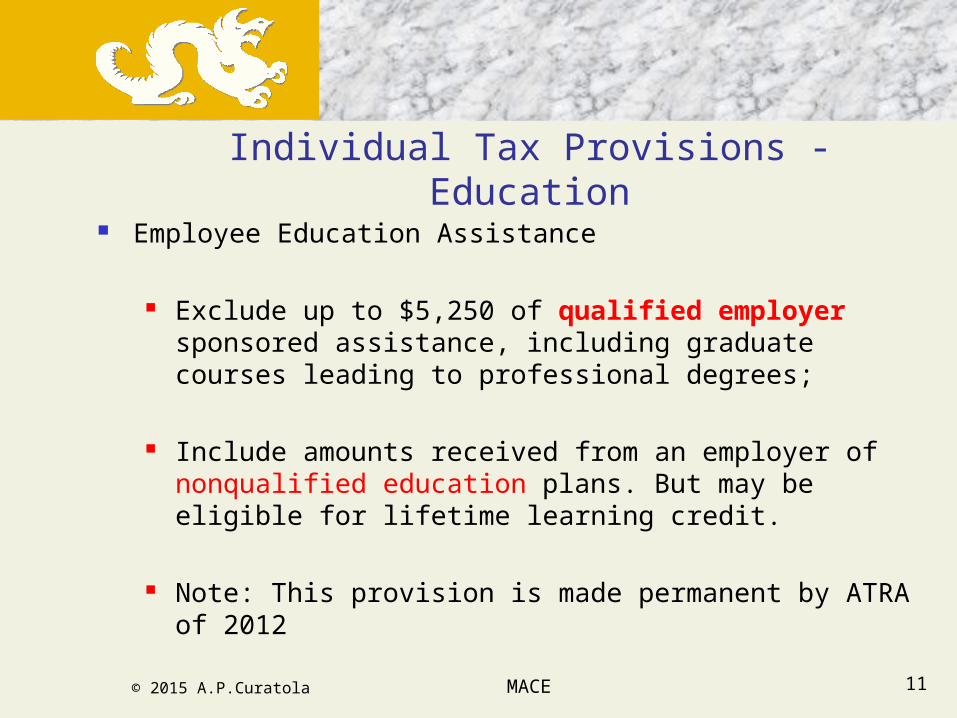

Individual Tax Provisions - Education

Employee Education Assistance

Exclude up to $5,250 of qualified employer sponsored assistance, including graduate courses leading to professional degrees;

Include amounts received from an employer of nonqualified education plans. But may be eligible for lifetime learning credit.

Note: This provision is made permanent by ATRA of 2012

MACE 11© 2015 A.P.Curatola

Individual Tax Provisions - Education

Student Loan Interest (made permanent by TRA of 2012)

Up to $2,500 of student loan interest deductible (not prepaid interest) above the line

Phased out for 2014 & 2015 begins when MAGI exceeds $65k-$80k for singles and $130k-$160k for MJ.

Note: 60-month limitation is not reinstated .

MACE 12© 2015 A.P.Curatola

Individual Tax Provisions - Education

Qualified Tuition and Related Expenses

Above the line deduction extended through 2015

Phase-out provision $4,000 where AGI is < $65,000 ($130,000 for MJ filing)

$2,000 where AGI is between $65,000 and $80,000 ($130,000 and $160,000 when filing married joint)

$0 for all others

MACE 13© 2015 A.P.Curatola

Individual Tax Provisions - Education

American Opportunity Tax Credit (old Hope Credit) For 2014-2017, maximum of $2,500 / year for first 4 years of

post-secondary education, and is calculated as 100% on 1st $2,000, and 25% on next $2,000

The credit is phased out where MAGI is Between $160,000 and $180,000 for married filing jointly, Between $80,000 and $90,000 for all other taxpayers

The credit is applicable to qualified tuition, fees, and course material (was tuition and fees) and may be partially refundable.

MACE 14© 2015 A.P.Curatola

15

Individual Tax ProvisionsAMT Exemption

Tax Year AMT Exemption Amount MFJ & Estate & SS Unmarried MFS Trusts For 2013 80,800 51,900 40,400 22,500

For 2014 82,100 52,800 41,050 22,500

For 2015 83,400 53,600 41,700 22,500

MACE © 2015 A.P.Curatola

16

Individual Tax ProvisionsGift Tax Exclusion in 2014 (2015)

Gift tax exclusion

$14,000 ($14,000) per person per year

And

$145,000 ($147,000) for gifts to a non-US citizen spouse

Estate tax exclusion - $5,340,000 ($5,430,000)

MACE © 2015 A.P.Curatola

17

2014 & 2015 Retirement Planning

Contribution to IRA and Roth IRAs - $5,500 / spouse AGI limitations for deductible IRAs & nondeductible Roth IRAs

Limitation is avoidable by converting nondeductible IRA

Conversion of Traditional IRA to Roth IRA by including entire taxable convertible amount in gross income

Be careful: The 39.6% tax rates & 3.8% tax requires some tax planning

Small business owners - convert SEP & SIMPLE plans to Roth IRA

MACE © 2015 A.P.Curatola

18

2015 (2014) Retirement Planning

SEPs qualifying compensation limit increased to $600 ($550)

Sec 402(g) increased to $18,000 ($17,500)

IRAs: Catch up limit remains at $1,000

SIMPLE: Contribution increased to $12,500 ($12,000) & Catch up increased to $3,000 ($2,500)

Non-SIMPLE: Catch up increased to $6,000 (5,500)

MACE © 2015 A.P.Curatola

19

2015 Inflation Adjustments

See, Revenue Procedure 2014-61, October 30, 2014 for Estate, gift and income tax inflation adjustment figures for calendar year 2015

See Information Release 2014-99 for Retirement plan inflation adjustment figures for calendar year 2015

MACE © 2015 A.P.Curatola

Part 2

Health Care IssuesIndividual Taxpayers

© 2015 A.P.Curatola MACE 20

21

Flexible Spending Account

Maximum deductible contribution

$2,500 in 2014 ($2,550 In 2015)

Options for plan administrators $500 carryover, or 75 day grace period, or Do not adopt either option

$500 carryover limits will be indexed in $50 increments after 2013

MACE © 2015 A.P.Curatola

22

Medicare Tax on Earned Income

Additional 0.9% Medicare Tax on wages, compensation and self-employment income

Over $250,000 filing MJ; Over $125,000 filing MS; or Over $200,000 for all others

Notes: Marriage penalty exists here & withholdings can be an issue Underpayment penalty applies Thresholds are not indexed for inflation

MACE © 2015 A.P.Curatola

23

Medicare Tax on Investment Income Additional 3.8% Medicare Tax on excess net investment income

Over $250,000 filing MJ; Over $125,000 filing MS; or Over $200,000 for all others

Notes: Marriage penalty exists here and withholdings can be an issue Underpayment penalty applies Thresholds are not indexed

MACE © 2015 A.P.Curatola

24

Medicare Tax Calculation

Example: Taxpayer A has wages $190,000 and self-employment income of $40,000.

Result: Taxpayer A has an additional tax of $270

Calculation: $270 = ($230,000 - $200,000) x 0.9%.

Note: The $270 Medicare tax is part of estimate tax payments.

MACE © 2015 A.P.Curatola

25

Medicare Tax Calculation

Example: Taxpayer B has wages and self-employment income of $240,000 and net investment income of $40,000.

Result: Taxpayer A has an additional tax of $1,880

Calculation: $1,880, which is the sum of $360 = ($240,000 - $200,000) x 0.9% and $1,520 = ($280,000 - $240,000) x 3.8%.

MACE © 2015 A.P.Curatola

Part 3

Hot Button IssuesIndividual Taxpayers

© 2015 A.P.Curatola MACE 26

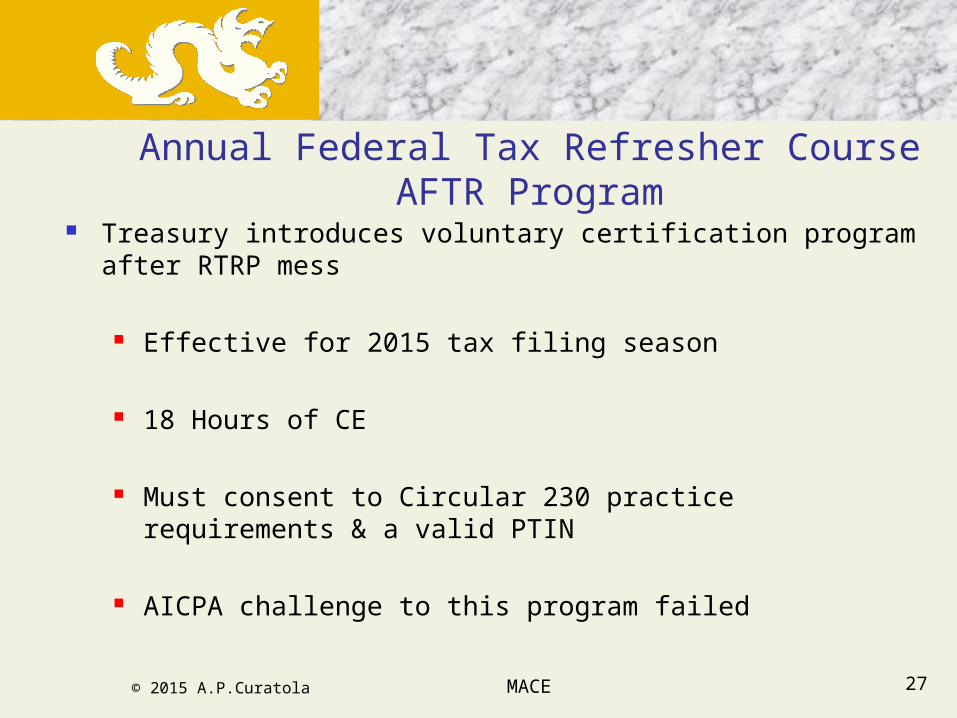

27

Annual Federal Tax Refresher CourseAFTR Program

Treasury introduces voluntary certification program after RTRP mess

Effective for 2015 tax filing season

18 Hours of CE

Must consent to Circular 230 practice requirements & a valid PTIN

AICPA challenge to this program failed

MACE © 2015 A.P.Curatola

28

RTRP

Is RTRP Dead or in a Coma?

Senators Wyden (D-OR) and Cardin (D-MD) introduced legislation on January 7th providing Treasury & IRS explicit authority to regulate paid tax preparers

MACE © 2015 A.P.Curatola

29

ABLE Act of 2014

Purpose:

To encourage and assist individuals and families in saving private funds for the purpose of supporting individuals with disabilities to maintain health, independence, and quality of life.

To provide secure funding for disability-related expenses on behalf of designated beneficiaries with disabilities that will supplement, but not supplant, benefits provided through private insurance, the Medicaid program under title XIX of the Social Security Act, the supplemental security income program under title XVI of such Act, the beneficiary's employment, and other sources.

MACE © 2015 A.P.Curatola

30

ABLE Act of 2014

New IRC Section 529A

Limited to annual gift tax amount (i.e., $14,000 in 2015)

Account accumulates on a tax free basis

Qualified distribution amounts are excluded in gross income

Non-qualified distribution amounts are included in gross income As determined by IRC Section 72, and 10% excise tax applies unless made after the death of the

beneficiary

MACE © 2015 A.P.Curatola

31

New IRC Section 529A

Example from Committee Report

Assume a qualified ABLE account with a balance of $100,000 (of which $50,000 consists of contributions) distributes $10,000 to a beneficiary who has incurred $6,000 of qualified disability expenses. Under section 72, one-half of the distribution ($5,000) is includible in gross income. Under the bill, the $5,000 amount otherwise includible in gross income is reduced by $3,000 ($6,000/$10,000 multiplied by $5,000) to $2,000. An additional tax of $200 (10% of $2,000) is imposed on the distribution.

Problem: When is the balance determined?

MACE © 2015 A.P.Curatola

32

Tax Legislation

Business Tax Overhaul Proposal

Drop tax rates to 25% for ALL businesses

No change in individual tax rates

MACE © 2015 A.P.Curatola

33

Earned Income Tax Credit

Due Diligence (see Reg. Sec. 1.6695-2): Completion & submission of Form 8867 (checklist); EIC worksheet (or other such form); Preparer must not know, or have reason to know, that any

information is incorrect; and Retain copy of Form 8867, EIC worksheet

Penalty: $500 per incident

The IRS is currently sending due diligence warning letters to preparers “who appear not to be complying”

MACE © 2015 A.P.Curatola

34

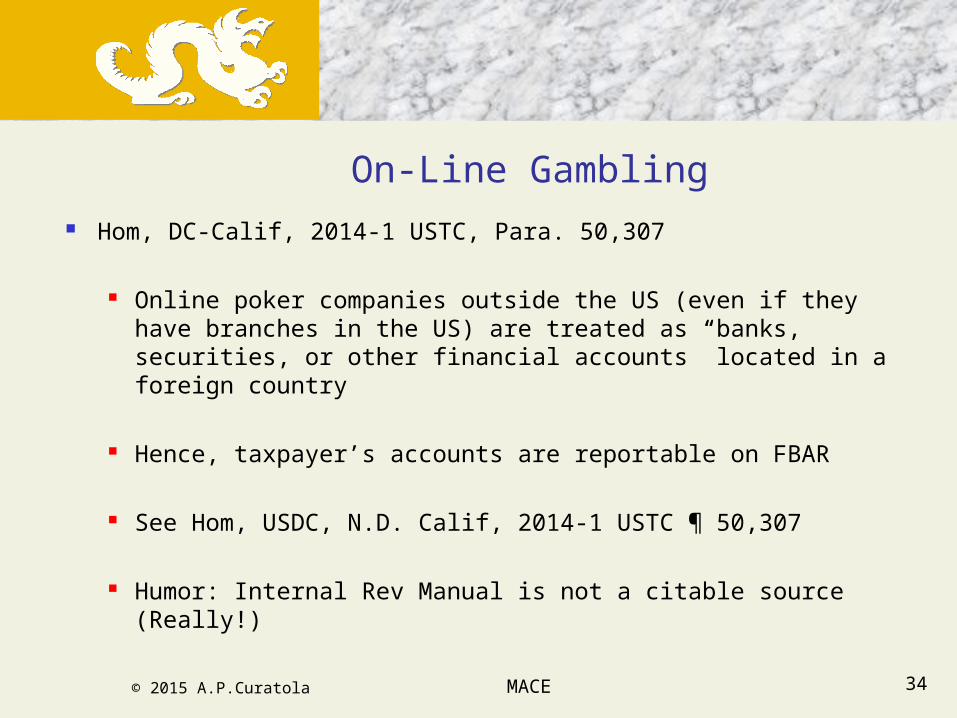

On-Line Gambling

Hom, DC-Calif, 2014-1 USTC, Para. 50,307

Online poker companies outside the US (even if they have branches in the US) are treated as “banks, securities, or other financial accounts” located in a foreign country

Hence, taxpayer’s accounts are reportable on FBAR

See Hom, USDC, N.D. Calif, 2014-1 USTC ¶ 50,307

Humor: Internal Rev Manual is not a citable source (Really!)

MACE © 2015 A.P.Curatola

35

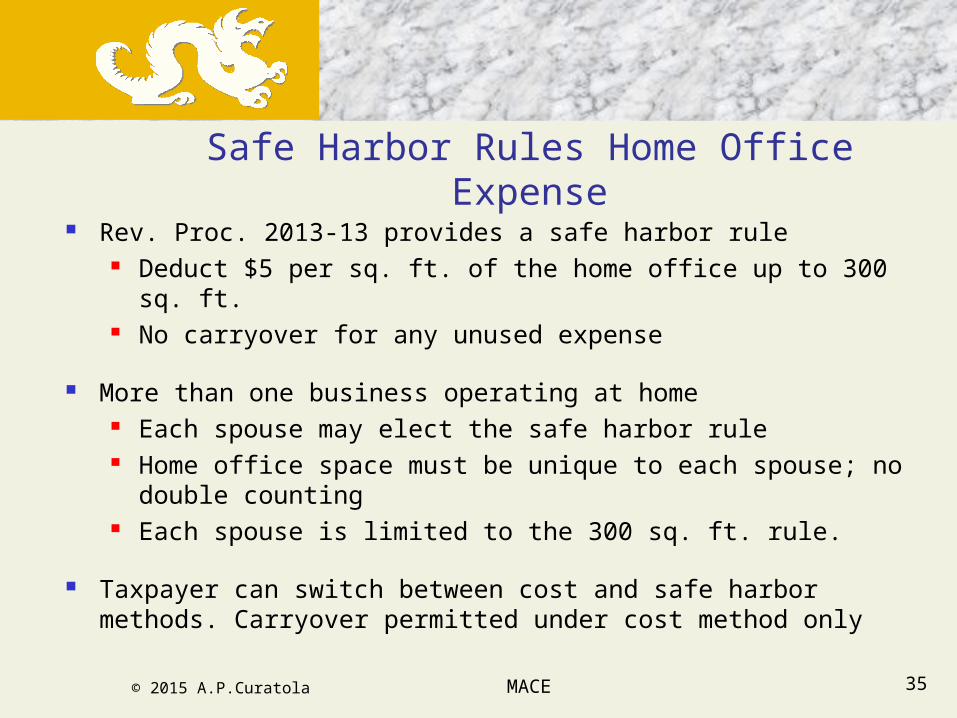

Safe Harbor Rules Home Office Expense

Rev. Proc. 2013-13 provides a safe harbor rule Deduct $5 per sq. ft. of the home office up to 300 sq. ft. No carryover for any unused expense

More than one business operating at home Each spouse may elect the safe harbor rule Home office space must be unique to each spouse; no double

counting Each spouse is limited to the 300 sq. ft. rule.

Taxpayer can switch between cost and safe harbor methods. Carryover permitted under cost method only

MACE © 2015 A.P.Curatola

36

Estimated Tax Payments

Chambers & Curatola (2012) show less underpayment penalties incurred when taxpayers pay monthly instead of quarterly

How do you pay monthly? Really!

MACE © 2015 A.P.Curatola

37

Non-Away-From-Home Lodging

TD 9696 (09/30/2014), Reg. §1.262-1

Tax free working condition fringe benefit if all facts & circumstances tests are passed:

1. Lodging is necessary to participate fully in or be available for a bona fide business meeting, training, conference, etc.

2. Lodging is for a period not to exceed 5 days in any given quarter,

3. Employer requires employee to remain at the activity or function overnight,

4. Lodging is not lavish or extravagant & doesn’t provide any significant element of personal pleasure, recreation, or benefit.

MACE © 2015 A.P.Curatola

38

Home Office Ruling (Odd Result)

Miller (TC Summary Opinion 2014-74) Taxpayer has a studio apartment (NY) that is split into 3 pieces:

Personal (entryway, bathroom & kitchen area), Office space (desk, shelving units, bookcase and sofa), and Bedroom area

Taxpayer meets with clients & performs work for company (CA) in the office space

Office space is occasionally used for personal use.

MACE © 2015 A.P.Curatola

39

Home Office Ruling

Court Decision states, in part that this evidence persuaded it that the Taxpayer's apartment was her principal place of business, that she was obliged to use the space as an office for the convenience and benefit of her employer, and that the employer (BIW) was not able or willing to reimburse her for any of her apartment-related expenses. Although the Taxpayer admitted that she used portions of the office space for nonbusiness purposes, the Court found that her personal use of the space was de minimis and wholly attributable to the practicalities of living in a studio apartment of modest dimensions. It therefore allowed her to deduct one-third of her rent and cleaning service charges for the year.

Court Decision: Non business use was de minimis

MACE © 2015 A.P.Curatola

40

Innocent Spouse

Notice 2012-8 – Equitable Relief under IRC Sec. 6015(f) Satisfy 3 safe harbor factors

OR

Satisfy 8 factor balancing test

De novo standard and scope of review to the Tax Court granted Wilson (9th cir. , 111 AFTR 2d 2013-522) and Neal (11th cir., 103

AFTR 2d 2009-8) The de novo scope of review provides the petitioner the ability to

introduce new evidence.

MACE © 2015 A.P.Curatola

41

1 Year IRA Rollover Rule

Pre 2015 Rule 1 Rollover per IRA per 365 days IRS Publication 590 (2013)

Bobrow Case (TC Memo 2014-21) 1 Rollover per Taxpayer per 365 days Service did not appeal case

Post 2014 IRS will follow Bobrow ruling (Announcement 2014-15)

MACE © 2015 A.P.Curatola

42

1 Year IRA Rollover Rule

Impact of Rule

Applies to SEPs and SIMPLEs IRA based plans IRA rules are unique for RMD rules

Does not apply to other types of Retirement Plans Generally, these are separate plans (see RMD rules)

MACE © 2015 A.P.Curatola

43

Rollover from designated Roth

Prop Reg (REG-105739-11) and Notice 2014-54

Allocation of after-tax amounts applicable to pre-January 1, 2015 distributions (or Sept 18, 2014 if chosen by taxpayer)

Pre 2015 distributions follow Sec. 72 allocation rule for pre & post contributions.

Direction of multiple destinations of distributions is discretion of taxpayer

MACE © 2015 A.P.Curatola

44

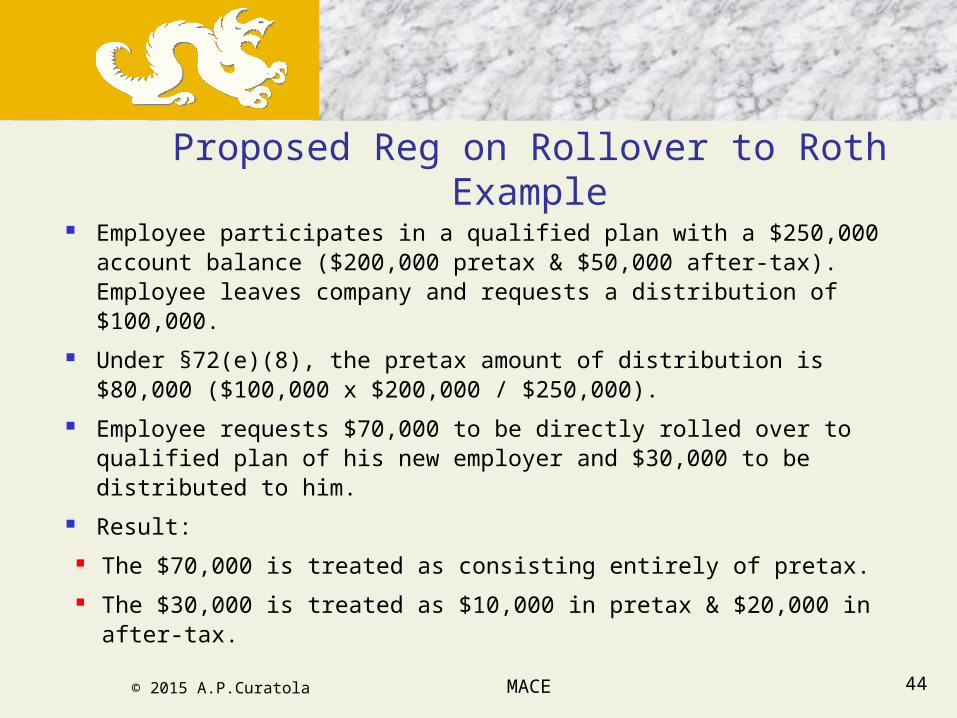

Proposed Reg on Rollover to Roth Example

Employee participates in a qualified plan with a $250,000 account balance ($200,000 pretax & $50,000 after-tax). Employee leaves company and requests a distribution of $100,000.

Under §72(e)(8), the pretax amount of distribution is $80,000 ($100,000 x $200,000 / $250,000).

Employee requests $70,000 to be directly rolled over to qualified plan of his new employer and $30,000 to be distributed to him.

Result:

The $70,000 is treated as consisting entirely of pretax.

The $30,000 is treated as $10,000 in pretax & $20,000 in after-tax.

MACE © 2015 A.P.Curatola

45

Proposed Reg on Rollover to Roth Example (continued)

Employee participates in a designated Roth IRA plan with a $250,000 account balance ($200,000 pretax & $50,000 after-tax). Employee leaves company and requests a distribution of $100,000.

Under §72(e)(8), the pretax amount of distribution is $80,000 ($100,000 x $200,000 / $250,000).

Employee requests $82,000 to be directly rolled over to qualified plan of his new employer and $18,000 to be distributed to him.

Result assuming new plan separately accounts for after-tax contrib.:

The $82,000 is treated as consisting of $80,000 in pretax & $2,000 in after-tax.

The $18,000 is treated as consisting of $18,000 in after-tax.

MACE © 2015 A.P.Curatola

46

myRA

New Government Backed Retirement Plan

President Obama signs presidential memo (1/29/2014)

Treasury directed to create the myRA

Same properties of Roth IRA

MACE © 2015 A.P.Curatola

47

myRA

Targeted for millions of low- & middle-income wage-earners without access to an employer-sponsored plan

myRA Open for as little as $25, and Contribute $5 or more every payday Earn interest at G Fund variable rate (same as 30 year bond rate) Backed by US Treasury

MACE © 2015 A.P.Curatola

48

myRA

Income limits same as Roth IRA

Transfer to the private sector Roth IRA: Anytime, but must be transferred After 30 years or account reaches $15,000

Info available at www.treasury.gov or www.treasurydirect.gov/readysavegrow

MACE © 2015 A.P.Curatola

49

TD 9673 - Qualifying Longevity Annuity Contracts

Modify RMD rules: Purchase of deferred longevity annuity to start at age 80-85

Maximum Annuity Investment is the lesser of: 25% of retirement plan account balance, or $125,000 (was $100,000 under proposed regs)

Issue Raised: 401(k) plan purchase: gender neutral tables used IRA plan purchase: sex-based mortality tables used

MACE © 2015 A.P.Curatola

50

TD 9673 - Qualifying Longevity Annuity Contracts

$125,000 is inflation adjusted at $10,000 increments ($25,000 under proposed regs)

QLAC may contain a return of premium feature that is payable by 12/31 of following year of death.

QLAC cannot consist of variable contract, an equity-indexed contract, or a similar contract.

A failed QLAC due to excess premium limits may return excess premium to non-QLAC portion of employee’s plan by 12/31 of following year.

MACE © 2015 A.P.Curatola

51

Small Business Owners

SEP Plan for 2014: Establish by April 15, 2015 (including extensions) Employer plan contributions due by April 15, 2015 (including

extensions) SIMPLE Plan for 2014:

Establish by October 1, 2014 Employer plan contributions due by April 15, 2015 (including

extensions) Employee plan contributions due by January 30, 2015

Note: Sole proprietor contribution on behalf of themselves as an employee is due by January 1st.

MACE © 2015 A.P.Curatola

52

Installment Sale &Repossessed Residence

DeBough (142 T.C. No. 17, May 19,2014) Issue: Installment Sale, IRC Sec. 121 Exclusion & Repossession

Installment Sale Rules apply to Recognizable Gain

IRC Section 121 exclusion applies to principal residence only

MACE © 2015 A.P.Curatola

53

Installment Sale &Repossessed Residence

Rub: Interplay of Sections 1038 & 121

Non-principal residence: Recognized as long term capital gain any money or property received prior to

reacquisition that was not taxed (i.e., return of property’s adjusted basis)

Principal residence: Recognized as long term capital gain any money or property received prior to

reacquisition that was not taxed (i.e., return of property’s adjusted basis AND any 121 exclusions)

Real Issue: Seller’s basis after reacquisition

MACE © 2015 A.P.Curatola

54

Virtual Currency & Bitcoins

Notice 2014-21: Treat virtual currency (VC) as property, not currency

TX CPA Society requesting IRS guidance because they content that not all VC transactions should be treated as property. Specifically,

Business owners accepting VC in their ordinary course of business should treat the transaction as a currency transaction

Investors should treat VC transactions as property transactions

MACE © 2015 A.P.Curatola

55

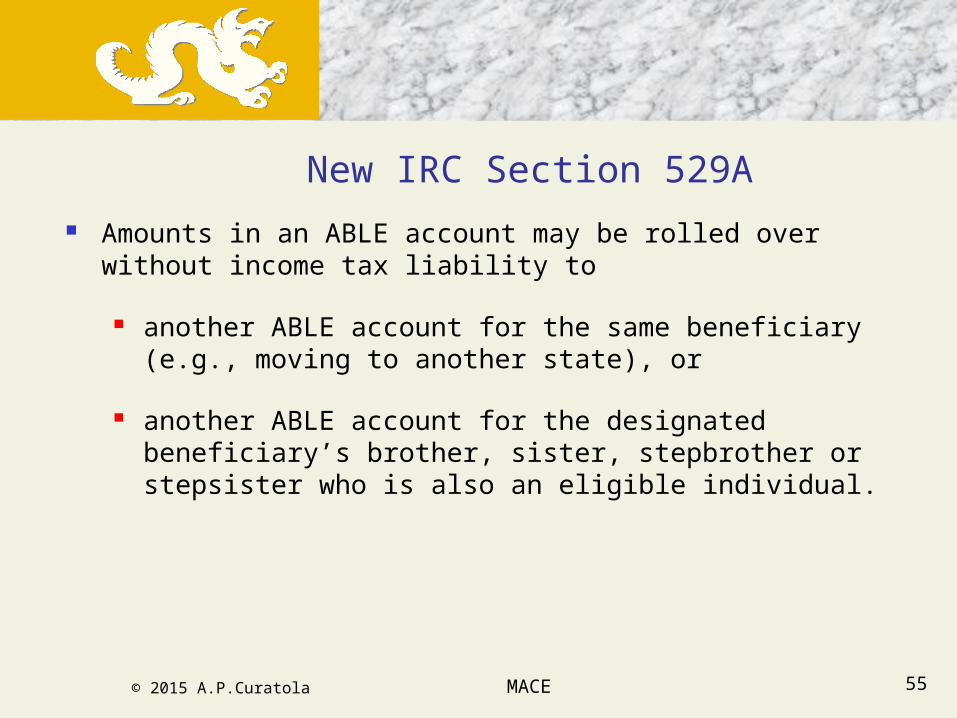

New IRC Section 529A

Amounts in an ABLE account may be rolled over without income tax liability to

another ABLE account for the same beneficiary (e.g., moving to another state), or

another ABLE account for the designated beneficiary’s brother, sister, stepbrother or stepsister who is also an eligible individual.

MACE © 2015 A.P.Curatola

56

Question and Answers

.

MACE © 2015 A.P.Curatola

57

Anthony “Tony” P. Curatola, Ph.D.Joseph F. Ford Professor of Accounting

Drexel University

Tony Curatola is the Joseph F. Ford Professor of Accounting at Drexel University. He holds an MA degree in accounting (1979) from the Wharton Graduate School of the University of Pennsylvania and a Ph.D. degree in accounting (1981) from Texas A&M University. Tony joined the faculty of Drexel University in 1989 by accepting the appointment to the Joseph F. Ford Professor of Accounting Chair.

Tony has been called on to provide information to the House Judiciary Committee concerning the source tax law. He is a regular contributor to numerous journals, such as The Tax Adviser, TAXES, Oil and Gas Tax Quarterly, National Public Accountant, Benefits Quarterly, Tax Executive, Journal of Pension Planning and Compliance, Tax Notes, and State Tax Notes. Tony’s findings have appeared in media such as Forbes, Washington Post, Money Magazine, Wall Street Journal and The New York Times to name a few. He is currently the Editor of the Tax Column for Strategic Finance, Journal of Legal Tax Research, and is an author of several MicroMash Interactive education courses in the employee benefit area and the Enrolled Agent’s Review Course of ExamMatrix.

MACE © 2015 A.P.Curatola