FAO Growth in 2010: Key Opportunities and Challenges

26

Today’s webinar is brought to you by Outsourcing Center Today’s webinar FAO Growth in 2010: Key Opportunities and Challenges Outsourcing Center Synopsis: Everest experts, Katrina Menzigian and Saurabh Gupta, will discuss the status of the FAO market and what buyers and suppliers must do to develop a strategic plan for 2010, including contract, supplier, and market evaluations. About Outsourcing Center Outsourcing Center is the world’s most prominent internet portal for authoritative information on outsourcing. The Center’s mission is to build the industry by helping people understand how to create value through outsourcing We serve the outsourcing community through: outsourcing. We serve the outsourcing community through: Trusted and objective third-party perspective Database of over 81,000 opt-in subscribers Relevant media including editorials, research, whitepapers, and the annual Outsourcing Excellence Awards Proprietary & Confidential. © 2010 Outsourcing Center 1 For more information, contact Peter Bowes at [email protected]

-

date post

20-Oct-2014 -

Category

Business

-

view

800 -

download

2

description

Everest Group experts, Katrina Menzigian and Saurabh Gupta, will discuss the status of the FAO market and what buyers and suppliers must do to develop a strategic plan for 2010, including contract, supplier, and market evaluations.

Transcript of FAO Growth in 2010: Key Opportunities and Challenges

Today’s webinar is brought to you by Outsourcing Center

Today’s webinar

FAO Growth in 2010: Key Opportunities and Challenges

Outsourcing Center

Synopsis:Everest experts, Katrina Menzigian and Saurabh Gupta, will discuss the status of the FAO market and what buyers and suppliers must do to develop a strategic plan for 2010, including contract, supplier, and market evaluations.

About Outsourcing Center

Outsourcing Center is the world’s most prominent internet portal for authoritative information on outsourcing. The Center’s mission is to build the industry by helping people understand how to create value through outsourcing We serve the outsourcing community through:outsourcing. We serve the outsourcing community through:

Trusted and objective third-party perspectiveDatabase of over 81,000 opt-in subscribersRelevant media including editorials, research, whitepapers, and the annual Outsourcing Excellence Awards

Proprietary & Confidential. © 2010 Outsourcing Center1

For more information, contact Peter Bowes at [email protected]

Q&A

To ask a question during the Q&A session

Click the question mark (Q&A) button located on the floating tool bar in the bottom right

Q&A

q ( ) g gof your screen. This will open the Q&A Panel

Be sure to keep the default set to “send to a Panelist”

Then, type your question in the rectangular field at the bottom of the Q&A box and click the send button to submit

Proprietary & Confidential. © 2010 Outsourcing Center2

IntroductionIntroduction

Katrina MenzigianVP-Research

Everest Group

Saurabh GuptaResearch Director

Everest [email protected]

Proprietary & Confidential. © 2010 Outsourcing Center3

FAO Growth in 2010: Key Opportunities and Challenges

April 6, 2010

Agenda

FAO definition and research methodology

Market size, growth, and buyer adoption

Evolution of contract characteristics

Supplier landscape

Outlook for 2010

Copyright © 2010, Everest Global, Inc. 5

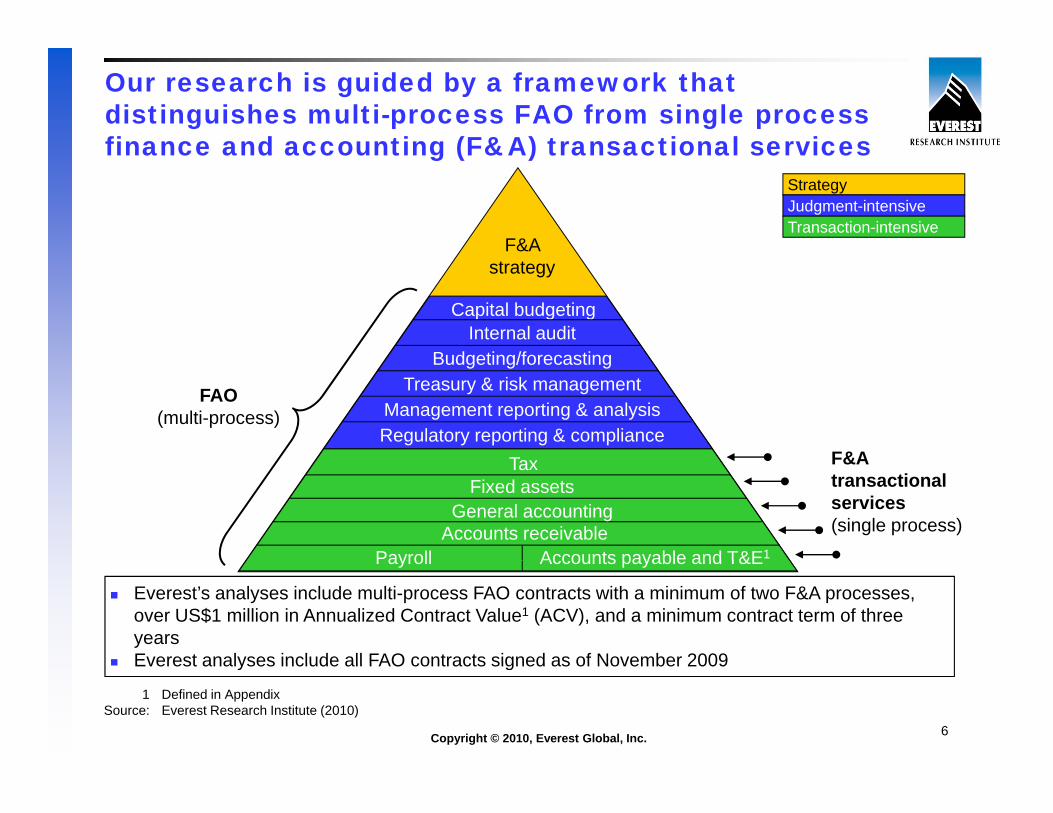

Our research is guided by a framework that distinguishes multi-process FAO from single process finance and accounting (F&A) transactional servicesfinance and accounting (F&A) transactional services

StrategyJudgment-intensiveTransaction-intensive

F&A strategy

Internal auditBudgeting/forecasting

Capital budgeting

FAO(multi-process)

F&A

Budgeting/forecastingTreasury & risk management

TRegulatory reporting & complianceManagement reporting & analysis

F&A transactional services(single process)Accounts receivable

TaxFixed assets

Payroll Accounts payable and T&E1

General accounting

Payroll Accounts payable and T&E

Everest’s analyses include multi-process FAO contracts with a minimum of two F&A processes, over US$1 million in Annualized Contract Value1 (ACV), and a minimum contract term of three yearsEverest analyses include all FAO contracts signed as of November 2009

Copyright © 2010, Everest Global, Inc. 6

Everest analyses include all FAO contracts signed as of November 2009

1 Defined in AppendixSource: Everest Research Institute (2010)

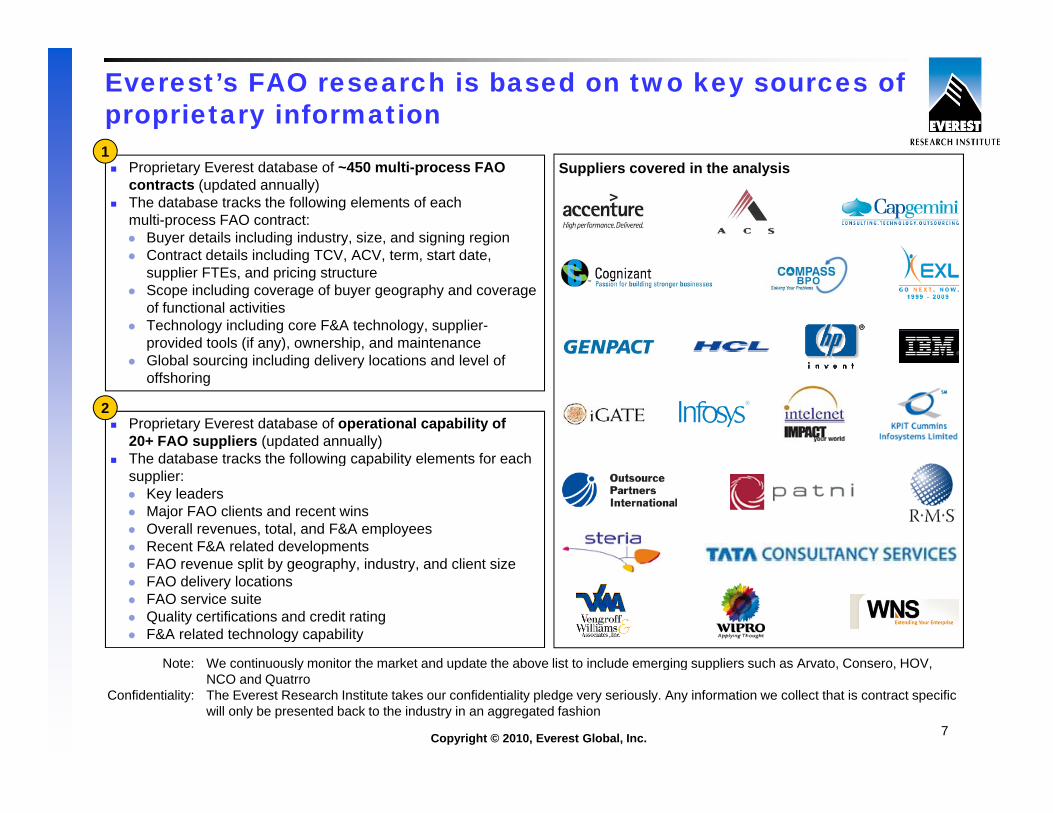

Everest’s FAO research is based on two key sources of proprietary information1

Proprietary Everest database of ~450 multi-process FAO contracts (updated annually)The database tracks the following elements of each multi-process FAO contract:

Buyer details including industry, size, and signing regionContract details including TCV ACV term start date

1Suppliers covered in the analysis

Contract details including TCV, ACV, term, start date, supplier FTEs, and pricing structureScope including coverage of buyer geography and coverage of functional activitiesTechnology including core F&A technology, supplier-provided tools (if any), ownership, and maintenanceGl b l i i l di d li l ti d l l fGlobal sourcing including delivery locations and level of offshoring

Proprietary Everest database of operational capability of 20+ FAO suppliers (updated annually)The database tracks the following capability elements for each

2

The database tracks the following capability elements for each supplier:

Key leadersMajor FAO clients and recent wins Overall revenues, total, and F&A employeesRecent F&A related developmentsFAO lit b h i d t d li t iFAO revenue split by geography, industry, and client sizeFAO delivery locationsFAO service suiteQuality certifications and credit rating F&A related technology capability

Note: We continuously monitor the market and update the above list to include emerging suppliers such as Arvato Consero HOV

Copyright © 2010, Everest Global, Inc. 7

Note: We continuously monitor the market and update the above list to include emerging suppliers such as Arvato, Consero, HOV, NCO and Quatrro

Confidentiality: The Everest Research Institute takes our confidentiality pledge very seriously. Any information we collect that is contract specific will only be presented back to the industry in an aggregated fashion

Agenda

FAO definition and research methodology

Market size, growth, and buyer adoption

Evolution of contract characteristics

Supplier landscape

Outlook for 2010

Copyright © 2010, Everest Global, Inc. 8

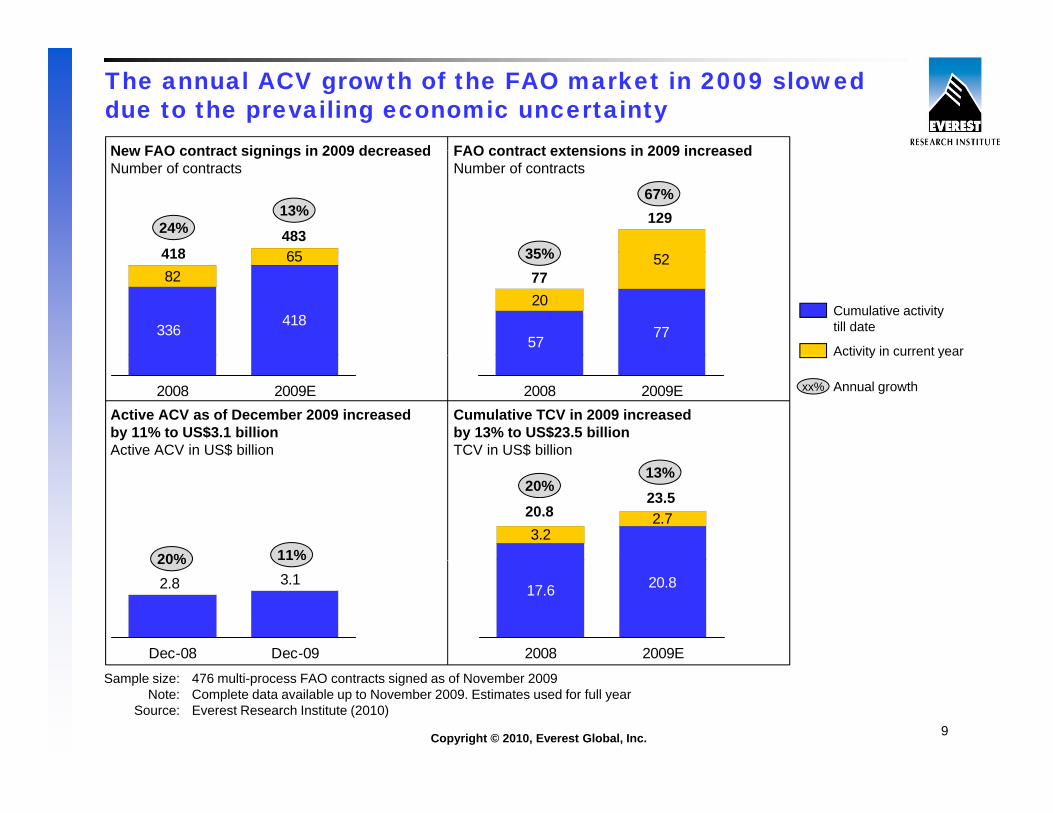

The annual ACV growth of the FAO market in 2009 slowed due to the prevailing economic uncertaintyNew FAO contract signings in 2009 decreased FAO contract extensions in 2009 increased

65

24%

New FAO contract signings in 2009 decreasedNumber of contracts

418483

13% 129

35%

67%

FAO contract extensions in 2009 increasedNumber of contracts

418

8265

336

418

77

20

52

57

7735%

Activity in current year

Cumulative activity till date

2008 2009EActive ACV as of December 2009 increased by 11% to US$3.1 billionActive ACV in US$ billion

2008 2009ECumulative TCV in 2009 increased by 13% to US$23.5 billion TCV in US$ billion

Activity in current year

xx% Annual growth

3.22.720.8

23.520%

13%

20% 11%3.12.8

Dec-08 Dec-09

17.6 20.8

2008 2009E

20%

Copyright © 2010, Everest Global, Inc. 9

Sample size: 476 multi-process FAO contracts signed as of November 2009Note: Complete data available up to November 2009. Estimates used for full year

Source: Everest Research Institute (2010)

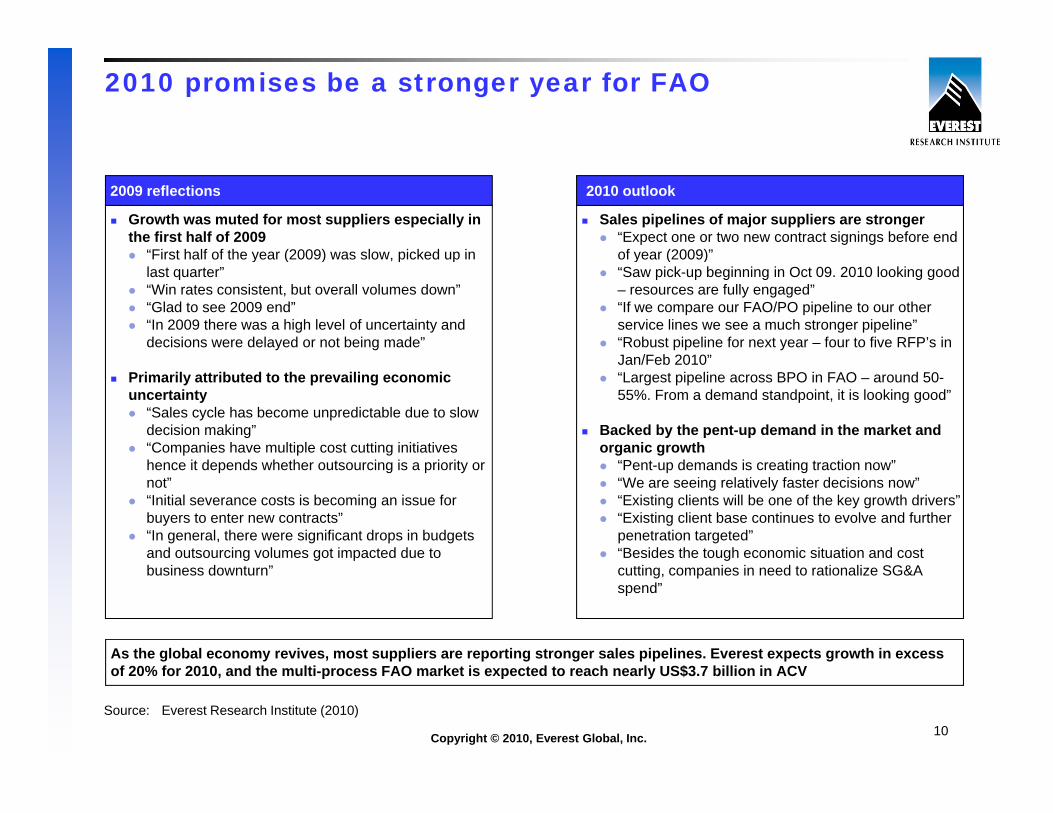

2010 promises be a stronger year for FAO

Growth was muted for most suppliers especially in the first half of 2009

“First half of the year (2009) was slow picked up in

2009 reflections

Sales pipelines of major suppliers are stronger“Expect one or two new contract signings before end of year (2009)”

2010 outlook

First half of the year (2009) was slow, picked up in last quarter”“Win rates consistent, but overall volumes down”“Glad to see 2009 end”“In 2009 there was a high level of uncertainty and decisions were delayed or not being made”

of year (2009)“Saw pick-up beginning in Oct 09. 2010 looking good – resources are fully engaged”“If we compare our FAO/PO pipeline to our other service lines we see a much stronger pipeline” “Robust pipeline for next year – four to five RFP’s in J /F b 2010”

Primarily attributed to the prevailing economic uncertainty

“Sales cycle has become unpredictable due to slow decision making”“Companies have multiple cost cutting initiatives

Jan/Feb 2010”“Largest pipeline across BPO in FAO – around 50-55%. From a demand standpoint, it is looking good”

Backed by the pent-up demand in the market and organic growth

hence it depends whether outsourcing is a priority or not”“Initial severance costs is becoming an issue for buyers to enter new contracts”“In general, there were significant drops in budgets and outsourcing volumes got impacted due to

“Pent-up demands is creating traction now”“We are seeing relatively faster decisions now”“Existing clients will be one of the key growth drivers”“Existing client base continues to evolve and further penetration targeted”“Besides the tough economic situation and cost

As the global economy revives, most suppliers are reporting stronger sales pipelines. Everest expects growth in excess

g g pbusiness downturn”

gcutting, companies in need to rationalize SG&A spend”

Copyright © 2010, Everest Global, Inc. 10

of 20% for 2010, and the multi-process FAO market is expected to reach nearly US$3.7 billion in ACV

Source: Everest Research Institute (2010)

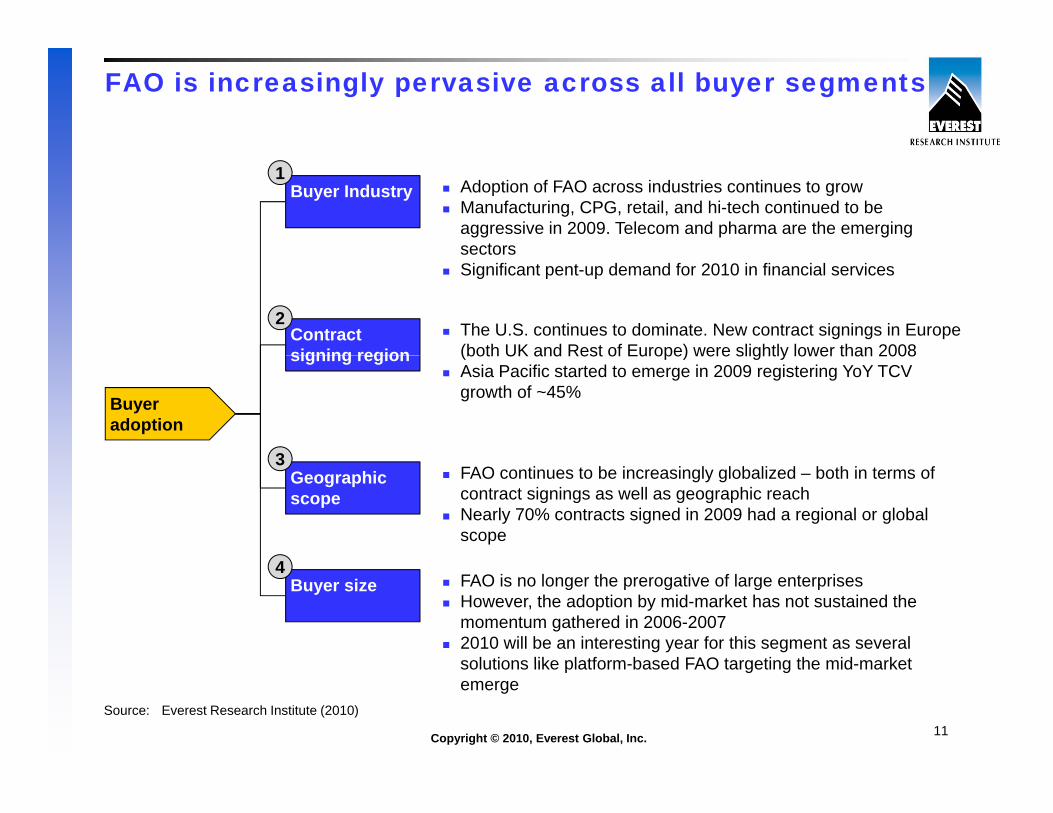

FAO is increasingly pervasive across all buyer segments

Buyer Industry Adoption of FAO across industries continues to growManufacturing, CPG, retail, and hi-tech continued to be aggressive in 2009. Telecom and pharma are the emerging sectors

1

sectorsSignificant pent-up demand for 2010 in financial services

Contract signing region

The U.S. continues to dominate. New contract signings in Europe (both UK and Rest of Europe) were slightly lower than 2008

2

Buyer adoption

signing region (both UK and Rest of Europe) were slightly lower than 2008Asia Pacific started to emerge in 2009 registering YoY TCV growth of ~45%

3Geographic scope

FAO continues to be increasingly globalized – both in terms of contract signings as well as geographic reachNearly 70% contracts signed in 2009 had a regional or global scope

3

Buyer size FAO is no longer the prerogative of large enterprisesHowever, the adoption by mid-market has not sustained the momentum gathered in 2006-20072010 will be an interesting year for this segment as several solutions like platform based FAO targeting the mid market

4

Copyright © 2010, Everest Global, Inc. 11Source: Everest Research Institute (2010)

solutions like platform-based FAO targeting the mid-market emerge

Agenda

FAO definition and research methodology

Market size, growth, and buyer adoption

Evolution of contract characteristics

Supplier landscape

Outlook for 2010

Copyright © 2010, Everest Global, Inc. 12

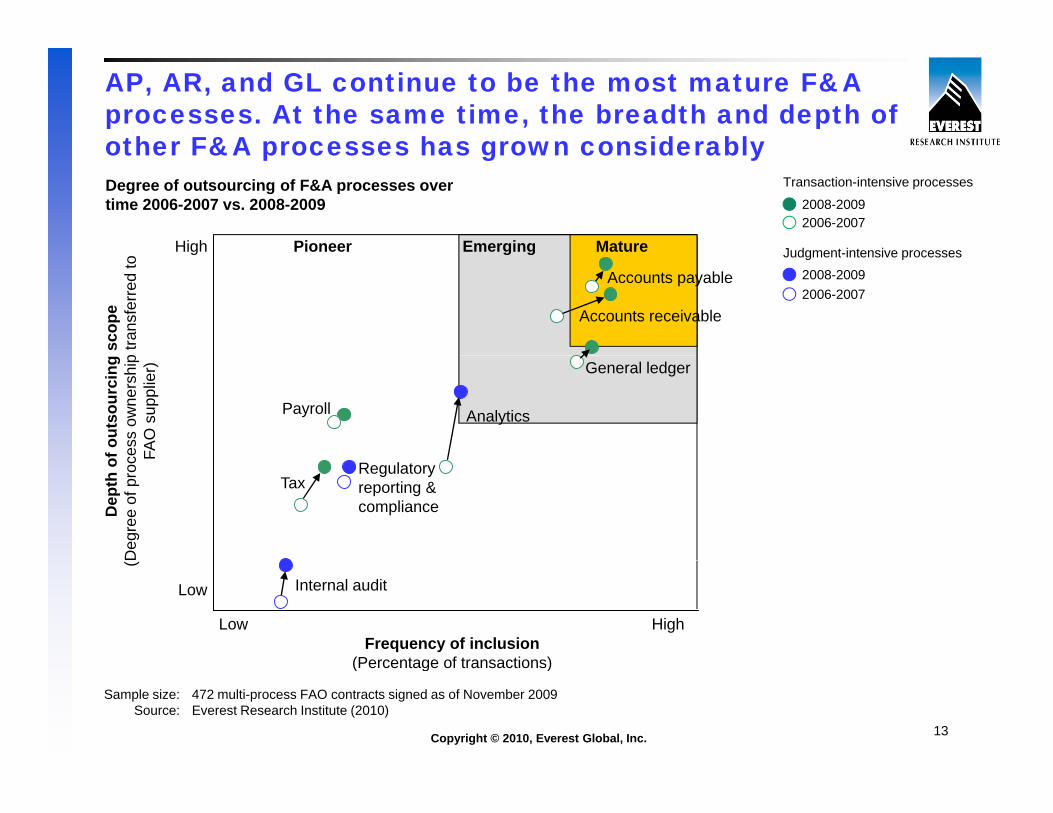

AP, AR, and GL continue to be the most mature F&A processes. At the same time, the breadth and depth of other F&A processes has grown considerablyother F&A processes has grown considerably

High Pioneer MatureEmerging

Transaction-intensive processes

Judgment intensive processes

2008-20092006-2007

Degree of outsourcing of F&A processes over time 2006-2007 vs. 2008-2009

scop

ep

trans

ferr

ed to

g g g

Accounts payable

Accounts receivable

Judgment-intensive processes2008-20092006-2007

f out

sour

cing

ce

ss o

wne

rshi

pFA

O s

uppl

ier)

Payroll

General ledger

Analytics

Dep

th o

Deg

ree

of p

roc F

TaxRegulatory reporting & compliance

(

Low

Frequency of inclusion(Percentage of transactions)

HighLow

Internal audit

Copyright © 2010, Everest Global, Inc. 13

(Percentage of transactions)

Sample size: 472 multi-process FAO contracts signed as of November 2009Source: Everest Research Institute (2010)

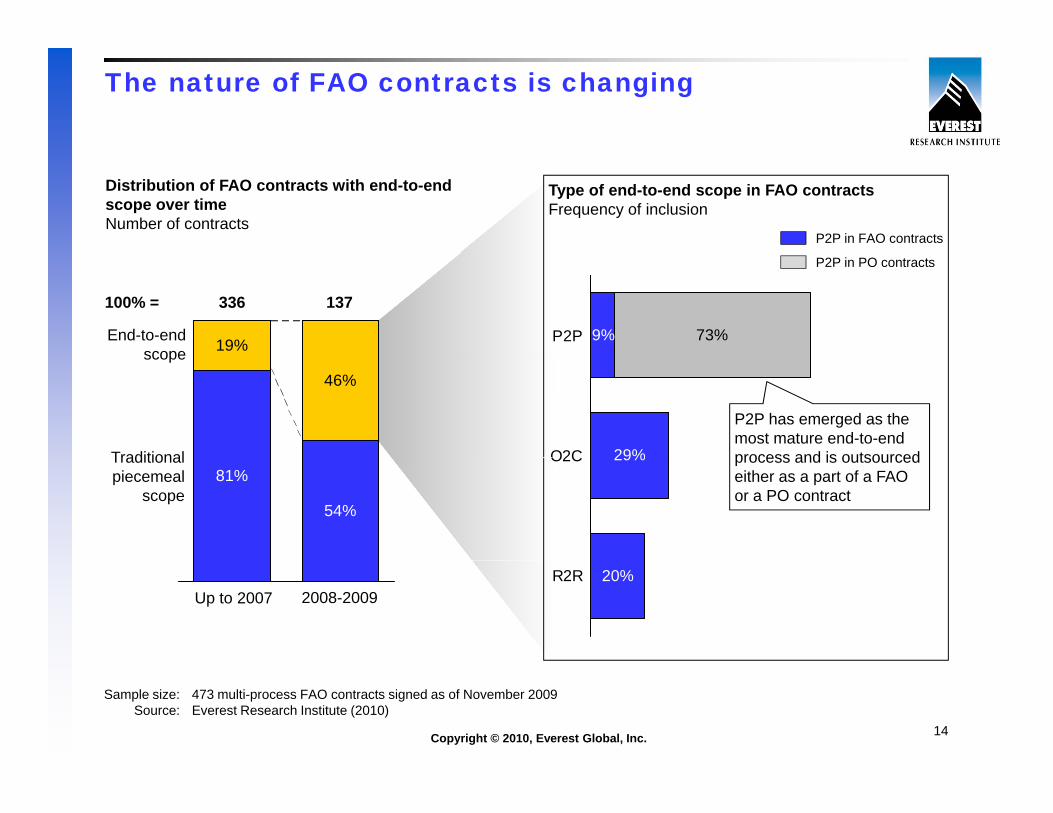

The nature of FAO contracts is changing

Distribution of FAO contracts with end-to-end scope over timeNumber of contracts

Type of end-to-end scope in FAO contractsFrequency of inclusion

P2P in FAO contracts

19%End-to-end scope

100% = 336 137

9% 73%P2P

P2P in PO contracts

46%scope

Traditional 29%O2C

P2P has emerged as the most mature end-to-end process and is outsourced

81%

54%

Traditional piecemeal

scope

29%O2C process and is outsourced either as a part of a FAO or a PO contract

2008-2009Up to 200720%R2R

Copyright © 2010, Everest Global, Inc. 14

Sample size: 473 multi-process FAO contracts signed as of November 2009Source: Everest Research Institute (2010)

The role of technology in FAO has evolved from the basic “tie-and-run” model to an “augmentation” model

Increasing role of technology in FAO

Tie-and-run Technology Core F&A technology Platform-based

Different flavors of technology in FAO and role of supplier

augmentation replacement/ implementation

Pre-integrated applications and pre-built processes owned

FAO

IT infrastructure and/or core F&A application implementation bundled with FAO

Limited role of technology where supplier plugs into the buyer’s existing

Supplier-provided tools that serve as “add-ons” around the periphery of the processes, owned

by supplier, with pricing built into the FAO contract

bundled with FAO services. Technology ownership resides with buyer

the buyer s existing systems to deliver services

the periphery of the existing systems to address specific gaps

F&A outsourcingoutsourcing services

Enabling tools & technologies

Core F&A processing system(s)

Traditional Prevalent

Copyright © 2010, Everest Global, Inc. 15

model model

Source: Everest Research Institute (2010)

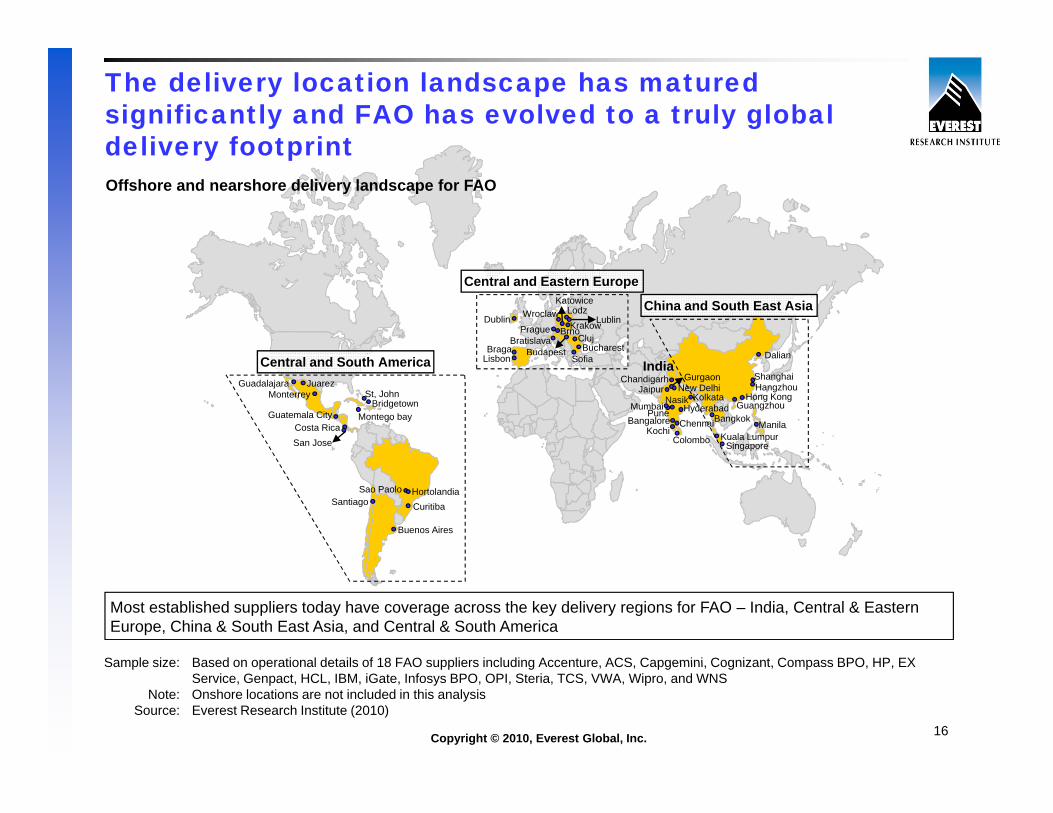

The delivery location landscape has matured significantly and FAO has evolved to a truly global delivery footprintdelivery footprintOffshore and nearshore delivery landscape for FAO

BrnoPrague Krakow

Li bBucharest

Bratislava

Dublin

S fi

WroclawKatowice

LodzLublin

Braga BudapestCluj

Dalian

China and South East Asia

Central and Eastern Europe

Bangalore

Chandigarh

Lisbon

San Jose

Juarez

Sofia

Costa Rica

p

St, John

Guatemala City Montego bay

GuadalajaraMonterrey

MumbaiPune Hyderabad

Kochi

Nasik KolkataNew DelhiJaipur

Gurgaon

Colombo

Dalian

Guangzhou

Shanghai

SingaporeKuala Lumpur

Hong KongHangzhou

BangkokManila

Bridgetown

Chennai

IndiaCentral and South America

Buenos Aires

Curitiba

Sao PaoloSantiago

Hortolandia

Most established suppliers today have coverage across the key delivery regions for FAO – India, Central & Eastern Europe, China & South East Asia, and Central & South America

Sample size: Based on operational details of 18 FAO suppliers including Accenture ACS Capgemini Cognizant Compass BPO HP EX

Copyright © 2010, Everest Global, Inc. 16

Sample size: Based on operational details of 18 FAO suppliers including Accenture, ACS, Capgemini, Cognizant, Compass BPO, HP, EX Service, Genpact, HCL, IBM, iGate, Infosys BPO, OPI, Steria, TCS, VWA, Wipro, and WNS

Note: Onshore locations are not included in this analysisSource: Everest Research Institute (2010)

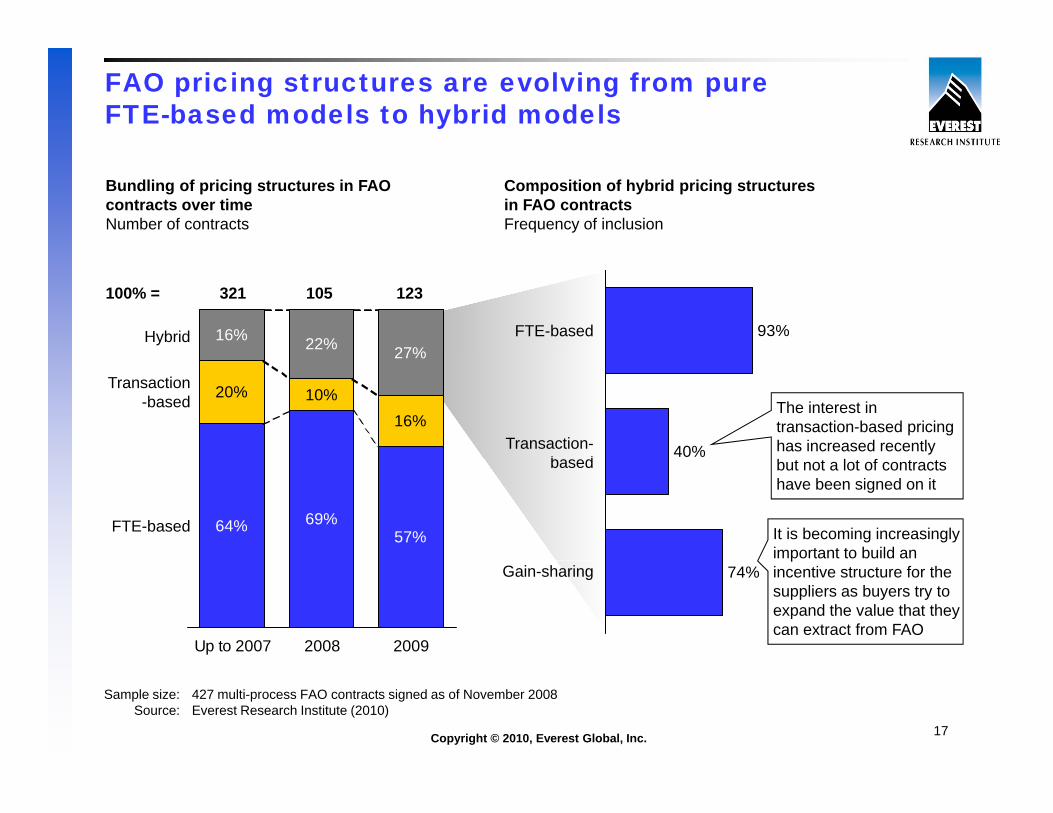

FAO pricing structures are evolving from pure FTE-based models to hybrid models

Bundling of pricing structures in FAO contracts over timeNumber of contracts

Composition of hybrid pricing structures in FAO contractsFrequency of inclusion

100% = 321 123105

16% 22% 27%93%Hybrid FTE-based

20% 10%16%

27%

40%

Transaction-based The interest in

transaction-based pricing has increased recently Transaction-

b d

64% 69%57%

FTE-based

but not a lot of contracts have been signed on it

based

It is becoming increasingly important to build an

Up to 2007 2008 2009

74%p

incentive structure for the suppliers as buyers try to expand the value that they can extract from FAO

Gain-sharing

Copyright © 2010, Everest Global, Inc. 17

Sample size: 427 multi-process FAO contracts signed as of November 2008Source: Everest Research Institute (2010)

Agenda

FAO definition and research methodology

Market size, growth, and buyer adoption

Evolution of contract characteristics

Supplier landscape

Outlook for 2010

Copyright © 2010, Everest Global, Inc. 18

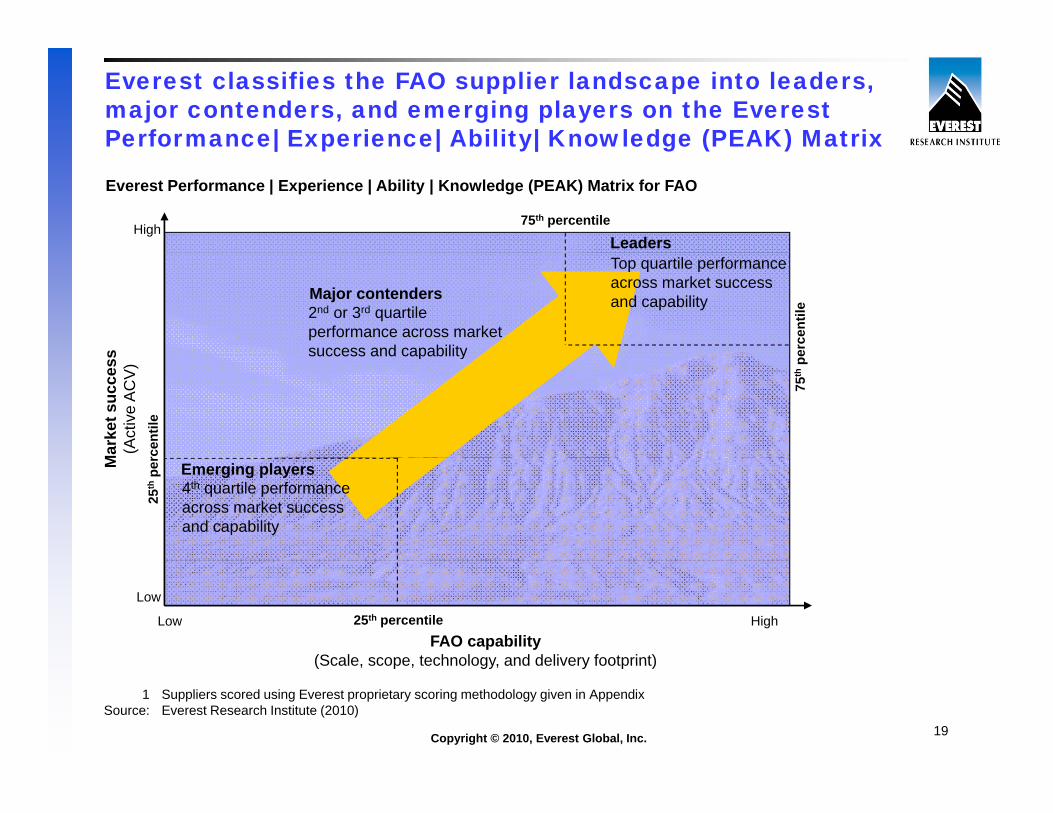

Everest classifies the FAO supplier landscape into leaders, major contenders, and emerging players on the Everest Performance| Experience| Ability| Knowledge (PEAK) Matrix| p | y| g ( )

LeadersHigh

75th percentile

Everest Performance | Experience | Ability | Knowledge (PEAK) Matrix for FAO

s

Major contenders

erce

ntile

Top quartile performance across market success and capability

2nd or 3rd quartile performance across market success and capability

Mar

ket s

ucce

ss(A

ctiv

e A

CV

)

75th

pe

rcen

tile

success and capability

M Emerging players

25th

per

4th quartile performance across market success and capability

FAO capability(Scale scope technology and delivery footprint)

Low

Low High25th percentile

Copyright © 2010, Everest Global, Inc. 19

(Scale, scope, technology, and delivery footprint)

1 Suppliers scored using Everest proprietary scoring methodology given in AppendixSource: Everest Research Institute (2010)

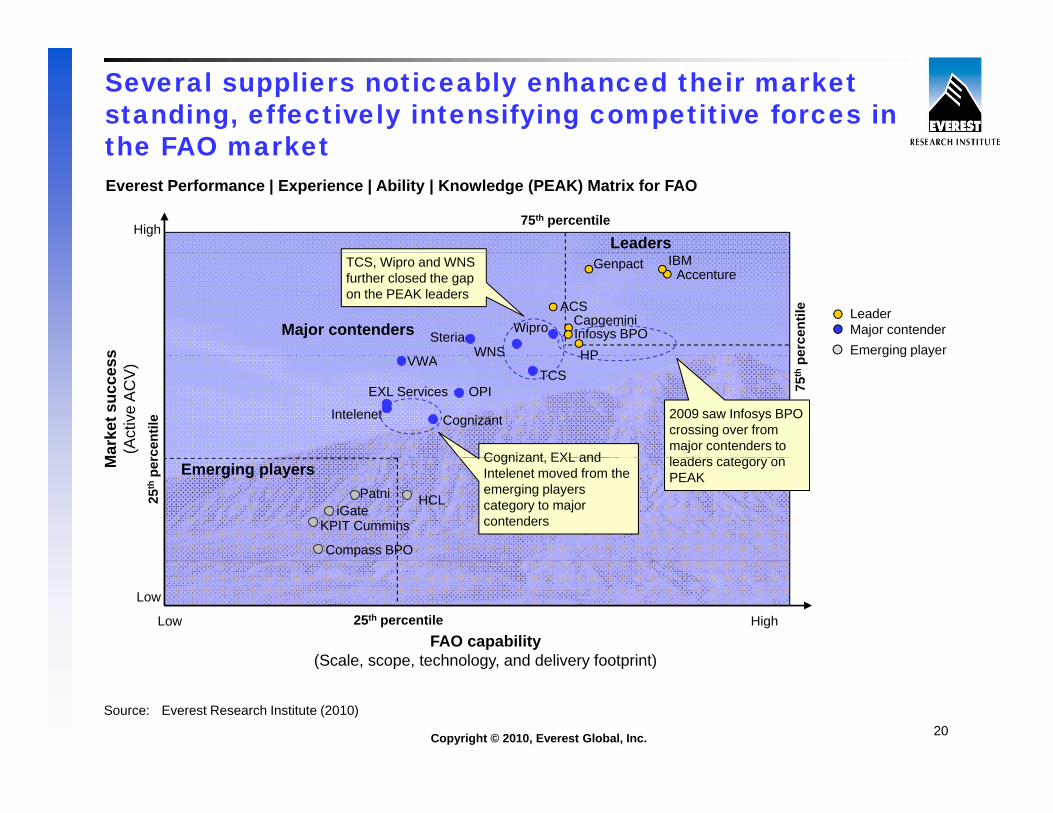

Several suppliers noticeably enhanced their market standing, effectively intensifying competitive forces in the FAO marketthe FAO market

LeadersHigh

Everest Performance | Experience | Ability | Knowledge (PEAK) Matrix for FAO

75th percentile

LeaderMajor contenderEmerging players

AccentureIBMGenpact

SteriaWNS

ACSWipro

HP

CapgeminiInfosys BPOMajor contenders

erce

ntile

TCS, Wipro and WNS further closed the gap on the PEAK leaders

g g p y

Mar

ket s

ucce

ss(A

ctiv

e A

CV

)

Intelenet

EXL Services

VWA

OPI

Cognizant

TCS

WNS HP

Cognizant EXL and

2009 saw Infosys BPO crossing over from major contenders to l d t

75th

pe

rcen

tile

M

Compass BPO

KPIT CumminsiGate

Patni HCL

Emerging playersCognizant, EXL and Intelenet moved from the emerging players category to major contenders

leaders category on PEAK

25th

per

FAO capability(Scale scope technology and delivery footprint)

Low

Low High25th percentile

Copyright © 2010, Everest Global, Inc. 20

(Scale, scope, technology, and delivery footprint)

Source: Everest Research Institute (2010)

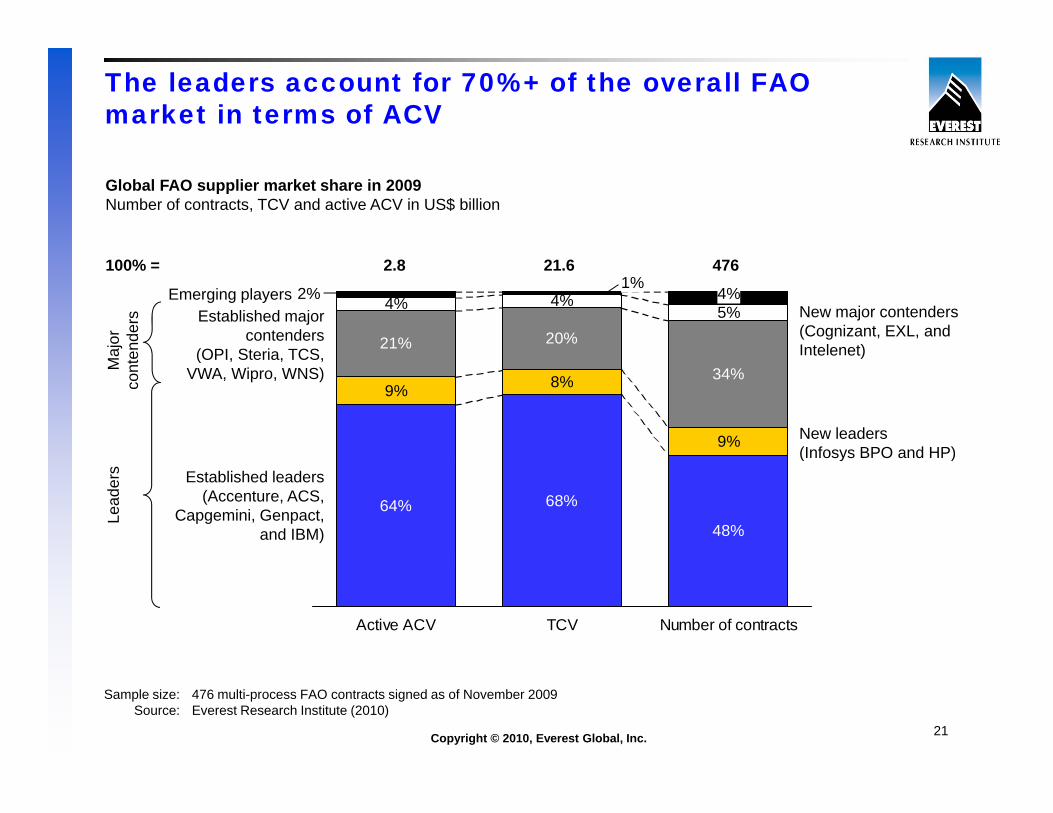

The leaders account for 70%+ of the overall FAO market in terms of ACV

Global FAO supplier market share in 2009Number of contracts, TCV and active ACV in US$ billion

21% 20%

4% 4%5%4%2%

1%100% = 2.8 21.6 476

Emerging players

ajor

en

ders Established major

contenders(OPI Steria TCS

New major contenders (Cognizant, EXL, and Intelenet)

9% 8%

9%

34%Ma

cont

e (OPI, Steria, TCS, VWA, Wipro, WNS)

New leaders(Infosys BPO and HP)

te e et)

64% 68%

48%

Lead

ers Established leaders

(Accenture, ACS, Capgemini, Genpact,

and IBM)

( osys O a d )

Active ACV TCV Number of contracts

Copyright © 2010, Everest Global, Inc. 21

Sample size: 476 multi-process FAO contracts signed as of November 2009Source: Everest Research Institute (2010)

Successful suppliers from all segments were able to fine tune their capability mix to the 2009 market requirementsrequirements

Type of FAO related investments reported in 2008-2009Percentage of events reported

11%Mergers & acquisitions

11%

18%

Partnerships & alliances

11%13%

9%

4%

15%Internal

investments 9% 7%

Technology-related Process/operationalexcellence related

Captive/provideracquisition

Delivery footprintexpansion

Internalreorganization

investments

Copyright © 2010, Everest Global, Inc. 22

Sample size: Operational details of FAO suppliersSource: Everest Research Institute (2010)

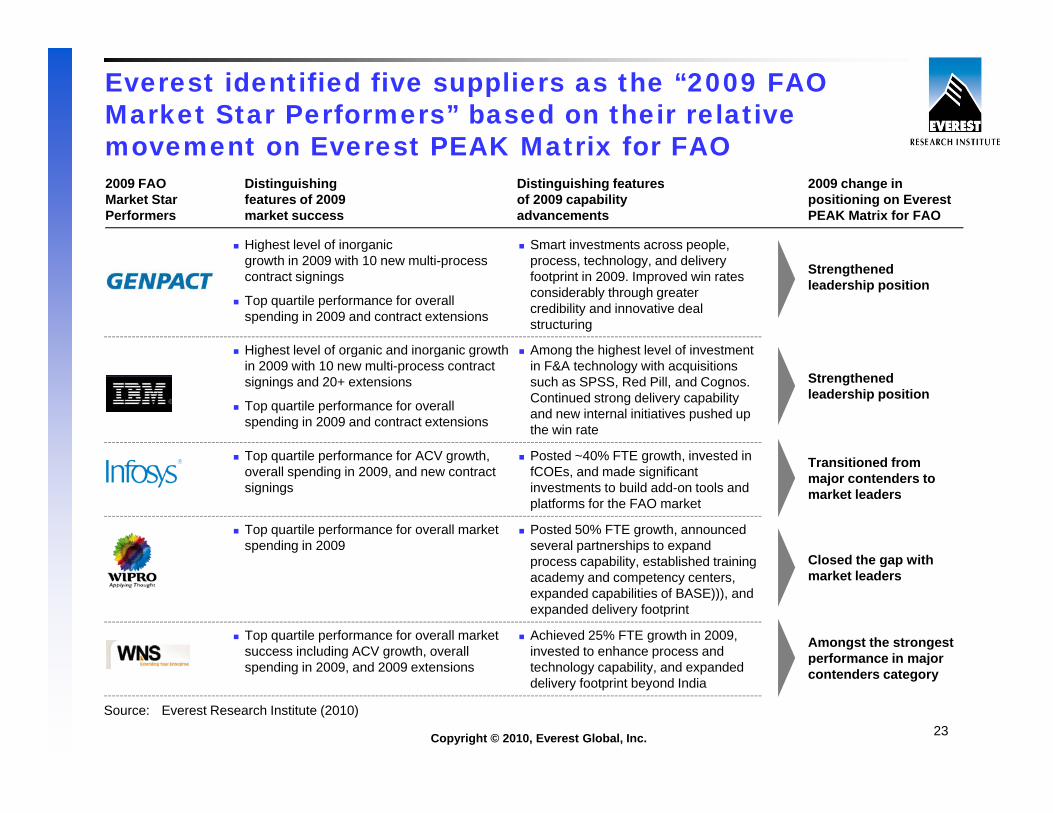

Everest identified five suppliers as the “2009 FAO Market Star Performers” based on their relative movement on Everest PEAK Matrix for FAOmovement on Everest PEAK Matrix for FAO

Highest level of inorganic Smart investments across people,

2009 change in positioning on Everest PEAK Matrix for FAO

Distinguishing features of 2009 capability advancements

Distinguishing features of 2009 market success

2009 FAO Market Star Performers

growth in 2009 with 10 new multi-process contract signings

Top quartile performance for overall spending in 2009 and contract extensions

process, technology, and delivery footprint in 2009. Improved win rates considerably through greater credibility and innovative deal structuring

Highest level of organic and inorganic growth Among the highest level of investment

Strengthened leadership position

g g g gin 2009 with 10 new multi-process contract signings and 20+ extensions

Top quartile performance for overall spending in 2009 and contract extensions

g gin F&A technology with acquisitions such as SPSS, Red Pill, and Cognos. Continued strong delivery capability and new internal initiatives pushed up the win rate

Top quartile performance for ACV growth Posted ~40% FTE growth invested in

Strengthened leadership position

T iti d fTop quartile performance for ACV growth, overall spending in 2009, and new contract signings

Posted 40% FTE growth, invested in fCOEs, and made significant investments to build add-on tools and platforms for the FAO market

Top quartile performance for overall market spending in 2009

Posted 50% FTE growth, announced several partnerships to expand process capability established training

Transitioned from major contenders to market leaders

Closed the gap withprocess capability, established training academy and competency centers, expanded capabilities of BASE))), and expanded delivery footprint

Top quartile performance for overall market success including ACV growth, overall

di i 2009 d 2009 t i

Achieved 25% FTE growth in 2009, invested to enhance process and t h l bilit d d d

Closed the gap with market leaders

Amongst the strongest performance in major

Copyright © 2010, Everest Global, Inc. 23

spending in 2009, and 2009 extensions technology capability, and expanded delivery footprint beyond India

p jcontenders category

Source: Everest Research Institute (2010)

Agenda

FAO definition and research methodology

Market size, growth, and buyer adoption

Evolution of contract characteristics

Supplier landscape

Outlook for 2010

Copyright © 2010, Everest Global, Inc. 24

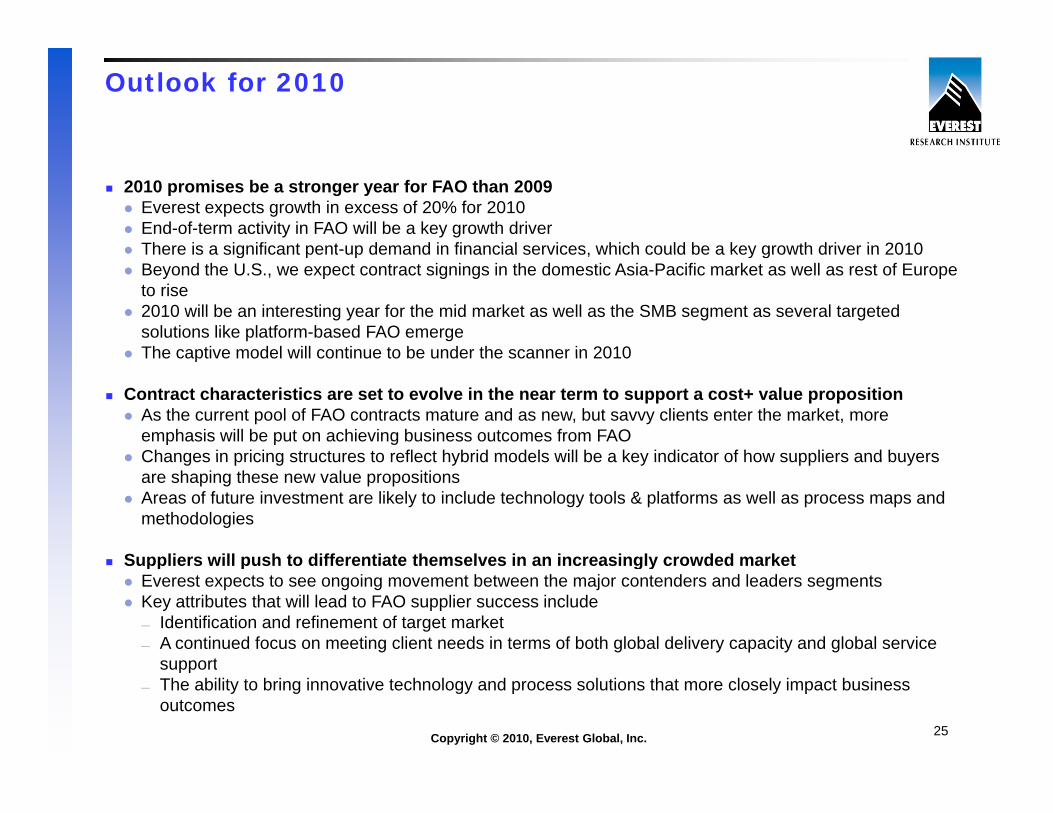

Outlook for 2010

2010 promises be a stronger year for FAO than 2009Everest expects growth in excess of 20% for 2010End-of-term activity in FAO will be a key growth driverThere is a significant pent-up demand in financial services, which could be a key growth driver in 2010There is a significant pent up demand in financial services, which could be a key growth driver in 2010Beyond the U.S., we expect contract signings in the domestic Asia-Pacific market as well as rest of Europe to rise2010 will be an interesting year for the mid market as well as the SMB segment as several targeted solutions like platform-based FAO emergeThe captive model will continue to be under the scanner in 2010The captive model will continue to be under the scanner in 2010

Contract characteristics are set to evolve in the near term to support a cost+ value propositionAs the current pool of FAO contracts mature and as new, but savvy clients enter the market, more emphasis will be put on achieving business outcomes from FAO Changes in pricing structures to reflect hybrid models will be a key indicator of how suppliers and buyersChanges in pricing structures to reflect hybrid models will be a key indicator of how suppliers and buyers are shaping these new value propositionsAreas of future investment are likely to include technology tools & platforms as well as process maps and methodologies

Suppliers will push to differentiate themselves in an increasingly crowded marketSuppliers will push to differentiate themselves in an increasingly crowded marketEverest expects to see ongoing movement between the major contenders and leaders segments Key attributes that will lead to FAO supplier success include — Identification and refinement of target market— A continued focus on meeting client needs in terms of both global delivery capacity and global service

support

Copyright © 2010, Everest Global, Inc. 25

support— The ability to bring innovative technology and process solutions that more closely impact business

outcomes

Q&A

Attendees will receive an email with a link to download today’s webinar presentation. To access a recorded audio version of this webinar, please contact Mark Williamson, [email protected]

Q&A

For advice or research on FAO, please contact Everest:Katrina Menzigian, [email protected] Gupta, [email protected]

For background information on Everest, please visit:www.everestgrp.comwww.everestresearchinstitute.com

Thank you for attending todayThank you for attending today

To ask a question during the Q&A session

Cli k th ti k (Q&A) b tt l t d th fl ti t l b i th b tt i ht fClick the question mark (Q&A) button located on the floating tool bar in the bottom right of your screen. This will open the Q&A Panel

Be sure to keep the default set to “send to a Panelist”

Proprietary & Confidential. © 2010 Outsourcing Center26

Then, type your question in the rectangular field at the bottom of the Q&A box and click the send button to submit