F1–What Are We Hedging Anyway? GAAP, Stat, or Economics? - Member | SOA · – A basket comprised...

20

Investment Symposium March 2010 F1: What Are We Hedging Anyway? GAAP, Stat, or Economics? Ross Bowen James Lloyd Moderator Jay Musselman

Transcript of F1–What Are We Hedging Anyway? GAAP, Stat, or Economics? - Member | SOA · – A basket comprised...

Investment Symposium March 2010

F1: What Are We Hedging Anyway? GAAP, Stat, or Economics?

Ross Bowen James Lloyd

Moderator Jay Musselman

1

F1–What Are We Hedging Anyway? GAAP, Stat, or Economic?, ,

Ross Bowen, Allianz LifeMarch 22, 2010

Hedging VA Risk

Most hedging programs started out hedging GAAP risk

Implementation of C3P2 and AG43 have created a disconnect with GAAP or pure economics

FAS 157 disconnected GAAP and Economic

Multiple constraints and objectives create the need for an interdisciplinary team to approach the problem

2

Economic

Economic measures look for sensitivities to the value of promises mademade

Define the value

Present value of claims less fees

Risk neutral framework

Key sensitivities

Change in market levels

Change in rates

Change in volatilities

Need a robust scenario generator

Match observable prices and greeks

GAAP

Most similar to economic – what are the differences?

Treatment of fees

Some companies set the value of the embedded derivative to zero at issue apply a factor to the fees so PV = 0

Not all VAGLBs are FAS 133

SOP 03-1 applied to GMIB

GMAB clearly FAS 133

GMWB may be a hybrid

Gain on hedges impacts k factor

3

GAAP – FAS 157

FAS 157 Own Credit Risk

Objections – value of promise declines as probability of paying declines

Release reserves when downgraded?

How to determine own credit risk spread?

CDS market offers view into credit risk

Large writers may have active CDS market

To hedge or not to hedge?

Sell CDS on self? Sell CDS on similar writers?

What is the goal of hedging?

Statutory

Moving from a factor based world to a Principles Based world

AG33 – Base Contract

AG34 - DB

AG39 – Living Benefits, accumulation of fees

There was a need to modernize AG39

C3P2 came first, then AG43 / VACARVM

Real world stochastic

Model hedges in a stochastic on stochastic framework

Standard scenario – comparable values between companies

4

AG43 Hedge Modeling - Stochastic

Stochastic scenarios

CTE70 – worst 30%

Possibility that hedges will cost rather than benefit

Existing hedges may be run off

If CDHS in place, may reflect hedging strategy

CTE Reported = E * CTE Best Efforts – (1-E) * CTE Adjusted

E < 70% or < 30% if hedges not directly modeledg y

Basis risk, transaction risk, hedging mismatch tolerance…

C3P2 Hedge Efficiency

Stochastic scenariosCTE90 worst 10% more likely that hedges will benefitCTE90 – worst 10% - more likely that hedges will benefitExisting hedges may be run offIf CDHS in place, may reflect hedging strategyCTE Reported = TAR Best Efforts –E * (TAR adj – TAR best

efforts) AdjustedE >5%Basis risk, transaction risk, hedging mismatch tolerance…

5

Value of Hedges – AG43 SS

PV of pre-tax cashflows at the one-year CMT rate less statement valuevalue

Must be held to hedge these contracts in compliance with state laws

Assume hedges are liquidated in one year or exercised if mature prior

Assume returns underlying SS, Black Scholes pricing, rate of five-year CMT, and solved-for implied volatility

Evaluation of Hedge Instruments

Review the differences between stat, GAAP, and economic

Evaluate hedge performance in the various regimes

Choices

Futures

Puts

Swaps

Swaptionsp

Calls

6

Evaluation of Hedge Instruments Futures

Linear in the market

Can be written on different indices

Very effective on standard scenario

13.5% / 20% of notional

Unlimited losses possible in up market

Evaluation of Hedge Instruments Futures

Futures Performance in AG43

(30 000 000)(20,000,000)(10,000,000)

-10,000,00020,000,00030,000,00040,000,00050,000,000

700 800 900 1000 1100 1200 1300Gai

n / L

oss

mkt gainHedge CreditCapital Impact

(40,000,000)(30,000,000)

S&P Level

7

Evaluation of Hedge Instruments Puts

Provide delta protection in Statutory world

Vega and rho protection in Economic world

Can be very expensive

Out of the money attractive (crash protection)

Sell a deeper OTM to offset cost

Can also fund by selling upside

OTM call

Sell deeper OTM call to limit losses

Puts – “Zero Cost” CollarEconomic payoff

Payoff profile

100

200

300

-300

-200

-100

0400 500 600 700 800 900 1000 1100 1200 1300 1400

8

“Zero Cost” Collar - Impact

Change in value of options as time passes and market levels changechange

Hedge Value

3 04.05.06.07.08.09.010.0

$mill

ions

Hedge Value

0.01.02.03.0

1300120011001000900800700600

S&P Level

“Zero Cost” Collar - Impact

Additional value of hedge credit under AG43 standard scenario

Hedge Value plus Hedge Credit

2 0

4.0

6.0

8.0

10.0

12.0

14.0

$mill

ions Hedge Value

Value After Credit

0.0

2.0

1300120011001000900800700600

S&P Level

9

Principle 5

“The use of …risk management strategies (e.g. hedging)… that serve solely to reduce the calculated TAR are inconsistent withserve solely to reduce the calculated TAR… are inconsistent with these principles.

The use of assumptions and risk management strategies should be appropriate to the business and not merely constructed to exploit ‘foreknowledge’ of the components of the required methodology.”

Summary

Economic, stat, GAAP

All behavior differently under market shocks

Interdisciplinary project

Need input from many financial areas

1

What are we HedgingGAAPSTATEconomics?

Société GénéraleGlobal Markets Cross-Asset Solutions

sg structuredproducts comJ 2009

James Lloyd

FOR QUALIFIED INSTITUTIONAL BUYER ONLY sg-structuredproducts.com

Equity Derivatives House of the Year

June 2009FOR QUALIFIED INSTITUTIONAL BUYER ONLY

This material is confidential and is provided for information purposes only. There is no assurance that a transaction will be entered into on anyindicative terms. SG Americas Securities, LLC (“SGAS”) believes the information in this document is reliable but makes no representation orwarranty as to whether the information is current, accurate or complete. SGAS is under no obligation to update, modify or amend thiscommunication or to otherwise notify you that any matter contained herein has changed or subsequently become inaccurate. SGAS and itsaffiliates expressly disclaim all responsibility for any use of or reliance upon this document. This document is provided solely for informationalpurposes and may not be construed as an offer to buy or sell or a solicitation of an offer to buy or sell any financial instrument or to engage in

Important Information

purposes and may not be construed as an offer to buy or sell, or a solicitation of an offer to buy or sell, any financial instrument or to engage inany particular trading strategy or as an official confirmation of terms. Investors must make their own investment decisions using their ownindependent advisors while considering their own financial situation and investment objectives. SGAS and its affiliates do not act as a financialadviser or as a fiduciary in respect of any transaction unless such entity expressly agrees so in writing. This document may not be relied uponas investment, accounting, legal, regulatory or tax advice or an investment recommendation.

You should refer to the offering document relating to the relevant financial instrument which includes important information, including related riskfactors. Financial instruments of the type described herein may involve a high degree of risk and their value may be highly volatile. Such risksinclude, without limitation, risk of adverse or unanticipated market developments, risk of counterparty or issuer default, risk of adverse eventsinvolving any underlying reference obligation or entity and risk of illiquidity. In some financial instruments, counterparties may lose their entireinvestment or incur an unlimited loss. This brief statement does not disclose all the risks and other significant aspects in connection withtransactions of the type described in the materials. You are urged to consider carefully whether any products discussed herein are appropriatefor you or any of your clients given your or their objectives, experience, financial and operational resources and other relevant circumstances.This document may not be reproduced, distributed or published by any person for any person without the prior written consent of SGAS.

[Thi d i i d d f l i h “Q lifi d P h ” h i d fi d i h I C A f 1940[This document is intended for use only with “Qualified Purchasers”, as such term is defined in the Investment Company Act of 1940, asamended. Use of this document by any other party is prohibited.]

© 2009 Société Générale (“SG”), SGAS and their affiliates. SG CIB is the Corporate and Investment Banking arm of SG. Certain servicesdescribed herein are provided by SGAS, a US registered broker-dealer, member of the NYSE, FINRA and SIPC, and a wholly owned subsidiaryof SG. Services provided outside the US may be provided by affiliates of SGAS.

2

2

Delta Hedging

VA Traditional Hedging Methodologies

Short futures or TRS, adjusted periodically No purchase of implied volatility

More economic in medium/low volatility environment

Significant risks retained

Hedge Volatility has large P&L Impact

Path Dependent P&L3 Greek Dynamic Hedging

Description Benefits

Limitations

Limitations

3- Greek Dynamic HedgingHedge interest rate exposure with futures, rate swaps and swaptions

Purchase 3-15 year put options, Variance Swaps on major indices to hedge vega exposure

Allows to mirror MtM movements of liabilities

Hedge portfolio of vanilla derivatives can be efficiently rebalanced

If listed option used, no counterparty risks

Infrastructure requirements to compute risk, trade and rebalance

Requires a very good communication to investor, analyst and ratings community

Model RiskAdvanced Dynamic Hedging

Use of additional derivatives instruments such as lookback, options on basket, hybrid options, Dividend Swap

Cross Greeks Sensitivity, convexity is hedged

Better hedge extreme event

Requires advanced modeling techniques

Smaller liquidity, transactions costs

Model RiskStructured/Static Hedge

Customized OTC derivative that fully hedges capital Tailored to include guarantee specificities and actuarial assumptions

Calibration of initial modeling requiredmarkets exposure

Possibility to fully incorporate Insurer actuarial assumption

actuarial assumptions

Possibility to do very long term hedge

Hedge of all the liabilities under 1 transaction. No infrastructure needed

Might allow for better Accounting, Capital, .. treatment

Big Counterparty Risk

Actuarial mismatch.

Liquidity, Transactions costs

ReinsuranceFull traditional reinsurance Fully hedge Cost and availability

3

Delta Hedging Case Study

• Objective: attempt to replicate a portfolio of Mutual Funds (equity, bonds and balanced) with two replication baskets:

– A basket comprised by 5 indices (EAFA, SPX, NDX, RTY, LBUSTRRU)– A basket comprised by 11 liquid indices (9 equity and 2 bond indices) plus a basket of CDS

• Academic Research: Semi-Static hedging with options in jumpy markets and stochastic volatility is > 2.5 X more effective than dynamic with underlying (Appendix 1)y y g ( pp )

60%

80%

100%

120%

Back-test Methodology

Quarterly adjustments

Results

a) R2 = 74% C t 40 b

Graph 1.1. Illustration of tracking error reduction with different replication vehicles

0%

20%

40%

Jan-08 Apr-08 Jul-08 Oct-08 Jan-09 Apr-09

Basket of Mutual FundsBasket comprised by 11 indices + Basket of CDSBasket comprised by 5 indices

Cost = 40 bps p.a.

b) R2 = 87%Cost = 90 bps p.a.

*See appendix

Source: SG Analytics. See Appendix for details on the basket components. 4

3

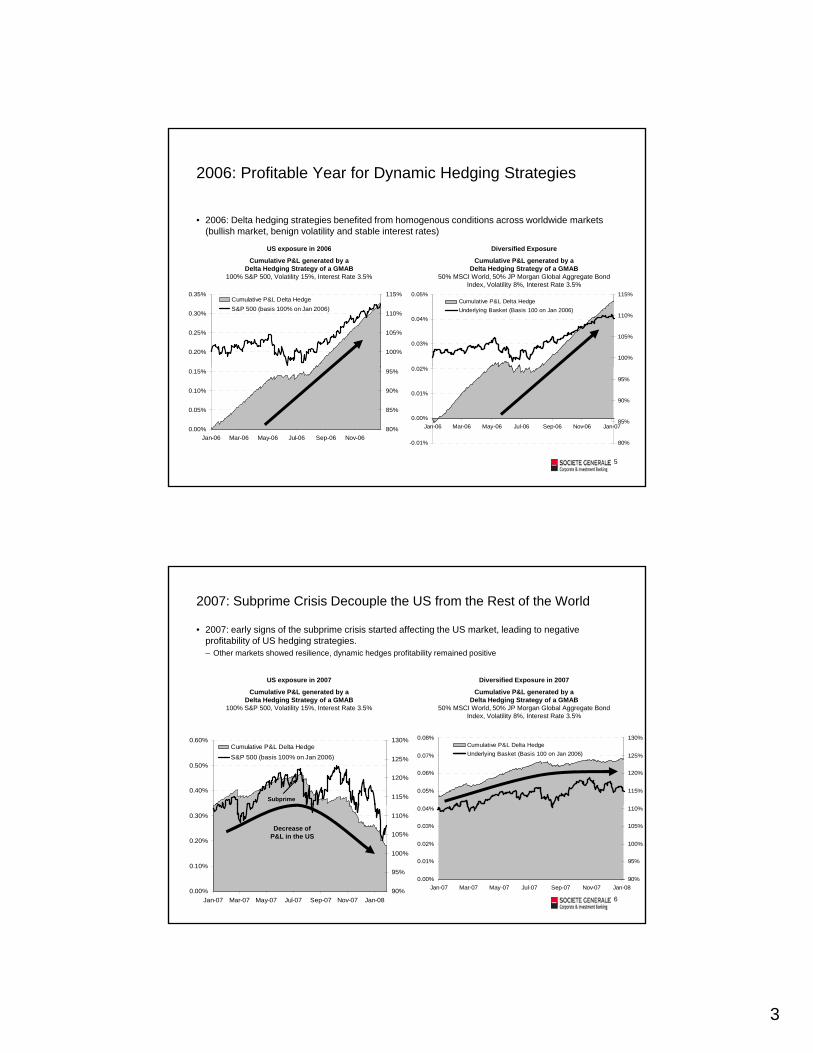

2006: Profitable Year for Dynamic Hedging Strategies

• 2006: Delta hedging strategies benefited from homogenous conditions across worldwide markets (bullish market, benign volatility and stable interest rates)

US exposure in 2006 Diversified Exposure

0 02%

0.03%

0.04%

0.05%

100%

105%

110%

115%Cumulative P&L Delta HedgeUnderlying Basket (Basis 100 on Jan 2006)

US exposure in 2006

Cumulative P&L generated by a Delta Hedging Strategy of a GMAB

100% S&P 500, Volatility 15%, Interest Rate 3.5%

Diversified Exposure

Cumulative P&L generated by a Delta Hedging Strategy of a GMAB

50% MSCI World, 50% JP Morgan Global Aggregate Bond Index, Volatility 8%, Interest Rate 3.5%

0.20%

0.25%

0.30%

0.35%

100%

105%

110%

115%Cumulative P&L Delta HedgeS&P 500 (basis 100% on Jan 2006)

-0.01%

0.00%

0.01%

0.02%

Jan-06 Mar-06 May-06 Jul-06 Sep-06 Nov-06 Jan-07

80%

85%

90%

95%

0.00%

0.05%

0.10%

0.15%

Jan-06 Mar-06 May-06 Jul-06 Sep-06 Nov-0680%

85%

90%

95%

5

2007: Subprime Crisis Decouple the US from the Rest of the World

• 2007: early signs of the subprime crisis started affecting the US market, leading to negative profitability of US hedging strategies. – Other markets showed resilience, dynamic hedges profitability remained positive

US exposure in 2007 Diversified Exposure in 2007

0.05%

0.06%

0.07%

0.08%

115%

120%

125%

130%Cumulative P&L Delta HedgeUnderlying Basket (Basis 100 on Jan 2006)

Cumulative P&L generated by a Delta Hedging Strategy of a GMAB

100% S&P 500, Volatility 15%, Interest Rate 3.5%

Cumulative P&L generated by a Delta Hedging Strategy of a GMAB

50% MSCI World, 50% JP Morgan Global Aggregate Bond Index, Volatility 8%, Interest Rate 3.5%

0.40%

0.50%

0.60%

115%

120%

125%

130%Cumulative P&L Delta HedgeS&P 500 (basis 100% on Jan 2006)

Subprime

0.00%

0.01%

0.02%

0.03%

0.04%

Jan-07 Mar-07 May-07 Jul-07 Sep-07 Nov-07 Jan-0890%

95%

100%

105%

110%

0.00%

0.10%

0.20%

0.30%

Jan-07 Mar-07 May-07 Jul-07 Sep-07 Nov-07 Jan-0890%

95%

100%

105%

110%

Decrease of P&L in the US

6

4

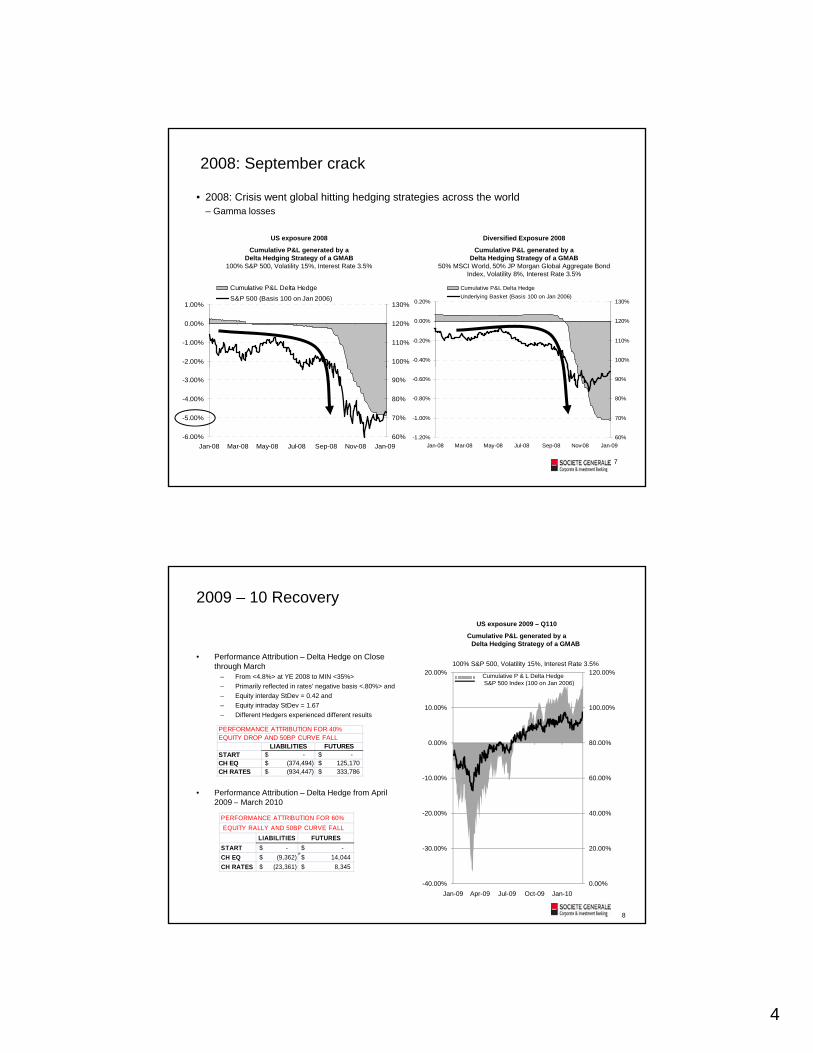

2008: September crack

• 2008: Crisis went global hitting hedging strategies across the world – Gamma losses

US exposure 2008

C l ti P&L t d b

Diversified Exposure 2008

C l ti P&L t d b

-2.00%

-1.00%

0.00%

1.00%

100%

110%

120%

130%

Cumulative P&L Delta HedgeS&P 500 (Basis 100 on Jan 2006)

Cumulative P&L generated by a Delta Hedging Strategy of a GMAB

100% S&P 500, Volatility 15%, Interest Rate 3.5%

Cumulative P&L generated by a Delta Hedging Strategy of a GMAB

50% MSCI World, 50% JP Morgan Global Aggregate Bond Index, Volatility 8%, Interest Rate 3.5%

-0.40%

-0.20%

0.00%

0.20%

100%

110%

120%

130%

Cumulative P&L Delta HedgeUnderlying Basket (Basis 100 on Jan 2006)

-6.00%

-5.00%

-4.00%

-3.00%

Jan-08 Mar-08 May-08 Jul-08 Sep-08 Nov-08 Jan-0960%

70%

80%

90%

-1.20%

-1.00%

-0.80%

-0.60%

Jan-08 Mar-08 May-08 Jul-08 Sep-08 Nov-08 Jan-0960%

70%

80%

90%

7

2009 – 10 Recovery

• Performance Attribution – Delta Hedge on Close through March

– From <4.8%> at YE 2008 to MIN <35%>Primarily reflected in rates’ negative basis < 80%> and

US exposure 2009 – Q110

Cumulative P&L generated by a Delta Hedging Strategy of a GMAB

100% S&P 500, Volatility 15%, Interest Rate 3.5%120.00%20.00% Cumulative P & L Delta Hedge

S&P 500 Index (100 on Jan 2006)– Primarily reflected in rates’ negative basis <.80%> and – Equity interday StDev = 0.42 and – Equity intraday StDev = 1.67– Different Hedgers experienced different results

• Performance Attribution – Delta Hedge from April 2009 – March 2010

60.00%

80.00%

100.00%

-10.00%

0.00%

10.00%

S& 500 de ( 00 o Ja 006)

PERFORMANCE ATTRIBUTION FOR 40% EQUITY DROP AND 50BP CURVE FALL

LIABILITIES FUTURESSTART -$ -$ CH EQ (374,494)$ 125,170$ CH RATES (934,447)$ 333,786$

2009 March 2010

0.00%

20.00%

40.00%

-40.00%

-30.00%

-20.00%

Jan-09 Apr-09 Jul-09 Oct-09 Jan-10

PERFORMANCE ATTRIBUTION FOR 60% EQUITY RALLY AND 50BP CURVE FALL

LIABILITIES FUTURESSTART -$ -$ CH EQ (9,362)$ 14,044$ CH RATES (23,361)$ 8,345$

8

5

Strategies seen in the Market with & without Rho hedges

• That Don’t Destroy Capital for Inforce Business– Variance Swap or option on VS– Timer Puts – Volatility “budget”– Capital Puts – variance based premia

Hybrids selling Vega buying delta buying floors– Hybrids – selling Vega, buying delta, buying floors

• Where Rates were unhedged for accounting or under-hedged (STAT vs. economic)

– Hybrids– Inverse Floaters – non-CDHS– RSAT – non-CDHS

• That address the problem of Cross-Greeks effects– Leveraged Puts– HybridsHybrids

• That address Tracking Error problems for Inforce Blocks– Factor models– CDS’s included in tracking basket for balanced funds

9

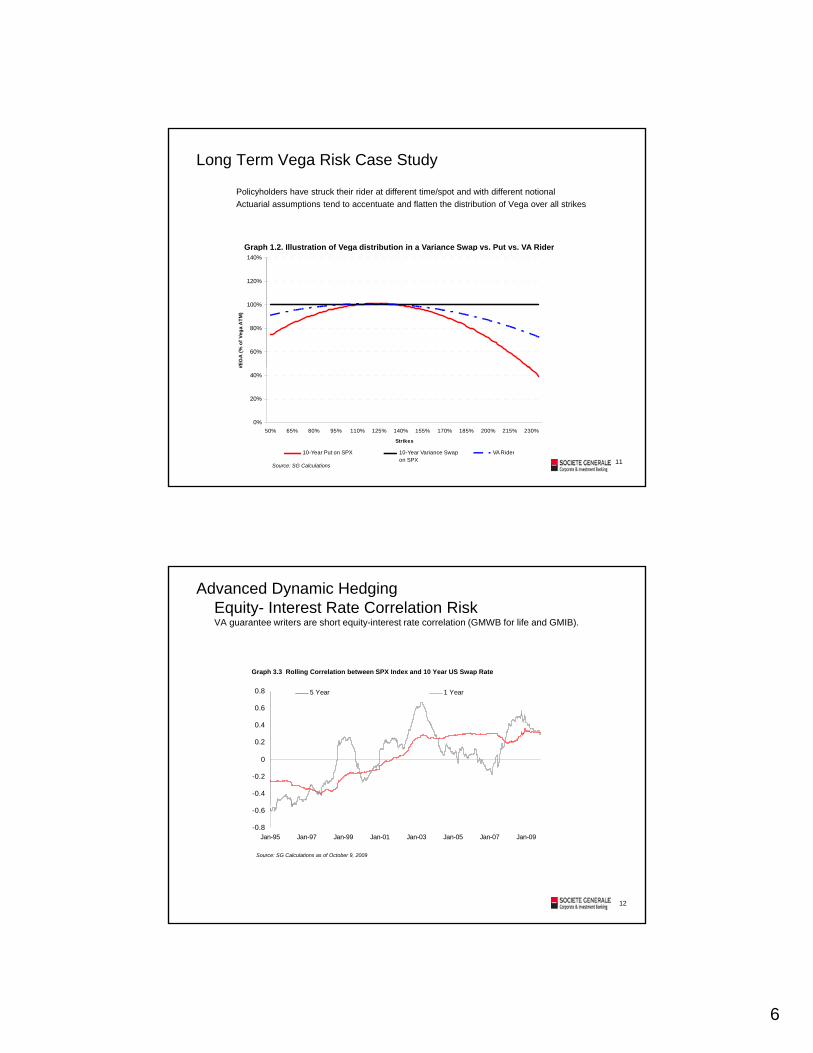

3-Greek Dynamic Hedging Long Term Vega Risk

Hedging Instruments

Long Term ATM Puts

Gamma: At the Strike

Variance Swaps

Gamma: Constant along VsBehaviors such as withdrawal and reset impact the strikes and create a complex Vega exposure relative to the spot price

Still bought by most insurers

gthe strikes (Non Fixed Strike)

Hedge strip for variance swap weights downside strikes to maintain constant Vega (1/k2)

Constant Vega profile offers different risk profile to fixed strike options

Off tt ti d t

Vs.

10

Offer attractive case due to their constant Vega profile relative to spot and in many cases better liquidity.

6

Long Term Vega Risk Case Study

Policyholders have struck their rider at different time/spot and with different notional Actuarial assumptions tend to accentuate and flatten the distribution of Vega over all strikes

Graph 1 2 Illustration of Vega distribution in a Variance Swap vs Put vs VA RiderGraph 1.2. Illustration of Vega distribution in a Variance Swap vs. Put vs. VA Rider

60%

80%

100%

120%

140%

VEG

A (%

of V

ega

ATM

)

11

0%

20%

40%

50% 65% 80% 95% 110% 125% 140% 155% 170% 185% 200% 215% 230%

Strikes

V

Poly. (Put on SPX) Poly. (Var SWAP) Poly. (VA Rider)10-Year Put on SPX 10-Year Variance Swap on SPX

VA Rider

Source: SG Calculations

Advanced Dynamic HedgingEquity- Interest Rate Correlation Risk VA guarantee writers are short equity-interest rate correlation (GMWB for life and GMIB).

Graph 3.3 Rolling Correlation between SPX Index and 10 Year US Swap Rate

-0.4

-0.2

0

0.2

0.4

0.6

0.8 5 Year 1 Year

12

Source: SG Calculations as of October 9, 2009

-0.8

-0.6

Jan-95 Jan-97 Jan-99 Jan-01 Jan-03 Jan-05 Jan-07 Jan-09

7

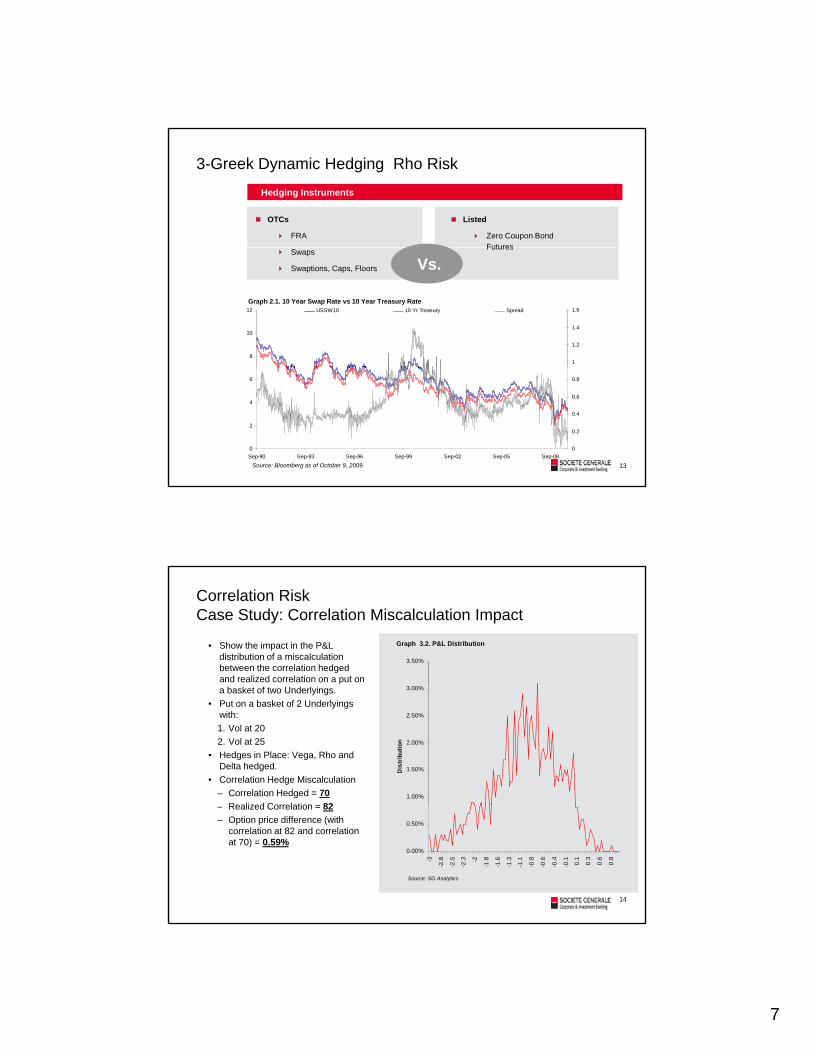

3-Greek Dynamic Hedging Rho Risk

Hedging Instruments

OTCs

FRA

Listed

Zero Coupon Bond Futures

8

10

12

1

1.2

1.4

1.6USSW10 10 Yr Treasury Spread

Swaps

Swaptions, Caps, Floors

Futures

Vs.

Graph 2.1. 10 Year Swap Rate vs 10 Year Treasury Rate

13

0

2

4

6

Sep-90 Sep-93 Sep-96 Sep-99 Sep-02 Sep-05 Sep-080

0.2

0.4

0.6

0.8

Source: Bloomberg as of October 9, 2009.

Correlation RiskCase Study: Correlation Miscalculation Impact

• Show the impact in the P&L distribution of a miscalculation between the correlation hedged and realized correlation on a put on

3.50%

Graph 3.2. P&L Distribution

a basket of two Underlyings. • Put on a basket of 2 Underlyings

with:1. Vol at 202. Vol at 25

• Hedges in Place: Vega, Rho and Delta hedged.

• Correlation Hedge Miscalculation – Correlation Hedged = 70

Realized Correlation 821.00%

1.50%

2.00%

2.50%

3.00%

Dis

trib

utio

n

14

– Realized Correlation = 82– Option price difference (with

correlation at 82 and correlation at 70) = 0.59%

0.00%

0.50%

-3

-2.8

-2.5

-2.3 -2

-1.8

-1.6

-1.3

-1.1

-0.8

-0.6

-0.4

-0.1 0.1

0.3

0.6

0.8

Source: SG Analytics

8

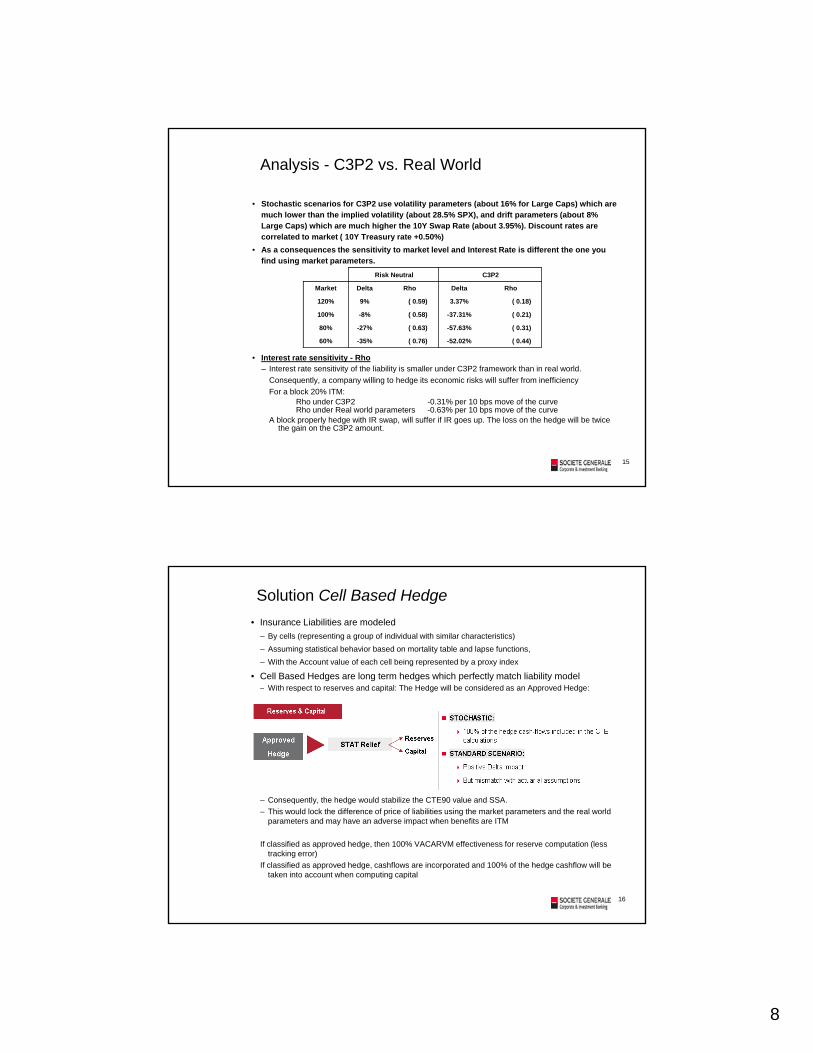

• Stochastic scenarios for C3P2 use volatility parameters (about 16% for Large Caps) which are much lower than the implied volatility (about 28.5% SPX), and drift parameters (about 8% Large Caps) which are much higher the 10Y Swap Rate (about 3.95%). Discount rates are correlated to market ( 10Y Treasury rate +0.50%)A th iti it t k t l l d I t t R t i diff t th

Analysis - C3P2 vs. Real World

• As a consequences the sensitivity to market level and Interest Rate is different the one you find using market parameters.

• Interest rate sensitivity - RhoInterest rate sensitivity of the liability is smaller under C3P2 framework than in real world

Risk Neutral C3P2

Market Delta Rho Delta Rho

120% 9% ( 0.59) 3.37% ( 0.18)

100% -8% ( 0.58) -37.31% ( 0.21)

80% -27% ( 0.63) -57.63% ( 0.31)

60% -35% ( 0.76) -52.02% ( 0.44)

– Interest rate sensitivity of the liability is smaller under C3P2 framework than in real world. Consequently, a company willing to hedge its economic risks will suffer from inefficiency For a block 20% ITM:

Rho under C3P2 -0.31% per 10 bps move of the curveRho under Real world parameters -0.63% per 10 bps move of the curve

A block properly hedge with IR swap, will suffer if IR goes up. The loss on the hedge will be twice the gain on the C3P2 amount.

15

• Insurance Liabilities are modeled – By cells (representing a group of individual with similar characteristics)– Assuming statistical behavior based on mortality table and lapse functions,– With the Account value of each cell being represented by a proxy index

• Cell Based Hedges are long term hedges which perfectly match liability model With t t d it l Th H d ill b id d A d H d

Solution Cell Based Hedge

– With respect to reserves and capital: The Hedge will be considered as an Approved Hedge:

– Consequently, the hedge would stabilize the CTE90 value and SSA.– This would lock the difference of price of liabilities using the market parameters and the real world

parameters and may have an adverse impact when benefits are ITM

If classified as approved hedge, then 100% VACARVM effectiveness for reserve computation (less tracking error)

If classified as approved hedge, cashflows are incorporated and 100% of the hedge cashflow will be taken into account when computing capital

16

9

New Hybrids

Hybrid option appropriate for GMIB hedging

PAYOFF 1: MAX (Strike - Leverage * USSW10 spot - SPX Yield, 0.0) where leverage is a fixed value which determines your rate sensitivity

PAYOFF 2: Hybrid swaption with a swaption strike which depends on Equity.

Both of them have the same background. The put allows the hedger to choose the notional of the cashflows to pay and the rate part, as multiplier, takes part of the rate sensitivity - due to the discount of all the cashflows. The two structures are made for two different purposes with different convexities for each.

Hybrid option appropriate for GMWB hedging

PAYOFF 3: leverage on rate * put. [Payoff is: MAX( Strike - SPX Yield,0.0) * Leverage] where leverage is for example: – 0 if USSW10 is above 5%– 1 if USSW10 is below 3%a linear interpolation,– Otherwise, formula is: [1 - (USSW10 - 3%)/2%]

This is a medium term product - created to buy correlation. It allows a hedger to buy a significant amount of sensitivity to correlation plus get access to some cross Greeks However it does not match maturity of the liabilities It does not provide a good Equity hedge or Interestaccess to some cross Greeks. However, it does not match maturity of the liabilities. It does not provide a good Equity hedge or Interest rate hedge. It allows the hedger to mainly realize P&L when correlation increases.

PAYOFF4: Put * Discount factor. Payoff is: [MAX(Strike - SPX Yield,0.0) * 1/(1+USSW10)^5]

This last product should be viewed more from a cash flow perspective. It's intended to hedge the cashflows - not the Greeks sensitivities (IR equity correlation sensitivity is small). Maturity is a good feature because the hedger buys some equity & interest rate volatility and avoids buying correlation, which, today, is may be viewed as expensive. It may represent a significant portion of any hedging strategy.

17

Conclusion

• Hedge Economic Liabilities– Uncertainty and Recovery combine to tilt the tables in favor of 100% hedge

• With Capital and Letters of Credit at a premium Variance-based fees minimize the increase ofWith Capital and Letters of Credit at a premium Variance based fees minimize the increase of reserves customarily caused by vega hedging

– RBC ratios have dropped from an average of 380 in 2007 to 285 today (even after $1.2TR)– Cost of capital in recent equity and debt offers have risen from 8% to as much as 16% today

• AG43 has pitched some insurers into SSA sensitivity– Hedges or reinsurance now has to cover both tails

• Rates Down : Equity Down – Greatest Reserve Hit• Rates up (lapse up) : Equity UP – Greatest Lapse Hit

– Over-hedging/Gamma hedging• AG43 opens up the opportunity to treat Reinsurance as “Approved Hedge”

– To be included in liability simulationsy– To be included in SSA as an asset that is liquidated down 13.5%

• Dynamic Hedging is punished under AG43

18

10

Appendix 1

Coleman, Kim, Patron, Robustly Hedging Variable Annuities with Guarantees Under Jump and Volatility Risks, 2004

19