Extension Summer Outlook Conference | Connecting Cows, Cooperatives, Capitol Hill, & Consumers |...

23

Extension Summer Outlook Conference | Connecting Cows, Cooperatives, Capitol Hill, & Consumers | August 2015 C o n n e c t i n g C o w s , C o o p e r a t i v e s , C a p i t o l H i l l , & C o n s u m e r s National Milk Producers Federation Extension Summer Outlook Conference Dairy Market Outlook John Newton [email protected] @New10_AgEcon

-

Upload

ethan-craig -

Category

Documents

-

view

213 -

download

0

Transcript of Extension Summer Outlook Conference | Connecting Cows, Cooperatives, Capitol Hill, & Consumers |...

Extension Summer Outlook Conference | Connecting Cows, Cooperatives, Capitol Hill, & Consumers | August 2015

C o n n e c t i n g C o w s , C o o p e r a t i v e s , C a p i t o l H i l l , & C o n s u m e r s

National Milk Producers Federation

Extension Summer Outlook Conference

Dairy Market Outlook

John [email protected]

@New10_AgEcon

19

80

19

85

19

90

19

95

20

00

20

05

20

10

20

15$8

$12

$16

$20

$24

M-W, BFP, and Class III Milk Price Dairy Support Price

M-W

, B

FP

, C

las

s I

II M

ilk

, a

nd

Su

pp

ort

P

ric

e i

n $

/hu

nd

red

we

igh

t

2015 Extension Summer Outlook Conference August 2015

2

Record High U.S. Milk Prices in 2014Dairy Product Support Price Ineffective Since 2010

Source: USDA AMS, FSA, and author’s calculations

2015 Extension Summer Outlook Conference August 2015

3

Forecast Annual Milk Production Growth Rates Big-5 Exporters

Source: USDEC. 2015 includes USDEC forecasts

EU-28 US NZ Australia Argentina0%

5%

2.2%

0.9%

2.5%

3.4%

0.6%

Projected 2015 Milk Production Growth(EU-28,U.S., New Zealand, Australia, Argentina)

%

Current YTD U.S. Milk Production Growth Rate at 1.4% Based on USDA NASS

2015 Extension Summer Outlook Conference August 2015

4

Milk Production Forecast Higher in 2015 Following Record Prices of 2014

2007 2008 2009 2010 2011 2012 2013 2014 2015F -

50,000

100,000

150,000

200,000

250,000

300,000

350,000

Milk Production from Major Exporters(EU-28,U.S., New Zealand, Australia, Argentina)

EU-28 US NZ Australia Argentina

(00

0 M

T)

Source: USDEC. 2015 includes USDEC forecasts

Total: 633 Billion Lbs.

+0.9% +0.4% +1.5% +3.0% +1.8% +0.1% +3.7% +1.8%

2015 Extension Summer Outlook Conference August 2015

5

Demand Missing, China and Russia Imports Needed to Offset Overhanging Supply

2011 2012 2013 2014 2015700

1,100

1,500

1,900

2,300

China imports(rolling 12 months)

(000

MT

)

2011 2012 2013 2014 20151,000

1,075

1,150

1,225

1,300

Southeast Asia-5 imports(rolling 12 months)

(000

MT

)

2011 2012 2013 2014 2015100

200

300

400

500

600

Russia imports(rolling 12 months)

(000

MT

)

Source: USDEC, GTIS. Southeast Asia-5 includes Indonesia, Philippines, Malaysia, Thailand and Singapore.

2014 Jan - Jun 2015 Jan - Jun0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

Non-Fat Dry Milk WheyCheese And Curd Other Dairy Products

Exp

orts

in M

illio

n U

SD

-26.9% YTD

2014 Jan - Jun 2015 Jan - Jun0

200

400

600

800

1,000

1,200

1,400

Non-Fat Dry Milk WheyCheese And Curd Other Dairy Products

Exp

orts

in T

hous

and

Met

ric T

ons

-10.6% YTD

2015 Extension Summer Outlook Conference August 2015

6

YTD U.S. Dairy Exports Down in 2015When Will China Return and Duration of Russian Ban Are Major Unknowns.

Source: USDA FAS GATS

U.S. Dairy Exports by ValueU.S. Dairy Exports by Volume

Value reduction driven by lower dairy

commodity prices

2015 Extension Summer Outlook Conference August 2015

7

Projections for Export Share of U.S. Milk Production is Flat in 2015-2016

Source: USDA NASS and WASDE. Export share based on author’s calculations.

96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15* 16*140

150

160

170

180

190

200

210

220

U.S. Milk Production and Volume Exported

Domestic use Exports

Bil

lio

n P

ou

nd

s

2015 Extension Summer Outlook Conference August 2015

8

Ample Supplies Weigh on Markets and Competition is Aggressive in Powders

Source: USDA AMS

1/5

/20

13

2/1

3/2

01

33

/24

/20

13

5/2

/20

13

6/1

0/2

01

37

/19

/20

13

8/2

7/2

01

31

0/5

/20

13

11

/13

/20

13

12

/22

/20

13

1/3

0/2

01

43

/10

/20

14

4/1

8/2

01

45

/27

/20

14

7/5

/20

14

8/1

3/2

01

49

/21

/20

14

10

/30

/20

14

12

/8/2

01

41

/16

/20

15

2/2

4/2

01

54

/4/2

01

55

/13

/20

15

6/2

1/2

01

5

$1.00

$1.50

$2.00

$2.50

$3.00

$3.50

US Butter Oceania Butter

$/lb

1/5

/20

13

2/1

2/2

01

33

/22

/20

13

4/2

9/2

01

36

/6/2

01

37

/14

/20

13

8/2

1/2

01

39

/28

/20

13

11

/5/2

01

31

2/1

3/2

01

31

/20

/20

14

2/2

7/2

01

44

/6/2

01

45

/14

/20

14

6/2

1/2

01

47

/29

/20

14

9/5

/20

14

10

/13

/20

14

11

/20

/20

14

12

/28

/20

14

2/4

/20

15

3/1

4/2

01

54

/21

/20

15

5/2

9/2

01

57

/6/2

01

5

$1.25

$1.75

$2.25

$2.75

US Cheese Oceania Cheese

$/lb

1/5

/20

13

2/1

3/2

01

33

/24

/20

13

5/2

/20

13

6/1

0/2

01

37

/19

/20

13

8/2

7/2

01

31

0/5

/20

13

11

/13

/20

13

12

/22

/20

13

1/3

0/2

01

43

/10

/20

14

4/1

8/2

01

45

/27

/20

14

7/5

/20

14

8/1

3/2

01

49

/21

/20

14

10

/30

/20

14

12

/8/2

01

41

/16

/20

15

2/2

4/2

01

54

/4/2

01

55

/13

/20

15

6/2

1/2

01

5

$0.60

$1.10

$1.60

$2.10

$2.60

$3.10

US Nonfat Oceania SMP

$/lb

1/5

/20

13

2/1

2/2

01

33

/22

/20

13

4/2

9/2

01

36

/6/2

01

37

/14

/20

13

8/2

1/2

01

39

/28

/20

13

11

/5/2

01

31

2/1

3/2

01

31

/20

/20

14

2/2

7/2

01

44

/6/2

01

45

/14

/20

14

6/2

1/2

01

47

/29

/20

14

9/5

/20

14

10

/13

/20

14

11

/20

/20

14

12

/28

/20

14

2/4

/20

15

3/1

4/2

01

54

/21

/20

15

5/2

9/2

01

57

/6/2

01

5

$0.30

$0.40

$0.50

$0.60

$0.70

$0.80

US Whey Europe Dry Whey

$/lb

CheeseButter

Dry WheyNonfat and SMP

2015 Extension Summer Outlook Conference August 2015

9

Butter and Cheese Prices Stabilizing, Nonfat Continues Slide

Source: USDA AMS

1/8

/20

11

2/1

9/2

01

14

/2/2

01

15

/14

/20

11

6/2

5/2

01

18

/6/2

01

19

/17

/20

11

10

/29

/20

11

12

/10

/20

11

1/2

1/2

01

23

/3/2

01

24

/14

/20

12

5/2

6/2

01

27

/7/2

01

28

/18

/20

12

9/2

9/2

01

21

1/1

0/2

01

21

2/2

2/2

01

22

/2/2

01

33

/16

/20

13

4/2

7/2

01

36

/8/2

01

37

/20

/20

13

8/3

1/2

01

31

0/1

2/2

01

31

1/2

3/2

01

31

/4/2

01

42

/15

/20

14

3/2

9/2

01

45

/10

/20

14

6/2

1/2

01

48

/2/2

01

49

/13

/20

14

10

/25

/20

14

12

/6/2

01

41

/17

/20

15

2/2

8/2

01

54

/11

/20

15

5/2

3/2

01

57

/4/2

01

5$0.50

$1.00

$1.50

$2.00

$2.50

$3.00U.S. Dairy Commodity Price Trends

Butter Cheddar Nonfat

$/lb

.

NFDM Prices At Old Price Support Levels of $0.80/lb

2015 Extension Summer Outlook Conference August 2015

10

Other Cheese

American-Type Cheese

Nonfat and Skim Milk Powders

Butter

Long Run Trends For All Products Show Increasing Consumption, But Butter Showing Short Run Decline

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

100

120

140

160

180 Export 12-Mo MA

Domestic 12-Mo MA

Mil

lio

n P

ou

nd

s

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

-

40

80

120

160

200

240 Export 12-Mo MA

Domestic 12-Mo MA

Mil

lio

n P

ou

nd

s

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

300

340

380

420 Export 12-Mo MA

Domestic 12-Mo MA

Mil

lio

n P

ou

nd

s

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

400

440

480

520

560

600

640 Export 12-Mo MA

Domestic 12-Mo MA

Mil

lio

n P

ou

nd

s

Source: USDA ERS

2015 Extension Summer Outlook Conference August 2015

11

Source: USDA NASS

2015 Butter Production YTD is Down 1.5% While Cheese and Nonfat Remain Firm Over Prior Year Levels

Nonfat Dry Milk

Dry WheyTotal Cheese

Butter

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

80

120

160

200

Butter Production 12-Mo Moving Avg

Mil

lio

n P

ou

nd

s

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

700

750

800

850

900

950

1,000

1,050

Cheese Production 12-Mo Moving Avg

Mil

lio

n P

ou

nd

s

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

507090

110130150170190210

Nonfat Production 12-Mo Moving Avg

Mil

lio

n P

ou

nd

s

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

60

70

80

90

100

110

120

Dry Whey Production 12-Mo Moving Avg

Mil

lio

n P

ou

nd

s

2015 Extension Summer Outlook Conference August 2015

12

Jan

Fe

b

Ma

r

Ap

r

Ma

y

Jun

Jul

Au

g

Se

p

Oct

No

v

De

c

100

150

200

250

300

Butter

2015 2014 2013

Mil.

Lb

s.

Jan

Fe

b

Ma

r

Ap

r

Ma

y

Jun

Jul

Au

g

Se

p

Oct

No

v

De

c

990

1,020

1,050

1,080

1,110

1,140

1,170Total Cheese

2015 2014 2013

Mil.

Lb

s.

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

1550

100

150

200

250

Nonfat Dry Milk Mfg Stocks(12-Month Moving Average)

Mill

ion

Po

un

ds

Butter Stocks Remain Relatively Tight While Cheese and Nonfat At Or Near Records

Source: USDA NASS

2015 Extension Summer Outlook Conference August 2015

13

Many U.S. Farmers Responded to Record 2014 Prices by Expanding Herd/Milk Output (U.S. +50K Head Through Jun YOY)

Source: USDA NASS

California milk production is down 85 Lbs/cow YOY

2015 Extension Summer Outlook Conference August 2015

14

Ample Supplies and Demand Slowdown in U.S. Pulling Milk Prices Down

Source: USDA NASS

2015 Extension Summer Outlook Conference August 2015

15

Source: USDA FAS and WAOB

80% of U.S. Milk Production in 2015 is Enrolled in MPP-Dairy (55% of Farms)

2015 Extension Summer Outlook Conference August 2015

16

Source: USDA FAS and author’s calculations

Cumulative Percent of Projected Milk Production Enrolled in MPP-Dairy

$4.00 $4.50 $5.00 $5.50 $6.00 $6.50 $7.00 $7.50 $8.000.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

90.0%80.1%

33.0% 32.7%29.6% 28.2%

13.9%

3.0% 2.5% 0.5%

MPP-Dairy Coverage Level

Pe

rce

nt

Higher coverage levels had higher premium rates

Weighted Average: $4.82/cwt

2015 Extension Summer Outlook Conference August 2015

17

Source: USDA FAS and author’s calculations

Estimate: $60 Million USD Collected in MPP-Dairy Premiums in 2015

Admin $4.00 $4.50 $5.00 $5.50 $6.00 $6.50 $7.00 $7.50 $8.000

5

10

15

20

25

30

$2.5

$0.0 $0.1$1.9 $1.4

$26.3

$15.9

$1.3

$7.0

$3.2

Estimate of MPP-Dairy Premiums and Administrative Fees Collected by Coverage Level, 2015 CY

MPP-Dairy Coverage Level and Administrative Fee

Mill

ion

Do

llars

Only $8 Has Triggered

MPP-Payments to Holders of $8 Coverage

Jan-Feb: $4,336Mar-Apr: $482,134May-Jun: $4,530

2015 Extension Summer Outlook Conference August 2015

18

U.S. Milk Prices Down Nearly 40% from 2014 Highs, Down 27% YOY

Source: USDA NASS

2015 Extension Summer Outlook Conference August 2015

19

Source: USDA NASS and author’s calculations

The Tale of Two Corn BeltsFavorable Weather in W. Corn Belt May Offset Yield/Acreage Losses in E. Corn Belt

168.8 BPA Corn is Only 2.2 BPA Less than 2014 RecordAbove 2014 Yields in W. Corn Belt

10 11 12 13 14 15* 16*2

4

6

8

10

12

14

16

MPP-Dairy Margin

$/c

wt.

2015 Extension Summer Outlook Conference August 2015

20

Low Feed Prices Keeps MPP Margin Near Historical Average Despite Milk Price Fall

*NMPF/USDA Forecast

Payments Possible Through 2016

25% Lower Bound

75% Upper Bound

Average

Source: USDA NASS, AMS, FSA. Forecast based on author’s calculations as of August 11, 2015.

2015 Extension Summer Outlook Conference August 2015

21

MPP-Dairy Outperforming MILC as a Dairy Farm Safety Net

Source: USDA NASS, FSA and author’s calculations.

8 9 10 11 12 13 14 15$0

$5

$10

$15

$20

$25

$30Milk Income Loss Contract Payments and Trigger

MILC Payment MILC Reference Price Boston Class I

Va

lue

in $

/hu

nd

red

we

igh

t

MPP-Dairy Has Been in Payment Status For All of 2015,MILC Would Not Have Triggered

C o n n e c t i n g C o w s , C o o p e r a t i v e s , C a p i t o l H i l l , & C o n s u m e r s

National Milk Producers Federation

John NewtonSenior Director of Economic Research

Extension Summer Outlook Conference | Connecting Cows, Cooperatives, Capitol Hill, & Consumers | August 2015

2015 Extension Summer Outlook Conference August 2015

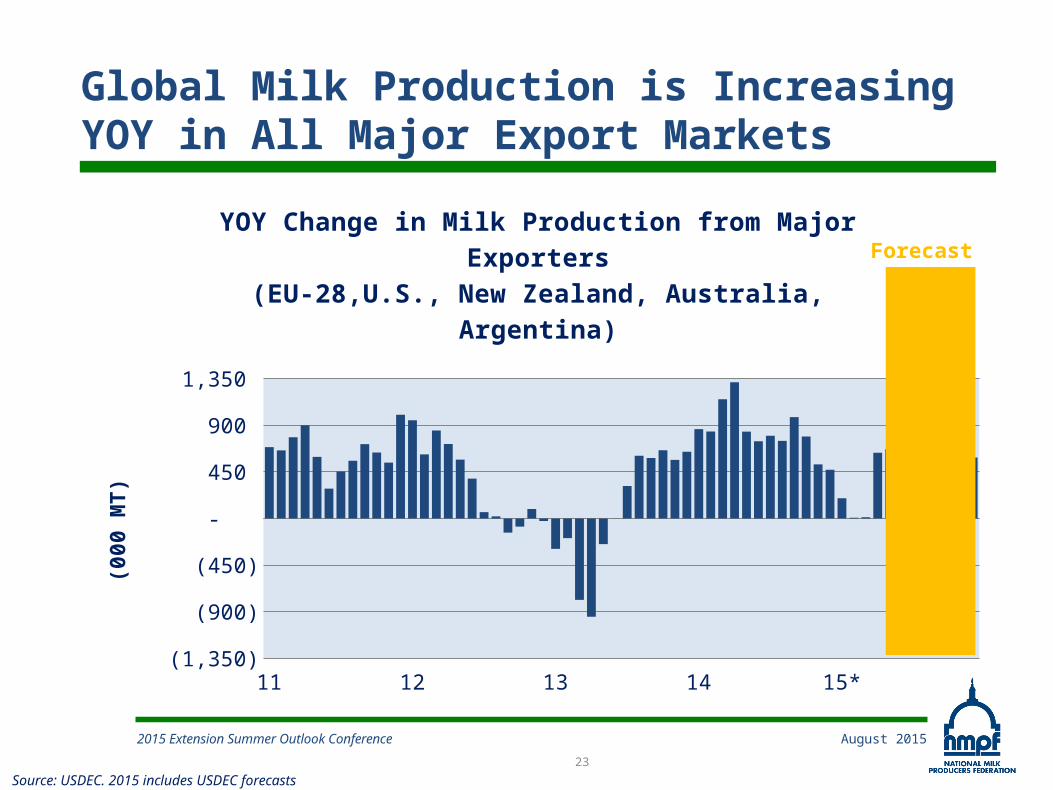

23

Global Milk Production is Increasing YOY in All Major Export Markets

Source: USDEC. 2015 includes USDEC forecasts

11 12 13 14 15* (1,350)

(900)

(450)

-

450

900

1,350

YOY Change in Milk Production from Major Exporters(EU-28,U.S., New Zealand, Australia, Argentina)

(00

0 M

T)

Forecast