Experiences with Structural Adjustment of the Australian ...

24

Experiences with Structural Adjustment of the Australian Steel industry Presentation by Dr Bob Every Managing Director and CEO of OneSteel Limited September 9, 2004

Transcript of Experiences with Structural Adjustment of the Australian ...

Experiences with Structural Adjustment of the Australian Steel industryPresentation by Dr Bob EveryManaging Director and CEO of OneSteel LimitedSeptember 9, 2004

Slide 2

Contents

• Global Industry Landscape• Australian Industry Landscape• Current Trends and Structural Impacts• The Future of Steel

Global Steel Industry Landscape

Slide 4

Global Steel Industry Landscape

• Period from 1970 to 2000– Global Over-capacity

• 800 million tonnes demand• 950 million tonnes capacity

– Fragmented Industry• 95 players produce more than 2 million tonnes p.a• Top player only produces 3-4% of world production

• Since 2000– Some consolidation is occurring– China has grown dramatically – 25-30% of world demand– Mega or niche to succeed

Slide 5

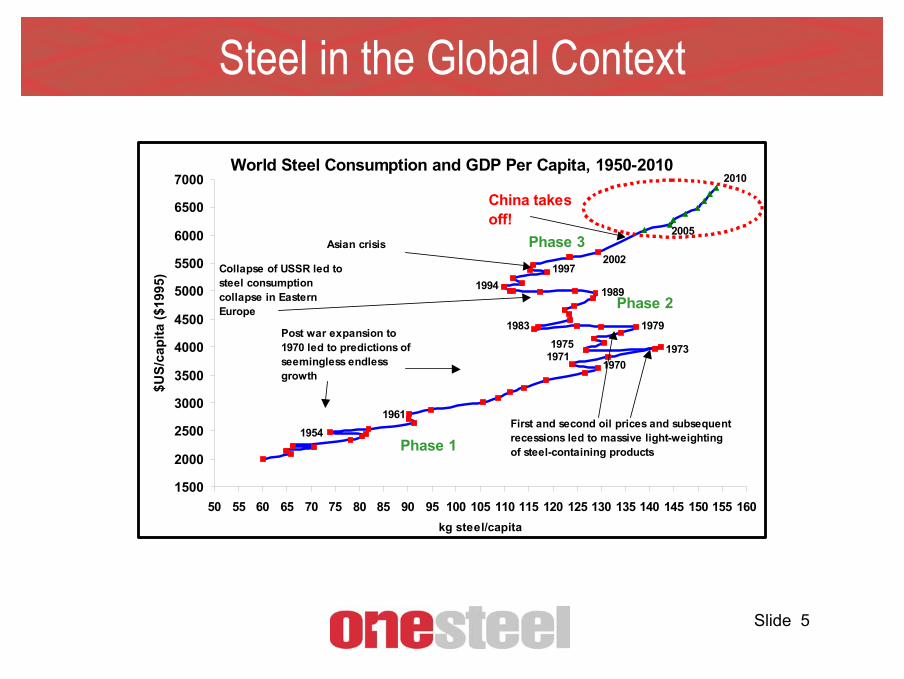

Steel in the Global Context

World Steel Consumption and GDP Per Capita, 1950-2010

1500

2000

2500

3000

3500

4000

4500

5000

5500

6000

6500

7000

50 55 60 65 70 75 80 85 90 95 100 105 110 115 120 125 130 135 140 145 150 155 160kg steel/capita

$US/

capi

ta ($

1995

)

20021997

1994 1989

1983 19791975

19711970

1973

1961First and second oil prices and subsequent recessions led to massive light-weighting of steel-containing products

Post war expansion to 1970 led to predictions of seemingless endless growth

Collapse of USSR led to steel consumption collapse in Eastern Europe

Asian crisis

China takes off!

1954

2005

2010

Phase 1

Phase 2

Phase 3

Source: Macquarie Research

Slide 6

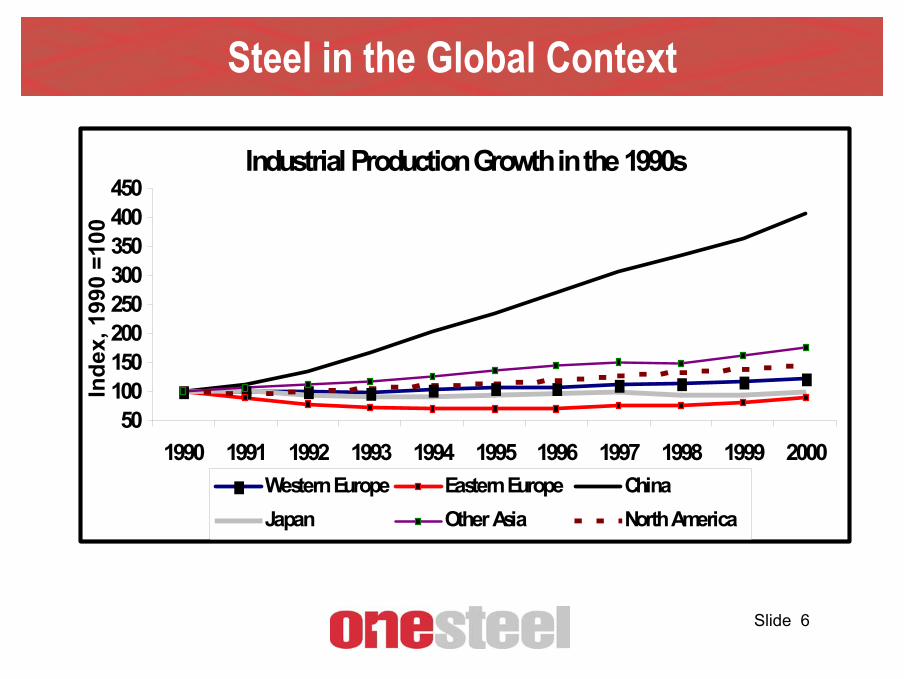

Steel in the Global Context

Industrial Production Growth in the 1990s

50100150200250300350400450

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000

Inde

x, 1

990

=100

Western Europe Eastern Europe ChinaJapan Other Asia North America

Source: Ecowin

Slide 7

Steel in the Global Context

World Steel Consumption by Region

0

100000

200000

300000

400000

500000

600000

700000

800000

900000

1955

1958

1961

1964

1967

1970

1973

1976

1979

1982

1985

1988

1991

1994

1997

2000

'000

t cru

de s

teel

ChinaJapanOther AsiaWestern EuropeEastern EuropeFormer Soviet UnionMiddle EastAfricaOceaniaLatin AmericaCanadaUSA

Source: IISI

Slide 8

International Steel Production and Prices

Slide 9

International Steel Forecast Demand

Slide 10

Steel in the Global Context

• Early signs of a complementary change on the production side

• Consolidation is occurring- Corus – from merger of British Steel and Hoogovens- Arcelor – from merger of Usinor, Arbed and Aceralia- JFE Steel – from NKK and Kawasaki- U.S. Steel acquired assets of National Steel- Nucor has made four acquisitions over two years

Slide 11

Steel in the Global Context

• So what does this all mean?– We may be entering a new period of growth

in international steel – the first time in three decades

– It has the potential to change the balance in the industry from over to under supply

Australian Steel Industry Landscape

Slide 13

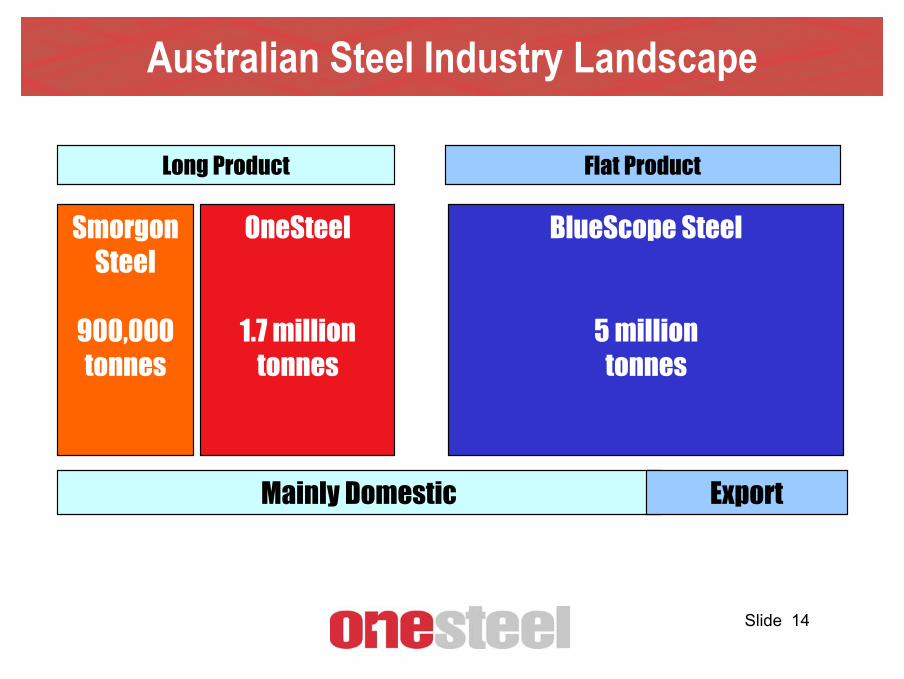

Australian Steel Industry Landscape

• 1970s– One Steel producer – BHP (Blast furnace based)

• 1980s– Emergence of Smorgon Steel (Electric Arc furnace)

• 1990s– BHP closes Newcastle steel works (1.5 million tonne facility)

• 2000s, BHP exits steel– BHP spins off OneSteel Limited (long products)– BHP Billiton spins off BlueScope Steel (flat products)

Slide 14

Australian Steel Industry Landscape

Smorgon Steel

900,000 tonnes

Long Product Flat Product

OneSteel

1.7 milliontonnes

BlueScope Steel

5 milliontonnes

Mainly Domestic Export

Current Trends and Structural Impacts

Slide 16

Scrap PricesAsian HM1 Scrap Price

Jan 1994 to Jul 2004

$80$100$120$140$160$180$200$220$240$260$280$300$320$340$360$380$400$420$440$460

Jul-9

5

Jan-

96

Jul-9

6

Jan-

97

Jul-9

7

Jan-

98

Jul-9

8

Jan-

99

Jul-9

9

Jan-

00

Jul-0

0

Jan-

01

Jul-0

1

Jan-

02

Jul-0

2

Jan-

03

Jul-0

3

Jan-

04

Jul-0

4

$/t

$US/t $A/t

Source : Tex Report

Slide 17

Trends in International Long Product Steel Prices

Long Products International PricesJan 1994 to Jul 2004. (US$)

150

200

250

300

350

400

450

500

550

600

Jan-94

Jul-94

Jan-95

Jul-95

Jan-96

Jul-96

Jan-97

Jul-97

Jan-98

Jul-98

Jan-99

Jul-99

Jan-00

Jul-00

Jan-01

Jul-01

Jan-02

Jul-02

Jan-03

Jul-03

Jan-04

Jul-04U

S$/T

onne

(c&

f int

o C

hina

) ex

Non

-CIS

BEAMS MER.BAR REBARS LC WIRE ROD

Source : CRU

Slide 18

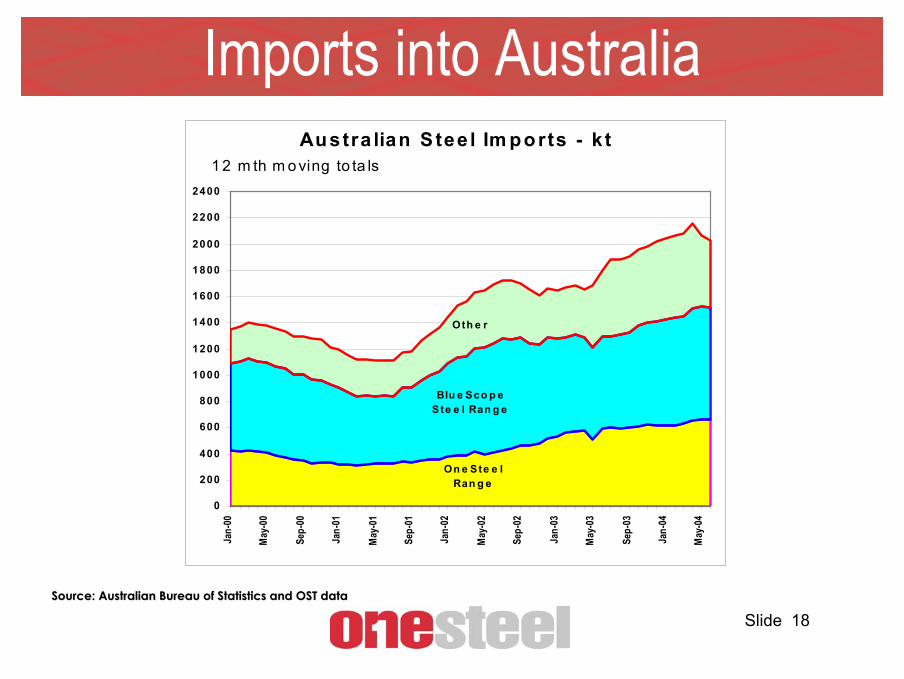

Imports into Australia

Source: Australian Bureau of Statistics and OST dataSource: Australian Bureau of Statistics and OST data

Austra lian S tee l Im ports - k t

On e Ste e l Ran g e

Blu e Sco p e Ste e l Ran g e

Oth e r

0

200

400

600

800

1000

1200

1400

1600

1800

2000

2200

2400

Jan-

00

May

-00

Sep-

00

Jan-

01

May

-01

Sep-

01

Jan-

02

May

-02

Sep-

02

Jan-

03

May

-03

Sep-

03

Jan-

04

May

-04

1 2 m th m o ving to ta ls

Slide 19

Import versus International Prices - $AUDFrom January 1999 to June 2004

0 .9

1.1

1.3

1.5

1.7

1.9

2 .1

Jan-9 9

M ay-9 9

S e p -9 9

Jan-0 0

M ay-0 0

S e p -0 0

Jan-0 1

M ay-0 1

S e p -0 1

Jan-0 2

M ay-0 2

S e p -0 2

Jan-0 3

M ay-0 3

S e p -0 3

Jan-0 4

M ay-0 4

Basket of Goods (Rebar, Mebar, Structural)

Inde

x

Import Price

International Price

Source: Australian Bureau of Statistics and OST dataSource: Australian Bureau of Statistics and OST data

Import versus International Prices

Australian Dollar Australian Dollar Appreciation Appreciation

ImpactImpact

Slide 20

Australian Steel Price Index

Source: Australian Bureau of StatisticsSource: Australian Bureau of Statistics

Prices for Steel Construction Materials from 1990-2004

90

100

110

120

130

140

150

QUARTERS FROM MARCH 1990 TO JUNE 2004

IND

EX (1

989-

90=1

00)

Steel decking and cladding Structural steel Reinforcing steel bar, fabric and mesh

Weighted Average of 8 Capital Cities CPI Steel products used in Res construction

Structural steel

Rebar & mesh

Decking & cladding

Steel in Res Construc

CPI

Slide 21

International Freight Rates

Source: Clarkson Research StudiesSource: Clarkson Research Studies

Slide 22

Performance of Australian Steel Companies

Share Price Performance of Australian Steel Companies versus All Ordinaries(Indexed at 100 on 21 July 2002)

80

100

120

140

160

180

200

Jul-0

2

Aug-

02

Sep-

02

Oct

-02

Nov

-02

Dec

-02

Jan-

03

Feb-

03

Mar

-03

Apr

-03

May

-03

Jun-

03

Jul-0

3

Aug-

03

Sep-

03

Oct

-03

Nov

-03

Dec

-03

Jan-

04

Feb-

04

Mar

-04

Apr

-04

May

-04

Jun-

04

Jul-0

4

Inde

x Va

lue

All Ordinaries Index

Australian Steel Companies Index*

* Index of the share prices of BlueScope Steel, OneSteel, Sims and Smorgon Steel (not weighted by market capitalisation)

Slide 23

The Future for Steel

• Steel Consumption is rising, driven by China

• Less government ownership

• Consolidation is occurring, at least regionally

Slide 24

Conclusion• Australian steel industry undergone massive

restructuring• An exciting decade ahead

- supply and demand changing- potential for strong sustainable steel prices

• Australian steel companies are creating value• OneSteel has undergone a process of

reinvention

I believe we really are seeing the reinvention of steel