EXCHANGE RATES AND TRADE - ccgi.fgv.brccgi.fgv.br/sites/ccgi.fgv.br/files/file/OMC x FMI - câmbio...

33

EXCHANGE RATES AND TRADE CENTER FOR GLOBAL TRADE AND INVESTMENTS SÃO PAULO SCHOOL OF ECONOMICS FGV-SP 2013 Prof. Vera Thorstensen,

-

Upload

trinhkhuong -

Category

Documents

-

view

215 -

download

0

Transcript of EXCHANGE RATES AND TRADE - ccgi.fgv.brccgi.fgv.br/sites/ccgi.fgv.br/files/file/OMC x FMI - câmbio...

EXCHANGE RATES AND

TRADE

CENTER FOR GLOBAL TRADE AND INVESTMENTS

SÃO PAULO SCHOOL OF ECONOMICS

FGV-SP 2013

Prof. Vera Thorstensen,

Big Mac Index – 1/2013

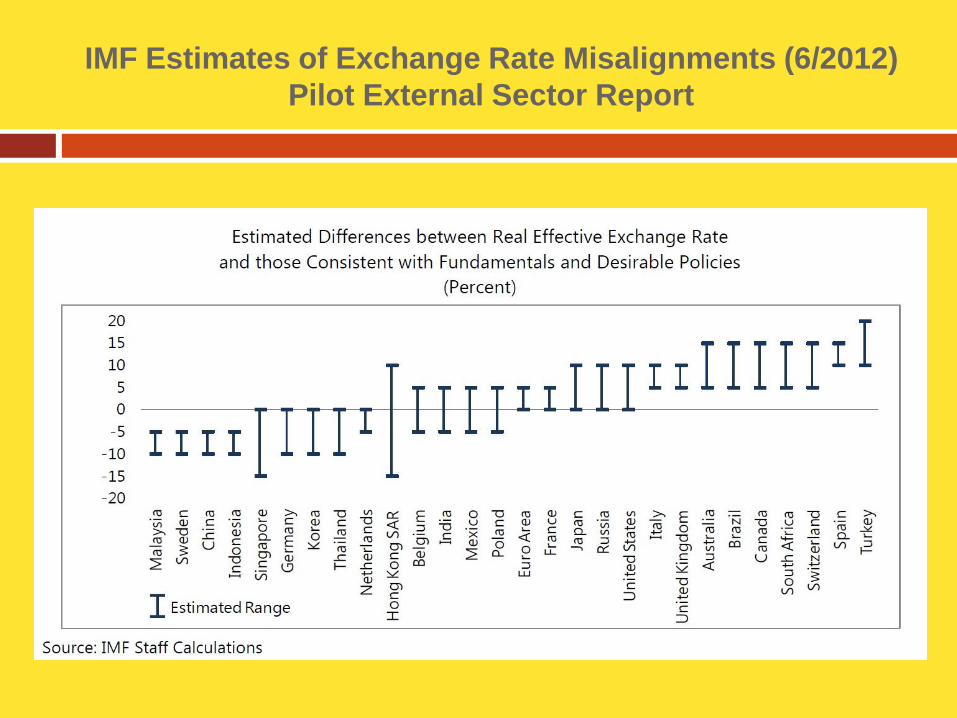

IMF Estimates of Exchange Rate Misalignments (6/2012)

Pilot External Sector Report

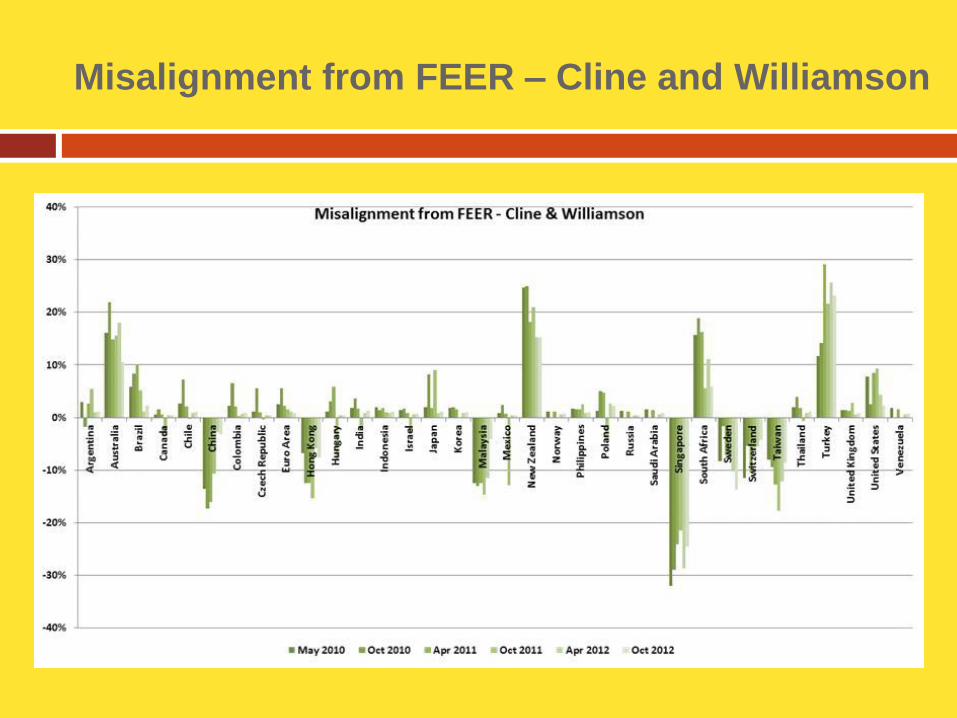

Misalignment from FEER – Cline and Williamson

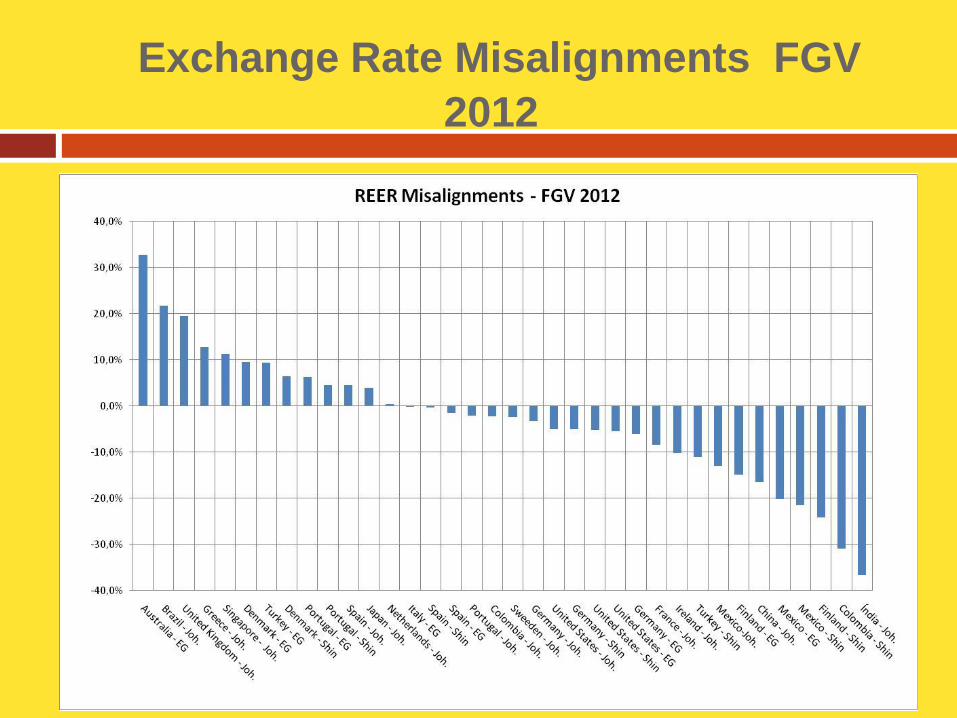

Exchange rate misalignments 2010 - 2012(Shin, Johansen, Engle-Granger) FGV

Exchange Rate Misalignments FGV

2012

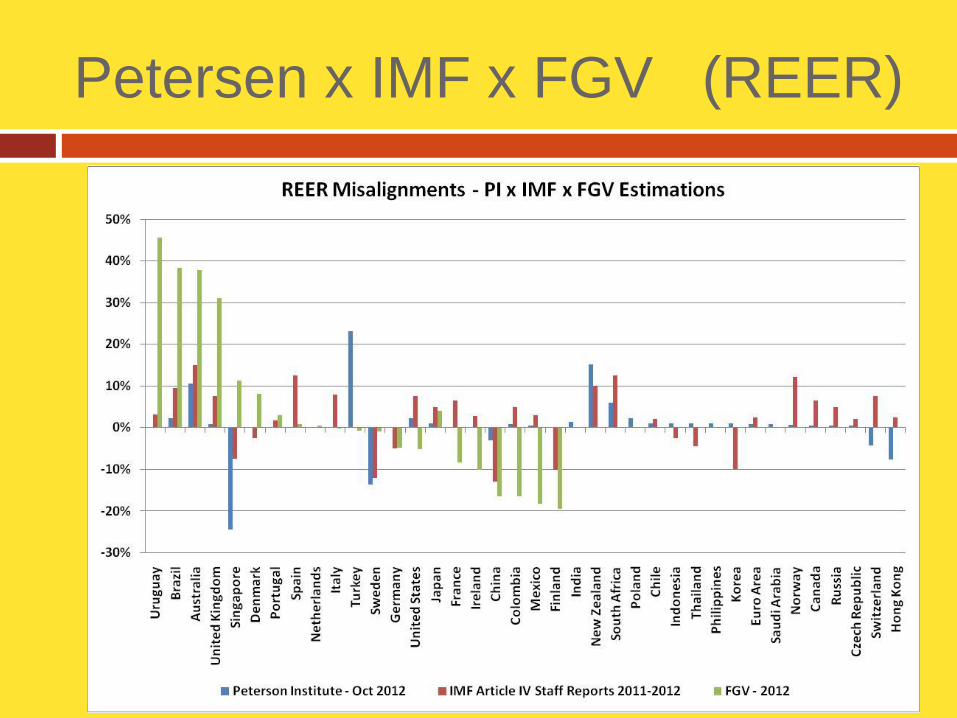

Petersen x IMF x FGV (REER)

Brazil: real exchange rate, fundamentals and exchange

rate misalignments (annually)

8

Sources: Misalignment estimates – Observatory on Exchange Rate - EESP/FGV (2013)

Real Effecitive Exchange Rate Fundamentals

1970 1975 1980 1985 1990 1995 2000 2005 2010

60

80

100

Real Effecitive Exchange Rate Fundamentals

Exchange Rate Misalignment

1970 1975 1980 1985 1990 1995 2000 2005 2010

-20

-10

0

10

20

30Exchange Rate Misalignment

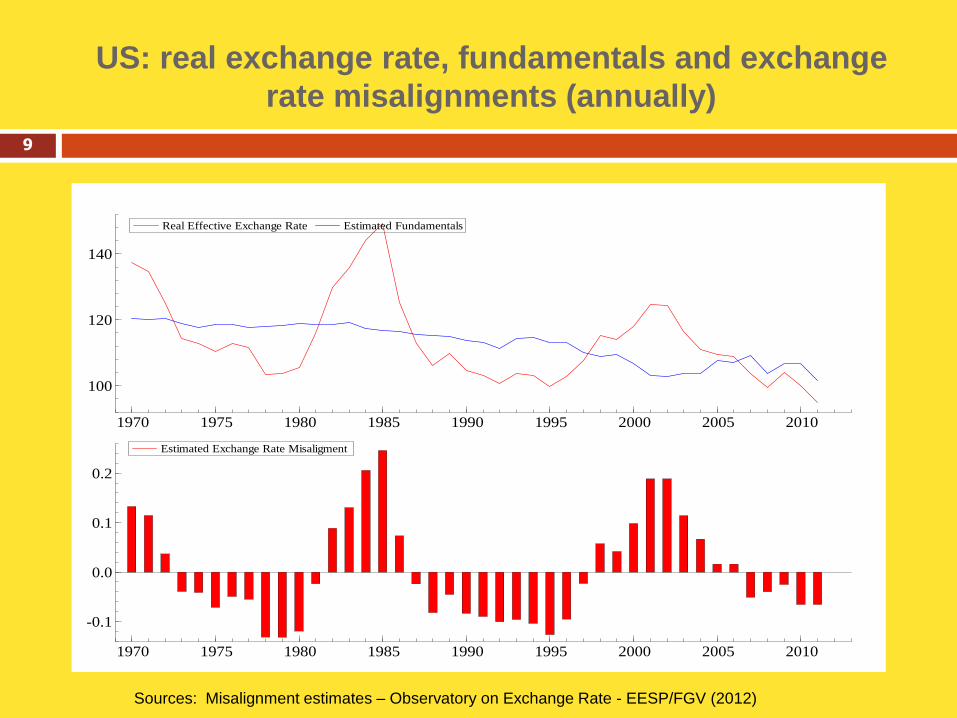

US: real exchange rate, fundamentals and exchange

rate misalignments (annually)

9

Sources: Misalignment estimates – Observatory on Exchange Rate - EESP/FGV (2012)

Real Effective Exchange Rate Estimated Fundamentals

1970 1975 1980 1985 1990 1995 2000 2005 2010

100

120

140

Real Effective Exchange Rate Estimated Fundamentals

Estimated Exchange Rate Misaligment

1970 1975 1980 1985 1990 1995 2000 2005 2010

-0.1

0.0

0.1

0.2

Estimated Exchange Rate Misaligment

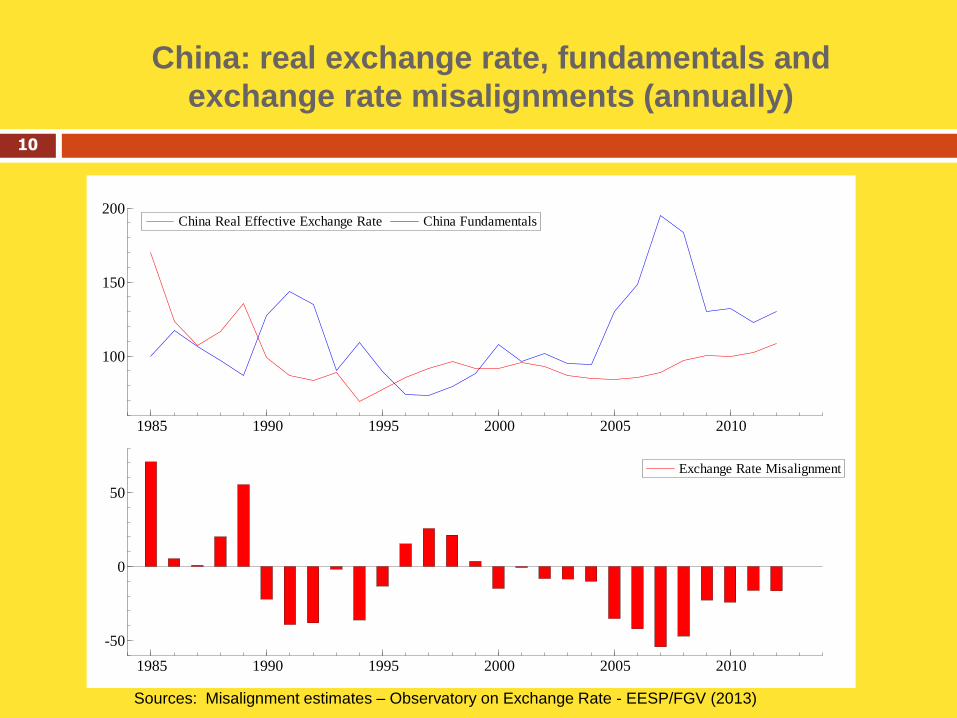

China: real exchange rate, fundamentals and

exchange rate misalignments (annually)

10

Sources: Misalignment estimates – Observatory on Exchange Rate - EESP/FGV (2013)

China Real Effective Exchange Rate China Fundamentals

1985 1990 1995 2000 2005 2010

100

150

200China Real Effective Exchange Rate China Fundamentals

Exchange Rate Misalignment

1985 1990 1995 2000 2005 2010

-50

0

50

Exchange Rate Misalignment

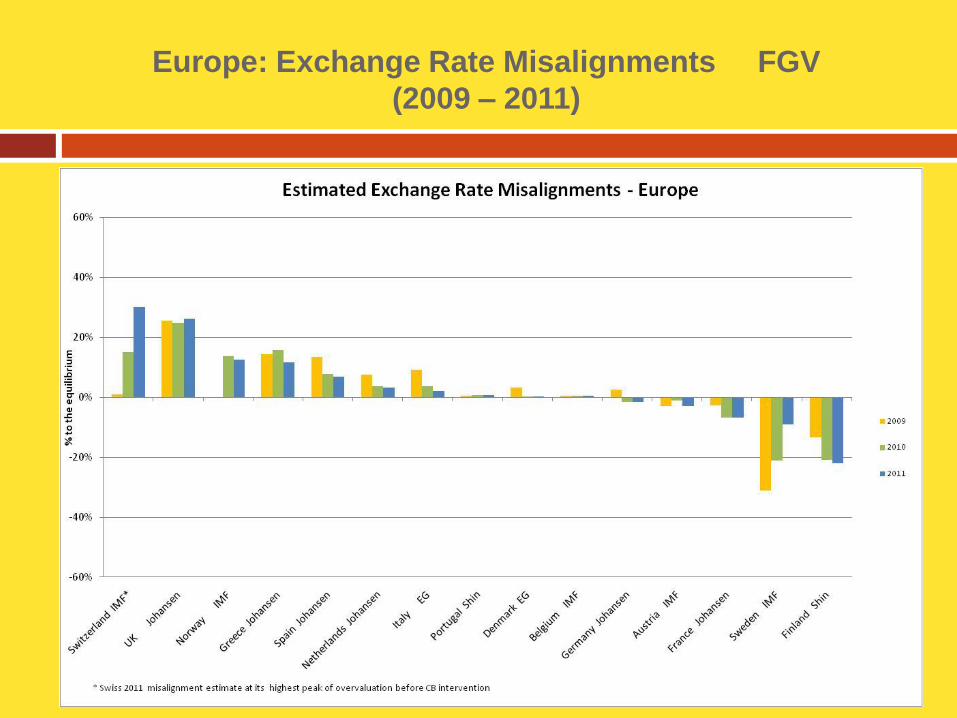

Europe: Exchange Rate Misalignments FGV

(2009 – 2011)

“Tariffication” of exchange rate misalignments

To exam the impact of exchange rate misalignments on trade, one possibility is to

transform a misaligment into a tariff and then to adjust the import tariff of each

country, through a “tariffication” exercise.

An overvalued exchange rate has the effect of reducing or nullifying the import tariffs

of the overvalued country, creating an incentive to imports from third countries.

An undervalued exchange rate, on the other hand, will give an incentive to exports

from the undervalued country. A country’s undervalued currency will have the effect

of increasing its import tariffs, sometimes above the bound levels at the WTO.

The equation used to “tarifficate” the effects of exchange rate misalignments is

presented in the next slide

Tariffication of Exchange Rates

13

Simulations regarding the effects of exchange rate

misalignments on selected Tariff Profiles

Using the “tariffication methodology”, one can represent the effects of exchange rate

misalignments on a country Tariff Profile.

The Tariff Profile is comprised of bound tariffs and applied tariffs

Bound tariffs are the tariffs negotiated at the WTO as the maximum permitted level of

an import tariff.

Applied tariffs are the import tariffs actually applied by a country and notified to the

WTO

After applying the “tariffication methodology” the results are adjusted bound and

applied tariffs that represent the actual level of protection of a given country.

In the following slides we present the simulations for Brazil, US and EU Tariff

Profiles, considering the effects of the exchange rate misalignments of selected

countries.

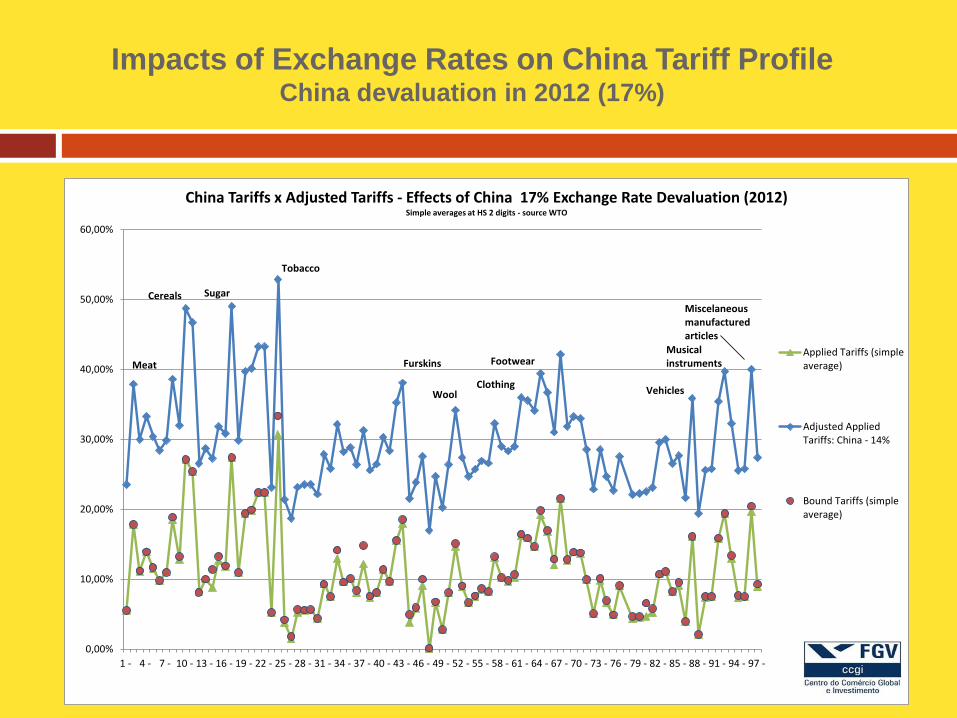

Impacts of Exchange Rates on China Tariff ProfileChina devaluation in 2012 (17%)

0,00%

10,00%

20,00%

30,00%

40,00%

50,00%

60,00%

1 - 4 - 7 - 10 - 13 - 16 - 19 - 22 - 25 - 28 - 31 - 34 - 37 - 40 - 43 - 46 - 49 - 52 - 55 - 58 - 61 - 64 - 67 - 70 - 73 - 76 - 79 - 82 - 85 - 88 - 91 - 94 - 97 -

China Tariffs x Adjusted Tariffs - Effects of China 17% Exchange Rate Devaluation (2012) Simple averages at HS 2 digits - source WTO

Applied Tariffs (simpleaverage)

Adjusted AppliedTariffs: China - 14%

Bound Tariffs (simpleaverage)

Cereals Sugar

Wool

Meat Footwear

Vehicles

Musical instruments

Miscelaneous manufactured articles

Furskins

Clothing

Tobacco

Impacts of Exchange Rates on China Tariff Profile

(2012)Ch-Brazil (37%), Ch-Germany (13%), Ch-US (12%) Bilateral

Misalignments

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

1 - 4 - 7 - 10 - 13 - 16 - 19 - 22 - 25 - 28 - 31 - 34 - 37 - 40 - 43 - 46 - 49 - 52 - 55 - 58 - 61 - 64 - 67 - 70 - 73 - 76 - 79 - 82 - 85 - 88 - 91 - 94 - 97 -

China Tariffs x Adjusted Tariffs - Effects of Selected Countries Exchange Rate Deviations (2012) Simple averages at HS 2 digits

Adjusted Applied Tariffs -effect of CH + BRdeviations - 37%

Adjusted Applied Tariffs -effect of GER + CHdeviations: 13%

Adjusted Applied Tariffs -effect of CH + USAdeviations: 12%

Bound Tariffs (simpleaverage)

Applied Tariffs (simpleaverage)

Brazilian exporter (2012)

American exporter

German exporter

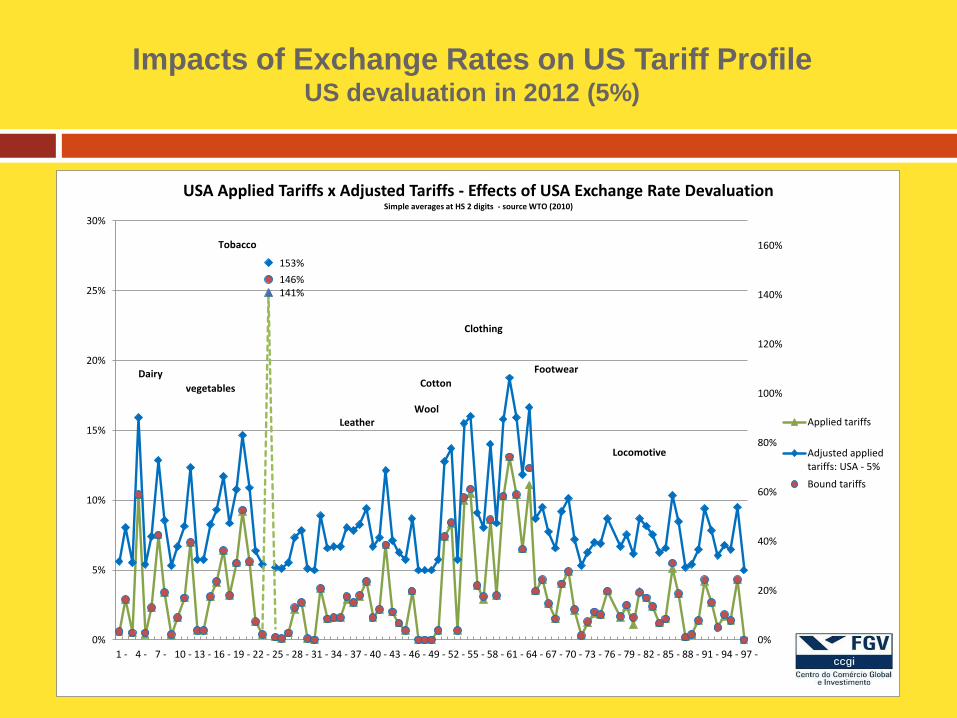

Impacts of Exchange Rates on US Tariff ProfileUS devaluation in 2012 (5%)

141%

153%

146%

0%

20%

40%

60%

80%

100%

120%

140%

160%

0%

5%

10%

15%

20%

25%

30%

1 - 4 - 7 - 10 - 13 - 16 - 19 - 22 - 25 - 28 - 31 - 34 - 37 - 40 - 43 - 46 - 49 - 52 - 55 - 58 - 61 - 64 - 67 - 70 - 73 - 76 - 79 - 82 - 85 - 88 - 91 - 94 - 97 -

USA Applied Tariffs x Adjusted Tariffs - Effects of USA Exchange Rate Devaluation Simple averages at HS 2 digits - source WTO (2010)

Applied tariffs

Adjusted appliedtariffs: USA - 5%

Bound tariffs

Dairy

Tobacco

vegetables

LeatherWool

Cotton

Clothing

Footwear

Locomotive

Impacts of Exchange Rates on US Tariff Profile (2012)US-Brazil (25%), US-Spain (9,5%), US-China (12%) Bilateral

Misalignments

-20%

-10%

0%

10%

20%

30%

40%

50%

1 - 4 - 7 - 10 - 13 - 16 - 19 - 22 - 25 - 28 - 31 - 34 - 37 - 40 - 43 - 46 - 49 - 52 - 55 - 58 - 61 - 64 - 67 - 70 - 73 - 76 - 79 - 82 - 85 - 88 - 91 - 94 - 97 -

USA Applied Tariffs x Adjusted Tariffs - Effects of Selected Countries Deviations (Article I)Simple averages at HS 2 digits - Except HS sector 24 (Tabacco)

Adjusted applied tariffs -effect of USA + BR: 25%

Adjusted applied tariffs -effect of USA + SPAIN:9,5%

Bound tariffs

Applied tariffs

Adjusted applied tariffs -effect of USA + CH: 12%

Dairy vegetables

Leather Wool

Cotton

ClothingFootwear

LocomotiveBrazilianexporter

Spanishexporter

Chineseexporter

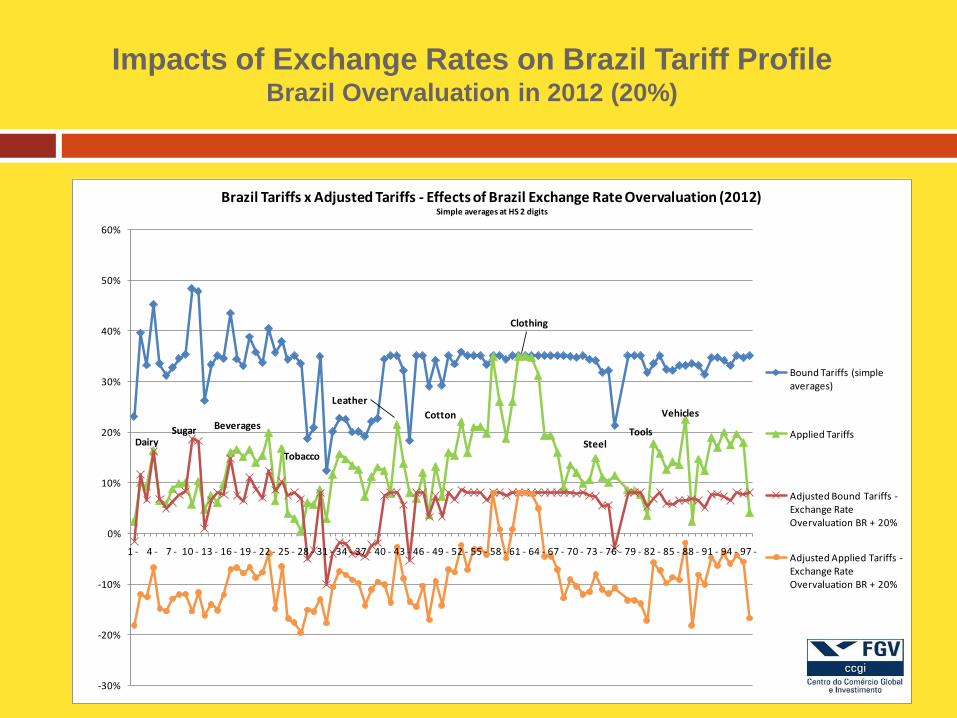

Impacts of Exchange Rates on Brazil Tariff ProfileBrazil Overvaluation in 2012 (20%)

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

1 - 4 - 7 - 10 - 13 - 16 - 19 - 22 - 25 - 28 - 31 - 34 - 37 - 40 - 43 - 46 - 49 - 52 - 55 - 58 - 61 - 64 - 67 - 70 - 73 - 76 - 79 - 82 - 85 - 88 - 91 - 94 - 97 -

Brazil Tariffs x Adjusted Tariffs - Effects of Brazil Exchange Rate Overvaluation (2012) Simple averages at HS 2 digits

Bound Tariffs (simple averages)

Applied Tariffs

Adjusted Bound Tariffs -Exchange Rate Overvaluation BR + 20%

Adjusted Applied Tariffs -Exchange Rate Overvaluation BR + 20%

DairySugar Beverages

Tobacco

Leather

Cotton

Clothing

SteelTools

Vehicles

20

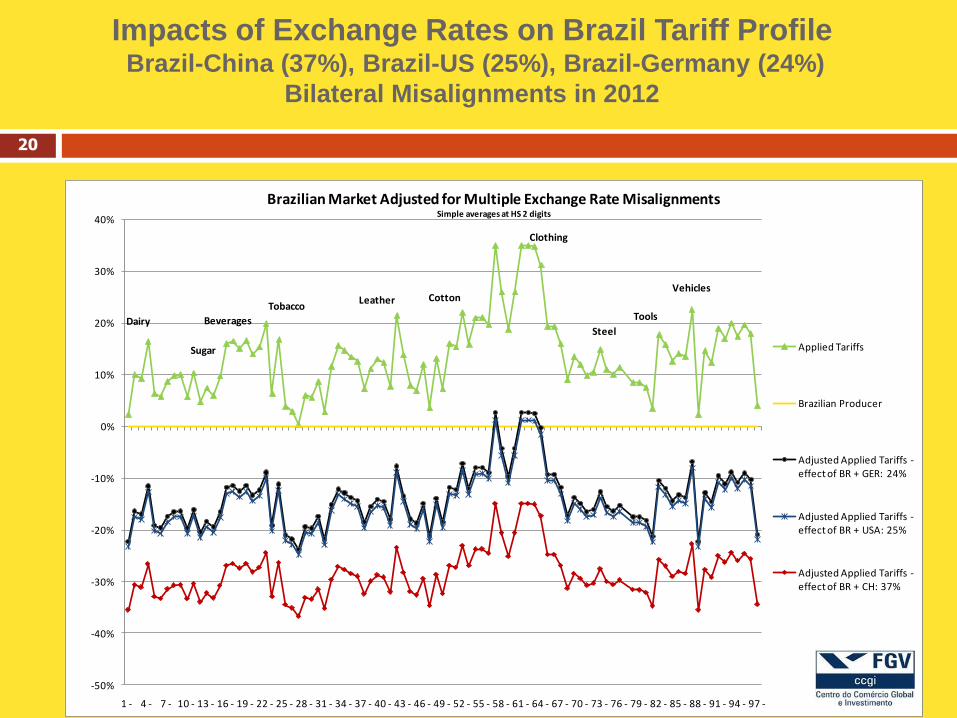

Impacts of Exchange Rates on Brazil Tariff ProfileBrazil-China (37%), Brazil-US (25%), Brazil-Germany (24%)

Bilateral Misalignments in 2012

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

1 - 4 - 7 - 10 - 13 - 16 - 19 - 22 - 25 - 28 - 31 - 34 - 37 - 40 - 43 - 46 - 49 - 52 - 55 - 58 - 61 - 64 - 67 - 70 - 73 - 76 - 79 - 82 - 85 - 88 - 91 - 94 - 97 -

Brazilian Market Adjusted for Multiple Exchange Rate Misalignments Simple averages at HS 2 digits

Applied Tariffs

Brazilian Producer

Adjusted Applied Tariffs -effect of BR + GER: 24%

Adjusted Applied Tariffs -effect of BR + USA: 25%

Adjusted Applied Tariffs -effect of BR + CH: 37%

Dairy

Sugar

Beverages

TobaccoLeather Cotton

Clothing

Steel

Tools

Vehicles

21

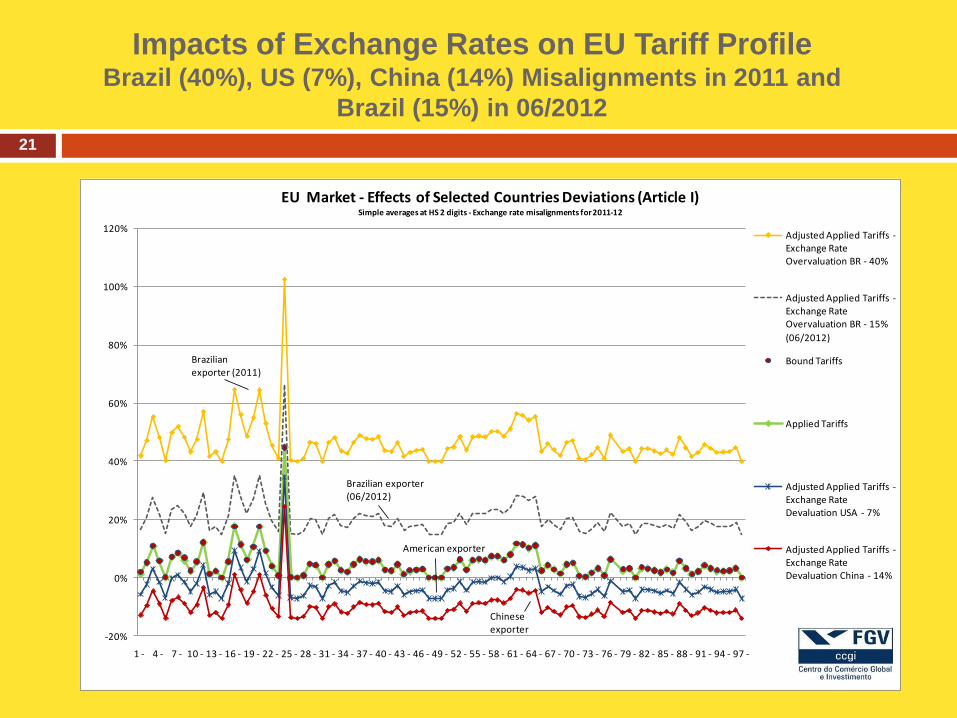

Impacts of Exchange Rates on EU Tariff ProfileBrazil (40%), US (7%), China (14%) Misalignments in 2011 and

Brazil (15%) in 06/2012

-20%

0%

20%

40%

60%

80%

100%

120%

1 - 4 - 7 - 10 - 13 - 16 - 19 - 22 - 25 - 28 - 31 - 34 - 37 - 40 - 43 - 46 - 49 - 52 - 55 - 58 - 61 - 64 - 67 - 70 - 73 - 76 - 79 - 82 - 85 - 88 - 91 - 94 - 97 -

EU Market - Effects of Selected Countries Deviations (Article I) Simple averages at HS 2 digits - Exchange rate misalignments for 2011-12

Adjusted Applied Tariffs -Exchange Rate Overvaluation BR - 40%

Adjusted Applied Tariffs -Exchange Rate Overvaluation BR - 15%

(06/2012)

Bound Tariffs

Applied Tariffs

Adjusted Applied Tariffs -Exchange Rate Devaluation USA - 7%

Adjusted Applied Tariffs -Exchange Rate Devaluation China - 14%

Brazilianexporter (2011)

Brazilian exporter (06/2012)

American exporter

Chineseexporter

Conclusions

- Countries with overvalued exchange rates (Brazil) have their

negotiated tariffs reduced or nullified.

- Countries with undervalued exchange rates (USA, China) grant

subsidies to their exports and their applied tariffs surpass the bound

levels agreed at the WTO.

- Substantial and persistent exchange rate misalignments significantly

affect or nullify most WTO rules:

tariffs, antidumping, countervailing measures, safeguards, rules of

origin, regional agreements, DSB retaliations…

- Problem:

the WTO does not have adequate rules to address the exchange rate

issue

22

IMF - manipulation (Article IV)

WTO - frustation (Article XV)

Solutions

General Agreement on Tariffs and Trade (GATT)

Article XV:4

Contracting parties shall not, by exchange action, frustrate* the

intent of the provisions of this Agreement, nor, by trade action, the

intent of the provisions of the Articles of Agreement of the

International Monetary Fund.

* Ad Article XV -Paragraph 4

The word “frustrate” is intended to indicate, for example, that infringements of the letter of any

Article of this Agreement by exchange action shall not be regarded as a violation of that Article if,

in practice, there is no appreciable departure from the intent of the Article. Thus, a contracting

party which, as part of its exchange control operated in accordance with the Articles of Agreement

of the International Monetary Fund, requires payment to be received for its exports in its own

currency or in the currency of one or more members of the International Monetary Fund will not

thereby be deemed to contravene Article XI or Article XIII. Another example would be that of a

contracting party which specifies on an import license the country from which the goods may be

imported, for the purpose not of introducing any additional element of discrimination in its import

licensing system but of enforcing permissible exchange controls.

WTO Rules relating trade and exchange rates

General Agreement on Tariffs and Trade (GATT)

Article II:6

(a) The specific duties and charges included in the Schedules relating to contracting

parties members of the International Monetary Fund, and margins of preference in

specific duties and charges maintained by such contracting parties, are expressed

in the appropriate currency at the par value accepted or provisionally

recognized by the Fund at the date of this Agreement. Accordingly, in case this

par value is reduced consistently with the Articles of Agreement of the

International Monetary Fund by more than twenty per centum, such specific

duties and charges and margins of preference may be adjusted to take

account of such reduction; provided that the CONTRACTING PARTIES (i.e., the

contracting parties acting jointly as provided for in Article XXV) concur that such

adjustments will not impair the value of the concessions provided for in the

appropriate Schedule or elsewhere in this Agreement, due account being taken of all

factors which may influence the need for, or urgency of, such adjustments.

Rules relating between exchange rates and trade

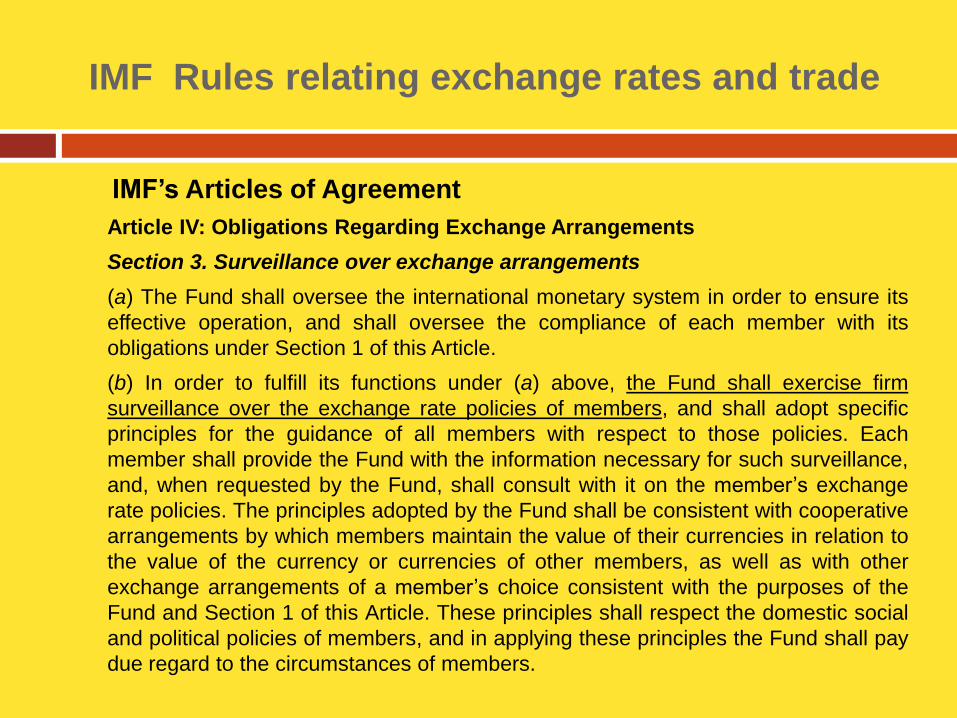

IMF’s Articles of Agreement

Article IV: Obligations Regarding Exchange Arrangements

Section 1. General obligations of members

Recognizing that the essential purpose of the international monetary system is to provide a

framework that facilitates the exchange of goods, services, and capital among countries, and that

sustains sound economic growth, and that a principal objective is the continuing development of

the orderly underlying conditions that are necessary for financial and economic stability, each

member undertakes to collaborate with the Fund and other members to assure orderly exchange

arrangements and to promote a stable system of exchange rates. In particular, each member

shall:

(i) endeavor to direct its economic and financial policies toward the objective of fostering orderly

economic growth with reasonable price stability, with due regard to its circumstances;

(ii) seek to promote stability by fostering orderly underlying economic and financial conditions and

a monetary system that does not tend to produce erratic disruptions;

(iii) avoid manipulating exchange rates or the international monetary system in order to prevent

effective balance of payments adjustment or to gain an unfair competitive advantage over other

members; and

(iv) follow exchange policies compatible with the undertakings under this Section

IMF Rules relating exchange rates and trade

GATT Guideliness to Art II.6(a) (Approved

by CP)

15 February 1980 (L/4938)

Assume a World with different exchange rate arrangements

. Allow undervalued countries to renegotiate especific tariffs

. CP ask IMF to calculate size of depretiation

. Undervaluation was more than 20%

. Basket of currencies of 85% of imports

. Period of analysis for size of depreciation:

rate of 6 months preciding the request x 6 months

preceding last bound (weighted avarage)

IMF’s Articles of Agreement

Article IV: Obligations Regarding Exchange Arrangements

Section 3. Surveillance over exchange arrangements

(a) The Fund shall oversee the international monetary system in order to ensure its

effective operation, and shall oversee the compliance of each member with its

obligations under Section 1 of this Article.

(b) In order to fulfill its functions under (a) above, the Fund shall exercise firm

surveillance over the exchange rate policies of members, and shall adopt specific

principles for the guidance of all members with respect to those policies. Each

member shall provide the Fund with the information necessary for such surveillance,

and, when requested by the Fund, shall consult with it on the member’s exchange

rate policies. The principles adopted by the Fund shall be consistent with cooperative

arrangements by which members maintain the value of their currencies in relation to

the value of the currency or currencies of other members, as well as with other

exchange arrangements of a member’s choice consistent with the purposes of the

Fund and Section 1 of this Article. These principles shall respect the domestic social

and political policies of members, and in applying these principles the Fund shall pay

due regard to the circumstances of members.

IMF Rules relating exchange rates and trade

- Create a world currency

- Negotiate a fluctuation band

- Solve the conflict bilaterally

A NEW PROPOSAL

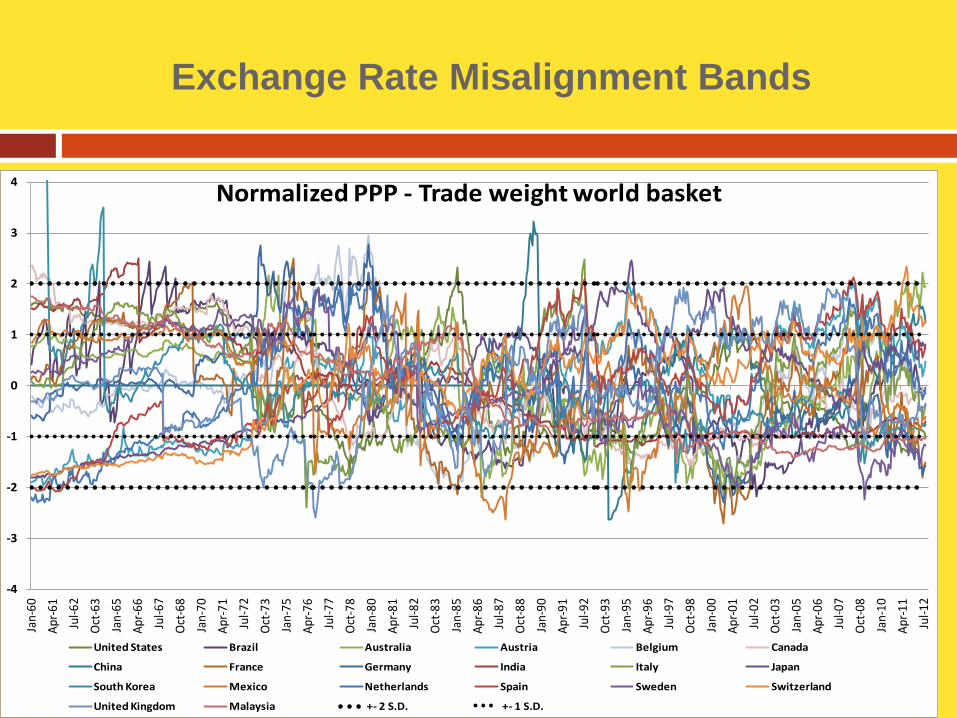

Exchange Rate Misalignment Bands

-4

-3

-2

-1

0

1

2

3

4

Jan-

60

Apr

-61

Jul-6

2

Oct

-63

Jan-

65

Apr

-66

Jul-6

7

Oct

-68

Jan-

70

Apr

-71

Jul-7

2

Oct

-73

Jan-

75

Apr

-76

Jul-7

7

Oct

-78

Jan-

80

Apr

-81

Jul-8

2

Oct

-83

Jan-

85

Apr

-86

Jul-8

7

Oct

-88

Jan-

90

Apr

-91

Jul-9

2

Oct

-93

Jan-

95

Apr

-96

Jul-9

7

Oct

-98

Jan-

00

Apr

-01

Jul-0

2

Oct

-03

Jan-

05

Apr

-06

Jul-0

7

Oct

-08

Jan-

10

Apr

-11

Jul-1

2

Normalized PPP - Trade weight world basket

United States Brazil Australia Austria Belgium Canada

China France Germany India Italy Japan

South Korea Mexico Netherlands Spain Sweden Switzerland

United Kingdom Malaysia +- 2 S.D. +- 1 S.D.

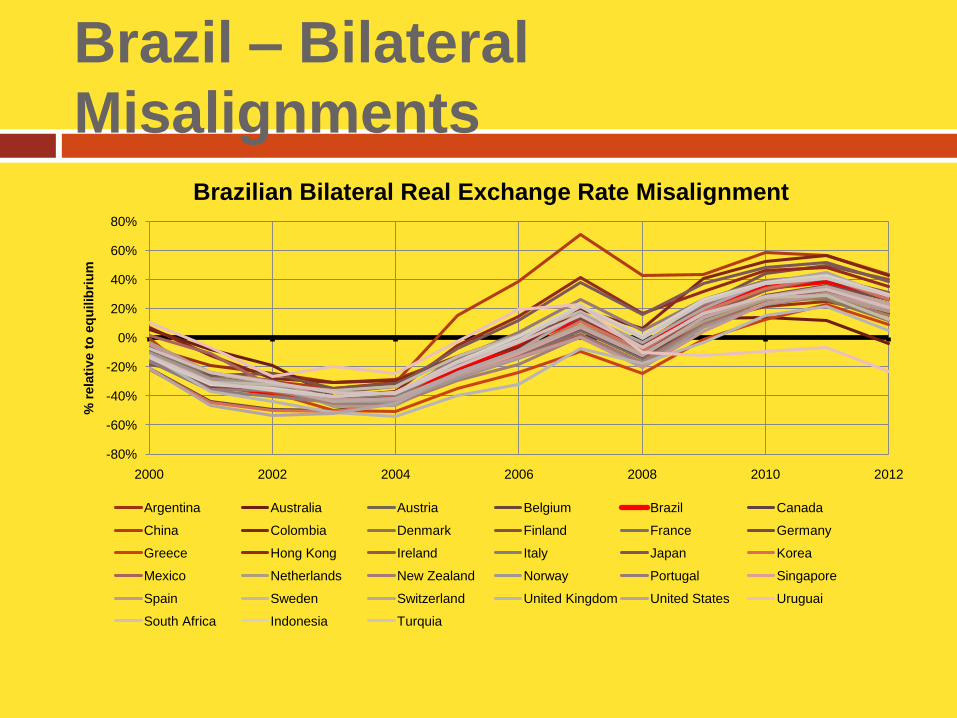

Brazil – Bilateral

Misalignments

-80%

-60%

-40%

-20%

0%

20%

40%

60%

80%

2000 2002 2004 2006 2008 2010 2012

% r

ela

tiv

e t

o e

qu

ilib

riu

m

Brazilian Bilateral Real Exchange Rate Misalignment

Argentina Australia Austria Belgium Brazil Canada

China Colombia Denmark Finland France Germany

Greece Hong Kong Ireland Italy Japan Korea

Mexico Netherlands New Zealand Norway Portugal Singapore

Spain Sweden Switzerland United Kingdom United States Uruguai

South Africa Indonesia Turquia

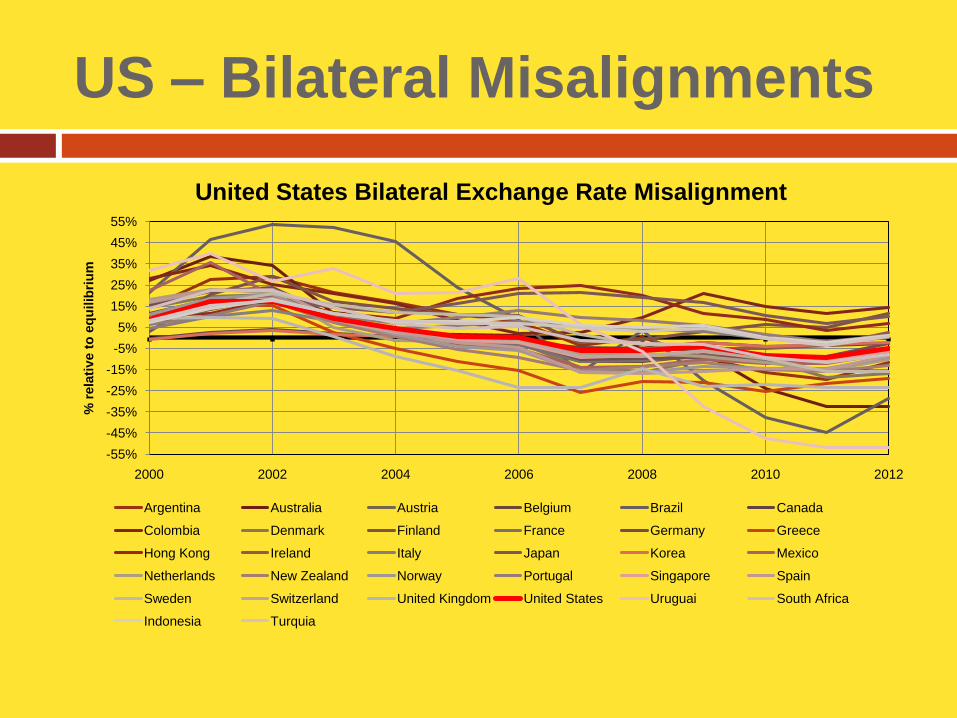

US – Bilateral Misalignments

-55%

-45%

-35%

-25%

-15%

-5%

5%

15%

25%

35%

45%

55%

2000 2002 2004 2006 2008 2010 2012

% r

ela

tiv

e t

o e

qu

ilib

riu

m

United States Bilateral Exchange Rate Misalignment

Argentina Australia Austria Belgium Brazil Canada

Colombia Denmark Finland France Germany Greece

Hong Kong Ireland Italy Japan Korea Mexico

Netherlands New Zealand Norway Portugal Singapore Spain

Sweden Switzerland United Kingdom United States Uruguai South Africa

Indonesia Turquia

Substantial and persistent exchange rate misalignments affect the

effectiveness of trade instruments negotiated at the WTO. Therefore,

they must be object of WTO regulation

Juridical concept of time x economic concept of time

(time of violation x time for long run equilibrium)

In summary:

The WTO must address the effects of exchange rate misalignments or

misaligned exchange rates will turn the WTO into a juridical and

economic fiction !!!

33

Conclusions