Excellence In Integrated Reporting Awards 2013 -...

32

EY’s Excellence in Integrated Reporting Awards 2013 A survey of integrated reports from South Africa’s top 100 JSE listed companies and top 10 state owned companies.

Transcript of Excellence In Integrated Reporting Awards 2013 -...

EY’s Excellence in Integrated Reporting Awards 2013A survey of integrated reports from South Africa’s top 100

JSE listed companies and top 10 state owned companies.

EY’s Excellence in Integrated Reporting AwardsA survey of integrated reports from South Africa’s top 100

JSE listed companies and top 10 state owned companies. 2013

Contents

Foreword 1

Interview with our Global CEO and Chairman, Mark Weinberger, member of the IIRC 3

2013 rankings 5

General impressions and overall performance 7

The mark plan and adjudication process 13

Feedback on the top 10 companies 19

Practical evolution of integrated reporting and the impact of the IIRC Consultation Draft on future reporting in South Africa 24

EY contacts

The purpose of the survey

The purpose of this survey is to encourage excellence in the quality of integrated reporting to investors and other stakeholders by South Africa’s top companies and state-owned entities.

Benchmarking

Each year, EY offers all listed companies and state-owned entities an opportunity to obtain a detailed analysis of their integrated reports. The integrated reports are reviewed using guidelines from the Excellence in Integrated Reporting survey and a benchmarking report is issued. The report contains practical suggestions and comments that can be used to improve the quality of future reports by the company. The recommendations in the report relate not only to the accounting and financial information contained in the integrated report, but also to the non-financial data that is used by analysts in assessing the company’s performance. The benchmarking report is prepared either by the adjudicators or by members of the EY Professional Practice Group.

Companies wishing to obtain a benchmark report on their company’s integrated report can contact Mary-Anne Donachie on +27 (0) 11 772 3034 or [email protected]

For more information on this survey, contact Larissa Clark, Director in the EY Professional Practice Group, on +27 (0) 11 772 3094 or [email protected]

Disclaimer

The views expressed in this report are those of the College of Accounting at the University of Cape Town and not of EY.

Foreword

EY’s Excellence in Integrated Reporting Awards 20131

Forewordby Larissa Clark and Jeremy Grist

We are excited to announce the results of the second EY Excellence in Integrated Reporting Awards. It is clear, looking at the quality of the integrated reports assessed, that South Africa has made significant progress in addressing the challenges faced by integrated reporting. Companies continue to set a higher standard than before.

Integrated reporting, as a concept, has evolved internationally over the last year through the work of the International Integrated Reporting Council (IIRC). In South Africa, we have seen significant growth and innovation as companies have made significant strides in their integrated reporting journeys.

From the results, it is clear that most of the companies that performed well in this survey in 2012 continued to perform well in 2013. This emphasizes the fact that integrated reporting is a journey, and early adopters are realizing the benefit thereof as the concept grows and develops.

There is, however, still work to be done and challenges to be overcome to achieve the “perfect” integrated report; one that reflects the true value, output and outcomes created by organizations.

We hope that, by continuing this survey, we continue to encourage companies to improve the standard of their integrated reporting, further encourage integrated thinking and provide good examples from which others can learn.

Larissa Clark

Director | Assurance Professional Practice Group

Jeremy Grist

Director | Climate Change and Sustainability Services

“What I do know is that our current economic system has not yet enabled us to properly value a company’s environmental, social and governance assets. The price on natural and other non-financial capitals does not reflect the importance of maintaining them and the market has not yet been sent the right signals. There is also a need to ensure that all parties work together on defining common valuation principles for economic capital and non-financial assets, liabilities and externalities, so as to agree on a meaningful way to report non-financial data and the value placed on it. Only then will we move a step closer toward that elusive goal of a truly sustainable and transparent economy.”

Christian Mouillon, Global Risk Leader

EY’s Excellence in Integrated Reporting Awards 2013 2

Interview with our Global CEO and Chairman

1. Why do you believe that integrated reporting is an

important evolution in corporate reporting?

There are two drivers that have helped Integrated Reporting gain momentum. First, the global financial crisis called into question the current corporate reporting regime. Namely, whether it’s giving global market participants and other stakeholders a comprehensive view of a company’s value creation and performance over the short, medium and long term and, importantly, whether a new reporting model could provide more balance. Second, the issue of sustainability is increasingly at the forefront of stakeholder concerns – driven by cost pressures, consumer preference and regulation. In my view, these two shifts are combining to drive the debate around Integrated Reporting and its potential to help stakeholders make better informed decisions on capital allocation and other matters.

2. What is your view on some of the challenges associated

with Integrated Reporting? How might these challenges

start to be addressed?

Before looking at the challenges, I’d like to say that I see Integrated Reporting as a means to simplify and harmonize current reporting, but there are naturally challenges associated with bringing a new dimension to the traditional reporting regime – both for companies and the IIRC.

Companies will need to put an infrastructure in place to address the requirements of Integrated Reporting – that will, of course, bring its own challenges. An important step in helping companies to meet these challenges will be the

development of the IIRC’s Framework and its field testing through the Pilot Programme. Clearly explaining the process of Integrated Reporting, what it entails and the expected outcomes will be key to establishing its credibility – as will explaining and defining the concepts at its core.

Developing a Framework that does this means that the IIRC itself faces the challenge of bringing together different reports; developing a common language, definitions and consistent measurement principles and metrics. Drawing on the knowledge and experience of other global standard setters, such as the International Accounting Standards Board and the Global Reporting Initiative, will be fundamental to the Framework’s success and relevance. Also, if the Integrated Report becomes a company’s main report, investors and other stakeholders will expect it to be subject to independent assurance. The IIRC will need to work with the International Auditing and Assurance Standards Board to review the Framework before it’s finalized in order to head off any potential auditability issues.

Finally, integrated reporting can’t be just another report on top of all that is done now. What it replaces is an important issue to explore.

3. What are the benefits of Integrated Reporting?

By encouraging a different way of thinking, Integrated Reporting seeks to advance a more sustainable global economy. Its fundamental premise is that, by taking a broader view of a company’s strategy, governance and performance prospects, and by helping to show the interdependencies between them, Integrated Reporting can help global market participants and other stakeholders to make better-informed decisions around investment and resource allocation. This in turn helps support value creation over the long term, as well as in the short to medium term. This takes some of the focus and pressure off short-term, quarter-to-quarter results. In addition, a comprehensive view of value creation and performance should help to promote integrated thinking and decision-making within an organization – enhancing accountability and fostering a culture of stewardship.

Interview with our Global CEO and Chairman, Mark Weinberger

Mark Weinberger is EY’s Global CEO and Chairman, and is also a member of the International Integrated Reporting Council

integrated reporting globally.

EY’s Excellence in Integrated Reporting Awards 20133

4. What are your reflections on the interplay between

Integrated Reporting and a company’s strategy going

forward?

As a new dimension to traditional reporting, Integrated Reporting will, by its nature, promote organizational change within a company. On an operational level, it should demand a more integrated approach to decision-making and accountability. On a strategic level, it could drive decision-making that systematically takes into consideration the future value of a company’s sustainable business activities.

From an Integrated Reporting perspective, value is created by aligning strategy with internal resources, such as financial capital, and external resources – such as environmental services and access to public infrastructure, for example. An integrated report should identify all the resources an organization requires to create value over time, even if they belong to society as a whole and it has free access to them.

Doing so reflects the Integrated Reporting ethos that value is co-created and shared between the organization and the community in which it operates.

5. Do you think the investment community understands

the value of Integrated Reporting and will use

integrated reports as a basis for decision-making?

As a new concept, it will take time for the investment community to become more familiar with the value and benefits of Integrated Reporting. Integrated Reporting is a concept that is gaining momentum, but there’s work to be done around helping the investment community to better understand the information communicated through the Integrated Report in the context of long-term performance, resource sustainability and governance.

6. What role do you think firms such as EY can play in

Integrated Reporting?

An important one, I think. Our organization is involved in a number of ways – thought leadership is one. We’ve just published a survey of integrated reports from South Africa’s top 100 companies and top 10 state-owned companies, for example. Our aim in publishing surveys such as this is to encourage excellence in the quality of Integrated Reporting.

We also contribute to the development of the Integrated Reporting Framework through our involvement with the IIRC. I became a member of the IIRC this March, succeeding James Turley, our outgoing Chairman and CEO, who had been a member of IIRC since its inception. My colleague Philippe Peuch Lestrade was appointed as Deputy CEO of the IIRC in 2012, and there are many other people from across EY who contribute as members of the IIRC’s Working Group in developing the Framework, or by drafting papers or on secondment.

We also encourage all stakeholders to get involved with the debate – by responding to the IIRC’s invitation to comment on the Framework, for example.

Perhaps most importantly, we play a very practical role in our day-to-day work with clients – advising them on how to make the transition from traditional reporting to integrated reporting, how to shape the content of their Integrated Report or through assurance of materials, to name just a few examples.

7. What value does the EY Excellence in Integrated

Reporting Awards add to companies?

It helps to encourage excellence by promoting best practice in Integrated Reporting, and it shines a light on those doing well. But it goes beyond publicity. We also offer all listed companies and state-owned entities included in the awards (and supporting survey) an opportunity to obtain a detailed analysis of how their integrated reports are rated against best practice. Included are practical suggestions and comments that can be used to improve the quality of future reports – relating not only to accounting and financial information, but also to the non-financial data that’s used by analysts in assessing performance. It’s the analysis that sits behind the award that drives value for companies, as well as the benefit of being showcased by the awards and survey itself.

EY’s Excellence in Integrated Reporting Awards 2013 4

2013 rankings

Top 1

0

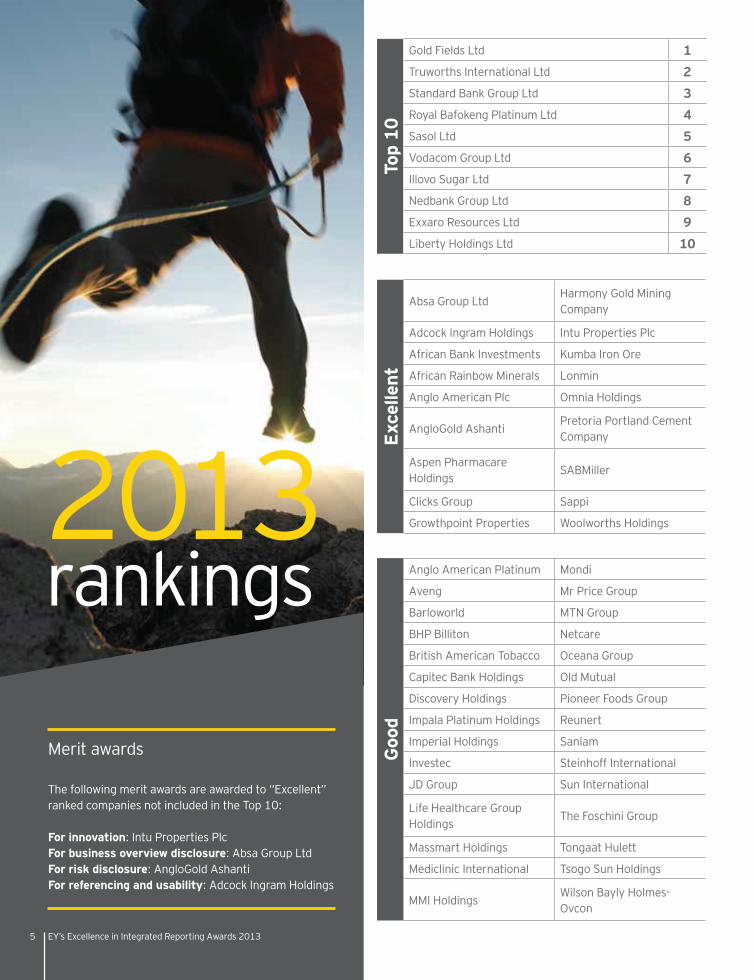

Gold Fields Ltd 1

Truworths International Ltd 2

Standard Bank Group Ltd 3

Royal Bafokeng Platinum Ltd 4

Sasol Ltd 5

Vodacom Group Ltd 6

Illovo Sugar Ltd 7

Nedbank Group Ltd 8

Exxaro Resources Ltd 9

Liberty Holdings Ltd 10

Excellent

Absa Group LtdHarmony Gold Mining Company

Adcock Ingram Holdings Intu Properties Plc

African Bank Investments Kumba Iron Ore

African Rainbow Minerals Lonmin

Anglo American Plc Omnia Holdings

AngloGold AshantiPretoria Portland Cement Company

Aspen Pharmacare Holdings

SABMiller

Clicks Group Sappi

Growthpoint Properties Woolworths Holdings

Good

Anglo American Platinum Mondi

Aveng Mr Price Group

Barloworld MTN Group

BHP Billiton Netcare

British American Tobacco Oceana Group

Capitec Bank Holdings Old Mutual

Discovery Holdings Pioneer Foods Group

Impala Platinum Holdings Reunert

Imperial Holdings Sanlam

Investec Steinhoff International

JD Group Sun International

Life Healthcare Group Holdings

The Foschini Group

Massmart Holdings Tongaat Hulett

Mediclinic International Tsogo Sun Holdings

MMI HoldingsWilson Bayly Holmes-Ovcon

EY’s Excellence in Integrated Reporting Awards 20135

Merit awards

The following merit awards are awarded to “Excellent” ranked companies not included in the Top 10: For innovation: Intu Properties Plc For business overview disclosure: Absa Group Ltd For risk disclosure: AngloGold Ashanti For referencing and usability: Adcock Ingram Holdings

SO

Cs

Excellent:

EskomIndustrial Development Corporation of SA Ltd

Transnet

Good:

Development Bank of SA

Average:

SA Post Office

Progress to be made:

Airports Company of South Africa

SAA

Central Energy FundTrans-Caledon Tunnel Authority

Landbank

Avera

ge

Acucap Properties KAP Industrial Holdings

AECI Murray & Roberts Holdings

Assore Nampak

The Bidvest Group Naspers

Brait SE Pick ‘n Pay Stores

Capital & Counties Properties Redefine Properties

Coronation Fund Managers Remgro

DatatecResilient Property Income Fund

Distell GroupSA Corporate Real Estate Fund

FirstRand Santam

Fountainhead Property Trust Telkom SA

Grindrod Tiger Brands

Hyprop Investments Arcelormittal South Africa

Pro

gre

ss t

o b

e m

ade

Afrox PSG Group

AVIRand Merchant Insurance Holdings

Capital Property Fund Reinet Investments

Caxton and CTP Publishers and Printers

RMB Holdings

Compagnie Financiere Richemont SA

Shoprite Holdings

Hosken Consolidated Investments

SPAR

New Europe Property Investments

Trencor

Northam Platinum Uranium One

EY’s Excellence in Integrated Reporting Awards 2013 6

General impressions

The integrated reports produced by the top 100 JSE-listed companies during 2012 can generally be classified as falling into one of three different categories. Firstly, there are those companies that have clearly embraced the process of integrated reporting and have produced a concise document that explains how their strategy, governance, performance and prospects, in the context of their external environment, will lead to the creation of sustainable value over the short, medium and long term. These are the integrated reports that have been ranked as “Excellent” or “Good.” Secondly, there are those companies that have taken a “business-as-usual” approach and have produced reports that include some elements of what is required in an integrated report, but have not achieved what The King Code of Corporate Governance Principles for South Africa 2009 (King III) describes as being ‘a holistic’ and integrated representation of the company’s performance in terms of both its finance and sustainability.” These integrated reports have been ranked as “Average.” Lastly, there are those reports that either make no claim to being an integrated report or that include so few of the elements that one would expect within an integrated report that they can only be ranked as “Progress to be made.”

It is quite clear that the title of the report does not necessarily reflect the reporting approach followed. Many dual-listed companies still produce an annual report, yet report in such a way that many of the goals of integrated reporting are achieved. Conversely, a number of local companies produce what they call an integrated report, but which contains very little of what we would expect within a true integrated report.

reports, we found that approximately

companies are making a serious effort to adopt the concept of integrated reporting. Approximately half of these companies produced an integrated report, which the adjudicators considered to be “Excellent.”

General impressions and overall performance by Professor Mark Graham

EY’s Excellence in Integrated Reporting Awards 20137

The preparers of integrated reports who have embraced the concept of integrated reporting have made significant strides in improving the quality of their 2012 integrated reports. A notable development in integrated reporting during 2012 is the increase in the diversity of the structure of the reports, and we enjoyed some of the novel and innovative approaches that were used. This is clear evidence that preparers are attempting to tell the story of their business in a way that reflects its particular and unique aspects, rather than follow a standardized “boilerplate” format. There has been some experimentation with the structure and format of the integrated report and, as with any experiment, some outcomes are more successful than others. We hope, however, that preparers will continue to try new and innovative ways in which to explain, in a crisp and concise manner, their company’s unique value-creation story.

A further development during 2012 is the increasing extent to which information is referred to, but not included, in the integrated report. This is linked to the way in which more companies are clearly distinguishing between the integrated report(their primary report)’ and the other reports in their reporting suite. Many more companies have now chosen to include only abridged or summarized financial statements within their integrated report, as is now allowed by the Companies Act (no. 71 of 2008), with the full annual financial statements being available elsewhere. Similarly, many companies have removed the detailed sustainability and corporate governance information from their integrated report and made this available online.

In most cases, this information is cross-referenced from the integrated report and has resulted in the integrated reports becoming more crisp and concise. We also noticed that companies are getting better at using navigation aids, icons and other forms of cross-referencing to connect information across the report, and thereby improve integration. Once again, in some instances, this experimentation perhaps may have gone too far, for example, when information that clearly should remain within the integrated reported is removed and placed online.

In at least one instance, the discussion of risks that will affect the businesses ability to create value was placed online and, in a number of cases, we were surprised to see that companies had elected to include the individual director’s remuneration in the online statutory financials, with only limited discussion and no individual details in the integrated report. While this might not be financially material, the disclosure of the factors that affect variable remuneration and the actual amount of the variable remuneration provides far more useful information about the priorities of management and the governance of the organization than the rand value might suggest.

Many companies are still struggling to strike a balance between the traditional annual report that comprises the chairman’s and CEO’s reports, financial statements, a sustainability report, divisional reviews, and some forward- looking information and presenting an integrated report that “tells a story” of how the business uses its stock of capitals to create value in the short, medium and long term.

EY’s Excellence in Integrated Reporting Awards 2013 8

General impressions

Many of the more highly rated integrated reports achieved this in 2012 by structuring their reports around what is important to the entity. In some cases, this was successfully done by structuring reports around different groups of stakeholders, with information on that group of stakeholders being clearly identified. This is not to suggest that the intention of the integrated report is to report to that group of stakeholders, but that information about various stakeholder groups, such as employees and customers, is important to an investor. Two companies in particular structured their report around the new concept of “capitals” (i.e., financial, manufactured, intellectual, human, social and relationship, and natural) that appeared in the integrated reporting discourse during 2012. While it is unlikely that companies will need to specifically use this terminology in their integrated reports, an explanation of how value is created within an organization can sensibly be structured around how value is embodied in the capitals that it uses.

While there has been much improvement in the structure of the integrated report, many companies still appear to interpret integrated reporting as being environmental reporting or sustainability reporting combined with financial reporting. There also appears to be a tendency among some companies to disclose non-financial indicators, because they are available without considering how material they are to the business. Indicators of how “green” a company is in its operations are only relevant if the measures, such as recycling, carbon emissions, etc., are material to the company.

We were pleased to see significant improvements in the introductory section of the integrated report. Many more companies are now including a prominent endorsement of the integrated report by the directors, and also outlining the scope and boundary of the report. However, there is sometimes a lack of clarity in the way in which scope and boundary issues have been dealt with.

EY’s Excellence in Integrated Reporting Awards 20139

EY’s Excellence in Integrated Reporting Awards 2013 10

For example, a comment along the lines of “on the same basis as IFRS” does not make it clear the extent to which the information of, for example, a joint venture is included. As this would be equity accounted, does that imply that none of the emissions, staff, etc. are included, or does it imply that 40% are included, or perhaps 100%? The disclosure of the extent to which various aspects of the integrated report has been independently assured is an area that could be improved by many companies.

Very few companies discussed the way in which integrated reporting is essentially the outcome of integrated thinking within the business, and we wonder whether companies could improve the way in which they communicate the objective of this new reporting format to their stakeholders. Another area where many integrated reports could benefit from improvement is by including an explanation of how materiality has been determined. This explanation should include an explanation of how material matters have been identified, how the importance of these matters has been assessed and how the material matters have been prioritized. In many integrated reports, the question of materiality has been simply explained with a brief general comment, such as “material issues are identified by the Board.”

We continue to believe that the first 20 or so pages of an excellent integrated report should convey the key information that the reader needs to understand about the philosophy of the business, the context within which it operates, the strategy of the business, the material issues (financial and non-financial) that affect the business, key performance indicators (KPI’s) and the risks that affect the business. This key information is then cross-referenced to other areas of the integrated report, other reports or online content, where the reader can find more detailed information.

The risk disclosures in integrated reports continue to improve, and we were pleased to see discussions of the processes for identifying, managing and mitigating risks that might affect the ability of the organization to create value. In some cases, the risk section of the integrated report merely lists the main or generic risks facing the business, and we would suggest that this does not go far enough to help the reader’s understanding of the risk profile of the business.

In addition to an explanation of the risk management process, we found that those integrated reports that defined, explained and prioritized risks, and perhaps used some form of “heat map” to categorize the intensity of the various risks, extremely informative. The better reports also linked strategy with risk and included some explanation as to whether risks had been reassessed since the prior period.

One area where many integrated reports fall short is in their ability to give equal prominence to both the “good” and the “bad” news. A number of integrated reports continue to include a “highlights” section near the front of the report that lists the company’s achievements during the year in a way that is simply a public relations exercise and which highlights only the positive achievements.

The guiding principles for integrated reporting clearly emphasize that the report should give equal prominence to all material information, both positive and negative, and we believe that this principle should inform the choice of information that is going to be included in any “highlights” presented.

A far better “highlights” presentation would be to summarize the achievements an organization has made with respect to its KPI’s.

General impressions

Stakeholder responsiveness is an area that is generally poorly handled. While it is debatable who the target audience of the integrated report may be, it would be useful if companies were clearer as to whom they were targeting, as opposed to making bland and generic statements about their stakeholders. What we would expect to see is greater insights into the organization’s relationship with its key stakeholders, and how and to what extent the organization takes into account and responds to their legitimate needs, interests and expectations.

A key principle of integrated reporting is identifying those factors that are most material to the organization and reporting on those. Although we have observed an increase in the number and variety of non-financial indicators presented, the usefulness of many of those indicators needs to be questioned. Furthermore, many non-financial indicators are currently presented without any context, thereby making any meaningful interpretation difficult. Disclosure of these non-financial indicators can be improved by providing measures per unit produced or consumed, as well as providing industry norms or best practice in the industry, in order to make the information more decision useful. Furthermore, while there has been an increase in the number of non-financial indicators that have been subject to some form of external assurance, this is off a very low base. Consideration should be given to that non-financial indicators are most material to the long-term sustainability of the business, in which case, management that are presumably relying on those indicators will have a better business case for incurring the costs attached to independent assurance of those indicators.

EY’s Excellence in Integrated Reporting Awards 201311

EY’s Excellence in Integrated Reporting Awards 2013 12

If management feels that it is not worth getting an indicator independently assured, one has to question how material that indicator is to the future ability of the entity to generate value and, if it is not material, the question is then raised as to why it is being disclosed in the integrated report. Indicators that may be of interest to only certain stakeholders should be reported elsewhere.

It appears that more thought is being given to presenting information in a more meaningful and understandable manner, particularly in relation to financial information.

Increasing use is being made of graphs that reflect inter-relationships and trends over time and, in particular, we noticed an increased use of waterfall graphs that explain the factors that influence the movement in key measures (e.g., profit) from year to year and thereby provide added financial insight into the business.

Only a few companies provide a useful summary of their key accounting policies, accounting assumptions and estimates that are used in preparing their financial statements. Most continue to provide extensive “boilerplate” disclosure of these items, and we believe that this is an area where most integrated reports could be improved.

The remuneration of executive directors is an area that continues to be poorly handled by most companies. In most cases, there is very little information or no clear indication how the variable portion of short-term bonuses are determined.

In some cases where the KPIs that determine bonuses are discussed, there is seldom any indication of how indicators translate into the rand amounts of the bonuses actually awarded. It is also not always clear as to whether the amounts disclosed are payments in respect of previous periods or accruals for current periods. Furthermore, much of the directors’ remuneration information is often extremely convoluted, and thereby loses any value that the user might have gained from it. While we are not suggesting that the detailed remuneration information should not be given, we suggest that the remuneration information that is presented in the integrated report be clear, concise and easily understandable by the reader.

Overall, we were pleased to see that the majority of the top 100 companies listed on the JSE are making progress on the journey toward producing an integrated report that complies with the spirit of King III and the developing guidance that is being provided by the IIRC. Although this reporting format is in a formative stage, it is quite clear that companies that wish to improve their integrated report have some excellent local examples against which they can benchmark their own reports. It should probably also be said that, although those companies with integrated reports that have been highly rated in this survey, i.e., those integrated reports that are ranked Excellent, there are none that are at a stage where they can say that they now have an integrated report that cannot be improved.

The mark plan and adjudication process

The mark plan and adjudication process by Professor Mark Graham

Choosing the companies

The companies included in this year’s EY Excellence in Integrated Reporting survey are the top 100 companies on the JSE, selected on the basis of their market capitalization at 31 December 2012, being the last trading day in December of that year.

It is interesting to note that the market capitalization of the 100 companies in this survey range from approximately R867 billion at the top end (British American Tobacco plc) to R7.4 billion (SA Corporate Real Estate Fund) at the lower end. Furthermore, these 100 companies account for approximately 90% of the total market capitalization of the JSE.

All companies were regarded as being eligible to be included in the survey, apart from pure holding companies, such as Pick n Pay Holdings. The final top 100 included the full range of listed companies on the JSE, from resources to industrials, retailers and financial institutions, and also included a number of companies with dual listings, such as SABMiller and Old Mutual. In the case of Investec Ltd and Investec plc, as well as Mondi Ltd and Mondi plc, which operate through a dual-listing structure, the combined group was included and, consequently, only the combined report was reviewed.

Following changes in market capitalization and other corporate activity, seven companies that appeared in last year’s survey were no longer regarded as being eligible, resulting in the appearance of seven newcomers. Two of the newcomers (Oceana Group and Tsogo Sun Holdings) were ranked as “Good” and newcomer Omnia Holdings was ranked “Excellent”.

EY’s Excellence in Integrated Reporting Awards 201313

EY’s Excellence in Integrated Reporting Awards 2013 14

The mark plan and adjudication process

Development of the mark plan

The mark plan for the Excellence in Integrated Reporting survey has been developed by the adjudicators from the College of Accounting at the University of Cape Town (UCT) in conjunction with EY’s Professional Practice Group. The UCT team comprises Professors Alex Watson and Mark Graham and Mr. Goolam Modack, all of whom were involved for many years in EY’s Excellence in Corporate Reporting survey and in the 2011 inaugural Excellence in Integrated Reporting survey.

All companies listed on the Johannesburg Stock Exchange have been required to produce an integrated report for financial years starting on or after 1 March 2010, in line with the requirements of King III.

Guidance on what should be included in the integrated report, for the purpose of this survey, has been sought by reviewing the Discussion Paper “Towards Integrated Reporting – Communicating Value in the 21st Century” issued by the International Integrated Reporting Council (IIRC) in September 2011. Cognisance has also been taken of responses to the September 2011 Discussion Paper that was issued by the IIRC in May 2012, the draft outline published in July 2012 and the Prototype Framework, published in November 2012. Much of the thinking within these various documents has now been encapsulated within the Consultation Draft of the International Integrated Reporting Framework issued by the IIRC in April 2013.

Although much guidance on integrated reporting is provided within these Discussion Papers, it is clear from the responses to the IIRC’s Discussion Paper that there are diverse views on a number of issues related to the definition of integrated reporting and the content of the integrated report. These uncertainties are, furthermore, specifically raised in a number of local integrated reports.

EY’s Excellence in Integrated Reporting Awards 201315

Where uncertainties in integrated reporting have been identified, the mark plan has been tailored so as to not be prescriptive as to what should be expected. So, for example, marks could be awarded for the quality of the discussion of how a company has addressed integrated reporting, rather than for whether they have the definition of integrated reporting correct. Another area where the mark plan has not been prescriptive is whether the main focus of the integrated report should be all stakeholders or merely investors. Nevertheless, we expect the company’s view to be explicitly stated.

We are also aware that companies with year-ends earlier in the year may not have had sight of some of the guidance published during the year. So, for example, while we would have looked for disclosures relating to the stock and flow of the six capitals (i.e., financial, manufactured, etc.), we would not have expected all companies to use this specific terminology.

The overriding objective in developing the mark plan has been to award marks for aspects of the integrated report that are in keeping with the spirit of integrated reporting as defined by King III as being “a holistic and integrated representation of the company’s performance in terms of both its finance and sustainability.”

Altogether, 35 separate specific aspects that should be present in an integrated report are included in the mark plan. Each of these aspects are rated on a 10-point scale that takes into account the quality of information presented, as well as the extent to which it is readily accessible. Emphasis has also been given to the IIRC’s recommendation that the information should be presented in a clear, concise, connected and comparable format. In addition to this, these 35 specific aspects are subjectively synthesised to give a mark, out of 10, for each of the IIRC’s five guiding principles (i.e., strategic focus, connectivity of information, future orientation,

responsiveness and stakeholder inclusiveness and the conciseness, reliability and materiality of the information).

As a consequence of our intention to change the mark plan on an annual basis and the subjectivity involved in its use, the mark plan is not made public. Furthermore, a mark plan that is publicly available could have the disadvantage of encouraging gamesmanship among the participants, rather than striving to encourage true excellence in integrated reporting.

Marking the integrated reportEach of the integrated reports of the top 100 companies has been separately marked by each of the three adjudicators from the College of Accounting at the UCT using the pre-agreed mark plan.

The document that has been reviewed and marked was the one that is labeled as the integrated report. For those dual- listed companies that do not produce an integrated report, the information contained in their annual report has been evaluated. This is not considered to be detrimental to these companies, as many of them nonetheless include many of the integrated reporting principles in their reports. In all cases, the online PDF or hard copy of the report has been reviewed.

The marking process is not simply about “ticking the box.” More emphasis is placed on the quality of information presented — the relevance, understandability, accessibility and connectedness of that information, whether users of the integrated reports would have a reasonable sense of the issues that are core to the operations of each of the companies, and whether companies have dealt with the issues that users would have expected. This implies that more credit is given for crisply presented information that highlights relevant facts, compared to the same information needing to be extracted from less relevant information.

EY’s Excellence in Integrated Reporting Awards 2013 16

EY’s Excellence in Integrated Reporting Awards 201317

The mark plan and adjudication process

Once the marking process is complete, the scores for the five guiding principles and individual members’ recommended rankings are collated, resulting in a final ranking being awarded based on a combination of the average of these scores, overall perceptions and discussions surrounding the final rankings for each company.

Where a member’s score differs widely from the others, this is reviewed to ensure that information had not been overlooked. Having said this, no attempt is made to arrive at a consensus score, as this would compromise the subjectivity of the scoring process.

In addition to marking the integrated reports in accordance with the mark plan, each adjudicator is required to record their recommendation of the category in which the integrated report should be ranked in the adjudication process. This is particularly important, as:

• The scoring process is subjective, and scores may differ based on the adjudicators’ impressions at the time of marking. Often, scores may vary widely, but despite this, there was a high degree of consensus among the adjudicating members’ overall perceptions and recommended rankings.

• Different types and levels of information are required for companies in different industries.

The adjudication process results in each of the 100 companies being ranked as “Excellent,” “Good,” “Average” or “Progress to be made.” A further evaluation then results in a ranking of the 10 best integrated reports from among those that are ranked as “Excellent.”

Finally, the adjudicators would be the first to acknowledge that others would produce a different mark plan that would doubtlessly yield different results. We do, however, believe that this process clearly differentiates between those companies that exhibit a high level of integrated reporting and those that do not. We therefore hope that this process has resulted in a ranking that gives credit to those that are doing well and encourages those that are not, to improve.

EY’s Excellence in Integrated Reporting Awards 2013 18

1 Gold Fields Ltd

Overall, Gold Fields scored excellently in almost every aspect of the marking process, and the reader is left with a clear sense of how the various aspects of the business relate to each other. The report is extremely well structured and easily navigable. The report is crisp and concise, and readers are directed to more detailed financial and non-financial information that is contained in the Annual Financial Report and the Mineral Resources and Mineral Reserves Report, as well as additional information that is available online. The report commences with a brief high-level overview entitled “Our business,” that outlines how the company adds value, its global footprint, details of its restructuring, its vision, values and stakeholder promises, its strategy and, finally, a financial overview. This overview is followed by more detail on its three strategic pillars that includes an excellent integration of the impact of the external environment on the performance of the business. Risk disclosure was a significant contributor to the high ranking of Gold Fields, and it has one of the best risk reports that we saw. Particularly impressive was the table that concisely summarized the group’s risk appetite and tolerance. The “Strategic performance dashboard” in the stakeholder engagement section cleverly integrates strategy, shareholder risks, KPI’s, performance and forward-looking information by strategic requirement. Furthermore, it explains how these strategic requirements impact on the CEO’s remuneration.

Feedback on the top 10 companies by Professor Mark Graham

EY’s Excellence in Integrated Reporting Awards 201319

2 Truworths International Ltd

Truworths’ report is crisp and concise, and it has wisely chosen to present abridged financial information within its integrated report. Additional information, including the annual financial statements and the Corporate Social Investment Report, are available online. The story of the business is told in an engaging manner, with a clear focus on both the risks of fashion and the risk of credit. The 16 pages that deal with the material sustainability topics of the business sensibly integrates performance against previous objectives, challenges faced in the current year and key risks, as well as objectives, plans and targets for the year ahead. Tables and other graphics are used to good effect, and the report is characterized by a lack of clutter, which improves the crispness of the report.

3 Standard Bank Group Ltd

Standard Bank’s user-friendly report is exceptionally well laid out, with excellent cross-referencing tools that make navigation, both within the report and to online information, extremely easy for the reader. The business model is clearly explained in a section entitled “How we make money” that outlines and explains the group’s various business activities, and links these to their income statement impact and the various risks that arise from these activities. The financial review includes a crisp table that innovatively outlines the impact of the economic environment on key financial ratios. The group’s risks are well explained and easily understandable, and the integrated report has an appropriate focus on issues, such as customer experience, that are considered to be key to a financial institution. We found that the Chairman’s introduction to the corporate governance section to be an appropriate way to introduce this important section of the integrated report.

EY’s Excellence in Integrated Reporting Awards 2013 20

5 Sasol Ltd

Sasol’s integrated report includes a section that details a strategic “line of sight” that sets out the changes made during the last year to Sasol’s common objectives, shared values and strategic agenda for the near to medium term. The CFO’s report provides a clear and concise summary of the key financial risks and uncertainties of the business, and is one of the best financial reviews that we saw. The financial and non-financial performance highlights at the beginning of the report are extremely useful and well laid out. The explanation of their business model and integrated value chain, together with their risk reporting, is excellent and justifies the high ranking of this report. The explanation of how materiality is determined in partnership with the group’s key stakeholders, taking into account their strategic objectives and integrated business chain, is excellent.

4 Royal Bafokeng Platinum Ltd

Royal Bafokeng’s integrated report is close to what the ideal integrated report should look like. Their December year-end allowed them to incorporate some of the integrated reporting thinking and terminology that gained traction during 2012. They were one of only two companies to embrace and report on the concept of “capitals.” The snapshot of each of their capitals (i.e., financial capital, manufactured capital, etc.) that highlighted disappointments, performance and future focus areas, followed by more detailed information, is well handled. The group’s material issues are crisply summarized early in the report, and these issues flow through into the CEO’s report. This report includes excellent integration of the business model, strategy and performance within an operational context.

6 Vodacom Group Ltd

Vodacom’s report is innovative, engaging and fun to read. We liked their approach of preparing a “storybook,” which includes a frank, transparent and readable assessment of the true economic value of the Group and its ability to create and sustain value over the short, medium and long term. We also applaud their stated approach of “less is more” that has resulted in a concise, yet comprehensive, report of some 129 pages – the shortest of all the reports ranked in the top 10. Good use is made of icons to cross-reference information and navigate the report and to help users find additional information on the company’s website. We particularly liked the way that icons were effectively used to highlight the positive and negative aspects of the business, and that equal prominence is given to the “good” and “not so good.”

7 Illovo Sugar Ltd

Illovo’s strategy, together with its goals and objectives, are clearly set out early in the report. This is followed by detailed information by geographic location on performance against previous targets together with objectives for the coming year, as well as major risk areas. A comprehensive market review establishes the context for understanding the group’s performance and ability to create value. The report also provides readers with a clear understanding of the sustainability of the business model.

EY’s Excellence in Integrated Reporting Awards 201321

8 Nedbank Group Ltd

Nedbank’s report is attractive and easy to read. The use of graphics allows the user to quickly absorb key information about financial and non-financial aspects of the business. Cross-referencing within the report is outstanding, and icons are used to direct the reader to additional information that may be found online. We found the presentation of key information by the stakeholder group to be a sensible way in which to convey to readers the issues that affect the various groups. Furthermore, the identification of “hot topics” within this section gives the reader a sense of the direction and focus of the group. The way in which the value-added statement is presented is innovative and informative.

9 Exxaro Resources Ltd

Exxaro’s report is well structured and the businesses strategies, risks and KPIs are appropriately integrated. The commodity review, together with various forecasts, provides very useful forward-looking information. The targets that are presented are particularly clear, and this report is one of the few that refers to the various capitals that are used in the business to generate value. Risks are particularly well handled in this report. A summary of the group’s material issues highlights the major risks, why they are an issue for the organization, what their response has been to the risk and references to where more detailed information can be found. A heat map is included that graphically depicts the severity of each of the major risks.

10 Liberty Holdings Ltd

Liberty’s report is excellent at simplifying and explaining a complex business model. The report emphasizes how value is created for both shareholders and customers, and the graphic that depicts the sources of shareholder value for each significant business segment is particularly useful. Furthermore, the dashboard that summarizes the performance in terms of previous strategies of the group, together with the key approved strategic objectives for 2013, provides valuable information for the reader. We found the page that outlined the group’s key accounting policies particularly useful and a welcome change to the “boilerplate” accounting policies that most companies disclose.

EY’s Excellence in Integrated Reporting Awards 2013 22

Until two or three years ago, annual reports published by South African companies were increasing in length and complexity, but not necessarily in respect of their usefulness. Global concerns that annual reports were not serving their purpose of providing decision-useful information applied equally in South Africa, despite the fact that South African annual reports were longer than most. Reporting practices had to change if the needs of users were to be met, and South Africa has been an active participant in the developments toward improved corporate reporting.

EY’s Excellence in Integrated Reporting Awards 201323

Practical evolution of integrated reporting

Practical evolution of integrated reporting and the impact of the IIRC Consultation Draft on future reporting in South Africa by Professor Alex Watson

Historical reporting background

Historically, statutory financial statements providing largely backward-looking financial information formed the major component of the annual communication with shareholders. Over time, management commentary was added to provide context to the financial information. More recently, additional “non-financial information” relating to employment issues (e.g., safety records and expenditure on training), environmental information (e.g., carbon emissions, electricity and water usage) and corporate social responsibility activities were disclosed. This additional information was often in a separate sustainability report or annual review, and often with little consideration to the relevance of that information to the company and its stakeholders. While, disclosure of the “triple-bottom-line” and “environmental, social and governance” information was a step in the right direction, its usefulness was limited if it did not highlight the link to the strategy of the business or its ability to add value to the company in the longer term.

The recent financial crisis highlighted that annual reports had not adequately addressed financial risks, despite the increasing length and complexity of the financial statements and reporting requirements. In addition, various natural and labour-related incidents, together with increasing evidence of a natural environment that is threatened, has highlighted the broad spectrum of risks that can threaten the sustainability of a business. These risks are considered by those investing in and lending to the company, but annual reports were not doing an adequate job of providing the information that investors and lenders needed to make informed investing decisions. It was becoming increasingly obvious that changes were required to the way in which companies report.

There have been a number of global and country-specific research projects on how reporting should and could be improved. Steps taken to address perceived weaknesses in reporting practices have generally focused on reducing the complexity and increasing the relevance of the material included in the annual report. There is increasing evidence that integrated reporting will emerge as the future of reporting, where integrated reporting is a process that results in the product of an integrated report.

EY’s Excellence in Integrated Reporting Awards 2013 24

Practical evolution of integrated reporting

Integrated reporting developments

South African companies have been required to prepare an integrated report for financial years beginning on or after 1 March 2010, or explain why they have not done so. Most companies will, therefore, be considering the publication of their third integrated report, and continue to do so in the absence of definitive guidance.

Preparers of reports have been challenged by limited and evolving draft guidance, with tight reporting deadlines and limited examples of best practice to refer to.

The South African Integrated Reporting Committee published a Discussion Paper on Integrated Reporting in January 2011. The International Integrated Reporting Council (IIRC) published a Discussion Paper in September 2011, “Towards Integrated Reporting – Communicating Value in the 21st Century” which incorporated many aspects from the South African Discussion Paper.

Both the local and international discussion papers are principle-based and do not provide detailed guidance of what should be included in the annual report.

In April 2013, the IIRC published a Consultation Draft of the International Integrated Reporting Framework (Draft Framework). The Draft Framework was published after a lengthy process, which included consideration of responses to its 2011 Discussion Paper, and publication of a draft outline in July 2012 and a Prototype Framework in November 2012.

The IIRC asked for feedback on the Draft Framework by mid July 2013, which would then be considered prior to the proposed publication of the initial version of the Framework in December 2013.

Integrated thinking, integrated reporting and the

integrated report

One of the many challenges with respect to integrated reporting is that there appears to be an element of confusion and misunderstanding about what some of the key terms mean. As a meaningful discussion of the reporting requirements requires an understanding of those terms, they will be considered before considering the impacts of the Draft Framework on the future of reporting in South Africa.

Integrated thinking is defined in the Draft Framework as “the active consideration by an organization of the relationships between its various operating and functional units and the capitals that the organization uses and affects. Integrated thinking leads to integrated decision-making and actions that consider the creation of value over the short, medium and long term.” As the Draft Framework explains more fully, the capitals include all resources and relationships that form part of the organization’s business model i.e. include financial, manufactured, intellectual, human, social and relationship as well as natural capitals. One of the landmark elements of the King III is the application of the “stakeholder-inclusive” approach, in which the board of directors should consider the legitimate interests and expectations of all stakeholders. Application of the stakeholder-inclusive approach envisaged by King III will give rise to integrated thinking.

Integrated reporting is the process that results in communication about value creation, whereas an integrated report is the product. An integrated report is the report that is intended to communicate concisely about how an organization’s strategy, governance, performance and prospects will lead to the creation of value over the short, medium and long term.

EY’s Excellence in Integrated Reporting Awards 201325

The report should explain the business model in the context of its external environment and communicate all the factors that influence the creation of value over time. As the creation of value depends on the extent to which resources or capitals are consumed and produced, an integrated report should highlight the inputs as well as the outputs arising from the business model.

While an integrated report should deal with environmental and social issues, it is far more than a report that focuses on the traditional “triple bottom line.” An integrated report highlights the connectivity between items and explains the interaction between the external environment of the business and the resources or capitals that it consumes and produces. An organization that applies integrated thinking will have no difficulty in producing an integrated report, as that report will simply report on the way in which decisions are made and performance is assessed. For those organizations that do apply integrated thinking, an integrated report should be a short summary of what the board discusses, i.e., the company’s strategy, the related risks and opportunities and its performance against that strategy.

Where companies are not applying integrated thinking, the production of an integrated report is challenging and is likely to be superficial and less relevant. In that case, the preparation of an integrated report is going to require extracting information from different departments, with probably the marketing department facing the challenge of trying to pull together a credible and cohesive report.

Draft Framework implications

The Draft Framework is a principle-based document that sets out the conditions that need to be fulfilled in order to maintain that the integrated report is prepared in terms of the (currently draft) Integrated Reporting Framework.

There are some required disclosures, some suggested content elements and some guiding principles. The required disclosures include some items that not all South African companies are currently providing, and specifically include the requirement to disclose:

• The organization’s materiality determination process

• The reporting boundary and how it has been determined

• The governance body with oversight responsibilities for integrated reporting

• The nature and magnitude of the material trade-offs that influence value creation over time

• If appropriate, the reason why the organization considers any of the capitals identified as being immaterial

The reference to the “capitals” in the list of prescribed disclosures above represents a significant development behind integrated thinking and integrated reporting. The earlier guidance on integrated reporting referred to “resources and relationships,” which is another term for capitals. The Draft Framework explains the six types of capitals that may be the inputs into a business model or the outputs from that model.

While a company is required to report on the effects that it has on the six capitals, it is not required to do that explicitly, i.e., it is not necessary to have a separate section dealing with manufactured capital, another with human capital, etc., although that may be an effective way of structuring the report. As indicated above, where a company feels it does not have one of the six capitals (financial, manufactured, intellectual, human, social and relationship, as well as natural), it is required to provide an explanation.

EY’s Excellence in Integrated Reporting Awards 2013 26

Practical evolution of integrated reporting

The Draft Framework contains guiding principles that underpin the preparation of the integrated report.(For those that are familiar with the Conceptual Framework for financial reporting, these guiding principles are the equivalent of the qualitative characteristics of that Framework.) These principles are mostly unchanged from the 2011 Discussion Paper published by the IIRC, with the inclusion of “completeness” and ‘comparability’ being the two new terms that have been added to the previous list. (The previous list was strategic focus, future orientation, connectivity, responsiveness and stakeholder inclusiveness, as well as conciseness, reliability and materiality.) The inclusion of “completeness” is appropriate as it emphasizes the importance of balanced reporting – the implication being that bad news should be reported with equal prominence as good news. “Comparability” does not imply that every organization should give the same information, as each organization should disclose only that which is material to its value creation story. “Comparability” implies making the information relevant by disclosing it in comparison to an appropriate benchmark, using a ratio that demonstrates a key relationship or where there are standardized ways of measuring information that is relevant to the organization, to present it in the standard format. (This will include preparing financial information using a generally accepted reporting framework, such as International Financial Reporting Standards (IFRS).)

The Draft Framework suggests some content elements for the integrated report, but makes it clear that the suggested content elements are not prescriptive, as they are dependent on the specific circumstances of the organization and there are likely to be many interconnections between the different elements. This point is emphasized by drafting the document in the form of questions, rather than statements. For example, the question is posed, “what does the organization do and what are the circumstances under which it operates?” as opposed to including a requirement to provide specific information.

These questions are intended to be a check to ensure that all the content elements that are appropriate are dealt with, without prescribing how that should be done.

The Draft Framework states unequivocally that “an integrated report should be prepared primarily for providers of financial capital.” While most South African companies appear to have prepared their integrated reports for providers of financial capital, there are a few who have indicated that their integrated reports have been prepared for a wider group of stakeholders, possibly because of the stakeholder-inclusive approach of King III. Integrated thinking implies considering the needs of all stakeholders in determining the strategy and measuring the performance of an organization, but it does not imply that the same reporting framework needs to be used for each stakeholder. An integrated report presents the results of integrated thinking in a way that is relevant for providers of financial capital. An alternate report could present the results of integrated thinking in a way that is more relevant to a different group of stakeholders, such as employees or customers.

The Draft Framework has addressed another area that has been contentious in South Africa, and that is whether the suite of reports that is prepared is the integrated report or only the high-level document. The consultation document makes it clear that the integrated report is “a concise communication,” thus making it clear that it is a single document that is relatively short. This integrated report will be supported by additional information, which will usually include statutory financial statements prepared in terms of the appropriate reporting framework (generally IFRS), additional sustainability information, which could be prepared in terms of the Global Reporting Initiative (GRI) requirements, and any other relevant or required information that has not been included in the integrated report.

EY’s Excellence in Integrated Reporting Awards 201327

ConclusionThe pace of the change is likely to be a challenge for both preparers and users of the reports, particularly as companies have been required to change their reporting focus without clear guidance about how that should be done. However, as the process evolves and companies better understand the new reporting frameworks, users are clearer about their information requirements, systems are changed and aligned to capture and report the information needed, and the usefulness of the reporting by the company, as well as to the company and its users, should increase.

EY’s Excellence in Integrated Reporting Awards 2013 28

EY | Assurance | Tax | Transactions | Advisory

About EY EY is a global leader in assurance, tax, transaction and advisory services. The insights and quality services we deliver help build trust and confidence in the capital markets and in economies the world over. We develop outstanding leaders who team to deliver on our promises to all of our stakeholders. In so doing, we play a critical role in building a better working world for our people, for our clients and for our communities. EY refers to the global organization and may refer to one or more of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit ey.com. © 2013 EYGM Limited. All Rights Reserved

Studio ref. 130625. Artwork by Sewpersadh.

EYG no. AU1733ED no. 0114, 0314, 0714 This material has been prepared for general informational purposes only and is not intended to be relied upon as accounting, tax, or other professional advice. Please refer to your advisors for specific advice.

ey.com

Contacts

Larissa Clark

Director for Assurance Professional Practice Group

Tel: + 27 (0)11 772 3094

Email: [email protected]

Jeremy Grist

Director for Climate Change and Sustainability Services

Tel: + 27 (0) 11 772 3029

Email: [email protected]

Kelly Gilman

Senior Manager for Climate Change and Sustainability Services

Tel: + 27 (0) 21 443 0473

Email: [email protected]